Abstract

Considering that the current cost control algorithm has the problems of poor control effect and high cost of manpower and material resources in enterprise cost control, a target cost control algorithm based on Hypercycle model is proposed. By analyzing the relationship between capital, price, technology and target cost control, this paper analyzes the influence of uncertain factors on target cost, and constructs a cost control super cycle model to realize enterprise cost control. Examples show that the algorithm can effectively improve the cost effect of enterprises, and has the practicability of reducing enterprise costs and improving enterprise profits.

Introduction

Since China’s accession to the WTO, China’s economy has developed rapidly, and various enterprises are also facing opportunities and challenges. In order to stand out among many enterprises, we need to improve our own economic benefits, increase enterprise profits and improve market competitiveness [1, 2]. The main problem is to strengthen the cost management of enterprises, reduce manufacturing costs, increase enterprise profits, implement the whole process cost control and obtain the best economic benefits on the basis of ensuring products. This is also an important way to improve the economic efficiency of enterprises [3, 4]. If an enterprise wants to implement cost control, it needs to organize all departments to cooperate to form an organic whole of overall cost control. The tasks and objectives of cost control should be clear to realize the overall cost control of the enterprise [5, 6]. As an important part of modern enterprise management, it has attracted the attention of enterprise producers and managers. Especially in industrial enterprises, cost control mainly lies in the cost control of raw materials, depreciation of fixed assets and management expenses. By reducing the product cost of industrial enterprises, on the basis of ensuring product quality, save enterprise costs, improve enterprise profits and achieve the purpose of improving enterprise economic benefits [7, 8, 9].

At present, with the increasingly fierce competition among enterprises, the reduction of business costs and the increase of business profits have attracted the attention of enterprises. Relevant scholars began to study the target cost control of enterprises, produced some mature theories and applied them [10]. Li et al. proposed a new variable cost control algorithm under the hospital accounting system, which uses the double control method to double control the supply cost and internal transfer price, but this method is not perfect in the implementation process and has poor effect on the target cost control of the enterprise [11]. Wang and Yang proposed an algorithm for establishing the evaluation index system of whole process cost control of coal mine materials [12]. Build different grade indicators around the coal mine material quota management, procurement, inventory, supply and other links, and form a cost control evaluation index system. This method can effectively realize cost control, but ignores the analysis process of cost control, which leads to the control effect is not obvious. Li and Ren proposed a cost control algorithm for coal enterprises based on value tree model. Based on the analysis of the cost components and influencing factors of existing coal enterprises, the value tree model of coal enterprises is established [13]. According to the focus of enterprise cost control, cost control is carried out from the aspects of development, recovery and outsourcing. However, in the analysis and control of cost control factors, the operation process is too complex and consumes a lot of manpower and material resources, Resulting in poor cost control effect.

In order to solve the problem that the existing methods consume a lot of human and material resources and have poor control effect in cost control, this study proposes an enterprise target cost control algorithm based on hyper cycle model, analyzes the factors affecting cost control, determines the impact of capital factors on cost, and constructs the hyper cycle model of cost control. Enterprise cost control is realized through super cycle model. The experimental results show that the proposed method can accurately analyze the factors affecting the effect of cost control, realize the effective control of enterprise target cost, reduce enterprise cost and improve enterprise profit.

Enterprise target cost control algorithm based on hypercycle model

Hypercycle theory and cost control

Hypercycle theory describes the interaction between substances. In the hypercycle structure, each replication unit can not only copy itself, but also induce the emergence of the next medium. The cost control needs to obtain its operation mode and role through practical operation, investigation and analysis. The specific cost control process is shown in Fig. 1.

Response cycle model for cost control.

As seen from Fig. 1, the first choice needs to determine the cost, then calculate the actual expenditure, find out the differences for comparison and analysis, then improve the corresponding cost control steps, and finally determine the cost criteria to form a cycle.

Hypercycle is a complex reaction cycle composed of multiple reaction cycles. Its application not only reduces the cost, but also improves the production efficiency of the enterprise. To build the enterprise target cost control hypercycle model, it needs to determine the control factors affecting the cost. As the basic of enterprise production, excess capital is the key factor to control the target cost [14, 15]. Currency is the main form of funds. Its function is circulation to realize the value of living materials produced by the company. This factor is objective and it does not change with the number of [16].

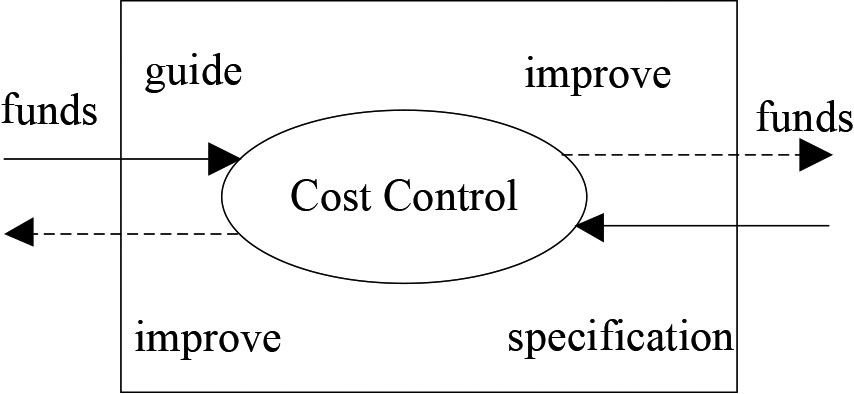

Specifically, following: Funds have an important role in cost control. In turn, cost control also has an impact on the funds of the enterprise. By guiding, improving and regulating funds, we can play the purpose of cost control, the cost can be effectively controlled, strengthen the utilization of funds, get higher returns, and the two interact and influence each other. Funding is also the key to achieving target cost control. In the sense, the nature of cost control depends on the funding factors. The function of capital factors is mainly reflected in its guidance and specification, through the guidance of cost control, optimize the allocation of enterprise resources, to ensure that the interaction between capital and cost reflects the interaction between the hypercycle and causal transformation, this hypercycle mode can make up for the lack of previous cost control methods.

Funds have an important role in cost control. In turn, cost control also has an impact on the funds of the enterprise. By guiding, improving and regulating funds, we can play the purpose of cost control, the cost can be effectively controlled, strengthen the utilization of funds, get higher returns, and the two interact and influence each other, as shown in Fig. 2.

The cycle model of funds factor and the target cost control.

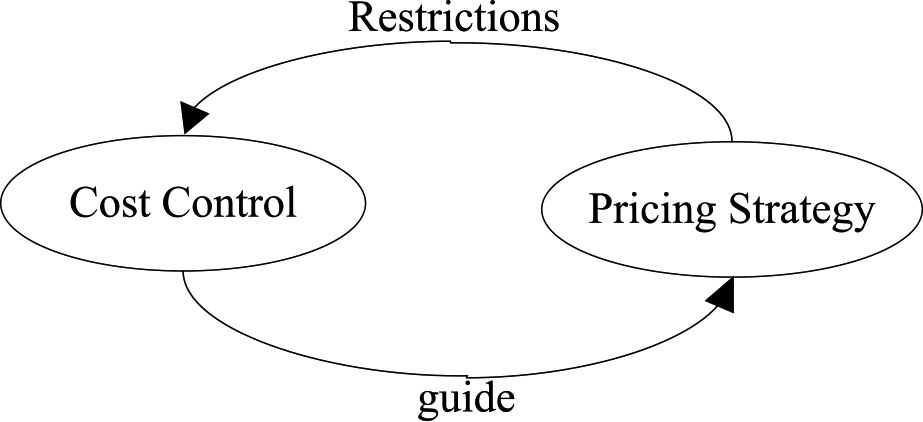

Generally, the price factor and the target cost control are interdependent. If the enterprise cost is determined, the lowest price of the product is obtained, and the cost control is the prerequisite of the pricing strategy. If the cost control is appropriate, the determined price can realize the profit maximize. As the market condition changes, the pricing strategy will be adjusted accordingly. The pricing strategy refers to a system that can quickly know the change of the external environment, and the system can be used to adapt to the environmental change [17]. In short, proper control over the target cost can promote the pricing strategy of the company, in turn, the pricing strategy will promote the company continued to grow, occupy a favorable market position, and close cooperation with partners, thus contributing to the company operating more and more successful. The relationship between the target cost control and the service pricing strategy is as shown in Fig. 3.

Catalytic cyclical response of target cost control and service pricing strategy.

The main contents of the impact of technical factors on the target cost control are: the method of controlling cost and the system supported by learning and information. Technical factors are the inherent conditions for target cost control. Its main functions are as follows: 1) As a technical support for the control of target costs, technological advances are conducive to the sharing and exchange of information and can share good experiences and practices with each other; 2) Technology innovation and development of the target cost control can enhance the cost control skills, which is the advanced technology that companies must introduce and master, as shown in Fig. 4.

Cycle model of technical environment and cost control.

As the process of target cost control is extremely complicated, and many factors affect each other, so managers should accurately grasp the linkages. If the external environment changes dramatically, the above three factors will change the target cost control effect, as shown in Fig. 5.

Macro model of cost control hypercycle.

As shown in Fig. 5, the motivation of target cost control is to pursue as many profits as possible. Capital, pricing and technology promote the control of target cost. The state of capital can determine the quality and quantity of cost control, pricing strategy is a role in promoting cost control, can promote the rapid and healthy development of cost control. Technical strategy can improve the management level of enterprises, and produce more products on the premise of ensuring quality, which shows the vital role of external environment in cost control. If the external environment changes dramatically, the main sign of its learning level of adaptation is whether enterprises are able to respond appropriately to the changing external environment [18]. The efficiency and effectiveness of cost control depends on the fund factor, while the driver is pricing. We will ensure the sustainability and stability of cost control and create favorable conditions for the development of enterprises. Corporate decision makers play an important role in cost control [19]. Fund quota refers to the optimal allocation of resources of a certain amount of funds, in accordance with the target cost control according to the allocation plan. The capital factor is the soft limitation of the target cost control, which ensures the company’s inventory.

Activity-based costing is the guarantee of the hypercycle model of target cost control. In addition, funds, technology, price, knowledge reserve and other factors are integrated into the activity-based costing model, as shown in Fig. 6.

Microcosmic model of cost control hypercycle.

The main objective of cost control of enterprises based on hypercycle model is to determine the criteria of cost control, calculate the actual cost, compare the difference, and evaluate the performance. Details are as follows:

Product demand estimation. By analyzing the market situation of the enterprise product demand and the function of the similar external conditions, the demand expectation of the enterprise in the future is estimated to help the company to carry out the planning and control effectively. Set service goals. To assess the results and grasp the status of the enterprise, all the factors will be comprehensively considered get the category and number of services provided by the enterprise and set up the service targets. Determine the operating cost control guidelines. For an enterprise, the company’s goals cover both the service and cost goals. Determining the effectiveness of the company’s decisions requires both goals and to find a single point that can balance both goals. In addition, there are two types of assignments: value-added activities and non-value-added activities. Therefore, enterprises should formulate guidelines for value-added activities and non-value-added activities separately. Calculation and comparison of actual production cost and difference. Cost control is based on activity to compare the differences and is affected by various factors. In a certain period of time, the actual cost of each activity often deviates from the expected cost, and the difference between the two is the cost difference [20]. The calculation of the actual cost is the basis for comparing the differences. The operating cost method is used to calculate the actual operating costs incurred by the logistics company. The actual costs are then compared with the estimated costs to analyze the causes of the differences and improve the cost control according to the differences. If the manager can control the cost, it is called the controllable cost, otherwise it is called the uncontrollable cost.

Enterprises can calculate the cost data based on the difference of operating cost, correct the operation process pertinently, improve the whole operation chain, and finally enhance the core competence of the enterprise in order to win the fierce market competition. The cost model runs through the entire control, its main function is to reflect the cost of product operations and to provide the basis for determining the cost control criteria and the comparative cost difference. Product operating costs include three categories: direct costs, indirect costs and fixed costs [21, 22]. Direct costs are positively related to the number of products, assuming a logistics contract contains

In the above formula,

In the above formula,

As described in Section 2.1, the target cost control of enterprises based on the hyper cycle model is to look at the cost control of the enterprise as a cycle system, in which the unit represents the executor and the promoter of the loop. Set the effect of unit A on unit B is considered as a force, and the effect of unit B to unit A is considered as a reaction force. Where:

The actual output

In the above formula,

When

Reduce the actual output of the next round to save costs. This situation often occurs when the actual input to unit A is much greater than expected. The actual output of unit A at this time is:

Increase the actual output of the next round to encourage each other to further improve. This is often the case when unit A wishes to obtain more satisfactory input. At this point, the actual output of unit

When

Reduce the actual output of the next round to force each other to take improvement measures. This situation usually occurs when unit B has a dependency on unit A, and unit A takes this measure to impose sanctions. In this case, the actual output expression of unit A has the same meaning as Eq. (5).

Increase the next round of actual output to encourage each other to take improvement measures. This is exactly the opposite of what was described above. At this point, the expression formula of the actual output of unit A is the same as that of Eq. (6).

Thus, the actual output function of unit A is obtained:

In the formula, when unit A wants to increase the next round of actual output, take a positive sign, when unit A wants to reduce the next round of actual output, take a minus sign.

Based on the above analysis, we can obtain four basic functions of cost control:

In order to facilitate the study, the analysis of the action of unit A to unit B is taken as an example, and it is assumed that the external disturbance

In non-cycle state, unit A will be output according to the preset reference value

Assuming the role of process

With the relative value that is:

That is, in non-cyclic state, a little change in the action of unit A on B in the acyclic state will all be accepted by unit B. In the actual operation of the enterprise, it shows the oversight and runaway of the errors in the business, and the errors will be delivered to the downstream units as they are. This will not only affect the output quality of the unit A, but also affect the cooperation with unit B [24].

In the cycle state, according to the Eq. (12) to Eq. (14), the conversion is obtained:

Then:

By algebraically calculating Eqs (15) and (16), we get:

Similarly, the reaction process of unit B and unit A can also be analyzed. Comparing Eq. (15) with Eq. (17), it can be concluded that under the control of enterprise cost, the influence of uncertain factors in unit A on unit B is only

The factors influencing external disturbances in the process of enterprise cost control are analyzed. In the non-cyclic state, the same unit A as an example for analysis. Similar to the previous section, in this case, the relationship between the functions is:

Then:

In the cycle state, according to Eq. (8) to Eq. (11) and Eq. (18), we can get:

It also exists that:

From the comparison between Eqs (19) and (21), it can be seen that the change of action value caused by external disturbances is directly proportional to the magnitude of the disturbances, while in the cycle state, the error caused by the disturbances is

In order to prove the validity and practicability of the algorithm proposed in this paper, an experiment was carried out. The processor of the experiment was htel (R) Pelltium (R) M processor 1.50 GHz, memory was King Max DDR400 1 G, motherboard was A3N, hard disk was 80 G, through the experiment, the results obtained are described below.

In order to realize the goal cost control of the enterprise, the cost of the enterprise needs to be analyzed. To ensure the accuracy of the control, the objective cost of the enterprise is predicted by the proposed algorithm and the algorithms proposed in reference [11, 12]. The cost of enterprise can be divided into direct cost, indirect cost and fixed cost. The fixed cost represents a fixed value. To realize the enterprise cost forecast, the direct cost and indirect cost of the production of the enterprise need to be predicted separately. The results of the experiment are shown in the Fig. 7.

Forecasting results of enterprise target cost in different algorithms.

In Fig. 7, a represents the prediction cost of the algorithm proposed in reference [11], b represents the prediction cost of the algorithm proposed in this study, c represents the actual cost, and d represents the prediction cost of the algorithm proposed in reference [12]. It can be seen from the figure that in the direct cost prediction results, the prediction cost of the algorithm proposed in reference [11] and the prediction cost of the algorithm proposed in reference [11] are far from the actual cost results; The predicted cost calculated using the algorithm proposed in this study is the algorithm closest to the actual cost. The indirect cost prediction result is the same as the direct cost prediction result. The prediction cost of the algorithm proposed in reference [11] and the prediction cost of the algorithm proposed in reference [11] are far from the actual cost result; The predicted cost calculated using the algorithm proposed in this study is the algorithm closest to the actual cost. It shows that the target cost prediction result of the proposed algorithm is more accurate, provides a reliable data guarantee for target cost control, and improves the effect of enterprise cost control.

In order to prove the practical application effect of the proposed method, taking A company as an example, the difficulty and focus of the target cost control of A company lies in the cost control of single ship, a representative ship product was selected for target cost control analysis. Company A has a large number of ship products, its main product positioning is multi-purpose workboat, multi-turn tugboat, STS Ro-Ro passenger ship, fireboat and live fish carrier. Through the analysis, it is found that the 127-meter Ro-Ro passenger ship takes up a large proportion of the orders of new ships undertaken by company A and is also the main profit source of company A. Therefore, the target cost control analysis of 127-meter ro-ro passenger ship is selected as the research object, the effect of cost control is intuitively demonstrated, and its contribution to the total profit of company A is analyzed.

In formulating the target selling price of 127-meter ro-ro passenger ship, Company A takes the competitor analysis method as the pricing method according to the situation of the enterprise, the price of the previous order and the bargaining power of the customer. When formulating the market price, Company A made full reference to the price when constructing the same or similar marine products in the same industry. According to the above principles, company A formulated a 127-meter ro-ro passenger ship priced at 1 million yuan in 2014.

Company A set the target profit and also considered the single ship profit level of the competitors in the same industry, if the target profit is too high, the customer may turn to its competitors, if the target profit is too low, it is difficult for company A to control their cost through the target cost method, and also violates the intention of the company to adopt the target cost method. Based on the above principles, the expected gross margin of 127-meter ro-ro passenger ship drawn up by Company A in 2016 is 10%.

In formulating the target cost of 127-meter ro-ro passenger ship, Company A fully considered a series of situations such as competitor’s situation, customer’s preference and satisfaction and market demand, finally adopted the profit-cost analysis and forecast method. There are three main steps in the calculation of the target cost. The specific process is as follows:

1) Calculation of comprehensive cost of capital ratio:

The capital cost ratio refers to the ratio between the company’s capital expenditure and the effective financing amount, which is usually expressed as a percentage [25, 26]. In 2016, the total long-term capital of company A was 30 million yuan, including long-term loans of 3 million yuan, long-term bonds of 2 million yuan, common shares of 3 million yuan, and retained surplus of 3 million yuan, accounting for 10%. Assuming that the individual capital cost rates of company A are 7%, 6%, 7% and 7% respectively, in the financing practice of the company, the comprehensive capital cost rate is:

2) Calculation of income tax payable:

The income tax rate of company A is 25%, so its income tax payable in 2014 is:

3) Calculate the special costs:

The special fees account for about 4.24% of the total production cost of a 127-meter ro-ro passenger ship. Therefore, the target special costs of company A in 2016 was:

According to the calculation of the above three steps, the target cost of 127 meters ro-ro passenger ship for company A can be drawn:

In 2015, the cost of 127-meter ro-ro passenger ship for company A is 90 million yuan. In order to control the cost within 82.88 million yuan to achieve the control effect of the target cost method, the cost should to be reduced is:

By using the algorithm proposed in this paper, target cost of 127-meter ro-ro passenger ship was controlled and the following control effects were obtained.

As of the end of 2016, the effectiveness of the cost control of a single 127-meter ro-ro passenger ship for Company A was summarized and analyzed. The implementation of cost reduction in various departments is shown in Table 1.

Cost reduction in various departments

Profit level comparison of company A before and after the target cost control.

Table 1 shows that through the calculation of the method in this paper, in the target cost control of 127 meter rail passenger ship of company a, the total planned cost is 7.58 million yuan, the actual cost reduction is about 7.67 million yuan, and the completion rate of cost control is about 101%, indicating that in the practical application of the cost control method proposed in this paper, all departments of the enterprise can complete the task of cost control, technology, the industrial manufacturing cost reduction of the material procurement and shipbuilding. Department has been significantly reduced, the set cost reduction goal has been achieved, and remarkable control effect has been achieved.

The cost saved by cost control activities is directly included in the profit and loss statement of the company. Through the control of the target cost method of a single 127 m rail passenger ship, the profit contribution of company a can be analyzed. After adopting this algorithm to control the target cost, the profitability of company a has been significantly improved. Compared with the return on net assets (ROE), profit margin on sales (ROS) and profit cost ratio (RPCE) in 2015, it has increased to 3.28%, 3.85% and 4.23% respectively. The overall profit level has increased. The specific trend is shown in Fig. 8.

As can be seen from Fig. 8, compared with 2015, the return on net assets, sales profit margin and profit cost ratio increased by 80.22%, 79.91% and 80% respectively, indicating that the proposed target cost control method has carried out significant cost control, significantly improved profitability and achieved the purpose of improving the economic benefits of the enterprise. Through the above experimental analysis, we can see that the algorithm proposed in this paper can accurately calculate the target cost of the enterprise, realize the target cost control of each department, reduce the product cost of industrial enterprises, and increase the profit of the enterprise on the basis of ensuring the product quality. Therefore, the algorithm has a good control effect.

In the cost control process, if the calculation process is too complicated, it is prone to error, and the cost control process will take a long time. The calculation process of target cost control is realized using the method proposed, and the experimental results are shown in Fig. 9.

Comparison of target cost control calculation process in different algorithms.

In Fig. 9, a represents the calculation process of the target cost control proposed in reference [12], b represents the calculation process of the target cost control proposed in reference [13], and c represents the calculation process of the target cost control proposed herein. As can be seen from Fig. 8, with the increase of business departments, the calculation process of target cost control gradually increases. When the number of business departments increases to 7, the calculation process of target cost control proposed in reference [12] increases the most, and the calculation times reach 20; b refers to the calculation process of target cost control proposed in reference [13], the increase range is general, and the number of calculations is 16; The calculation process of the proposed target cost control algorithm increases the least, and the calculation times are only 14 times. This shows that the algorithm proposed in this paper has the least calculation times and the calculation process is relatively simple.

By using this method to control the cost of company a, all departments of the enterprise can complete the task of cost control, achieve the set cost reduction goal, reduce the manufacturing cost of industrial enterprises, significantly improve the profitability of company a and realize the purpose of improving the economic benefits of the enterprise. And the calculation process of cost control is relatively simple.

At present, the competition among enterprises is fierce. In order to improve the economic benefits and competitiveness of enterprises, the enterprise target cost control algorithm based on Hypercycle model proposed in this paper can effectively control the enterprise cost.

This method can effectively reduce the product cost of industrial enterprises. On the basis of ensuring product quality, it is conducive to produce more products by saving cost, improve enterprise profits and realize the purpose of improving enterprise economic benefits. The proposed enterprise target cost control algorithm based on Hypercycle model can well solve the problems of more human and material resources and poor control effect of the original method in controlling enterprise cost. The calculation process is relatively simple, the calculation effect is accurate, and the enterprise cost can be accurately predicted. This method is used for multi department cost control of industrial manufacturing target cost of company A. through a period of control, each department has achieved the set cost reduction goal, achieved remarkable control effect, and the overall profit level of company a has increased, which proves the effectiveness and practicability of this method in practical application.