Abstract

In a complex financial market, people pay more attention to the portfolio selection model in some fuzzy environment. Some properties and definitions of semivariance and entropy are given and proved in this paper. Then, the fuzzy tri-objective mean-semivariance-entropy portfolio model is proposed based on credibility theory when the return rates are fuzzy numbers. We present a novel layer-by-layer tolerance evaluation method to solve the proposed model in this paper. Finally, a numerical example is given to illustrate the effectiveness of the model and method proposed in this paper. There are two improvements in our proposed method: one is that the evaluation function idea is considered in the process of laying objective functions; the other is that the preference degree and subjective wills are presented by tolerant amounts of objective function values.

Introduction

The fundamental goal of the portfolio is to help the investor to allocate money among different financial securities in certain some “optimal” way [1]. In the classical Markowitz’s mean-variance model [2], the selection is guided by a quantitative criterion that considers a tradeoff between the return and risk of the investment. When the return rates are random variables, the traditional mean-variance model is proposed with the known expected mean and covariance matrix. The portfolio selection problem usually has two criteria: to maximize the expected return (profit) and to minimize the risk. The optimal solution of the portfolio model depends on the investor’s risk aversion. As it is often difficult to weigh the two criteria (return and risk) before the alternatives are known, it is common to search for the whole set of efficient or Pareto-optimal solutions, i.e., all solutions which cannot be improved in both objectives simultaneously. This set of solutions is often called “efficient frontier” or “Pareto-optimal frontier” [3].

Markowitz published his work that paved the foundation of modern portfolio theory. It combines probability and optimization theory to model the behavior of economic agents under some uncertainties. The mean-variance approach has also been subjected to a lot of criticisms [4]. One of the most important reasons is the computational difficulty associated with solving a large-scale quadratic programming portfolio problem. Besides, there are many different risk measurements in the real financial market such as Value at Risk, semivariance, and entropy. For example, Konno and Yamazaki [5] used absolute deviation risk function to replace the risk function in Markowitz’s model.

The estimation of uncertain quantities is important in decision making [6]. In order to represent uncertainty in a financial model in this paper, we regard return rates as fuzzy variables which have two kinds of uncertainties, i.e., randomness and fuzziness. Randomness is applied to the uncertainty regarding the belief degree of frequency, and fuzziness is applied to the linguistic imprecision of data because of a lack of information regarding the current stock market. Because of the information incompleteness and the complexity of a financial market, it is impossible to precisely predict the future return and the actual risk of a portfolio [7]. In order to quantify vagueness in the real life, Zadeh [8] introduced the concept of fuzzy set. Carlsson and Fuller [9] presented the notation of interval-valued possibilistic mean value of fuzzy numbers. Fuller and Majlender [10] defined a weighted interval-valued possibilistic mean. Fuller and Majlender [11] proposed the concept of possibilistic covariance. Carlsson, Fuller and Majlender [12] proposed the concept of possibilistic correlation. Carlsson, Fuller and Majlender [13] assumed that the return rates could be presented as possibility distributions rather than probability distributions. Bellman [14] studied decision making theory in a fuzzy environment and Liu [15] introduced the credibility theory. Many researchers studied portfolio models when the returns are considered as fuzzy random numbers based on credibility theory. Ramaswamy [16] presented a portfolio selection method using the fuzzy decision theory. Deng [17] proposed a fuzzy portfolio model with borrowing constraint based on possibility theory. Huang [18] did some research work on fuzzy portfolio models. Mehlawat [19] considered that credibilistic entropy of the fuzzy returns as a measure of the portfolio risk. Yue [20] proposed a new entropy function based on Minkowski measure. Within the framework of credibility theory, Guo [21] formulated a mean-variance model with the objective of maximizing the terminal return under the total risk constraint over the whole investment.

Another hottest topic is how to solve the portfolio models. In the past, many researchers presented different solving methods. For example, Amelia [22], Deng [23] and Zhang [24] used programming methods such as linear programming and goal programming methods to solve these proposed models; Chang [25], Chang [26] and Xiang [27] used intelligence algorithms such as genetic algorithm and particle swarm optimization algorithm to solve these portfolio models; Deng [28] used strictly mathematical proof method to solve the model. Kalayci [29] presented an efficient solution approach based on an artificial bee colony algorithm with feasibility enforcement and infeasibility toleration procedures for solving cardinality constrained portfolio optimization problem; Saborido [30] proposed new mutation, crossover and reparation operators for evolutionary multi-objective optimization. In this paper, we use the semivariance and entropy to measure the risk. Therefore, the tri-objective mean-semivariance-entropy model is built up. In our work, considering the investor’s subjective will and the importance of the objective function, we present a novel approach: layer-by-layer tolerance evaluation method that is applied to solve our proposed model.

The rest of this paper is organized as follows. In Section 2, we introduce credibility theory, expected mean, semivariance, entropy and some corresponding properties. In Section 3, the fuzzy tri-objective mean-semivariance-entropy model is proposed. The basic ideas and computation steps of layer-by-layer tolerance evaluation method are proposed to solve the model in Section 4. In Section 5, a numerical example is used to illustrate the model and method through a case study on stocks. Finally, concluding remarks are presented in Section 6.

Preliminaries

Credibility theory

The concept of fuzzy set was initiated by Zadeh [8] by membership function in 1965. In order to measure a fuzzy set, Zadeh [8] proposed the concept of possibility measure in 1978. Although possibility measure has been widely used, it does not obey the law of truth conservation, and it is inconsistent with the law of excluded middle and the law of contradiction [15]. The main reason is that possibility measure has no self-duality property. However, a self-dual measure is absolutely needed both in theory and in practice. As an alternative measure of a fuzzy event, Liu [15] defined credibility measure. The important characteristic of credibility theory is self-dual. When the credibility value of a fuzzy event achieves 1, the fuzzy event will surely happen. Therefore, in this paper, we adopt credibility as the measure of occurrence chance of a fuzzy event [31].

In credibility theory, there are three fundamental concepts. The first fundamental concept is uncertain measure that is used to measure the belief degree of an uncertain event. The second one is uncertain variable that is used to represent imprecise quantities. The third one is uncertainty distribution that is used to describe uncertain variables in an incomplete but easy-to-use way. In the real life, the fuzziness is deeper than the randomness of uncertainty. The existence of fuzziness is more extensive and more important than the existence of randomness. In the practical financial market, the return of the portfolio is an uncertain variable, and thus, it is suitable to describe the return rate by a fuzzy number.

This above formula is also called the credibility inversion theorem by Liu [10]. Conversely, if ξ is a fuzzy variable, then its membership function is derived from the credibility measure by

Expected value is the average value of an uncertain variable in the sense of the uncertain measure, and represents the size of the fuzzy variable.

In fact, the expected value is a finite integral of one variable. If the integral result exists, effective expected value exists, too. Otherwise, the effective expected value doesn’t exist.

This section provides a definition of entropy to characterize the uncertainty of fuzzy variable resulting from information deficiency.

Fuzzy entropy is used to measure the uncertainty associated with each fuzzy variable. If ξ has continuous membership function μ, then we have

By the formula Cr { ξ ≤ x } + Cr { ξ ≥ x } = 1 and the credibility inversion theorem, we have

In the portfolio selection problem, since uncertainty causes loss, we use entropy to measure the risk degree of a portfolio. Uncertainty causing loss is defined as the “accidental loss” plus the “uncertain measure of such loss”. Then how to measure the kind of loss? Liu [31] uses “risk index” to be the measure index. A system usually contains uncertain factors, for example, lifetime, demand, production rate, cost, profit, and resource. Risk index is defined as the uncertain measure that some specified loss occurs. Note that the loss is problem-dependent. In the special case, V S [ξ] =0 ⇔ Cr {ξ = e} =1 where the investor has no idea at all about the portfolio return, he/she will have no preference among insight into all the values that the fuzzy portfolio return will take. Thus, the portfolio return can be regarded as an equipossible fuzzy number, which means the fuzzy variable is fully determined by the pair (a, b) of crisp numbers with a < b, and membership function is given by μ (x) =1, a ≤ x ≤ b. The entropy of the portfolio return reaches its maximum, which means that the uncertainty of the portfolio is maximal and the portfolio is a most risky one (see Liu [31] and Huang [33]). To use entropy as the measure of risk, we need not assume that membership functions of security returns are symmetrical.

Markowitz in [1, 2] proposed the well-known M-V portfolio model, and his principle for selecting the optimal portfolio was maximizing investment return for a preset level of risk, or minimizing investment risk for a preset level of investment return in a random environment. In his portfolio model, the expected return is used to measure the investment return and the variance of return is used to measure the investment risk.

In this paper, we build up a tri-objective portfolio model by maximizing the expected value (return), minimizing the semivariance (risk), and minimizing the entropy (risk). Let x

i

be the proportion of total funds devoted to the i - th asset;

According to formulae (3), (4) and (6), we obtain the following tri-objective mean-semivariance-entropy portfolio model:

The ideas of layer-by-layer tolerance evaluation method

Now consider the priority stratifying programming problem

(i) If many objective functions are concluded in P1-layer, we select some evaluation method to solve the following multi-objective programming problem

(ii) If only one objective function is concluded in P1-layer, we use linear programming or non-linear programming method to solve the following minimizing programming problem

Assume r : =2, and turn to Step 2.

In order to obtain the ideal objective point

Then turn to Step 3.

(i) If the P r -layer contains many objective functions, then select some appropriate evaluation function method to solve the following problem

Assume the preferred solution is

(ii) If the P

r

- thlayer contains only one objective function, we use some numerical optimization method to solve the following problem

Assume the optimal solution is

If r < L, assume r : = r + 1, turn to Step 2. If r = L, output the solution

In this section, a real portfolio selection example is illustrated to verify the effectiveness of the proposed model and method. In this example, our tri-objective mean-semivariance-entropy model is applied to the practical data, which is composed of membership functions of seven security returns. The fuzzy returns of the seven securities and corresponding expected values and entropies are showed in Table 1. According to model (17) and the data in Table 1, the corresponding return of the portfolio is ξ = ξ1x1 + ξ2x2 + ⋯ + ξ7x7, l i = 0.05, u i = 0.8, we can build up the following tri-objective fuzzy mean-semivariance-entropy portfolio model:

Fuzzy returns of 7 securities and corresponding expected values and entropies (units per stock)

Fuzzy returns of 7 securities and corresponding expected values and entropies (units per stock)

For convenience of computation, model (25) is transformed into the following model:

And the model (26) is equivalent to the following tri-objective minimizing programming model:

First, model (27) is solved by linearly weighted method of Chang [25]. The above model (27) is written as

Where objective functions f1, f2, f3 are the same as those in model (27). Select λ, μ as the preference parameters of f1, f2, then the model (28) is transformed into model (29) using linearly weighted method:

There is only one solution when parameters λ, μ are fixed. For example, when λ = 0.5, μ = 0.3, the optimal solution is

The corresponding values of objective functions are

Namely, the expected mean, semivariance and entropy are 1.49250, 0.70339 and 1.40500.

Next, model (27) is solved by layer-by-layer tolerance evaluation method proposed in this paper. According to the investor’s preferences of each objective function, the expected mean and semivariance are regarded as the first priority layer problem, and the fuzzy entropy is considered as the second priority layer problem. The computation steps of layer-by-layer tolerance evaluation method solving model (27) are as follows.

Next, we use the maximum target value evaluation method to solve the layer problem:

(i) Objective function normalization. Select the normalized interval [0,1]. We have the minimal and maximal values for every objective function:

Obtain the normalized objective function:

(ii) Normalize weighted objective functions. According to the importance of objective function in the problem, the investor assumes that the weighted coefficients are w1 = 0.6, w2 = 0.4. Therefore, obtain the normalization objective functions 0.6φ1, 0.4φ2.

(iii) Now, solve the following problem:

We introduce the auxiliary variable λ and let

Therefore, the problem (33) is transformed into the following equivalent linear programming problem:

That is,

We have the optimal solution of model (38):

Then, obtain the preference solution of the P1-layer problem:

Then, turn to Step 2.

Now, the investor thinks that he/she can make some concessions Δ1 (⩾0) for the expected mean (return) and Δ2 (⩾0) for semivariance (risk). Then, construct the next layer constraint set with tolerance constraint conditions:

When Δ1 = 0.08, Δ2 = 0.04, we have

Then turn to Step 3.

Different optimal solutions and different objective function values as to different tolerant mounts of Δ1, Δ2

It is easy to obtain the optimal solution of model (43):

L = 2, therefore the solution

We obtain the corresponding objective function values:

According to different tolerant mounts of Δ1, Δ2, we can obtain different optimal solutions and different objective function values of Table 2.

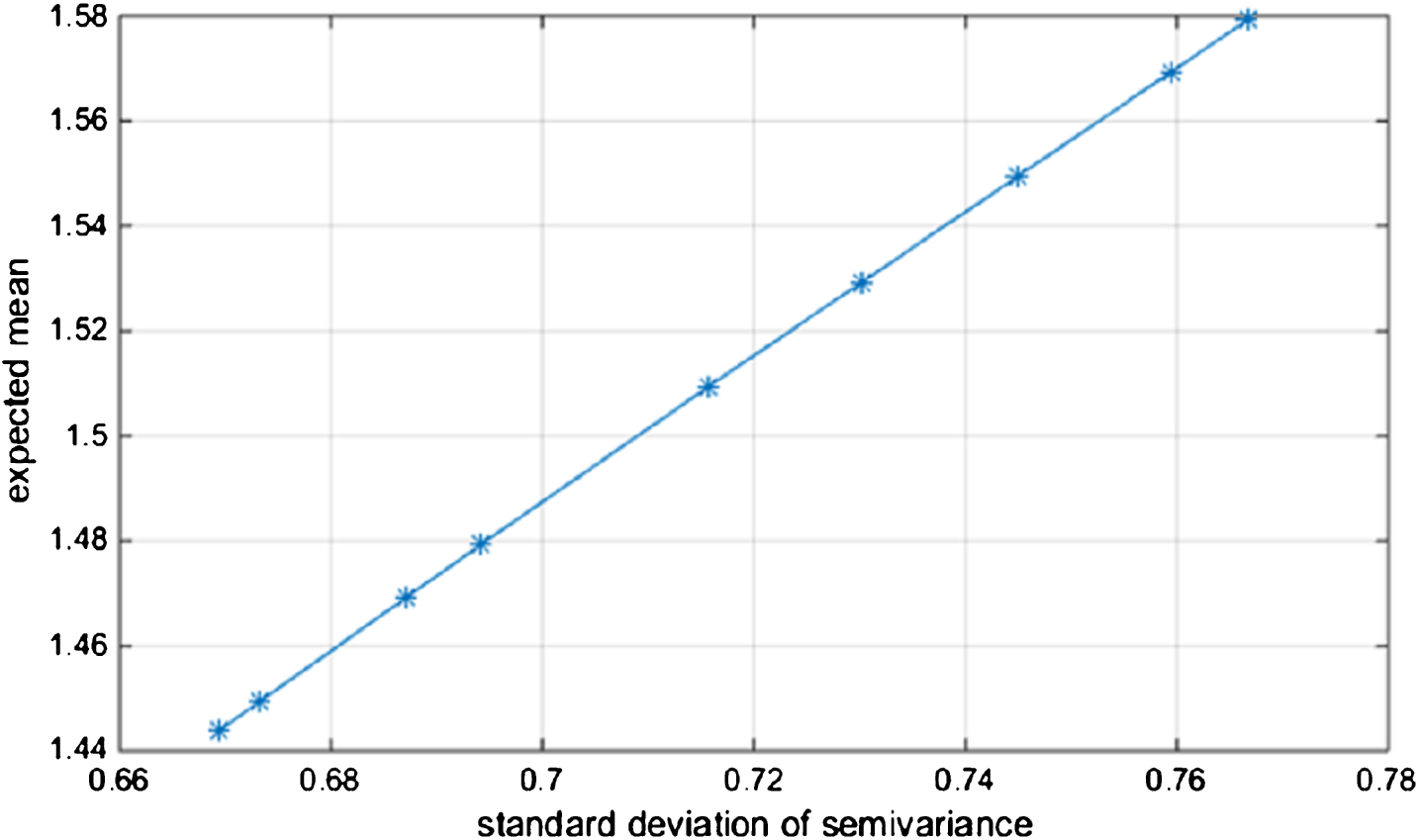

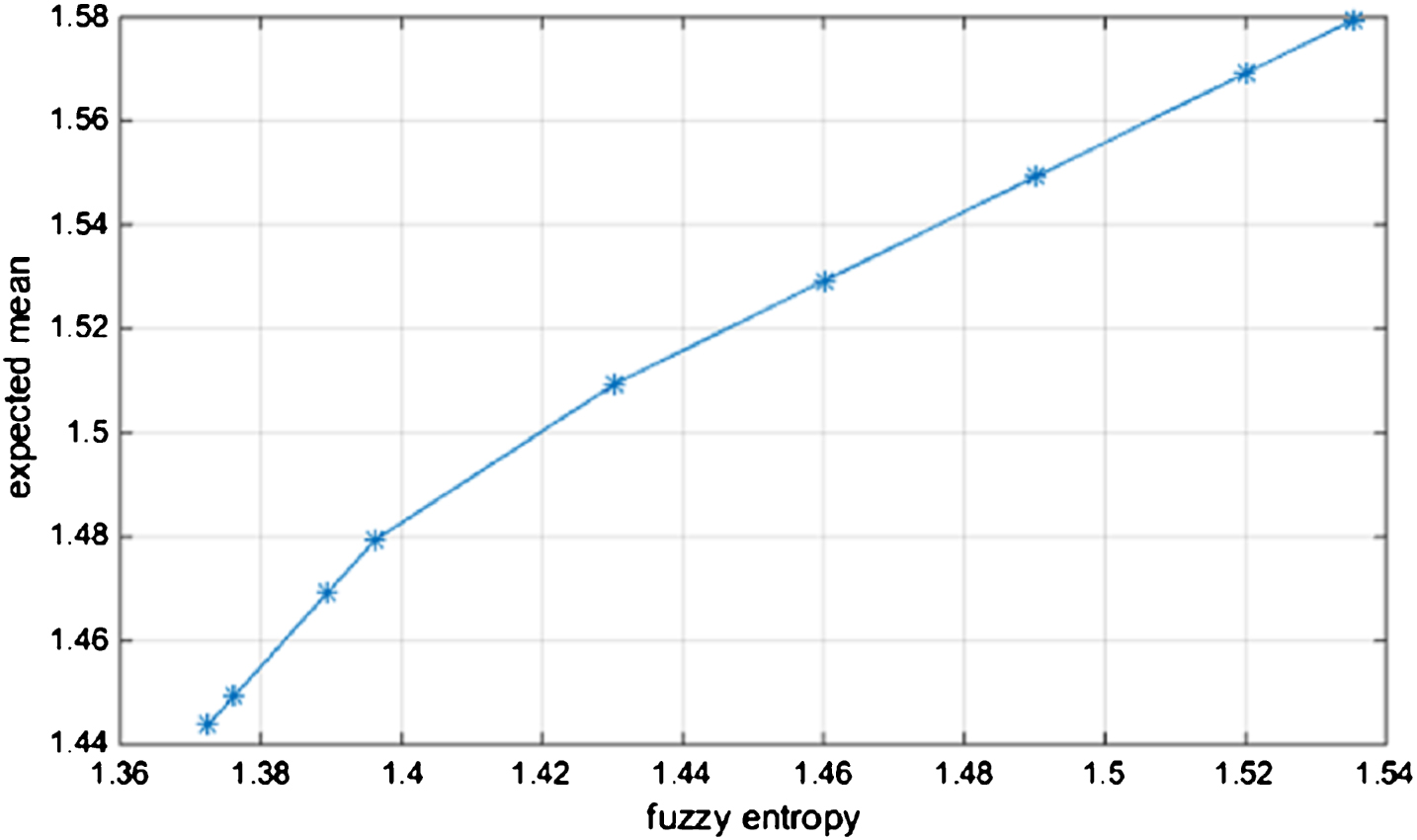

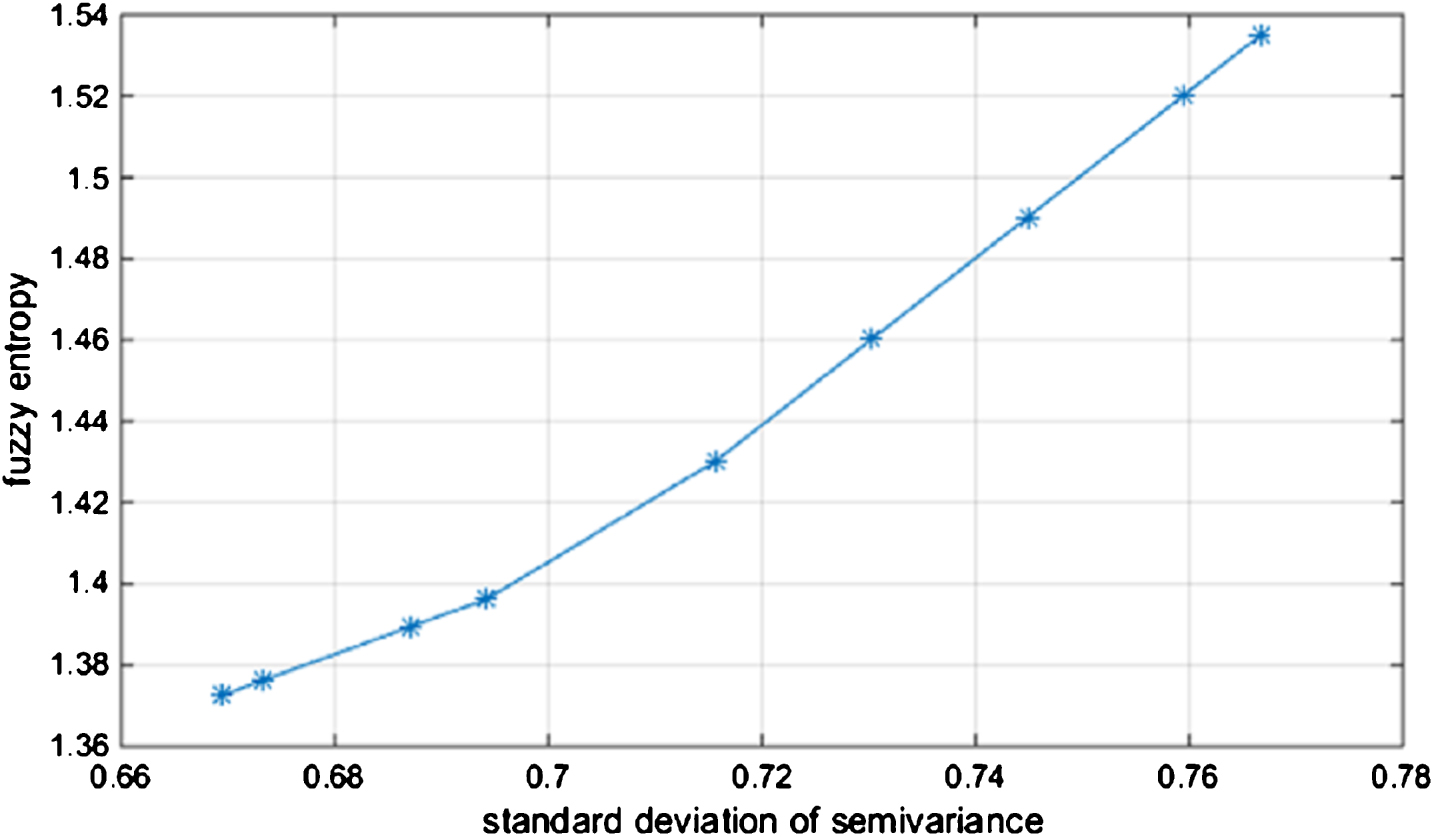

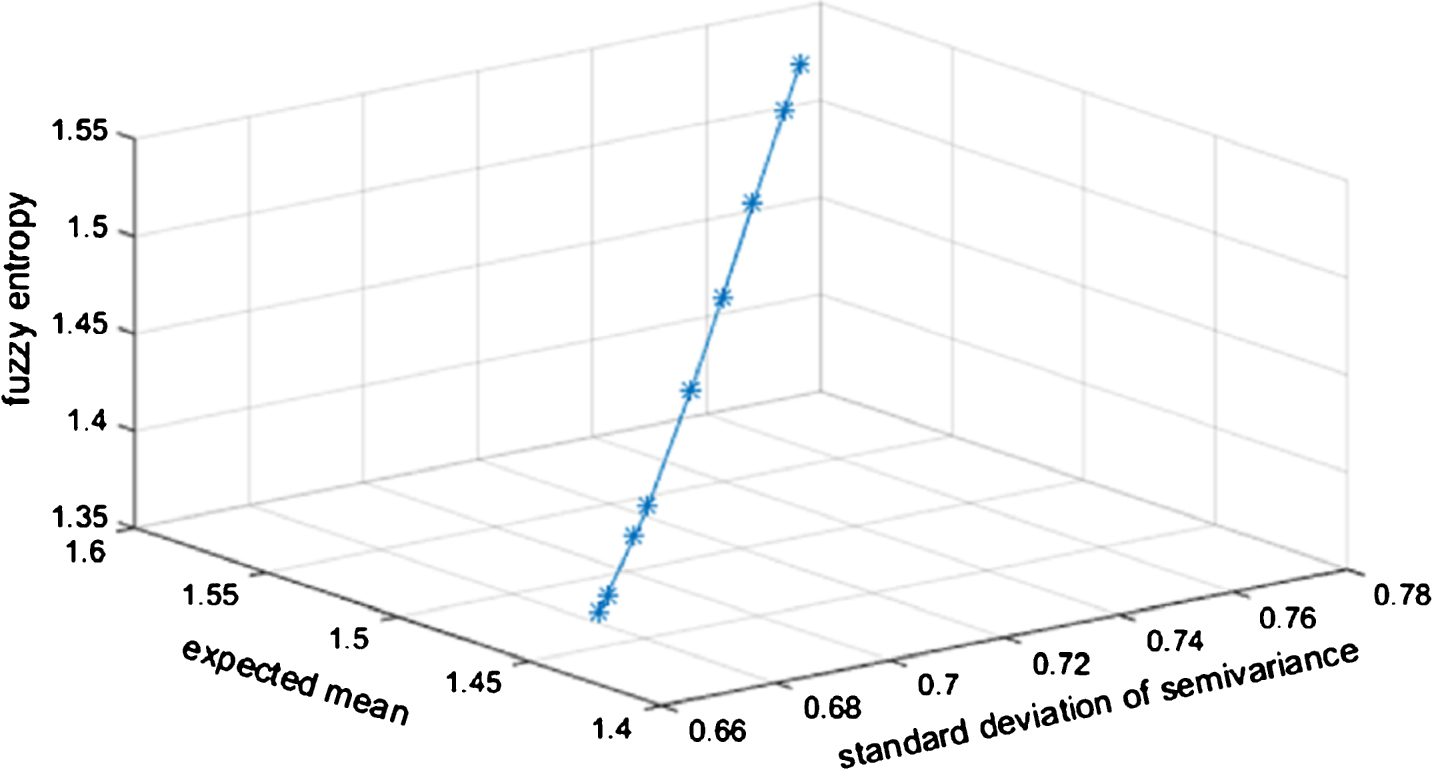

From the data of Table 2, we can find the following facts: The tolerant amounts are different., and the corresponding optimal solutions and objective function values are also different. The bigger the summation of the amounts Δ1 + Δ2 is, the lager the expected mean becomes, the smaller the semivariance is, the lower the fuzzy entropy becomes. The more summation of the tolerant amounts means that the investor can make more concessions for the expected mean and semivariance, which means investor can obtain the least return, and of course the investor can obtain the least risk (semivariance and fuzzy entropy). When Δ1 = 0.24, Δ2 = 0.16 and Δ1 = 0.30, Δ2 = 0.16, the optimal solutions are the same, and of course, the objective function values are the same, which means that when the expected mean reaches the minimum value. Namely, the change of tolerant amounts summation can not make any change for the optimal solution. According to the data of Table 2, we can obtain the effective frontiers as follows in Figs. 1–4.

In Figs. 1–3, the effective frontiers are increasing functions, which means the more standard deviation of semivariance, the more expected mean; the more fuzzy entropy, the more expected mean; the more standard deviation of semivariance, the more fuzzy entropy. These facts are consistent with the financial market practical regulations. The three-dimensional effective frontier of Fig. 4 effectively shows the above second fact that the semivariance and fuzzy entropy are decreasing with the decrement of expected value.

According to Section 5.1 and Table 2, we can obtain different optimal solutions by linearly weighted method and our proposed layer-by-layer tolerance evaluation method in Table 3.

The optimal solution obtained by different methods

The optimal solution obtained by different methods

From the data of Table 3, we can find the fact: compared with linearly weighted method (there is only one optimal solution) for the same model (27), our proposed method can offer several groups of solutions according to investors’ different tolerant mounts of objective functions, which reflects the investors’ subjective preferences for objective functions. We will care more investor’s subjective will in a complex financial market.

The effective frontier of standard deviation of semivariance and expected mean in model (27).

The effective frontier of fuzzy entropy and expected mean in model (27).

The effective frontier of standard deviation of semivariance and fuzzy entropy in model (27).

The effective frontier of standard deviation of semivariance, expected mean and entropy in model (27).

When the return rate is a triangular fuzzy number, we use the expected mean to measure the portfolio return and use semivariance and entropy to measure the portfolio risk. We propose a tri-objective mean-semivariance-entropy portfolio model. The important work of this paper is how to solve the proposed tri-objective model and how to make concession according to the investor’s subjective will and preference for objective functions. We propose a novel layer-by-layer tolerance evaluation method. According to the investor’s subjective preferences, the objective functions are stratified. On one hand, if there is more than one objective function in some layer, the investor uses max-min evaluation method to find the preference solution. On the other hand, our proposed method pays more attention to the objective function and the investor’s subjective will, which is more reasonable and more effective in practical financial market. One natural extension of this work is the application of layer-by-layer tolerance evaluation method on multi-period portfolio model in the future. The other is how to apply swarm intelligence algorithm to solve the complex portfolio models with more constraints.

Footnotes

Acknowledgments

This research was supported by “the Natural Science Foundation of Guangdong Province, No. 2016A030313545 and 2015A030310401”, “the Graduate Education Innovation Projects of Guangdong Province, No. 2015JGXM-ZD03 and No. 2016QTLXXM-19”. The authors are highly grateful to the referees and editor in-chief for their very helpful comments and suggestions.