Abstract

Current accounting methods for small and medium-sized enterprises (SMEs) have long running times and low user satisfaction. Therefore, a method for the selection of accounting models for

Keywords

Introduction

Current accounting methods are based on the generation and development of traditional data environments [1]. However, big data is having a huge impact on today’s global economy, and it has also caused setbacks to traditionally-developed accounting models. With the continuous emergence of relevant data, accounting market big data (

Ding Shenghong analyzed the general characteristics of “Internet Plus” from the perspective of human rights in [4]. Its impact on the transformation of property rights to human rights was obtained. According to Maslow’s Hierarchy of Needs, the choice of measurement method for human capital accounting confirmation is explored as one of the human rights accounting products in the era of “Internet Plus”. There are two alternative hypotheses of completely low-level demand and high-level demand, human capital accounting of their respective human rights accounting reporting modes. Under the above assumptions, Shenghong summarizes the exploration of human capital accounting infrastructure theory. The process is simple; however, user satisfaction from the process is low.

The current “three phases of superposition” in China, the “new normal” and the scientificconnotation of the grim situation at home and abroad are explained by Liu Jinbin in [5]. The new requirements of the “new normal” on corporate environmental accounting information disclosure are revealed. Using the “four comprehensive” elements of strategic thinking, meanwhile, relying on the state to promote the national governance system and the modernization of governance capabilities, different disclosure models in different companies based on the comprehensive classification of enterprises are proposed. The method discloses different environmental accounting information and accepts the construction of information disclosure modes of environmental accounting enterprises with different regulatory requirements. This method has a high operating efficiency; however, the rationality coefficient is low.

Tang Mei proposes that the tea market in the Central Plains Economic Zone is becoming more competitive [6]. If tea production enterprises are to gain a foothold and develop in such a fierce market, Mei claims, they must rely on and adopt more scientific and effective management methods. Furthermore, cost accounting is an important part of the production, operation, and management of tea companies. Tea companies can understand their own production and operation conditions and the dynamic needs of the tea market in a timely manner by accounting for costs in production and operations. This can help enterprises to achieve the optimal allocation of resources and rational use of tea production and operation, so as to obtain the benefits of growth. Combining the status and characteristics of tea production and operation as well as cost accounting, in the significance of tea enterprise value growth, Mei analyzes and discusses how to solve some cost accounting problems in tea production and management. Therefore, the method is more specific in its operation process. However, its operating efficiency is lower than other methods.

Big data is diverse and unstructured, and is difficult to store, process and mine [7]. It also exhibits a large size, multiple data types, fast propagation speed, authenticity, strong understanding, and strong innovation. Here, the choice of accounting model is explored based on characteristics of Several representative indicators are selected to establish a market-based constraint system for ( A combination of particle swarm optimization and ant colony optimization is used to select the optimal accounting model for small and medium-sized enterprises to improve selection rationality and user satisfaction. The selection method of The proposed method is summarized, and future research directions are proposed.

The choice of accounting models for small and medium-sized enterprises under the constraints of accounting big information market data

Principles of accounting model selection

Principle of the rational division of labor A reasonable division of labor means that any relevant work is divided into several processing steps to be completed by different people, which prevents anyone from completing the accounting process alone. Therefore, by this principle, the entire process of any economic business should be divided amongst two or more people. For example, a business should not have one person be responsible for accounts receivable as well as shipping, or else errors will surface in the work. The principle of separation of money and goods Money management and property management are required in the principle of separation of money and goods. This means that management and accounting staff responsible for money and goods should be completely dispersed, and accounting should not be both accountable and managed. Principles of inspection The principle of inspection includes the procedure for the superior to verify the lower level review, internal review, and independent inspection. The internal review refers to the accounting documents of the financial institution. When accounting documents are filled out, they must be submitted to an accountant for review before the cashier can make a payment or register a transaction. Independent inspection mainly refers to the regular inspection of accounting materials by internal audit institutions or full-time auditors. Principle of economic responsibility Under this principle, when there is a problem in filling out accounting vouchers, it must be submitted to the accountant for re-examination and the view before payment or registration. Trading

Establishment of accounting Big information market data constraints

The information market refers to the complete exchange relationship between the information product producers, the information service operators and the information product demanders in the market. It covers the entire distribution and exchange process, and the circulation of commoditized information products from production to consumption. Specifically, the information market is a multi-faceted, multi-level, multi-form market system which meets the needs of social information, using information products and information services like content and using information labor law to conduct transactions [11].

On the basis of the principles of comparability, completeness, accessibility, non-overlapability, etc., we refer to the relevant literature and combine the status quo of

Among them, the solvency ratio is the basis for responding to the growth of

The ratio of operational capacity is an indicator reflecting the growth level of

The index of profitability is a decisive indicator reflecting the growth of

Enterprise development ability is a fundamental part of the growth of

Principal Component Analysis (

In essence, principal component analysis is a statistical analysis method that converts multiple variables into a few comprehensive indicators. From the perspective of mathematics, this is a dimensionality-reduction processing technique that can improve the efficiency of accounting choices for small and medium-sized enterprises. Assume that there are n samples, each of which has a total of p variable descriptions. This forms an n × p-order data matrix. p-dimensional random vectorx = (X1, X2, ⋯ , X

p

) · n samples x

i

= (xi1, xi2, ⋯ , x

ip

), i = 1, 2 ⋯ , n. The accounting big information market data constraint standard function can be expressed as Equation 1.

According to Eq. 1, the following correlation coefficient function R can be solved.

Assuming 86% utilization of accounting big data information, Eq. 3 can be obtained.

In Eq. 3, λ j represents the utilization of accounting big data information.

For λ

j

, there is a system of equations R = λ

j

, then according to the equation, the unit eigenvector

In Eq. 4, U1 is called the first principal component, U2 is called the second principal component, and so on, so that U p is called the pth principal component.

Conventional cluster analysis methods can be adopted for cluster analysis of the constraint factors of

Assume that the distance between the projection point of a test sample in the feature space and the center point of the point group is y

i

. The following formula to completes the SME AMBD cluster analysis.

In Eq. 6, y

i

is the clustering result of the

The above process’ main purpose is to roughly divide the constraint factors of the

Ant colony optimization (

Particle swarm optimization (

Based on the

The ant colony representing particle swarms with different combinations of accounting models is initialized. The position and velocity of the particles are denoted as The fitness values for all particles is calculated based on the fitness function in Eq. 7.

In Eq. 7, w1, w2, w3 and w4 represent weights, and qi′j′, ui′j′, ci′j′, ti′j′, and ri′j′ represent different accounting models, respectively. The fitness value of each particle is compared with the fitness value of the best position The fitness value of each particle is compared with the fitness value of the global best position g

best

= (gi′1, gi′2, ⋯ , gi′m). If it is larger, g

best

is reset. The particle velocity and position are updated by using Equations 8-9.

In Eqs. 8-9, C represents the learning factor, After updating the particle velocity and position, it is judged whether or not the algorithm end condition is satisfied. If the assumption is satisfied, the end condition is considered to be satisfied. Otherwise, the process is repeated from step 2.

According to the fitness function of the chromosome in the population selected by the above particle swarm algorithm, all possible paths between candidate accounting models τ (·) are set up based on the ant colony algorithm for SME accounting model selection model diagrams, using the expression shown in Eq. 10.

In Eq. 10, τ (e, l)

new

represents the updated path, τ (e, l)

old

represents the current path, and Δτ (e, l) k′ represents the amount of pheromones released after the k′-th ant passes the accounting mode e and the accounting mode l. The search iteration G is set to 1 and the optimal objective function value Fmax is set to 0. An ant is placed on each candidate accounting model, and n′ is defined as the total number of ants. The initial solution set and feasible set for each ant is defined. Assuming that the starting point of ant k′ is u1, the initial solution set is tabuk′ ={ u1 }, and the initial feasible set is allowedk′ ={ u2, ⋯ , u

m

}. The probability In Eq. 11, η represents the inertia factor, After n moments, a search is traversed and completed by all ants. Then, the amount of information on all paths is updated by Eq. 10, and G is incremented by 1. The above process is iterated until the most suitable accounting model is selected. The expression to select the best accounting model is defined by Eq. 12.

In Eq. 12, Fmax is the finally selected accounting model.

In the realization of accounting mode selection for

To verify the feasibility of the selection method of the Mode rationality Mode selection user satisfaction Mode selection efficiency

The experimental results are as follows.

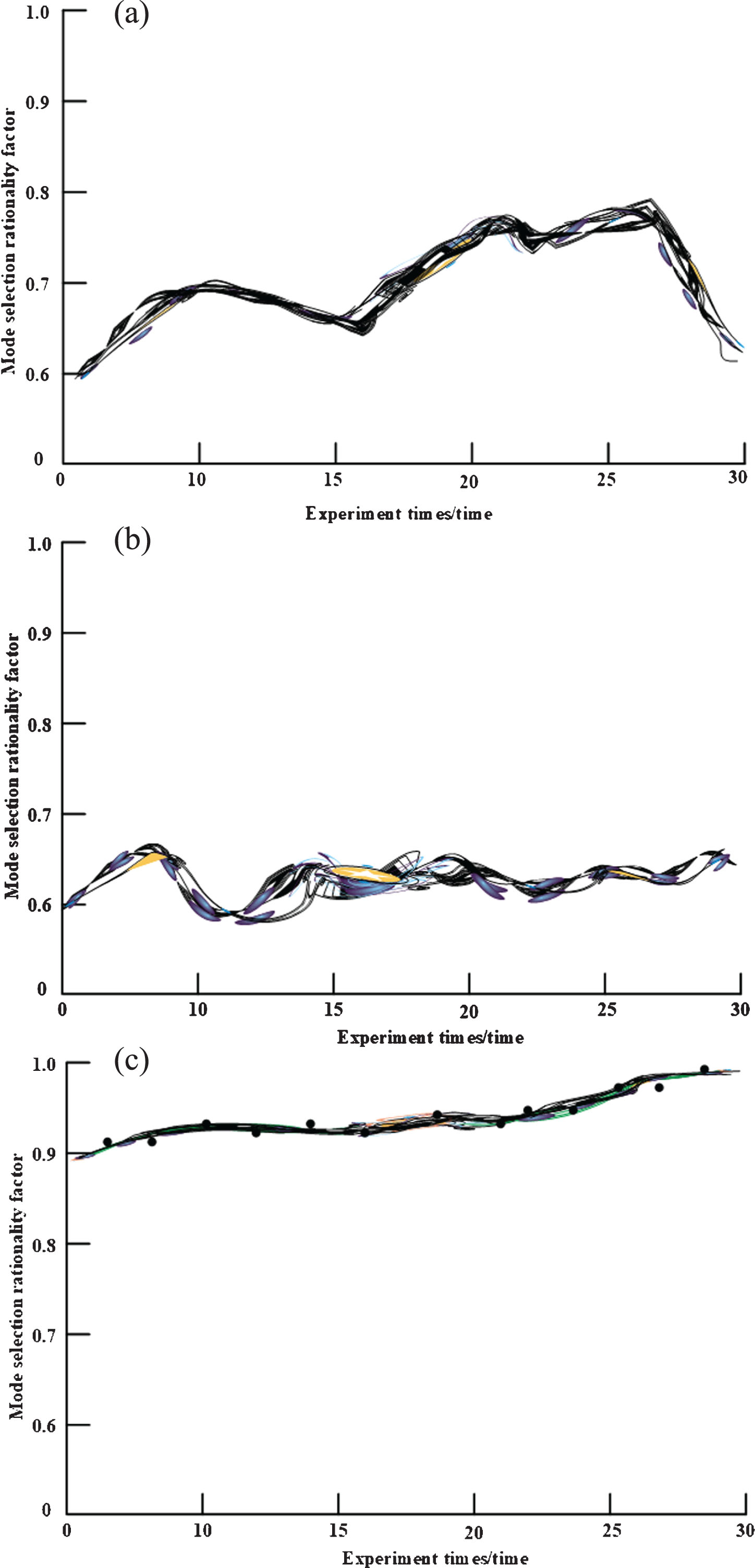

Fig. 1 shows that the stability curve of method 1 is less stable. Method 2 proposes a strategy based on a comprehensive classification of enterprises and different companies adopting different disclosure models to achieve a choice of accounting models. The process does not analyze the specific financial indicators of each company, and the division of the classification results is not clear, leading to poor rationality. When the choice of accounting model is based on the constraints of the

Comparison of rationality for different methods. (a) Method 1, rationality. (b) Method 2, rationality. (c) The rationality of choice of an accounting model for SMEs based on AMBD.

Fig. 2 shows that the choice of

Comparison of user satisfaction for different methods. (a) Method 2, User Satisfaction. (b) Method 1, User Satisfaction. (c) User satisfaction based on the selection method of accounting mode for SMEs under accounting big information market data.

Fig. 3 shows that the method of selecting an accounting mode is to substitute the

Comparison of operating efficiency for different methods. (a) Method 2, operating efficiency. (b) Method 3, operating efficiency. (c) Operation efficiency of the selection method of accounting mode for SMEs based on AMBD.

The choice of accounting model is very important. If

Conflicts of interest

We declare that there are no conflicts of interest in this paper.

Footnotes

Acknowledgments

The study was supported by “Social Science Foundation of Fujian Province of China (Grant No. FJ2018C037)” and “Education and Scientific Research Project for Young Teachers in Fujian Province of China” (Grant No. JAS170344). We also thank Logan Praznik for his thorough editing work.