Abstract

BACKGROUND:

In order to gain a competitive advantage or survive, organizations need to reorient themselves once in a while, and in distress tend to rely on turnaround strategies. The organization must ensure that the turnaround strategy implemented is effective.

OBJECTIVE:

This study explores and investigates the implementation of turnaround strategies during a crisis by manufacturing firms with the help of a conceptual model combining turnaround strategies and McKinsey’s 7s framework as the mediating variables.

METHODS:

A questionnaire comprising 35 questions was circulated amongst the employees of various manufacturing firms operating in India and 230 data samples were collected.

RESULTS:

The findings of this study indicate that manufacturing firms tend to implement turnaround strategies in the form of Operational, Financial, Leadership, Structural and Strategic methods for their survival and reorientation. Additionally, turnaround strategies and strategic reorientation variables of the McKinsey 7s framework showed a significant relationship through a set of Hard S and Soft S.

Keywords

Introduction

Many firms today face organizational declines at some point in their life cycles because of both external and internal factors and need some set of robust strategies to sustain those periods of adversities. There are external and internal factors [1]. Organizations often descend into decline as a result of not anticipating, recognizing and adapting to external and internal pressures that threaten their very existence. A lack of competitive pressures eventually resulted in diseconomies of scale and inefficiencies within the enterprise, leading to a turnaround that led companies to divest everything [2].

As one of the important factors leading firms to decline, distress represents a significant threat to firms’ high priority values and demand a time-pressured response [3]. Globally, the continuing threat of organizational decline - coupled with the turnaround processes it often entails - has remained a serious concern for managers facing distress or crisis. Companies in high growth stages can also experience declines for a variety of reasons. Working on performance improvement in a normal business operation scenario is very different from working on it during a time of distress or crisis, which has become a cause of concern for many managers [1]. The concerns and challenges managers face when improving performance in a time of distress or crisis are distinct from those faced when executing organizational turnarounds [4].

A turnaround occurs, “when a firm is experiencing performance declines which are threatening its survival over the long run, but is able to reverse the decline and stabilize profit margins” [5]. The turnaround process can be divided into two distinct but interconnected steps, namely decline stemming strategies and recovery [6, 7]. The influence of causality on the subsequent turnaround response is a key topic of debate in the literature. Retrenchment (e.g., cutting costs) is a critical first stage in a successful turnaround strategy and can even be considered the dominant strategy [6]. In view of this, O’Neill [8] had earlier asserted that recovery could be achieved through efficiency and retrenchment and was not strictly dependent on growth strategies. Furthermore, a study asserted that operating/efficiency strategies were more effective than entrepreneurial initiatives due to their ability to produce dramatic results and to serve as indicators of intent for management and stakeholders [9].

Another study [10] states that turnaround strategies are the strategies implemented by the firms for the recovery in the performance. Further, they state that every business firm suffers a decline in its fortune from time to time. Of interest, there are management decisions and environmental changes that are associated with substantial decline and subsequent recovery in the performance of business firms— in what can be called a turnaround in the performance.

The study will find out what turnaround strategies are implemented by firms to successfully survive and compete in the time of distress or crisis. On further investigation, the relationships between these turnaround strategies will be found out. Ability to respond to crisis is conferred via strategy, structure, culture, leadership, and people [11]. These turnaround strategies act as independent variables and the Hard S and Soft S of McKinsey 7s model will be mediating variables. The study of relationships between these variables will find what among the Hard and Soft S of McKinsey 7s model acts as a catalyst to the different turnaround strategies. The manufacturing firms implement the different turnaround strategies and they should be able to focus on critical factors to successfully implement the turnaround strategies across multiple denominators. Continued acceleration of the rate of change is the common denominator across all phenomena be it social, physiological or psychological [12]. Thus, the study has been established to find out the relationship between different critical factors which the manufacturing firms should focus on while going for reorientation in the time of distress. This article describes a framework for designing such overall turnaround strategies for manufacturing firms, including (1) the types of turnaround strategies possible, (2) the nature of turnaround situations, and (3) a framework for deciding which type of turnaround should focus on which part of McKinsey 7s model.

Theoretical lens

The emerging context spurred by the economic crisis, turnaround and survival as a research area has gained momentum [13–17]. The dynamic capabilities view represents an appropriate framework for the development of a theory of organizational change in turbulent environments [18–20]. Scholars argue that dynamic capabilities are applicable not only to more stable environments [21], but also to rapidly and moderately changing environments [19]. In order to be resilient as an organization, a company needs to be able to effectively absorb disruptive surprises that threaten its survival, develop situation-specific responses, and ultimately engage in transformative activities [22]. There are several advantages to taking a capabilities-based approach to turnaround [23]. In the capabilities perspective, resilience is included as part of the hierarchy of activities through an accepted, well-established lens. Under this hierarchy, activity sets are applied to existing resources as zero order activities, robust and reliable routines of action yield competitive advantages as first order activities, known as operating capabilities, and further actions reconfigure these routines in response to environmental changes as second order activities, or otherwise referred to as dynamic capabilities [24–26].

Within the context of resilience, routines, operating capabilities, and dynamic capabilities are divided into segments that are used to segment actions for building robust adaptations at various levels of organization. In addition, such an approach incorporates the notion of repeatability and reliability into this interpretation of resilience, going beyond simple phases of evolution and revolution by looking at various sequences of crisis and subsequent growth based on firm size and maturity [27]. This means that a resilience capability is not simply an option that may be nice to have under some circumstances, but rather an essential quality to be developed for a firm to realize competitive advantage through good, strategically coherent and resource sufficient times, along with the challenges accompanying adverse conditions of strategic and resource collapse [28]. Third, capabilities and in particular dynamic capabilities, embody change where the firm must make rational decisions based on the opportunities and resources it can attract and develop [29]. Since resilience is primarily concerned with the process of adapting to challenging complex conditions, viewing resilience through the capability lens represents a dynamic alignment [22] that seeks to avoid the converging focus of a path dependency approach [30] and to rebuild efficient yet flexible performance [31]. The literature has established the distinction between two types of actions to achieve a successful turnaround. These are “operating” and “strategic” actions [10, 32]. Operating actions address efficiency achievements and seek short-term cost reductions [1, 15]. They include financial, structural and operational Turnaround. Strategic actions address adjustments in a firm’s domain or the way in which the firm competes within those domains [15] and are oriented toward sustained long-term profitability [5] including strategic and leadership turnaround.

By integrating findings from relevant research streams and theoretical lenses, this work describes the status quo of turnaround research. The article presents a holistic framework emphasizing operational, strategic, structural, leadership, and financial turnarounds. We account for the different facets of content, process, and context research to bridge the gap between mostly detached sub streams. Further, the study focuses on the McKinsey 7s model to measure the corporate turnaround success and aims to provide a basis for the role played by the McKinsey 7s framework in successful implementation of turnaround strategies. Competencies drive competitive advantage [33], they reside in the elements of McKinsey 7S.

Insights from existing literature

In the 1980s, the addition of mergers and acquisitions and the resultant bankruptcies boosted the number of bankruptcy filings, enhancing the topic’s relevance [34]. The turning point wave of the 1980s as seen in early empirical studies were crucial [6]. On the basis of this initial trend in publications, scholars have steadily advanced our understanding of the topic, yielding many findings and definitions. In general, turnaround can be defined as the process of recovering from distress [10]. According to corporate turnaround literature, organizational responses to crises are grouped into two categories: either operational or strategic [1, 36]. Despite the incorporation of new features such as different stages in the process or contextual interdependencies, corporate turnaround research appears to stick to this dichotomous classification of organizational change. Due to the necessity for organization-wide change faced by firms in survival mode, recovery strategies are diverse and fundamentally differ in their function or theoretical basis [37]. Reviewing corporate turnaround and distress works in a two-dimensional manner could lead to erroneous conclusions. It was found in a 2020 study that turnaround strategies were categorized into strategic and operational categories according to their cash flow impact, with strategic interventions aimed at increasing long-term cash flows while reducing short-term cash flows [38].

Strategic change & McKinsey 7S

McKinsey 7’s model was developed by Peters, Waterman and Philips [39]. Seven critical factors are incorporated into the model to evaluate the effectiveness of an organization design in order to steer the firm towards its goals. The seven critical factors include staff, shared values, structure, styles, systems, skills and strategy. According to Otsupius and Otsu [40], an organization’s effectiveness is determined by seven critical factors. Further, any organization’s effectiveness depends on its understanding of the seven critical factors. An organization’s policies, structure, culture, and vision must be aligned with its turnaround strategy in order for it to succeed. In accordance with Bowman and Faulkner [41], a systematic approach to decision-making is essential for any successful organization. According to Hill [42], the McKinsey model’s critical factors must align with the organization in order to effectively have an impact. Furthermore, by using the Mckinsey model, organizations can identify issues within their organization and solve those issues so that they achieve their goals.

We employ a more detailed conceptual organizational change framework to close this gap and overcome the shortcomings of a merely dichotomous classification of turnaround. We follow the concept of organizational inertia when hiring new management after a company has been in distress for several years. This results in a diminished ability to react and lower turnaround probabilities. Despite the inclusion of various contexts, such as exogenous or internal causes for decline [43], or considering different stages in the process [5], the interdependencies between process, context, and the selected turnaround strategy have been overlooked. However, when comparing different turnaround decisions, it is important to consider the underlying context and timing to avoid misinterpretation [44].

A firm can implement various turnaround strategies in times of distress or crisis for survival. These turnaround strategies are:

Operational turnaround strategy

Financially distressed companies often undertake operational restructuring as their first turnaround strategy, since it makes little sense to assess the strategic health if they will go bankrupt soon [35]. The evidence of the effects of operational actions on turnaround performance has been fragmented, inconsistent, and without much cumulative theory building. A study found that declining industrial firms that proactively downsized, and did so across the board, performed better during turnaround [45]. A similar outcome of asset retrenchment was found for declining firms [46]. A firm’s ability to retrench would vary depending on its industry condition [5]. In declining industries, however, asset retrenchment adversely affects performance, while cost retrenchment positively affects performance [47].

This leads us to the research question and subsequent hypothesis focusing on “How does operational turnaround strategy affect strategic change and assists a firm’s survival”.

Strategic turnaround strategy

The evidence has confirmed the importance of strategic actions in turnarounds. In fact, it is believed that strategic actions are what drive long-term performance gains after a decline. Combining a firm’s existing stock of resources to produce a new product, process, or technology, or acquiring resources through mergers or acquisitions, are both positive factors for organizational recovery [47]. In order to gain access to new resources, both of these actions were more important than allying. A firm’s internal capabilities are seen as major sources of economic value creation and sustainable competitive advantage [48]. When decline is caused by a jolt of environmental magnitude, acquisitions made during the jolt produce greater returns than acquisitions made either before or after [49]. Moreover, related acquisitions perform better than unrelated acquisitions for distressed firms in declining industries [50]. When examining a broader spectrum of strategic actions, similar results were found.

This leads us to the research question and subsequent hypothesis focusing on “How does strategic turnaround affect strategic change and assists a firm’s survival”.

Structural turnaround strategy

Structures in strategy are closely related [51]. Survival strategies will call for alterations in organizational structure [52]. Structure establishes relationships between the triad of authority, accountability, responsibility [53]. It is essential to modify the structure during a crisis in order to tie it over. Context is a crucial factor in predicting a given ‘structure”s effectiveness [54]. In particular, an organization that aligns its characteristics with its contingencies performs better than one that does not align [53]. A number of scholars have found a positive relationship between organisational structure and performance [55–57].

According to Bowman [58], restructuring can encompass a wide range of transactions, such as selling business lines or making significant acquisitions, changing the capital structure through a substantial infusion of debt, and changing the organizational structure of the company. A business portfolio restructuring may involve selling lines of business that are not central to the organization’s long-term objectives [59]. Restructuring can also involve a sequence of acquisitions and divestitures to develop a new configuration of the lines of business of the corporation. Capital structure changes usually involve the infusion of large amounts of debt to either finance leveraged buyouts or to buy back stock from equity investors or to pay large one-time dividends. Organizational restructuring is intended to increase the efficiency and effectiveness of management teams through significant changes in organizational structure, often accompanied by downsizing. Restructuring involving mainly organizational structure change is often accompanied by asset disposal or acquisition. Corporate rhetoric about the motives behind the somewhat drastic action of restructuring typically cites productivity enhancements, cost controls and other actions designed to maximize shareholder wealth. The financial press provides high visibility to such assertions, in prominent feature articles in popular business publications. The sources of gains in the post-restructuring phase may be due to the sale of assets, operational efficiencies, or at times to a new concept of the business.

This leads us to the research question and subsequent hypothesis focusing on “How does structural turnaround strategy affect strategic change and assists a firm’s survival”.

Financial turnaround strategy

There is no evidence of financial restructuring as an essential component of corporate turnaround strategies in the existing strategy-based research. A study [60] however, that their sample of sharp benders followed debt reduction less frequently than their control firms. In our study, we include financial restructuring as a key element of corporate restructuring and evaluate its importance. Financial restructuring refers to the reworking of a firm’s capital structure in order to relieve the burden of interest and debt repayments, and there are two types of restructuring: equity-based and debt-based. Financial and non-financial factors play a key role in the organization’s success [61]. Dividend cuts or omissions and equity issues, such as rights issues, public offerings, and institutional placements, fall under equity-based strategies. As a result of liquidity constraints, covenants imposed by creditors, or strategic considerations such as improving the firm’s bargaining position with unions, in financial distress firms often reduce or omit dividends. Observations suggest that large firms respond to financial distress by rapidly and aggressively reducing dividends [62].

This leads us to the research question and subsequent hypothesis focusing on “How does financial turnaround strategy affect strategic change and assists a firm’s survival”.

Leadership turnaround strategy

Leadership change is based on agency theory, which explains how top managers represent the interests of stockholders and creditors as agents [25]. A CEO dismissal in times of distress circumvents a ‘threat-rigidity response’ [63]. Strategy innovation is a critical success factor during turnarounds, one that is greatly influenced by the CEO’s intrinsic belief in this opportunity, thus necessitating a change in leadership [64]. The ability to make critical decisions implies an overidentification risk related to the organization and its current strategy; this renders organizational failure a personal defeat, increasing commitment to a failing strategy. Leadership impacts enterprises’ technological innovation capability and thus guides success [65]. A manager replacement is common, but not necessary in order to turn around a company [66]. While Trahms [1] discussed factors related to managerial cognition, strategic leadership, and stakeholder management, our review also discusses the effects of debt restructuring and other turnaround strategies. The research agenda of the researcher focuses on resource orchestration, strategic leadership, and stakeholder management. By integrating results from relevant research streams and theoretical lenses, this work provides a comprehensive overview of the status quo in turnaround research.

This leads us to the research question and subsequent hypothesis focusing on “How does leadership turnaround strategy affect strategic change and assists a firm’s survival”.

As a component of the organizational change theory, the study contributes to the research on corporate turnarounds. A limited number of resources can make it difficult for organizations to overcome barriers and obstacles. Therefore, it is crucial to recognize the role of systemic changes, expert advice, and a resilient contingent tool to deal with further escalation of any distress [28]. As part of the strategic transformation process, companies ensure a balance between cost configurations, asset management, focusing on core activities and implementing processes designed to implement procedural and systemic changes in a way that aligns with corporate transformations [37].

A strategic shift or transformation through a turnaround requires the identification of preconditions and the understanding of the strategy to be implemented, as well as identifying the levers that will be used to execute those strategies, which may range from cash-based dynamics to operational diligence to cultural mechanics [30].

As managers, we are supposed to consider the principal agent phenomenon, which should be applied also here in the context of corporate turnarounds where we have the opportunity to synthesize two opposing perspectives, i.e., deterministic view and voluntaristic view. In addition, a dialectical strategic view has also emerged that balances the gap between the two traditional viewpoints. Essentially, all this revolves around the role and influence of managers in the strategic shift process [67]. Strategic management literature highlights corporate turnaround as a process that is a strategic move at the corporate level, one that has ripple effects across the organization to maintain corporate performance and operational efficiency with a multitude of determinants [68].

Turnaround is generally the way an organization responds to a crisis and ensures survival dynamics, and is the result of well formulated policies and decisions from the top of the organization. However, capturing the patterns of strategy combinations that help turn a firm around, or identifying which combinations of turnaround strategies an organization uses to reorient itself, is essential. To come up with a standardised strategy solution to better understand how it guides the organization, is it unique in these decision patterns, or is it a generic move? There have been many independent studies, but here we see the interaction among turnaround strategies. We might be able to identify and address some critically important research questions regarding the following:

How can companies implement turnaround strategies? In the McKinsey 7S framework, how do these turnaround strategies affect the Hard S and Soft S? In times of distress, how can turnaround strategies ensure survival?

Following the understanding developed, we will try to unravel the role played by turnarounds in the survival of an organization through a set of corporate decisions that revolve around operational, strategic, financial, structural and leadership turnarounds. We attempt to decipher how each of these plays a significant role in reorienting the firms through a strategic fit of a turnaround strategy. In order to understand managerial cognition, awareness of decline, and perception of the severity of the decline, it is crucial to understand managerial cognition.

The study’s objectives are as follows:

Investigate the turnaround strategies used by firms to reorient themselves in times of distress. Determine what turnaround strategies will be most effective based on the nature of the distress. Discover what the turnaround strategies aforementioned mean. The purpose of this study is to examine the correlation between turnaround strategies and the Hard S and Soft S of McKinsey 7s.

Mapping the constructs

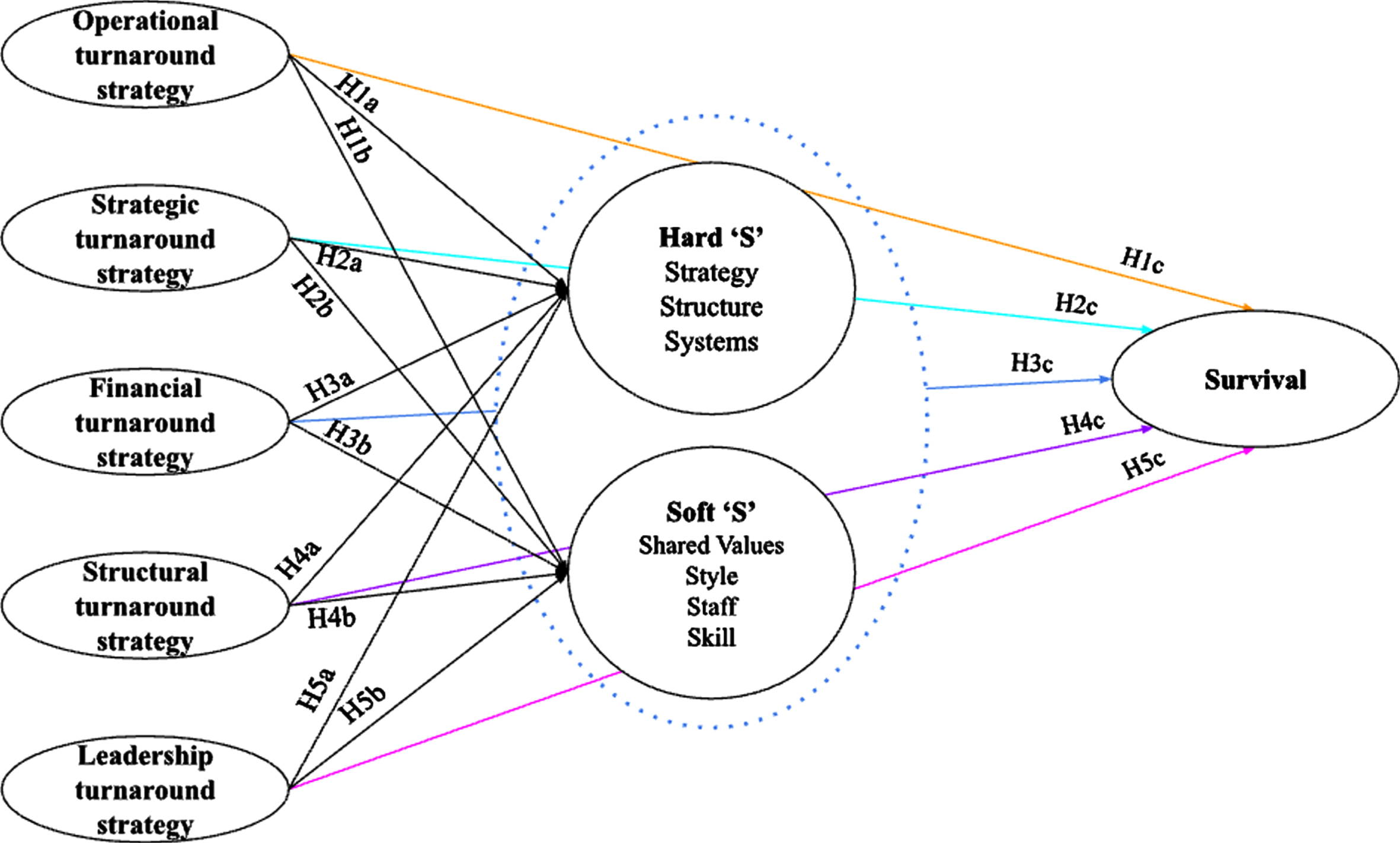

H1: Operational turnaround strategy - survival of firm link

There is fragmented and inconsistent evidence on how operational actions affect turnaround performance, with only a few cumulative theories developed. Declining industrial firms that proactively downsized across the board did better in turnarounds [45]. For declining firms, asset retrenchment resulted in improved performance [46].

The evidence, however, suggests that downsizing negatively affects firm performance [69]. Individual actions also interact significantly with one another to explain variance in operating performance, but this evidence is barely visible [70, 71]. Mixed results may be explained by this, despite broad conceptual support [72]. Based on Barker and Mone’s [73] argument, retrenchment actions would depend on the condition of the declining firm’s industry. Morrow, Johnson, and Busenitz [47] provided evidence that asset retrenchment leads to performance gains in growth industries; yet, in declining industries, asset retrenchment negatively affects performance, but cost retrenchment positively affects performance. Similarly, Ndofor et al. [15] found evidence that both cost and asset retrenchment negatively impact turnaround for firms facing decline in growth industries. Importantly, Barker and Mone [73], however, did not find any evidence that firms engaging in retrenchment actions in a declining industry had better performance than those who did not. Indeed, firms that engage in retrenchment actions experience reductions in industry- and firm-specific human capital as well as industry-specific social capital that increase the probability of firm failure [74].

H1a: There is a significant positive relationship between Operational turnaround strategy and Hard S (strategy, structure & systems) elements of McKinsey 7s framework

H1b: There is a significant positive relationship between Operational turnaround strategy and Soft S (shared values, style, staff & skills) elements of McKinsey 7s framework

H1c: Operational turnaround strategy is practised by firms to survive in the time of distress.

H2: Strategic turnaround strategy - survival of firm link

Research has demonstrated that strategic actions are crucial to turnaround. In fact, strategic actions are believed to be the key to sustained performance gains after declines. The study by Morrow et al. [75] shows that recombining existing resources or acquiring resources through mergers or acquisitions can lead to organizational recovery. Additionally, researchers have studied how environmental conditions affect turnaround strategies. In growing industries, firms tend to fail more often than in declining industries, indicating the importance of adapting strategic actions to the environment. Acquisitions made during a decline driven by environmental jolts produce greater returns than acquisitions made before or after the jolt [49]. A related acquisition performs better than an unrelated acquisition for distressed firms in declining industries [50]. A broader range of strategic actions produced the same results. According to Ndofor et al. [15] new products are critical to turning around declining growth industries through acquisitions and strategic alliances. The research conducted by [5] also showed that firms in growing markets tended to engage in more strategic actions than firms in declining markets.

H2a: There is a significant positive relationship between Strategic turnaround strategy and Hard S (strategy, structure & systems) elements of McKinsey 7s framework

H2b: There is a significant positive relationship between Strategic turnaround strategy and Soft S (shared values, style, staff & skills) elements of McKinsey 7s framework

H2c: Strategic turnaround strategy is practised by firms to survive in the time of distress.

H3: Financial turnaround strategy - survival of firm link

There has been no identification of financial restructuring as an integral component of corporate turnaround strategies in existing strategy-based research, compared to finance-based research [76–78]. According to Ginyer, Mayes, and McKiernan [60], sharpeners behave differently than control firms when it comes to debt reduction. As part of our corporate restructuring framework, we consider financial restructuring as a key element. DeAngelo and DeAngelo [62] found that firms in financial distress usually reduce or omit dividends due to liquidity constraints, debt covenant restrictions, or strategic considerations such as improving their bargaining position with trade unions. Large firms respond to financial distress by reducing dividends rapidly and aggressively, according to DeAngelo and DeAngelo [62] and John, Lang, and Netter [78]. Firms that use debt-based strategies restructure their debt extensively. In order to avoid financial distress or to resolve an existing financial distress, companies restructure their debt. According to Gilson [77, 79] debt restructuring occurs when an existing debt is replaced by a new contract that has one or more of the following characteristics: (1) interest or principal reduction; (2) maturity extension; (3) debt-equity swap. Raising additional funds through equity and loans was more common in the UK than debt restructuring until recently [80]. In this study, we examine whether debt restructuring can help turn around a business.

H3a: There is a significant positive relationship between Financial turnaround strategy and Hard S (strategy, structure & systems) elements of McKinsey 7s framework

H3b: There is a significant positive relationship between Financial turnaround strategy and Soft S (shared values, style, staff & skills) elements of McKinsey 7s framework

H3c: Financial turnaround strategy is practised by firms to survive in the time of distress.

H4: Structural turnaround strategy - survival of firm link

A number of recent studies have investigated factors that facilitate or impede reorientation of firms [81, 82]. During times of distress, firms may become more rigid and less likely to make innovative changes, thereby reducing their ability to reorient themselves strategically. In a variety of contexts, organizational sociologists have examined restructuring from both the viewpoint of the dependent and independent variables. These include institutional change [83], corporate structures and control [85, 85], interfirm networks [86], and concepts of work and career [87–89]. Different political and economic conditions have slowed and sped up the process of organizational change, but it has not stopped [90]. In some cases, sociologists’ negative perceptions of organizational restructuring may signal a disciplinary disconnect with those who frame it as a positive and beneficial process for society and the economy [91] debates over economic sociology’s assumptions and domain. A large-scale shift in bureaucratic form and process has demonstrated the ability of social organizations to adapt and benefit from changes of this kind in the past. As a result of additional systemic changes at local, national, and global levels, future restructurings could be viewed as positive [92]. Organizational changes are characterized by high levels of uncertainty and chaos [93]. A tendency towards rigid behavior patterns and a strong resistance to change can often be found among people [94]. The threat-rigidity theory [95] explains why changes in the workplace may occur. In studies of organizational crisis and resistance to change, threat-rigidity theory has received substantial empirical support [96–99]. Employees will be less receptive to changes if they are extensive and perceived as negative, such as redesigned workflows and reorganizations that result in additional duties and work overload [100]. Even if the changes are perceived to be beneficial, it is envisaged that a transitional period of time for adaptation is necessary.

H4a: There is a significant positive relationship between Structural turnaround strategy and Hard S (strategy, structure & systems) elements of McKinsey 7s framework

H4b: There is a significant positive relationship between Structural turnaround strategy and Soft S (shared values, style, staff & skills) elements of McKinsey 7s framework

H4c: Structural turnaround strategy is practised by firms to survive in the time of distress.

H5: Leadership turnaround strategy - survival of firm link

According to behavioural theory, CEO dismissals during distress circumvent a threat-rigidity response [63, 43]. Innovation in strategy is critical to turnaround success, and is highly dependent on the CEO’s intrinsic belief in this opportunity [64]. Accordingly, researchers initially viewed CEO replacement as a critical component of every turnaround effort [35]. Organizational failure becomes a personal defeat when people over identify with their organization and its current strategy, which escalates their commitment to an unworkable strategy [66]. Whitaker [101] claims that mismanagement causes more firms to enter financial distress than economic distress. It is possible, however, to reduce agency costs by mckinsey 7S aligning management action with shareholder interests by drastically reducing the income of CEOs who remain in distressed firms [79]. A successful turnaround requires a manager replacement, but it is not a necessity [66, 102]. According to Gilson and Vetsuypens [79], 33% of CEOs are replaced during turnarounds. Legal contingencies, however, must be considered. According to Barker et al. [103], there is little systematic evidence that replacements lead to organizational change during corporate distress. It has been argued that CEO replacement does not affect turnaround likelihood by Chen and Hambrick [104] and Daily and Dalton [63]. As long as the prior share performance was not extremely good or bad, CEO replacement doesn’t appear to have a significant impact on share performance [105]. Firms’ late response to default might be responsible for these findings. As early as 10 years before bankruptcy, decline can be detected, but management is not replaced until the company is in immediate distress [106]. Consequently, saving the already half-sunken ship becomes increasingly difficult.

H5a: There is a significant positive relationship between Leadership turnaround strategy and Hard S (strategy, structure & systems) elements of McKinsey 7s framework

H5b: There is a significant positive relationship between Leadership turnaround strategy and Soft S (shared values, style, staff & skills) elements of McKinsey 7s framework

H5c: Leadership turnaround strategy is practised by firms to survive in the time of distress.

The theoretical framework

The aspects of fragmented disciplines need to be consolidated into coherent bundles with sufficient generality [107]. According to Blalock [108], three strategies can be used to group diverse constructs into smaller groups with mutually interrelated concepts that are more understandable.

These are:

Theories that describe causal relationships between constructs Providing a link between certain indicators and their corresponding constructs using an operational language Integrated theory that explains the causal relationships between constructs and indicators.

In terms of the objective, the first two strategies are important since they aim to develop a theoretical language used to describe causal relationships between the examined constructs. Correlation has been used to explore causal ties, which in research terms cannot be viewed as causation in its most accurate sense, but still offers meaningful insights into the integrative framework. According to the literature reviewed, the synthesised theory can be represented by the following hypothesised model (Fig. 1). Table 1 summarizes the hypotheses that were proposed during the research.

Proposed conceptual model.

Mapping the constructs

As part of this study, it is determined if manufacturing firms implement operating turnaround strategies during times of distress or crisis; if they do, what are the factors that affect the results. Reviewing literature in a theoretical framework determined the conceptual scope of this study to examine turnaround strategies and their variants. Statistical methods are applied to test what operating turnaround strategies are implemented for successful reorientation and how they affect business results. Correlational research analyzes the extent to which dependent variables, mediating variables, and independent variables are related. The purpose of this research is to explore and interpret relationships between and among a number of facts. The research also identifies patterns and trends in the data. Data, relationships, and distributions of variables are examined. Variables cannot be manipulated; they can only be identified and studied as they occur in a natural setting.

Measures

Adopting from the literature reviewed we identified suitable scales for measuring the constructs and relationships; recoverability as five item scale by Brandon-Jones et al. [109], five measures from Wong et al. [110], Ward and Duray [111], and Gligor et al. [112] to capture operational efficiency; nine items to measure operational disruption by Essuma et al. [113]. Sixty item organisational turnaround scale was adopted by Moran [114]. Strategic turnaround scale was adopted by BeeriItai Beeri [115]. Four-point strategic turnaround scale has been adopted by Barker and Duhaime [5]. Leadership turnaround via top management scale by Barker and Patterson [116]; eight item scale for financial turnaround was from Ukaidi [117]. Strategic change scales were drawn from Barker and Duhaime [5].

Unit of analysis

The organization was the level of analysis identified for this study. The level of analysis is determined by the level at which the main research questions are posed and analyses are carried out rather than the level at which data are collected [118]. Snow and Hrebiniak [119] affirm that “ managers have the best vantage point for viewing the entire organizational system’. So, based on the methods employed by earlier researchers to collect data in manufacturing sectors the information was collected from managers and executives [120] and the data was hypothesized to represent aggregated measurements at the organizational level. The assumption is made that managers are in the position to judge firm-level attributes for drivers of advantage. This assumption was tested by Gibson & Birkinshaw [121], who found that data gathered from managers was strongly correlated with ratings from employees at four hierarchical levels in the business.

Data collection method

Data were collected using a survey methodology in this study. A longitudinal study would have been more appropriate, as the constructs developed here are better suited to long-term studies and have little relevance to short-term outcomes. Using the available literature survey, a series of measures were developed using the proposed conceptual model. The conceptual model developed and the objective to be achieved led to the formulation of 35 questions. Respondents were approached personally over LinkedIn in order to maximize the response rate. Based on our research, we narrowed down our list to 30 manufacturers in India who manufacture products. On LinkedIn, we contacted 1180 employees from the 30 companies that we identified and received responses from 230 employees across 18 manufacturing companies. 18 manufacturing firms operating in India responded to the survey, totaling 230 responses. This provides a satisfactory response rate of over 20%. Hitt [122]; Malhotra and Grover [123] have proposed valid studies if the response rate is above 20%.

As part of COVID-19, the confidential surveys were distributed at a time when most manufacturing firms were reorienting to keep up with the changing circumstances. Manufacturing firms got involved in manufacturing products needed to combat this global pandemic during this time. In particular, the manufacturers from which employees were contacted were from different sectors, such as FMCG and automobiles. It is important to collect comprehensive data at the decision-making level of the firm, including all of its innovation outputs and activities, since the subject approach in this study is largely based on self-evaluation by the respondents.

Measurement

In this study, survey items were based on a five-point Likert scale, where possible (1: strongly disagree, 5: strongly agree). The questions were straightforward and not ambiguous. To reduce measurement errors associated with single-item measures, multi-item measures have been developed. We conducted exploratory factor analyses to identify and refine the constructs used in the data analysis. The questions in the survey were specifically targeted to the period of time following the COVID-19 outbreak, which was six months after the pandemic outbreak.

To correspond with the five turnaround strategies, there were seven questions. There were also questions regarding Hard S and Soft S of the McKinsey framework. In SPSS, the mean of the responses was used to calculate the variables. Different items were considered for different variables. KMO and Bartlett’s tests as well as reproduced and coefficient were selected for factor analysis in SPSS. Analysis of the Correlation matrix was selected for the extraction process. Eigenvalues greater than one were also selected. We selected an unrotated factor solution and screen plot for the display. Varimax was selected for rotation.

Findings

Respondents

Table 2 below provides an overview of the respondents over 18 manufacturing firms. All in all, 230 responses were collected from 18 manufacturing firms operational in India. The group of respondents is a mix of male and female employees working in manufacturing firms. Also, the position of the employees working ranges from management trainee to executive level position.

Characteristics of respondents

Characteristics of respondents

The relationships between the variables are extracted from the data collected through responses for thirty-five different items. Approximately five items are associated with each turnaround strategy. The mean of the data is used to determine the relationship between variables. The mean of the first five items is taken for operational variables, and the mean of the next five items is taken for strategic turnaround variables, and the same was done for the three other independent variables. The critical factors put in items for specific mediating variables are taken into consideration when determining the mediating variables. In the questionnaire, fifteen critical factors affecting the Hard S and ten critical factors affecting the Soft S have been included to determine how strong the relationships are between the dependent and independent variables. The correlation between the turnaround strategies implemented and the survival of the firm is determined using Hard S and Soft S separately calculated. Now, the correlation between the turnaround strategies implemented and the survival of the firm is found. Also, the mean calculated for operational turnaround strategy is directly related to firm survival to check if there is no relationship between the mediating variables and the independent variable.

In Table 3, the total number of data points for each variable, the mean of the data, and the standard deviation are shown. The table includes all independent, mediating, and dependent variables. The 230 responses for each variable are taken into account. In the table, the mean of Strategic turnaround strategy is the highest, while the mean of Leadership turnaround strategy is the lowest. In addition, the standard deviations are highest in leadership variables, indicating that a greater number of respondents have given varying responses. When it comes to survival, we see that the deviation is less, which means that if any of the five turnaround strategies are implemented, the chances of survival increase.

Descriptive statistics

Descriptive statistics

For the two variables to be correlated, the correlation should be greater than 0.7. Cronbach’s Alpha coefficient values were greater than 0.6, indicating a high level of reliability. When correlation analysis was performed, no multicollinearity issues were identified. The results of reliability are presented in Table 4. The construct reliability (CR) value was found to be higher than 0.6, indicating the appropriateness of construct reliability and internal consistency [124].

Results reliability

Results of constructs

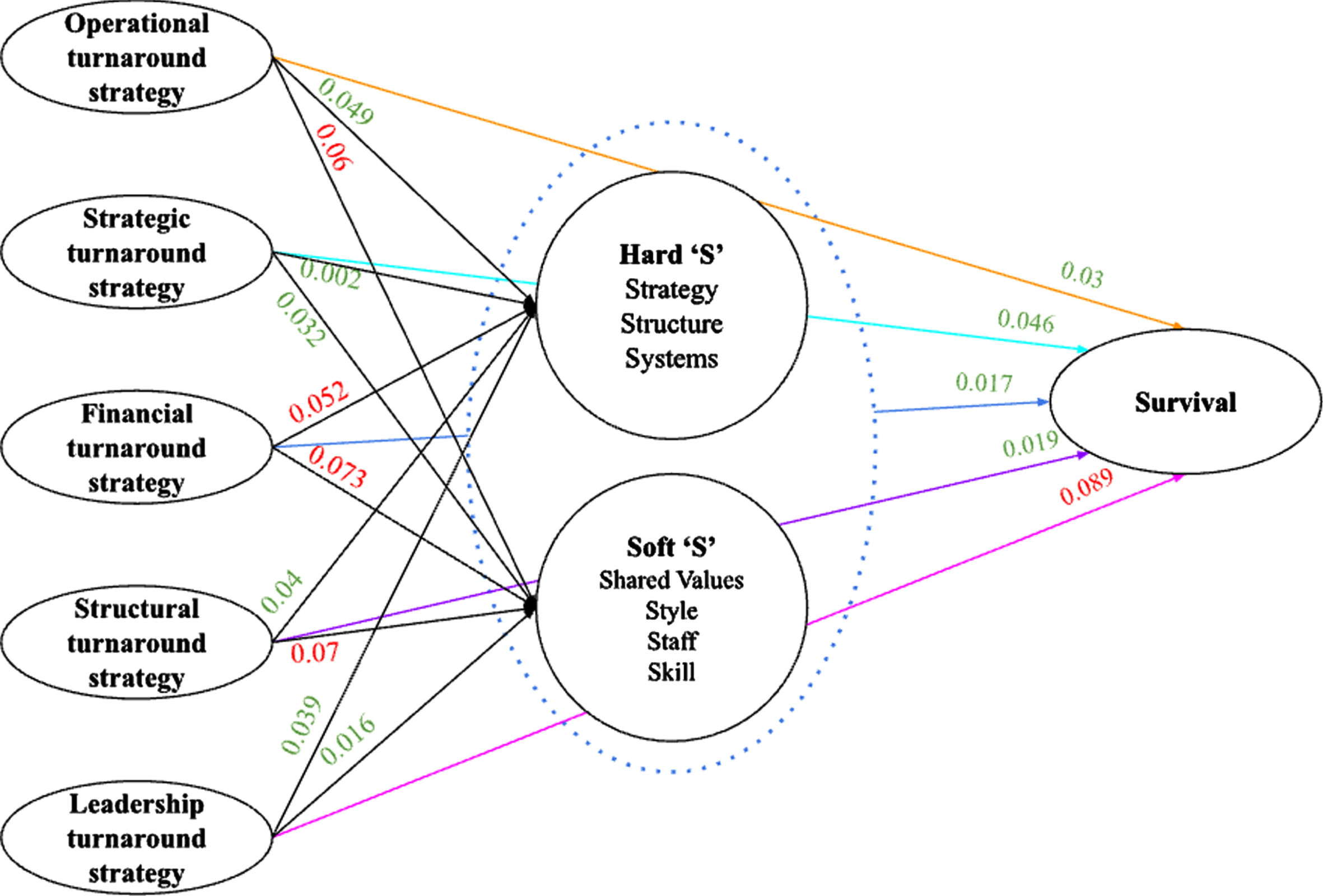

Hypothesis testing results based on P-Values (Green: Supported, Red: Not supported).

This study focuses on turnaround during a crisis. Extensive literature has been reviewed to develop the constructs. The scales were hypothesized to be unidimensional, therefore, all items under a construct loaded on that factor by having KMO greater than 0.5. The scale is reliable as the Cronbach Alpha values are greater than 0.5 [125, 126]. Stringent items loading retention rules as proposed by Bawa [125] and Tansey et al. [126] were followed where at least 3 items should load on a factor with items loading more than 0.5. Thus,

The EFA on Operational turnaround scale yielded one factor with 55% of total variance.

The EFA on Strategic turnaround scale yielded one factor with 45% of total variance.

The EFA on Financial turnaround scale yielded one factor with 57% of total variance.

The EFA on Structural turnaround scale yielded one factor with 48% of total variance.

The EFA on Leadership turnaround scale yielded one factor with 55% of total variance.

Implementing an operational turnaround strategy has a positive impact on the implementation of strategy, structure, and system. For this reason, manufacturing companies that implement operational turnaround strategies for reorientation in a time of distress should also revamp their structure, strategy and systems. The values, skills, style, and staff of companies looking to implement operational turnaround strategies need not be revised. During times of distress, it has no positive impact on the firm’s survival. It is important for firms in distress to implement operational turnaround strategies and have a positive effect on the firm’s survival. Reorienting the firm’s operations during times of distress allows it to survive. The primary objective of operational restructuring is to improve cash flow and profit in the short term. It is a firefighting effort and does not address the longer-term competitive position and performance of the firm. As a result, operational strategies may be necessary for recovery, but they aren’t sufficient in many cases. The hard S, consisting of the strategy, the structure, and the system, has a positive impact on the implementation of turnaround strategies in times of distress. For this reason, manufacturing firms looking to implement a strategic turnaround strategy for reorientation when they are in distress should also revamp their strategy, structure, and systems.

For turnaround, organizations need to be agile to transform threats into opportunities. An organization’s ability to turnaround is defined as the ability of its senior management to adapt, be flexible, and creative, as well as to anticipate unexpected shocks within and outside of its business environment. Threats can be transformed into opportunities if threats are addressed proactively, quickly, and effectively [127–129]. Doz and Kosonen [130] describe ability to turnaround as the ability to change the organization’s strategy dynamically as the business environment changes. According to Doz and Kosonen [130], strategic agility combines sensitivity to strategy, collective commitment, and resource availability. Two broader dimensions of turnaround have been identified and have been observed by the scholars which fall under strategic and operational [131].

Cost reductions, process improvements and restructuring collectively constitutes operational turnaround capability. Among the three hypotheses proposed, operational turnaround is driven by revamping strategy, structure and systems and it is necessary for firms survival at the time of distress. The hypothesis pointing relationship between operational turnaround and Soft S in Mckinsey 7S is not supported. It might be an indication that harsh, stringent and radical measures are required to implement strategies for operational efficiency. Thereby, ignoring the soft cultural attributes. Operational effectiveness and efficiency is deterministic to an organizational survival during a crisis. The versatility of resilient organizations enables them to manage their activities while minimizing losses when faced with severe operational disruptions and economic shocks [132, 133]. This finding is supported by the results revealed from hypothesis testing. Although communication, brainstorming, and an exchange of perspectives are crucial to achieve sustainability during the COVID-19 pandemic [134], it was not revealed by the respondents, maybe, due to acuteness and severity in the impact.

The dynamic capability view as a source of competitive advantage has proposed strategic turnaround as a bouncing back mechanism for organizational resurgence and turnaround. It also represents “strategic actions that provide the firms new resources or new ways to use existing resources” [135]. All the three proposed and validated hypotheses are supported. This brings to light the significance of strategic turnaround in managing crises and ensuring survival in line with the findings of [15, 136].

However, the process of turnaround is dependent on an organizational adaptation and learning [137–139] which indicated a robust relationship with strategic turnaround and McKinsey 7S Soft S elements. On the other hand, it is also relevant to radical reorientations in an organization’s strategy and structure [140] which suggests robust relationships with the Hard S elements of McKinsey 7S. In fact, researchers on the subject of organizational decline and turnaround have long maintained that performance declines will lead to organizational rigidity and negatively impact its innovative choice by lessening organizational abilities to implement its needed strategic reorientations [95]. This is in line with our findings indicating a positive relationship between strategic turnaround and organizational survival.

A general defect of all existing approaches in the strategy literature is the relative absence of research on the financial aspects of turnaround [47]. Both agency [131, 142] and strategic management [142, 143] research acknowledges that the structure of financial liabilities and related governance aspects may have an important impact on the firm’s strategic decisions. The leading indicators in event of crises are the financial indicators. This becomes a priority and focus area because they are the most visible indicators. While some organizations experience financial distress and struggle with declining or challenging operating margins, a “turnaround” is a significant improvement of the organization’s financial health and operating margins. Liquidity of enterprises suffers when the demand for products and services drops during a crisis. In addition to micro-level disruptions, macro-level disruptions pose a threat to organizational financial sustainability and the viability of entire sectors [144, 145].

Our findings are in parlance to the earlier research on financial turnaround whereby it has a significant relationship with organizational survival capabilities. Insufficient standard financial regimes lead to the emergence of complex financial decision-making [146]. Capital structure dynamics vary among organizations, and thus rely on attributes of asset volatility, tax and growth rate, transaction, and liquidity [146, 147]. Without financial risk management, all organizational efforts to survive the crisis will be ineffective [148, 149]. It is also observed that financial turnaround strategy acts through Hard S elements of McKinsey 7S which is supported by recent research on turnaround suggests that the performance outcomes of asset and cost retrenchment are contingent on industry dynamics, which, in turn, affects the underlying value of the firm’s assets [47].

In an effort to overcome crisis, organizations can modify formal structures, improve sense-making, and adapt to improvisations through managerial mindfulness [150]. According to literature, communicating with employees more effectively and engaging in proactive interactions with them helps mitigate adverse effects after disasters [151–153]. The tested hypothesis indicating relationships between structural turnaround and McKinsey Soft S is not supported contradicts the literature emphasizing communication. We feel that this deviation might again be attributed to the acuteness and severity of impact which Covid 19 has presented.

Dewar and Dutton [136] proposed that a shift towards a mechanistic structure that leads to centralization of authority and decision making processes will have a negative effect on the adoption of incremental innovations. On the other hand, decentralization leads to empowering individuals at lower levels to take a sense of ownership on what they do and propose the needed change that accelerates performance. This confirms our findings of a positive relationship between structural turnaround strategy and Soft S. Similarly, Barker and Mone [73] argued that mechanistically oriented organizations may have difficulties changing their strategic orientation during the time of decline, as authority is consolidated with people who have less dealing with the environment. Jones [154] poised that organizations with organic structure and adaptive cultures value innovation, encourage both explorative and exploitative learning, and are more likely to actively seek new ways to improve.

The leaders of the system should bring together all participants in one place, engage them in a dialog, collect a variety of viewpoints, experiences, and visions about the event, and reach a consensus [155]. Organizations are commonly depicted as pyramids, with system agents as the component parts of a network. It is accomplished through “conversation-for-action” formulas that engage them in information exchange [156]. Leadership must take such action as a first step toward building a more resilient organization. Such an initiative must be the first step of leaders while forming a more resilient organization. This supports hypothesis H5a and H5b, wherein leadership has a positive relationship with Hard and Soft elements of McKinsey 7S.While many variables are a part of the turnaround process, management in general and Top management team in particular has the ultimate responsibility as it is the principal catalyst in the revival of troubled firms [157]. In their study of the 100 largest organizational crises over a five year period, Probst and Raisch [158] identified leadership as one of the major problem areas. Because of the extensive prolonged and widespread crisis, no leadership style could make a turnaround. This might be the reason why the hypothesis establishing the relationship of survival with leadership turnaround was not supported. This is in line with the decline and turnaround literature where scholars have often attributed decline to organizational leadership as they have often failed to achieve organizational goals or to change and/or turn their organization around [159–162].

Conclusion, managerial implications and directions for future research

The purpose of this study is to determine the relationships between the turnaround strategies implemented by the firms, the hard S and soft S of McKinsey 7s model, and their survival. During times of distress, manufacturing firms implement turnaround strategies to ensure their survival. Consequently, the implemented turnaround strategies help the firm to reorient itself, therefore, contributing to the firm’s survival. Firms go through periods of downtime when they are distressed or in crisis. In order to survive in the current business environment and compete, a company needs to change the way things are done. Turnaround strategies are implemented for firms to bring about a change. In times of distress or crisis, companies implement operational turnaround strategies in order to survive by redesigning their strategy, structure, and systems. It is easier to identify and manage strategy, structure, and systems, which are the hard things.

In addition, firms reorient themselves through financial, structural, and strategic turnaround strategies. A strategic turnaround strategy and financial turnaround strategy also have a significant positive relationship with the odds of a firm’s survival during times of distress. By reorganizing the style, staff, skill and shared values of an organization, firms practice structural turnaround strategies. The soft S will be the most difficult to manage, but they will provide a more sustainable competitive advantage since they are the foundation of the organization. During times of distress, firms also implement leadership turnaround strategies that change their top management team and board of directors. In this study, however, there was no positive correlation between the adoption of leadership turnaround strategies and the survival of firms in times of distress.

This study suggests that firms in distress should be longing to implement operational, strategic, and financial turnaround strategies in order to reorient themselves. These strategies typically require less time to implement than structural turnaround strategies. If manufacturing firms are looking to implement changes and have time restrictions, they should focus on operational, strategic, and financial turnaround strategies, as these are easier to identify and implement. Companies seeking reorientation and wishing to gain a sustainable competitive advantage should implement structural turnaround strategies.

This study, like any other research, needs to be interpreted carefully due to its methodological limitations. The data collected from respondents were working in manufacturing firms operational in India. If they had collected information from respondents in a variety of manufacturing firms across the globe, their sample could have been more diverse. A person unfamiliar with a turnaround strategy would also have difficulty simplifying some of the terms used in the questionnaire. This might have impacted the quality of the data collected. Most of the data collected is from the FMCG and automobile industries, but it could have been diversified further by collecting data from other manufacturing firms. The findings may be biased due to the complexity of the distress or crisis. We only considered external stress factors in this study. To gain a deeper understanding of the distress caused by internal factors, further research is needed.

The external stress factors are the only ones considered in this study. The internal factors of distress in a company can be the subject of further study. Moreover, the sample size should be greater than what was used in this study in order to extract meaningful information from the data. McKinsey 7s has been used in this study as a mediating variable, finding the relationships between turnaround strategies and the survival of the firm during distress or crisis. Further studies could examine the impact that individual moderating variables have on the survival of the firm by using the McKinsey 7s model as a moderating variable. Other industries or other turnaround strategies, such as retrenchments within the same industry, may also apply. Perhaps we can even map the relationship between some economic conditions and the given set of turnaround strategies.

Author contributions

This manuscript was conceptualized, developed, analyzed, and prepared collaboratively by all authors.

Questionnaire:

Dear Survey Respondent:

We, Janvee Garg and Sonika Jha are FPM Scholar at FORE School of Management, New Delhi, and are doing research on Manufacturing firms and the turnaround capability during Crisis. I am investigating the effect of different turnaround strategy options on the organizational capability to change for survival.

Can you please help us? We are trying to find out the factors that drive the Turnaround capability of manufacturing firms. We are enclosing a questionnaire which you will kindly complete. By completing the enclosed questionnaire which will take 20-15 minutes, you will be helping us to make a contribution to research on business in India. We want to contribute in whatever small way we can to a very significant sector in the Indian economy.

Your answer to the following questionnaire will be used in a research study concerning the drivers of Turnaround and survival in the Indian Manufacturing Sector. Your responses will indicate your perception about what contributes to the survival of firms during crisis and how firms manage turnaround. Response indicating your opinion about the better performing firms should be marked in the space provided against the statements. There is no right or wrong answer, only your opinion. This study is for academic purposes only. Your privacy will be protected. All responses will be reported in aggregate only; nothing is reported on an individual basis.

Thank you for your help!

Footnotes

Acknowledgments

The infrastructural support provided by the FORE School of Management, New Delhi in completing this paper is gratefully acknowledged. We also sincerely thank Mr. Saqib Ahmad for the crucial support in the execution of this study and the HSM reviewers for helping us improve the outcome of the research.