Abstract

Financial time series data is very chaotic, noisy, fluctuating and nonlinear as different events have occurred in various time periods. Therefore, it is very challenging for researchers to develop the accurate predictive model. Prediction for Foreign Exchange rate is also a very crucial task for

Keywords

Introduction

Exchange rate expectations play an important role in the literature on exchange rate determination [1]. Understanding how exchange rate expectations are formed is crucial for academic analysis of exchange rate behavior, as well as for decision-making of both practitioners and policymakers [2]. Models of exchange rate determination in open-economy, macroeconomics often rely on assumptions about rationality of exchange rates expectations [3]. It is practically impossible to test the implications of theoretical exchange rate models, without running into the problem of joint hypothesis testing in the absence of survey-based expectations [4]. In addition to analyze exchange rate behavior, the rationality assumption can have serious implications for evaluating the effectiveness of many government policies [5, 6]. The availability of survey forecasts allows us to evaluate the rational expectations hypothesis directly.

Although survey-based forecasts of other macroeconomics variables have been studied in the literature for at least 60 years, research on rationality and accuracy of exchange rate forecasts goes back only to the late 1980s [7]. Limited data availability on professional exchange rate forecasts is partially responsible for the short history of research on survey-based exchange rate forecasts. Following early studies of Dominguez [1] and many other researchers who, have studied the nature of exchange rate expectations using survey data, we have two most commonly examined questions in the literature on survey-based exchange rate expectations as rationality of the forecasts and their predictive accuracy [8].

In this paper we have focused on currency exchange rate that is the rate at which currency of two countries exchange against each other. Currency exchange rate plays an important role in financial markets. Exchange rates are determined in the foreign exchange market [9, 10]. A stable exchange rate is helpful for financial institution for investment, where as a fluctuation in exchange rate will affect interest rate, unemployment, prices and wages of a country. Prediction of correct exchange rate will be helpful for the economical growth of any country. There are many statistical models used for prediction of currency exchange rate such as Random walk (RW), Autoregressive integrated moving average (ARIMA), Generalized autoregressive conditional heteroskedasticity (GRACH), Simple averaging, Stack regression and Variance based models [11, 12, 13, 14, 15]. In this paper, we have focused on some of the biologically inspired network models for prediction of currency exchange rate. Input dimension and the time delay are two critical factors that affect the performance of neural networks [16]. Many researchers have proved the effectiveness of predicting currency exchange rate by using multi-layer perception (MLP), radial bias function neural network (RBFN), and functional link artificial neural network (FLANN) models [17, 18, 19, 20, 21, 22, 23, 24, 25]. Researchers are taking the currency exchange rate data of different countries on daily, monthly, and quarterly basis and then predict the exchange rate and analyzed the percentage of error. The model having a less percentage of error considered as a best model for currency exchange rate prediction. From the research analysis we found that RBFN and Cascaded functional link artificial neural networks (CFLANN) models have better accuracy rate than the other models.

This paper is set out as follows. The second Section gives an overlook to the foreign exchange rate and the factors affecting the exchange rate. It also describes the necessity of prediction of exchange rate with different approaches. The third Section gives a brief idea about different neural networks used for exchange rate prediction. The fourth Section describes ARMIA model to predict the exchange rate. In the fifth Section we have analysed an integrated model using ARMIA and neural networks. The sixth Section presents the performance comparison and analysis that we have obtained form the intensive empirical analysis of different exchange rate predictions techniques and in the last Section, we have given the conclusion and future work about the empirical analysis.

Exchange rate prediction fundamentals

Exchange rate is the rate at which one currency will be exchanged for another, which is determined in the foreign exchange market. Forecasting of exchange rate are necessary to determine the foreign denominated cash flow involved in international transactions, so predicting the accurate exchange rate help any country to determine the benefits and risks in the international business environment. Forecasting of exchange rate will be done using an information set selected by the forecasters. Factors that affect the exchange rate are as follows:

Interest rate – Interest rate directly affects the exchange rate. Exchange rate increases with increase in interest rate. Inflation – Lower inflation increases the currency value. Current account deficits – Current account is the balance of trade between a country and its trading partners. Deficit in current account shows the country is spending more on foreign trade than earning, so it decrease the currency exchange rate of that country. Public debts – Public invest their money in government projects or public projects and foreign investors also invest their money if inflation is more. If government is unable to refund the money of public when the country export something and at that time other country does not give appropriate money, then exchange rate will decrease. Terms of trades – If the export price of a country rises by greater than that of its import then it’s terms of trade will be improved and currency value will be increased. Political stability and economical performance – Foreign investors search stable country with stro-ng economics performance in which they can invest their capital.

Based on the information set two approaches for prediction of exchange rate are presented as fundamental approach and technical approach.

The fundamental approach is based on some fundamental economics variables on which exchange rates are predicted. Usually these variables are inflation rate, interest rate, term of trade, trade balance, etc. Fundamental model is based on structural model which is a mixture of art and science [1, 2, 3, 4, 5, 26]. Structural model are used by practitioners to generate equilibrium exchange rate. Projections or trading signal are generated by using these equilibrium exchange rate. A trading signal is generated every time, when the practitioner determine difference between expected exchange rate and actual rate is due to mismatch in pricing then buy or sell signal is generated. Fundamental approach starts with a model which is based on purchasing power parity (PPP) theory [27], Based on this model first the data are collected using different statistics and measure forecasting equations. Let

Mean square error (MSE) for the model is calculated as:

Where,

It is based on price information. Turning points are detected by computer and based on this trading signal is generated. Mainly we are using moving average (MA) for technical approach. Simple average of past price will be done in MA model [28]. In simple moving average (SMA) model we use unweighed mean of the previous

When, we take most recent past price then short-run MA (SRMA) will be calculated [29]. When, longer series of past prices are taken then long-term MA (LRMA) is calculated. A double MA system uses LRMA and SRMA. In MA model when SRMA past rates cross LRMA, buy and sell signals are usually triggered. When the currency moves downward its SRMA will below its LRMA and when currency rises then it crosses LRMA by generating a buy foreign currency signal. Instead of using these direct methods we can use several supervised learning methods such as neural networks for the accurate prediction of foreign exchange rates, which are discussed in the next Section.

Prediction of exchange rate is very essential because it affects the economics and financial management of a country, so different methodologies are develop to predict exchange rate more accurately. Some of the neural networks methodologies used to predict the foreign exchange rates have been discussed below:

Multi-layer perceptron neural network

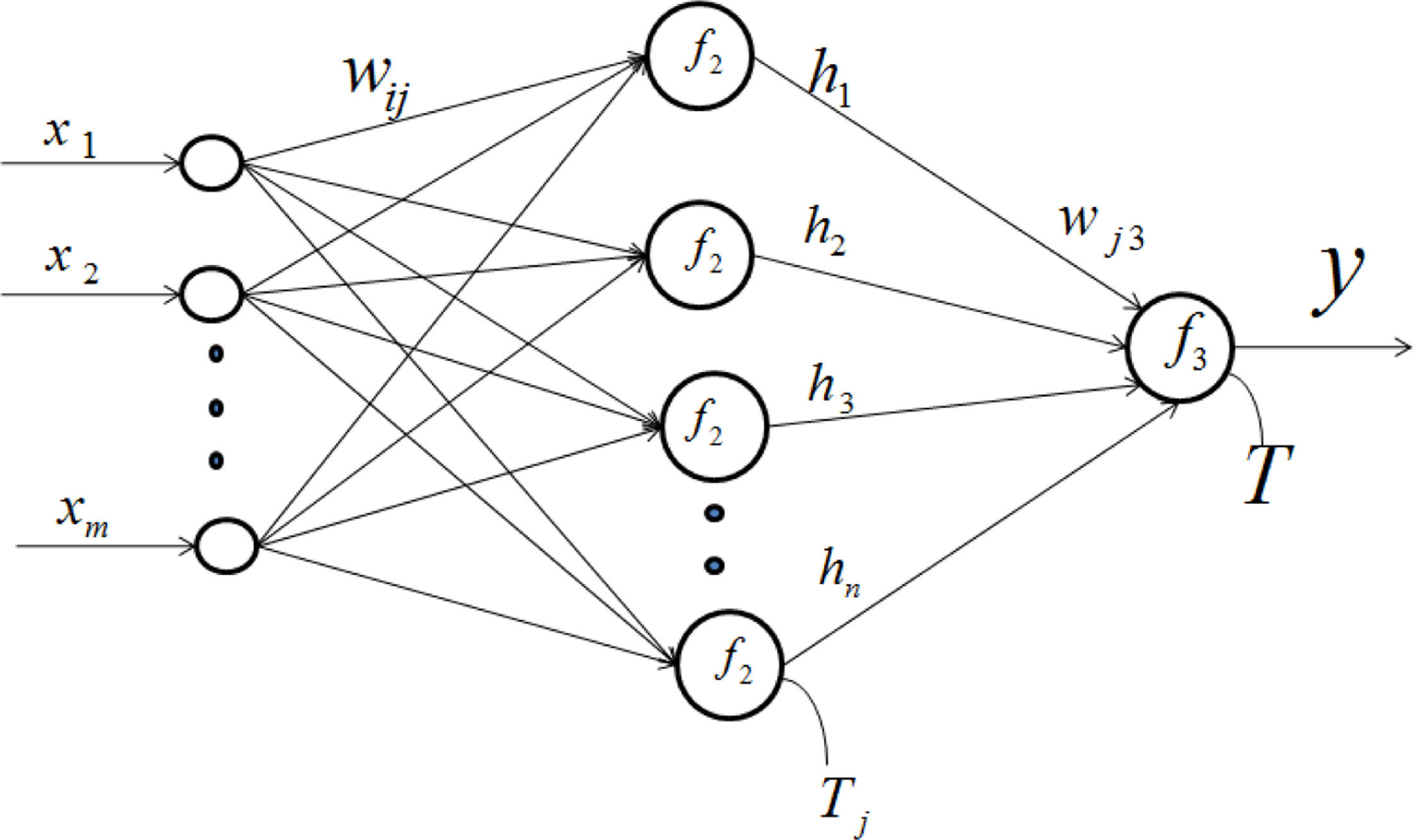

A single layer artificial neural network is unable to solve the non-linear problem, so a model is required to solve the nonlinear problems because most of the input data are noisy and non-linear in nature. A multi layer model solves the nonlinear problem [30, 31]. Multi-layer perceptron neural network is an artificial neural network used for classification, pattern recognition and prediction [32, 33]. MLP consists of input layer, hidden layer and output layer, the number of hidden layer changes depending on training data [34, 35, 36, 37, 38, 39, 40]. Most common activation function for MLP are sigmoid and hyperbolic tangent. All nodes in hidden layer uses same activation. By increasing number of hidden layer does not mean that accuracy of MLP will increase, so a network always try to take maximum two number of hidden layer, because hidden layer increase the complexity of the network. MLP use a supervised learning technique where desired output was known by the network. Architecture of MLP is given in Fig. 1.

The generic architecture of the MLP neural network.

Out put of the MLP network ‘

where,

where,

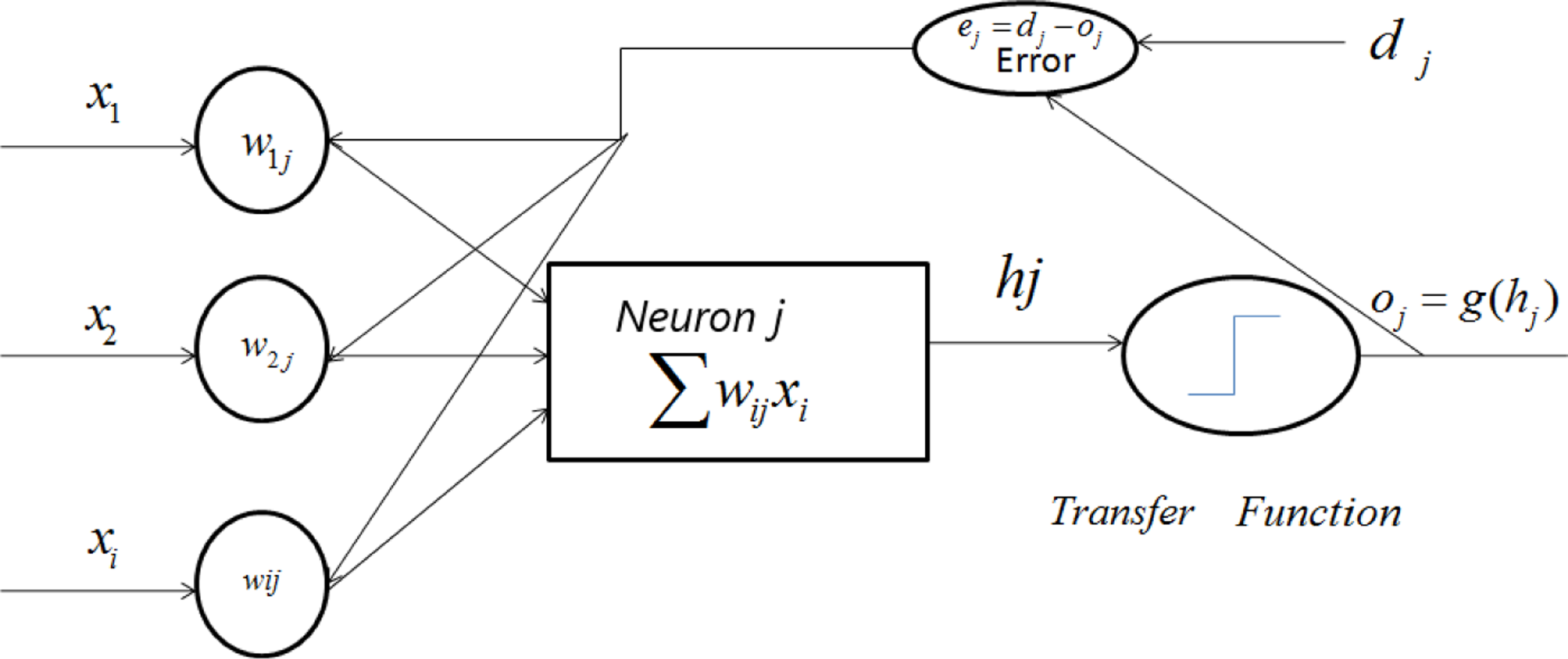

Back-propagation learning allows supervised lear-ning procedure where desired output is known by the network before training process. Learning occurs by changing connection weights based on the amount of error in the output. Error produced in the output propagate towards backward direction to the network for minimizing the error produced by the network. It uses gradient descent method for minimizing the error in weight space because weight is the solution of the learning problem. If the state of system moving in the opposite direction to the largest local scope then weight are updated in downward direction [40, 41, 42, 43, 44, 45, 46, 47]. An activation function is used in the hidden layer and output layer which compute the gradient of error as shown in Fig. 2.

Back-propagation of errors for a single neuron.

where,

Bayesian network is a directed acyclic graph, used for regression, classification, and inverse problem [48, 49, 50, 51]. In Bayesian learning entire distribution of model prediction estimation is done instead of the mean prediction estimation of the model. This estimation take noise in the data and variance of the model. For all unknown data Bayesian approach produce posterior probability distributions [52, 53, 54, 55]. In Bayesian learning for MLP neural network the natural end variables are the predictions of the model for new input. For input

where,

The MLP neural network uses many layers and many hidden neurons in each layer, which potentially increases the complexity of the overall network. So, we can also use the simpler RBFN models to predict the exchange rate of any country having less complex neural networks, which is discussed in the next Section.

RBFN is a simple neural network having powerful problem solving ability. Name of the network is RBFN because it uses radial basis activation function. It has three layers, that are input layer, hidden layer and output layer as shown in Fig. 3. In the input layer data are given to the network, then this input multiply with the weight and given to the hidden layer.

Architecture of RBF neural network.

The distance between the input node and hidden node are calculates as:

Radial basis activation function is used to transforms the Euclidean summation

The out put of the RBFN is calculated as:

The error is calculated as

where,

Combination of RBFN models produce less amount of error and gives better result than single RBFN model. So a multistage RBFN model was develop where numbers of single RBFN are combine together and consider as a single RBFN model [64, 65, 66, 67, 68, 69, 70]. A multistage RBFN have three stage as shown in Fig. 4 and are presented as:

Architecture of multistage RBF neural network.

Producing multiple single RBFN predictorsPerformance of a RBFN depends on number of node in the hidden layer, cluster center, width of cluster and on the training data, so in the first stage multiple number of RBFN are produced by varying the number of node in the hidden layer or by changing the cluster center or by adopting different cluster radius of the RBFN neural networks or by using different training data. Choosing appropriate ensemble membersEvery RBFN produced different result when input data are given to it, generally PCA (Principle Component Analysis) technique is used to choose appropriate RBFN having less amount of error in order to increase network efficiency. However, the PCA is a kind of data-reduction technique, which does not consider the internal correlations between different ensemble members. To overcome this problem, a Conditional Generalized Variance (CGV) minimization meth-od is proposed. Combining the selected membersAfter selecting the appropriate model the out put of all the model are combine and final output is produced

where,

We can also use another simple technique such as FLANN to predict the exchange rate, which is discussed in the next Section.

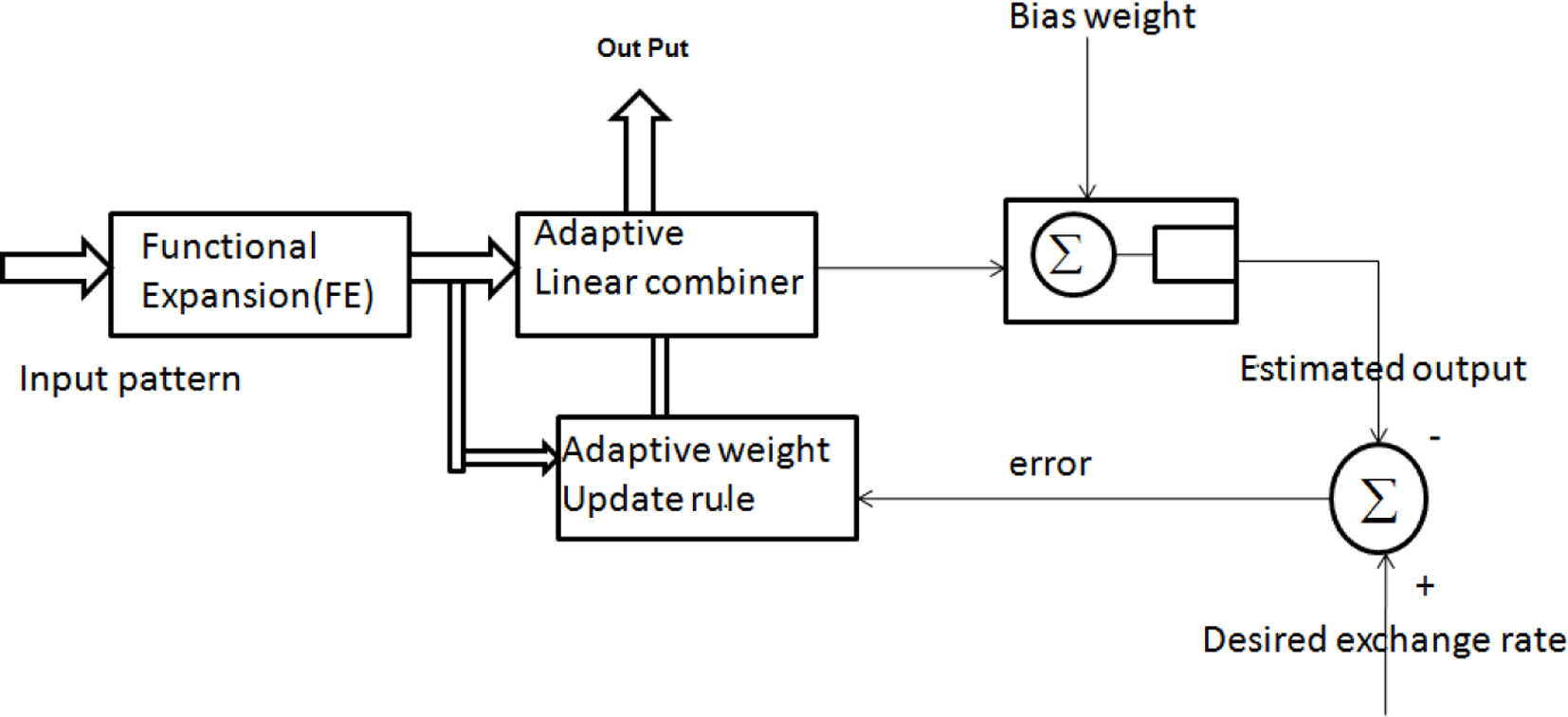

FLANN is a single layer artificial neural network. It is capable of performing complex decisions i.e. it can work with nonlinear data with out hidden layer [71, 72, 73, 74, 75, 76, 77]. Hidden layer is removed to reduce its computational cost. Inputs are functionally expanded using some trigonometry expansion. Let’s consider a two dimensional input

Functional expansion process: In this input element is nonlinearly expanded to create numbers of inputs. The number of element after expansion becomes more than original input. Estimation process: It compute the output of adaptive model and generate the error signal. Adaptive process: It adjust the weight by weight update learning rule.

The learning process of FLANN is given in the next Section.

Block diagram of FLANN.

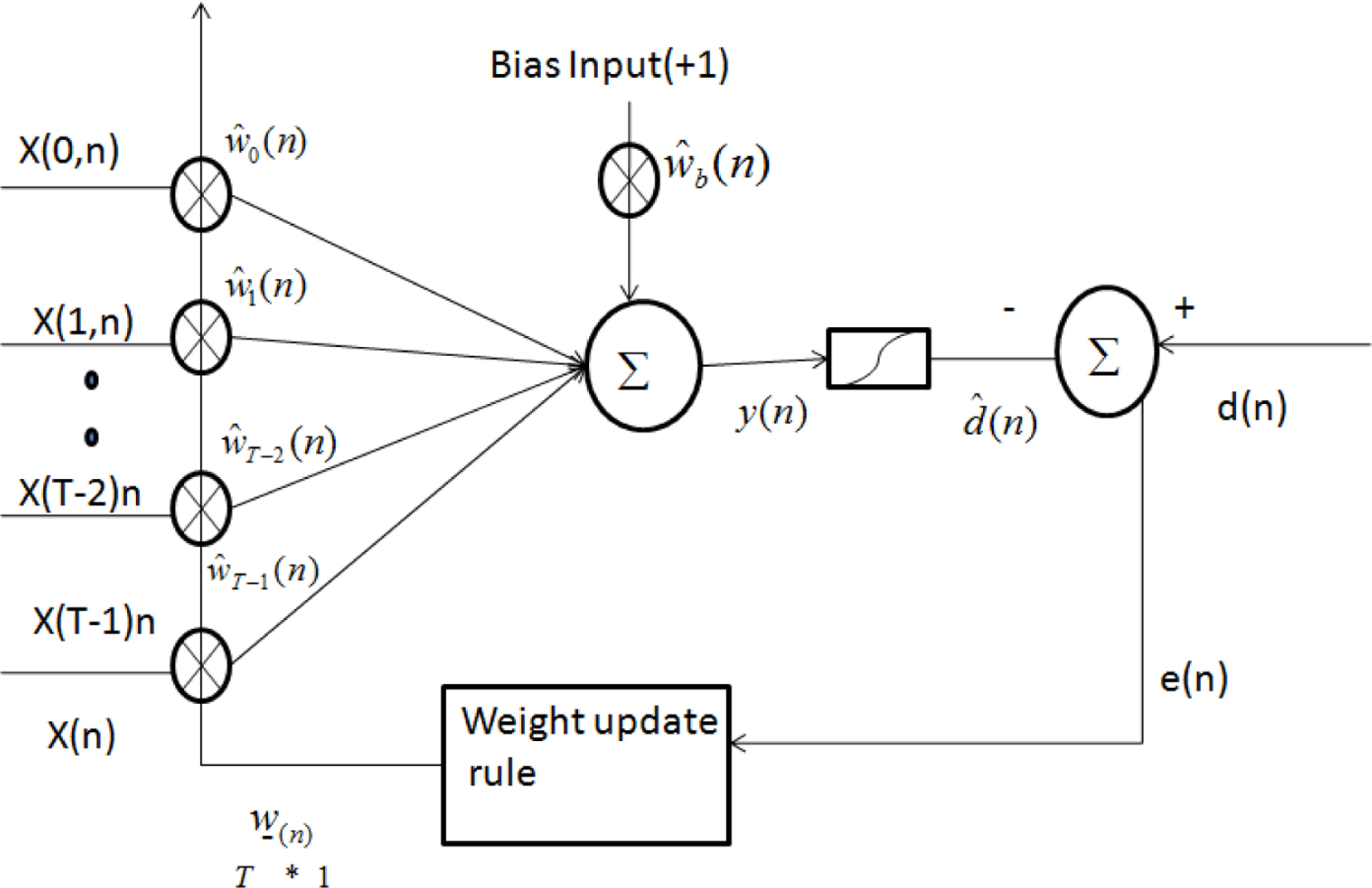

FLANN use back-propagation learning algorithm for training the network [78, 79, 80, 81, 82]. Error produced by it is calculated by substituting the estimated output from desired output and propagate backward for weight updating using weight update rule as shown in Fig. 6.

Architecture of FLANN.

Let

where, the system output is denoted as

Then the correction weight vector is given by

The change in bias weight can be obtained and is given by

where,

Weight are updated as follows

Change of bias is calculated as follows

Bias will be updated as

Experiment is continue until MSE will reach a minimum value. MSE will be calculated as

When, the training process is completed weight are fixed with the new value and the testing process will be conducted. We can also use CFLANN to predict the exchange rate as discussed in the next subsection.

In this model two single FLANN are connected in series as shown in Fig. 7. Each FlANN are passed through back-propagation algorithm and output of first FLANN given to the second FLANN as its input. This value also expanded using trigonometric function [83, 84, 85, 86, 87]. The block diagram of CFLANN is presented in Fig. 7.

Block diagram of CFLANN.

Where, FL1 is the first FLANN and

and the output

The operational principle is same as single FLANN till we get a minimum MSE. In the next Section we have analysed some of the statistical models integrated with neural networks.

ARIMA models are generally combination of autoregressive (AR) and moving average model (MA), a non seasonal ARIMA model is denotes ARIMA

AR represent the current time series value

where,

where,

We can also use integrated ARIMA model with neural networks to produce better results as discussed in the next Section.

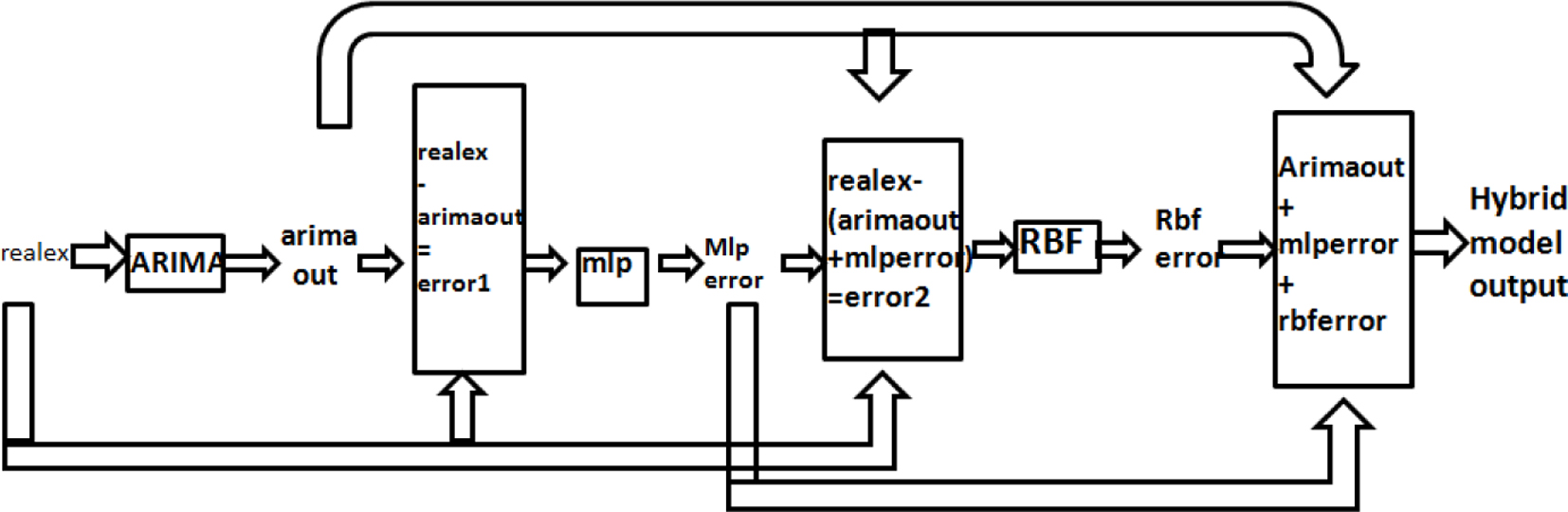

An integrated model is produce by using ARIMA, MLP and RBF model. In this model real exchange rate is called relax and predicted exchange rate is called arimaout. First the time series data is given to the ARIMA model and the produced output and error is called error1 as shown in Fig. 8.

Error in ARIMA model.

Error1 is the error produced by ARIMA model. This error1 is given to MLP and result is mlperror as shown in Fig. 9.

Error in MLP model.

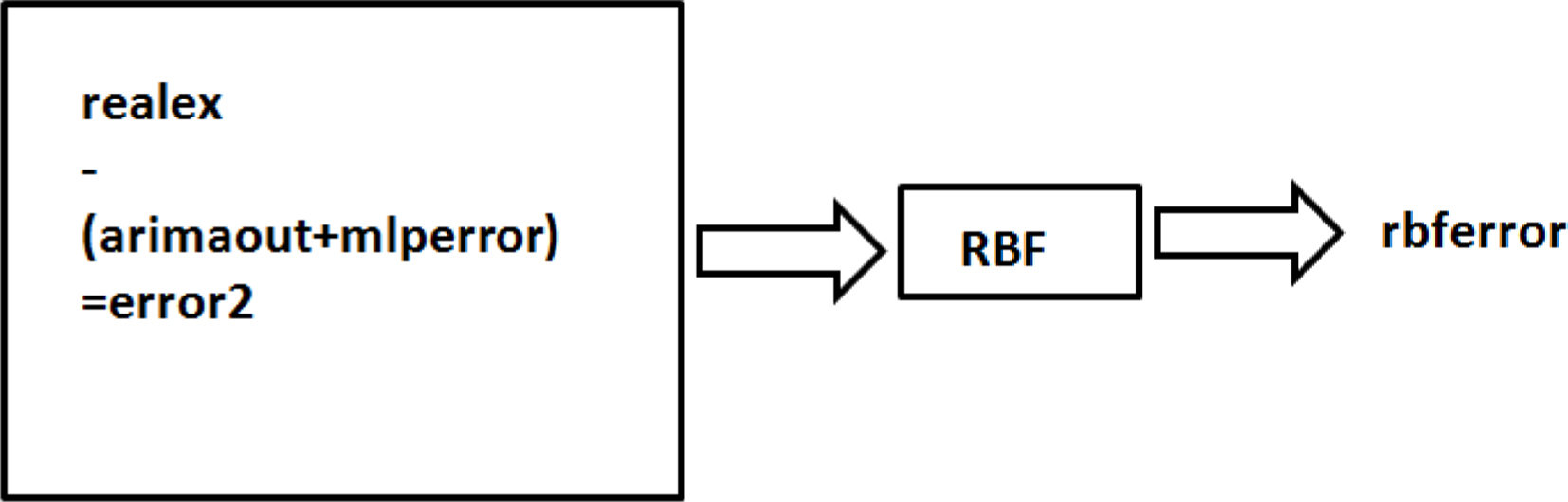

Relax

The final result of the proposed integrated model comes from the summation of the error modeled by RBFN and the error modeled by MLP with the time series that was modeled by ARIMA [88, 89, 90, 91, 92, 93, 94]. Final model is given in Fig. 11.

Error in RBFN model.

Integrated model using MLP, RBFN and ARIMA.

In this review paper different models are analysed that takes different exchange rates from different countries with varying time duration. The number of training and testing data are also vary with different types model and are described in this Section.

Dataset preparation

In this Section we have explained the various type of data used in different models for their analysis. Each set of data are normalized by dividing each value by the maximum value of each set such that each normalized value is less than or equal to unity.

MLP with back-propagation learning For this model data has been collected as follows

Daily datasetDaily exchange rate of EUR/USD, GBP/USD, USD/JPY are taken from the site. Monthly datasetThe monthly exchange rate of EUR/USD, GBP/ USD, USD/JPY are taken from. Quarterly datasetThe quarterly data of EUR/USD, GBP/USD, USD/JPY are taken from site: MLP with BAYESIAN LearningFor this model data has been collected as: U.S. dollar against the British Pound (GBP/USD) and Japanese Yen (JPY/USD) from Jan 1990 to Dec, 2002 are taken daily wise, which was given by Professor Werner Antweiler, University of British Columbia, Canada. Sixty patterns are used for testing and rest of the data are taken for training the network. RBF CNY Exchange Rate For this model data has been collected as follows GBP – CNY and USD – CNY, are taken from 27-Apr-2005 to 12-Feb-2009, and from 1-Apr-2005 to 13-Feb-2009 respectively. The daily closing price of the two spot exchange rates were found on the Web site: Integrated modelFor this model data has been collected as follows EUR/USD (Euro to US Dollar) exchange rate is used for the model design, validation and testing. The data are taken from the Federal Reserve Bank of St. Luis, economics research center’s web site. The data set from 1 April 2001 to 31 July 2010 are taken and 7:2:1 ratio is used for training, validation and testing purpose. Multistage RBFData are obtained from site: FLANN and CFLANNFor this model data has been collected as follows: Exchange rate of US dollar to Pound, Rupees and Yen are taken. Some common features from past conversion rates are extracted for training and testing purposes. Each set of data are normalized by dividing each value by the maximum value of each set such that each normalized value is less than or equal to unity. Normalization of input data is necessary for obtaining correct trigonometric expansion.

In this work, most of the models have used neural network tool box provided by Matlab software package. The author has taken one input variable, six hidden nodes and 6000 iterations to compare NN models with RW, GARCH, and ARIMA model. For MLP neural networks the authors have used (7-6-5-1), (7-4-2-1) and (5-10-1) network architectures and for RBF neural networks the authors have used (7-11-1) and (7-9-1) network structures. The learning parameters for learning algorithm of MLP neural network were eta

Error function

In this Section, we have discussed various error functions as follows:

We can determine the error of a system as Root – mean – square error and can be calculated as follows

where,

where,

where,

where,

if

Error in The MLP with back – propagation learning

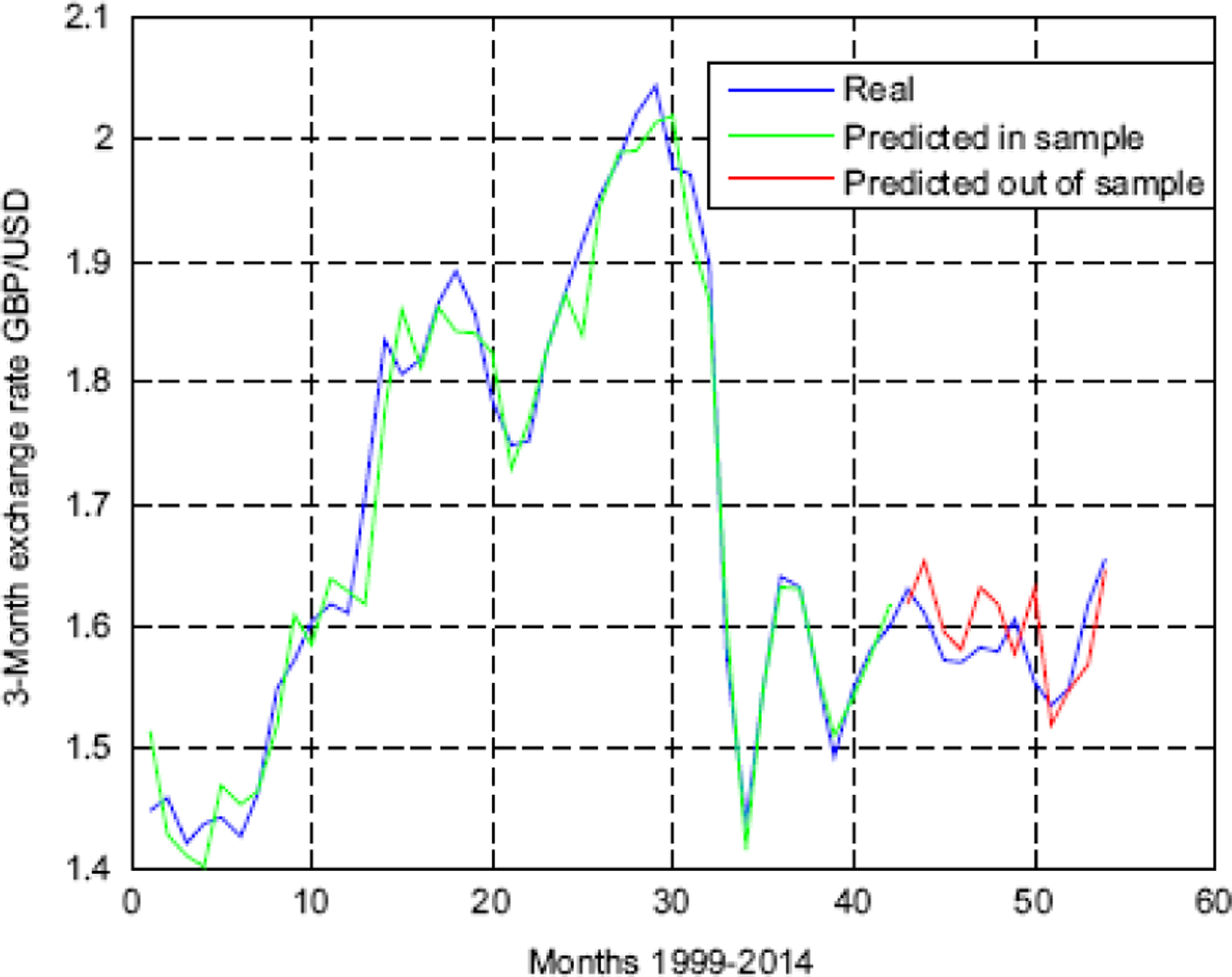

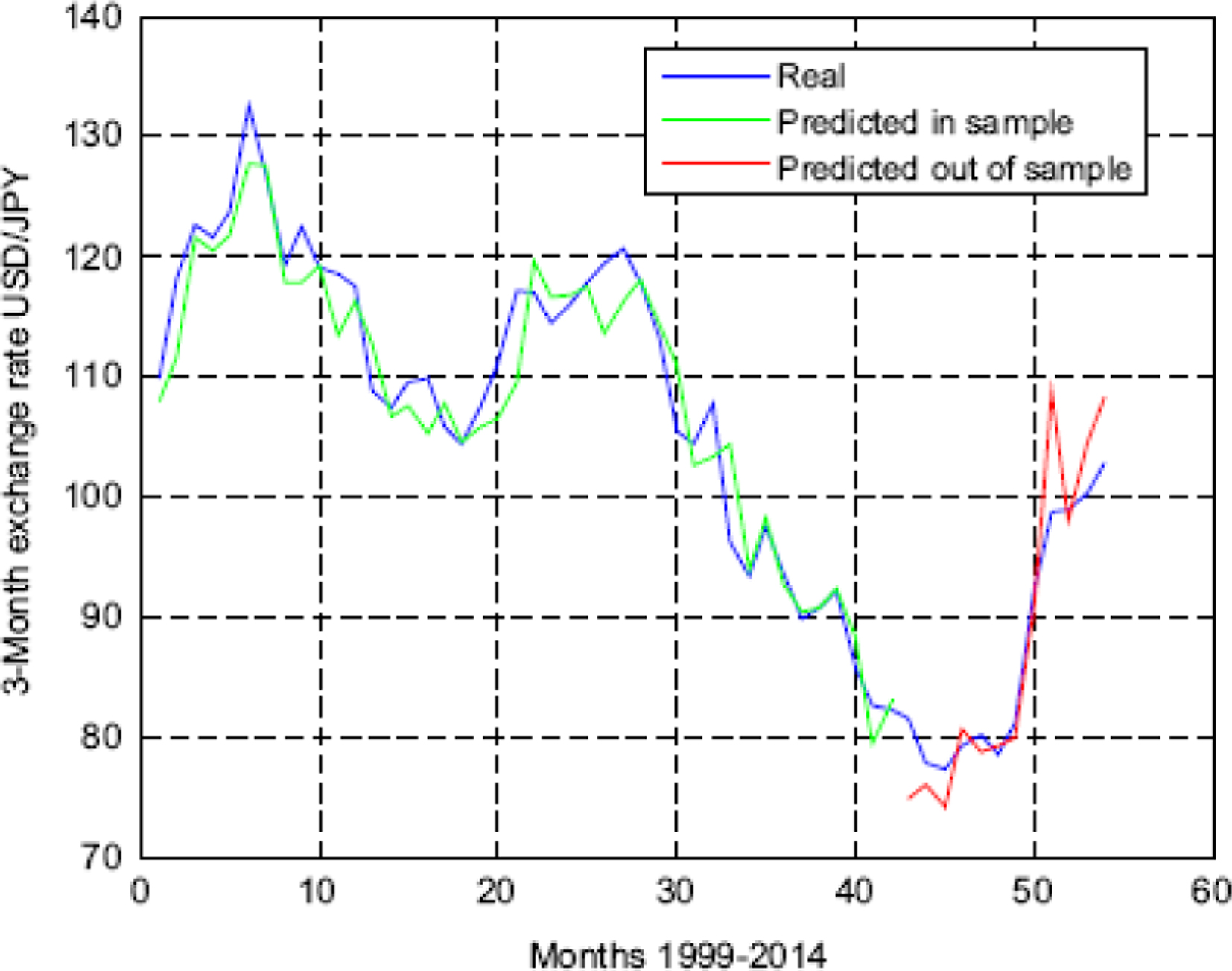

Error in neural network models (GBP/USD)

Error in the neural network models (JPY/USD)

Error produced in different models

In this Section we have analysed the performance of different models and we have determine which model produces less amount of error and more accurate output based on the survey analysis. The details of the analysis are given below. At last we have provided a comparison table for the above analysis.

MLP with back-propagation learning

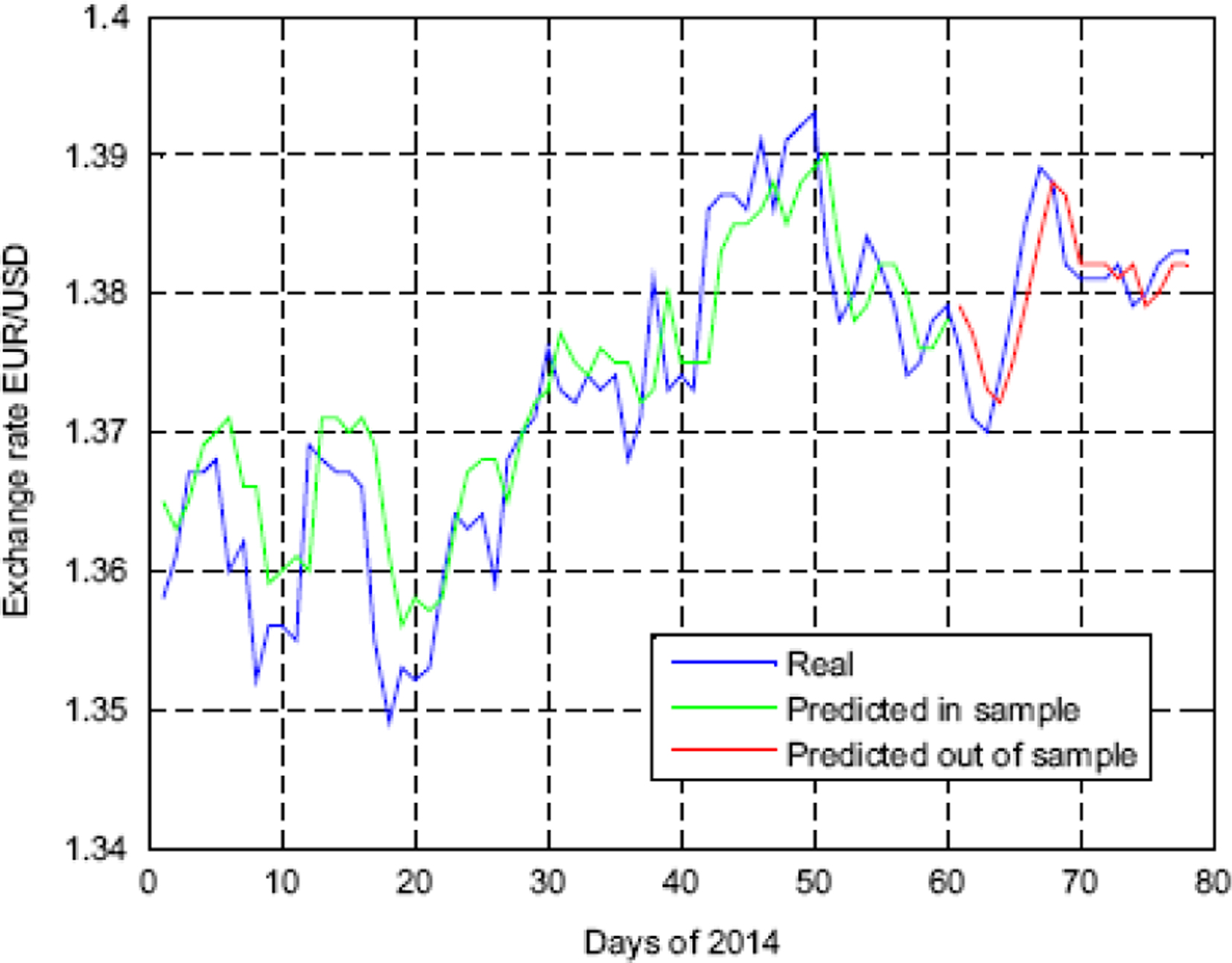

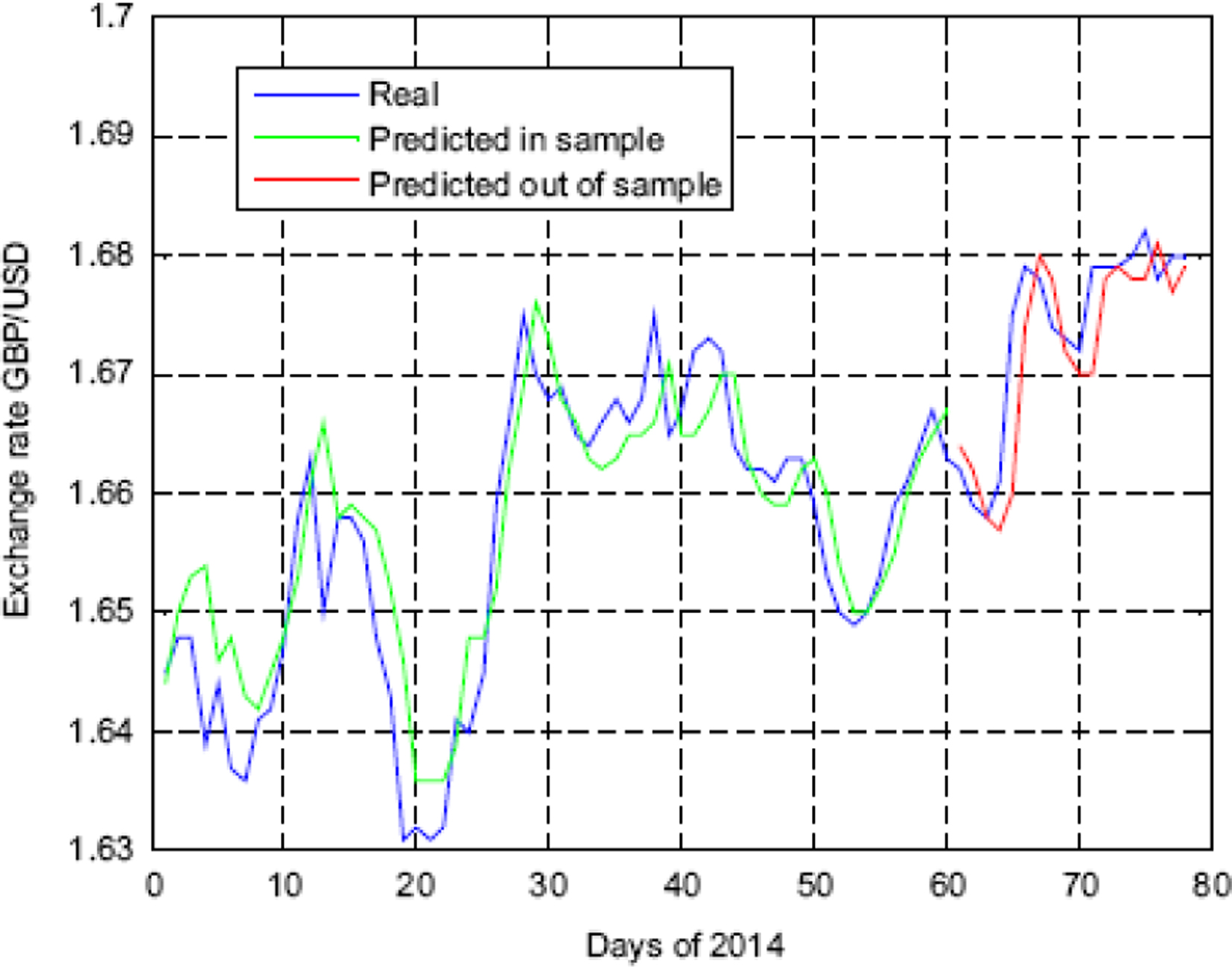

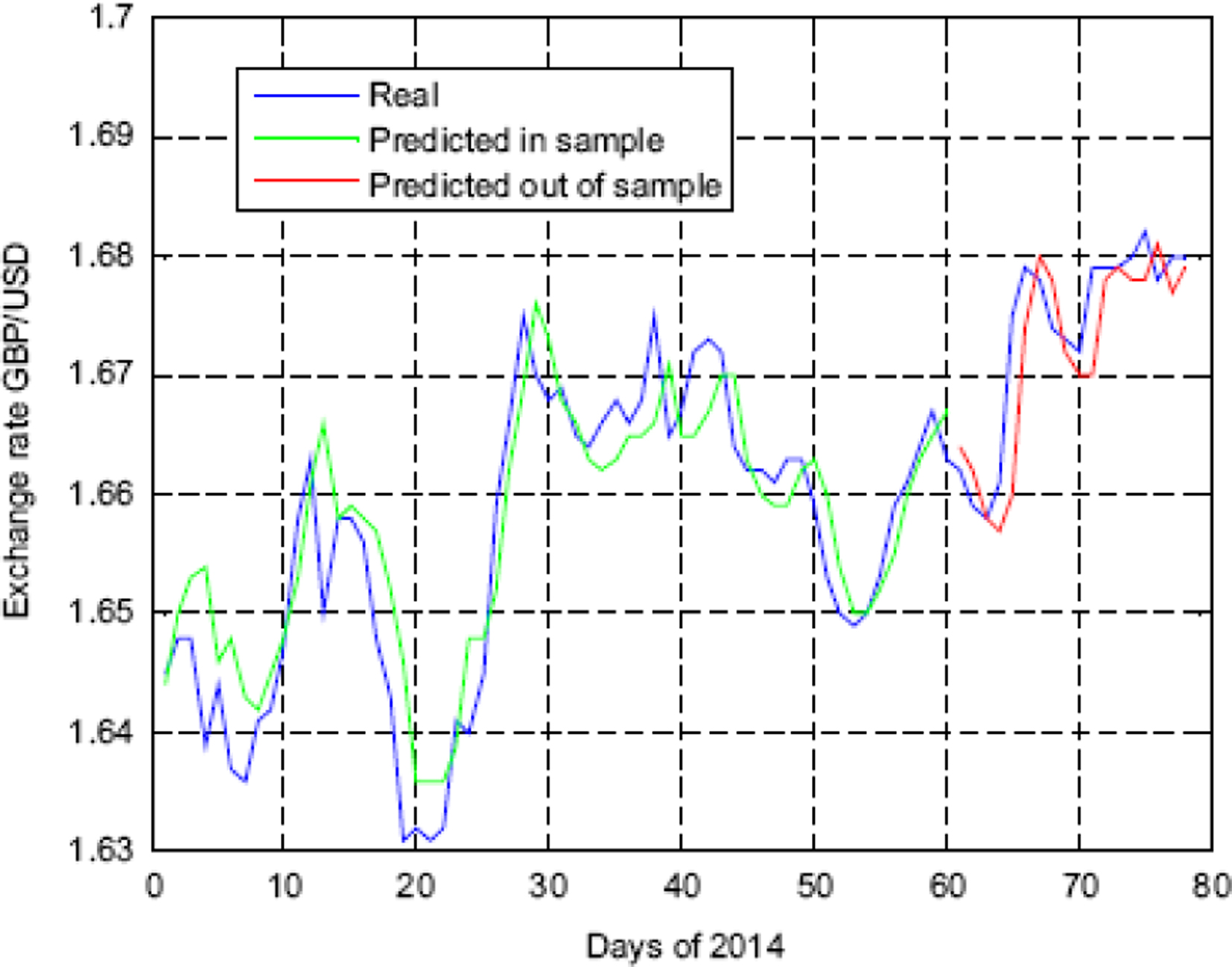

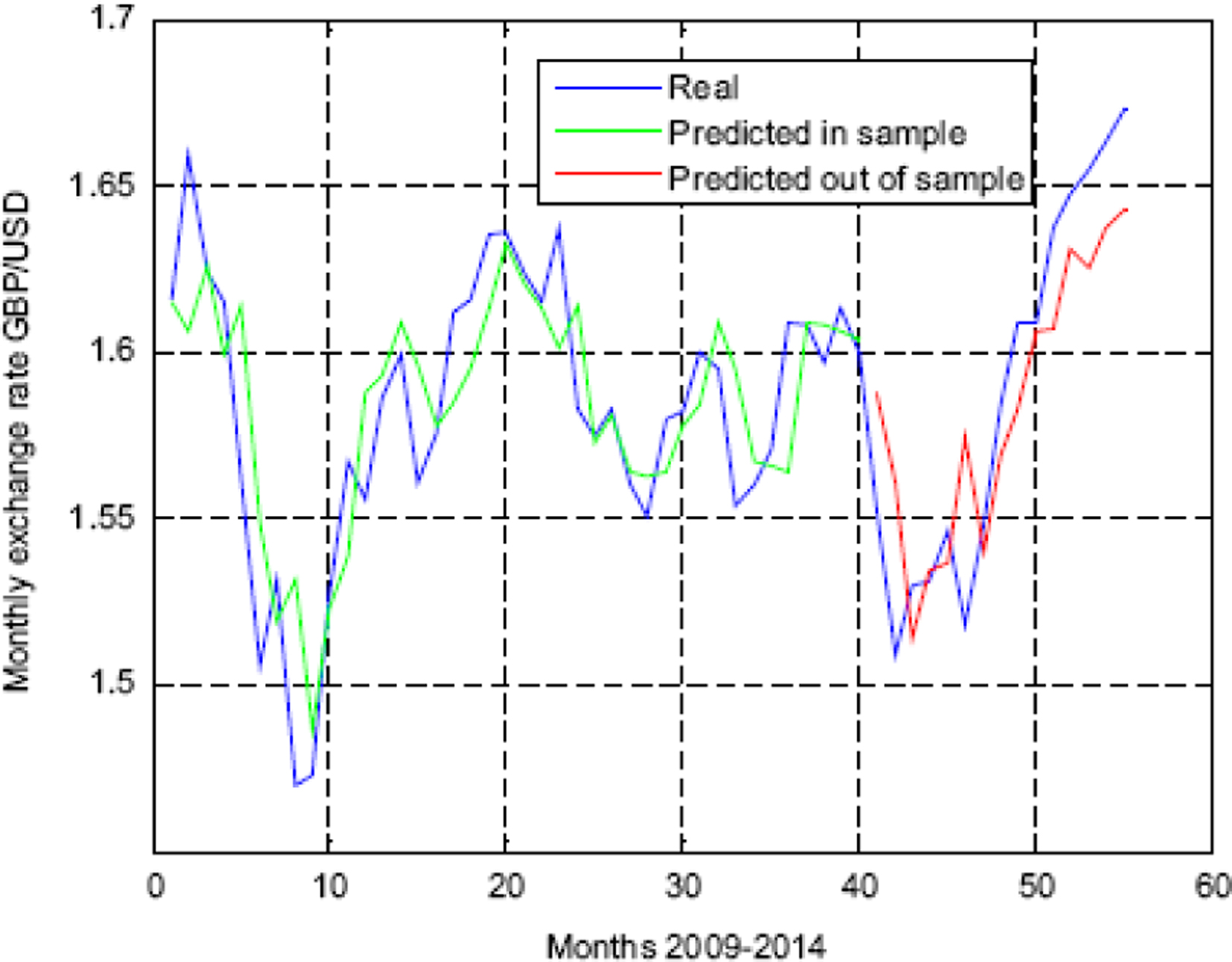

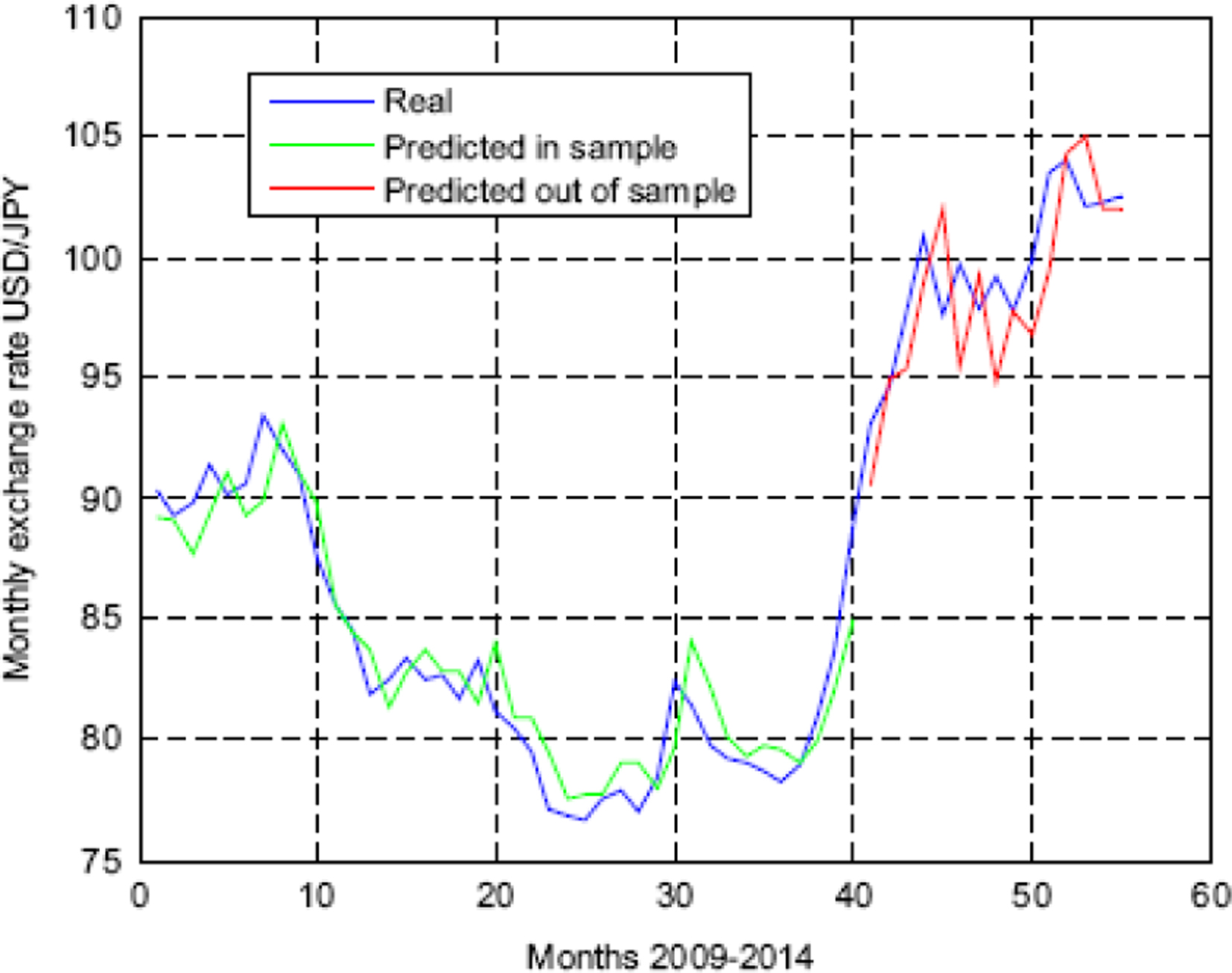

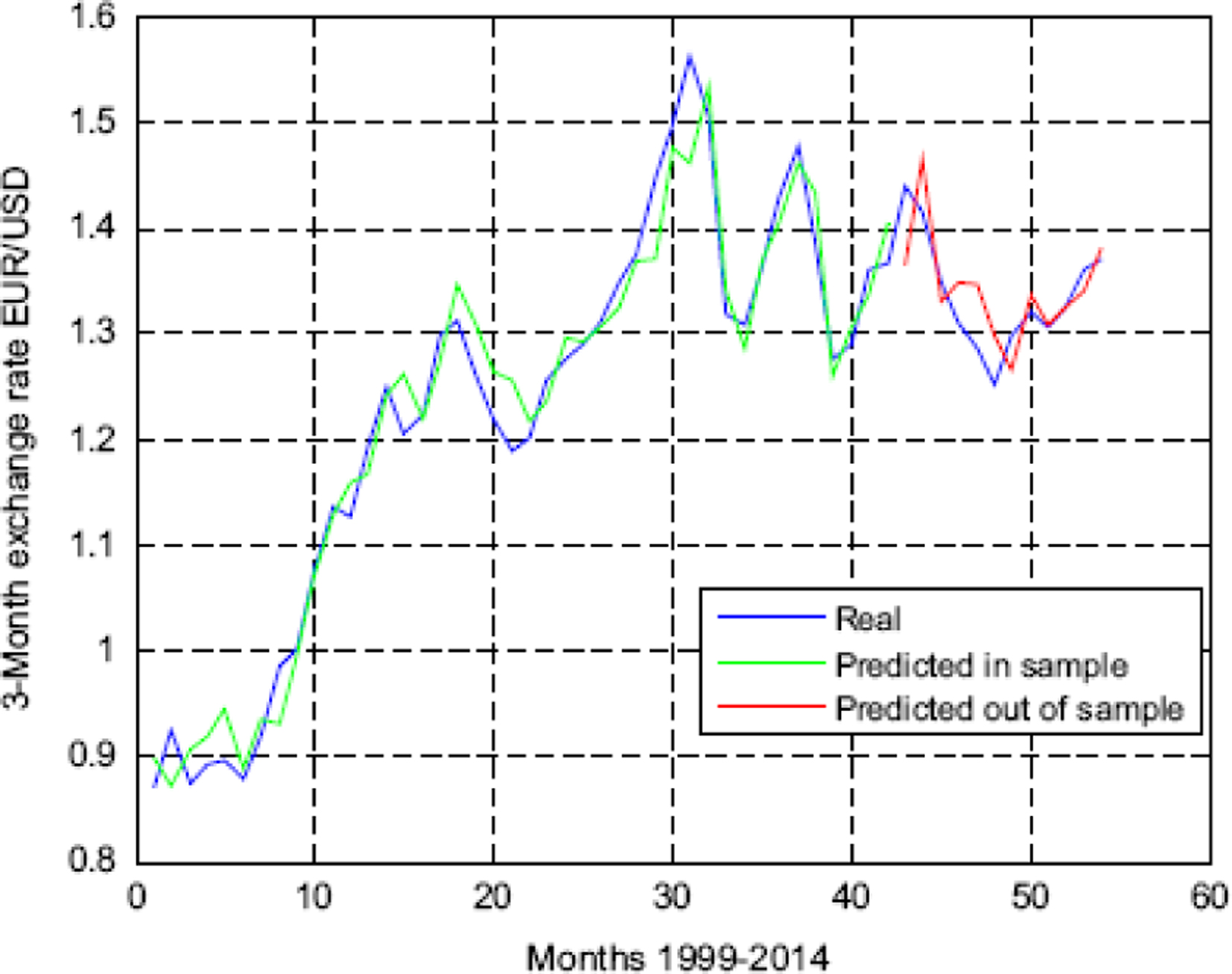

Table 1 shows the daily, monthly and quarterly error rate of different exchange rates using MLP with back propagation learning. The prediction results with daily, monthly and quarterly step are depicted in Figs 12–20 for EUR/USD, GBP/USD and USD/JPY. These results show that the short-term prediction method using MLP provides good accuracy of the prediction.

Prediction of exchange rate EUR/USD with daily step.

Prediction of exchange rate GPB/USD with daily step.

Prediction of exchange rate JPY/USD with daily step.

Prediction of exchange rate EUR/USD with monthly step.

Prediction of exchange rate GPB/USD with monthly step.

Prediction of exchange rate JPY/USD with monthly step.

Prediction of exchange rate EUR/USD with quarterly step.

Prediction of exchange rate GBP/USD with quarterly step.

Prediction of exchange rate JPY/USD with quarterly step.

Tables 2 and 3 show the error rate of GBP/ USD and JPY/USD exchange rates using MLP with Bayesian learning. The experimental results shows that predicting exchange rates using MLP with Bayesian learning is producing better results than BPNN model.

Performance of integrated model

In this Section we have compared the proposed integrated model to simple ARIMA and simple MLP and RBF in terms of error level with RMSE. Table 4 show the error rate of different exchange rates using Integrated model. The results from the Table 4 show that the integrated model works better than the other single models both in terms of error level and directional status.

Performance of multistage RBFN model

In this Section, four main currency exchange rates are used to test the proposed RBF neural network ensemble forecasting model. Tables 5 and 6 show the error rate of different exchange rates using Multi stage RBFN model. The low NMSE does not necessarily mean that there is a high hit ratio for foreign exchange movement direction prediction. Thus, the Dstat comparison is necessary for business practitioners. Focusing on Dstat of Table 6, it is not hard to find that the proposed RBF neural network ensemble forecasting model outperforms the other ensemble models and the single RBF model.

NMSE of multistage RBF with different mode

NMSE of multistage RBF with different mode

In this Section the authors have proposed two efficient low complexity neural network based forecasting models for exchange rate prediction. The first model is very simple with one layer and single neuron but with nonlinearly mapped input features. The second model consists of two stage FLANNs. The output of the first stage undergoes nonlinear expansion and then fed to the second FLANN for predicting the exchange rate. Computer simulation study of both the models reveal that each of them offer better prediction performance compared to the LMS model. However, out of the FLANN and CFLANN models, the later offers superior prediction performance in all cases. Table 7 shows the error rate of different exchange rates using FLANN and CFLANN model.

Accuracy in FLANN and CFLANN

Accuracy in FLANN and CFLANN

Here, we have investigated whether NN models can offer improvements in terms of forecasting accuracy over RW models and extensively used ARIMA and GARCH models. Given that most rate data contain nonlinear structures, one would expect NN models to be able to exploit the nonlinear structures to provide better forecasts as NN models can approximate any continuous function to a good degree of accuracy without the imposition of the assumptions regarding the form of nonlinearity. The experimental analysys, indicate that NN models can provide better forecasts than RW models and traditional models, such as, ARIMA and GARCH models. The better performance of NN models is likely to have stemmed from the fact that they are nonlinear models, that can exploit the nonlinearity in the exchange rate data without the imposition of assumptions about the form of nonlinearity. Tables 8 and 9 show the daily exchange rate predictions of Australian dollar and British pound using linear and non-linear models. It has been observed from the experimental analysis that neural network (NN) models have lessor error rates than the other linear models.

Out-of-sample forecasts of Australian dollar

Out-of-sample forecasts of Australian dollar

Out-of-sample forecasts of British pound

Result analysis table

Finally in Table 10 we have summarised the whole experimental study on exchange rate prediction based on different types of statistical and biologically inspired algorithms.

Conclusions and future work

From the above empirical study we have analyzed that in MLP if daily exchange rate data are taken to train the network then error rate will be less in comparison to exchange rate data taken monthly and quarterly basis to train the network. MLP with Bayesian learning give better result than MLP with back propagation learning. Combination of RBFN gives more accurate result than single RBFN network. The performance of integrated model with combination of RBFN, MLP, ARIMA is better than individual model. To avoid complexity and for better result FLANN can be used to predict the exchange rates of different countries. Combination of FLANN which is called CFLANN gives more accurate result than individual FLANN. From this intensive empirical study we have concluded that no single model in this study consistently outperforms the others. The forecast capability of a particular model depends on the exchange rate of interest and the forecast horizon. Given the uncertainty in selecting a model, the combined forecasts seem to have an edge over the others and in general have relatively smaller RMSE ratios and higher percentage in predicting the direction of changes correctly. In spite of the attractiveness of combining forecasts, it should be stressed that forecasting exchange rate movement is still a daunting task. The forecasts of exchange rates from any of these models should be used with caution. For the forecast-performance comparison of the models, the results suggest that in future we can involve exchange rates of different developed, under developed countries and better optimised biologically inspired algorithms to increase the prediction accuracy. We can perform fine tuning of the parameters by using biologically inspired optimization algorithms to get better performance. This will open a broad research domain for the researchers. Time series forecasting is a fast growing area of research and as such provides many scope for future works. One of them is the Combining Approach, i.e. to combine a number of different and dissimilar methods to improve forecast accuracy. A lot of works have been done towards this direction and various combining methods have been proposed in literature. Together with other analysis in time series forecasting, we have thought to find an efficient combining model, in future if possible. With the aim of further studies in time series modeling and forecasting, here we conclude the present paper.

Footnotes

Conflict of interest

We do not have any conflict of interest with other authors.