Abstract

Central Bank Digital Currency (CBDC) pledges to realize a vast array of new functionalities, such as frictionless consumer payment and money-transfer systems, as well as precise supervision of money circulation, thereby enabling a number of new financial instruments and monetary policy levers. This study proposes, from a system feedback loop and cybernetics perspective, a Dynamic Issuance Mechanism (DIM) for CBDC that can theoretically enhance the vitality of economic operations. In accordance with this mechanism, the central bank implements dynamic issuance by monitoring cash leakage in real-time, so as to maintain the stability of the amount of money circulating on the market, thereby boosting the currency turnover rate and financial vitality. To demonstrate the efficacy of the DIM, we employ the Agent-Based Modeling (ABM) tool to develop a macroeconomic simulation model for qualitative analysis that includes four entities: Central Bank, households, firms, and commercial banks. The multi-cycle operation process of the model includes a variety of economic indicators demonstrating that DIM has the potential to boost economic vitality and social production efficiency without exerting an adverse effect on citizens’ incomes, commodity prices, or the stability of the macroeconomic system. Finally, the function principle and potential risks of DIM are explained from a systems perspective, which offers a novel perspective for the functional design of CBDC and highlights that the hierarchical structure is a meaningful domain as the developmental direction.

Keywords

Introduction

The proliferation of digital currency was made possible by the development of encryption and distributed ledger technologies. Although private release currencies such as Bitcoin and Ethereum served as a precursor to the introduction of these currencies [1], policymakers in a number of nations have begun to cautiously evaluate the prospect of releasing their own Central Bank Digital Currency (CBDC) [2]. The term “CBDC” refers to a virtual digital currency that is based on digital technology, issued, and administered by the central bank of a country or region [3]. According to an analysis of various countries’ plans conducted by the Bank for International Settlements [4], more than one-fifth of the world’s population has begun the process of issuing its own CBDC. China is one of the pioneers in this field and is currently in the lead. Many experts were flabbergasted by the CBDC’s rapid growth, but it also raised some concerns in economics, finance, and other fields [5, 6]. To fully appreciate CBDC’s potential and ensure its benign development, a considerable measure of its aspects such as function, technology, monetary policy, and potential risks necessitate further exploration.

Currently, the overwhelming majority of relevant literature focuses on the potential micro benefits of deploying CBDC, such as cost reductions [7], convenient payment [8], and crime prevention [9]. In contrast, while researchers are aware that CBDC can provide new monetary policy tools [10], there is insufficient research on the specific macro policies and their interaction with the macroeconomy. While some experts argue that implementation risk is modest since CBDC cannot be used to replace paper currency in the near future [11], others remain cautious and believe that the generation of low-risk CBDC revenues should satisfy strict criteria. In specific, some academics asserted that in the case of quantitative data, the income of CBDC is dependent on factors such as the acceptability of various payment methods and the degree of competition in the deposit market [12]. However, some believe that the CBDC must be properly established to promote bank lending, increase deposit funds, and reduce financial instability [13]. CBDC is not a specific single behavior or policy, but rather a complex multi-level system including the underlying technology, application mode, monetary policy, use scenarios, etc., which has led to the emergence of numerous contradictory opinions. Therefore, it is only possible to draw precise and reliable conclusions that can be expanded upon by concentrating on the specific operation mode of CDBC. And this is the research content of this paper.

The focus of this research is on the viable application mode and its implications for the macroeconomy and individuals, including benefits and risks, which have not yet been thoroughly studied as CBDC research is still in its infancy. Firstly, this study proposes a Dynamic Issuance Mechanism (DIM) based on CBDC from the perspective of the system feedback loop and cybernetic theory, which can theoretically eliminate cash leakage in the economic system and boost currency circulation efficiency and economic vitality. Secondly, there is a lack of empirical evidence to support the CBDC theoretical investigation because the typical CDBC has not been utilized in a wide variety of settings for an extended period of time. In order to provide more comprehensive recommendations to the Central Bank and monetary policy-making departments, we utilized the experimental simulation method to simulate and observe the application of CBDC under various conditions in order to conduct a comprehensive analysis of the feasible policies, potential benefits, and associated risks associated with CBDC. Specifically, to qualitatively simulate how macroeconomics works, we utilized Agent-Based Modeling (ABM) tools. The DIM’s efficiency is assessed in depth by comparing key economic indicators before and after its application, such as total goods output, price changes, savings rate, and technological level. Consequently, this study incorporated the system feedback principle to investigate the causes of DIM’s remarkable effect and assess its potential risks. Finally, we discussed the potential evolution of CBDC toward a hierarchical structure by integrating the effectiveness of the mechanism and its inclusiveness to the underlying technology.

Our research is intended to contribute to research and practice in various aspects: First, we review the existing research field on digital currency and CBDC, and propose a viable DIM based on system feedback loops and cybernetic theory and demonstrate its efficacy, which explores the CDBC’s application potential from the perspective of monetary policy and policy-making institutions. Secondly, this study extends the ABM tool to the CBDC domain. ABM can observe the law of system operation by simulating entity (agent) behavior and interaction between entities, thereby expanding the research tool in CBDC from the system perspective and allowing researchers to focus more directly on the potential macroeconomic impact of CBDC in the absence of empirical evidence. Thirdly, the economic model we present under the operation of DIM also addresses the lack of macroeconomic dynamic modeling and conclusion in the context of CBDC application, thus contributing to the CBDC literature. In conclusion, based on the results of the DIM application, we explore the evolution of CBDC toward a hierarchical structure.

The remaining sections of the paper are structured as follows. Section 2 explains the specific DIM based on the CBDC. Section 3 describes the technical aspects of ABM pertinent to the study. Section 4 discusses the macroeconomic simulation model and operating conditions for DIM. The operation results of the simulation model are presented in Section 5 and discussed in Section 6. The entire body of the work for the study is concluded in Section 7.

A Dynamic Issuance Mechanism

According to the description of system control in cybernetics, as people obtain more information from the system, their comprehension of the system improves, which paves the way for the possibility of more precise control methods [14]. The CBDC application enables the monitoring of previously unmeasured cash flows, such as household consumption. Along with the numerous widely discussed micro benefits of CBDC, including effective allocations [15], prevention of economic crimes, payment methods [16], exchange efficiency [17], and tax evasion [18], some researchers have started to discuss the efficient and controllable monetary policy based on CBDC from its technical characteristics [19]. However, it is still insufficient to explore control methods from a system perspective that studies the interactive relationship and dynamic operation process between the application of CBDC and various economic agents [20]. In light of the pervasive issue of cash leakage in today’s paper money (currency), we, therefore, propose a DIM based on the effective information tracking properties of CBDC. In addition to increasing the effectiveness and vitality of the currency cycle, the mechanism aims to avert cash leakage through currency issuance process.

Cash leakage has long been a concern in the traditional monetary policy issuing process, as it compromises the accuracy of money issuance and the operational efficiency of the economy [21]. In the field of macroeconomics, it is widely held that the cash leakage rate is inevitable under the current conditions, and that the impact can only be mitigated by a suitable monetary issuance policy [21]. From a systematic standpoint, however, the issue of cash leakage that traditional currencies face cannot be resolved since the currency issuers are unable to accurately monitor the leakage and, as a result, cannot carry out an accurate currency supply. Thus, the application of CDBC offers economic management departments a more effective and streamlined method of systematic monitoring, which may contribute to the innovation of money issuance and regulation policy [22], which is the prime objective of the DIM.

In the study, we propose the DIM, which enables the Central Bank to monitor the amount of money held by households (cash leakage) in the economic system in real-time via CBDC and dynamically allocate the same volume of money to commercial banks. This system achieves its objective of precisely managing and ensuring the market’s cash supply remains constant. In addition, the Central Bank will issue money in a dynamic manner in response to the amount of cash that households have on hand (cash leakage). The dynamic issuance can be expressed by Formula 1:

In Formula 1, B

i

represents the amount of money issued by the Central Bank to commercial bank i, X

j

is the amount of money owned by household j but not used for economic activities. The number of commercial banks in the economy is n and the number of households is m. Based on the above conditions, the Central Bank’s issuance rules in each cycle t are as Formula 2:

In Formula 2 Bt,i represents the amount of money transmitted by the Central Bank to commercial bank i iperiod t, Xt,j represents the amount of money owned by household j but not used for economic activities in cycle t k

i

represents the proportion at which the Central Bank allocates all manipulated currencies to commercial banks i, which satisfies Formula 3:

Theoretically, on the basis of the DIM, the Central Bank can directly regulate the quantity of currency (money) in circulation and maintain a constant level to prevent fluctuations caused by cash leakage. This mnism satisfies both the demand for money storage and does not hinder the efficiency of money circulation, compared to the conventional system. In the section on system model operation, the consequences of the DIM will be discussed in depth.

Agent-based modeling and simulation (ABMS) is a novel modeling technique for systems composed of autonomous, interacting agents [23]. The ABM approach is extensively utilized to study complex systems that have not been mathematically formalized, including fields of the social sciences such as economics, communication, psychology, and others [24, 25]. Equations are able to be applied to formally describe the behavior of each entity as well as their interactions since the agents in the model can represent entities such as organizations, corporations, firms, or countries and their interactions. Therefore, it is easier to evaluate the influence of entity behavior differences (“heterogeneity”), random effects, or changes (“randomness”) under rules [26].

Currently, the majority of CBDC research focuses on its function and characteristics, while the relationship between CBDC and the economic system receives less attention. The systematic feedback of CDBC caused by the change of time dimension and its impact on the entity level should be included in the CBDC research scope. This study thereby adopts the ABM tool to simulate the macroeconomic scenario with CBDC so that the researchers can gain a better understanding of the potential effects that the implementation of CBDC could have on the functioning of the economy. The details of the macroeconomic simulation model will be shown in Section 4.

Agent-based modeling method

Model synopsis

Base model: Model conceptualization

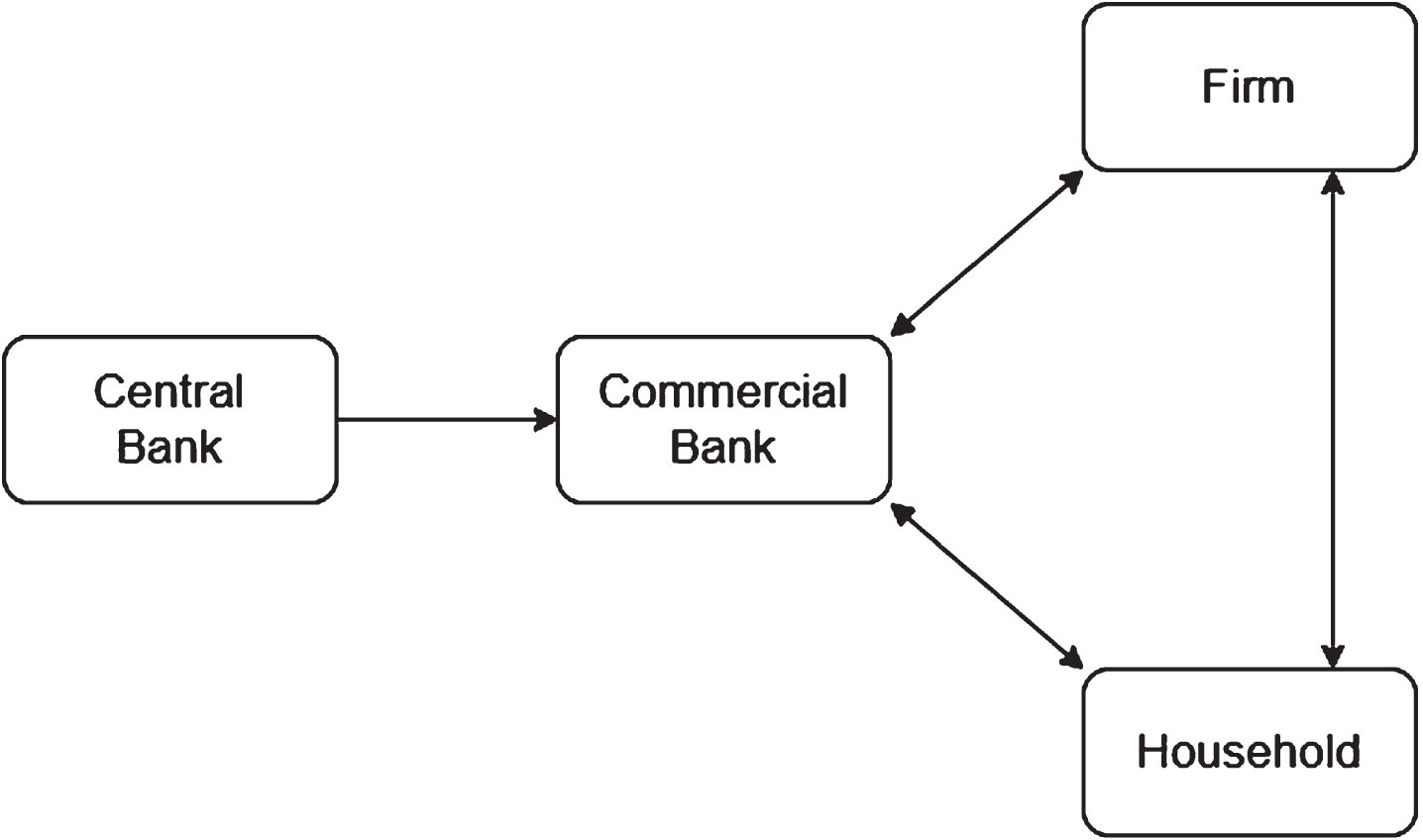

According to Samuelson’s theory, the functioning of the macroeconomy can be reduced to the interactive relationship between the government, firms, and households [27]. In addition, some scholars have demonstrated that the financial sector should be regarded as the fourth main entity in economic operation since its role in the macroeconomic operation is distinct from that of general firms and organizations [28]. Some researchers in the field of CBDC have also attempted to establish a DSGE interaction model among households, central banks, and commercial banks [29], while others have focused on the (static) economy with banks, firms, and households [30], or households, financial investors, unions, banks, and a government [31]. This study analyzed the various division methods of economic entities in the macroeconomic field and selected four types of economic entities in the macroeconomic operations from which to construct the economic operation model. Financial institutions represented by Commercial Banks, natural-person households, firms producing general goods, and the Central Bank, which regulates the money supply and monetary policy on behalf of the government, are the four types of entities. Figure 1 and Table 1 illustrate the interacting link among the four types of entities.

Interaction pattern between entities in the model.

Introduction of the entities in the model

In addition to the attributes of the entities (agents), the modeling approach emphasizes the interaction between them. The interaction between agents alters the state of the agents and the system’s operation. In this study, interactions in the simplified macroeconomic system can roughly be divided into three categories: Money Interactions, which include the flow of currency issued by the Central Bank to commercial banks or payment behavior when trading commodities; Commodity Interactions, which include the supply of goods to households and other firms; and Information Interactions, which include the Central Bank’s detection of household cash leakage and the households’ issuance of goods. It should be noted that the model is a system operation model for qualitative analysis to verify the effectiveness of the DIM, rather than a quantitative economic model. Therefore, the design of model details is only utilized to fulfill the description of available qualitative economic theories and carried out to investigate the qualitative differences that existed prior to and subsequent to the implementation of the DIM.

The interaction between the four entities can be classified in the following manner. Consumption between households and firms is the largest contributor to GDP. Since the 1950s, a succession of models of consumer behavior have been proposed [32]. In this study, consumption is viewed as a function of available household cash (personal income), the price level, and the personal demand coefficient. Sales correspond to purchases and are influenced by numerous factors. A concise perspective is that price-reduction activities are positioned based on the duration and proportion of the retail assortment involved [33]. In this study, the sales price is determined using the sales price and surplus from the previous period. If there is a surplus of goods, the firm will reduce prices to maximize profits, and vice versa. (There is only one general commodity that is used to denote all types of goods.) It is important to note that the purchasing behavior of firms is discussed separately. The purchasing behavior of firms is highlighted individually to illustrate the investment and growth of firms, despite being nearly identical to that of households [27]. Salary payments are made to employees after labor and production activities have been performed by employees, when the firm employs laborers from households. This model randomly assigns each household to a firm at the start of the procedure to simulate the employment relationship in the real world. (In order to focus more on the feedback loop, this model does not address household layoffs and rehiring, as well as corporate insolvency and registration.) The salary paid by firms is influenced by the average salary on the market and the firm’s current cash flow [34]. The personal talents of the employed households, the firm’s capital status, and the firm’s technical level influence the output efficiency of the firm [35]. In this scenario, in addition to the interaction between households and firms, commercial banks serve as the market’s financial institutions. They provide households with interest on deposits that are obtained from the households [36]. In addition, they charge periodic interest on the controlled cash they lend to firms [37]. The interest rate on households is fixed. The interest rate charged to firms is influenced by the funds held by banks and the firm loan market situation. The rate of interest on a business loan cannot be lower than the rate of interest on a family deposit. The interactions between entities are depicted in detail in Fig. 2 and Table 2.

Interaction between the entities in the model.

Model entities, interactions and details

Simulation scenarios

The model simulates economic activity using the natural month under the real-world scenario as a cycle and tracks each index at the conclusion of each cycle. The paper then discusses the effect of the DIM on the macroeconomic operation by examining various indexes during the 120-week operations of the economic model before and after the DIM implementation.

In addition, it is worth pointing out that we simplified several macroeconomic operation details in this model to better account for the impact of the CBDC application on the macroeconomic operation. The first is the excessive issuance of currency by the Central Bank. Due to the short observation timespan of only ten years, this research model does not consider the excess currency. On the one hand, it can simplify the model to observe the constant state of the total amount of currency and the amount of money in circulation prior to and after the adoption of DIM. On the other hand, it can obviate the need to evaluate the precise proportion of benign policy for money issuance. Secondly, the amount of money that can be utilized as a measurement of the model’s monetary value is applied as the monetary measurement of the model rather than the concept of the money multiplier, which is not introduced in this research. It, therefore, avoids analyzing how the deposit reserve ratio of the Central Bank influences the money multiplier but has no effect on the cash leakage rate. The model selected the final currency circulation without considering the currency multiplier as its own currency.

Model building and observation

The ABM tool is used to assist in the process of developing the simulation model [39, 40]. NetLogo, a multi-agent programming language and modeling environment for simulating natural and social phenomena, was used to run the simulation [41]. It features a graphical user interface and a corresponding coding interface, allowing researchers to easily develop the behavioral logic of numerous agents, simulate them, and observe the consequences of their behavior [42]. Since its inception in the complex system community, NetLogo has been successfully utilized in a vast array of organizational research [41, 43]. Software version 6.2 of Netlogo is implemented to complete this research model. The model is available for download at github.com/LvAobo/ABM.

To construct the model, this study uses a variety of widely used indices derived from actual economic operations to evaluate model performance and compare policy effects: the Distribution of Currency (Money) Among Entities, a healthy economic society should have a stable or periodic distribution of currency (money) among different entities. Consequently, determining whether DIM would result in changes to the wealth structure should be our leading priority. The Total Amount of Goods Production, which is the amount of consumption in the model for each unit cycle, corresponds to the Gross Domestic Product (GDP) in the actual world; The Price Index measures the variation in the average price of goods during each model cycle. Average Scientific and Technological level, reflects the average level of scientific and technological development in a society; The savings rate of households and the loan volume of firms are indicators of the operation of financial institutions.

Result

With the original parameters of the model intact, it is run over 120 cycles with and without DIM application. Due to the stability of model results under the same conditions, this article will present the two sets of results listed below. The following table provides a summary of the changes in various observation indicators throughout the operation of the model.

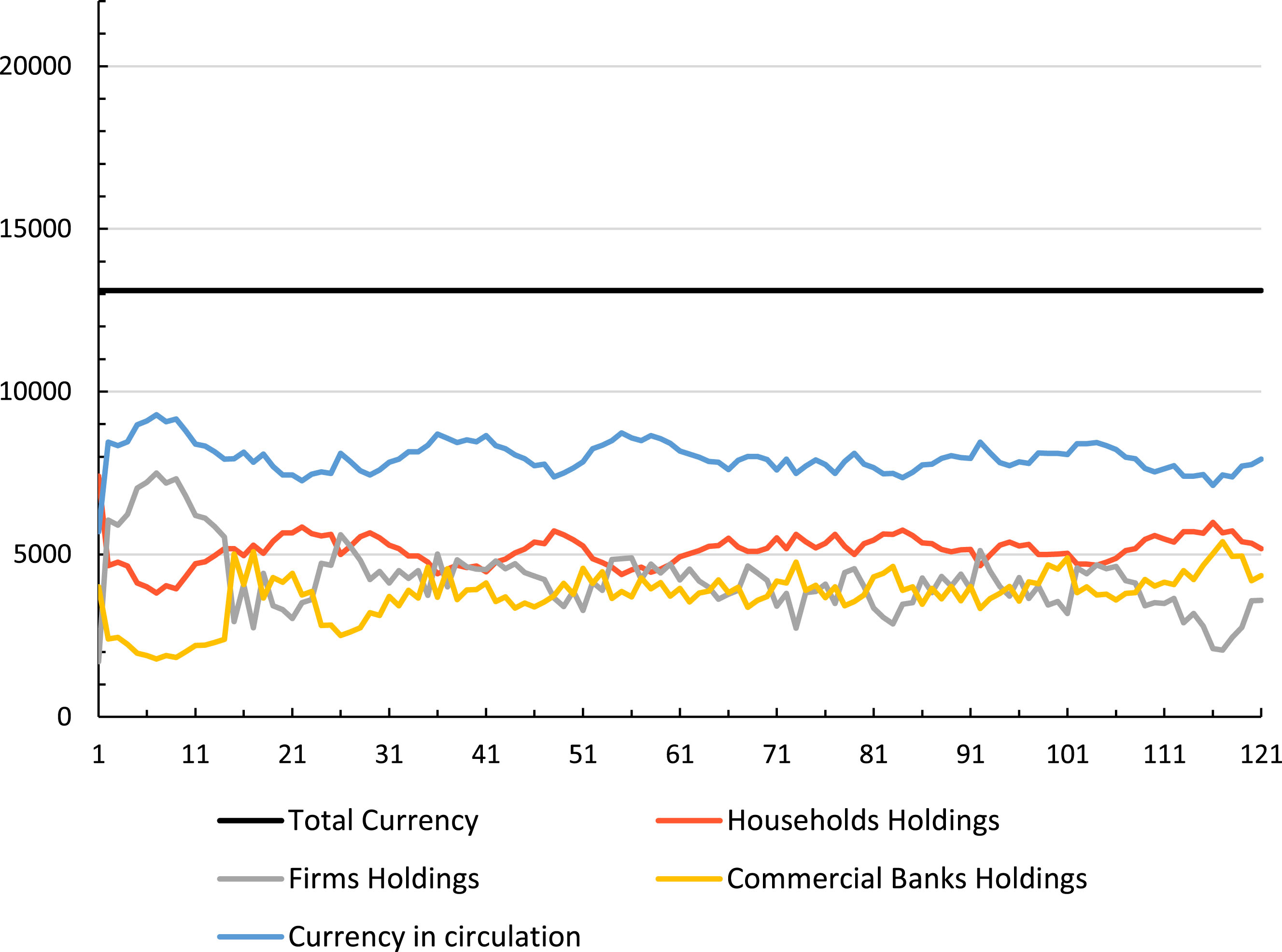

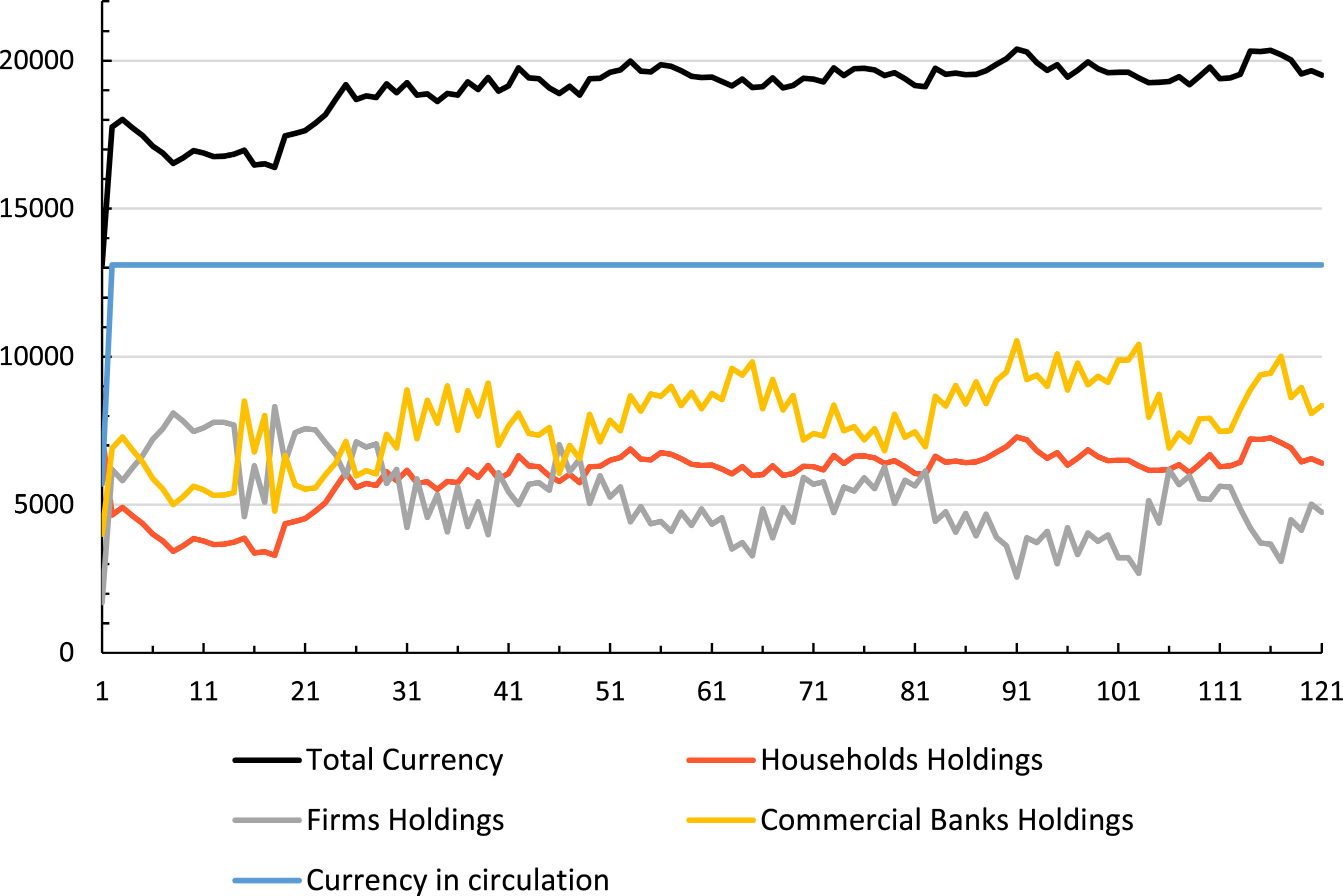

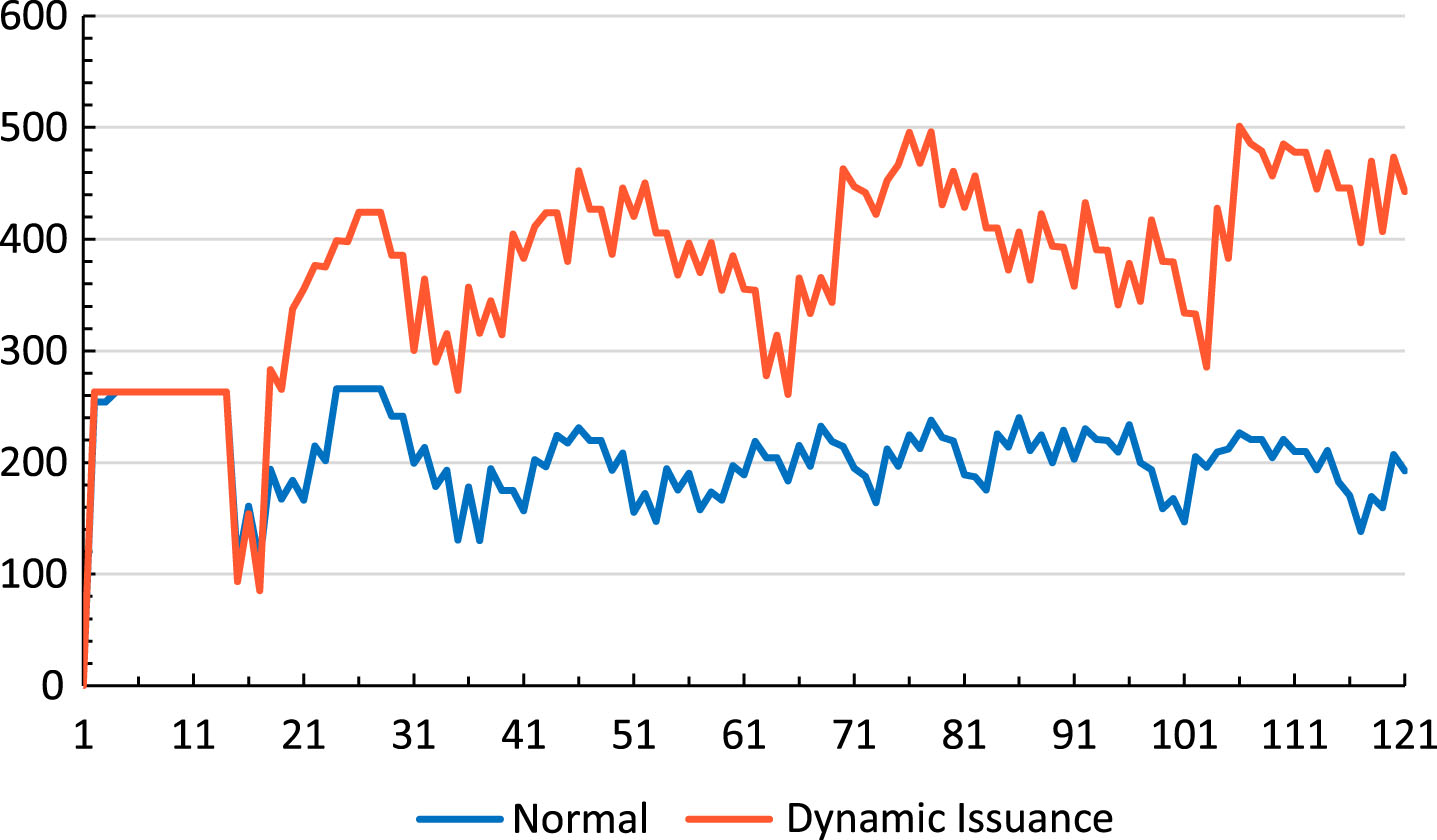

Figures 3 and 4 depict the variations in currency (money) held by each entity throughout the operation of the model. Figure 3 depicts the money distribution under normal circumstances. It can be observed that the total amount of currency in the economic system has not changed during 120 cycles (the model does not consider the problem of over-issuance of money). In this period, the model only considered the money circulation relationship between commercial banks, firms, and households, and the sum of money held by commercial banks and firms, which is the amount of money circulating in the economy fluctuates greatly at this time. Its changing trend is inversely proportional to the amount of money held by households (leakage cash). Figure 4 depicts the distribution of funds under the DIM. In this scenario, the initial values are typical of typical conditions. Throughout the operation, it is evident that the Central Bank first provided a significant amount of cash to commercial banks in proportion to the volume of cash leakage and maintained the total amount of money in circulation in the economic system for 120 cycles at the initial total amount. The changing trend in the amount of cash held by households (leakage cash) corresponds to the changing trend in the total amount of money, whereas the changing trend in the amount of cash held by commercial banks and firms exhibits mirror symmetry. Within 120 cycles, the proportion of money held by households, firms, and banks remained relatively stable, with no discernible capital flow to a specific entity.

Currency distribution under the normal situation.

Currency distribution under the Dynamic Issuance Mechanism.

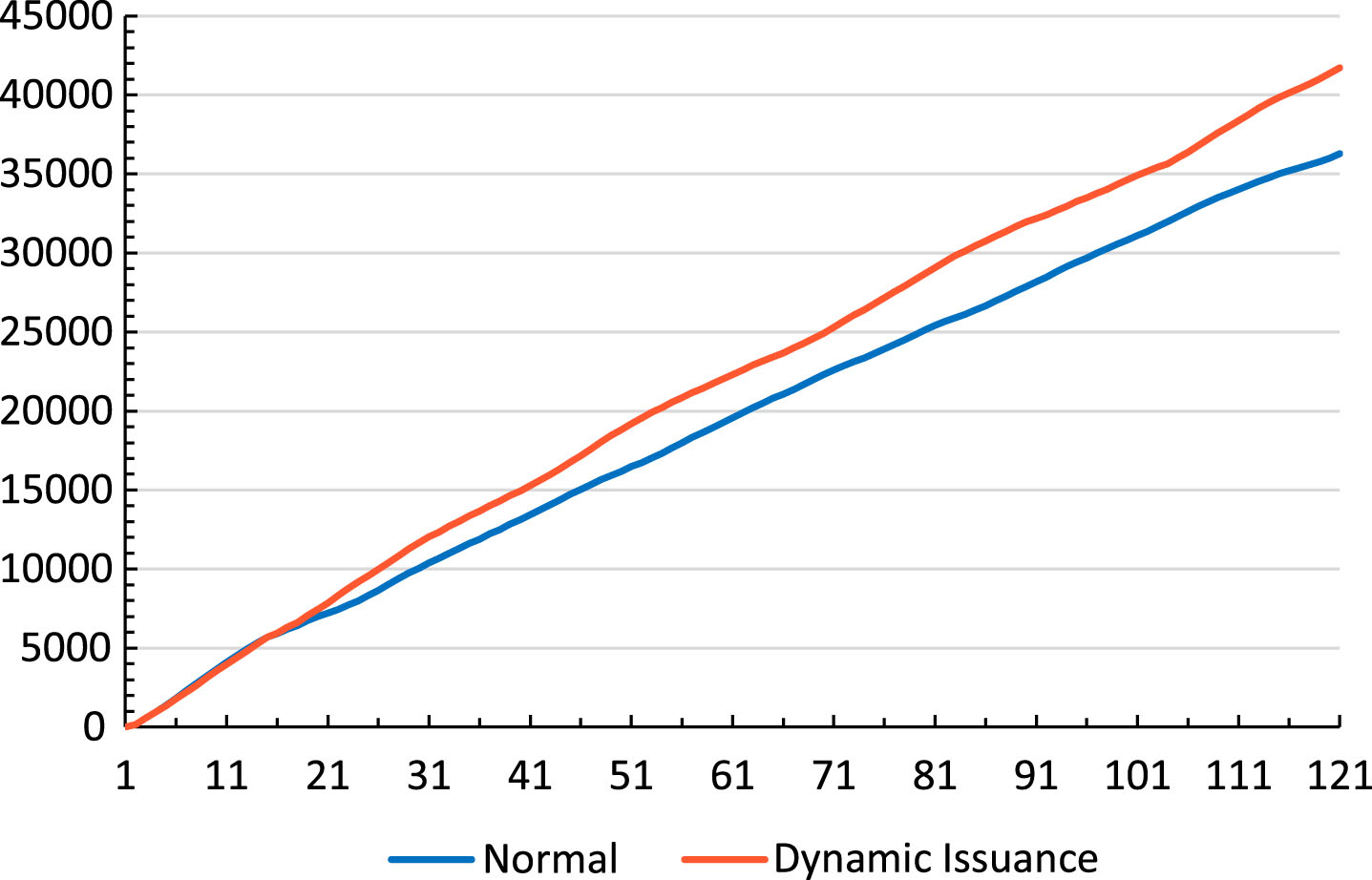

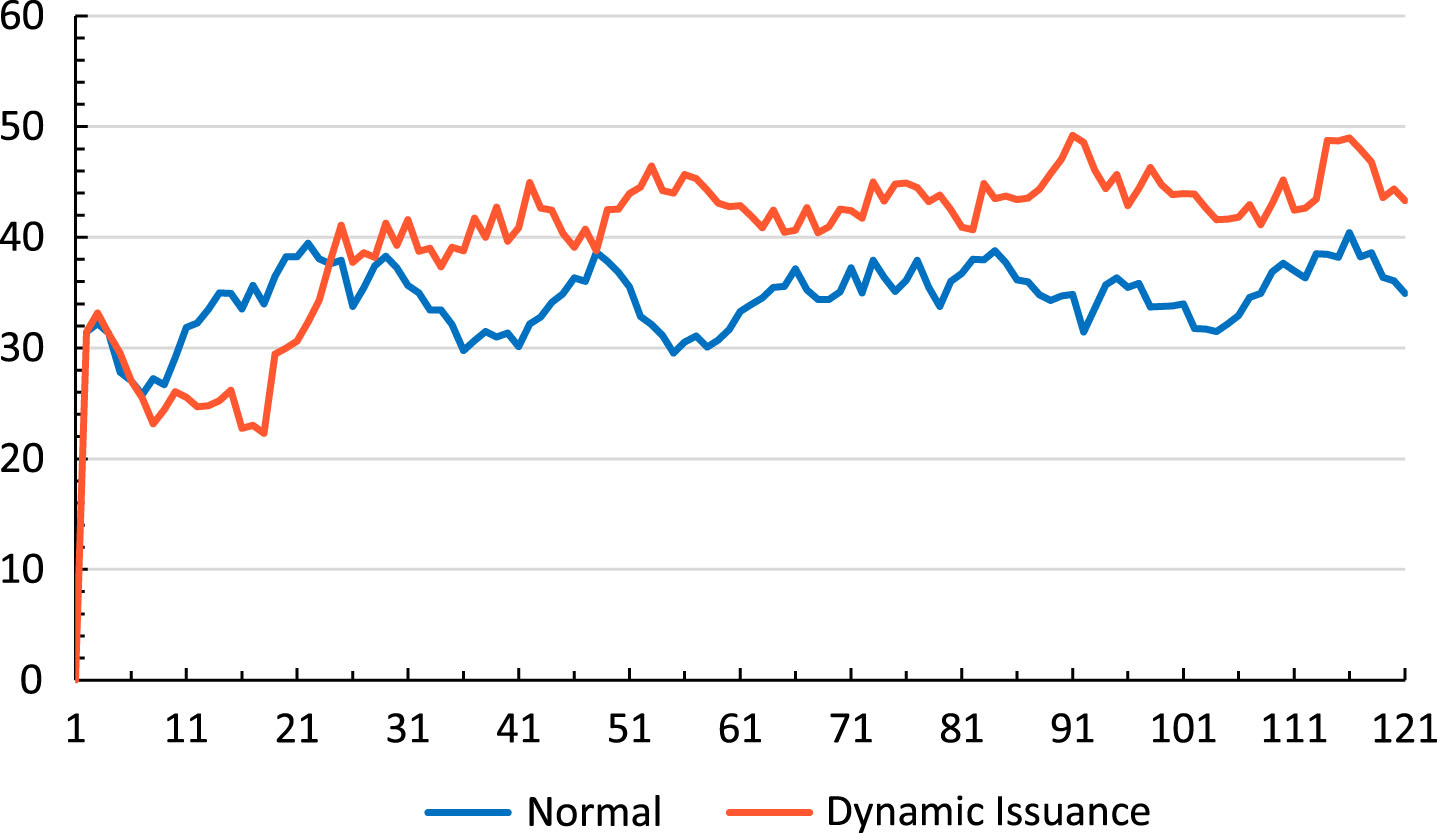

Figure 5 depicts the changes in the total quantity of goods produced by the economic system during the operation of the model, also referred to as gross national product (GDP). The blue line represents the change in total production volumes under normal conditions. Within 120 cycles, 36,277 items of goods were produced by the economic system. As a result of the DIM, the red line depicts the change in total production quantities. Within 120 cycles, the economy produced 41,729 items, which is 15% more than if the DIM had not been implemented. In addition, the DIM economic system causes the slope of the commodity production curve to increase uniformly when compared to a conventional economic system.

Total goods production volume.

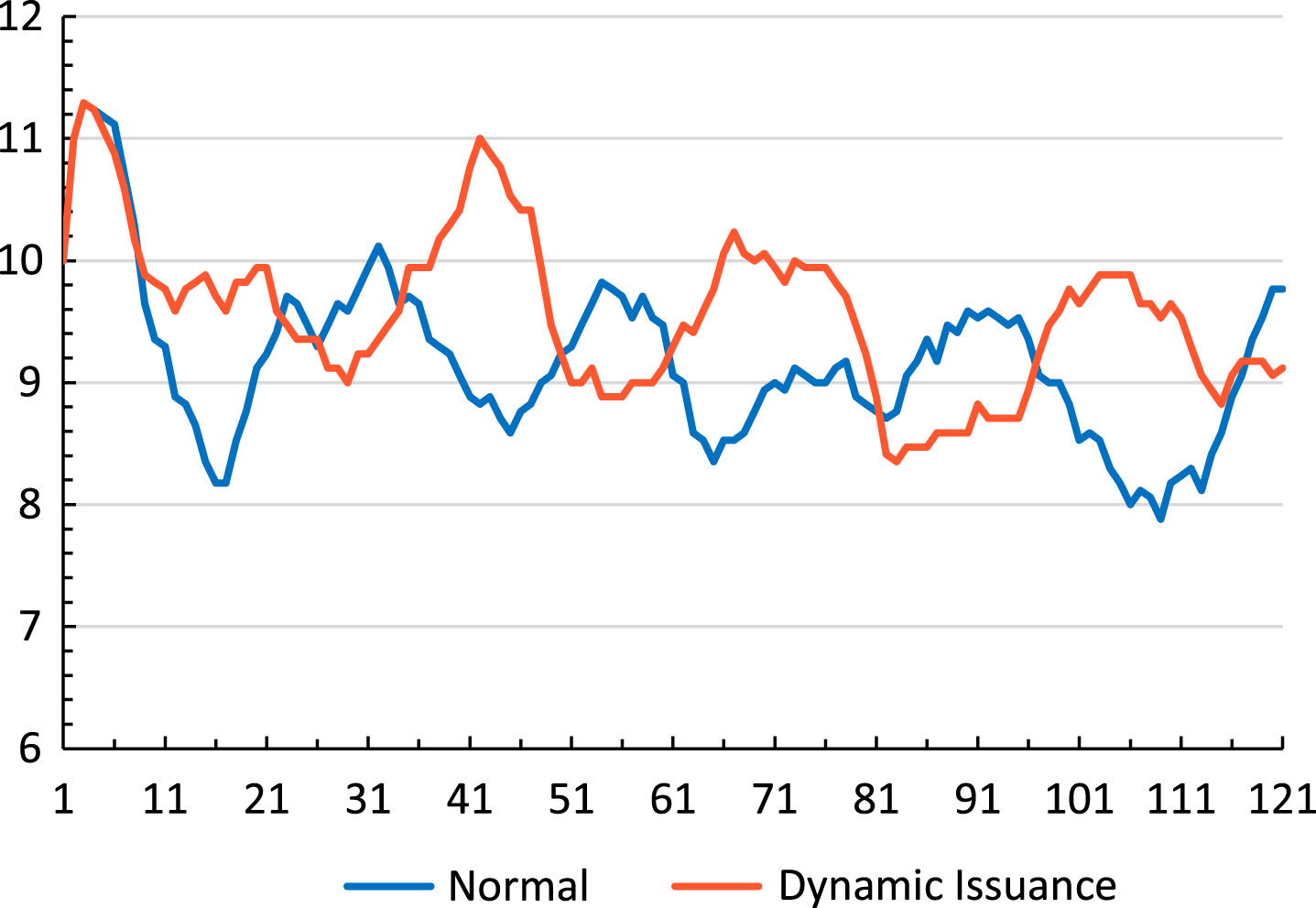

Figure 6 depicts the varying average price of goods in the economy over the course of the model’s operation, which is referred to as consumer pricing. The blue line represents the variation in the average commodity price under normal circumstances. The price of goods frequently fluctuated over a period of 120 cycles (the fluctuation interval is 25), with a small fluctuation range and an average price of 9.16. The red line represents the fluctuation in the average price of products subject to the DIM. The fluctuation range was comparable to the average one even though the average price stayed at 9.57, which is 5% higher than usual. Additionally, under the DIM, the goods price fluctuation interval decreased significantly while the average fluctuation interval increased to 30 cycles, showing that the mechanism has, to some extent, lengthened the cycle of economic fluctuations. Figures 3 and 4 illustrate that when the total amount of money in the economy and the amount of cash held by households both increase substantially, the average price remains relatively stable. Despite the fact that the total volume of currency increased (45%) in comparison to the change in the total volume of goods (15%), the average price did not fluctuate significantly (5%).

Average goods price fluctuation.

Figure 7 depicts the evolution of the average technological level (equipment level) of the economic system during the operation of the model. The blue line depicts the typical change in the technological level of a firm under normal conditions. After 120 cycles of economic system operation, the average enterprise technology level is 1.12, a 13% increase from its initial value. The red line represents the average scientific and technological level of firms after 120 cycles of operation with the DIM, which is 1.35, a 35% increase over the initial value and 191% faster than under normal circumstances, demonstrating that the DIM encourages firm reinvestment and explains why the economic system’s production of goods increased.

Firm technological level changes.

Figures 8 and 9 depict the changes in the average amount of household savings and the average amount of firm loans in the economic system during the operation of the model. The blue lines represent changes that occur under normal conditions, while the red lines represent conditions that occur under the DIM. While an increase in household income resulted in a slight increase in average household savings, from 34.2 to 39.7 on average over the entire cycle (a 16% increase), the number of corporate loans increased significantly, from 203.9 to 371.9 on average over the entire cycle (an 82% increase), due to the amount of currency dynamically paid to commercial banks by the Central Bank, thus explains why firms are able to achieve accelerated technological advancements.

Average household savings.

Average firm loans.

Analysis of system feedback loop changes.

Cause analysis

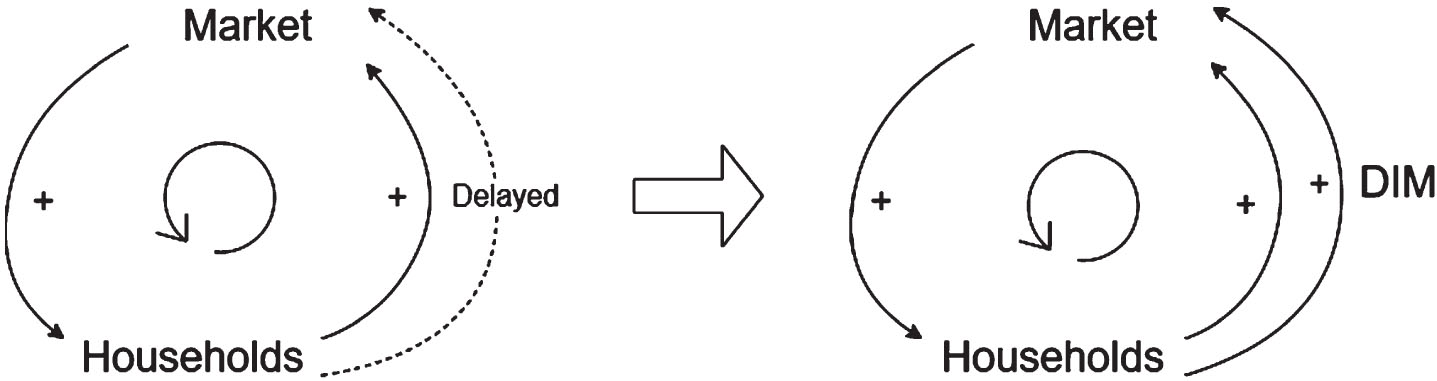

The results of the model simulation indicate that the DIM augments economic production efficiency without affecting prices by preventing cash leakage throughout the application process. The use of DIM will have a positive impact on the economic system, notwithstanding the fact that the qualitative analysis model’s results cannot be used to draw rigorous quantitative conclusions. We believe that increase operational efficiency is contingent upon minimizing cash leakage, which ensures that money is always circulated at the optimal multiplier [27]. Moreover, the variation in efficiency caused by the total amount of currency in circulation is eliminated. Systematically, macro currency (money) circulation creates a positive feedback loop between the household and the market, in which a change in one direction causes another change in the same direction [44]. However, since money is retained in the family for a protracted period and is not included in the feedback loop, cash leakage contributes several delayed inputs to the positive feedback loop. The DIM precisely reduces cash leakage through the dynamic money supply regulation carried out by the bank. By eliminating the delayed feedback cycle present in the traditional currency scenario, it achieves real-time stability and the most efficient positive feedback flow between market households. This is followed by optimizing the system’s operational efficiency.

It is crucial to recognize that there is a distinction between the DIM and the interest-bearing CBDC. Since the CBDCs currently under consideration are predominantly of the non-interest-bearing variety [30], DIM can better adapt to the current CDBC mode and achieve economic operation efficiency. Moreover, the policy of directly issuing interest to any CDBC does not involve direct currency issuance. For the entire macroeconomy, the total amount of money with higher interest rates may continue to exist as “cash leakage,” or it may enter the commercial banking system as deposits and contribute to “money creation.” If the central bank puts this fraction of money into commercial banks while monitoring CBDC data, it will participate in “money creation” as a whole, and create the total amount of money for the entire society with a money multiplier of approximately 1/ legal deposit reserve ratio, thereby achieving the effects of a loose monetary policy, such as stimulating investment and consumption.

Risk analysis

Despite the fact that the DIM offers the aforementioned benefits, there are risks associated with its operation. In essence, the way to reduce cash leakage is to allow the central bank to temporarily transfer household cash to commercial banks for savings. This method transfers the risk associated with household capital investment to the Central Bank. This transformation necessitates that the Central Bank, a risk-averse organization, assume the potential risks associated with households leaking cash for investment and then release the circulation vitality of this portion of funds. However, since commercial banks have acquired more liquidity funds, they will focus on investment objects with a higher risk profile than their traditional business scope, thereby increasing the risk of commercial banks. This change may be viewed as a prudent step toward encouraging innovation and reviving entrepreneurial vitality within the context of a thriving and expanding economy. Nevertheless, given the deteriorating economic conditions, it will also increase the investment risk of commercial banks, thereby increasing the risk to the economic system.

However, it is important to note that this high risk corresponds to high yields in similar interest-bearing CBDC models. Moreover, according to a number of studies, the implementation of CDBC carries the risk of reducing the amount of bank savings, and even a modest loss of deposits is sufficient to generate significant funding gaps for the banking sector, which will trigger repercussions throughout the financial network [45]. However, compared to the interest-bearing CBDC model, DIM will not directly influence the behavior and preferences of families and individuals, thereby minimizing the likelihood of such risks.

Central bank digital currency development outlook

The implementation of CBDC has led to significant shifts in a variety of spheres, ranging from the underlying levels of technology to the top levels of monetary policy (such as DIM). The CBDC application framework has not yet been developed; however, we anticipate that its operation style will be hierarchical, similar to that of the Internet, with little interaction between the various encapsulation layers and layers supporting the upper layer [46]. The technical feasibility of a CBDC design with a two-tier or multi-tier ledger is currently being researched by some researchers [47]. Nevertheless, we reckon that the multi-level architecture design should extend beyond the technical level, as focusing too much of the conversation on technologies, such as blockchain— will limit our capacity to innovate in the development of CBDC. This paper, for instance, analyzes the potential for policy flexibility enabled by the traceable characteristics of CDBC and simulates the policy’s effectiveness at the level of monetary policy (CDBC policy). This study glosses over the technical details of the bottom layer of CDBC, demonstrates the changes that CBDC can bring through an examination of innovative monetary policy applications, such as DIM, and examines the viability of exploring the development of CDBC on multiple levels. Thereby, in order to fully explore the potential advantages and changes of CDBC based on the premise of resolving the compatibility issues in the bottom layer, the author proposes that scholars in the field of CDBC research should deem CDBC as a multi-level application system, establish a unified CDBC hierarchy, and analyze the mechanism of each layer.

Conclusion

This paper offers a synopsis of the previous research on CBDC and, in conjunction with the technical aspects of digital currency, renders a proposal for a DIM based on CBDC from the perspective of system feedback loop theory and cybernetics. The mechanism seeks to resolve the issue of currency issuance cash leakage while enhancing the liquidity efficiency and vitality of currency. Whereupon, based on the findings of concluded macroeconomic research, we utilized ABM tools to simulate the operation of macroeconomics. By comparing several economic indicators before and after the implementation of DIM, such as total production, price fluctuations, savings rate, and technological level, the effectiveness of the mechanism is evaluated in depth. To further explore the rationale behind the remarkable results of DIM and weigh the associated risks, this study applied the principle of system feedback. Finally, we covered the prospect of CBDC development in a hierarchical framework by fusing the effectiveness of the mechanism and the inclusiveness of the underlying technology.

Contributions

This study has made contributions to the field of macroeconomy and CDBC in four aspects: Firstly, this study presents a pioneering discussion on the subject of CDBC regulation (monetary policy), and proposes an innovative DIM from the perspective of cybernetic and system feedback. The DIM raises public awareness of CDBC monetary policy and offers suggestions to the CDBC regulatory departments by promoting economic benefits and enhancing the quality of life for residents. Second, in contrast to previous empirical or theoretical research models on the subject, our simulation analysis of the potential effects of CDBC is novel. By introducing ABM tools and focusing on the system’s perspective, this study provides a unique contribution to the field of CDBC research. As CBDC has not yet been widely adopted in any region, system-level analysis and methods such as ABM can partially compensate for the absence of empirical evidence, providing a more thorough and sensible approach to CBDC utilization. Thirdly, this study illustrates the practical utility of CBDC and increases public awareness of it. By confirming and analyzing the effectiveness of the DIM model based on CBDC, this study reaches a number of intriguing conclusions, such as the vitality of economic operation, stable prices, and the level of social scientific-technological advancement. When the findings of previous studies are compared [12, 48], it is evident that the CDBC with DIM has produced more significant results in those indices. In addition, the findings of this study challenge several preconceived notions regarding CBDC. For instance, some studies argue that while CBDC implementation generally improves welfare, it also squeezes bank deposits, increases bank financing costs, and reduces investment [49]. This study, on the other hand, demonstrates how CDBC policy (DIM) can be utilized to increase investment and enhance welfare. These findings will contribute to and broaden public awareness of CDBC as a new monetary medium, in addition to shedding light on the study of ’its other application effects. Fourth, in light of the impact of CDBC policy, we examine the development orientation for CBDC. The remarkable effect of the DIM and its independence from underlying technology lends credence to the viability of advancing CBDC toward a hierarchical framework design. In contrast to the existing framework for CBDC evaluation [50] and project management, the proposed hierarchical structure regards the CBDC as a multi-independent level application [51].

Limitations of this paper and future directions for research

It should be acknowledged that there are still some limitations in our research: The first relates to the simplification of the model. The research model reduces economic entities, market circulation commodities, and the interaction between domestic and international markets in order to provide a more straightforward and succinct simulation of economic operation. While this model highlights the emphasis of the study and the qualitative conclusion has not been compromised, it has to be recognized that the simplification leaves out some potential effects of DIM, which should be accounted for in subsequent research. Second, the theory will have a direct impact on the operation results since the model is founded on macroeconomic conclusions. In the field of macroeconomics, numerous details of macroeconomic operation are still the subject of contention. Consequently, whilst the model of this study is based on widely-accepted economic theories, future research must address the robustness of conclusions drawn from different theories. Finally, the results of this study cannot be supported by empirical evidence. It is impossible to obtain empirical data to support the conclusions as CBDC has not been widely implemented in any region and the DIM is an original concept of this study. This, however, does not hinder the pioneering discussion and theoretical contribution that the qualitative analysis model in this study provides.

Based on the aforementioned limitations, the subsequent stage of this study will simulate more complex macroeconomic activities in order to strengthen the conclusions of the study. In the meantime, additional economic operation data will be used to assess the validity of the quantitative operation model that will be developed in the future. One of the research’s further areas of inquiry shall encompass the examination of the CBDC hierarchy. Clarifying the CDBC hierarchical structure will facilitate our projections for its long-term growth.

In brief, the ultimate objective of this study is to propose the DIM based on CBDC, demonstrate its efficacy through simulation experiments, and introduce ABM to the field of digital currency and CBDC from a system perspective. Thereby, we have contributed to the migration of ABM to the field of CBDC, while also advancing CDBC policy and demonstrating its potential. We invite additional researchers to look into the interactive relationship and dynamic changes between CBDC and various economic entities throughout the macroeconomic operation, to examine and expand existing theories in the field, and to develop new theories in the field from a hierarchical (system-level) perspective. It is our hope that the findings of this study will contribute to the advancement of CBDC.

Footnotes

Acknowledgments

This work is supported by the Research on the Operation Mechanism and Future Development of Digital RMB in Beijing of Beijing Society Science Fund Project, Grant No. 22JJC038.

About the authors

Aobo Lyu is a graduate student majoring in System Science and Mathematics, McKelvey School of Engineering, Washington University in St. Louis. His research interests lie in the field of Complex System and Information System, in particular, the analysis of complex phenomena from a system and information perspective.

Jingjing Jiang is an associate professor and senior economist in the Management College, Beijing Union University, and the director of Beijing digital currency research center of Beijing Union University. She obtained her Ph.D. at the School of Finance, Renmin University of China. Her research is focused on monetary theory, financial technology and CBDC. She has published dozens of academic papers in Economic Science, Bank of China Insurance News, Journal of Coastal Research, and other newspapers and magazines, undertaking projects such as “young backbone talents in Beijing”.

Liang Zhou is an assistant researcher and postdoctoral fellow in the Department of Information Management and Technology, Sichuan University. He obtained his Ph.D. at the Business School, Renmin University of China, China. His research is focused on human-computer interaction, smart decision, and informetric. He has published in major IS and business journals, such as Information Systems and e-Business Management, Journal of The China Society for Scientific and Technical Information, and China Journal of Information systems, among others.