Abstract

This paper presents a network index system for assessing investor sentiment. The proposed comprehensive investor sentiment index is based on intuitionistic fuzzy analytic network process (IFANP) and regression model, and is compared with a sentiment index constructed on the basis of principal component analysis (PCA). The long-term relationship and dynamic relationship between the yields of these investor sentiment indexes and the Shanghai Composite Index (SHCI) are explored. Based on autoregressive moving average models and cointegration models, short-term and medium-term forecasts of the yields of investor sentiment index and SHCI are derived. The results of cointegration test, short-term forecasting and medium-term forecasting all show that the investor sentiment index based on IFANP is superior to that based on PCA.

Keywords

Introduction

Sentiment is a general term for a series of subjective cognitions. It is the psychological and physiological state of a variety of feelings, thoughts, and behaviors. Investor sentiment, which can affect decision making, plays an important role in studies of behavioral finance.

The Bearish Sentiment Index first appeared in the American magazine “Investor Intelligence” in 1963, also describing the concept of investor sentiment for the first time. Since then, scholars have defined investor sentiment from different perspectives. For instance, Zweig developed a theory of investor expectations from the values of the underlying securities [1]. Lee et al. believed that investor sentiment was a kind of market judgment based on investors’ psychological emotions, rooted in the cognitive bias caused by the irrational psychological factors of investors [2]. Brown and Cliff stated that investor sentiment incorporated optimistic or pessimistic expectations about stock prices [3], whereas Baker and Wurgler argued that investor sentiment was not only a certain expectation, but it is also investors’ propensity to speculate [4]. Wurgler pointed out that the past definitions of investor sentiment had only been derived from traditional finance, and their boundaries were not very clear [5]. Bormann explained market sentiment from a psychological perspective [6], while Galariotis et al. pointed out that expectation and sentiment may affect the relationship between momentum and state [7].

Investors receive a lot of information from the stock market every day. Because of different cognitions about the market or different information processing abilities of the investors, different expectations for the stock market are formed. The present paper considers this bullish or bearish expectation to be “investor sentiment.”

Fuzzy set is a powerful tool to deal with the imprecision and vagueness, and it has been widely used in decision-making and evaluation process. For instance, Ali Khan et al. introduced multiattribute group decision-making based on Pythagorean fuzzy set [8], while Shakeel et al. investigated information aggregation methods under Pythagorean trapezoidal fuzzy environment and proposed new multi-attribute group decision making methods under the Pythagorean trapezoidal fuzzy environment [9]. Khan et al. defined some operators for Pythagorean fuzzy sets and interval-valued Pythagorean fuzzy sets and suggested multi-criteria decision-making approach based on the developed operators [10], while Ashraf et al. examined the basic operations of spherical fuzzy sets and developed a multi attribute decision making method [11]. Khan et al. proposed new Pythagorean trapezoidal uncertain linguistic fuzzy aggregation information and studied its properties [12].

This paper focuses on constructing a comprehensive investor sentiment index, which is based on intuitionistic fuzzy analytic network process and regression model. This paper has scientific value for its following contributions.

Compared with other literatures, a new perspective for constructing investor sentiment index is provided. We take into account the interaction and feedback relationships among criteria and indices, and also consider the fuzziness and uncertainty in the evaluation process. This paper presents an application study to demonstrate the effectiveness, applicability and superiority of IFANP in practical application. As far as these authors are able to identify, there is no extant research which combines IFANP with regression model for constructing investor sentiment index. To demonstrate the superiority of the proposed method, we compared it with the sentiment index based on principal component analysis.

Literature review

It is difficult to find a unified definition of investor sentiment, because it belongs to the category of behavioral finance and is difficult to observe and measure directly. Scholars usually choose different market variables as proxies for investor sentiment. These variables can be divided into four categories. The first includes subjective indicators of investor sentiment. These are generally obtained through questionnaire surveys and statistical analysis, and can directly reflect whether the investors are optimistic or pessimistic about the future of the market. These indices are subjective and ex ante, such as the Wall Street Analyst Index, Friendship Index, the American Association of Individual Investors, and the Investors Intelligence. Liston developed individual investor sentiment and institutional investor sentiment for different investors [13]. Sun et al. examined the predictability of intraday market return with changes in high-frequency investor sentiment, and their investor sentiment measure was based on the proprietary Thomson Reuters MarketPsych index [14].

The second category covers objective indices of investor sentiment. These indicators can be acquired by applying certain statistical methods to public stock market trading data. These indices are relatively objective and ex post, such as the closed-end funds discount rate, turnover rate, and IPO quantity. Jitmaneeroj argued that the trading volume, advance-decline ratio, and price volatility are strong proxies for market-based sentiment [15]. Ruan et al. investigated the cross-correlation between individual investor sentiment and the Chinese stock market by analyzing the Yu¢ebao Sentiment Index, the daily closing prices of the SHCI and the Shenzhen Component Index [16].

The third category incorporates invisible factors of non-economic variables that affect investor sentiment. For example, these could be weather-related variables such as temperature [17], air pressure, and humidity, or other factors such as noise and sports games [18]. These indicators are not directly relevant to the financial market, and their internal influence mechanisms are difficult to elaborate.

The fourth category is the comprehensive sentiment index, which is constructed from a number of subjective or objective proxy variables. Baker and Wurgler presented a comprehensive investor sentiment index using the net asset values of closed-end stock fund, the raw turnover ratio, the number of IPOs, first-day returns, the share of equity and the dividend premium [19]. With this investor sentiment index, scholars further explored investor sentiment and the stock returns and the role of investor sentiment in the long-term correlation between U.S. stock and bond markets [20]. A comprehensive index has been developed using proxy variables such as the average stock return and average turnover volume [21]. A separate study selected the German Consumer Confidence Index and trading volume as the variables [22].

Investor sentiment is affected by stock prices, which in turn are affected by investor sentiment. Moreover, investor sentiment will increase the volatility and duration of market trends. Through the study of investor sentiment in Britain, the United States, Japan, Germany, France, and Canada, Baker and Stein found that investor sentiment had cross-sectional effects on different types of stock portfolios [23]. Brown and Cliff believed that investor sentiment and the market return index had a negative correlation over the next 1–3 years, arguing that investor sentiment had a certain predictive ability with respect to long-term stock returns [24]. Schmeling stated that the consumer confidence index represented individual investor sentiment, which was negatively correlated with market return [25]. Huang et al. believed that aligned investor sentiments are a powerful predictor of stock returns, outperforming well-recognized macroeconomic variables and predicting cross-sectional stock returns [26]. Sibley et al. showed that the power of the sentiment index to predict cross-sectional stock returns is mainly driven by the risk/business cycle component [27]. Bekaert and Hoerova found the variance premium to contain a substantial amount of information about risk aversion, whereas the credit spread broadly reflects uncertainty, and discussed sentiment indices and financial stress indices on the basis of risk aversion and uncertainty [28]. Xu and Zhou stated that changes in sentiment had a positive impact on future stock returns in the Chinese A-share market, and the predictive power of the sentiment index was most significant for small-sized portfolios [29].

In the current research, when constructing the investor sentiment index, scholars generally adopt mathematical statistical method to make multiple variables synthesize a new variable. The most common method is principal component analysis [4, 30], and some scholars also adopt kalman filtering method. Although previous studies have presented many factors related to investor sentiment, the interaction and feedback relationships among these factors were not considered. For example, margin trading has an impact on the trading volume, advance decline ratio, and net capital flow, and vice versa. Moreover, when evaluating the importance of the indicators, there are uncertainties and ambiguities caused by differences in experience and cultural background of evaluators. Therefore, a new method for constructing a composite index of investor sentiment should be proposed.

When the relationship between independent and dependent variables was vague, the event was ambiguous, or the problem was complex and complicated, scholars introduced fuzzy regression analysis. Bisserier et al. proposed a revisited approach for possibilistic fuzzy regression methods [31]. Jiang et al. presented a multi-objective evolutionary approach to fuzzy regression analysis to acquire optimal solutions [32]. Chukhrova and Johannssen provided a comprehensive systematic review and bibliography on the topic of fuzzy regression analysis [33].

This paper examines the comprehensive sentiment index. Although previous research introduced many factors related to investor sentiment, the interaction and feedback relationships among these factors were not taken into account. For example, margin trading has an impact on the trading volume, advance decline ratio, and net capital flow, and vice versa. Therefore, the interaction and feedback relationships among criteria and indices must be considered. This paper develops a network structure of the various indicators related to investor sentiment. Moreover, when evaluating the importance of the indicators, there are uncertainties and ambiguities caused by differences in experience and cultural background of evaluators. Consequently, the fuzziness and uncertainty in the evaluation process are considered in this paper, and a comprehensive sentiment index is proposed based on the IFANP.

Preliminary knowledge

Analytic network process

ANP was introduced by Saaty as an extension of the analytic hierarchy process (AHP) [34]. Importantly, ANP considers the interaction and feedback relationships among elements, thus overcoming several limitations of AHP. In ANP, elements are divided into two parts, the control layer and the network layer. The structure of ANP is shown in Fig. 1. Wherein, “Goal” represents the overall objective, and “C1 ... C n ” represents the criteria in the control layer. “A, B ... N” represents the indicator sets that have interaction and feedback relationships in the network layer. Generally, if the indicator set A has an influence on set B, then an arrow is added from A to B; if there are interaction relationships within the indicator set A, then an arrow is added from A to A.

A typical ANP structure.

As shown in Fig. 1, the first part is the control layer, which mainly includes the overall objective and criteria. In this part, each criterion is independent and is governed solely by the overall goal. In particular, it is possible to have no criteria in the control layer, but there must be at least one goal. Therefore, the control layer can be regarded as a traditional AHP structure, and the corresponding weights can be acquired by the AHP method.

The second part is the network layer, which consists of all elements that have interaction and feedback relationships. The possible relationships in this layer include the domination of upper elements over lower elements; the interdependence of elements in the same layer; and the feedback of elements in the lower layer to those in the upper layer. The weights can be obtained by constructing an unweighted supermatrix, weighted supermatrix, and limit supermatrix on the basis of the interaction and feedback relationships.

When comparing the importance of indicators, experts or decision makers need to provide information about their preferences for each indicator. However, because of the fuzziness and uncertainty in the environment and differences in people’s way of thinking, the preference information given by the evaluators generally cannot be expressed by an exact number. A more realistic approach is to use fuzzy values instead of exact numerical values. Atanassov introduced the definition and operation rules of intuitionistic fuzzy sets [35]. In an intuitionistic fuzzy set, each element is assigned a membership degree, a non-membership degree, and a hesitation degree. Dimitrov defined the intuitionistic fuzzy preference relationship (IFPR), a generalization of the fuzzy preference relationship that allows the fuzziness and uncertainty to be described more comprehensively and flexibly [36].

Let X = {x1, x2, …, x n } be evaluation indices. Judgment matrix R is formed by the preference information of the evaluators. The elements in R are represented by intuitionistic fuzzy numbers, denoted as (μij, vij), where μij indicates the degree to which xi is more advantageous than xj; vij indicates the degree to which xi is more disadvantageous than xj; and π ij = (1 - μ ij - ν ij ) indicates the degree of hesitancy or uncertainty.

The least-squares and goal programming methods can be applied to determine the local weights of IFPRs. In this paper, the optimal priority optimization (OPO) model is adopted to acquire the local weights [37].

In recent years, considering the fuzziness of ideographic meaning, the study of fuzzy analytic network process (FANP) is very prosperous. FANP is an extension of ANP in uncertainty and fuzziness problems. Mikhailov and Singh proposed a fuzzy extension to the network analysis of Saaty, adding human preference information to the ANP method, and proposing a two-dimensional interval [a, b] to express the uncertainty and fuzziness in the decision-making process [39]. Bueyuekoezkan et al. constructed a fuzzy network analysis method based on triangular fuzzy Numbers, which solved the fuzziness problem in the process of criterion measurement and judgment [40]. Chang et al. proposed to use triangular fuzzy number to represent the preference information of decision makers, and to use expert knowledge system and fuzzy network analysis to solve uncertain or inaccurate evaluation problems [41]. Lin applies FANP method to supplier selection in the supply chain [42].

However, how to apply ANP under intuitionistic fuzzy environment becomes a difficult problem. In the existing studies, the combination of intuitionistic fuzzy set and AHP can be found. For example, Sadiq and Tesfamariam applied IFAHP to handle both vagueness and ambiguity related uncertainties in the environmental decision-making process [43]. Abdullah and Najib proposed a new IFAHP method characterised by new preference scale of pair-wise comparison matrix measurement [44]. Kahraman et al. proposed an interval-valued IFAHP for order of preference by similarity to ideal solution based methodology, and an application is provided for the evaluation of outsource manufacturers [45]. AHP and ANP are different technologies, and IFANP is rarely used in literature. Buyukozkan et al. combined IF with ANP with limited computational steps [46]. Liao et al. combined these two theories and proposed the calculation of intuitionistic fuzzy network analysis for the first time [37]. At present, limited applications of IFANP imply some gaps in the literature.

Principal component analysis

Principal component analysis is a multivariate statistical method that examines the correlation between multiple variables. It is often used as a method to reveal the internal structure among multiple variables through a few principal components. The main purpose of principal component analysis is to reduce dimensionality. Suppose there are n sentiment indicators, and the initial matrix reflects the p phase observations of these indicators.

For X1, X2, . . . , X

n

in the matrix, the following linear combination can be constructed:

Generally,

A number of scholars have explored the PCA-based sentiment index. For instance, Chen et al. developed a PCA-based investor sentiment with six important economic and market factors [47], and Saka et al. revealed the perceived commonality in default risk among peripheral and core Eurozone sovereigns based on PCA [48]. Ding et al. proposed an investor sentiment index for the Chinese stock market based on PCA and an autoregressive model [49].

In this section, we first select investor sentiment indicators and examine their interaction and feedback relationships. Then we establish the investor sentiment index based on IFANP and PCA, respectively.

Sentiment indicator selection and data processing

Inspired by existing research, 13 objective indices were chosen to construct the investor sentiment index considered in this paper. The main reason for excluding subjective indicators is that subjective variables are obtained through questionnaires, and the timeliness of the survey samples will gradually be weakened by the inherent time delays.

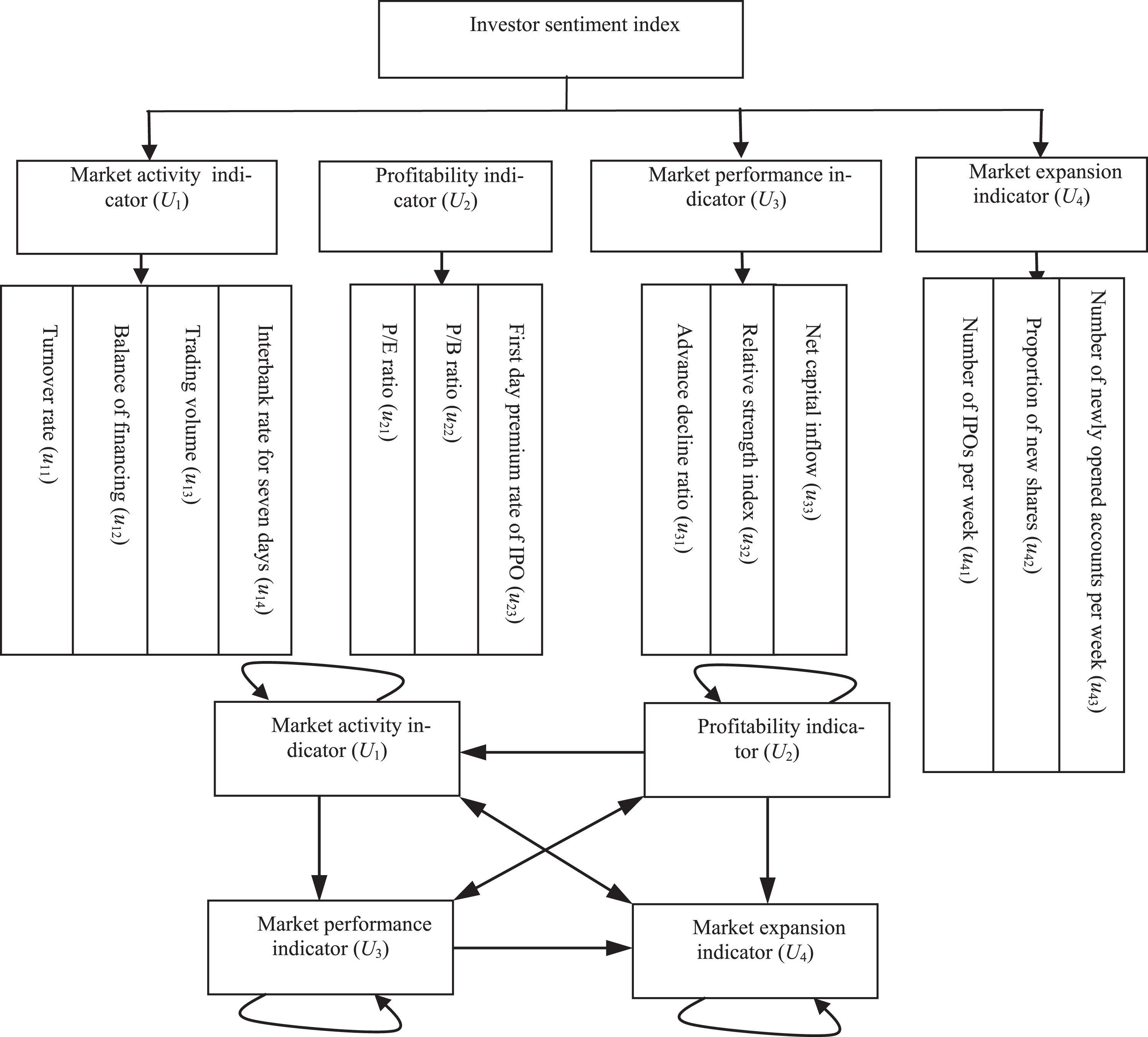

The indicators are divided into four categories: market activity index, profitability index, market performance index, and market expansion index. Each indicator is described in Table 1.

Sentiment indicators

Sentiment indicators

Chinese A-share data from May 1, 2015, to December 31, 2017, obtained from the Wind and Reith databases, were used as sample data. For various reasons, there are several missing values from IPOs during the selected period; the relevant data were assigned values of zero. As the measurement units vary for different indicators, Equations (5) and (6) were adopted to standardize the data for the comparison, ensuring the values of all indices were within the range [0, 1].

If indicator i is a cost indicator,

If indicator i is a benefit indicator,

Based on the interrelationships among indicators, we now describe the ANP network structure. The local weights and global weights of the indices are then determined, and the regression model for obtaining the investor sentiment index is proposed. The steps of establishing the investor sentiment index based on IFANP are shown as Fig. 2. The specific steps are as follows.

The steps of establishing the investor sentiment index based on IFANP.

Step 1: Build the ANP network structure.

Considering the interaction and feedback relationships among indicators, a network index system of investor sentiment is presented. For example, the turnover rate (u11) influences the trading volume (u13), and vice versa. The balance of financing (u12) interacts with the trading volume (u13), as well as the advance decline ratio (u31), relative strength index (u32), and net capital inflow (u33). The network structure of investor sentiment is shown in Fig. 3.

ANP network structure of investor sentiment index.

Step 2: Establish the IFPRs.

People tend to make decisions in a familiar language. For example, the preference for a product can be described by linguistic variables such as like and dislike. IFPRs can express this ambiguity and uncertainty, although linguistic variables can only be used for qualitative analysis. If quantitative analysis or computations are to be performed, the linguistic variables should be converted accordingly. Considering their relative importance, the preference information of evaluators can be divided into nine grades (see Table 2). Note that, according to the actual situation, linguistic variables can also be divided into different levels.

Intuitionistic fuzzy linguistic variables

A voting system can be adopted when there are many inconsistent opinions. An intuitional fuzzy number (μ A , ν A , π A ) can be obtained by counting the number of votes in support, opposition, and abstention, where μ A = votes in support / the total number of votes, ν A = votes in opposition / the total number of votes, and π A = number of abstentions / the total number of votes.

Under the overall goal, the indicators U1, U2, U3, and U4 are compared one by one. For instance, compared with U2, U3, and U4, the indicator U1 is considered relatively important, more important, and very important, respectively. By analogy, a judgment matrix expressed by linguistic variables can be acquired.

According to Table 2, the linguistic variables are converted into corresponding IFPRs, and the following intuitionistic fuzzy judgment matrix is obtained.

According to the relationships shown in Fig. 3, a total of 45 IFPR matrices was generated.

Step 3: Construct the unweighted supermatrix.

The local weights of the IFPR matrices were calculated by equation (2). After determining the local weights of all intuitionistic fuzzy judgment matrices, the unweighted supermatrix W is constructed according to Fig. 2 (see Table I in the appendix).

Step 4: Solve the weighted supermatrix.

Only the interaction and feedback relationships among the second-level indicators are considered in the unweighted supermatrix. The global weights of the indices must be calculated. To construct the weighted supermatrix, the weighted matrix a

ij

of the relative importance in the first-level indicators is multiplied by the unweighted supermatrix.

Step 5: Calculate the limit supermatrix.

To maintain the stability of the weighted supermatrix, its limit can be determined; this is the limit supermatrix. The values of each row in the limit supermatrix are the same, and thus any column can be taken as the global weights of the indicators. The result is presented in Table II in the appendix.

According to Table II, the global weights of the indicators are ω i = (0.1629, 0.0858, 0.1117, 0.0412, 0.0367, 0.0515, 0.0256, 0.1448, 0.1067, 0.0819, 0.0769, 0.0330, 0.0412) T .

Step 6: Acquire the investor sentiment index using a regression model.

The SHCI data from May 1–September 1, 2017, were used to determine the parameters of the investor sentiment index. This period was selected because the data were relatively stable over this time, with relatively little fluctuation, and as this period is relatively recent, the data are representative. Regression and least-squares curve fitting methods are adopted to determine the parameters of the function.

Computations show that [beta(1), beta(2), ... , beta(14)] = [2.22E-14, 2.22E-14, 535.40, -926.78, 16972.13, 3263.53, 2.09E-05, 1.44E-10, 442.25, 410.82, 2.26E-14, 364.17, 2.22E-14, 3049.37].

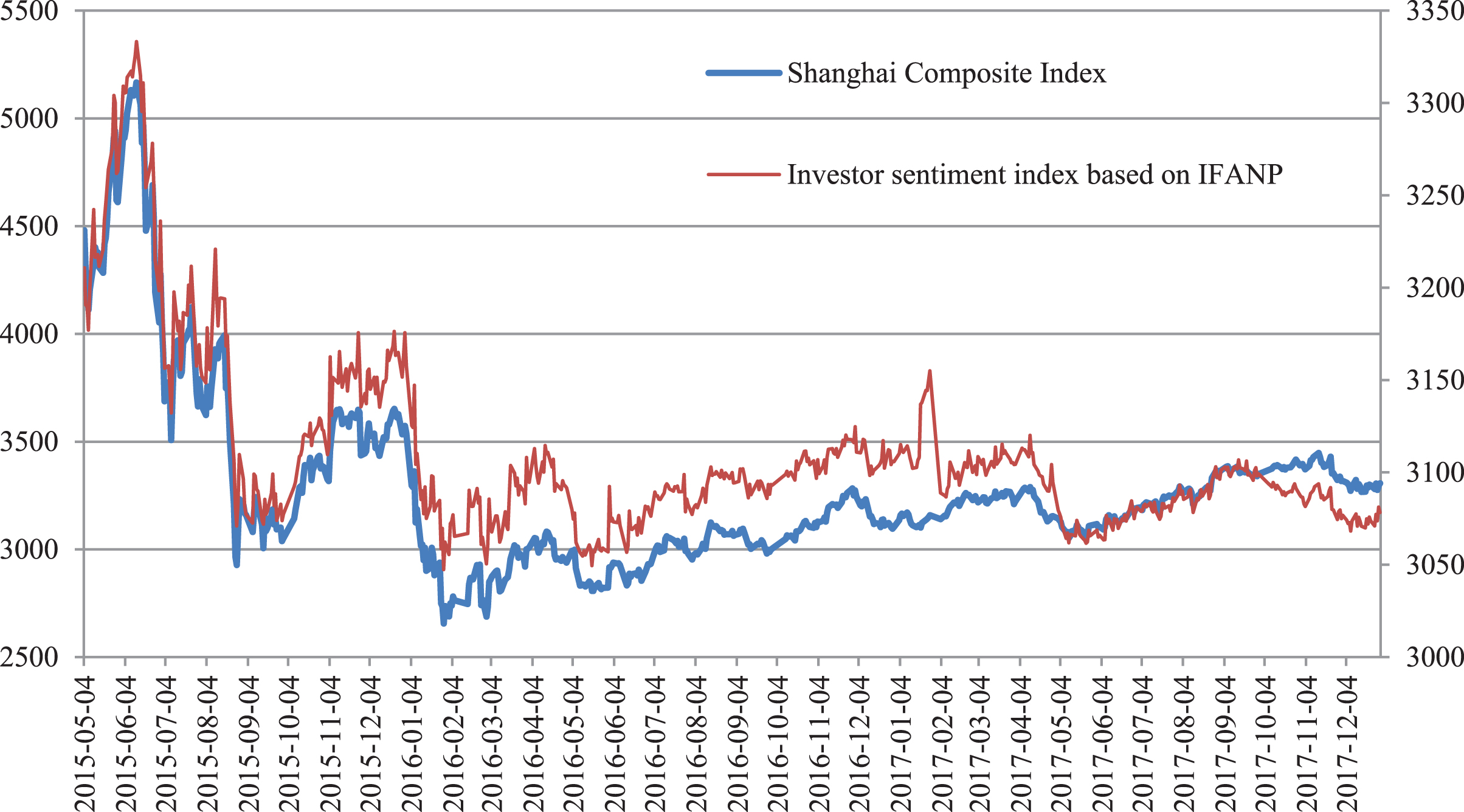

The investor sentiment index from May 1, 2015, to December 31, 2017, was obtained by Equation (8). A comparison with the SHCI is shown in Fig. 4.

SHCI and investor sentiment index based on IFANP.

In Fig. 4, the trend in the investor sentiment index based on IFANP is basically consistent with that of the SHCI, and there is a significant positive correlation (the correlation coefficient is 0.9157). The investor sentiment index peaked on June 12, 2015, before dropping to around 3175 within one month. During the same period, the SHCI had also dropped rapidly after reaching a high point of 5178.19. Although the investor sentiment index fluctuated during the study period, it has never exceeded the high point of 2015. Correspondingly, the SHCI has also not been able to reach its high point again.

In addition, the investor sentiment index is more sensitive to the stock market than the SHCI. This indicates that the investor sentiment index has a certain reference to the returns on stocks.

Liao et al. implemented the method to a case study concerning the brand management of the six golden flowers of Sichuan liquor to show the applicability and efficiency of the IFANP [33].

To illustrate the scientific nature and superiority of the investor sentiment index based on IFANP, the same data were used to construct an investor sentiment index based on PCA for comparative analysis. The steps of establishing the investor sentiment index based on PCA are shown as Fig. 5. Investor sentiment index based on PCA was constructed as follows.

The steps of establishing the investor sentiment index based on PCA.

Step 1: Factor analysis was conducted to determine the correlation among indicators, so as to ensure reasonable dimension reduction. The results of the common factor analysis of variance indicate that, except for the trading volume, more than 85% of the information of other variables is retained in the PCA (see Table 3). In Table 3, there are four eigenvalues greater than one, but the cumulative contribution rate is only 71.26%. To raise the cumulative contribution rate above 80%, six principal components were extracted.

Total variance of the variables

Step 2: Calculate the coefficient matrix. The component matrix is the initial factor load matrix.

Step 3: The function of each principal component is determined as follows.

Step 4: Derive the comprehensive function of the principal components. This is the linear combination of the six principal component functions given by

The above analysis gives the investor sentiment index based on PCA. A comparison with the SHCI is shown in Fig. 6.

SHCI and investor sentiment index based on PCA.

According to Fig. 6, the trend of the investor sentiment index based on PCA is basically consistent with that of the SHCI. Although there is a significant positive correlation (the correlation coefficient is 0.8395), it is not as significant as the correlation between SHCI and the investor sentiment index based on IFANP (for which the correlation coefficient is 0.9157).

Suppose P t is the closing price of the SHCI on the tth trading day, and H t and S t indicate the investor sentiment index values based on IFANP and PCA, respectively. To reduce the heteroscedasticity of the data without changing the trend, the natural logarithm of P t , H t , and S t was taken. The resulting yields are denoted as R t , I t , and L t .

Cointegration test

An augmented Dickey–Fuller (ADF) test was performed to check the stationarity of the sequences. The results show that the null hypothesis of unit roots is accepted for P t , H t , and S t , indicating that these sequences are nonstationary. However, the null hypothesis is rejected for R t , I t , and L t , indicating that these are stationary sequences. As R t , I t , and L t are single-integer sequences of the same order, they meet the prerequisites for cointegration analysis. Therefore, the cointegration relationships between R t and I t (model 1), R t and L t (model 2) were constructed to examine whether any long-term equilibriums exist. The results of the cointegration analysis are presented in Table 4.

Results of cointegration analysis

Results of cointegration analysis

In Table 4, the cointegration coefficients of I t , L t , and R t are significant. At the same time, the R values of models 1 and 2 are 0.720898 and 0.597189, respectively. The latter is lower, indicating that the sentiment index based on PCA is not as effective as the sentiment index based on IFANP in terms of model fitness.

Furthermore, stationarity tests were performed on the residuals of the cointegration equations. The results in Table 5 indicate that the residuals are stable, suggesting that there are cointegration relationships between R t and I t and between R t and L t . In other words, there is a long-term relationship between the yields of the SHCI and the investor sentiment index.

Results of ADF tests of the residuals

As there is a cointegration relationship between the yields of the SHCI and the sentiment index, the Granger causality test was applied to examine the causal relationship between them. The results are presented in Table 6.

Results of Granger causality tests

Results of Granger causality tests

This analysis shows that the Granger causality between R t and I t is significant. Regardless of whether the lag order is one, two, or three, I t is always the Granger cause for the change in R t , and R t is the Granger cause for the change in I t . That is, there is a two-way causality between I t and R t . In short, I t and R t are an interactive process.

Regardless of the number of lag orders, the causality of L t to R t is not significant, whereas that of R t to L t is significant. This indicates that there is a one-way causality of the yield of SHCI to the yield of the sentiment index, which is inconsistent with reality.

To analyze the degree of fit of I

t

/ L

t

to R

t

, an autoregressive moving average (ARMA) model was used to predict I

t

and L

t

. Short-term and medium-term forecasts for R

t

were then generated based on the cointegration model. The fit error rate is given by

According to the results of the ADF test, I t and L t are stationary sequences, and thus the ARMA model can be adopted. As the autocorrelation function (ACF) is trailing off and the partial ACF (PACF) is a second-order truncation, AR(1), AR(2), MA(1), and ARMA(1, 1) for I t are presented in Table 7.

Comparison of different models

From Table 7, we find that the Akaike information criterion (AIC) and Schwarz information criterion (SIC) values of model AR(2) are the smallest, which indicates that this model is superior to the others in terms of the model fit. Therefore, model AR(2) is selected. After parameter estimation, the adaptability of the model was tested. Essentially, this is the white noise test of the residual error. If the residual error is not white noise, then some important information has not been extracted, and the model should be reset. The ACF and PACF tests were applied to determine the residual error of model AR(2). The autocorrelation coefficients of the residual error all fell into a random interval, and are significant at the 0.05 confidence level. Therefore, model AR(2) is reasonable, as shown by equation (12). For simplicity, this is named model 3 in the following.

Similarly, ACF and PACF tests were applied to L

t

, and models AR(1), AR(2), MA(1), and ARMA(1, 1) were generated. Comparing the AIC and SIC values of these models indicates that ARMA(1, 1) is optimal. As the residual error is white noise, ARMA(1, 1) is a reasonable model, as shown by equation (13). This is referred to as model 4 in the following.

Short-term prediction

The ARMA model was used to predict the yield of the investor sentiment index and the cointegration model was applied to predict the yield of SHCI. The SHCI data from January 1–31, 2018, were used to conduct short-term predictions. Excluding statutory holidays, there were 22 trading days. The results are shown in Fig. 7, where R t f1 represents the prediction value based on model 1/3 and R t f2 represents the prediction value based on model 2/4.

Short-term prediction results.

Fig. 7 shows that the trends of the prediction values are in line with the actual values, indicating that the models are effective for short-term predictions. Furthermore, the p-value of the fit error rate of model 1 is 2.55E-05 and that of model 2 is 1.61E-04. The fit error rate of model 1 is obviously lower than that of model 2. This shows that, for short-term forecasting, the sentiment index model based on IFANP is better than that based on PCA.

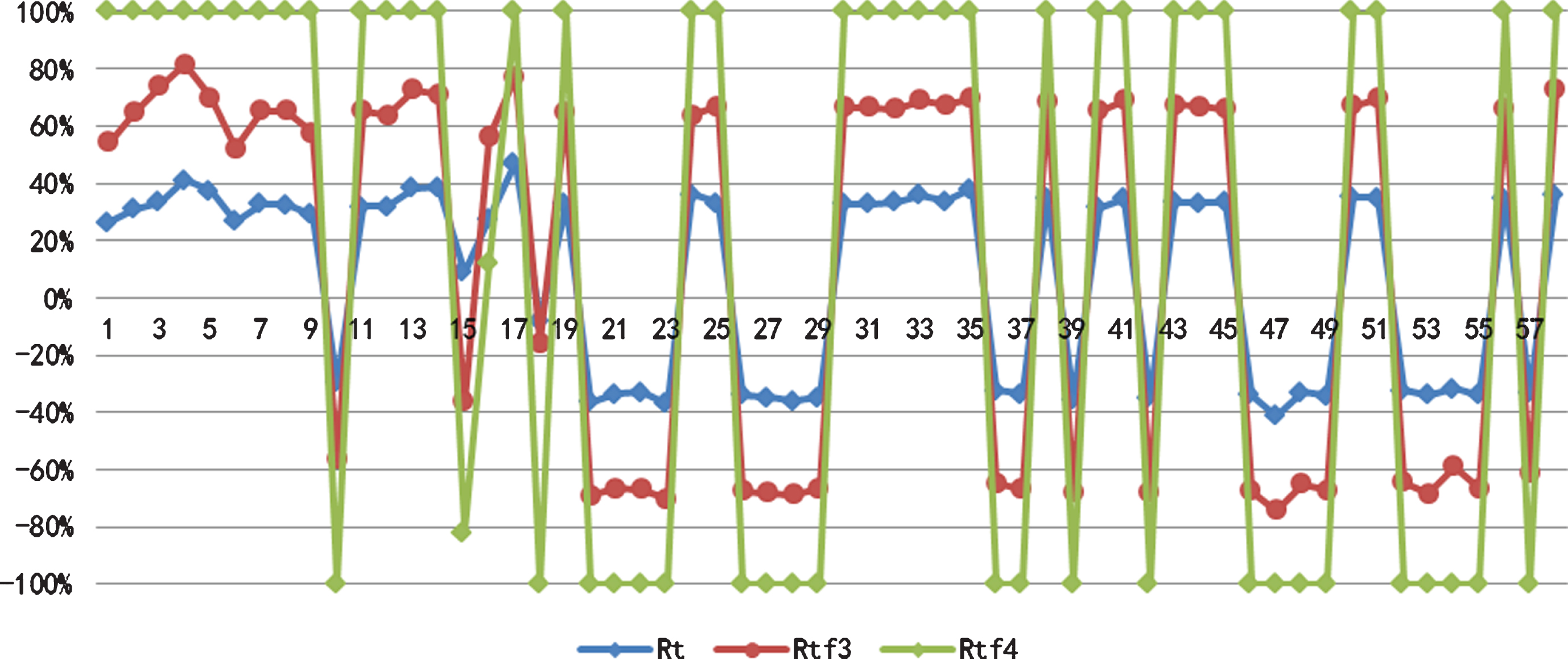

The SHCI data from January 1–March 31, 2018, were used to make medium-term predictions. Excluding statutory holidays, there was a total of 58 trading days. Dynamic predictions were generated based on model 1/3 and model 2/4, respectively. The results are shown in Fig. 8, where R t f3 represents the prediction values based on model 1/3 and R t f4 represents the prediction values based on model 2/4.

Medium-term prediction results.

Figure 8 shows that the trends of the predicted values are in line with the actual values, indicating that the models are effective for medium-term predictions. Furthermore, the p-value of the fit error rate of model 1 is 1.03E-05, and that of model 2 is 4.85E-04. The fit error rate of model 1 is again less than that of model 2. This shows that, for medium-term forecasting, the sentiment index model based on IFANP is better than the model based on PCA.

Compared with the short-term predictions, the fit error of the medium-term forecasts is obviously lower. The fit error rate of model 1 has decreased from 2.55E-05 to 1.03E-05, and that of model 2 has decreased from 1.6E-04 to 4.85E-05, indicating that the medium-term predictions based on these models are better than the short-term predictions.

Objective indicators of market trading were used to construct investor sentiment indexes based on IFANP and PCA, respectively, and the relationship between these indexes and SHCI was analyzed. On the basis of the yields of the investor sentiment indexes and SHCI, the long-term equilibria and dynamic relationships were examined. Short-term and medium-term forecasts of the rate of return were then generated. The main conclusions are as follows.

The cointegration test shows that there is a long-term equilibrium relationship between the yield of the investor sentiment index and the yield of the SHCI. The degree of fit of the investor sentiment index based on IFANP is better than that based on PCA.

According to the Granger causality test, there is a two-way causality between the yield of the investor sentiment index based on IFANP and the yield of the SHCI. The investor sentiment and the stock market are a mutual promotion process. In contrast, there is a one-way causality of the yield of the SHCI to the return from the sentiment index based on PCA, which is inconsistent with reality.

The total weight of four indicators (turnover rate, trading volume, advance decline ratio, relative strength index) is 0.5261. These account for more than half of all the 13 sentiment indicators. Therefore, if it is necessary to regulate the stock market, regulators should focus on these four indicators.

Based on the ARMA model and the cointegration model, short-term and medium-term forecasts of the yields of the investor sentiment index and SHCI were generated. The medium-term predictions are better than the short-term predictions. Moreover, whether in the short-term or medium-term, the results of the investor sentiment index based on IFANP are superior to those of the sentiment index based on PCA.

General time series methods are based on accurate information and there are definite functional relations between the past, present and future values of time series and white noise. However, the intrinsic behaviors and decision-making characteristics of investors are not clear in financial markets. At the same time, people’s judgments of the past can be ambiguous, and incomplete historical data are abundant. Therefore, in the future research, we will try to introduce fuzzy thinking into the prediction of financial series and establish the prediction model of intuitionistic fuzzy time series. From the perspective of investor sentiment, intuitionistic fuzzy analytic network process can be further used to study the pricing and forecasting of risky assets.

Footnotes

Appendix

The unweighted supermatrix The limit supermatrix

u

11

u

12

u

13

u

14

u

21

u

22

u

23

u

31

u

32

u

33

u

41

u

42

u

43

u

11

0.0000

0.6618

0.8068

0.4578

0.2395

0.2338

0.4673

0.0000

0.0000

0.0000

0.5133

0.1407

0.4716

u

12

0.2593

0.0000

0.1594

0.2169

0.3605

0.4293

0.1611

0.0000

0.0000

0.0000

0.1773

0.5760

0.1529

u

13

0.6296

0.3043

0.0000

0.3253

0.2395

0.2226

0.2683

0.0000

0.0000

0.0000

0.0932

0.1511

0.2735

u

14

0.1111

0.0338

0.0338

0.0000

0.1606

0.1143

0.1033

0.0000

0.0000

0.0000

0.2162

0.1322

0.1020

u

21

0.0000

0.0000

0.0000

0.0000

0.0000

0.8500

0.6000

0.3253

0.3253

0.2105

0.0000

0.0000

0.0000

u

22

0.0000

0.0000

0.0000

0.0000

0.6000

0.0000

0.4000

0.2169

0.2169

0.1403

0.0000

0.0000

0.0000

u

23

0.0000

0.0000

0.0000

0.0000

0.4000

0.1500

0.0000

0.4578

0.4578

0.6491

0.0000

0.0000

0.0000

u

31

0.5601

0.3012

0.4578

0.5601

0.2105

0.2921

0.4578

0.0000

0.8500

0.6000

0.0000

0.0000

0.0000

u

32

0.2921

0.2452

0.3253

0.2921

0.1403

0.1478

0.3253

0.6000

0.0000

0.4000

0.0000

0.0000

0.0000

u

33

0.1478

0.4535

0.2169

0.1478

0.6491

0.5601

0.2169

0.4000

0.1500

0.0000

0.0000

0.0000

0.0000

u

41

0.5601

0.4578

0.4578

0.5601

0.5601

0.5601

0.4578

0.4578

0.4578

0.5601

0.4000

0.6000

0.8500

u

42

0.1478

0.2169

0.2169

0.1478

0.1478

0.1478

0.2169

0.2169

0.2169

0.1478

0.6000

0.0000

0.1500

u

43

0.2921

0.3253

0.3253

0.2921

0.2921

0.2921

0.3253

0.3253

0.3253

0.2921

0.0000

0.4000

0.0000

u

11

u

12

u

13

u

14

u

21

u

22

u

23

u

31

u

32

u

33

u

41

u

42

u

43

u

11

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

0.1629

u

12

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

0.0858

u

13

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

0.1117

u

14

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

u

21

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

0.0367

u

22

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

0.0515

u

23

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

0.0256

u

31

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

0.1448

u

32

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

0.1067

u

33

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

0.0819

u

41

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

0.0769

u

42

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

0.0330

u

43

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412

0.0412