Abstract

Portfolio optimization is concerned with the optimal allocation of limited capital to the available financial assets to achieve a reasonable tradeoff between risk and profit. The main contribution of this paper is to introduce a new risk measure, conditional value-at-risk (CVaR) of fuzzy variable, to build a class of credibilistic mean-CVaR portfolio optimization model. In the proposed credibilistic portfolio optimization model, the CVaR is used as a measure tool to assess market risk resulted from the financial asset price fluctuations. The computational formulas for common triangular, trapezoidal and normal fuzzy variables are established. Under mild assumptions on the uncertain returns, the proposed credibilistic portfolio optimization model can be turned into its equivalent deterministic mixed-integer parametric programming models, which can be solved by the CPLEX software. The computational results from our numerical experiments demonstrate the efficiency of the proposed CVaR modeling approach as a risk management tool.

Keywords

Introduction

Risk management has received much attention in portfolio selection problems, with variance emerging as one of popular tools [28]. The classical mean-variance model [39] formulated the portfolio selection problem as a bi-criteria optimization problem with a tradeoff between risk and profit. The developments of stochastic portfolio optimization are motivated by the following two basic requirements, one is to model adequately the utility functions, risks and constraints [17], another is to address the computational efficiency for handling large numbers of scenarios [30, 57]. In addition, the technique of stochastic dynamic programming has been applied to multi-period portfolio selection problems [2, 49].

In the literature, variance as a risk measure has been widely criticized by practitioners due to its symmetrical measure with equally weights desirable positive returns and undesirable negative returns [23]. This limitation has led to the research directions where realistic risk measures are used to separate undesirable downside movements from desirable upside movements. Among those risk measures, Vale-at-Risk (VaR) and expected shortfall are the widely accepted popular risk measures [20, 46, 53]. Furthermore, when the distribution information of stochastic returns are partially available, robust portfolio optimization problems have also been studied in the literature [22, 24]. Robust optimization was also used to tackle effectively a newsvendor problem [55].

Since the concept of fuzzy set was introduced in the seminal work of Zadeh [58], fuzzy theory and its applications have been well-developed by a number of researchers [5–10, 59]. The developed fuzzy techniques have been used to model portfolio selection problems [4, 60], in which the variance of fuzzy variable was used as a risk management tool on an agent’s portfolio selection problem. As for various extensions of the fuzzy mean-variance model, the interested reader may further refer to [32, 54].

In fuzzy decision systems, the downside risk measures like absolute semi-deviation and value-at-risk of fuzzy variables have also been studied [1, 51]. Among them, Chen et al. [12] introduced the absolute semi-deviation of fuzzy variable by nonlinear fuzzy integrals, and developed three classes of mean-absolute-semideviation fuzzy portfolio optimization models. Based on the VaR optimization criterion, Liu and Liu [35] discussed how uncertainty and interaction impact the project portfolio return and staff allocation. Wang et al. [51] proposed a VaR-based fuzzy portfolio selection model, where the VaR can directly reflect the greatest loss of a selected portfolio under a given confidence level.

The motivation of this paper is based on the following considerations. Among the downside risk measures in fuzzy portfolio optimization problems, there is no study about the CVaR of fuzzy variable. The difficulty to define such a risk measure is that there is no conditional expectation of fuzzy variable we can apply in fuzzy decision systems. To overcome this difficulty, this paper addresses an alternative approach to defining the CVaR risk measure. Our approach is based on a desirable property that the VaR is an optimal solution to an unconstrained optimization problem. The proposed CVaR can measure adequately the tail information of the loss distribution. That is, for the loss of the portfolio that exceeds a given VaR, the CVaR can effectively measure its risk information.

Overall, this paper contributes to the area of portfolio optimization and management in the following three aspects: First, it introduces a new concept about the CVaR of fuzzy variable. The proposed CVaR is the optimal objective value of a convex optimization model with the VaR being its optimal solution, and is a new downside risk measure that can measure the tail risk adequately. Second, our proposed optimization approach employs the CVaR risk measure to separate undesirable downside movements from desirable upside movements, thus it is an enhancement of the traditional mean-variance portfolio optimization. Third, when fuzzy returns follow common credibility distributions, the equivalent deterministic parametric programming models of the proposed mean-CVaR model are computationally tractable due to their linear objective and constraint functions. Hence, from the computational viewpoint, the proposed mean-CVaR model has some advantages over the traditional mean-variance approach.

The rest of the paper is structured as follows. Section 2 introduces the concept CVaR of fuzzy variable and establishes the CVaR computational formulas for common credibility distributions. Section 3 formulates the mean-CVaR model and derives its equivalent deterministic mixed-integer programming models. Section 4 discusses the performance of the proposed mean-CVaR modeling approach and compares this method with the existing mean-risk optimization method. Finally, conclusions and future work are presented in Section 5. All proofs are given in the Appendix.

The CVaR risk measure

In credibilistic optimization models, one way for addressing simultaneously the loss size and the credibility of loss requires the fractiles of fuzzy variable. If ξ is a fuzzy variable with monotone increasing credibility function F

ξ

(r) = Cr {ξ ≤ r} and 0 < α < 1, then

Assume that 0 < α < 1 holds and define the following Value-at-Risk (VaR) for fuzzy variable ξ:

According to this definition, for a given credibility level α,

Based on the expected value of fuzzy variable [33], one has the following convexity property about unconstrained optimization problem (2):

Under the assumption that F

ξ

(r) = Cr {ξ ≤ r} is continuous, the set of solutions to problem (2) consists of the set of α-fractiles of fuzzy variable ξ. Indeed, by the following integral representation

The above analysis motivates us to introduce the following new risk measure for fuzzy variables:

The CVaR risk measure is defined on the linear space of fuzzy variables with finite expected values. If F

ξ

(r) is continuous, then VaR v

α

is an optimal solution to problem (2). As a result, the following inequality holds true:

For a fuzzy variable with a triangular credibility distribution [21], its α-CVaR computational formula is given in the following theorem:

The next theorem discusses the α-CVaR computational formula for a trapezoidal fuzzy variable:

The following theorem deals with the α-CVaR computational formula for a normal fuzzy variable:

Taking the CVaR as a risk measure, a new class of credibilistic mean-CVaR portfolio optimization model will be built in the next section.

Formulation of mean-CVaR model

A portfolio manager may use his/her experience in stock picking to decide on an appropriate mix of assets in the portfolio selection process. For illustrating the use of the proposed CVaR risk measure in practice, we present a novel credibilistic portfolio selection model. We consider a one-period financial portfolio optimization problem with n risk assets. Denote η T = (η1, η2, …, η n ) as the vector of fuzzy returns of assets and r i = E [η i ], i = 1, 2, …, n, the mean returns, where the fuzzy vector η is assumed to follow a known joint credibility distribution.

A portfolio is a collection of nonnegative numbers x

j

, j = 1, 2, …, n, that sum to one. The return one would obtain using a given portfolio is given by η

T

x. Since for the CVaR risk measure we have interpreted negative values of fuzzy returns as losses, we take ζ (x, η) = - η

T

x. Thus, the expected value E [η

T

x] of η

T

x and CVaR

If y

j

is a binary variable that is equal to 1 if asset j is selected in the portfolio and 0 otherwise, then

Since the investment proportions will not be infinitesimal in actual investment operations, we introduce the lower bound l

j

of fraction of the capital budget that can be invested in the jth asset. Taking into account the issue of investment diversification, we also introduce the upper bound u

j

of the fraction. These considerations can be represented as

In addition, a portfolio should satisfy the following constraints under the assumption that short sales are not permitted:

As a consequence, to find a portfolio with the minimum risk, we develop a new credibilistic mean-CVaR optimization model in the following form:

The interpretation of mean-CVaR model (8) is as follows: the portfolio manager is looking for a portfolio with the minimum risk in the sense of CVaR, under prescribing a minimum acceptable level μ p of mean portfolio return.

In mean-CVaR model (8), the optimal objective value Ψ (μ

p

), as a function of μ

p

, plays an important role. The graph of Ψ (μ

p

) in

To solve mean-CVaR model (8), we now identify the cases when model (8) can be turned into its equivalent deterministic programming model. Under the assumptions that fuzzy returns are mutually independent in the sense of [36], and follow common credibility distributions [21], one can obtain the desirable results, which are provided in the following theorems.

Firstly, when fuzzy returns follow the triangular credibility distributions, one has the following results:

If the credibility level 0 < α ≤ 0.5, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

If the credibility level 0.5 < α < 1, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

Secondly, when fuzzy returns follow the trapezoidal credibility distributions, one has the following results:

If the credibility level 0 < α ≤ 0.5, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

If the credibility level 0.5 < α < 1, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

Finally, when fuzzy returns follow the normal credibility distributions, one has the following results:

If the credibility level 0 < α ≤ 0.5, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

If the credibility level 0.5 < α < 1, then mean-CVaR model (8) is equivalent to the following mixed-integer parametric programming

On the basis of Theorems 5, 6 and 7, when fuzzy returns are mutually independent and follow the triangular, trapezoidal and normal credibility distributions, the original mean-CVaR model (8) can be turned into its equivalent deterministic mixed-integer parametric programming models, which can be solved by conventional optimization software like the CPLEX solver. As a consequence, Theorems 5, 6 and 7 benefit us to find the optimal portfolio choice when the proposed mean-CVaR model (8) is used to model the actual fuzzy portfolio selection problems.

Based on the analysis of mean-CVaR model (8) in the above subsection, when fuzzy returns are mutually independent and follow the triangular credibility distributions, we can find the optimal solution to model (8) by solving its equivalent mixed-integer parametric programming model (9) or (10) according to the value of the credibility level α. Given the values of model parameters m, μ p , l i , u i , model (9) or (10) becomes a mixed-integer programming model, which can be solved by the CPLEX software. This solution procedure described above can be summarized as follows.

Step 1. Set the values of model parameters m, μ p , l i , u i and the credibility level α in model (8);

Step 2. If the credibility level 0 < α ≤ 0.5, then solve model (9) via the CPLEX software, and denote the optimal solution as

Step 3. If the credibility level 0.5 < α < 1, then solve model (10) via the CPLEX software, and denote the optimal solution as

Step 4. Return the optimal solution

When fuzzy returns follow the trapezoidal or normal credibility distributions, the solution procedure can be described similarly. In the next section, the effectiveness of the above solution method is demonstrated by an application example.

Numerical experiments

In this section, a one-period portfolio selection problem is considered. We demonstrate the proposed modeling ideas via some numerical experiments.

Statement of problem

An investor wants to invest his/her capital in 200 assets by investing proportion x i in the asset i. The first 199 assets are risky, while the last one is a risk-free asset. Suppose that risk asset i has a return η i at the end of the investment period, and the returns of risky assets are mutually independent. In addition, assume that short sales are not permitted, all available wealth should be invested. The maximum number of assets that can be selected in a portfolio is m, while the lower and upper bounds of fraction of the capital budget that can be invested in the ith asset are l i and u i , respectively. Under the condition that the expected return is not less than a prescribed return level μ p , the investor desires to find a portfolio with the minimum risk.

In practice, one day in the future the open price, the highest price, the lowest price, and the close price may be affected by many factors. Therefore the future returns η i of the risk assets cannot be exactly estimated by the available historical data. On the basis of available information about the potential assets and the estimated values provided by stock experts, the returns can be expressed as fuzzy variables η i , i = 1, …, 199 . The return of the risk-free asset is η200 = 1.0169 . As a consequence, the considered portfolio selection problem is a fuzzy optimization problem.

To help the investor make up his mind, if the investor employs model (8) to find the optimal portfolio decision, then the above portfolio selection problem can be built as the following optimization model:

In model (15),

In this subsection, we use the CPLEX software to solve models in our personal computer (Think-PC with Intel(R) Core(TM) i5-5200U CPU 2.20 GHz and RAM 8.00 GB). The computational results are reported in the following two cases.

When the credibility level is 0.85, according to Theorem 5, mean-CVaR model (15) is equivalent to the following mixed-integer parametric programming model:

We use the CPLEX software to solve this equivalent mixed-integer programming. Setting the acceptable return level μ p as 1.2669, 1.2169, 1.1669 and 1.1169, respectively, the optimal investment policies are reported in Table 1, from which we observe that under different return levels, the recommended investment policies are different. Although the asset 1 is always invested in, the investment proportions are different. With the decrease of the minimum acceptable return level μ p , the minimum risk in the sense of CVaR decreases.

The optimal solutions to model (15-1) under the credibility level 0.85

Next the effects of the credibility level α on optimal solutions are analyzed. Given an acceptable return level 1.2169 and different credibility levels 0.85, 0.75, 0.65 and 0.55, according to Theorem 5, mean-CVaR model (15) is equivalent to the mixed-integer programming model (15-1). We use the CPLEX software to solve this model. The optimal investment policies are reported in Table 2, from which we observe that the recommended investment policies are different under different credibility levels. Even if some assets are always invested in, the investment proportions are different. For example, when the credibility level is 0.85, the investment proportion in asset 1 is 0.2, while the investment proportion in asset 1 is 0.19458 under the credibility level 0.75. With the decrease of the credibility level, the minimum risk in the sense of CVaR decreases.

The optimal solutions to model (15-1) under the return level 1.2169

Under the credibility level 0.85, the efficient frontier of model (15-1) is plotted in Fig. 1, where the horizontal axis corresponds to risk in the sense of CVaR and the vertical axis corresponds to return.

The efficient frontier of model (15-1) under the credibility level α = 0.85.

We first analyze the effects of the model parameter μ

p

on optimal solutions. When the credibility level is 0.85, according to Theorem 7, mean-CVaR model (15) is equivalent to the following mixed-integer parametric programming model:

Setting the minimum acceptable return level as 1.2669, 1.2169, 1.1669 and 1.1169, respectively, the recommended investment policies are reported in Table 3. The computational results demonstrate that the recommended investment policies are different under different return levels. For example, the investor is not recommended to invest in the asset 195 under the return levels 1.2669 and 1.2169, while the asset 195 is recommended under the return levels 1.1669 and 1.1169. In the latter two situations, even if the asset 195 is always invested in, the investment proportions are different. With the decrease of the minimum acceptable return level, the minimum risk in the sense of CVaR decreases.

The optimal solutions to model (17) under the credibility level 0.85

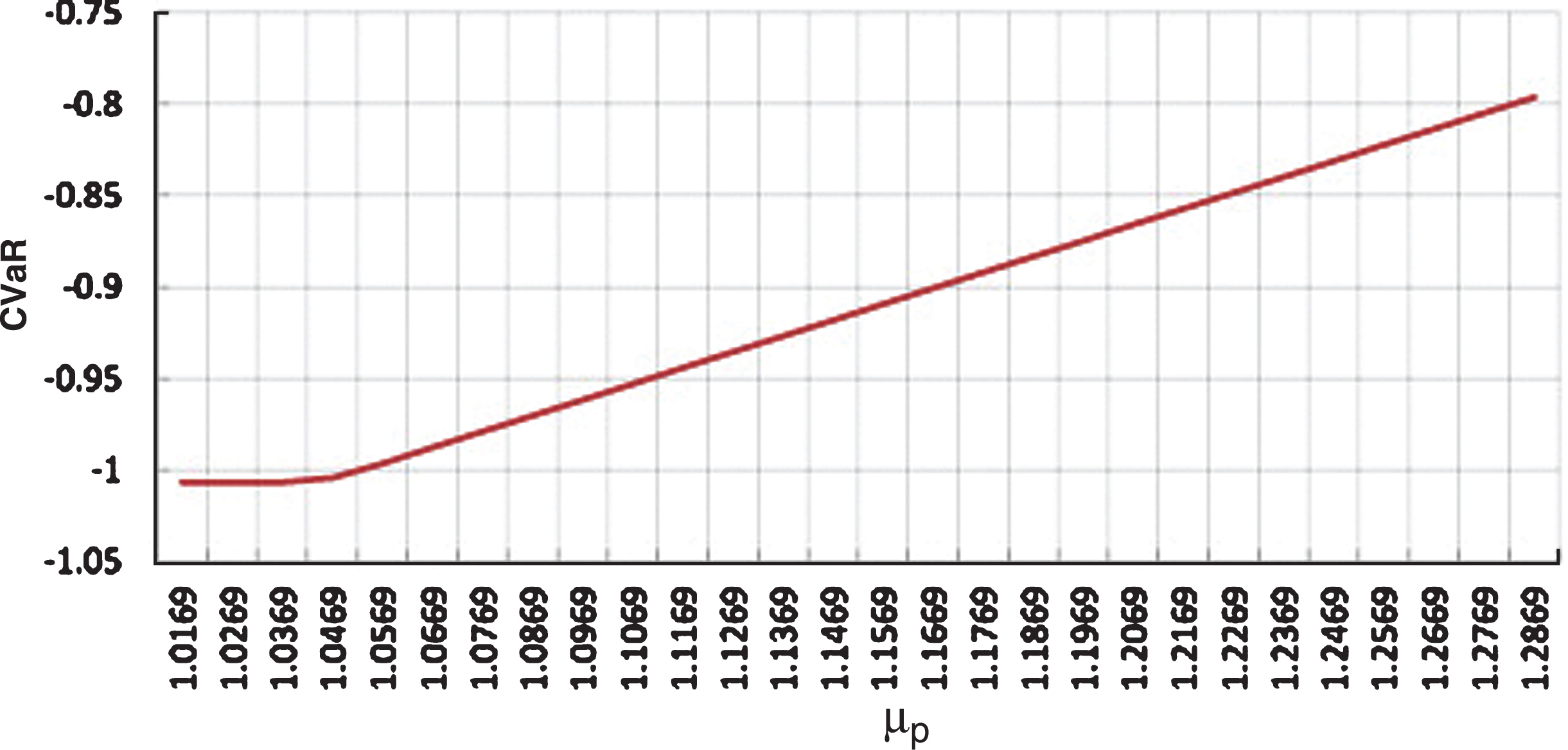

Under the credibility level α = 0.85, the efficient frontier of model (17) is plotted in Fig. 2, where the horizontal axis corresponds to risk in the sense of CVaR and the vertical axis corresponds to return.

The efficient frontier of model (17) under the credibility level 0.85.

We next analyze the effects of the credibility level α on optimal solutions. Given an acceptable return level 1.2169, and different credibility levels 0.85, 0.75, 0.65 and 0.55, using the CPLEX software, the obtained optimal investment policies are reported in Table 4, from which we find that when the credibility level is 0.85, the investment proportion in the asset 1 is 0.1002, while the investment proportions in the asset 1 corresponding to the credibility levels 0.75, 0.65, 0.55 are 0.2, 0.15391, 0.096852, respectively. The asset 2 is only recommended under the credibility level 0.75. As a consequence, under different credibility levels, the recommended investment policies are different. With different credibility levels, even if some assets are always invested in, the investment proportions are different. In addition, from Table 4 we observe that the minimum risk in the sense of CVaR decreases with respect to credibility level α.

The optimal solutions to model (17) under the return level 1.2169

For the sake of comparison, based on the risk-reward optimization method [12], we model the above portfolio selection problem as the following mean-EAD model:

According to [12, Theorem 7], for triangular fuzzy returns η

i

∼Tri (μ

i

- s

i

, μ

i

, μ

i

+ s

i

) , i = 1, …, 199, model (18) is equivalent to the following mixed-integer parametric programming model:

Under some acceptable return levels 1.2669, 1.2169, 1.1669 and 1.1169, we employ the CPLEX software to obtain the optimal investment policies in Table 5.

The optimal solutions to model (19)

From the computational results reported in Tables 1 and 5, we observe that when the minimum acceptable return level μ p is 1.2669, the mean-CVaR optimization model recommends the investor to invest in assets 1, 2, 3, 26, 46 and 86, and the corresponding investment proportions are 0.2, 0.2, 0.10641, 0.2, 0.2 and 0.093586, respectively. Under the same return level, the mean-EAD optimization method recommends the investor to invest in assets 1, 2, 3, 45, 55 and 97, and the corresponding investment proportions are 0.2, 0.2, 0.2, 0.19324, 0.15676 and 0.05. Although the asset 3 is recommended by both methods, the investment proportions are different.

In summary, the recommended investment policies by our mean-CVaR optimization method and the mean-EAD optimization method are different under the same return level; even if some assets are recommended by both methods, the investment proportions are different.

This work focused on downside risk as an alternative risk measure in uncertain financial markets, and contributed to the area of portfolio optimization and management in the following several aspects.

First, a new concept about the CVaR of fuzzy variable was introduced. The difficulty to define such a risk measure is that there is no conditional expectation of fuzzy variable we can use in fuzzy decision systems. This work presented this risk measure based on a desirable property that the VaR of fuzzy variable is an optimal solution to an unconstrained optimization problem. The proposed CVaR risk measure can measure the tail risk adequately.

Second, we considered an alternative mean-variance model in which the variance was replaced with the CVaR risk measure, in order to better assess market risk exposure related to the financial asset price fluctuations.

Third, from computational viewpoint, the proposed mean-CVaR model has some advantages over the traditional mean-variance optimization approach. When fuzzy returns follow common credibility distributions, the equivalent deterministic parametric programming models of the proposed mean-CVaR model are computationally tractable by conventional optimization softwares. The computational results from our numerical experiments supported our arguments.

There are several issues deserve to be further addressed. First, granular computing is a novel computation theory to build an efficient computational model for complex optimization problems with huge amounts of data, information and knowledge [3, 56]. Thus, it is worth of using the granular computing technique to solve fuzzy portfolio selection problems. Second, when fuzzy returns are not mutually independent, the efficient solution method for the proposed mean-CVaR model is a challenging research issue.

Footnotes

Appendix

In this Appendix, the proofs of Theorems 1, 3 and 6 are provided, and Theorems 2, 4, 5 and 7 can be proved similarly.

By the property of absolute semi-deviation of fuzzy variable [12], u (z) can be represented as

For each fixed r, (r - z) + is obtained from the convex function (·) + by substituting a linear function, therefore it is convex. Taking the L–S integral clearly preserves convexity, the proof of theorem is complete.

By calculation, the credibility of event {ξ ≤ t} is

If the credibility level 0 < α ≤ 0.5, then the solution v

α

of the following equation

By calculation, the α-CVaR of ξ is

On the other hand, if the credibility level 0.5 < α < 1, then the solution v

α

of equation

The proof of theorem is complete.

Since η

i

∼ Tra (ri1, ri2, ri3, ri4) for all i, given a portfolio x

T

= (x1, x2, …, x

n

), one has

Since fuzzy variables η

i

x

i

, i = 1, 2, …, n are mutually independent, one has

Then the expected value of trapezoidal fuzzy variable η

T

x is

As a consequence, the constraint E [η

T

x] ≥ μ

p

is equivalent to the following linear constraint

On the other hand, if we denote ζ (x, η) = - η

T

x, then one has

When the credibility level 0.5 < α < 1, by Theorem 3, the α-CVaR of ζ (x, η) is represented by

As a consequence, the objective in model (8) can be rewritten as the following equivalent form:

The proof of assertion (ii) is complete.

Acknowledgments

This work is supported by the National Natural Science Foundation of China [No. 61773150].