Abstract

Players are often assumed to be perfect rational in Bertrand game. However, the decision-making of players is influenced by their behavioral characteristic, psychology preferences and other uncertain factors. Therefore, this paper focuses on investigating the price strategies of players with risk aversion in a Bertrand game under a fuzzy environment. Based on the credibility theory, a fuzzy Bertrand game model with risk aversion is constructed, where optimistic value criterion is applied to model players’ risk aversion. The market demand for each player is assumed as a fuzzy variable. Then, a solution concept of the (α1, α2)-optimistic equilibrium price is defined and investigated. Finally, some numerical studies are applied to analyze how the risk aversion behavior of players (the confidence levels of players) affects the (α1, α2)-optimistic equilibrium prices and the profits of the fuzzy Bertrand game.

Introduction

Bertrand game is a model about price competition between players, which presents the interactive behaviors among players that make price decisions and their consumers that choose quantities at a set price [2]. There are a lot of researches about the Bertrand game, including equilibrium of game models [16, 29], strategic choice of timing [1, 45], asymmetric costs [3, 36], and some applications to the economic problems [8, 41]. These above studies are assumed to be in a certain environment. However, many uncertain factors, such as consumer demand and fluctuation in production, may limit the application in the practice, which can’t be ignored.

Fuzzy set theory proposed by Zadeh [50] offers a proper approach to handle these uncertain problems, which has already been adopted to describe the uncertainty in games. Maeda [26] explored the bimatrix games with fuzzy payoffs. Nishizaki and Sakawa [33] proved the equilibrium of multi-objective bimatrix games with fuzzy payoffs and goals. Campos [4] constructed a Fuzzy Linear Programming to obtain the optimal solutions of a two-person zero-sum game with uncertain payoff matrix. Sakawa and Nishizaki [37–39] explored the Max-min solutions and Pareto-equilibrium solutions of two-person zero-sum games with fuzzy multiple payoff matrices. Wu and Soo [47] defined a fuzzy Nash equilibrium and explored an n-person matrix game with fuzzy strategies. Garagic and Cruz [15] analyzed an n-person non-cooperative fuzzy game. Fuzzy set theory is very popular in fuzzy games. Based on fuzzy set theory, the existence of fuzzy Nash equilibrium for fuzzy games can be proved.

Recently, abundant researches have investigated the oligopolistic competition game under a fuzzy environment, such as Cournot game and Bertrand game. Dang and Hong [6] studied duopoly competition with fuzzy demand and costs. Based on Dang and Hong [6], Dang et al. [7] further extended duopoly competition to multioligopoly competition. Tan et al. [43] employed the rank-dependent utility theory to analyze Cournot competition with fuzzy market demand. The significance of fuzzy profit function was emphasized strongly in the above papers. Meanwhile, it was also introduced into a fuzzy supply chain with Bertrand competition. Zhao et al. [52] explored the pricing problem of two substitutable products in a fuzzy supply chain with fuzzy market demand and costs, where a retailer purchased the products from two manufacturers competing in a Bertrand game. In a fuzzy environment where market demand and costs are fuzzy, the optimal pricing strategies of two substitutable and complementary products in Bertrand price competition were analyzed respectively [46, 53]. Based on the expected value criterion that denotes the player’s desire to maximize his/her expected payoff, all these studies examined the effect of the fuzzy parameters on the optimal pricing decision. The expected value criterion is a credibilistic method that credibility theory offers. Despite much attention on price competition between two players in a fuzzy environment, research on the Bertrand game composed of two competitive players under a fuzzy environment is inadequate. Thus, according to these achievements, we incorporate credibility theory into this paper to depict the uncertainty in Bertrand game.

Additionally, many works on game under a fuzzy environment are based on the assumption that players are full rational and desire to maximize their own expected profits. However, people in reality are often tend to show the behavioral characteristics of bounded rationality with risk aversion and do not seek to maximize their profits as they are in the face of gain. For example, a risk averse stakeholder would take a conservative watershed development plan to increase chances of system feasibility, which might reduce the agricultural profits [38, 44]. Under the fuzzy environment, optimistic value criterion, another credibilistic method that credibility theory offers, is suitable for its application to describe the situation where players desire to maximize the α-optimistic value of their profits at a predetermined confidence level α [12]. Each confidence level corresponds to a level of players’ risk aversion. Nowadays, optimistic value criterion has been incorporated into fuzzy games to model players’ risk aversion behavior, such as bimatrix game [9, 12], coalitional game [14, 40], extensive game [13], two-person nonzero-sum game [11] and n-person non-cooperative game [42]. However, little attention has been paid to analyze the risk aversion behavior in a fuzzy Bertrand game through optimistic value criterion. We thus adopt optimistic value criterion to model risk aversion of players in fuzzy Bertrand game and investigate the effect of risk aversion on the optimal price strategies.

The purpose of this paper is to explore the effect of risk aversion in a Bertrand game under a fuzzy environment. The market demand for each product are posited as a fuzzy variable. Based on credibility theory, a fuzzy Bertrand game model with risk aversion is established. To model risk aversion of players, optimistic value criterion is applied. By game-theoretical approach, the (α1, α2)-optimistic equilibrium price is obtained. Some numerical studies are conducted to analyze how the (α1, α2)-optimistic equilibrium prices and the profits of players change when both two players are risk averse. There are some interesting findings. For example, under a fuzzy environment, a higher risk aversion leads to a lower price and a lower profit. Moreover, the price and profit of a player are more greatly affected by his own risk aversion than the other player’s risk aversion. Our study extends the classical Bertrand game to a fuzzy Bertrand game with risk aversion and provides a multi-perspective analysis of the impact of risk aversion on the prices and profits to make results more reasonable and closer to reality.

The rest of this paper is organized as follows. In Section 2, the basic concepts of fuzzy variable, possibility theory, and credibility theory are discussed. In Section 3, a fuzzy Bertrand game model with risk aversion is established, and a solution concept of (α1, α2)-optimistic equilibrium price is defined, and four cases of (α1, α2)-optimistic equilibrium price is solved. In Section 4, some numerical studies are used to analyze the influence of risk aversion on the (α1, α2)-optimistic equilibrium prices and the profits in the fuzzy Bertrand game. In Section 5, some conclusions are summarized.

Preliminaries

In this section, some basic concepts of fuzzy variable, possibility theory, and credibility theory are presented, respectively. The classical Bertrand game under crisp environment is also introduced.

Fuzzy environment

Fuzzy set theory put forward by Zadeh [50] offers an alternative approach to solve uncertain problems about internal ambiguity and imprecision of human cognitive processes. Fuzzy variable is one of the most important concepts in fuzzy set theory [18, 51]. As mathematical tools in fuzzy set theory, possibility theory [34, 51] and credibility theory [22, 23] are applied to explain and handle fuzzy phenomena, and have been widely used in many fields, such as option pricing [10] and transportation planning [19, 49]. Hence, some basic concepts of fuzzy variable, possibility theory and credibility theory are introduced in this subsection.

A fuzzy variable

Then, the triplet (Θ, P(Θ), Cr) is called as a credibility space, and the function Cr is called as a credibility measure.

As a special fuzzy variable, a triangular fuzzy variable [22] is denoted as

For two triangular fuzzy variables

It means that the fuzzy variable

Then, the α-optimistic value and α-pessimistic value of a triangular fuzzy variable

In a classical Bertrand game, players make their own price decisions to maximize their profits respectively. There are two players with two substitutable products in the market. More specifically, product 1 is produced by player 1 and product 2 is produced by player 2. Both two players decide their price strategies independently and simultaneously. They also have a commitment to supply whatever the market demand is forthcoming at the price it sets.

For player i, let Q i (i = 1, 2) be the market demand, p i (i = 1, 2) be the market price, and c i (i = 1, 2) be the marginal production cost, and p i > c i . Then, the market demand function of player i is Q i = a i − b i p i +θp j , i, j = 1, 2, where a i represents the market potential, b i denotes the price flexibility coefficient, and θ is the cross-price flexibility coefficients, and b i > θ. To ensure that the market demand conform to reality, we assume that a i > b i p i , namely p i < ai /bi.

According to the above description, the profit of player i can be written as

The unique Nash equilibrium of Bertrand game is

In this section, the market demand of Bertrand game is posited to be fuzzy. Then, based on credibility theory, a fuzzy Bertrand game model is established to analyze the optimal price strategies of two players. Under a fuzzy environment, both two players desire to pursuit their profits maximum. First, notations and assumptions are used to formulate the model. Second, a fuzzy Bertrand game model is constructed and the equilibrium analysis of this game is conducted.

Notations and assumptions

Notations for the fuzzy Bertrand game model

pi: The player i’s unit sale price, which is the decision variable, pi > 0, i = 1, 2;

ci: The unit cost incurred by player i, c i > 0, i = 1, 2;

Based on the above descriptions, we have the following assumptions. Assumptions

i) According to the demand function of the classical Bertrand game model, we have the fuzzy market demand function

The fuzzy market demand

The parameters

ii) Since the decision variable of the fuzzy Bertrand game is price, the marginal cost c i (i = 1, 2) is assumed to be a constant.

Therefore, the profit function

Given that people always tend to have the behavioral characteristic of risk aversion in the face of gain, in this subsection, we consider a fuzzy Bertrand game where two players are risk aversion. Under a fuzzy environment, α-optimistic value is always used to depict the behavior that the decision-makers are risk aversion, where α denotes the confidence level of players. At a certain confidence level α, two players maximize their α-optimistic value of their profits.

Thus, two players are posited to obey optimistic value criterion. If player 2 choose a price strategy

Similarly, if player 1 choose a price strategy

Then, we define a (α1, α2)-optimistic equilibrium price of the fuzzy Bertrand game.

When player 1 is risk aversion, according to optimistic value criterion and Equations (7) and (12), the profit of the player 1 is

Then,

So, we can have that

Similarly, when player 2 is risk aversion, according to optimistic value criterion and Equations (7) and (12), the profit of player 2 is

To obtain the (α1, α2)-optimistic equilibrium price, it is necessary to solve the following quadratic programming model.

Secondly, taking the second-order derivatives of

So

The first order derivatives of

Let Equation (21) equals to zero, we have

Similarly, taking the second-order derivatives of

So

The first order derivatives of

Let Equation (23) equals to zero, we have

Finally, according to Equation (22) and (24), the (α1, α2)-optimistic equilibrium prices are obtained as follows,

These complete the proof of Proposition 1. □

According to the different range values of the confidence levels α1 and α2, the (α1, α2)-optimistic equilibrium prices of the fuzzy Bertrand game are shown in Table 1.

(α1, α2)-optimistic equilibrium price of the fuzzy Bertrand game

From Table 1, if α1 = α2 = 0.5, then the (α1, α2)-optimistic equilibrium prices of two players are

In China, fixed broadband is an important part of the Telecom industry as well as a representative oligopoly industry. There are two competitive companies in Chinese fixed broadband market, i.e., China Unicom and China Telecom. At present, two companies roughly enjoy 80 percent of the Chinese market for fixed broadband, and are famous for their favorable price and good quality [24]. So, China Unicom and China Telecom are engaged in the Bertrand competition game [5].

Recently, two companies are confronted with many different risks and a cloud of uncertainties. As facing these risks and uncertainties, most companies tend to show the characteristics behavior of risk aversion. To provide some management highlights for managers, the proposed fuzzy Bertrand game model is used to analyze the (α1, α2)-optimistic equilibrium prices of China Unicom and China Telecom.

For convenience, the fixed broadband products of China Telecom and China Unicom are called as product 1 and 2, respectively. The fixed broadband costs of China Telecom and China Unicom are $1 and $2 per unit, respectively. Under a fuzzy environment, the market demand is assumed as a triangular fuzzy variable. The confidence levels of China Telecom and China Unicom are denoted by α1 and α2 respectively. The corresponding fuzzy parameters are shown in Table 2.

Values of triangular fuzzy variables

Values of triangular fuzzy variables

According to the above analysis, there are four cases: If α1 ≤ 0.5 and α2 ≤ 0.5, then we have the (α1, α2)-optimistic equilibrium prices are given by

If α1 ≤ 0.5 and α2 > 0.5, then we have the (α1, α2)-optimistic equilibrium prices are shown as follow

If α1 > 0.5 and α2 ≤ 0.5, then we have the (α1, α2)-optimistic equilibrium prices are given by

If α1 > 0.5 and α2 > 0.5, then we have the (α1, α2)-optimistic equilibrium prices are shown as follow

Sensitivity analysis of the confidence levels

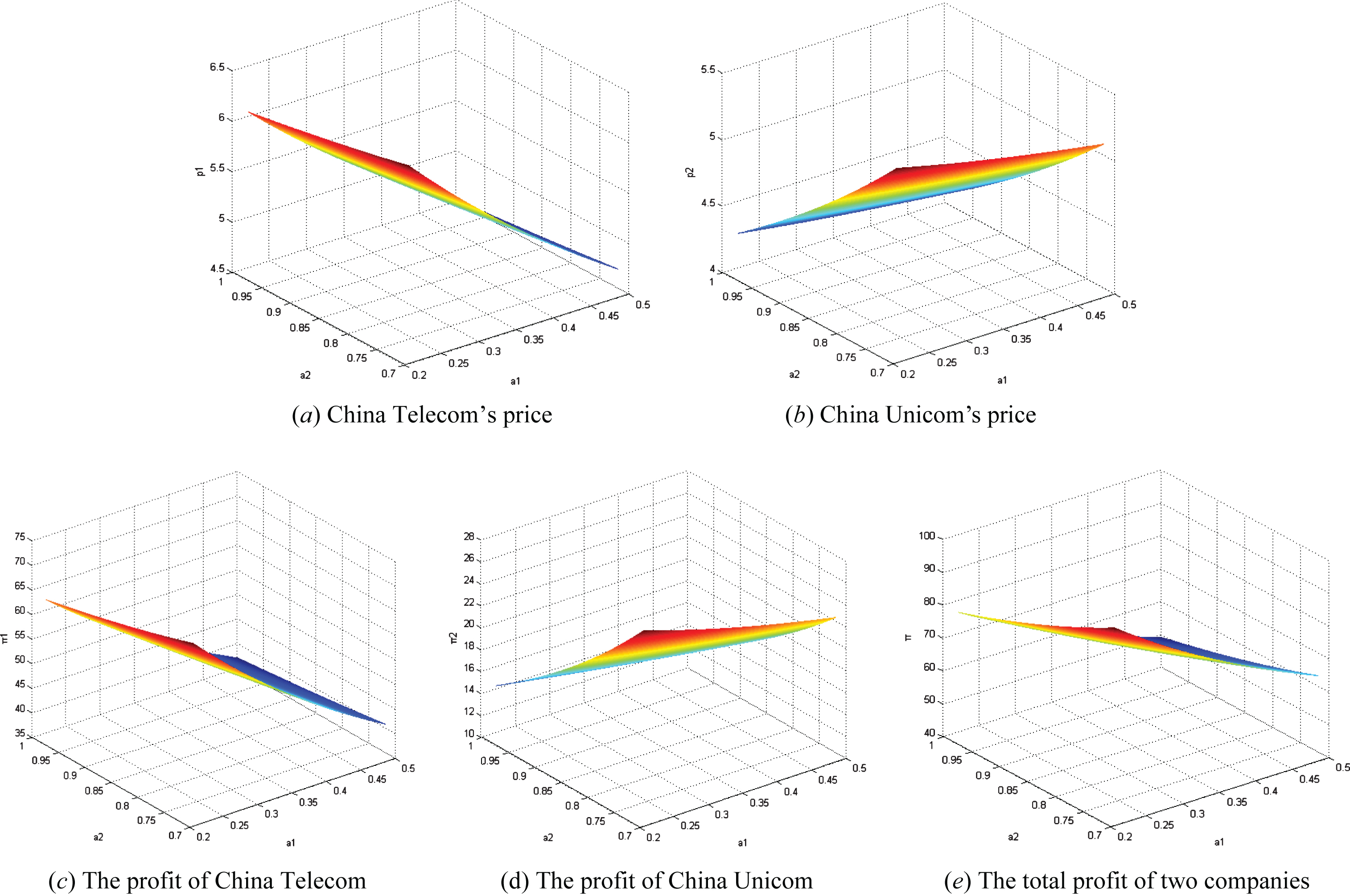

In this section, we explore the effect of confidence levels on the (α1, α2)-optimistic equilibrium prices and maximal profits of China Telecom and China Unicom. First, suppose α1 and α2 are continuous variables with the range of 0 to 1, which reflects the degrees of two companies’ risk aversion. We define that the degree of a company’s risk aversion is low if the confidence level of a company is no more than 0.5 and vice versa. So, in this paper, four situations for sensitivity analysis of companies’ risk aversion degree on (α1, α2)-optimistic equilibrium price and profits are analyzed, including 1) both the risk aversion degree of two companies are low, i.e., α1 ≤ 0.5 and α2 ≤ 0.5; 2) the risk aversion degree α1 of China Telecom is low and the risk aversion degree α2 of China Unicom is high, i.e., α1 ≤ 0.5 and α2 > 0.5; 3) the risk aversion degree α1 of China Telecom is high and the risk aversion degree α2 of China Unicom is low, i.e., α1 > 0.5 and α2≤0.5; 4) both the risk aversion degrees of two companies are high, i.e., α1 > 0.5 and α2 > 0.5. Low risk averse China Telecom and China Unicom (α1≤0.5 and α2≤0.5) In this situation, the (α1, α2)-optimistic equilibrium prices and the profits of two companies are shown in Fig. 1. Since market demand must be positive, the confidence levels of two companies must be in the range of 0.2 to 0.5. Figure 1 shows that as the confidence levels of two companies increase, the prices and profits of two companies and the total profit decrease correspondingly. Moreover, the price and profit of one player decline faster than those of the other player as his own confidence level increases, which implies that player’s price and profit are greatly affected by his own risk aversion. China Unicom’s price is higher than China Telecom’s price. Low risk averse China Telecom and high risk averse China Unicom (α1≤0.5 and α2 > 0.5) In this situation, the results are shown in Fig. 2. Since market demand must be positive, the confidence level of China Telecom must be in the range of 0.2 to 0.5 and the confidence level of China Unicom must be in the range of 0.7 to 1. From Fig. 2, the change of the prices and profits of two companies with risk aversion in the second situation is similar to that in the first situation. However, the prices and profits of both two companies in the second situation are lower than those in the first situation. The profit of China Telecom is higher than that of China Unicom. China Telecom may benefit from his low risk aversion while China Unicom may be hurt by his high risk aversion. High risk averse China Telecom is and Low risk averse China Unicom (α1 > 0.5 and α2≤0.5) In this situation, the results are shown in Fig. 3. Since market demand must be positive, the confidence level of China Telecom must be in the range of 0.7 to 1 and the confidence level of China Unicom must be in the range of 0.2 to 0.5. Figure 3 shows that the changes in this situation are similar to those in the first situation. And, the price and profit of China Unicom are higher than those of China Telecom. China Unicom may benefit from his low risk aversion but China Telecom may be hurt by his high risk aversion. High risk averse China Telecom and China Unicom (α1 > 0.5, and α2 > 0.5). In this situation, the results are shown in Fig. 4. Since market demand must be positive, the confidence levels of two companies must be in the range of 0.7 to 1. Figure 4 shows that the changes are similar to those in the first situation. Moreover, the prices and profits of two companies in this situation are the lowest among the four situations, which means that a high risk aversion of player may hurt himself. The price of China Telecom is lower than that of China Unicom.

The impact of confidence level on the prices and profits of companies (α1≤0.5, α2≤0.5).

The impact of confidence level on the prices and profits of companies (α1≤0.5, α2 > 0.5).

The impact of confidence level on the prices and profits of companies (α1 > 0.5, α2≤0.5).

The impact of confidence level on the prices and profits of companies (α1 > 0.5, α2 > 0.5).

Comparing with the four situations, we can obtain the following conclusions. The prices and profits of companies in the first situation are the highest among the four situations, while the prices and profits of two companies in the last situation are the lowest. A higher risk aversion leads to a lower price and a lower profit. If two companies are lower risk averse, they may raise their prices to obtain more profits. Meanwhile, if two companies are higher risk averse, price competition between companies is more furious, and they may cut their price to attract more customers. Therefore, a risk averse player may benefit from his low risk aversion but be hurt by his high risk aversion. Moreover, the price of a player with lower risk aversion and higher cost is higher than that of a player with a higher risk aversion and a lower cost, while the price of a player with a higher risk aversion and a higher cost may be lower than that of a player with a lower risk aversion and a lower cost. The price and profit of a player are more greatly affected by his own risk aversion than the other player’s risk aversion.

In this section, we contrast the findings of our study with the results of Zhao et al. [50] and Wei and Zhao [44], who studied the pricing problem of substitutable products in a fuzzy supply chain with one retailer and two manufacturers. We use optimistic value criterion to model risk aversion of players and explore how the prices and profits change when players are risk averse in a fuzzy Bertrand game. We find that the increased risk aversion of players leads the prices and profits of the fuzzy Bertrand game to decline. However, Zhao et al. [50] and Wei and Zhao [44] adopted expected value criterion to analyze the effect of the fuzziness of market demand on the prices and expected profits, and found that the prices and expected profits of two manufactures are decreasing with the fuzziness of marked demand. There is no contradiction between our study and these two papers mentioned. In a fuzzy environment, the prices and profits of players may be affected by the fuzziness of market demand and risk aversion. Player with a lower risk aversion may prefer the upper limits of the fuzzy market demand and player with a higher risk aversion may prefer the lower limits of the fuzzy market demand. Therefore, combining our study and the works of Zhao et al. [50] and Wei and Zhao [44], both the fuzziness of market demand and the risk aversion of players may decline the prices and profits.

Conclusions

In this paper, we consider a Bertrand game between two players with two substitutable products under a fuzzy environment. The market demand for each product is posited as a triangular fuzzy variable. A fuzzy Bertrand game with risk aversion is investigated. Optimistic value criterion is applied to formulate risk aversion of players. The (α1, α2)-optimistic equilibrium prices of the fuzzy Bertrand game are analyzed. The results show that risk aversion of players has an important role in the price decisions of a fuzzy Bertrand game. First, a higher risk aversion leads to a lower price and profit. Therefore, a risk averse player may benefit from his low risk aversion but be hurt by his high risk aversion. Second, the price of a player with lower risk aversion and higher cost is higher than that of a player with a higher risk aversion and a lower cost, while the price of a player with a higher risk aversion and a higher cost may be lower than that of a player with a lower risk aversion and a lower cost. Finally, the price and profit of a player are more greatly affected by his own risk aversion than the other player’s risk aversion. This paper may offer a managerial insight into price competition for both theoretical researchers and practical practitioners.

For future research, an n-person fuzzy Bertrand game can be discussed; on the other hand, the degree of players’ risk aversion may be private information, so this game should be in a condition where player has no ideal of the other player’s risk aversion.

Footnotes

Acknowledgments

This research is supported by National Natural Science Foundation of China (Nos. 71671188, 71571192, and 71271217), the state key program of NSFC (No. 71431006), Natural Science Foundation of Hunan (No. 2016JJ1024) and the Postgraduate Innovation Project of Central South University (2017zzts048).