Abstract

Aiming at the image features of stock data, considering the picture features of stock data and the characteristics of CNN’s good at extracting picture features, the paper proposed a stock price trend prediction model CNN-M based on a Convolutional Neural Network. At the same time, based on the excellent image feature extraction ability of the residual network, this paper proposed a residual network-based stock price trend prediction model ResNet-M based on the Conventional Neural Network. The experimental results showed that the prediction ability of the improved residual network-based prediction model Resnet-M is superior to the CNN model.

Introduction

Convolutional neural network (CNN) is a kind of deep feed-forward artificial neural network, which was inspired by the study of cat vision mechanism. Professor Yann LeCun of the United States successfully applied CNN to the recognition of MNIST handwritten fonts [1], reducing the overall error rate to less than 1%, which is also the most mainstream structural form of convolutional neural networks. At present, convolutional neural networks are widely used in the field of computer vision, and it has excellent image feature extraction capabilities. Generally, it is not directly used in time series data analysis. Financial time series have rich picture feature information. In the past, the technical analysis methods used a certain mathematical formula model to process the stock data to obtain the corresponding index data, then plotted the index data to a chart, and finally predicted the stock price trend.

Financial time series data is not only regarded as numerical data, but it can also convert numerical data into image data for analysis and processing. The technical indicator analysis method is a typical method that transforms time series data into an image and then looks for the regularity in the image (for example, moving average, KDJ, random oscillators, etc.) to predict the stock price [2–4]. In deep learning models, convolutional neural networks (CNN) are most widely used in image feature extraction. At present, there are not many studies using convolutional neural networks for financial data prediction problems.

Zhang et al. [5] proposed a deep learning model based on convolutional neural networks to predict the trend of China’s stock market. It converted daily opening, closing, minimum, maximum, and trading volume information into one-dimensional image data and inputs it into the deep model for training. Finally, the experimental results showed that the model proposed by the paper is effective, the model has good robustness. Considering the picture characteristics of stock time series and CNN’s ability to extract picture features, this paper will try to convert one-dimensional sequences of basic stock market data and technical indicator data into two-dimensional stock phase image data. The x-axis represents the specified market data (or technical indicator data) in the past T period series, the y-axis represents N market data (or technical indicator data), and T * N together form the stock picture features to enter. The problem of transforming financial time series into image classification is realized. The paper proposes a stock price trend prediction model CNN-M based on a convolutional neural network.

Convolutional neural networks obtain higher-level abstract features by extracting features from each layer and performing convolution pooling operations on multiple layers. Theoretically, the deeper the network, the stronger the ability to extract features. However, from the current experimental research results, as the network depth increases, the model has not been improved. Instead, the efficiency of learning and training is greatly reduced. In the paper written by KaiMing He et al. [6], with the same number of training iterations, the error rate graph of the training set and the test set can find that the error rate of the 56-layer neural network is higher than that of the 20-layer neural network. Therefore, it is not that the deeper the neural network is, the better the feature extraction capability of the model will be, or even it will decline.

In 2016, KaiMing He et al. proposed a deep residual network (ResNet). By introducing the concept of a residual learning module, it not only solved this “degeneration phenomenon”, but also improved the number of hidden layers in the network and improves the model performance. Given the above reasons, based on the conventional convolutional neural network, this paper proposes a stock price prediction model ResNet-M based on a deep residual network and conducts modeling and experimental analysis of the two models CNN-M and ResNet-M.

Dataset description

This paper obtained the stock trading data of 42 Chinese SSE50 from Great Wisdom Client from January 5, 2009, to December 31, 2017. Each trading day has information such as the opening price, the closing price, the highest price, the lowest price, the trading volume and so on. The 2016 and 2017 data of each stock are selected as the test set, and the rest is used for model training. The data set of 42 stocks together constitute the total data set and collectively reflects the market situation. Research [7] pointed out: Some technical indicators can predict the future trend of stocks, and Kara et al. adopted ten technical indicators. Based on the use of basic transaction data, this study will use two different input representation methods for indicator data. The first method uses the actual indicator time series of each stock, that is, continuous type; the second method uses each indicator trend, that is, discrete type. The basic information of the data set is shown in Table 1.

Data set overview

Data set overview

a) Missing value processing

There are missing values in the original stock trading data. This paper adopts the following methods to deal with missing values: 1. For a training set with a sufficient number of samples, a single piece of data will be directly discarded, that is, when there is a vacancy value in a data record, the corresponding entire data record will be deleted directly; 2. For a test set with a small sample, the mean value filling method is selected., that is, when there is a vacancy value in a data record, the average value of the corresponding variables in the above and below two adjacent days is taken to fill the vacancy value.

b) Data standardization

As can be seen from the basic stock transaction data listed in Table XX, the values of each variable are in different orders of magnitude. Without normalization, the effect of a large number of variables on the result will overwrite the effect of small, leading to the loss of the information contained in the small order variable. Therefore, each variable of the original sample data must be standardized. It should be noted that, because there is a correlation between the opening price, the closing price, the highest price and the lowest price of the variables, these four variables must be standardized. This paper will use min-max standardization:

Min-max normalization method:

Where x

i

is the raw data to be normalized, x

max

and x

min

represent the maximum and minimum values in the raw data sequence to be normalized, and

c) Define ups and downs labels

Among them, Opnprc t is the opening price on the tth day. If the opening price Opnprct+1 on the t + 1 day is greater than or equal to the opening price Opnprc t on the t day, then the t day is up and marked as “1”; otherwise, it is “down”. Marked as “0”.

a) Continuous technical indicators-actual time series

The following seven technical indicators are used in this paper: MA, K, D, WR, MACD, RSI, and CCI. According to Table 2, this 7 technical indicator value can be calculated by using the original transaction data, and these 7 technical indicator values are also used as inputs in the prediction model. By observing Table X, it is not difficult to obtain that the technical indicators obtained based on the corresponding formula are also continuous values, and they will be normalized between [–1, 1] to avoid the situation where large orders of magnitude cover small orders of information.

Technical indicators and calculation formulas

Technical indicators and calculation formulas

Among them, C

t

, L

t

, H

t

represents the closing price, the lowest price, and the highest price on the t day, respectively. EMA is an exponential moving average, EMA (k)

t

= EMA (k) t-1 + ∝ (C

t

- EMA (k) t-1) ∝ isthesmoothingfactor, ∝=2/(k + 1) UP

t

, DW

t

represent the rise and fall during the t period, respectively. M

t

= (H

t

+ L

t

+ C

t

)/3,

b) The discrete technical indicators-the trend of the indicators

Research [7] pointed out that some technical indicators that can predict the future movement of stocks, so continuous technical indicators are cited in part. The prediction model is based on the existing data to extract valid credits for prediction. This paper proposes to add a new decision-making layer to convert continuous technical indicators into discrete ups and downs through existing expert knowledge and experience. The actual indicator time series sequence calculated by part a is used to determine the stock’s rise and fall based on the characteristics of the indicator data through certain rules. Among them, “+1” represents an increase and “-1” represents a decline. This discrete value reflects the forecast of stocks’ rises and falls based on the existing expert knowledge from this indicator. The following will introduce in detail the expert experience rules for the judgment of the fluctuation of each discrete indicator data. The Moving average (MA)

The Moving average, which is obtained by averaging the closing prices of stocks (indexes) within a certain period. The averages of different times of stock are connected to form an MA, which is used to observe the trend of stock changes. According to expert experience: if the current price is higher than its moving average, it will generate a buying signal, which indicates that the future market is bullish; if the current price is lower than its moving average, it will generate a sell signal, which indicates that the future market is bearish. Therefore, the following provisions are made: If the current closing price Clsprc is higher than MA, the market’s trend is “up” and marked as “+1”; if the previous closing price Clsprc is lower than MA, the market’s trend is “down”, marking Is “-1”. There are five-day, 10-day, 30-day, 60-day, 120-day, and 240-day indicators in the stock market. This article uses the 10-day moving average, which is MA2. Stochastic indicators K, D

K and D use the fluctuations of the highest price, the lowest price, and the closing price in the past few trading days to estimate the future stock price fluctuation trend, which can accurately reflect the random amplitude of the stock over a period, so they are good technical indicators for short-term trend band analysis and judgment. Some experts pointed out: Generally when the KDJ values of the month are low, it will gradually enter the market to absorb, which will generate a purchase signal. Therefore, the following provisions are made: if the current K value is greater than the previous day’s K value, the market’s trend is “up” and marked “+1”; if the current K value is less than the previous day’s K value, the market’s trend is “down”, marked as “-1”. Also, D complies with this requirement. William Index (WR)

The highest, lowest, and closing prices of the “last cycle” can be used to calculate the swing point of the closing price of the day, to determine whether the market is overbought or oversold. Some experts have pointed out that WR is a swinging reverse indicator, that is, when the stock price rises, the WR indicator goes down; when the stock price falls, the WR indicator goes up. Therefore, the following provisions are made: if the current WR value is less than the previous day’s WR value, the market’s trend is “up” and marked as “+1”; if the current WR value is greater than the previous day’s WR value, the market’s trend is “down”, marked as “-1”. WR1 is a 10-day trading strength indicator; WR2 is a 6-day trading strength indicator. This paper uses WR1. Exponential Smoothing Moving Average (MACD)

MACD is obtained by subtracting the slow exponential moving average (EMA26) from the fast exponential moving average (EMA12). Some experts point out that when MACD changes from negative to positive, it is a signal of purchase. When MACD changes from positive to negative, it is a signal to sell. Therefore, the following provisions are made: if the current MACD value is greater than the previous day ’s MACD value, the market’s trend is “up” and marked as “1”; if the current MACD value is less than the previous day ’s MACD, the market’s trend is “down” marked “-1”. Relative Strength Index (RSI)

The relative strength index (RSI) is a numerical calculation to quantitatively analyze the market’s trading intention and strength. The relative strength index RSI believes that in a normal stock market, the stock price can be stable only when the strength of long and short sellers and buyers must be balanced. Some experts point out that the value range of the RSI indicator is between 0 and 100. Above 70 can be considered overbought and below 30 can be considered oversold. In the normal (30, 70) interval, if the upward force is large, the RSI curve rises and it is a signal to buy; if the downward force is large, the RSI curve is down and it is a signal to sell. Therefore, the following provisions are made: if the current RSI value is less than 30, the market’s trend is “up” and marked as “+1”; if the current RSI value is greater than 70, the market’s trend is “down” and marked as “-1 “; If the RSI value is between 30 and 70, the current RSI value is greater than the previous day’s RSI value, the market’s trend is” up “, marked as”+1 “, the current RSI value is less than the previous day RSI value, the market’s trend is up “Down” and marked “-1”. Commodity Channel Index (CCI)

CCI is an indicator that specifically measures whether the stock price has exceeded the normal distribution range and fluctuated between positive infinity and negative infinity. Some experts point out that over 100 can be considered overbought, and below 100 can be considered oversold. In the shock zone (-100,+100), if the upward force is large, it is a signal to buy; if the downward force is large, it is a signal to sell. Therefore, the following provisions are made: if the current CCI value is less than -100, the market’s trend is “up” and marked as “+1”; if the current CCI value is greater than 100, the market’s trend is “down” and marked as “- 1 “; if the CCI value is between -100 and+100, the current CCI value is greater than the previous day’s CCI value, the market’s trend is” up “, marked as”+1 “, the current CCI value is less than the previous day’s CCI value, the market’s trend is “down” and marked as “-1”.

The input of the prediction model includes two parts: basic transaction data and technical indicator data. The output of the prediction model is the ups and downs prediction label, which adjusts our model by comparing the results predicted by the model with the actual ups and downs. Among them, this research will use two methods to represent technical indicator data. The first method is to use the time series of actual technical indicators calculated based on the basic transaction data of each stock, that is, continuous type; the second method is to obtain the trend of each indicator through the experience of relevant experts, that is, the discrete type. Discrete technical indicators refer to the use of existing expert experience to obtain effective stock trend information from actual technical indicator data. When the discrete technical indicator data is directly used as the input of the model instead of the actual continuous value, the trend information perceived by each technical indicator has been input to the model. Compared to the method of directly inputting the original indicators for stock price fluctuation prediction, this is a step forward in a sense. Subsequent experimental sections will discuss whether the use of discrete technical indicator data as input to the model is more effective than actual continuous values.

Model design

The prediction model design based on convolutional neural network (CNN-M)

In this section, the prediction model of the stock price trend based on the convolutional neural network constructed in this paper is shown in Fig. 1. The structure is divided into the following seven layers: an input layer, five hidden layers, and an output layer.

The prediction model based on convolutional neural network.

Input layer: which is accept two-dimensional stock image samples. This paper uses the data of the previous T trading days to predict the stock price change on the (T + 1)th day, and the dimension of the stock data feature set is 20, 6 basic market indicators plus 14 stock technical indicators. Therefore, the dimension of the data accepted by the input layer is [T×20]. In this experiment, the time window size is 20. Therefore, the 2D image sample size specification for stock data is [20 * 20].

Convolution layer 1(Conv1): Use 64 3 * 3 size filters to extract 2D stock image features for convolution operations. The horizontal and vertical sliding window steps are both 1. The padding method uses “SAME” to keep the picture size unchanged. Therefore, after the convolutional layer 1 operation, the matrix size becomes: [20 * 20 * 64].

Convolution layer 2(Conv2): Use 128 3 * 3 size filters to extract image features and perform convolution operations. The sliding window has a step size of 1. The padding method uses “SAME” to keep the picture size unchanged. Therefore, after the conv2 operation of the convolutional layer, the matrix size becomes: [20 * 20 * 128].

Pooling layer: The maximum pooling method is used. The horizontal and vertical sliding window steps are both 2. The padding method uses “SAME”. Through the pooling operation, the output matrix size is reduced by half in both the horizontal and vertical directions. Therefore, after the convolution layer pooling operation, the matrix size becomes: [10 * 10 * 128].

Fully connected layer 1(Fc1) and fully connected layer 2(Fc2): Set 256 and 64 neurons respectively, and set Dropout = 0.5.

Output layer: Use Softmax to implement ups and downs classification.

See Table 3 for specific network parameters.

Parameter setting of the prediction model based on convolutional neural network

In this section, the prediction model of the stock price trend based on the residual neural network constructed in this paper. At present, only the superposed two-layer residual module is considered, and the superposed multi-layer residual module will be analyzed in Experiment 5.5.2. As shown in Fig. 2, the model is divided into the following layers:

Structure of prediction model based on residual network.

Input layer: which is accept two-dimensional stock image samples. As this paper uses the data of the previous T trading days to predict the stock price change on the (T + 1)th day, and the dimension of the stock data feature set is 20, 6 basic market indicators plus 14 stock technical indicators. Therefore, the dimension of the data accepted by the input layer is [T×20]. In this experiment, the time window size is 20. Therefore, the sample size of the two-dimensional stock image for stock closing is [20 * 20].

Convolution layer 1: Use 64 3 * 3 size filters to extract two-dimensional stock image features and perform convolution operations. The horizontal and vertical sliding window steps are both 1. The padding method uses “SAME” to keep the picture size unchanged. Therefore, after the convolutional layer 1 operation, the matrix size becomes: [20 * 20 * 64].

Residual module layer: The residual module uses the Bottleneck structure, which can be stacked by one or more Bottleneck. Bottleneck’s internal structure is shown in 4.X, which consists of three convolutional layers. The function of the convolutional layer 1 is to reduce the dimension; the feature of the convolutional layer 2 is to extract the feature without any change in the dimension; the function of the third layer is to increase the dimension and return the dimension to the original dimension. By this method, one function is to increase the number of network layers (from two to three layers), and the second function is to greatly reduce the parameter amount. To improve the model learning rate and performance.

Pooling layer: The maximum pooling method is used. The horizontal and vertical sliding window steps are both 2. The padding method uses “SAME”. Through the pooling operation, the output matrix size is reduced by half in both the horizontal and vertical directions.

Fully connected layers 1 and Fully connected layers 2: Set 256 and 64 neurons respectively and set Dropout = 0.5.

Output layer: Use Softmax to implement ups and downs classification.

Taking the stacked two-layer Bottleneck residual module as an example. See Table 4 for specific network parameters.

Parameter setting of the prediction model based on the residual network

Step 5: Experiment and analysis. A total of two experiments are proposed in this section. In the first experiment, the research will explore the performance differences between CNN-M and Resnet-M; In the second experiment, the research will explore the impact of network layers on CNN-M and Resnet-M.

Contrast experiment setting

In the first experiment, the research will explore the performance difference between CNN-M and Resnet-M. CNN-M’s network structure uses a seven-layer CNN model designed in section 3.1, with five hidden layers, two convolutional layers, a pooling layer, and two fully connected layers. The Resnet-M’s network structure uses a prediction model based on the residual network designed in Section 3.2 and uses two layers of Bottleneck stacking.

In the second experiment, the research will explore the impact of network layers on the Resnet-M. In theory, the more layers of convolutional layers, that is, the deeper the neural network, the stronger the ability to extract features. However, deepening the network structure will slow down the learning rate of the model, and the amount of data in this article is relatively small. Deeper neural networks will not necessarily achieve better results. Therefore, based on the 3.2 model, two Bottleneck structures in the original model were stacked to three, four, and five. Explore the impact of network layers on the Resnet-M.

Two-dimensions sequence samples constructed by sliding window

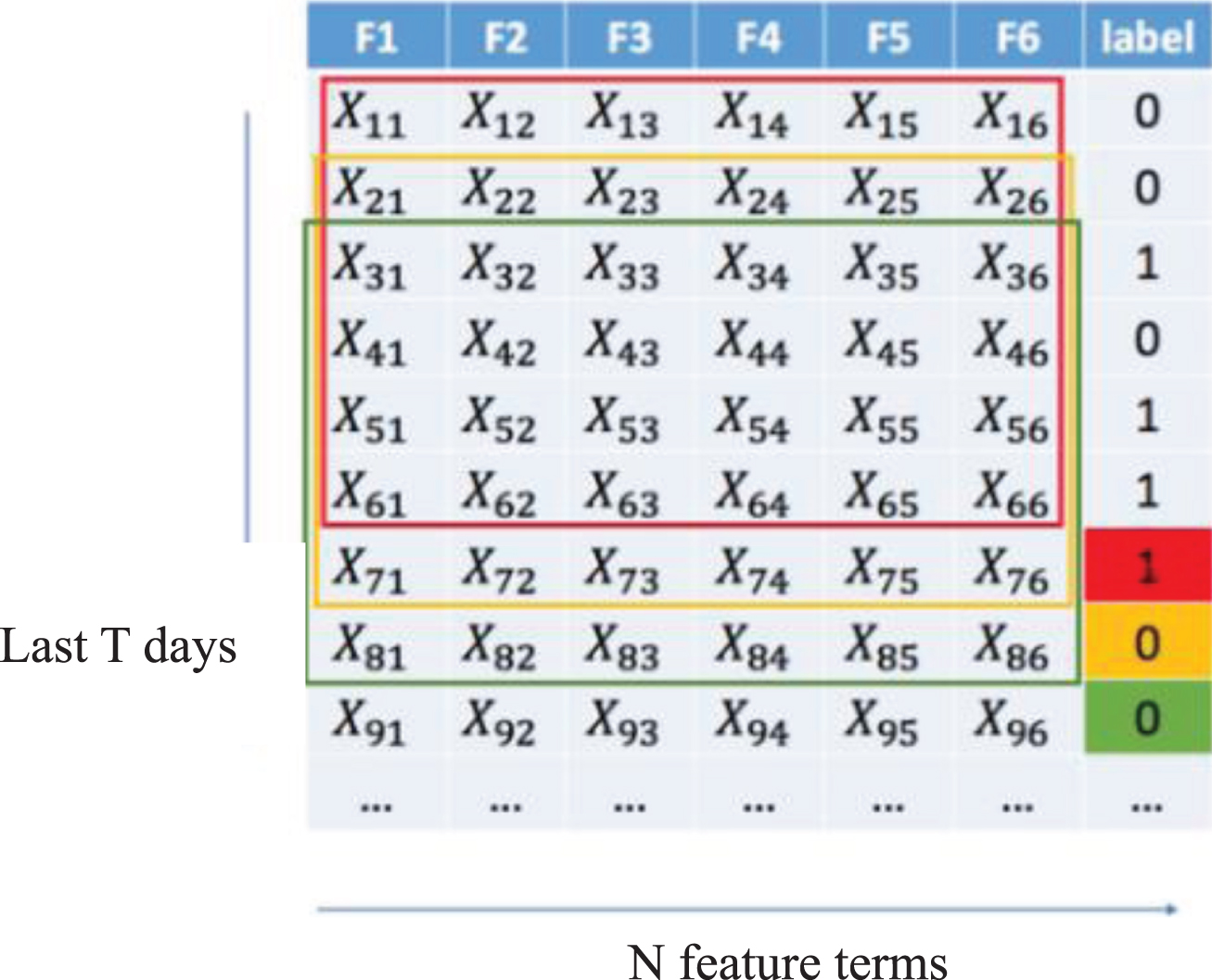

The input of the convolutional neural network is a sequence of two-dimensional stock image samples (shown in Fig. 3), which converts the one-dimensional sequence of basic stock market data and technical indicator data into two-dimensional stock image data.

Schematic diagram of constructing a two-dimensional stock image sample (T = 6, N = 6).

The Y-axis represents the specified market data (or technical indicator data) in the past T period sequence and the X-axis represents N market data (or technical indicator data), which is composed of T * N stock picture features input. This is also a two-dimensional stock image sample using a sliding window. Because the data of the previous T days is used to predict the stock price change on the T + 1 day, the input sequence is {x i , xi+1, … , xi+T-1|x i = (Xi1, Xi2, … X in ) }, and the corresponding label is {yi+T}. Fig. 5 is a schematic diagram generated by a sliding window construction input sequence when the window sizes T and N are 6. The red box is a two-dimensional image sample with 6 * 6 input and the corresponding label is “1” in the red area. A 6×6 input two-dimensional image sample in the next yellow box is obtained through the sliding window and the corresponding label is in the yellow color area “0”. In this way, all two-dimensional stock image inputs and corresponding labels are obtained in order.

Comparison of CNN-M and Resnet-M prediction results (accuracy & F value).

The influence of the number of network layers on the Resnet-M (accuracy & F value).

The experimental environment parameters are shown in Table 5.

Table of experimental environment parameters

Table of experimental environment parameters

The experiment uses open-source Tensorflow as a deep learning platform and uses Python 3.5 to write the experimental program. The model hyperparameters are shown in Table 6.

Model hyperparameter settings

In this experiment, relevant statistical indicators are used to evaluate the predictive performance of the six model stocks that have been set up previously. Evaluation index accuracy (Accuracy) and F value (F-Score) [8]. First, the prediction results of the model will be described. See Table 7 for details.

Model prediction results

Model prediction results

Before calculating precision and F value, “precision and calling rate” must be obtained first.

The accuracy indicates that in the samples that are predicted to be “up”, the true trend is the proportion of “up”. The recall represents the proportion of samples predicted to be “rising” among the samples whose true trend is “rising”. The calculation formulas are:

Accuracy indicates the proportion of correctly predicted samples to the total sample data. F-Score is the average accuracy and recall. The calculation formulas are:

The larger the Accuracy and F-Score values, the more predictive the model is.

Exploring Performance differences between CNN-M and Resnet-M

In this section, the paper will explore the performance differences between CNN-M and Resnet-M. CNN-M’s network structure uses a seven-layer CNN model designed in Section 3.1 with five hidden layers, two convolutional layers, a pooling layer, and two fully connected layers. The Resnet-M’ network structure uses a prediction model based on the residual network designed in Section 3.2 and uses two layers of Bottleneck stacking.

The prediction results of each model are shown in Fig. 4.

It can be seen from Fig. 4 that the prediction accuracy of the ResNet-M reaches 54.8%, while the accuracy of the CNN-M with two convolutional layers is only 52.2%. The ResNet-M in the experiment has 2 Bottleneck structures and each Bottleneck structure has 2 convolutional layers. In other words, the ResNet-M in this experiment, plus the initial convolution operation, has a total of 7 convolutional layers. The accuracy of the ResNet-M is two percentage points higher than the CNN-M, which is expected.

The test results show that the prediction ability of the Resnet-M is better than the CNN-M.

Exploring the impact of network layers on Resnet-M

In the previous section, the prediction accuracy of the Resnet-M is significantly higher than that of the CNN-M. Therefore, in subsequent research, Resnet-M will be selected for further research and analysis. In this section, the paper will explore the impact of network layers on the Resnet-M. Theoretically, the more layers of the convolutional layer, the deeper the neural network, the stronger the ability to extract features. However, deepening the network structure will slow down the learning rate of the model and the amount of data in this article is relatively small. Deeper neural networks will not necessarily achieve better results. Therefore, based on the 3.2 model, the two Bottleneck structure stacks in the original model are superimposed on 2, 3, 4 and 5 Bottleneck, which are counted as Resnet-2, Resnet-3, Resnet-4, and Resnet-5. Explore the impact of network layers on the Resnet-M.

The prediction results of each model are shown in Fig. 5.

First, in terms of accuracy, Resnet-4 reached 55.9%, followed by Resnet-3, which reached 55.2% and the lowest accuracy was Resnet-2. Resnet-5 performed slightly worse than Resnet-3 and Resnet-4. It is worth mentioning that although Resnet-4 has the highest accuracy rate, it does not perform as well as Resnet-3 in terms of F value. So overall, Resnet-3 performed best in this trial.

The results show that in this experiment, Bottleneck’s superposition of 3 layers is better, not that the deeper the neural network is, the better extract features will be. This is related to the small amount of data in this article and deeper neural networks may not achieve better results.

Conclusion

This paper mainly expounded, modeled and experimentally analyzed the stock price trend prediction model based on convolutional neural networks. Based on the explanation of convolutional neural network principles, two models were proposed. One was the most basic model of stock price trend prediction based on CNN and the other was a stock price trend prediction model based on Resnet on the basis of CNN-M. And the model was experimentally analyzed to explore the performance differences between CNN-M and Resnet-M and the influence of the number of network layers on the Resnet-M. The experimental results showed: The prediction ability of the improved Resnet-M based on the residual network was better than CNN-M. Deeper neural networks did not necessarily achieve better results. For this experiment, Bottleneck’s superposition of 3 layers was more effective.

Footnotes

Acknowledgments

This work was supported by the National Natural Science Fund (71071114), National Key Research and Development Program of China (2018YFC0830400) and Natural Science Fostering Foundation (1F-19-303-001).