Abstract

After several decades of reform and opening up, the economy has developed rapidly, and the development speed of the real economy has slowed down gradually. In order to obtain sufficient funds in a short period of time to meet the production and operation needs, many enterprises carry out financial capital management, which has a certain impact on the profitability of enterprises. In addition, in order to study the impact of financial capital management on profitability, in this paper, relevant data of some non-financial listed companies from 2007 to 2013 in China was selected, and the multiple linear regression analysis was carried out. Through the analysis, it can be seen that the proportion of financial assets and the return on net assets shows a significant negative correlation, which means that there is a negative correlation between the financial capital operation scale of non-financial listed companies and the profitability of listed companies. Based on the empirical analysis, in this paper, the capital management and structure optimization proposal for improving enterprise profitability were proposed; which is of great significance to the development of enterprises and finance in China.

Introduction

With the expansion of Britain exiting from the EU and American trade protection thinking, “globalization” has shown signs of retrogression. In recent years, the global economic development has also entered a relatively slow period. In 2015, China’s GDP growth rate fell below 7%, compared with GDP growth rate in 2014, it’s 6.9%. In 2016, the GDP growth rate was further slowed down, which was 6.7%. China’s economic growth rate continues to slow down, and the domestic excess capacity and backward production capacity is gradually being adjusted and eliminated, then, the enterprise structure optimization and upgrading becomes an important strategic policy to support China’s economic development [1]. In order to ensure the normal operation of enterprises, many enterprises apply the capital for the purchase of financial assets, and then, the financial capital operation is conducted. At present, the financial investment has become an important way for many listed companies to achieve profitability. But the development of enterprises should still be based on the expansion of production scale, only to continue to expand the size of the main business, the stable and long-term profits can be truly achieved [2]. In addition, the global financial crisis in 2008 sounded the alarm for the listed company’s financial investment behavior again. And furthermore, the blind investment in financial markets is prone to financial bubbles. It is an urgent problem to be solved about how to achieve the profitability of financial investment on the basis of ensuring the main business of listed companies. China’s financial market development starts late, even after several decades of rapid development stage, it still has many imperfections [3].

With the continuous development of the economy, on the one hand, the financial industry needs to be gradually expanded, and a short period of profit can be used to make up for business’ deficiencies, such as long main business cycle, poor profitability. At the same time, it’s necessary to fully recognize many deficiencies in the capital market in China [4]. The process of enterprise development is essentially a capital game, which requires to rationally use the limited capital at all stages of development, and then achieve the maximum capital and corporate value [5]. Thereupon, it is necessary to carry out in-depth study on the financial capital operation of non-financial listed companies and analyze their impact on the profitability of the company. Then, the fundamental for the enterprise to survive and develop is to achieve the profitability of enterprises, and constantly enhance their profitability. Through the empirical analysis of non-financial listed companies in China, the significance of theoretical research can be provided for the operation of financial capital of listed companies in China. On the other hand, the financial risks of enterprises can be reduced through research, so as to realize the economic benefits of enterprise financial capital operation, which is beneficial to the long-term and healthy development of non-financial listed companies, and there’s certain realistic meaning.

The non-financial listed companies and the financial capital management’s relevant theory

Non-financial listed companies

Listed companies have large scale, high technology content and other characteristics, which have a certain indicator role for other companies in the same industry. While the non-financial listed companies include all other listed companies except insurance and finance, so the business scope involved is very wide, and the quantity is too many, covering power, transportation, fisheries, manufacturing and other industries [6]. It can be seen that non-financial listed companies play a very important role in the development of social economy, which are the important indicators for measuring the national comprehensive strength [7]. Then, the listed companies can carry out their own financing in the open market, in addition to conduct the expansion of production scale and production management, the financing funds can be used to achieve the growth of the scale of the enterprise, at the same time, the company can demonstrate its own enhancement and development in an identity of a listed company, which shows the strength of the enterprise, thereby increasing the credibility and profit growth of the firm [8]. Financial listed companies are mainly to obtain profits through the purchase of financial assets, while the non-financial listed companies are quite different, which are to exclude the listed companies except the finance and insurance industry, their main business development is dependent on the development of the real economy. According to the industry classification standards, the specific industry distribution of China’s non-financial listed companies in 2013 was classified, as shown in Table 1:

The distribution of non-financial listed companies in China

The distribution of non-financial listed companies in China

As can be seen from Table 1, among the non-financial listed companies, the largest number is transportation, social services and warehousing, the proportion of these three accounts for more than 73%. The manufacturing industry accounts for a very high proportion, which shows that China is still a manufacturing power, meanwhile, it also indicates that China’s manufacturing enterprises are gradually inclined to financial capital management [9]. Non-financial listed companies involve many industries, and they grow the company by depending on the development of the main industry. Then, the non-financial listed companies have a clear feature, that is, the product production cycle and the product’s added value are different, in addition, there are also some differences in profitability. When the pace of solid economic slows down, the non-financial listed companies will invest a lot of money into the purchase of financial products, so as to expect a higher profit, and achieve the short-term capital return [10].

Operating capital is also known as capital operation or capital management, which refers to the product management that isn’t completely out of the business, however, an enterprise’s product management has certain differences, furthermore, the premise of capital management is to meet the production and business needs of enterprises, so as to maximize the capital of enterprises, and secure the maximum profit through the investment of corporate capital [11]. The broad capital operation refers to that the enterprise optimizes the capital allocation, measures the finance, property rights, industry, etc., so as to make that the enterprise capital is effectively used. Then, in the narrow sense, the capital operation of the enterprise refers to that the enterprise optimizes the capital through the asset merger, reorganization and acquisition and so on, so that after the reorganization of property rights, the enterprise can obtain the development vitality, and promote the improvement of the business efficiency in the case of continuous improvement in operating efficiency. The main purpose of capital operation is to preserve and add value of capital. Through the reasonable capital investment, the optimization of capital structure can be realized, as well as the maximization of the enterprise value [12]. According to different forms, the operating capital can be divided into industrial capital, financial capital, equity capital and intangible capital operation such four categories.

In the process of analyzing the origins of the enterprise, Coase first proposed the concept of transaction costs, and this referred to the cost of the process of running the market. In order to be able to reduce the transaction costs in the market mechanisms as much as possible, the enterprise was born. In order to achieve long-term development, companies must take full account of transaction costs and reduce costs, thereby using lower transaction costs [13]. Then, in order to reduce costs, companies also need to optimize the allocation of their own capital, so that the same capital can get more benefits, and the maximization of the corporate value of listed companies is achieved [14]. However, the capital investment of enterprises is also different, at the same time of developing the industry, the investment in the financial industry can also be carried out, so as to achieve the short-term benefits and convenience, make the business managers save transaction costs, then, obtain benefits by relying on financial markets.

In the process of investing in stocks and claims, the modern portfolio theory puts forward the avoidance of its own risk, which is mainly to help investors to be able to measure the risk of investment system in the choice of stock or creditor’s right, thereby making their capital investment more reasonable, and obtaining greater returns [15]. The problem of enterprises’ capital operation is how to use the assets of enterprises, in the reorganization of capital management, both the business benefits and risks prevention need to be considered at the sane time, for the investment with uncertainty and harmfulness, it is likely to cause incalculable loss to the enterprise [16]. Therefore, in the process of capital operation, not only the individual investment needs to be carried out, the effective risk prevention measures and early warning mechanism should be established, so as to improve the management level of capital. In the context of the current economic development, due to the global economic slowdown and overcapacity, in order to better develop themselves, the non-financial listed companies need to adopt a diversified development strategy [17]. Then, in the context of today’s financial heat, most of the non-financial listed companies have also increased investment in the financial industry, which can disperse the singleness of corporate capital. Besides, the use of financial investment can get a higher return and achieve short-term liquidation [18]. However, in the process of the financial investment, the enterprises must develop a suitable business investment strategy in accordance with their own development situation and capital level, and pay attention to the capital regulation before event, in event and after event, as well as strengthening the financial risk prevention.

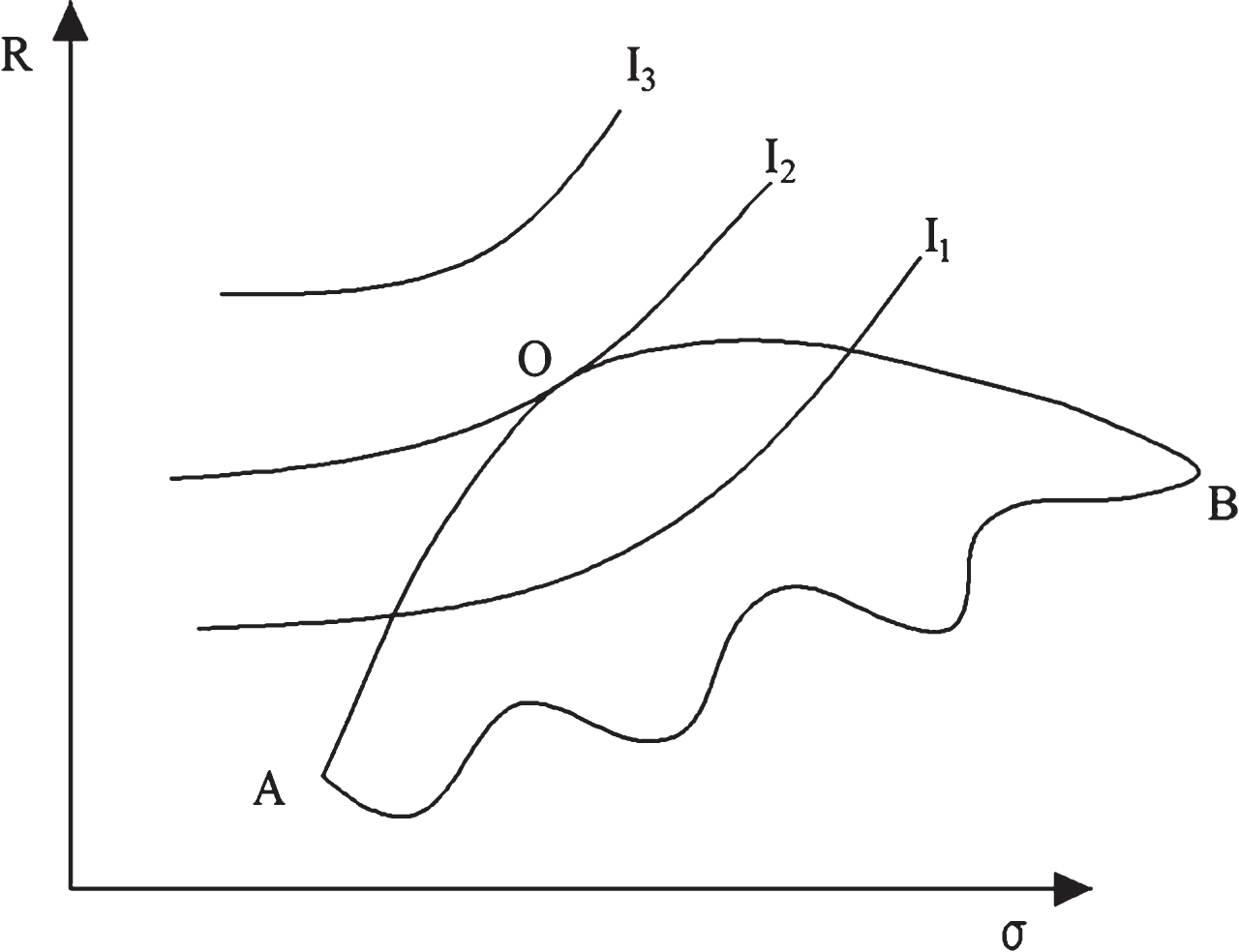

In 1952, Markowitz first put forward the portfolio theory. The theory mainly includes two aspects: the effective boundary model of the portfolio and the mean-variance analysis. In the stock market, the theory has proven its effectiveness. Furthermore, it is increasingly used in asset allocation and portfolio selection [19]. This theory has a good application in the optimal portfolio, as shown in Fig. 1, the upper convexity of the effective set and the lower convexity of the indifference curve are used to jointly determine the uniqueness of the optimal portfolio.

Modern portfolio optimization theory.

Assuming the portfolio income is r

p

, the incomes of the number i and the number j are respectively r

i

, r

j

, then, the overall portfolio risk is δ2 (r

p

), according to Markowitz optimization model, it can obtain:

Using the Markowitz optimization model, the risk of the portfolio can be controlled below the established risk level, so that the appropriate investment assets can be determined for the investor, the risks and expected returns during the asset holding period can be analyzed, the efficient set of the securities can be built, and the optimal portfolio can be determined [20].

Variable design

This study was mainly to study the impact of the financial capital operation of non-financial listed companies on the profitability, the data service center of Tai’an was used to obtain the relevant data, and then, the Shanghai and Shenzhen A-share listed companies were screened, the financial listed companies were put forward, and the data of the non-financial listed companies were used as research samples. The data from 2007 to 2013 were selected as a research sample, then, 4680 valid samples were supplied. According to this empirical analysis, the mutual influence relationship between the financial capital operation and corporate profitability was researched.

The indicators involved in the variable design were mainly profitability, financial capital management and control variables. The specific indicators are shown in Table 2. Among them, the profitability was the explanatory variable of this study, the return on net assets were used to measure, and then, the index was also a common index for reflecting the company’s profitability, which was often used as a key core of the DuPont analysis system. Therefore, the indicators were selected to measure the profitability, and the goal of enterprise development was to maximize the owner’s equity, so the indicators could also directly reflect the value-added capacity of corporate capital. The financial capital management index was the explanatory variable of this research. According to the existing research data, the financial capital management index specifically included the financial assets of the transaction, the net purchase of financial assets, the net assets available for sale, as well as the net amount of held-to-maturity investments. Among them, the transactional financial assets referred to the use of fair value to the dose, and its changes were recorded in the profit and loss of corporate financial assets, furthermore, it could be further divided into transactional financial assets and designated as the profit and loss of financial assets. The transactional financial assets in the industry often had a strong capital management. The four indicators were used to characterize the operation of financial capital, then, according to the numerical value of the proportion of financial assets held, the analysis was carried out, the greater the value was, the higher the degree of financial capital management was. Because there were many influencing factors of the non-financial listed company profitability, therefore, in order to better explain the data, the specific control variable indicators needed to be set. This time, a total of five indicators were selected as the control variables. The first was the size of the company scale, to a certain extent, this could reflect the number of the available resources of non-financial listed companies, and the companies with larger scale often had better popularity and development prospects, and they also generally had a strong profitability. At the same time, in the development process, the large companies generally needed more transaction costs, which would also affect the profitability of enterprises. Thus, in the selection of data, the listed companies in different industries were selected to carry out the data testing, and moreover, the analysis results were more convincing and representative. The capital structure referred to the proportion composition between debt capital and equity capital of enterprises, through the debt financing, the profitability of enterprises would be affected. Then, the operating profit margins directly reflected the profitability of the enterprise, and the higher the operating margin was, then, the better the profitability of the enterprise was. The risks of an enterprise included financial and operational risks, which reflected the overall risk of the business. And the integrated lever could also be used to evaluate the overall risk level of the enterprise, so as to study its impact on corporate profitability. In addition, the inventory turnover rate reflected the company’s inventory turnover rate, and under normal circumstances, the faster the turnover was, the stronger the profitability of enterprises was.

Variable definition and description

Variable definition and description

The SPSS software was used to conduct the descriptive statistical analysis and correlation analysis to various variables set before, and then, the regression analysis was used to carry out the empirical research to various data, so as to test the influence of the capital operation of non-financial listed companies on the profitability. In order to be able to test each hypothesis, firstly, an empirical model was built to achieve an intuitive data analysis. The specific model is as follows:

This model was to specifically describe the relationship between the variables X, Y, among them, X was explanatory variable, Y was the variable being explained, then, Y linear changed by X change. Among models, β0 was regression constant, β1 ⋯ β6 was regression coefficient, ɛ was the effect caused by other random factors, in general, it was shown as the unpredictable random error.

SPSS software was used to analyze all the variables of this time, so as to get all the variables and soil conditions. The results are shown in Table 3.

Descriptive statistics for all variables

It can be seen from Table 3 that the return on net assets of non-financial listed companies had a large absolute difference, which showed that their profitability and return on net assets were quite different; meanwhile, it also indicated that there was a big gap among the non-financial listed companies. In order to verify the validity of the selected variable, the variance expansion factor needed to be used to test the multiple collinearity indexes. When VIF > 100, it showed that there was a more serious multi-collinearity; when 10 < VIF ≤ 100, it indicated that there was no a strong multi-collinearity; when 0 ≤ VIF ≤ 100, there was no multi-collinearity. The results of multi-collinearity tests using the model are shown in Table 4.

Multiple collinearity test results

Through Table 3, it can be seen that the tolerance calculated by the six indicators was greater than 0.1, VIF maximum value was only 1.110, all VIF values were less than 10, which showed that there was no multi-linearity between the various variables, and then, it fully illustrated that the constructed model was suitable for the corresponding correlation analysis and regression analysis.

According to the analysis of 4680 sample data, the Pearson correlation coefficient between the variables can be obtained. The analysis results are shown in Table 5. Through Table 5, it can be seen that there was a positive correlation between the rate of return on net assets of the enterprise and the scale of the listed company, the operating profit margin and the turnover rate of the stock, while there was a negative correlation among the index of return on net assets and capital structure as well as the comprehensive leverage. The proportion of financial assets held, the size of the company, the operating margin, the capital structure and the inventory turnover were significant above the 0.01 level, however, the maximum value was only 0.05, which showed that their correlation was not highly correlated. Then, there was a significant negative correlation between the proportion of financial assets held and the size of the company. According to further analysis, it can be seen that the small-scale companies could only obtain capital through smaller channels, but the listed companies in non-financial sectors were generally to get the profits through a long cycle of the main industry, whereupon these smaller companies would put some of the capital into the financial market, so as to hope to get some capital in a short time to meet the main production and business, on the other hand, this was also because of the awareness of risk management of listed companies.

Pearson correlation coefficients of each variable

Pearson correlation coefficients of each variable

In order to further analyze and explain the effect of financial capital management on the profitability of non-financial listed companies, the model in the formula (3) was used to study, the financial capital management index was used as the explanatory variable, and then, the return on net assets was regarded as the explanatory variable, and through other factors influence, the regression analysis of the model was carried out to the 4680 sample data. From the analysis results, it can be seen that the negative correlation coefficient, determination coefficient values were respectively 0.486, 0.236. The closer the determination coefficient of the sample was to 1, the better the fitting effect of the model regression equation was. Then, from the determination coefficient values analyzed, it can be seen that the rate of return on net assets obtained based on the financial capital management indicators was 0.005, the value and value were respectively 3.840 and 0.001, which indicated that the selected regression equation was highly significant, the financial capital management indicators had a very significant linear effect on the profitability of non-financial listed companies.

The significance test results of the regression coefficients of the model are shown in Table 6. As can be seen from Table 6, both the size and operating profit of non-financial listed companies passed the 0.05 level test, then, the proportion of financial assets held by the company had a significant negative correlation with the return on net assets. It can be further seen that there was a significant positive correlation among the firm size, the inventory turnover rate, the operating margin and the return on net assets of non-financial listed companies in the control variables, while the comprehensive leverage, capital structure and non-financial listed companies were negatively correlated.

Coefficient of regression

The reason why the financial capital negatively correlated with the return on net assets of non-financial listed companies was not significant at 0.05 was because of the global financial crisis in 2008. Even after the financial crisis, the global economy got certain recovery, but the whole was still in a long-term downturn in the market trend. On the whole, at this stage of the financial market investment strategy, the enterprise management layer maintained a relatively conservative strategy, then, coupled with the scale limitation of the financial capital management, the enterprises were generally unwilling to invest the high-risk projects for the high returns. Through the analysis conclusions, the following suggestions were made to the financial capital management of the non-financial listed companies in China: (1) controlling the size of capital management, in the specific investment process, the market environment and enterprises’ own main business development need to be considered comprehensively, focusing on the scientific and technological innovation, so as to form a modern enterprise development model; (2) strengthening the capital management capacity, in particular, improving enterprises’ inventory management, under the premise of ensuring the normal operation of enterprises, improving the inventory turnover as far as possible, so as to ensure that enterprises can have a higher capital use efficiency; (3) optimizing the capital structure, reducing the enterprise’s asset-liability ratio, starting from the actual business situation, rationally developing the decision making of access capital, besides, fully considering the market risk, expanding the financing channels, and comprehensively improving the profitability of enterprises.

The size of listed companies is generally larger, and furthermore, the enterprises have more abundant operating capital and financing channels. In the environment of the global economic downturn, the main business of the non-financial listed companies operating has also entered a stage of slow development. And many companies have to take investment into the financial market. However, the financial capital management of non-financial listed companies is not a multi-interest matter, and it will also face the impact of the high-risk market environment. Therefore, it is very important to study the impact of the company’s profitability on the survival and development of non-financial listed companies. This time, according to conduct an empirical analysis to the 4680 valid sample data of the non-financial listed companies from 2007 to 2013, mainly including profitability, financial capital operation, control variables index, the empirical model was constructed, and the SPSS software was used to carry out the correlation and regression analysis. From the results of Pearson correlation coefficient in each variable it could be seen that there is a positive correlation between the return on net assets of enterprises and the company size, operating margin and inventory turnover, then, there’s a negative correlation between the return on net assets of enterprises and the comprehensive leverage and capital structure. In addition, from the overall regression model analysis it could be seen that the regression equation selected was highly significant, namely, the index of financial capital operation had a significant linear effect on the profitability of non-financial listed companies. According to the results of this study, some suggestions were put forward on the capital operation of non-financial listed companies, namely, controlling the scale of capital operation, strengthening capital management ability and optimizing capital structure. However, this is only to conduct a unilateral relationship between the financial capital management and profitability, the in-depth demonstration analysis is not carried out comprehensively from both positive and negative aspects.