Abstract

Business investments are prone to market risks, so pre-analysis is mandatory. The type of risk, its period, sustainability, and economic impact are the analyzable features for preventing loss and downfall. In recent years, mathematical models have been used for representing business cycles and analyzing the impacting risks. This article introduces a Decisive Risk Analytical Model (DRAM) for identifying spur defects in business investments. The proposed risk analytical model exploits the investments, returns, and influencing factors over the various market periods. The risk model is tuned for identifying the influencing factors across various small and large investment periods. The model is tuned to adapt to different economic periods split into a single financial year. In the process of tuning and training the mathematical analysis model, deep learning is used. The learning paradigm trains the risks and modifying features from expert opinion and previous predictions. Based on these three factors, the risk for the current investment is forecasted. The forecast aids in improving the new investment feasibilities with minimal risks and model modifications. The frequent market status is identified for preventing unnecessary risk-oriented forecasts using the training performed. Therefore, the proposed model is reliable in identifying risks and providing better investment recommendations.

Introduction

Generating educated choices through data analysis and simulations, evaluating prospective investment possibilities using quantitative approaches, and determining the risks and benefits involved. Businesses may make more unbiased based on informed choices regarding investments with mathematical models and risk analysis, which can enhance performance and profitability. Entails assessing possible investment opportunities and related risks using quantitative approaches for calculating the chance of various scenarios and possible returns on investment; it entails analyzing data, creating models, and performing simulations. Investing is a demanding and, at the same time, risky signal for businesses, not just during depressed periods like the pandemic but also during times of regular economic volatility. Existing strategies could have downsides and restrictions, like too much dependence on quantitative data and failure to account for unforeseen occurrences and market movements properly.

A mathematical model is a concrete system that uses mathematical languages and concepts. Mathematical models are widely used in many fields to improve the overall effectiveness range of the systems [1]. The mathematical model is also used in business investments for analyzing financial status and statements for customers and organizations. The main goal of the mathematical model in business investment is to solve the financial problems that occur during a task [2, 3]. Various mathematical models are used for the business investment process. An Ordinary Differential Equation (ODE) based mathematical model is commonly used for business investments. ODE contains functions and operations to evaluate or calculate the investing range for the users. The ODE-based model identifies the attributes and variables required for the investment process. ODE calculates the rights and functionalities of the profits, reducing the latency in investing processes [4, 5]. A Keynesian IS-LM model is also used in business investments. Investment-Saving (IS) and Liquidity preference-Money supply (IS-LM) model detects digital marketing features and the investment growth range of a particular business. IS-LM model maximizes the capital growth and investment growth of the business. The IS-LM mathematical model minimizes the error range in business investment systems [6, 7].

Risk analysis is an important task in business investment systems and applications. Risk analysis identifies and analyzes the risk factors which are presented in investments. Risk analysis eliminates the risks by providing proper solutions at early stages. Risk analysis methods are used in business investment to predict the risk in the early stage [8, 9]. The main aim is to identify the factors affecting investment systems’ success ratio. The Monte Carlo method is used for risk analysis in business investments [10]. Carlo method identifies the exact Net Present Value (NPV) and Internal Rate of Return (IRR) values. NPV measures the negative impacts that occur in the investment process. The actual NPV and IRR produce relevant data for a secure investment process which maximizes the performance and efficiency level of the business [11, 12]. Support Vector Machine (SVM) algorithm-based risk analysis method is also used in business investments. SVM uses a classifier that classifies the necessary key values for the analysis process [13]. The extracted data produce optimal information for analysis that minimizes the latency in risk prediction processes. SVM achieves high-risk prediction accuracy, reducing the investment process error level [14]. The different type of investment risks is diagrammatically illustrated in Fig. 1.

Types of investment risks.

The major risks and their impact (low, high, or variable) are illustrated in Fig. 1. Cashflow risk: This is the risk that an investment will not provide the anticipated cash flows, which events like default, insolvency, or alterations to the rate of interest can bring on. Based on the internal model amendments, risk mitigation, and investment suggestions are provided for balanced operations. The risk of losing money due to alterations in market circumstances, such as shifts in the value of shares, interest rates, or exchange rates for currencies, is referred to as market risk. Social and political risk: This is the risk that changes in social or political circumstances, such as altered rules, instability in government, or social unrest, will have a detrimental effect on investments. Business risk is the possibility that an investment will suffer harm due to elements specific to that company or sector, such as competition, supply chain interruptions, or technological advancements.

The risk of decreasing money’s value due to inflation, which can lower an investment’s real worth over time, is called inflation risk. Surviving retirement funds or investments is referred to as longevity risk. Things like rising life expectancy and changes in economic value can bring on this risk. The adaptable models are robust across various market conditions preventing downfalls. Decision-making is a complicated task to perform in every business investment system. Decision-making requires proper datasets which are collected from the database. Various decision-making methods are used for risk-based business investments [15]. A Strategic Investment Decision-making (SID) method is used in businesses. SID identifies the actual difference between the strategies and profit range. A systematic contextual framework is used in SID to identify the key values for the decision-making process. SID increases decision-making accuracy, enhancing business investment performance and efficiency [16, 17]. The Ordinary Least Square (OLS) regression method is also used for decision-making. OLS method tests the datasets presented in the database and identifies the optimal key values for the further process [18]. OLS also analyses the variables which contain important functions for investments. OLS reduces both the time and energy consumption ratio in the computation process. OLS provides transparent data to the decision-making process, improving investment systems’ significance and feasibility range [19, 20]. However, the business cycle process and analyze has impacting risk which affects the business process. The research issues are overcome by applying the Decisive Risk Analytical Model (DRAM) for identifying spur defects in business investments. This research addresses the challenges and risk factors involved in company investments and presents a trustworthy and practical method for locating and evaluating potential risks. Making informed judgments on business investments, which significantly impact a company’s growth and profitability, necessitates a complete grasp of the associated risks.

The contributions of this article are listed below: Designing a risk analytical model for validating business investment precision and identifying the influencing factors over various financial quarters Integrating expert opinions and return management through financial and previous quarter data through deep learning for stabilized risk mitigation Performing a valid data source analysis that coexists with the proposed steps given in this article for effective analysis Performing a quarterly analysis of the provided data using different metrics for identifying the risk mitigation impacts and efficiency of expert opinions. DRAM is employed to determine market risks in advance while considering various market instances, investments, potential returns, and influencing factors also can adjust within a single financial year to different economic cycles. Deep learning techniques are used to train and fine-tune the risk model and learn from historical data, expert judgments, and prior predictions to enable more precise risk forecasting and improved investment decision-making. Enhancing new investment viability with no risk can also help identify potential flaws and reduce risks, which can improve investment results and risk management approaches. Recognize frequent market conditions to avoid producing irrational risk-oriented predictions. Expanding the model’s application, enhancing its dependability in spotting hazards, and offering insightful investment guidance.

The general part of this paper is arranged as follows: Section 2 discusses the existing algorithms in related works of business investments and plans. Section 3 discusses the proposed scheme implementation procedure with risk model recommendations. Section 4 discusses the performance analysis with various metrics. Section 5 concludes the research work.

The related works section presents tabulation and summarized contributions of different authors from the past. Table 1 presents the different methodologies introduced by various authors, along with the findings.

Different methodology and findings

Different methodology and findings

The included contents of Table 1 contain references related to [21–26] in which we have analyzed various techniques and analyzed investment strategies, decision plans, a market economy, and risk factors by various metrics to update the proposed work with the challenges faced in the previous work.

Dohtani and Matsuyama [21] utilized a statistical technique to link such diverse macro- and micro-investment behaviors. The macro-investment function naturally introduces nonlinearity and shows that persistent business cycles result from the nonlinear macro-investment function, and a generalized hopf bifurcation occurs. Created a straightforward Keynesian investing formula that takes animal spirits into account. The findings show that animal spirits are active, and large-scale and small-scale investments are carried out with a high propensity to invest when there is a significant shift in income. However, it consumes high computation time while processing the macro-investment functions.

Stefanelli et al. [22] focused on classifying and mapping the key attributes of the Credit Supply offered by nine Lending Business Crowdfunding (CS-LBC) platforms using a qualitative multi-case approach. The investigation discovered various restrictions on the services provided to small and medium enterprises with access to LBC regarding information openness. Along with this, certain positive aspects, like the promptness of the service, as well as some negative aspects, like the substantial fees and high-interest rates charged to crowd-borrowers, became apparent. Because the platforms frequently omit to mention the prerequisites for access to funding, interest rates, guarantees, and charges associated with the service, the results suggest limited openness and greater disparity in information for crowd lenders as opposed to crowd investors.

Cummins et al. [23] evaluated institutional participation in the retail market as not a factor that distorts loan performance. The platform’s switch to a fixed rate system negatively affected institutional investors’ loan outcomes. However, the platform-administered loan allocation process is not biased toward institutional investors. Institutional investors only had control over interest rate setting during the auction period, which is when they attained superior loan performance.

Based on a micro-foundational perspective, Yu et al. [24] propose a cognitive framework for making strategic decisions emphasizing emotion’s significance. This framework includes an integrated hierarchy of cognitive processes underlying entrepreneurs’ strategic decision-making and interactions with external affective events. Introducing new methods utilizing biological, physiological, and neuroscientific tools supplements this field of inquiry. Finally, suggestions for future study are presented, emphasizing complex emotions, implicit cognitive processing, and cognitive therapies.

Alaeddini and Mir-Amini [25] outline a thorough framework for identifying the forerunners and heirs of each operation in a roadmap to manage and govern IT. The outcome of integrating the COBIT, a well-known IT standard, with a hybrid group decision-making approach, which has not yet been thoroughly investigated to prioritize the prospective actions of an IT roadmap in a real-world situation in Iran, to show the viability of the suggested framework. Create a consistent evaluation standard, identify the right characteristics, and systematically establish the IT portfolio-building objectives to support a company’s business goals and strategy.

Lacerda et al. [26] analyze the micro-generation wind energy project’s economic potential for micro and small companies. The next step is to conduct a stochastic analysis using Monte Carlo simulation (MCS), followed by a feasibility analysis. Finally, Artificial Neural Network (ANN) models are employed to assess the variables’ Relative Importance (RI). The findings indicate that none of the states appear economically viable in the given circumstances. The chance of viability in the stochastic analysis ranges from 17.2% to 24.6% in all phases, demonstrating the low possibility of durability for microgeneration. However, this process attains high deviations while analyzing the output values.

Yao et al. [27] proposed a decentralized risk-based approach for a non-utility-owned Distributed Generator (DG). The actual aim of the proposed approach is to address the problems that occur in DGs. Leasing Planning and Operation Strategy (LPOS) is used in the proposed approach to identifying the relationship between rights and pricing mechanisms. The proposed approach reduces DG’s overall complexity and risks, enhancing the systems’ performance level. In addition, the method requires the learning process to reduce the risk level on further data investigations.

Yazdani et al. [28] introduced a stakeholder-centric decision support model for digital education technology. The introduced model is an evaluation model which evaluates the factors and dimensions. The introduced model is mostly used during covid-19 pandemic era. Quality matrix and variables are detected from the database, which provides various dimensions for the financial process. The introduced model maximizes the quality and efficiency range of educational technologies. Difficulties while examining the factors and dimension with minimum computation time.

Liu et al. [29] designed an investment efficiency model for business investment using the Gaussian Mixture Model (GMM) method. GMM analyzes the datasets produced by the database and identifies necessary data for the estimation process. GMM is mainly used here to improve the accuracy in the estimation and evaluation process, which reduces the latency in the investment process. Experimental results show that the proposed model achieves high effectiveness in the investment process. This process requires the optimization models to improve the business investment analysis.

Zhang et al. [30] developed a multi-attribute decision-making model for commercial space investments. Prospect theory is used in the model to identify the key values for the decision-making process. The actual weights and parameters are detected which are relevant to commercial investments. Both optimization problems and challenges are reduced in decision-making processes. Compared to other models, the proposed model maximizes commercial space investments’ performance and efficiency range.

Torres et al. [31] proposed a dynamic linguistic decision-making approach for crypto currency investments. Crypto currency investment contains various challenges which cause severe money loss in the investment process. The proposed approach analyzes investors’ weight and trading qualities, producing optimal information for decision-making. The proposed approach achieves high accuracy in decision-making, improving the systems’ effectiveness level. This process requires the learning techniques to analyze the trading qualities in business process.

Li et al. [32] introduced a K-means algorithm-based analysis method for intelligent business investments. The main aim of the proposed method is to improve the efficiency ratio of investment systems. A data mining technique is used here to filter the important features and patterns for the analysis process. The introduced method investigates the important factors for the investment process. The introduced method maximizes the performance and efficiency range of investment systems. The above discussions summarize their major contributions to risk management, as presented in Fig. 2.

Contributions to risk management.

Chen et al. [33] presented a numerical analysis based on the Fractional Order Economic and Environmental Mathematical Model (FO-E2M2). Controlling achievement expense, manufacture component capacity, and technological exclusion diagnostics price. The Scaled Conjugation of Gradient Neural Networks (SCGN2) is used for numerical illustration. As 76% training, 13% testing, and 11% certification with the comparison of the attained and previous approaches, the validity of the designed SCGN2 is verified. The mean square error, regression, state transitions, error histograms, and correlation performances of the SCGN2 are used to evaluate their validity, accuracy, reliability, and competency.

Chen et al. [34] analyzed the Ivancevic pricing model for options calculated with the newly designed Rational Sine-Gordon Expansion Approach (RSGEA) and the modified exponential method. Extract various solutions, including complicated, periodic, mixed dark-bright, single, traveling, and hyperbolic functions. The method reported the family and strain conditions for the workable answers at the modulation instabilities assessment and the dependent variable’s option price wave functions. Results show the high and low pricing levels during the abovementioned times using contour simulations.

The above representations are flexible, illustrating the decisions are more claimable for investments and risk management. Standing next to the decisions are the investments that concern financial stability. Therefore, the proposed model identifies the above factors following the expert opinion and previous risks analyzed for training and the model recommendation (Fig. 2).

An investment business company is a monetary establishment substantially intended to snatch, maintain, and finance securities. Business investment is commonly known as squandering by peculiar businesses and philanthropic on corporal capital everlasting possessions used to provide goods and services. Business investments are exposed to delicatessen imminence, so prior investigation of the risks is important. The type of risk, period, sustainability, and economic impact are the decipherable characteristics for forestalling loss and destruction. In recent years, mathematical models have been used for instantiating business cycles and examining concussion risks. This article introduces a Decisive Risk Analytical Model (DRAM) for determining spur deformity in business investments. Deep learning is an approach in Artificial Intelligence (AI) that educates computers to proceeds data in a way that is encouraged by the human brain. Deep learning models can concede difficult pictures, text, sounds, and other data exemplars to provide perfect perceptions and prognostications. Risk analysis is an approach used to determine and estimate circumstances that may threaten the success of a project or achieve the perfect goals. This technique also helps delineate precautionary measurements to decrease the feasibility of these considerations from manifesting and determining the retaliatory measures to flourishingly deal with these constraints when they develop to turn away the possible negative effects on the company’s competitiveness. After determining and classifying the risks, identifies the controls that could alleviate the risk. A mathematical model is a hypothetical explanation of a substantial system using mathematical concepts and language. The fundamental risk assessment model is illustrated in Fig. 3.

Risk assessment model.

The business investments are first identified over several years to determine the risk based on the factors. The basic risk model is processed based on the characteristics such as expert opinion, previous risks that occurred, and the number of periods. The proposed risk analytical model achieves the investments, returns, and influencing factors over the various market periods. It also determines the market values and the stock exchange between the periods. The risk model is tuned for estimating the influencing factors which cause the loss across various small and large investment periods. This risk model is synthesized to adapt to distinguishable economic periods rend into a single financial year. Then this will be given as the input to the deep learning method to train the risk model and also to give recommendations to enhance the analytical model. In the process of tuning and training the mathematical analysis model, deep learning is used.

The deep learning approach trains the risk models and identifies characteristics from expert opinion and previous risk predictions. Based on the three factors mentioned earlier, the risk for the current investment is predicted. This prediction will help enhance the new investment possibilities with minimal risks and model modifications. The repeated market imminence is estimated for averting unnecessary risk-based predictions using the training performed by the deep learning technique, for training and tuning the mathematical analysis model by deep learning technique to detect the influential factors across all investment periods. The risk for the current investment is estimated. These estimates impacted business investments, returns, and market period. Investment can be made by considering the risk analysis, objectives, potential returns, and expert opinion.

The business investments are determined based on the number of years. It will be useful in achieving the risk analytical model depending on the features of the business investment processes. The basic risk model will be trained according to the characteristics of the investments in the business. Thus, it will be given as the input to the deep learning technique to enhance the training of the risk model and to provide effective recommendations for the upcoming risk analysis procedure. Through the factors, the risk model will be designed to analyze the influencing features and to reduce them accordingly. The process of achieving the basic risk analysis model in the business investment procedure based on the factors acquired to determine the influencing factors is explained by the following equation (1) given below:

Where in equation (1) α t is denoted as business investments, M is denoted as the basic risk model, x is denoted as the number of years of investments, φ is denoted as the possessions determined from the investments, T is denoted as the characteristics of the basic risk model, Δ is denoted as the efficiency of the present risk analytical model. Now the factors are determined for the risk analytical model. The factors are expert opinion, previous risk, and the stock exchange analysis period. The opinions of the expert for the past risk model are determined for identifying the influencing features of the risks over the various market periods. It estimates the risk analysis model’s efficiency and provides product recommendations for further risk analytical models. The opinions of the expert will be useful in predicting the risks in the present analytics model and will help detect the influencing factors in a shorter period. From equation 1, the notations T are denoted as the characteristics of the occurrences of the basic risk model and the efficiency of the present risk analytical model for identifying the basic risk factors rather than analyzing the probability and severity. The factors for the risk analytical model are evaluated by expert judgment, historical risk, and the period of the stock exchange study are the factors. The expert judgments for the historical risk model are determined to determine the influencing characteristics of the risks over the various market periods. It is done to determine the effectiveness of the risk analysis model and to make effective recommendations for additional risk analysis models to avoid the highest severity in the future.

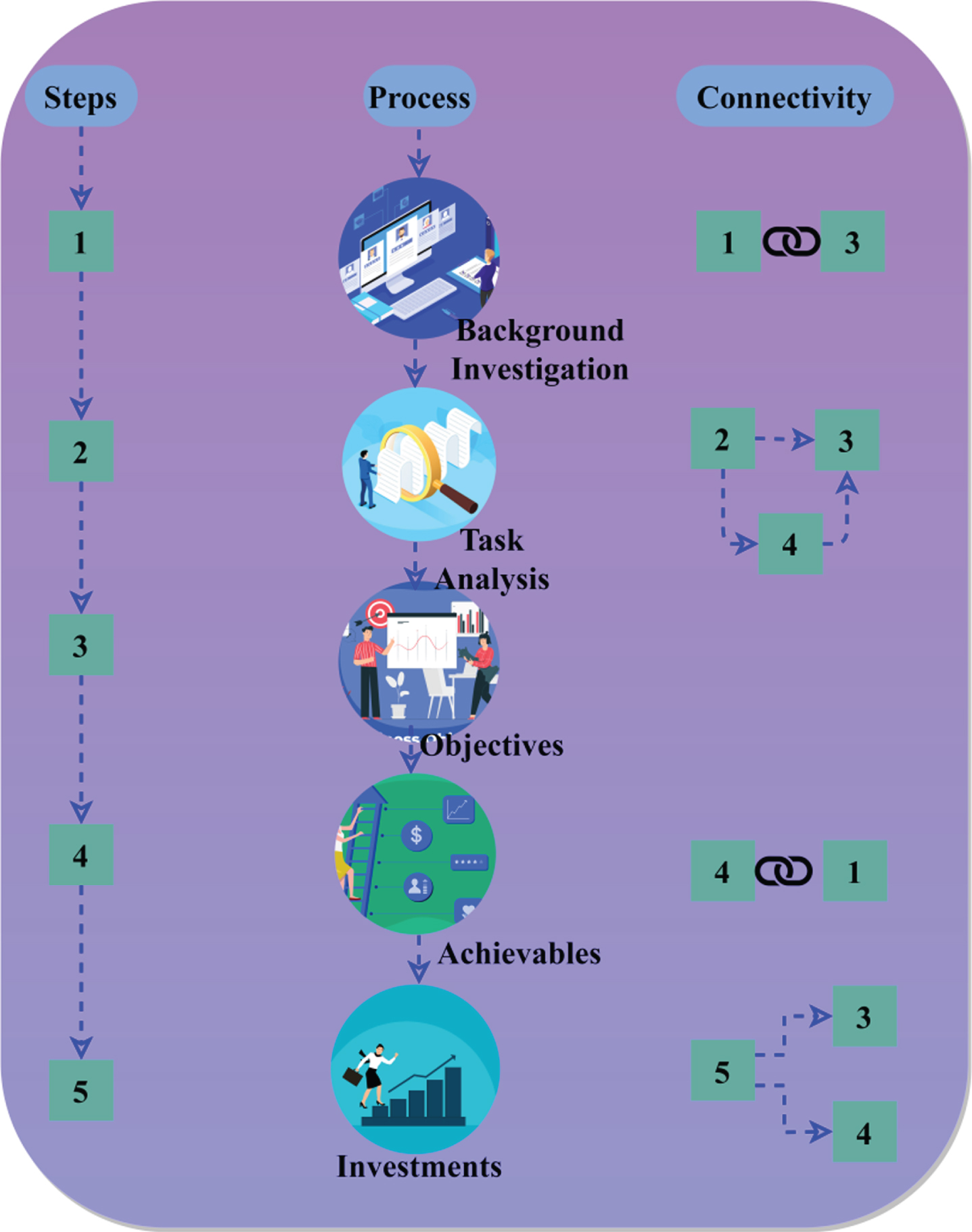

The business’s investment can be determined by identifying the influencing factors during the risk analysis procedures. The company’s business investment decision was made for identifying the market rate and business inflation risk. Expert opinions come from the financial institution persons, and achievement is measured by quarter analysis. The data from (https://www.kaggle.com/datasets/ankurnapa/stock-portfolio-financial-risk-analytics) is utilized to analyze the proposed risk model. First, the data provided in the source is represented diagrammatically for analysis, as in Fig. 4.

Source data representation.

The representation for a single risk assessment is shown here. The connectivity includes the succeeding steps and the risk assessment order. It includes modifications (connectivity), risk-based expert opinions, etc. (Refer to Fig. 4). The main goal of this Fig. 4 is to identifying the objectives and achievable from the background study. Expert opinions detect errors in the present risk analytical models. Based on this factor, the risk model will be achieved and given as input to the deep learning technique. The investment period will also be maintained to extract the influencing factors that enhance the business investments’ risk. Expert opinions are used to maintain the efficiency of the risk analytical model to enhance the training of the upcoming model. The opinions will help balance the business investments by preventing loss to it. Based on these factors mentioned earlier, the risk model will be achieved to improve the learning technique and provide recommendations for further models. These features are given to the risk model to achieve the business’s investments, returns, and market period. The risk model is used to identify the influencing factors over small and large business investments. By collecting the experts’ opinions, the risk can be modified for the present procedure and also will help enhance the training session of the model. This model will identify the defects during the process; thus, further steps will be taken to reduce the errors. It can also be useful in acquiring the previous risk during the procedure. The process of acquiring expert opinions to model the risk facsimile is explained by the following equations (2) & (3) given below:

Where σ is denoted as the opinions of the expert, β is denoted as the process of representing the influencing factors, L is denoted as the process of identifying the various time of investments, w is denoted as extracting the returns. Then the previous risk factors of the model will be identified to enhance the present risk analytical model. Along with the expert opinion and the period, this will be given as the input to the deep learning technology, which helps in tuning and training the risk model. Based on these factors, the risk estimate model will be designed to provide the perfect recommendations and reduce errors. The previous risk helps design the risk model without errors and enhances the model’s efficiency. It is used to detect errors and to pre-analyze the risks before it exploits the other procedures. Based on the previous risk during the model procedure, the present risk analytical model will be established.

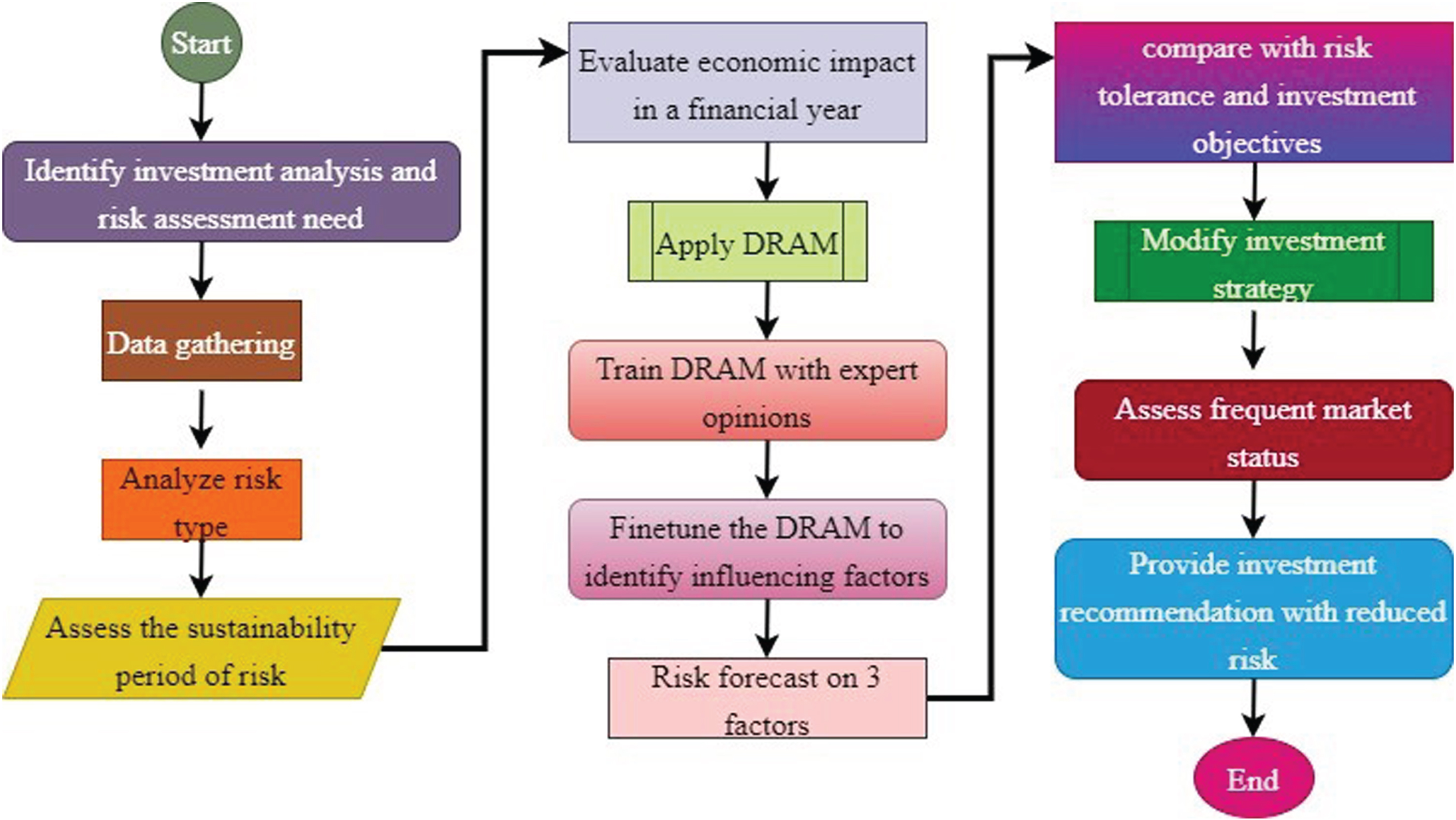

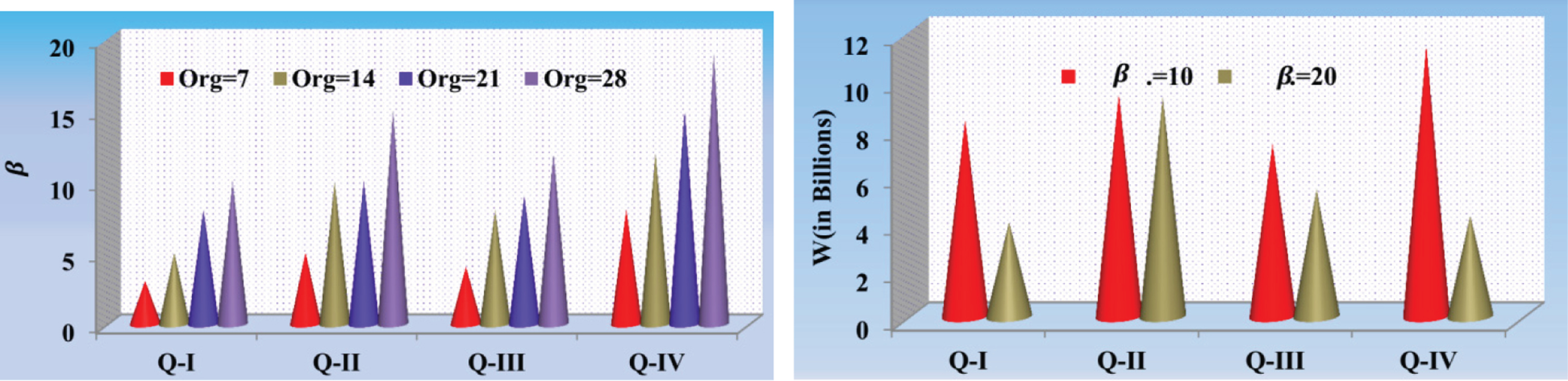

As described in Fig. 5, the flowchart describes the overall procedure in a step-by-step process. The influencing factors (count) for four quarters are analyzed in Fig. 6. The data is obtained from the data source for 28 organizations provided. The influencing factor analysis is calculated for different quarters of various financial, healthcare, life science, and stock exchange organizations. The investment decisions are conservative and aggressive types. The probability and risk impact decisions are raised from the different investment plans.

Implementation flowchart.

Influencing factor analysis.

The β is obtained as the total low values observed divided by the quarters presented for which 7, 14, 21, 28 organization variations are presented. Similarly, the W (in billions) is the least (downfall) faced at an average by the organizations for β= 10 and 20. As the influencing factor increases, the risk impact due to which W shows up least possibilities. The analysis is performed for four quarters (Q-I, Q-II, Q-III, and Q-IV); the available data is random, for which the above analysis is presented. The previous risk factors will be gainful in making the perfect risk analysis model to improve efficiency. Based on this, the model is trained and tuned for identifying the influencing factors over the different market years. The previous risks that already happened in the model will be reduced and eliminated in the present analytical model. Thus, the previous risk consolidations will help make the risk analysis model more efficacious. Then this procedure will be helpful in the deep learning technique used to train the risk model and provide precise recommendations to avoid errors during the business investment processes. Then the recommendations given by the learning technique will help enhance the risk model by giving the needed training. These factors help determine the investment and return amounts from the analyzing model. Also, the market period was estimated along with this expert opinion and the previous risk factors. Then it will be combined and used as the input in the learning approach. The process of acquiring the previous risk to eliminate the errors and the risks in the present model is explained by the following Equations (4) & (5) given below:

Where Z is denoted as the previous risks acquired, ξ is denoted as the errors in the previous model, I is denoted as the output of the present model, j is represented as the process of reducing the risk in the present model, G is denoted as the combination of expert opinion and this previous risk. Now the period of the market investments will be identified to design the risk analytical model. It is used to identify the invested period of the business based on the market values and the stock exchange. These analyses will be done to estimate the period of the investments. It can also be determined depending on the risk impact on the business economy and will be used in eliminating errors. The risk model is trained for estimating the influencing factors across various small and large investment market periods. The model is tuned to cope with the different economic periods split into a single financial year. These three factors will help make the risk analytical model in the business investments process. In Table 2 the attribute low W discusses about the low-value risk analysis and least possibilities of the risk impact that was analyzed previously in a quarter compared with all possible influential risk factors that represents the probability of risk occurrences and severity level for measuring the risk analyzed. Both probability and severity components may be explicitly considered for improvement in further analysis. And also, three factors will be helpful in the deep learning technique for providing efficient training for the model and establishing the recommendations. Based on the data, the consecutive quarter is analyzed for risk mitigation through expert opinion. It creates a positive impact over the previously identified risk (low value in any quarter, as in Fig. 6). Such impact (only for successive) quarters are analyzed for the possibility in Table 2.

Successive quarter analysis

The impact (as an improvement) is analyzed in Table 2 for the considered risks. The risks are analyzed in different aspects such as inflation, credit, social, business, market, longevity, reinvestment, liquidity, stakeholders and inflation. The consecutive quarter delegations are identified/ unidentified for the precise risks. Therefore, the low W identified in one quarter is suppressed for the varying improvements. In this case, the changes in consecutive quarters are identified for maximizing σ. Therefore, the model is influenced by modifications for the successive quarter preventing downfall. The period will be identified to enhance the risk model and avoid the previous model’s errors and mistakes. The basic risk model will be trained according to the three features mentioned earlier to enhance the present characteristics of the risk analytical model. These will be given as input to the deep learning technique and used to determine the influencing factors of the risks that occurred. It reduces the risk factors, and modifications will be done to enrich the process of business investments by avoiding errors in the upcoming procedures. The procedure of acquiring the period of the investment to train the risk model and also to send as the input to the learning process is explained by the following Equations (6) & (7a-7c) given below:

Where R is denoted as the investment period, O is denoted as the stock exchange period. These three factors are input to the deep learning technique, which trains and tunes the risk analytical model. The model will receive efficient training to reduce errors and influence factors during investment. It also gives the investment feasibility without any issues and errors in the risk analysis model. This learning approach trains the risks model and alters characteristics from expert opinion and previous predictions. Depending on these three factors, the risk of the present investment is identified using the risk analytical model. This prediction enhances the new investment possibilities with fewer risks and model alterations. The regular market results will be identified to prevent unwanted risk-based features and modifications. Deep learning stores the factors while training the new model for the current investment problems.

The deep learning technique uses the three features for training the risk analysis model. It is used in the elimination of errors in the current investment issues. It can also enhance the perfect modifications if there are any issues during the training period of the model. This learning technique helps in tuning and training the risk analysis model for pre-estimating the risks during the investment procedure to eliminate error issues. The process of deep learning technique to train the model effectively and to provide effective modifications to the upcoming risk model is explained by the following equations (8) & (9) given below:

Where H is denoted as the process done by the deep learning technique with the help of the three factors as mentioned earlier, ranges from αϵφ, tϵ [0, T]. This learning technique helps train the risk during the investment procedure. The predicted results may help train the risk during the learning algorithm procedure. The learning technique also helps modify the model to enhance the efficiency of the present analytical model. It is also used to analyze the risk during the current investment prior. The training will be given to reduce the previous risk, and based on the expert opinion, further steps will be taken to enhance the present risk analytical model. If there are any issues during the training process, precise recommendations will be given for further model enhancement. The process of giving the training to the risk model to avoid errors during the investment procedure by using the deep learning technique is explained by the following Equation (10) given below:

Where D is represented as the training given to the risk model, E is denoted as the process to determine the efficiency of the current risk model given by equations 11(a) and 11(b). If there are any issues in the training process, then some of the recommendations will be given to the risk analytical model to enhance the model’s efficiency. The risk model recommendation and the training improvements are tabulated in Table 3.

Risk model recommendation and training improvements

In the above representation, the low W is identified, and the maximum risk confronted is disclosed. The risks include those in Table 2 and its expert opinion for training improvements. The training improvements for new risk analysis and existing risk mitigation is analyzed using the improvement in positive factor (refer to Fig. 6). Therefore, the positively impacted risks (addressed) in the successive quarters are alone extracted for consideration (Table 3). The definitions and formulas used in this manuscript are written independently. To make a better understanding of the equations, the complexity level is reduced by splitting the equations 7(a, b, c), 11(a, b), and 12(a, b, c) in a step-by-step process. Equation 7a is used for identifying the market investment period, 7b is for analyzing the stock exchange period,7c is for business investment. Equations 11a and 11b is for determining the efficiency of the current risk model. Equation 12a is used to represent the modifications given to the analytical model,12b is for recommending the risk analysis model and 12c is used for increasing the investment possibilities.

This recommendation is given to overcome the risk in the model, then to increase the investment possibilities. The process of providing the perfect recommendations for the risk analysis model is explained by the following Equations (12a-12c) given below:

Where λ is denoted as the modifications given to the analytical model, S is represented as the efficiency of the model after applying the recommendations in Equation 13 as follows:

This method determines the possible feasibility of overcoming the risk in the process. The risk analytical model will receive a few recommendations to improve its effectiveness if there are any problems with the training procedure. The recommendation is made to reduce the model’s risk and thus raise the investment’s potential. The following equations (12a–12c) below describe how to provide the risk analysis model with the ideal recommendations. Based on expert opinions, previous risk prediction, and investment period, the three models were suggested with the help of deep learning techniques.

Based on the expert opinion, previous risk, and the investment period, deep learning technology is used to effectively train the risk analytical model and provide recommendations to upgrade the risk model to reduce errors. This model helps provide the best outputs in the lesser time. The assessment evaluation of modification factor analysis is discussed in Table 4 rather than before. The proposed way is after identifying risk model recommendations and improvements for training, which is discussed later in Table 4.

Modification factor analysis

No large modifications are done to the process using the deep learning technique. Finally, the modification factor against the nine risk factors in each quarter is validated using the data provided by the source. This analysis is presented in Table 4. The modification factor is computed using the W (high) compared to the previous W (low) between R and O.

In Table 4, represented above, the W (low to high) between Q-I and Q-IV, and the s is analyzed. Based on H and D, the ϵ post the j and G implication this tabulation is presented. In the above tabulation, the connectivity between different processes, as given in Fig. 4, is pursued analysis. Some other models possess different routines, so the achievable is planned per β. Therefore R ∀ W and L ∀ Δ are the liable characteristics for business investment risk analysis.

The discussion on models and periods (R and O) is presented in this section. A maximum of 12 models and 60 months are considered for four quarters of an organization. The investment tenure period is taken for five years; hence it is represented as 60 months duration; likewise, the attributes of the data source represent the maximum count of 12 models; hence, the discussion defines it. From the accounted data source, one company’s (name undisclosed) W is used for the following analysis. In this analysis, the W is used for risk prediction, investment forecast, model modification, modification time, and model error.

The risk prediction is productive in this method by using the deep learning technique and is also used to reduce the risk in the current investments. Based on the expert opinions, the previous risks, and the investment period, the deep learning approach is used to train the risk and provide efficient recommendations to the present risk analytical model. This learning technique helps train the risk during the investment procedure. The predicted results may help train the risk during the learning algorithm procedure. The learning technique also helps modify the model to enhance the efficiency of the present analytical model. It is also used to analyze the risk during the current investment prior. The risk prediction is better with the help of the three factors from the business investments. The training will be given to reduce the previous risk, and based on the expert opinion, further steps will be taken to enhance the present risk analytical model. The training will be given to the present risk model to eliminate the errors and the risk rate during the procedure (Fig. 7).

Risk prediction.

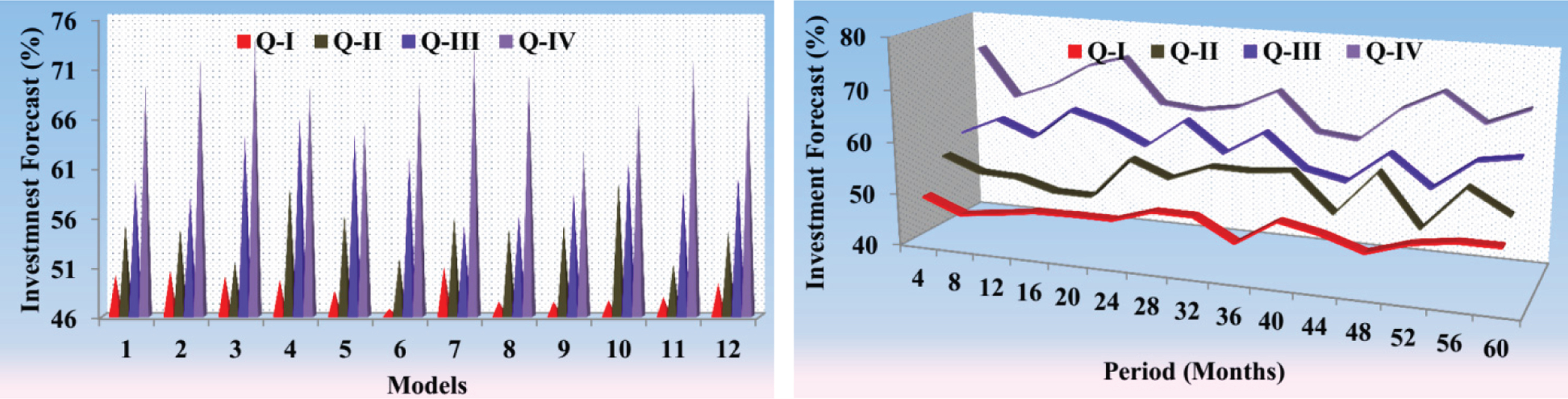

The investment prediction is productive in this method by reducing the previously happened risk and errors. The investment in the business is identified based on the market values, and also it should analyze the stock exchange during the procedure. The present risk analytical model can efficiently reduce the errors and modifications rate for the upcoming processes in the risk model. Using the deep learning technique, more possible feasibilities will be invented for the current investments. The business investments will be identified based on the number of years the process takes place. The risk model is tuned for estimating the influencing factors which cause the loss across various small and large investment periods. This risk model is synthesized to adapt to distinguishable economic periods rend into a single financial year. The deep learning approach trains the risk models and identifies characteristics from expert opinion and previous risk predictions. By this, the investment prediction for the business is determined for the effective risk model training (Fig. 8).

Investment forecast.

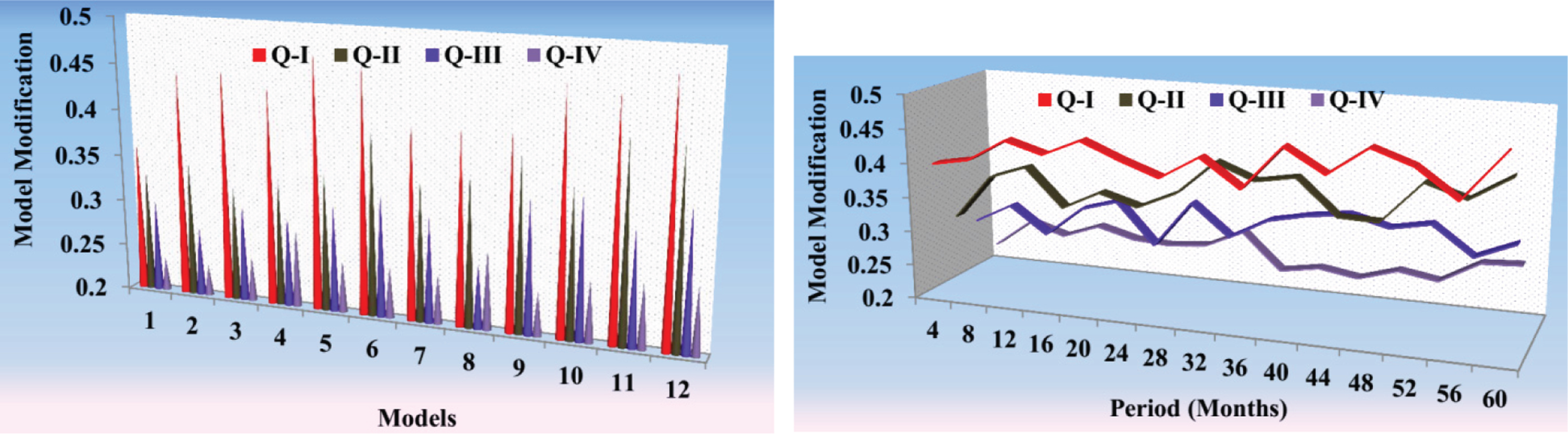

The model modifications are less in this process as it eliminates the errors and the risk analysis before it ends in a negative output. The learning approach will be used to perfectly train the risk analytical model to reduce the previously happened risks. The modifications will be given to the risk model to enhance the procedure for identifying the possible feasibilities and determining the influencing factors. The modifications are made in lesser time to enhance the efficiency of the present risk analytical model. The learning technique uses the three factors for training the risk model. And if there are any issues over there, then the modifications will be done to alter the way of processing to eliminate the errors and risks increase rate. Through the factors, the risk model will be designed to analyze the influencing features and to reduce them accordingly. The prediction aids in improving the new investment feasibilities with minimal risks and model modifications (Fig. 9).

Model modification.

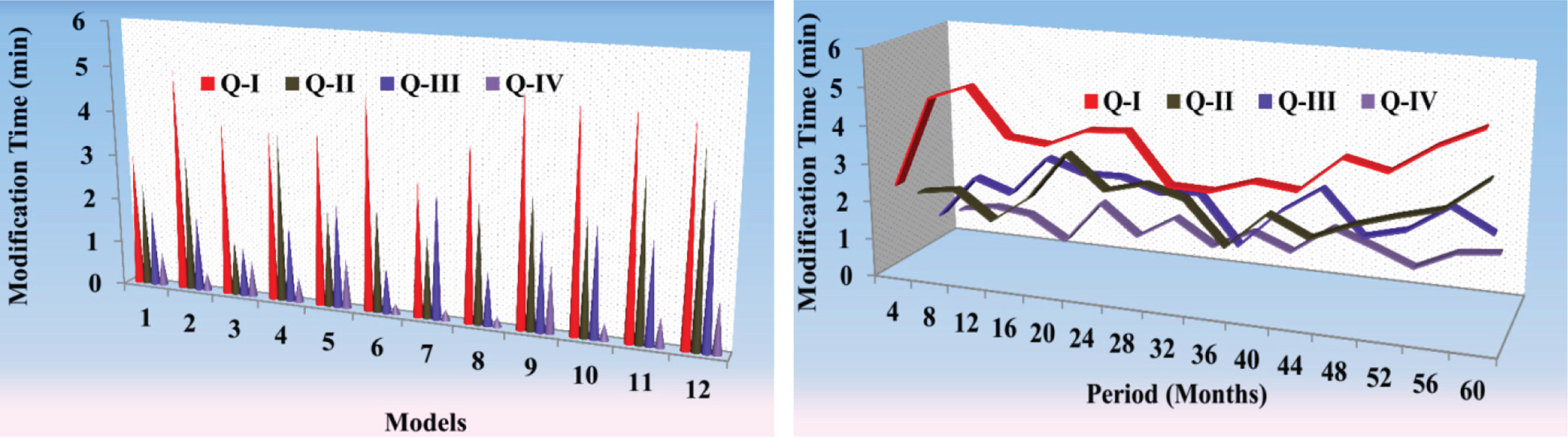

The time taken for the modifications is less as it detects the errors and risks monastery and some of the steps taken to remove them. The deep learning technology is used to determine the three factors to train the risk model and to give modifications if there is any issue in the output of the present risk model. The modification time is lesser as it uses the learning technique to review and resolve the process to enhance the procedure’s efficiency. The opinions of the expert will be useful in predicting the risks in the present analytics model and will help detect the influencing factors in a shorter period. The business’s investment can be determined by identifying the influencing factors during the risk analysis procedures. The modifications are done to overcome the risks during the investment process. The three factors help train the risk model to develop the efficiency of the present risk analytical model. These are the procedures that are done to reduce the time of the modification process (Fig. 10).

Modification time.

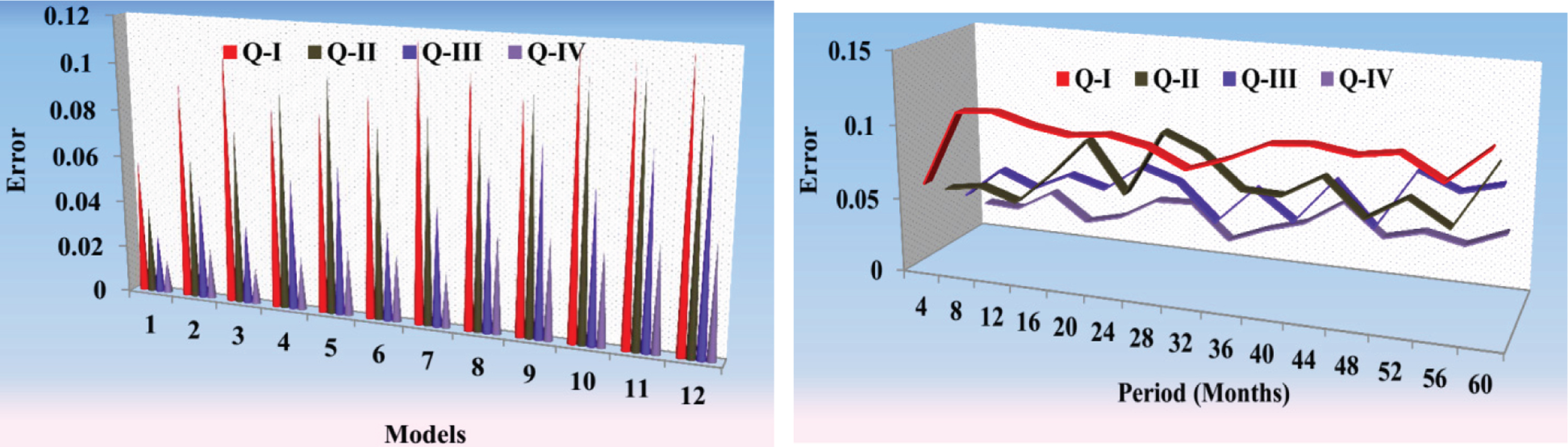

The error that occurred in the model is less by using the deep learning technique, which uses the expert opinion, previous risk, and the period of the investments as inputs. The model will receive efficient training to reduce errors and influence factors during investment. It also gives the investment feasibility without any issues and errors in the risk analysis model. Depending on these three factors, the risk of the present investment is identified using the risk analytical model. This prediction enhances the new investment possibilities with fewer risks and model alterations. Deep learning stores the factors while training the new model for the current investment problems. The deep learning technique uses the three features for training the risk analysis model. It is used in the elimination of errors in the current investment issues. This learning technique helps in tuning and training the risk analysis model for pre-estimating the risks during the investment procedure to eliminate error issues (Fig. 11).

Error.

Implementing the proposed DRAM model in real-case markets involves collecting historical data for improvement, financial records, market trends, and economic indicators. Data gathered from organizations involves investment and returns based on various market periods. A deep learning technique is used to train the DRAM model with this collected information. The model’s parameters represent the numerical information like learning rate, number of hidden layers, influencing factors like regulatory changes, market strategy, and macroeconomic conditions impacts on investment performance to solve the model in real-life implementation. Utilized the DRAM in real-life scenarios involving investments in technology. Evaluated the predictions of the model and compared them with the actual results. Evaluated the model’s effectiveness in correctly identifying risks and offering insightful recommendations. The DRAM proved useful in real-world circumstances through ongoing evaluation and improvement, enhancing investment decision-making and reducing potential risks. In addition, the efficiency of the system is compared with the [33] and [34] and the obtained results are shown in Table 5.

Accuracy analysis

From the above Table 5, it clearly states that proposed DRAM approach attains the maximum accuracy for four quarters such as Q-I (97.67%), Q-II (97.92%), Q-III (97.23%) and Q-IV (96.43%) compared to the other methods such as FO-E2M2 and RSGEA. Thus the proposed DRAM approach identifies the organization risks and improve the data analysis efficiency.

This article introduced a decisive risk analytical model for validating the investment feasibility over the various quarters of the organizations. In this model, deep learning provides a stabilized risk assessment model by considering various inputs such as investments, returns, expert opinions, and influencing factors. These features are required for a steady operation of the organization over a long time and controlled risk. First, the influencing factors are identified for which the model changes and expert opinions are incorporated for tuning the implication. The learning paradigm provides sufficient training for improving the investment forecast under controlled risks. Therefore, the new investment period and the reinvestment characteristics are estimated based on model modifications. This model reduced the model modifications regardless of the variations in quarterly data and improved the forecast. Thus, the proposed model is valid in handling financial and risk data with expert opinion features for preventing downfalls. This model, however, is less robust against multivariate financial models due to short-term investment schedules. Therefore, an affirmative market-dependent risk modeling is planned for short-term investments in future work. This model is hoped to handle multivariate market data regardless of the influencing factors.

Funding

This work was supported by the National Social Science Foundation project, “Research on the Integration of Heterogeneous Family Farm Entrepreneurship Resources in the Digital Background”. (Project No. 22BGL175).