Abstract

Asian option is known as a derivation financial product. And uncertain finance takes uncertain situation into account, and there comes uncertain stock models based on uncertain theory. This paper follows the mean-reverting stock model which based in uncertain situations presented by Liu. The mean-reverting model under asian option is discussed in this paper. This paper deals with the problem of pricing an Asian currency option. Based on the principle of making fair deal, the pricing formula is verified. Furthermore, a simple discussions about the situation of single variable in the option pricing model are also drawn in this paper. Basic relations between parameters and result are also discussed.

Introduction

Based on probability theory, stochastic process is an traditional method for many researchers to study financial cases. Based on the probability theory, many academic results were concluded. Black and Scholes [1] proposed Black-Scholes formula in 1973, trying to verify the stock price in financial market. In addition, the currency option was also studied in detail by early researchers based on the stochastic process. The traditional finance theory is established under the assumption that stock price, interest rate, and exchange rate all follow stochastic differential equations. Paradox was given by Liu [13] against this preassumption. The paradox shows that real stock price is impossible to follow any stochastic differential equations. Considering the conflicts between probability theory and real situations, we have to invite some domain experts to evaluate the belief degree that each event will happen. In order to model the belief degree, uncertainty theory was founded by Liu [9] in 2007. It is suggested by Kahneman and Tversky [17] that human beings tend to overweigh unlikely events, thus the belief degree has a much larger range than the probability distribution. Probability theory is inefficient to deal with belief degree. Uncertainty theory has developed greatly ever since 2007. There are many branches such as uncertain programming, uncertain logic, uncertain calculus, uncertain differential equation, uncertain finance, uncertain statistics, chance theory and many others. In uncertain calculus, which is a branch of mathematics that deal with differentiation and integration of uncertain processes, Liu process, a special uncertain process was proposed [11] in 2009. Liu process is an uncertain process whose value equals 0 at time 0 and all sample paths are Lipschitz continuous. Also, Liu process has stationary and independent increments. Thereby uncertain calculus developed on the basis of Liu process. Nowadays, uncertain calculus is consisting of many features such as Liu integral, Liu process and many useful assertions such as chain rules, change of variables, integration by parts and other theorems. With the work on uncertain calculus, another aspect of study was suggested by Liu [10] in 2008. uncertain differential equation is a type of differential equation involving uncertain processes. Nowadays, the uncertain differential equation has brought some breakthrough both in theory and practice. To get the solution of uncertain differential equations, an analytic solution to linear uncertain differential equations was obtained by Chen-Liu [5]. On the other hand, Liu [15] and Yao [25] presented a group of analytic methods to solve some special classes of nonlinear uncertain differential equations. What’s more, it is discovered that the solution of an uncertain differential equation can be represented by a group of solutions of ordinary differential equations by Yao-Chen [24]. Asian option was first introduced in Tokyo by some American banks. Compared to American and European options, Asian option is a special type of option contract. The payoff of the Asian option depends on the average price of underlying asset over some pre-set period of time. The payoff of the option contract depends on the price of the underlying instrument at exercise.

As an alternative to classical finance theory, the idea of uncertain finance was firstly suggested by Liu [13]. As a strong tool, Liu [11] introduced uncertain differential equations into finance in 2009. Then an uncertain stock model was proposed. Thus European option price formulas were provided. And Chen [2] proved American option price formulas. Furthermore, Asian option pricing is studied by Sun-Chen [20] and Zhang-Liu [27]. No-arbitrage theorem for this type of uncertain stock model is proved by Yao [22]. It is emphasized that uncertain stock models were also actively investigated among others by Peng-Yao [18], Yu [26], Chen-Liu-Ralescu [6], Yao [23], and Ji-Zhou [8]. Uncertain differential equations were used to simulate floating interest rate by Chen-Gao [4] in 2013 and an uncertain interest rate model was presented. Following that, Jiao-Yao [7] presented a price formula of zero-coupon bond, and Zhang-Ralescu-Liu [28] discussed the problem of interest rate options.

Yet uncertain differential equations were employed to model currency exchange rate. In 2015, Liu-Chen-Ralescu [16] proposed an uncertain currency model. This model assumed that the exchange rate follows an uncertain differential equation thus formed the model. Domestic currency and foreign currency are presented with different interest rate. In this paper, the situation of fixed interests rate is discussed. The effects of certain parameters on the result are also concluded. With Liu-Chen-Ralescu [16] currency model, currency option pricing becomes feasible and some currency option price formulas were proved for the uncertain currency markets. Uncertain currency models were also actively investigated among others by Liu [14], Shen-Yao [19] and Wang-Ning [21]. For further explorations on the development of the theory of uncertain finance, you may consult papers on uncertain finance [3].

The rest of this paper is organized as follows. In Section 2 we will present some basic concepts and properties in uncertainty theory, including concepts such as uncertain variables and distributions, Liu process, uncertain differential equations, Liu-Chen-Ralescu currency model and mean-reverting model and so on. In Section 3 we will introduce the Asian currency option and derive its pricing formulas. In Section 4, numerical experiments were proposed and influence of single variable on results are also discussed. Finally, some conclusions are made in Section 5.

Preliminary

Axiom 1: (Normality Axiom) M { Γ } = 1 for the universe set Γ.

Axiom 2: (Duality Axiom) For any measurable set Λ:

Axiom 3: (Subadditivity) Any series of events Λ1, Λ2, …,

Axiom 4: (Product Axiom) Assume (Γ

k

, L

k

, M

k

) is an uncertainty space for k = 1, 2, 3, ⋯. Thus product measure M is an uncertain measure satisfying:

C0 = 0 and almost all sample paths are Lipschitz continuous, C

t

has stationary and independent increments, every increment Cs+t – C

s

is a normal uncertain variable with an uncertainty distribution:

Then Liu integral of X

t

with respect to C

t

is defined as

The uncertain differential equations are commonly used in financial markets. In modern society, the international business becomes more and more frequent, and the capital market is no longer within one country. Thus the foreign exchange market becomes an active market, and changes in foreign exchange rates (FXR) draw a lot of attentions from researchers all over the world. Uncertain finance is a powerful tool in solving foreign exchange rate problems. Liu-Chen-Ralescu [16] proposed an uncertain currency model

The Liu-Chen-Ralescu [16] currency model is based on the assumption that exchange rate Z

t

follow a geometric Liu process. In the long term currency markets, the geometric Liu process will not be valid as it increases to infinity. Mean-reverting model was proposed by Shen and Yao [19] takes one general economic behavior into accounts: mean-reverting process. In the real global market, the change of foreign exchange rate is not so dramatic, and instead, it stays around an average level in the long term. In the following model, the foreign exchange rate stays around the average

An Asian currency option is a contract that gives the holder the right without the obligation to buy one unit of foreign currency at the expiration date T with a striking price K. Let f e represent the price of the contract.

Because the price of Asian acts the same as an European option, but the final feasible price is based on the expected value of the integral of all the prices before the strike time T. Anytime before strike time T, the feasible price of an Asian option is Z

t

, but at strike time, the feasible price becomes

Consider the general uncertain stock model (refLCRstockModel), we assume that the Asian call option has strike price K and expiration time T. Let Z

t

be the price of the underlying stock, then the payoff of the Asian call option is defined by

It is known that profit only comes from interest and the action of trading this option. If the exchange rate Z0 increase. The buyer can buy certain amount of foreign currency at the striking price K and instantly sell the foreign currency at the exchange rate

While the return of bank at time 0 is

The fair price of this contract should make the investor and the bank have an identical expected return, i.e. we can obtain the following theorem.

Thus the pricing formula can be presented as follows:

Furthermore, this pricing formula can be solved as follows,

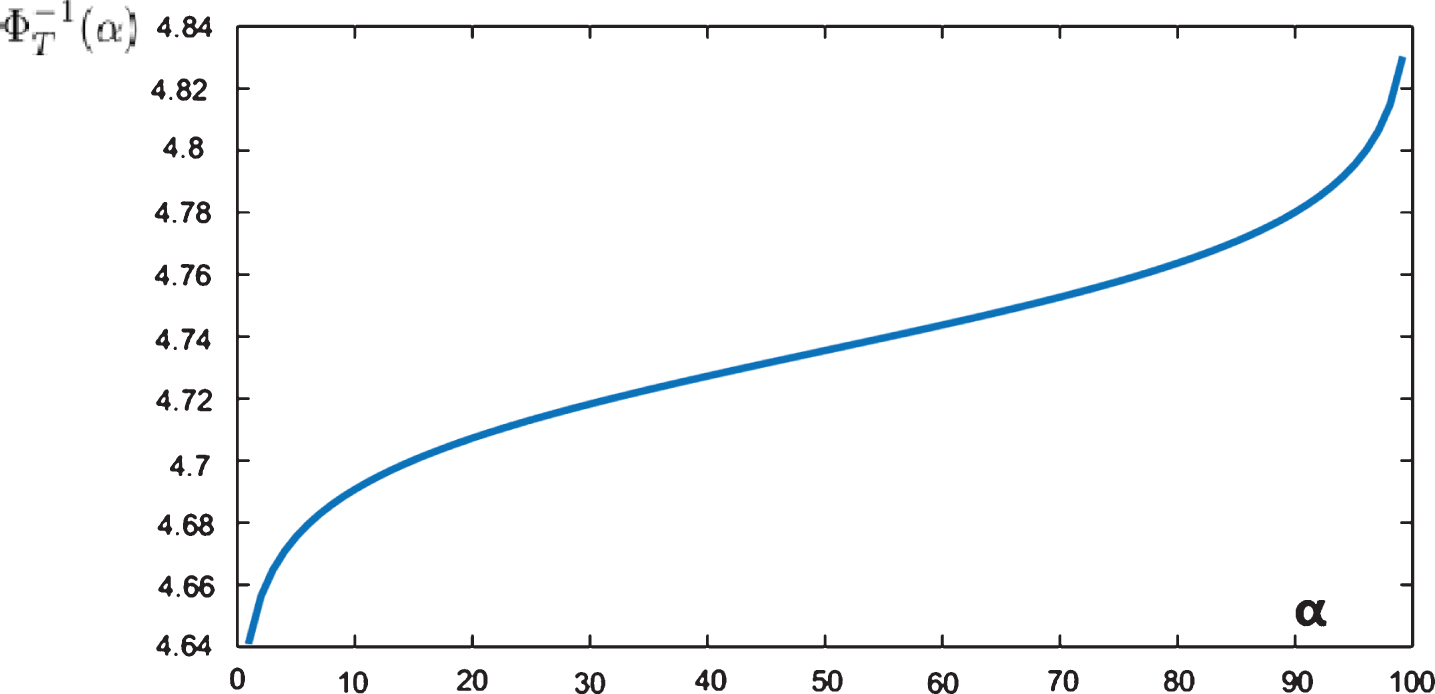

The inverse distribution of time integral

According Equation (1), Z

t

can be presented as

And by Definition 2.10, conclude the ordinary differential equation

Solving the ordinary differential equation, and get the α-path of Z

t

:

Set Z0 initial price and Φ the standard normal uncertainty distribution, i. e.

By Theorem 2.3, the average price

By Theorem 2.1, the inverse distribution of

An algorithm was designed to calculating the price f e .

And

To decide the best range of parameters, we need to review the definition of pricing

Thus we could draw the figure on the relation between

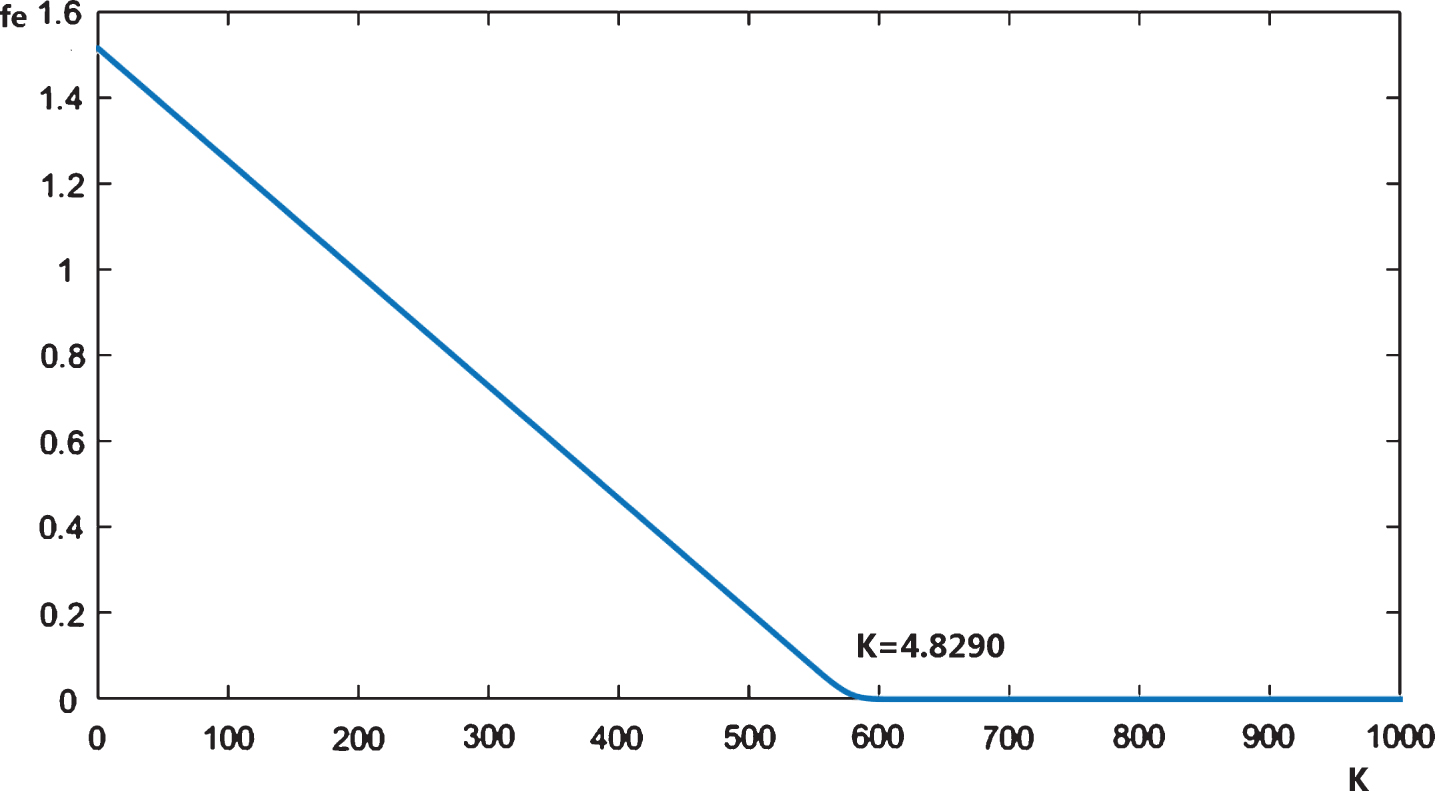

Under the condition m = 6, a = 1, Z0 = 4, T = 1, σ = 0.1, u = 0.05, v = 0.04, it is found out that the reasonable value of K should be less than 4.8290. If not, the value of f e bound to be 0 if the strike price is higher than 4.8290.

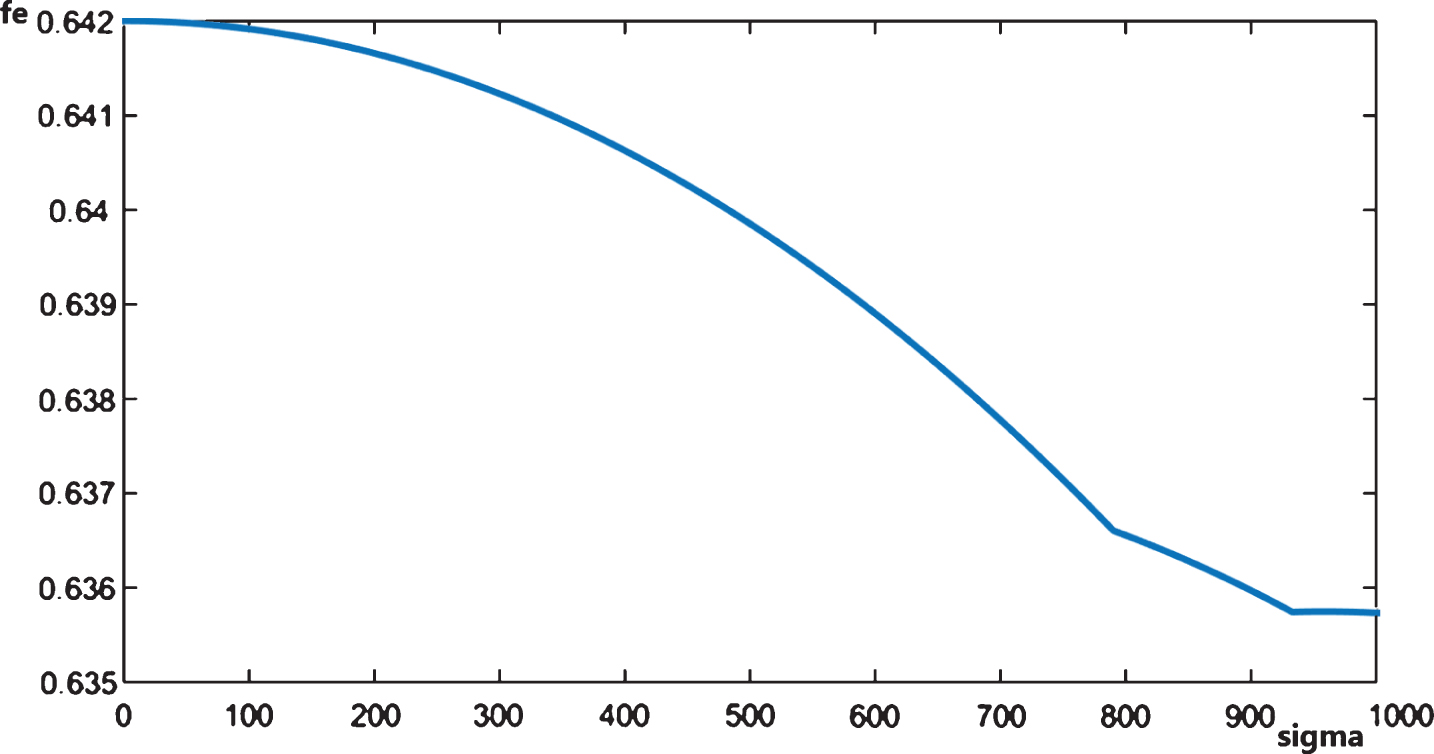

When other parameters except σ are constants. We assume m = 6, a = 1, K = 4, Z0 = 4, u = 0.05, v = 0.04, T = 1; And change σ from 0 to 1 with the step 0.001, and we can draw the figure of option price f e :

As the log-diffusion increases, the instability rises, thus the price should be lower.

After analysis, it is founded that K is linear related to f e . As strike price K increases, it is more difficult to gain profits as exercise price increase higher than strike price K. And the option price should be lower. But when strike price K is higher than 4.8270 under the assumed conditions, the price of Asian option is bound to be 0.

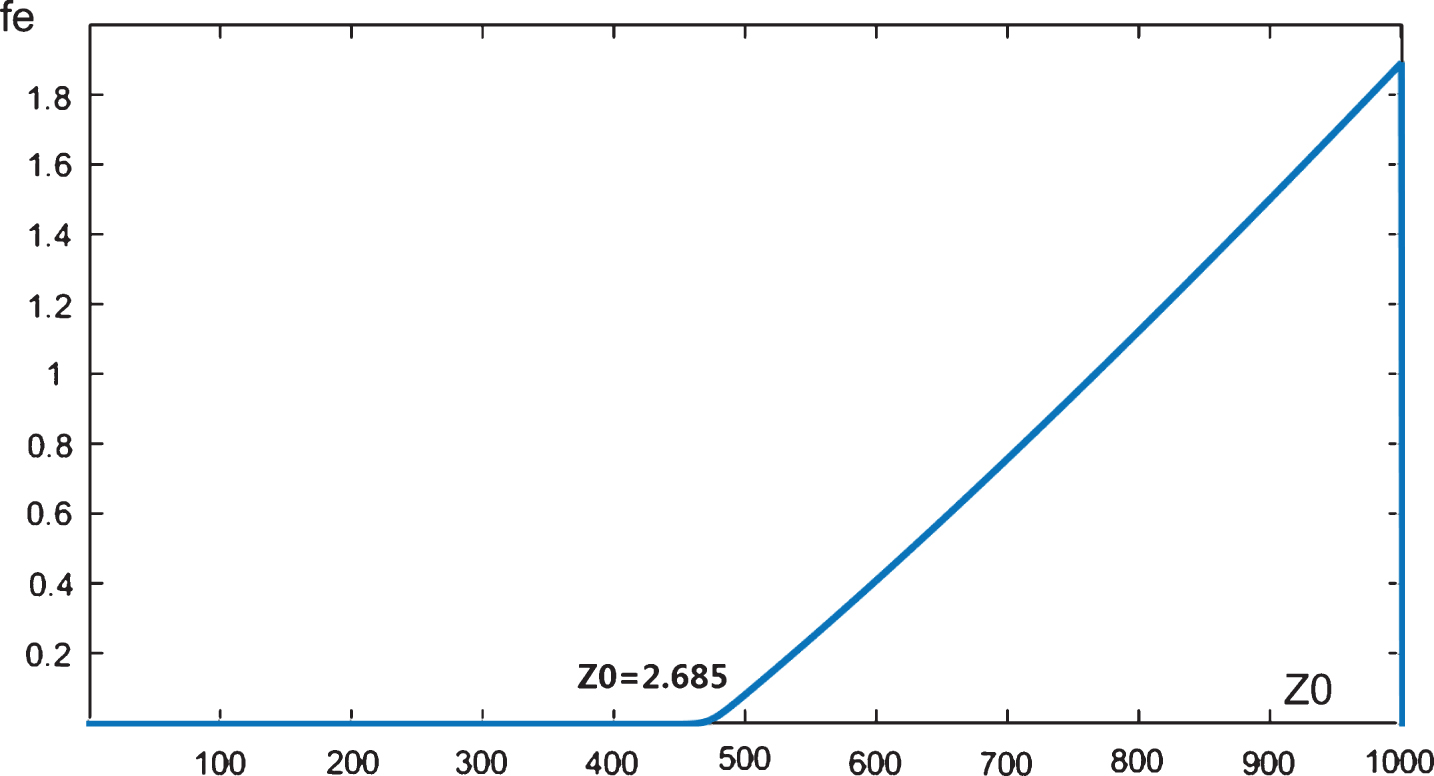

Under the assumption that the strike price K and log-diffusion σ don’t change, analysis also shows that f e is linear related to initial exchange rate Z0, the Asian option price goes up as the initial exchange rate Z0 increases. When initial exchange rate is lower than 2.685, it is merely impossible for buyer and bank to gain profits. Thus the option price is bound to be 0.

f

e

with the change of σ

f e with the change of σ

f e with the change of K

f e with the change of Z0

In this paper, the mean-reverting model under Asian currency option was proposed. Thus the pricing formula of Asian currency under mean-reverting process can be verified. Numerical experiment with respect to single variable: log-diffusion σ, strike price K, initial exchange rate Z0 is proposed. The analysis on the value’s range of K, Z0 and the effects of them on f e are also discussed.

Footnotes

Acknowledgments

This work was supported by National Natural Science Foundation of China (Grants Nos. 61563050, 61462086) and National Natural Science Foundation of China (No. U1703262).