Abstract

Considering the uncertainty of financial market and the investor’s different attitudes towards risk caused by the various goals, in this paper, a portfolio selection problem with background risks and mental accounts constraints is studied to explore their impact on investment decisions. Firstly, we establish a model with normal uncertain variables, and the optimal solutions of portfolio models with and without background risk are compared. Secondly, considering that the investors always divide an account into several sub-accounts, we put forward an uncertain portfolio model combining uncertainty theory and mental account theory. Thirdly, a portfolio model with background risk and mental accounts is proposed, and the total expected returns of the models in with different proportions of mental accounts are compared. Finally, some numerical applications are provided to validate the model. The result shows that when the levels of tolerance are the same, the expected return of a portfolio with background risk is lower than that without background risk. In addition, the result also shows that when the percent of savings account decreases and that of the consumption account increases, the total expected return increases.

Introduction

The portfolio is about investment choice and combination of multiple assets. Markowitz [1] defined the return as the mean of the random variable; the risk as the variance of the random variable. Many scholars have contributed a lot to this. In the classic study, mainly the loss of investors is studied from indirect measurements. In this way, there are different forms of mean-variance model [2, 3], mean half-variance model [4], and so on.

Because of occurrence of unexpected incidents in economic and social environment, we are lack of enough historical data to evaluate risk. The uncertainty theory based on the axiom system proposed by Liu [5] has been proved to one of powerful tools to deal with the above problem. Afterward, many scholars have studied uncertain portfolio selection in different ways. Huang [6] used the uncertainty theory to study the portfolio problem, and put forward the theory of uncertainty portfolio. Since then, Huang and Zhao [7] have used a method based on expert estimation to evaluate the proceeds of securities, and an uncertain portfolio model is proposed. Later, Chen et al. [8–11] were devoted to the uncertain portfolio selection, where a novel hybrid heuristic algorithm for a new uncertain mean-variance-skewness portfolio selection model with real constraints is proposed in the literature [8], and the muti-period mean-semivariance portfolio optimization based on uncertain measure was constructed in the literature [10]. Deng et al. [12, 13] discussed the different fuzzy portfolio models with some realistic constraints.

In the aforementioned studies, it has been assumed that the investors were only exposed to the risk of financial assets within portfolio, which ignored the risk out of the financial market. However, in real life, investors have to undertake that risk out of the financial market, such as labor income, housing prices, and health risks. These risks are called background risks [14], which may affect their investment decisions. Heaton and Lucas [15] found that the labor force would affect the portfolio’s decision. Hara et al. [16] found that background risk made investors more cautious. Koo [17] set up the optimal investment model of continuous investment in terms of liquidity constraints and labor income in the mixed investment and consumption combination. Menoncin [18] maximized the ultimate wealth of the expected exponential utility function, analyzing the portfolio of issues that take background risks into account. Baptista [19] added a background risk to the portfolio of mean-variance models and discusses the optimal entrusted portfolio management in the presence of background risks. Huang and Wang [20] analyzed the portfolio frontier characteristic given dependently additive background risk. Moreover, in recent years, some researchers have considered background risks under the framework of uncertain portfolio selection. Li et al. [21] developed a fuzzy portfolio selection model with background risk based on the definitions of the possibilistic return and possibilistic risk. Huang and Di [22] discussed an uncertain portfolio election problem in which background risk was considered. Bai and Zhai [23] proposed mean-risk model for uncertain portfolio selection with background risk.

Alternatively, behavioral portfolio theory has clarified that investors’ attitudes toward risk also play a crucial role in the investment process. The concept of mental account was first proposed by Thaler [24], which reveals that people have a clear or potential mental account system when making wealth decisions. In reality, people usually have a variety of contradictory investment objectives and different attitudes towards risk. To integrate these conflicting risk attitudes into one risk attitude and different objectives into one comprehensive objective, Das et al. [25] first introduced the mental account into the classical mean-variance model, and proposed a portfolio theory with mental accounts and compared it with the classical portfolio theory. Das et al. [26] further elaborated on the need for a mental account portfolio study. Alexander [27] constructed a portfolio model with a mental account when the investor had a proxy, and gave the condition that the model mean-variance is valid. Bilbao-Terol et al. [28] designed a portfolio model based on goal programming based on a behavioral portfolio theory with mental accounting. Alexander et al. [29] theoretically characterized the existence and composition of optimal portfolios within mental accounts.

It is worth noting that all the above-mentioned researches concentrate either on developing different portfolio selection models with background risk, or on studying the portfolios with mental accounts. But, the above literature has not yet been carried out from both above aspects. Recently, Baptista [30] combine background risk and mental account theory to develop the uncertain portfolio model, but did not show the influence of the change of mental account proportion on the total expected return. Inspired by the above work, this paper studies the issue of portfolio selection considering background risk and mental accounts in an uncertain environment. It discusses how the total expected return changes when the proportion of different mental accounts changes in detail. In addition, it also explores the impact of background risk and mental accounts on investment decisions.

The paper is structured as follows. In Section 2, necessary knowledge of uncertain variables is introduced for better understanding of the paper. In Section 3, an uncertain portfolio selection model with background risk is discussed. An uncertain model with mental accounts is proposed. And both mental accounts and background risk are taken into account and the model over previous two models is compared. In Section 4, a numerical example is given to analyze the different models. Finally, conclusion is drawn in Section 5.

Preliminaries

Uncertainty theory

The three most central knowledge-points in the theory of uncertainty are: uncertainty measures, uncertain variables and uncertain distributions. Where the uncertainty measure reflects the event size and the measure of the event; the uncertainty variable describes the inaccurate event that may occur: the uncertainty distribution reflects the distribution of the uncertain variables in order to use the uncertain variables. The Uncertainty theory is based on these three important core concepts step by step to develop a mathematical branch of the phenomenon of uncertainty, so that real-life uncertainty phenomenon can be reflected through the mathematical method. Uncertainty theory is developed based on the following four axioms [5]:

(Normality)

(Self-duality)

(Countable sub-additivity) For each countable sequence of events Γ

i

, we have

The triplet (Ω, L, M) is called an uncertainty space. (Product measure) For uncertainty spaces (Ω

i

, L

i

, M

i

) , i = 1, 2, ⋯ , n the product uncertain measure is

Where Γ

i

are events arbitrarily chosen from L

i

for i = 1, 2, ⋯ , n, respectively. It is easy to prove that any uncertain measure M is increasing. That is,

for any event Γ1 ∈ Γ2

In application, an uncertain variable is characterized by an uncertainty distribution function.

For example, a normal uncertain variable is the one that has the following normal uncertainty distribution

Where η and σ are real numbers and σ > 0. For convenience of expression, we denote the normal uncertain variable by

The operational law of the uncertain variables is given as follows:

To tell the size of an uncertain variable, Liu defined the expected value of uncertain variables.

In application, we call

The paper “Portfolio Selection” [1] by American economist Markowitz in 1952 marked the beginning of quantitative financial analysis. He used the mean-variance analysis to conclude that the investment portfolio can effectively diversify the investment risk. However, this theory only considers the financial portfolio risk. In addition to the financial risks, investors are subject to non-financial market risk such as labor income risk, real estate investment risk and health status risk. Heaton and Lucas [15] and Campbell [31] define the risk arising from a risky non-financial asset as a background risk that distinguishes it from the financial risk an investor assumes in a financial market. Specifically, the background risk can be understood as the risk of not being able to diversify through portfolio allocation in financial markets, such as the risks associated with labor income, health status, age status, holdings of real estate and inflation.

The traditional portfolio model ignores the background risk, but the total portfolio risk investors are concerned with not only the portfolio risk but also the background risk. We refer to assets exposed under a background risk as background assets (non-trade assets) and, in addition, financial assets (trade assets). Background assets are non-liquid or non-trading (liquid) assets. In the short term investors cannot control the background risk by adjusting these assets. The existence of background risk largely affects investors’ investment in financial assets. Investors largely underestimate the optimal investment risk if the background risk interaction is ignored in the portfolio model. For example, if the background risk is not considered in the human capital investment, the investor underestimates the optimal investment in the asset, resulting in the overestimation of the risk asset demand and the equilibrium price of the risky asset [32]. Frankke [33] points out many political risks, social risks. Some financial risks are not traded, and these non-tradable risks can be indirectly hedged by “cross-hedging.” The background risk is different, and the background risks cannot be hedged in any way regardless of whether the other risks are independent with background risk or not. However, the impact of background risk on venture capital strategy is very important.

In recent years, the impact of background risk on the investment portfolio has gradually been recognized and concerned, and has stimulated more and more related research. From the literature in China and other countries, background risk is mainly studied from three aspects: one is to study the influence of background risk on investment portfolio from empirical aspects; another is to study the influence of background risk on investment portfolio based on utility theory; the third is to study the background risk from impact of dynamic planning on the portfolio.

Because all background assets have the same characteristics, the most commonly used method is to use the parameter r b to describe the impact of background risk when studying the impact of background risks on investment decisions. For the same reason, in reality we can use a background asset yield r b to represent the return rate on all background assets. In addition, for the sake of convenience, just like many other researchers [19, 35], we assume that the average return of background assets is 0. Our approach also applies to the case where the return rate of the background is nonzero.

Mental accounts

Mental accounts play a significant role in investors’ decision-making. Investors allocate funds to a security account in order to avoid poverty and losses, and the required rate of return is generally low. With the allocation of funds in the risk account, investors hope that this part of the investment will bring them huge profits. Das et al. [25] introduced the mental account into the classical mean-variance model for the first time, and put forward the theory of the portfolio of mental accounts, and compared it with the classical portfolio theory. In so doing, investors with mental accounts in the process of building a portfolio of funds will do sub-account management, each account under the risk attitudes not the same, which can better match the investment objectives. Das and Markowitz’s research assumes that the return rate of securities is a random variable, and the historical data of the securities yield are sufficient and can be better reflected in the study of the portfolio of mental accounts. But in reality, there are times when there is a lack of historical data or historical data failure situation. At this time, we cannot make investment decisions according to Das, Markowitz and others’ approaches.

In this section we will explore the issue of uncertain portfolios of mental accounts. Regarding the return rate of securities as an uncertain variable, we construct an uncertain portfolio model with mental accounts, and give the equivalent form of the model.

Thaler [24] first proposed the concept of mental accounts to explain why individuals in the consumer decision-making are influenced by the impact of sunk cost effect. Thaler argues that people use historical inputs and current payments as a total cost to measure the consequences of a decision. This kind of money is divided into different categories of account management and budget mental process is the mental account of the valuation process. Kahneman and Tversky [34] used the concept of mental accounts in the analysis of performance experiments, demonstrating that consumers form corresponding mental accounts based on different decision-making tasks when making decisions. Kahneman and Tversky argue that mental accounts are the process of accounting, coding, valuation and budgeting for the classification of results.

Uncertain portfolio models with or without background risk and mental account

Uncertain portfolio models with or without background risk

Uncertain portfolio model with background risk

Assume that the investor will make a portfolio on n securities; note ξ

i

is the return rate of security i (i = 1, 2, ⋯ , n). x

i

represents the optimal ratio of investment on security i. After considering the background risk, the total return of the investor includes the return of the portfolio and the income of the background asset. Because the background asset has a non-tradable feature, and in the short term investors can not adjust the background assets to control the background risk, then the total return of investors r

p

:

The investor’s investment objective is that the total return is expected to be the largest under the constraint that the total return below the threshold H is less than α. The uncertain portfolio model considering the background risk is as follows:

Where E is the expected value of the uncertain value, M is the uncertain measure.

As to the constraint

According to Theorem 2.1, since

Formula (16) is equivalent to the following expression:

And note that the given conditions, ξi has a continuous monotonically increasing uncertainty distribution function Φ

i

, and r

b

has a continuous monotonically increasing uncertainty distribution function Θ, according to the monotonicity property of uncertain variable of Theorem 2.1, the constraint of Formula (17) is transformed into:

Thus, the model (13) is transformed into model (14).□

Similarly, for ξ

i

∼ N (μ

i

, σ

i

) , i = 1, 2, ⋯ , n, we have

Hence, the model is obtained.□

When the background risk is not considered, the model becomes:

Assume that the return rate of securities has a continuous monotonically increasing uncertainty distribution function Φ

i

(i = 1, 2, ⋯ , n), the background asset returns r

p

have a continuous monotonically increasing uncertainty distribution function. We can rewrite model (19) into the following form:

Let’s look at the portfolio that considers background risk and disregard the background risk.

Below we give a mental account of the portfolio model. Assuming there are n alternative financial assets, investors divide their funds into m separate sub-accounts. Note ξ

i

for the return rate of security i (i = 1, 2, ⋯ , n). For any account k ∈ {1, 2, ⋯ , m}, it is assumed that X

ki

represents the proportion of investment in asset i under the k - th account. The investor’s return rate r

kp

for the portfolio under the k - th account is:

The risk attitudes of investors in each account are different, so different mental accounts under the threshold value are different. The threshold for each account is H k (k = 1, 2, ⋯ , m). The investor’s goal is that under each mental account, the total return is expected to be the largest under the constraint that the total return below the threshold H k is less than α. At this point, the k - th mental account of the uncertainty of the portfolio model is as follows:

Where E is the uncertainty of the variable and M is the uncertainty measure, the upper limit in constraint 0 ⩽ x ki ⩽ 0.8 indicates that the investor is willing to keep the portfolio diversified while avoiding the risk brought by the single investment. It can be taken in accord with the investor’s preference, such as 0.8 in this model. It is easy to see that the risk appetite of each sub-portfolio is not the same because the risk attitude of the investors in each account is not the same. Assuming that the proportion of investors in each account of the k - th account is d k , then the total optimal portfolio X is:

Through theorem 4.1, we can get the following theorem.

Assuming there are n alternative financial assets, the investor divides their funds into m separate sub-accounts. Note ξ

i

for the return rate of security i (i = 1, 2, ⋯ , n), r

b

for the return rate of the background assets. For any account r

b

assume that x

k

represents the proportion of investment in the k - th account in the asset. Then consider the background risk, the investor in the k - th account under the return rate of portfolio r

kp

is:

The risk attitudes of investors in each account are different, so different mental accounts under the threshold level are different. Note the threshold level in each account for H

k

(k = 1, 2, ⋯ , m). The goal of the investor is that each mental account is under the constraint that the total return below the threshold value of H

k

is less than the requirement that the expected total return is greatest. At this time, the k - th mental account to consider the background risk of the uncertainty of the portfolio model is as follows:

Where E is the uncertainty of the variable, and M is the uncertainty measure. It is easy to see that the optimal solution of each sub-portfolio is not the same because the risk attitude of the investors in each account is not the same. Assuming that the proportion of investors in each account of the k - th account is d

k

, then the total optimal portfolio X is:

In order to get the solution of the model, we will give the following different models of the equivalent form.

Through the Theorem 3.3.1, we can get the following theorem:

Comparison of uncertain portfolio model with and without background risk

In order to better illustrate our proposed uncertain portfolio model with background risk, we will analyze it through a numerical example. We selected 20 securities from the Shanghai Stock Exchange, and the return rate of securities and background assets are considered as normal uncertainvariables.

Suppose the return threshold is set by investors at -8%, and give their tolerance toward the occurrence chance of the portfolio return failing to reach the threshold at 5%. According to the following model, model (14) α = 5% , H = -8 %is:

Using MATLAB, we get the optimal solution with background risk: x4 = 0.0352, x10 = 0.9648, x

i

= 0 (i ≠ 4, 10). The corresponding maximum expected return rate is 8.70%. Setting the same threshold level for model (20), we select the portfolio again when background risk isn’t considered. Then the selection model (20) with α = 5% , H = -8 %becomes:

The optimal portfolio now changes, which is presented in Table 3. The corresponding maximum expected return rate is now 10.02%. It can be seen that 0.8070 < 0.1002, which means that the expected return of the optimal portfolio with background risk is smaller than that without background risk. Using MATLAB, we get the optimal solution without background risk: x4 = 0.1982, x10 = 0.8018, x i = 0 (i ≠ 4, 10)

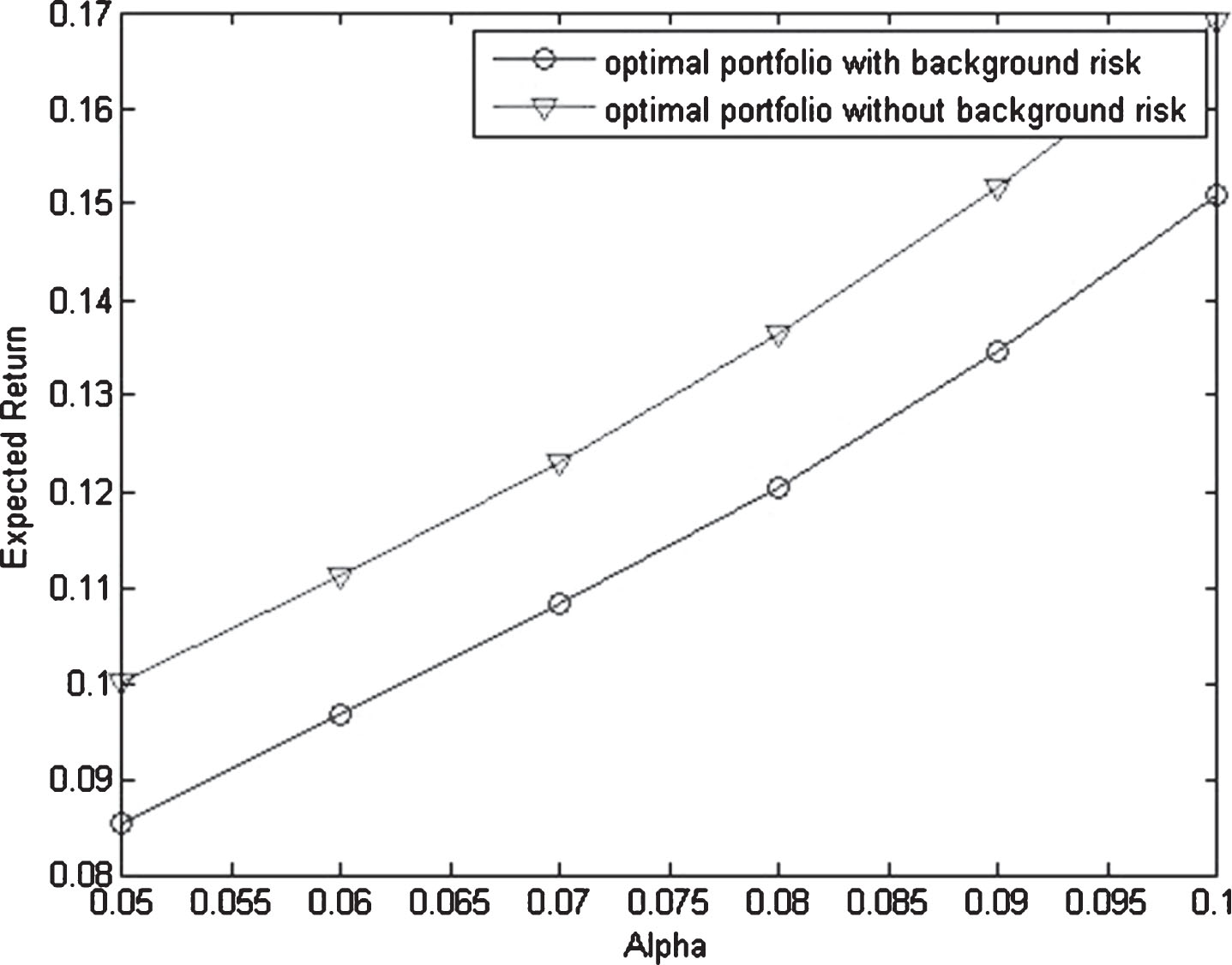

To demonstrate more clearly the difference of optimal portfolios with background risk from those without, we do experiments by keeping the threshold return level at – 8% and changing. The optimal portfolios with or without background risk at different tolerable chance levels are obtained and shown in Tables 2 and 3, respectively.

Through Tables 2, 3 and Fig. 1, we can see the results as follows. (a) When the tolerable level is the same, the expected return of the portfolio with background risk will be lower, and the expected return will increase when the tolerable level increases; (b) The effective frontier without background risk is more than that with background risk; (c) When α = 0.06, 0.1111 > 0.0966, which means in the same situation, the expected return without background risk is larger than that with backgroundrisk.

This numerical example is to illustrate our proposed approach for the uncertain portfolio selection with mental accounts. We give a numerical example here. We select twenty stocks from Shanghai Stock Exchange. Normal uncertain distributions of the stock return are shown in Table 1. Suppose the investors have two mental accounts: Savings (50%) and Consumption (50%). The investors choose the same 20 stocks in Table 1.

Normal uncertain distribution of the stock return ξi

Normal uncertain distribution of the stock return ξi

Optimal portfolios with background risk at different tolerable chance levels in model (14)

and

Optimal portfolios without background risk at different tolerable chance levels in model (20)

In the savings account, suppose the threshold of the expected return α = 5% , H1 = -5 %. So the model (25) can be written in this form:

In the consumption account, we suppose the threshold of the expected return α = 5% , H2 = -10 %. So the model (25) can be written in thisform:

Using MATLAB, we can get the optimal portfolio of different mental accounts and provide it in Table 4. The optimal solution of the total account is also shown in Table 4. It is obvious that because the risk tolerance level is different, the proportions of stocks of different optimal portfolios of two accounts are not the same. And the expected return of consumption account is higher while the expected return of savings is lower. The expected return of total account is between those two.

Optimal portfolio of different mental accounts

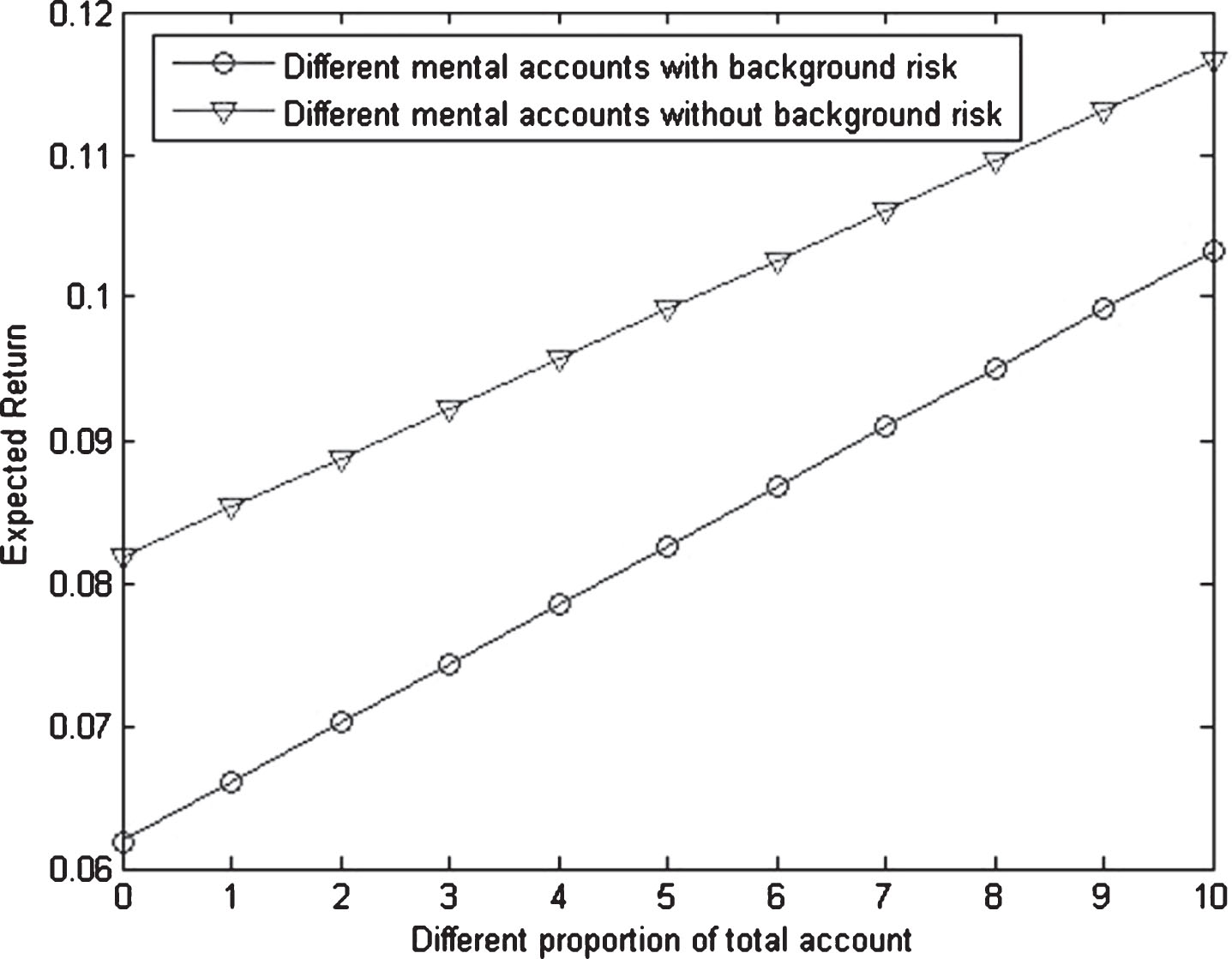

We change the proportion of two accounts from 10 : 0, 9 : 1 to 0 : 10 so that we get the optimal solution and the total expected return. We draw the result in Fig. 2.

Expected return of different total accounts in Table 4.

Figure 2 shows these facts as follows. (a) When the proportion of savings account decreases while that of the consumption account increasing, the total expected return increases; (b) When the proportion of savings to consumption account is 9 : 1, the expected return is 7.36%; when the proportion of savings to consumption account is 5 : 5, the expected return is 9.27%; when the proportion of savings to consumption account is 1 : 9, the expected returnis 11.17%.

We describe the uncertain portfolio considering both the background risk and the mental account model through a numerical example. We suppose that the investor has two mental accounts: savings (50%) and consumption (50%). Assuming that the investor also chooses the same 20 securities as those in Chapter 3, experts considers that the return rate of the background asset has an uncertain distribution function r b ∼ N (0, 0.01).

Model for uncertain portfolio of savings account with background risks

Under the savings account, assume that the investor sets the threshold of the proceeds α = 5% , H1 = -6 %. According to the model, investors should be based on the following model for the portfolio.

When the background risk is not taken into account, we set the same threshold level (α = 5% , H1 = -6 %.). At this time, investors should base on the following model for the portfolio.

Figure 3 shows these results as follows. (a) When the level of tolerance is the same, the expected return of a portfolio that considers background risk is lower than that doesn’t; (b) The result also shows that when the percent of savings account decreases while that of the consumption account increasing, the total expected return increases; (c) When the proportion of savings to consumption is 9 : 1, the expected return is 8.53%; when the proportion of savings to consumption is 5 : 5, the expected return is 9.92%; when the proportion of savings to consumption is 1 : 9, the expected return is 11.30%; (d) the effective frontier without background risk is more efficient than that with background risk.

In the consumption account, investors set the threshold of income α = 5% , H1 = -10 %. We can also get an uncertain portfolio model that considers background risk and one that does not. By solving the model, we obtain the optimal solution of the uncertain portfolio of background risk and the uncertain portfolio model which does not consider the background risk under different mental accounts, as shown in Tables 5 and 6. Under the savings account, if the background risk is taken into account, the maximum expected return for the investor is 5.96%. If the background risk is not taken into account, the maximum expected return for investors is 8.38% and we can see that 5.96% <8.38 %, which means that the expected return of the sub-portfolio considering background risk is less than the sub-portfolio expected return. In the consumption account, we can get the same conclusion. The optimal solutions of the total portfolio considering and not considering the background risk are also shown in Tables 5 and 6, respectively. We can see that the expected return of the total portfolio considering the background risk is 10.33%, and that without considering the background risk is 11.65%, obviously 10.33% <11.65 %. The expected return is also less than the expected return of the total portfolio without considering the background risk.

Optimal portfolio of different mental accounts with background risk in model (35)

Optimal portfolio of different mental accounts without background risk in model (36)

The uncertain model with background risk is considered in the research of portfolio. We compare the optimal solution of the background risk model and the optimal solution without considering the background risk. We propose an uncertain portfolio model with mental accounts. Then an uncertain portfolio model that considers both background risk and mental accounts is discussed. Finally, the numerical results show that the expected return of a portfolio that considers the background risk when the tolerable level is the same will be lower than the expected return of the portfolio without considering the background risk. The results also show that the expected return will increase when the tolerable level increases, which conforms to an essential idea in finance and economics that the greater the amount of the risk that an investor is willing to take on, the greater the potential return. And when the proportion of savings account decreases while that of the consumption account increases, the total expected return increases. The above results give investors suggestions to their own choices about expected return and risk in real financial market.

In future work, we will further study how investors’ psychological state affects the optimal portfolio selection, especially, a portfolio selection programming based on prospect theory will be considered and researched to discuss the investors’ different attitudes towards gain and risk. In addition, other kind of uncertain variables would be considered in the model and make comparison.

Compliance with ethical standards

Footnotes

Acknowledgment

This research was supported by the “Humanities and Social Sciences Research and Planning Fund of the Ministry of Education of China, No. x2lxY9180090”, “Natural Science Foundation of Guangdong Province, No. 2016A030313545”, “Soft Science of Guangdong Province, No. 2018A070712002” and “Fundamental Research Funds for the Central Universities of China, No. x2lxC2180170”. The authors are highly grateful to the referees and editor in-chief for their very helpful comments and suggestions.