Since the practical production is not continuously available and sometimes suffers unexpected breakdowns, this paper applies uncertainty theory to introducing an uncertain production risk process with breakdowns to handle the production problem with uncertain cycle times (consisting of uncertain on-times and uncertain off-times) and uncertain production amounts. The concept of shortage index of the uncertain production risk process with breakdowns is provided and some formulas for the calculation are given. Furthermore, the shortage time of the uncertain production risk process with breakdowns is proposed and its uncertainty distribution is obtained. Finally, some numerical examples are revealed.

One type of production problems is about some continuous production cycles in which the data of cycle time and the production amount or cost are known. Muth [14] contributed to the first work of renewal process in production problems by taking the cycle times as random variables with exponential distribution functions and the production amounts as one unit each cycle, and then the work was extended by Papadopoulos [15] into the case in which the random distribution functions of the cycles times are non-identical. Furthermore, the model with multiple production lines was also solved by Papadopoulos [16]. However, in most practical production problem, it is unwise to assume that the machines used in production are continuously available and without any breakdowns. Therefore, Birge and Glazebrook [2] suggested a production model in which the cycle times are regarded as on-times plus off-times, that is, a production model with breakdowns. The breakdowns existing in the production model reduce the machine capacity, and the production amount may not be enough to satisfy the demand and then shortage occurs. Hence Groenevelt et al. [4] proposed safety level to handle the case with breakdowns where the crisp production rate and demand rate are known and the cycle times for demand are regarded as random variables. Moreover, for a production model with breakdowns and random demand, Parlar [17] applied random renewal reward theorem (Ross [18]) to calculating the average cost per time. Some applications of production process with breakdowns were proposed by Christer and Keddie [3] (block replacement policy) and Billatos and Kendall [1] (age replacement policy).

Probability theory is the best mathematical tool to deal with frequency. However, as one common type of emergency occurring in production, it is not easy to accurately forecast when the breakdowns happen. That means, the estimated distribution functions of the on-time and off-time (caused by breakdowns) in each cycle may not be closed enough to the frequency. Especially, for a new product, the data about the production amounts are inadequate and the practical distribution functions deviate far from the frequency. To make matters worse, even for an old product, the historical data about the cycle times and production amounts may become unavailable for estimating the distribution functions due to the unexpected breakdowns. In order to deal with the production model with breakdowns, Wang [19] regarded the cycle times as fuzzy random variables and applied fuzzy random renewal reward theorem (Zhao et al. [24]) to calculating the average cost per time. Following that, by separating back-order cost and holding cost from the production cost and regarding them as fuzzy random variables, a modified fuzzy random production model with breakdowns was introduced by Kumar and Goswami [5].

Unfortunately, in some practical production problems, neither probability theory nor fuzzy theory can be used to reasonably deal with the emergency such as breakdown (Liu [11]), and uncertainty theory proposed by Liu [7] and perfected by Liu [9] is the only suitable mathematical tool to measure the indeterminacy of breakdowns occurring in production. As an axiomatic mathematical branch, uncertainty theory was developed by a great number of scholars. In 2008, the concept of uncertain renewal process was introduced by Liu [8], and then in 2010 the concept of uncertain renewal reward process was presented by Liu [10]. Following that, by dividing the interarrival time into on-time and off-time, uncertain alternating renewal process was first suggested by Yao and Li [20]. Furthermore, uncertain delayed renewal process was proposed by Zhang et al. [23]. One important application of uncertain renewal process is the uncertain insurance model introduced by Liu [12] in 2013, which is essentially an uncertain process in which the interarrival times and claim amounts are assumed to be uncertain variables and the premium rate is crisp. After that, a theorem to evaluate the uncertainty distribution of ruin time of the uncertain insurance model was proved by Yao and Zhou [22], and a modified model was suggested by Yao and Qin [21] to solve the case in which both the claim process and premium process of the uncertain insurance model have to be considered as uncertain renewal reward processes.

For another important application, Lio and Liu [6] first proposed an uncertain production risk process and calculated its shortage index and shortage time. However, their model assumed that the production process has no any breakdown in every production cycle. This paper aims to modify the uncertain production risk process to evaluate the shortage index and shortage time with breakdowns. The rest of the paper is organized as follows: the modified uncertain production risk process with breakdowns is presented in Section 2. In Section 3, the concept of shortage index with breakdowns is proposed and some formulas are provided for its evaluation. In Section 4, the concept and the uncertainty distribution of shortage time with breakdowns are further given. Some numerical examples are documented in Section 5 and a concise conclusion is reviewed in Section 6.

Uncertain production risk process with breakdowns

In this section, an uncertain production risk process with breakdowns will be given based on the following notation:

Notation

ξ1i: the i-th uncertain on-time, i = 1, 2, ⋯

ξ2i: the i-th uncertain off-time, i = 1, 2, ⋯

ξ1i + ξ2i: the i-th uncertain cycle time, i = 1, 2, ⋯

Nt: the number of production cycle up to time t

ηi: the i-th uncertain production amouts, i = 1, 2, ⋯

Pt: total production amount up to time t

a: initial inventory level

b: demand rate The production problem we concern with is an uncertain production model with uncertain cycle times (i.e., the times consumed by one production cycle), uncertain production amounts and breakdowns. Due to the breakdowns existing in the production process, the uncertain cycle times should be divided into uncertain on-times and uncertain off-times. Let us suppose the uncertain on-times ξ11, ξ12, ⋯ are iid uncertain variables with a common uncertainty distribution Φ1, and the uncertain off-times ξ21, ξ22, ⋯ are iid uncertain variables with a common uncertainty distribution Φ2. By the operational law (Liu [10]), the uncertain cycle times ξ11+ ξ21, ξ12 + ξ22, ⋯ are iid uncertain variables with a common uncertainty distribution

Then the number of production cycles Nt up to time t is an uncertain renewal process. Essentially, the uncertain renewal process Nt is a maximal integer which makes n production cycles finish up to time t, i.e.,

where S0 = 0 and Sn = (ξ11 + ξ12) + (ξ12 + ξ22) + ⋯ + (ξ1n + ξ2n) for n ≥ 1. Moreover, an uncertain renewal process was proved by Liu [8] to have an uncertainty distribution

where ⌊x⌋ is the maximal integer that is less than or equal to x. Now suppose the production amounts η1, η2, ⋯ are iid uncertain variables which have a common uncertainty distribution Ψ. Then the total production amount up to time t can be represented by an uncertain renewal reward process

and it was proved by Liu [10] to have an uncertainty distribution

Here we assume Ψ (x/0) =1 for any x ≥ 0.

Given the fixed values for the initial inventory level a and demand rate b, the definition about the uncertain production risk process with breakdowns is presented as follows:

Definition 2.1. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If a is the initial inventory level and b is the demand rate, then the uncertain production risk process with breakdowns is

where Nt is the renewal process with uncertain cycle times ξ11+ ξ21, ξ12 + ξ22, ⋯

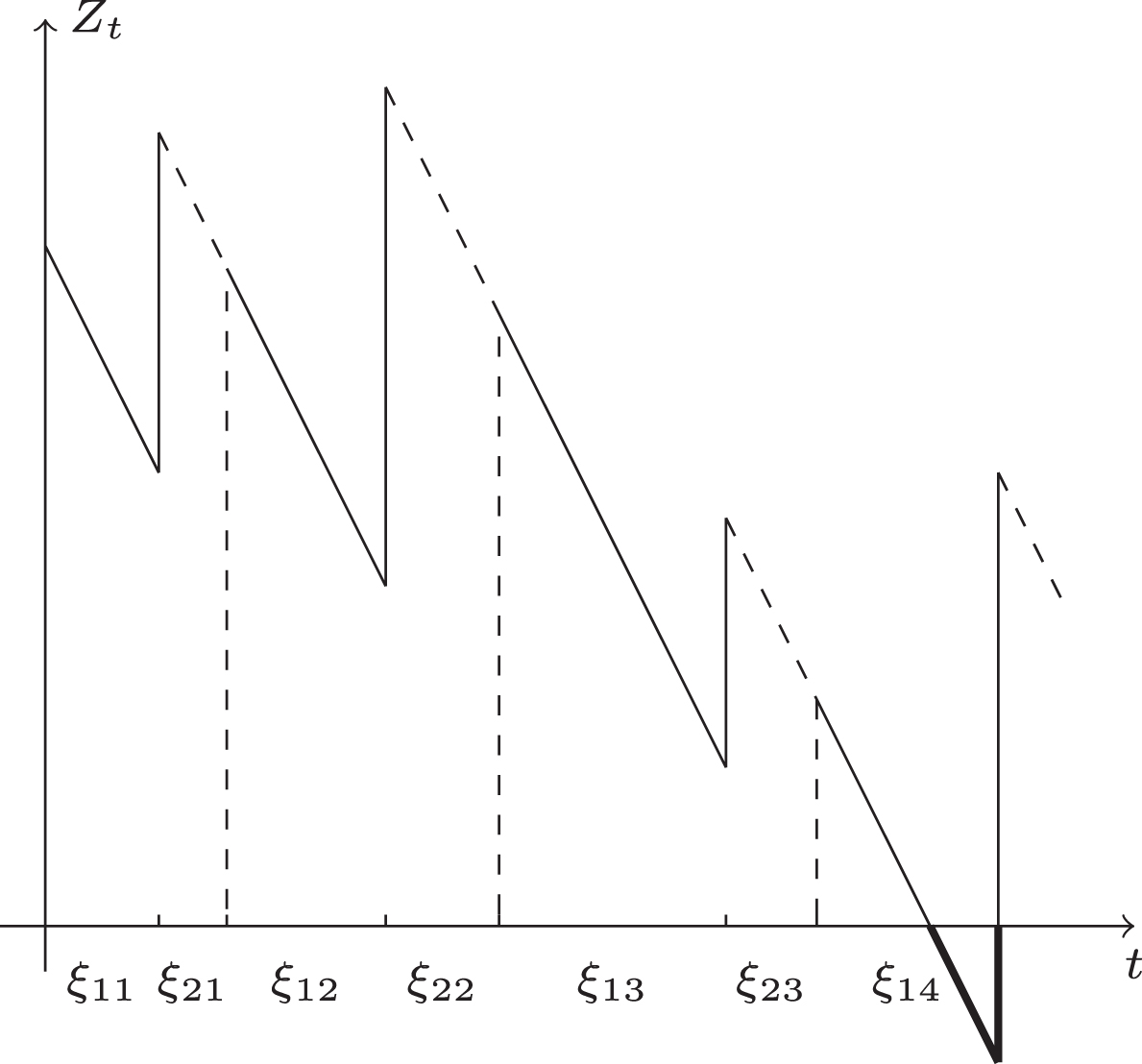

An example of the uncertain production risk process with breakdowns is revealed in Figure 1.

An Uncertain Production Risk Process with Breakdowns.

Shortage index with breakdowns

Shortage occurs when the quantity demanded is greater than the surplus inventory. Due to the breakdowns in the uncertain production risk process, the production capacity decreases or the production planning becomes unavailable. Hence the decision makers have to suffer shortage and solve the trouble caused by production risk. Lio and Liu [6] proposed the concept of shortage index to measure the belief degrees of shortage, but the shortage index was based on the case without breakdowns. Therefore, this section modifies the existing concept of shortage index and introduces the shortage index with breakdowns.

Shortage index with breakdowns is essentially the uncertain measure that the uncertain production risk process with breakdowns becomes negative.

Definition 3.1. Suppose Zt is an uncertain production risk process with breakdowns. Then the shortage index with breakdowns is defined as

Theorem 3.1.Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and those on-times, off-times and production amounts have continuous uncertainty distributions Φ1, Φ2 and Ψ, respectively, then the shortage index with breakdowns isHere we setand

Proof. For each positive integer k, we define an uncertain process indexed by k as follows,

Then Yk is an independent increment process with an uncertainty distribution

It follows by extreme value theorem (Liu [12]) that for an independent increment process Yk with uncertainty distribution Fk (z), the minimum has an uncertainty distribution

Since it is clear that Zt eventually becomes negative if and only if Yk < 0 for some k, we get

The theorem follows immediately.

Theorem 3.2.Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and those on-times, off-times and production amounts have regular uncertainty distributions Φ1, Φ2 and Ψ, respectively, then the shortage index with breakdowns iswherefor each k.

Proof. It follows from Theorem 3.1 that

Therefore, for each k, the optimal solution of the maximization problem (9) satisfies

Now for each k, suppose ) is a solution such that

Then we have

and then

Hence we have

i.e.,

That means ) is also an optimal solution of the maximization problem (9). Then we should have

It is clear that , and

Thus αk satisfies equation (8) and the theorem follows immediately.

Shortage time with breakdowns

For the case that the decision makers cannot prevent shortage, it is necessary to estimate the shortage time when the shortage happens. By regarding the shortage time as uncertain variable, Lio and Liu [6] proposed the concept of shortage time and characterized the shortage time by its uncertainty distribution. However, the existing concept of shortage time is based on the case without breakdowns. Hence this section introduces the concept of shortage time with breakdowns.

Shortage time with breakdowns is essentially the first time that the uncertain production risk process with breakdowns becomes negative.

Definition 4.1. Suppose Zt is an uncertain production risk process with breakdowns. Then the shortage time with breakdowns is defined as

Theorem 4.1.Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and those on-times, off-times and production amounts have continuous uncertainty distributions Φ1, Φ2 and Ψ, respectively, then the shortage time with breakdowns τ has an uncertainty distributionHere we setand

Proof. Please note that 1 - Φ (y1/k) and 1 - Φy2 /(k - 1)) are decreasing with respect to y1, y2 and

is increasing with respect to y1, y2. The proof breaks down into the following three cases. Case I: For any time t satisfying a > bt, we have

for any s ≤ t because it is impossible for Zs to become negative before time t. That means the shortage time τ > t, and then

Furthermore, for any y1, y2 satisfying y1 + y2 ≤ t, we have b (y1 + y2) ≤ bt < a and

for each k. Thus

and equation (11) is proved.

Case II: For any time t satisfying a = bt, it follows from the definition of shortage time that τ ≤ t if and only if the first production has not been finished before time t, i.e., ξ11 > t. Thus

Furthermore, for any y1, y2 satisfying y1 + y2 ≤ t, since we have b (y1 + y2) ≤ bt = a, it can be obtained that

Hence

and equation (11) is also proved.

Case III: For any time t satisfying a < bt, let us define

for each k and time t. Next, we verify that one of the following alternatives holds:

Assume is the supremum solution of equation (12). If k = 1, then and , and we obtain

i.e.,

Thus equation (14) holds. If k ≥ 2 and , then we have

i.e.,

Thus equation (13) holds. If k ≥ 2 and , then we have

i.e.,

Thus equation (14) holds. Therefore, one of the alternatives (13) and (14) holds. Now we are going to get the uncertainty distribution of shortage time τ. On the one hand, it follows from the definition of shortage time that for each t, we have τ ≤ t when

By using equation (13) or (14), we get

On the other hand, it follows from the definition of shortage time that for each t, if τ ≤ t, then we have

By using equation (13) or (14) and Fubini theorem, we get

Hence we obtain

and the theorem is verified.

Theorem 4.2.Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and those on-times, off-times and production amounts have regular uncertainty distributions Φ1, Φ2 and Ψ, respectively, then the shortage time with breakdowns τ has an uncertainty distributionwhereand

Proof. It immediately follows from the alternatives (13) and (14) in Theorem 4.1.

Numerical examples

In this section, two numerical examples for calculating the shortage index and shortage time with breakdowns are presented. Example 5.1. Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and the on-times are linear uncertain variable Ł(10, 12), the off-times are linear uncertain variable Ł(19, 20) and the production amounts are zigzag uncertain variable Z (30, 31, 33), that is, they have uncertainty distributions

and

respectively, then the shortage indices with breakdowns can be calculated. Table 1 reveals some results in different initial inventory levels a’s and demand rates b’s.

Shortage Indices with Breakdowns in Example 5.1

b\a

0.9e+7

1.1e+7

1.3e+7

1.5e+7

1.00

0.3998

0.3998

0.3997

0.3997

1.01

0.4611

0.4610

0.4610

0.4609

1.02

0.5155

0.5154

0.5154

0.5154

1.03

0.5584

0.5584

0.5583

0.5583

1.04

0.6010

0.6010

0.6009

0.6009

1.05

0.6432

0.6432

0.6432

0.6431

1.06

0.6851

0.6851

0.6851

0.6850

1.07

0.7266

0.7266

0.7266

0.7266

b\a

1.7e+7

1.9e+7

2.1e+7

2.3e+7

1.00

0.3997

0.3996

0.3996

0.3995

1.01

0.4609

0.4609

0.4608

0.4608

1.02

0.5153

0.5153

0.5153

0.5153

1.03

0.5583

0.5583

0.5582

0.5582

1.04

0.6009

0.6009

0.6008

0.6008

1.05

0.6431

0.6431

0.6431

0.6430

1.06

0.6850

0.6850

0.6849

0.6849

1.07

0.7265

0.7265

0.7265

0.7264

It can be seen from Table 1 that the shortage index with breakdowns decreases when the initial inventory level a increases, but the values do not change a lot. It is coincident with the intuition that the shortage often occurs after a long time. Also, the shortage index with breakdowns increases when the demand rate b increases.

If the initial inventory level is supposed to be a = 1.5e + 7, and the demand rate is supposed to be b = 1, then the uncertainty distribution ϒ (t) of the shortage time with breakdowns is revealed in Figure 2.

Uncertainty Distribution of Shortage Time with Breakdowns in Example 5.1.

As t tends to infinity, Figure 2 shows that the uncertainty distribution ϒ (t) has a limitation, that is, the shortage index

when a = 1.5e + 7 and b = 1.

Example 5.2. Suppose Zt is an uncertain production risk process with breakdowns, a is the initial inventory level and b is the demand rate. Let ξ11, ξ12, ⋯ be iid uncertain on-times, ξ21, ξ22, ⋯ be iid uncertain off-times, and η1, η2, ⋯ be iid uncertain production amounts. If (ξ11, ξ12, ⋯), (ξ21, ξ22, ⋯) and (η1, η2, ⋯) are independent uncertain vectors, and the on-times are zigzag uncertain variable Z (5, 6, 8), the off-times are zigzag uncertain variable Z (15, 17, 18) and the production amounts are zigzag uncertain variable Z (25, 26, 28), that is, they have uncertainty distributions

and

respectively, then the shortage indices with breakdowns can be calculated. Table 2 reveals some results in different initial inventory levels a’s and demand rates b’s.

Shortage Indices with Breakdowns in Example 5.2

b\a

0.9e+7

1.1e+7

1.3e+7

1.5e+7

1.00

0.4999

0.4999

0.4999

0.4999

1.01

0.5446

0.5445

0.5445

0.5445

1.02

0.5887

0.5886

0.5886

0.5886

1.03

0.6322

0.6322

0.6321

0.6321

1.04

0.6752

0.6751

0.6751

0.6751

1.05

0.7176

0.7176

0.7175

0.7175

1.06

0.7595

0.7594

0.7594

0.7594

1.07

0.8008

0.8008

0.8007

0.8007

b\a

1.7e+7

1.9e+7

2.1e+7

2.3e+7

1.00

0.4999

0.4998

0.4998

0.4998

1.01

0.5444

0.5444

0.5444

0.5443

1.02

0.5885

0.5885

0.5885

0.5884

1.03

0.6321

0.6320

0.6320

0.6320

1.04

0.6750

0.6750

0.6750

0.6750

1.05

0.7175

0.7174

0.7174

0.7174

1.06

0.7593

0.7593

0.7593

0.7592

1.07

0.8007

0.8007

0.8006

0.8006

It can be seen from Table 2 that the shortage index with breakdowns also decreases when the initial inventory level a increases, but the values do not change a lot. Furthermore, the shortage index with breakdowns increases when the demand rate b increases.

If the initial inventory level is supposed to be a = 1.5e + 7, and the demand rate is supposed to be b = 1, then the uncertainty distribution ϒ (t) of the shortage time with breakdowns is revealed in Figure 3.

Uncertainty Distribution of Shortage Time with Breakdowns in Example 5.2.

As t tends to infinity, Figure 3 shows that the uncertainty distribution ϒ (t) has a limitation, that is, the shortage index

when a = 1.5e + 7 and b = 1.

Conclusion

This paper first introduced an uncertain production risk process with breakdowns to handle the production problem with uncertain on-times, uncertain off-times and uncertain production amounts. In order to measure the risk of shortage and rationally prepare for the shortage in the case with breakdowns, the methods of calculating the shortage index and shortage time with breakdowns were presented. Furthermore, for some given initial inventory levels and demand rates, two detailed numerical examples were documented.

Footnotes

Acknowledgments

This work was supported by the National Natural Science Foundation of China Grant (No. 61873329), the Young Academic Innovation Team of Capital University of Economics and Business (No. QNTD202002), and the special fund of basic scientific research business fees of Beijing Municipal University of Capital University of Economics and Business (No. XRZ2020016).

References

1.

BillatosS.B. and KendallL.A., A general optimization model for multi-tool manufacturing systems, Journal of Engineering for Industry113 (1991), 10–16.

2.

BirgeJ.R. and GlazebrookK.D., Assessing the effects of machine breakdowns in stochastic scheduling, Operations Research Letters7(6) (1988), 267–271.

3.

ChristerA.H. and KeddieE., Experience with a stochastic replacement model, Journal of the Operational Research Society36 (1985), 25–34.

4.

GroeneveltH., PintelonL. and SeidmannA., Production batching with machine breakdowns and safety stocks, Operations Research40(5) (1992), 959–971.

5.

KumarR.S. and GoswamiA., A continuous review production-inventory system in fuzzy random environment: Minmax distribution free procedure, Computer and Industrial Engineering79 (2015), 65–75.

6.

LioW. and LiuB., Shortage index and shortage time of uncertain production risk process, IEEE Transactions on Fuzzy Systems, DOI: 10.1109/TFUZZ.2019.2945246, 2019.

LiuB., Fuzzy process, hybrid process and uncertain process, Journal of Uncertain Systems2(1) (2008), 3–16.

9.

LiuB., Some research problems in uncertainty theory, Journal of Uncertain Systems3(1) (2009), 3–10.

10.

LiuB., Uncertainty Theory: A Branch of Mathematics for Modeling Human Uncertainty, Springer-Verlag, Berlin, 2010.

11.

LiuB., Why is there a need for uncertainty theory, Journal of Uncertain Systems6(1) (2012), 3–10.

12.

LiuB., Extreme value theorems of uncertain process with application to insurance risk model, Soft Computing17(4) (2013), 549–556.

13.

LiuB., Polyrectangular theorem and independence of uncertain vectors, Journal of Uncertainty Analysis and Applications1, Article 9, 2013.

14.

MuthE.J., Stochastic processes and their network representations associated with a production line queuing model, European Journal of Operational Research15 (1984), 63–83.

15.

PapadopoulosH.T., The throughput of multistation production lines with no intermediate buffers, Operations Research43(4) (1995), 712–715.

16.

PapadopoulosH.T., An analytic formula for the mean throughput of K-station production lines with no intermediate buffers, European Journal of Operational Research91 (1996), 481–494.

17.

ParlarM., Continuous-review inventory problem with random supply interruption, European Journal of Operational Research99 (1997), 366–385.

18.

RossS., Stochastic Processes, John Wiley, New York, 1983.

19.

WangX., Continuous review inventory model with variable lead time in a fuzzy random environment, Expert Systems with Applications38(9) (2011), 11715–11721.

20.

YaoK. and LiX., Uncertain alternating renewal process and its application, IEEE Transactions on Fuzzy Systems20(6) (2012), 1154–1160.

21.

YaoK. and QinZ., A modified insurance risk process with uncertainty, Insurance: Mathematics and Economics62 (2015), 227–233.

22.

YaoK. and ZhouJ., Ruin time of uncertain insurance risk process, IEEE Transactions on Fuzzy Systems26(1) (2018), 19–28.

23.

ZhangX., NingY. and MengG., Delayed renewal process with uncertain interarrival times, Fuzzy Optimization and Decision Making12(1) (2013), 79–87.

24.

ZhaoR., TangW. and WangC., Fuzzy random renewal process and renewal reward process, Fuzzy Optimization and Decision Making6(1) (2007), 279–295.