Abstract

Intuitionistic fuzzy sets and soft sets describe the different types of uncertainty. Their fusion gets intuitionistic fuzzy soft sets, forms a more powerful mathematical tool for uncertainty description and further enlarges the scope of applications. This is more advantageous to solve decision-making problems. This paper proposes an intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis. According to the known evaluation information, this method describes stochastic decision-making problems as intuitionistic fuzzy soft sets. Firstly, a score function is defined and intuitionistic fuzzy numbers are converted the values of this score function. Secondly, the prospect decision matrix is given by utilizing the prospect value formula. Thirdly, the weight of each parameter is determined through grey relational analysis. Fourthly, the comprehensive prospect value of each scheme is gotten on the basis of the weight of each parameter. Fifthly, the optimal choice is obtained according to the comprehensive prospect values. Sixthly, an algorithm is presented. Finally, two applied examples are employed to illustrate the effectiveness and feasibility of this method.

Keywords

Introduction

Problems in many fields involve data which may contain uncertainties. Uncertainties may be dealt with using a wide range of existing theories such as probability theory, fuzzy set theory [31], interval mathematics and rough set theory [25]. But all these theories have their own difficulties. To overcome these difficulties, Molodtsov [22] proposed a completely new method, which is called soft set theory, for dealing with uncertainties.

Recently there has been a rapid growth of interest in soft set theory and its applications. Maji [24] put forward intuitionistic fuzzy soft sets. Aktas et al. [2] initiated soft groups. Feng et al. [12] established the connection between soft sets and semirings. Jiang et al. [14] extended soft sets with description logics. Li et al. [17, 18] considered roughness of fuzzy soft sets and obtained the relationship among soft sets, soft rough sets and topologies. Li et al. [21] studied parameter reductions of soft coverings.

Soft set theory is very different from traditional mathematics tools in describing and setting objects. We can describe approximately objects by means of soft sets. There is no limiting conditions when objects are described. Researchers can choose parameters and their forms according to needs. The fact that setting parameters is non-binding greatly simplifies decision-making process and then we can do effective decisions under the circumstances of less information.

Maji et al. [23] first applied soft sets to solve decision-making problem with the help of rough method. Cağman et al. [6, 7] presented soft matrix theory and uni-int decision-making method. Basu et al. [3] introduced the mean potentiality method. Li et al. [20] gave an application of fuzzy soft sets in decision-making based on grey relational analysis and Dempster-Shafer theory of evidence in medical diagnosis. Li et al. [19] investigated decision-making based on intuitionistic fuzzy soft sets. Xie et al. [30] proposed a method to fuzzy soft sets in decision making based on grey relational analysis and MYCIN certainty factor.

Because of the uncertainty of decision environment, decision makers face a variety of states. Assuming that the probability of occurrence under each state is given. In this way, there are stochastic decision-making problems. But the above methods can not be used to solve stochastic decision-making problems. Then it is necessary to pay attention to this issue.

The study of stochastic decision-making problems usually bases on expected utility theory. This theory assumes that decision makers are fully rational, but there are unexplained phenomena such as Allias paradox and Ellsberg paradox. In 1979, the Nobel prize winner in economics Kahneman and Tversky [15] proposed prospect theory. This theory replaces the utility function and the subjective probability with the value function and the decision weight, respectively, and reflects and describes the actual process of decision-making [15, 28]. Then this theory improves expected utility theory. Therefore, prospect theory has been applied to stochastic decision-making problems. For example, Li et al. [16] gave intuitionistic fuzzy stochastic multi-criteria decision-making methods based on prospect theory; Salminen et al. [27] proposed a decision model for solving the discrete multiple issues group secretary using a linear prospect theory-type value function to represent a decision maker’s preference structure.

The purpose of this paper is to investigate stochastic decision making based on intuitionistic fuzzy soft sets by combining prospect theory and grey relational analysis.

The remaining part of this paper is organized as follows. In Section 2, we recall some concepts about bout about soft sets, intuitionistic fuzzy soft sets, prospect theory and grey relational analysis. In Section 3, we give an intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis and present its algorithm. In Section 4, two applied examples are employed to illustrate the effectiveness and feasibility of this method. In Section 5, we conclude this paper.

Preliminaries

In this section, we briefly recall some basic concepts about soft sets, intuitionistic fuzzy soft sets, prospect theory and grey relational analysis.

Throughout this paper, U denotes an initial universe, E* denotes the set of all possible parameters, 2 U denotes the family of all subsets of U, IF (U) denotes the family of all intuitionistic fuzzy sets of U. We only consider the case where U and E are both nonempty finite sets.

Soft sets

In other words, a soft set over U is a parameterized family of subsets of the universe U. For e ∈ E, F (e) may be considered as the set of e-approximate elements of the soft set (F, E).

F (a1) = {h1}, F (a2) = {h2, h3, h5}, F (a3) = {h4}, F (a4) = {h1, h2, h3}, F (a5) = {h4, h5}, F (a6) = {h1, h2, h3}, F (a7) = {h4, h5}.

Then the soft set (F, E) can be described as the following Table 1. If h i ∈ F (a j ), then h ij = 1; otherwise h ij = 0, where h ij are the entries in Table 1.

Tabular representation of the soft set (F, E)

Tabular representation of the soft set (F, E)

(F, A) is called a soft subset of (G, B), if A ⊆ B and F (e) = G (e) for each e ∈ A. We denote it by (F, A) is called a soft super set of (G, B), if

Obviously,

(H, C) is called the intersection of (F, A) and (G, B), if C = A ∩ B and H (e) = F (e) ∩ G (e) for each e ∈ C. We denote it by (H, C) is called the union of (F, A) and (G, B), if C = A ∪ B and

We denote it by (H, C) is called the bi-intersection of (F, A) and (G, B), if C = A × B and H (a, b) = F (a) ∩ G (b) for each a ∈ A and b ∈ B. We denote it by (f, A) ⋀ (G, B) = (H, C). (H, C) is called the bi-union of (F, A) and (G, B), if C = A × B and H (a, b) = F (a) ∪ G (b) for each a ∈ A and b ∈ B. We denote it by (f, A) ⋁ (G, B) = (H, C).

μ A (x) and ν A (x) are called the membership degree and non-membership degree that the element x belongs to the set A.

In other words, an intuitionistic fuzzy soft set over U is a parameterized family of intuitionistic fuzzy sets in U. For any e ∈ E, F (e) is referred as the set of e-approximate elements of (F, E) and can be written as:

For any x ∈ U and e ∈ E, (μF(e) (x), νF(e) (x)) is called e-intuitionistic fuzzy number of x; μF(e) (x) and νF(e) (x) are called the membership degree and non-membership degree that the element x belongs to the set F (e), respectively.

If x is viewed as a scheme (or object), then μF(e) (x) and νF(e) (x) may represent the degree that the parameter e supports and opposes the scheme (or object) x, respectively.

Denote U = {x1, x2, …, x m } and E = {e1, e2, …, e n }. Put

a ij = (μF(e j ) (x i ), νF(e) (x)) (i = 1, 2, ⋯, m, j = 1, 2, ⋯, n).

Then (a ij ) m×n is called the matrix induced by (F, E).

Then (F, E) is an intuitionistic fuzzy soft set over U, which describes “the attractiveness of the cars” to the purchasers. For example,

Then the characteristic of the car x1 under the parameter e3 is (0.5, 0.4). Since 0.5 and 0.4 are the membership degree and non-membership degree that the element x1 belongs to the set F (e3), respectively, 0.5 and 0.4 may represent the degree that the performance e3 supports and opposes the car x1, respectively. In other words, the car x1 is good performance on the degree of 0.5 and it is poor performance on the degree of 0.4.

The matrix induced by (F, E) is

Prospect theory

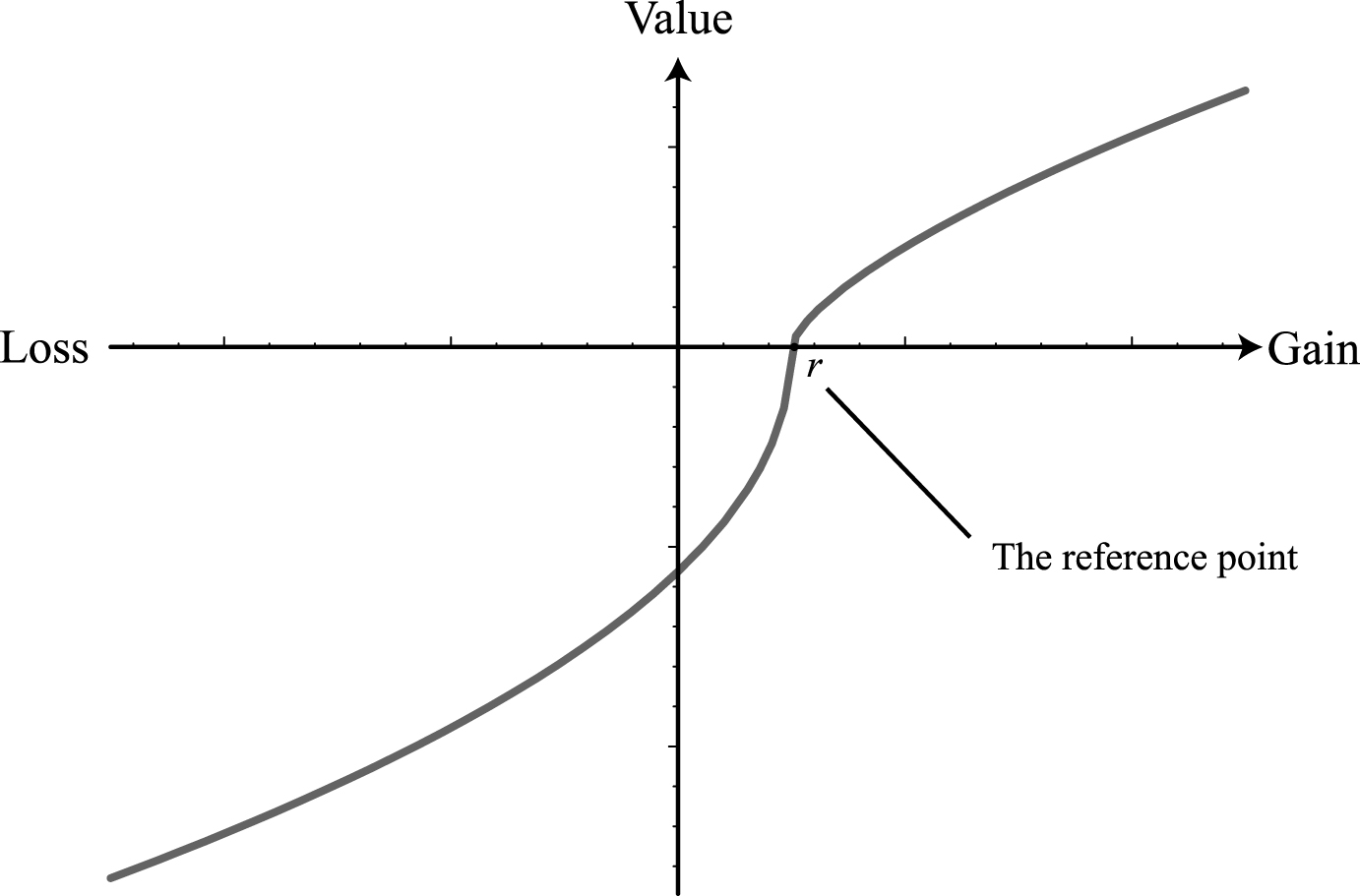

Prospect theory mainly considers the value function and the decision weight. From the point of view of cognitive psychology, the value function and the decision weight proposed by Tversky and Kahneman [15] is conducted to replace the utility function and subjective probabilities, respectively. This theory implies three important characteristics: (1) reference dependence, (2) diminishing sensitivity and (3) loss aversion. Reference dependence refers to the fact human perception ability is built on relative change of value, also called the endowment effect or the status quo bias. People tend to maintain the current state to save on trading costs. Diminishing sensitivity refers to the phenomenon that utility decreases when income increases. Loss aversion suggests human impressions of losses are deeper than those towards gains.

Value function. Data source: Kahneman and Tversky [29].

Prospect theory distinguishes two phases in the selection process: an early phase of editing and a subsequent phase of evaluation. In the editing phase,outcomes are expressed by means of gains and losses from a reference point. In the evaluation phase, the edited prospects are evaluated by a value function and a weighting function, and the prospect of highest value is selected. The value function is defined on deviations from the reference point. The value function is defined in the form of a power law according to the following expression:

α, β < 1 yields an s-shape value function; α, β > 1 produces an inverse s-shape value function. Estimating λ is a very complicated job because there is no agreed-upon definition of loss aversion.

In general, r = 0. The values α, β and λ are determined through experiments. For simplifying the computation, this study takes the values as follows: α = β = 0.88, λ = 2.25.

The value function v (x) has the following characteristics: The meaning of v (x) is the gain or loss relative to the reference point r, and it is the relative level of wealth, not the absolute of wealth in traditional theory. v (x) is a s-shaped curve, which is a convex function above the reference point r and is a concave function under the reference point r. s-shaped curve means that the behavior subject tends to risk aversion in the face of gain and tends to risk preferences in the face of loss. v (x) has the asymmetry, namely, when the slope of the loss part of v (x) is greater than the slope of the gain part of v (x), the sensitive degree of the behavior subject to the amount of loss is higher than that of the same amount of gain.

Decision weight function is defined as follows:

The decision weight function π (p) has the following features: π (p) is an increasing function and π (0) =0, π (1) =1. π (0) =0 expresses that the impossible event will not be chosen in decision-making and then its weight is 0; π (1) =1 shows that the certain event will be chosen in decision-making and then its weight is 1. Subadditivity: in the low probability region, π (p) is a sub-additive function, namely, π (rp) > rπ (p) when 0 < r < 1. The high probability event is underestimated and the low probability event is overestimated in decision-making, namely, when p is very small, π (p) > p; when p is very big,π (p) < p. Subcertainty: the sum of the decision weights of the probability of complementary events, namely, π (p) + π (1 - p) <1.

Let X

j

= (x

j

(1), x

j

(2), …, x

j

(m)) be the system behavior sequence (j = 0, 1, …, n) where X0 is the signature sequence, X1, X2, ⋯, X

n

are the factor sequences. Denote

Then |x

j

(i) - x0 (i) | is called the difference information between x

j

(i) and x0 (i); r (x0 (i), x

j

(i)) (for short, r

ij

) is called the grey mean relational degree between x

j

(i) and x0 (i); ρ is called the distinguishing coefficient.

The distinguishing coefficient ρ is an important factor that affects the correlation analysis resolution and the value distribution of the grey mean relational degrees r ij . The purpose of ρ is to weaken the Max value’s affect when this value is so large that its purpose is lost and to improve the difference between the grey mean relational degrees r ij .

According to the experience, we pick ρ = 0.5 to obtain strong distinguishing effectiveness, which can more accurately reflect the related degree between x j (i) and x0 (i).

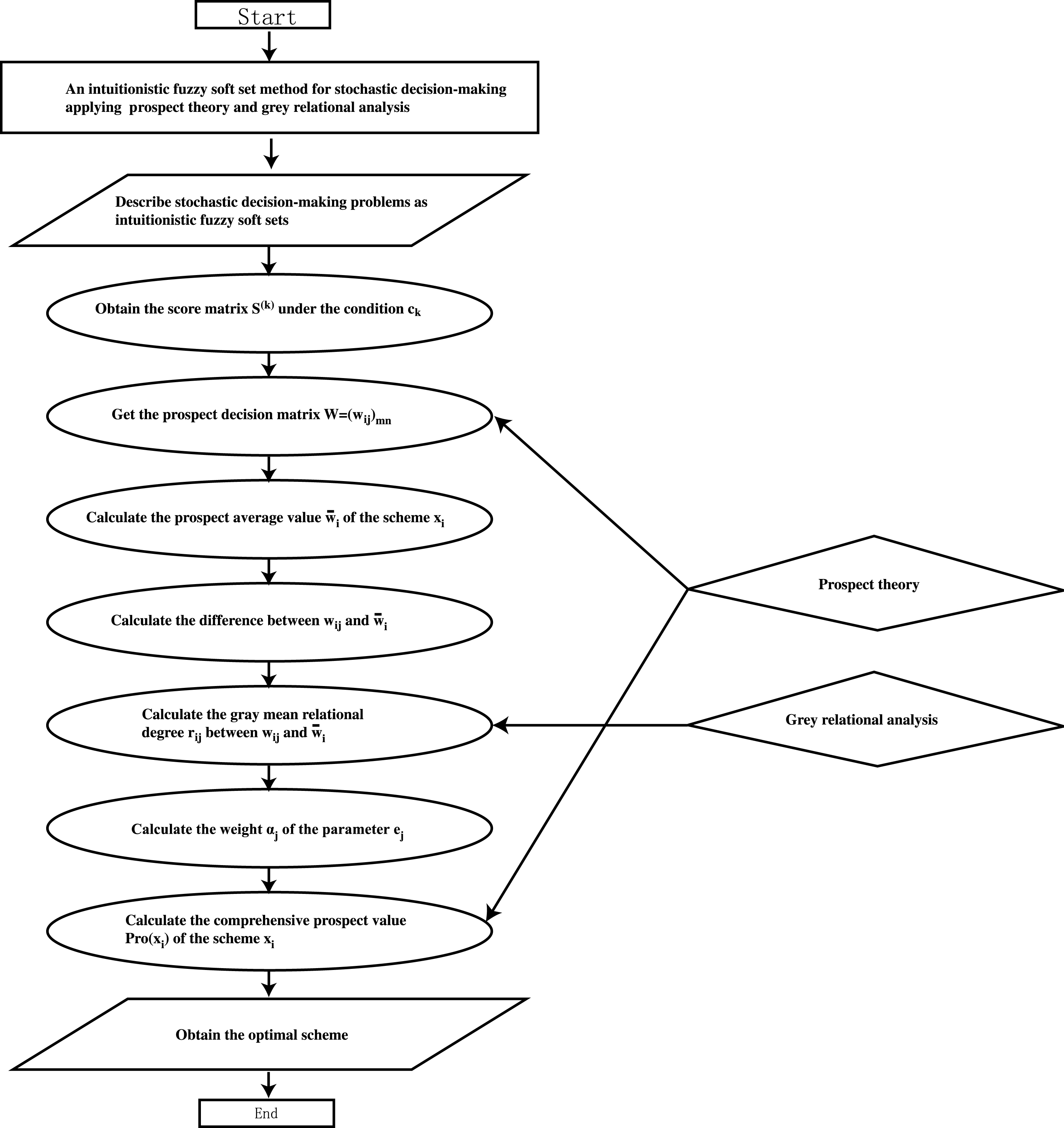

An intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis

Now we give an intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis. This method is effective and practical for stochastic decision-making problems in which the parameter’s wights are incomplete and the indices value of schemes are in the form of intuitionistic fuzzy numbers.

In the following, we consider a stochastic decision-making problem concerned with m mutually exclusive schemes x1, x2, ⋯, x

m

, n evaluation parameters (or indexes) e1, e2, ⋯, e

n

and l states s1, s2, ⋯, s

l

where the probability of the state s

k

is p

k

. Assuming that

Put

For each k (1 ≤ k ≤ l), define F(k) : A → IF (U) by

Then (F(k), E) is an intuitionistic fuzzy soft set over U under the state s k .

Put

Then

In general, σ = 2.25, α = β = 0.88, γ = 0.61.

W = (w ij ) m×n is called the prospect decision matrix.

Based on the prospect decision matrix W, we have the following results: The prospect average value of the scheme x

i

is

The difference between w

ij

and The grey mean relational degree between w

ij

and The weight of the parameter e

j

is

The comprehensive prospect value of the scheme x

i

is

Based on the above analysis, the detailed step-wise procedure as an algorithm is given as follows:

Input: an intuitionistic fuzzy soft set (F, E).

Output: the optimal decision-making result.

Step 1. We can get the score matrix

Step 2. Through the score matrix S(k) induced by (F(k), E) and the prospect value formula

Step 3. Calculate the prospect average value

Step 4. Calculate the difference ▵w

ij

between w

ij

and

Step 5. Calculate the grey mean relational degree between w

ij

and

Step 6. Calculate the weight α

j

of the parameter e

j

by

Step 7. Calculate the comprehensive prospect value Pro (x

i

) of the scheme x

i

by

Step 8. Obtain the optimal choice of the schemes. If Pro (x k ) = max {Pro (x i ) |1 ≤ i ≤ m}, then the optimal choice of the schemes is the scheme x k .

Flow chart of an intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis.

In this section, we apply our method to solve decision-making problems through two applied examples.

Aviation industry belongs to a high-tech industry and is an important embodiment of the national comprehensive strength. In order to promote the overall development level of aviation industry, in addition to increasing support for independent innovation and breakthrough a number of core technology, key technology and cutting-edge technology, we also need to purchase foreign major aviation equipment of high technology as much as possible.

In the process of the investment projects of major aviation equipment procurement, there are many aspects of impacting on procurement projects. For example, equipment needs to solve the complex requirements of aviation technology, but also needs that equipment is in the state of stable, normal, efficient operation in the whole life cycle of the equipment. So the investments of the projects of major aviation equipment procurement is of high uncertainty. But if these investments can eventually succeed, then we often can get considerable investment income. It is visible that the evaluation and selection of investment projects are very important in the process of the investment projects of major aviation equipment procurement.

The following example attempt to solve the optimal choice problem of the investment projects of major aviation equipment procurement by applying our method.

Due to the state in the future is uncertain, we suppose that there are three states: (1) the state of international environmental will be stable, this state is denoted by s1; (2) the surrounding local will occur small-scale war, this state is denoted by s2, (3) the surrounding local will outbreak large-scale war, this state is denoted by s3. And we suppose that the probabilities of these three states are 0.7, 0.2, 0.1, respectively.

According to the known evaluation information, the intuitionistic fuzzy soft set (F(k), E) under the state s

k

can be obtained (k = 1, 2, 3). Assume that the decision matrix induced by (F(k), E) is

Below we choose the optimal investment project by using the method of this paper. The steps are summarized as follows: Calculate the score matrix Through calculation, we can get the prospect decision matrix W = (w

ij

) 5×4 as follows:

Calculate the prospect average value of each investment project as follows:

Calculate the difference ▵w

ij

between w

ij

and Calculate the grey mean relational degree r

ij

between w

ij

and Calculate the weight of each parameter as follows: α1 = 0.2358, α2 = 0.2462, α3 = 0.2532, α4 = 0.2647; Calculate the comprehensive prospect value of each investment project as follows: Pro (x1) =0.4381, Pro (x2) =0.3556, Pro (x3) = 0.2864, Pro (x4) = 0.4069, Pro (x5) = 0.3162; The final rang order is Pro (x1) > Pro (x4) > Pro (x2) > Pro (x5) > Pro (x3). The optimal choice of the investment projects is the investment project x1 according to the maximization principle.

Due to the state in the future is uncertain, suppose that there are the following three states: (1) the economy will be in a stable state, this state is denoted by s1; (2) the social will occur small scale financial crisis, this state is denoted by s2, (3) the social will occur large scale financial crisis, this state is denoted by s3. And suppose that the probabilities of three states are 0.6, 0.3, 0.1, respectively.

According to the known evaluation information, Mr. X obtain the intuitionistic fuzzy soft set (F(k), E) under the state s

k

(k = 1, 2, 3). Assume that the matrix induced by (F(k), E) under the state s

k

is

Below we obtain the optimal choice of the houses by using the method of this paper. The steps are summarized as follows: Calculate the score matrix

Get the prospect decision matrix W = (w

ij

) m×n as follows:

Calculate the prospect average value

Calculate the difference ▵w

ij

between w

ij

and Calculate the grey mean relational degree r

ij

between w

ij

and Calculate the weight α

j

of the parameter e

j

as follows: α1 = 0.1775, α2 = 0.2127, α3 = 0.1989, α4 = 0.2055, α5 = 0.2064; Calculate the comprehensive prospect value Pro (x

i

) of the house x

i

as follows: Pro (x1) =0.3054, Pro (x2) =0.3858, Pro (x3) =0.3409, Pro (x4) =0.2365, Pro (x5) =0.2732, Pro (x6) =0.3473; The final rang order is Pro (x2) > Pro (x6) > Pro (x3) > Pro (x1) > Pro (x5) > Pro (x4); The house x2 is the optimal choice of the houses according to the maximization principle.

Conclusions

This paper has proposed an intuitionistic fuzzy soft set method for stochastic decision-making applying prospect theory and grey relational analysis. This method provides a new tool for stochastic decision-making problems and widen the application range of prospect theory and grey relational analysis. In future work, we will extend this method to neutrosophic soft sets.

Footnotes

Acknowledgments

The authors would like to thank the editors and the anonymous reviewers for their valuable suggestions which have helped immensely in improving the quality of this paper. This work is supported by the National Natural Science Foundation of China (11461005), the Natural Science Foundation of Guangxi (2016GXNSFAA380045, 2016GXNSFAA380282, 2016GXNSFAA380286), Key Laboratory of Quantitative Economics, Key Discipline of Guantitative Economics in Guangxi University of Finance and Economics and the Research Institute of Guangxi Economic Forecasting and Decision-Making (2016ZDKT02, 2016ZDKT06), Research Project on Developing the Professional Master Degree of Applied Statistics in Guangxi University of Finance and Economics in 2016 (2016TJYB06), Research Project of the Collaborative Innovation Center for Integration of Marine and Terrestrial Economies and Construction of Marine Silk Road (16&YB07), Key Laboratory of Optimization Control and Engineering Calculation in Department of Guangxi Education, and Special Funds of Guangxi Distinguished Experts Construction Engineering.