Abstract

In the 40 years of global microcredit practice, loan technology has played a positive role in microcredit as one of the most important supporting elements. The development and evolution of microcredit institution lending technology is the result of comprehensive consideration of specific regional economic, social, cultural, and geographical factors. In the context of the diversified trend of microcredit technology, choosing loan technology reasonably, exploring flexible guarantee conditions, and innovating diversified loan technology combinations will become practical problems faced by microcredit institutions, and also the direction of theoretical research. The timely innovation of group loan technology in microcredit has practical value and theoretical significance for promoting the innovation of financial agricultural products in the implementation of China’s rural revitalization strategy, as well as bridging the theoretical controversy of microcredit loan technology. The performance evaluation of microfinance groups lending is a MAGDM issues. In this paper, the distances measures of single-valued neutrosophic sets (SVNSs) and maximizing deviation method (MDM) is used to obtain the attribute weight values. Based on the classical Multi-Attributive Border Approximation area Comparison (MABAC) method, the single-valued neutrosophic numbers MABAC (SVNN-MABAC) method is constructed for MAGDM under SVNSs. Finally, an example for performance evaluation of microfinance groups lending and some comparative decision analysis are constructed to verify the SVNN-MABAC model.

Introduction

In the practice of microcredit in China for over 20 years, group loan technology has always been the most important loan technology [1, 2]. Group loans have always been the most important loan technology in poverty alleviation projects of international institutions, microcredit practices of poverty alleviation societies, and government promoted microcredit poverty alleviation projects [3, 4]. However, during the implementation process, technical elements such as weekly meetings, sequential loans, and group funds were revised. In addition, among the small loans promoted by rural credit cooperatives, the loan technology arrangement of “letter of credit

The multi-attribute decision-making (MADM) method is widely used in various fields such as project evaluation management and engineering technology analysis [23, 24, 25, 26, 27, 28, 29]. It is a decision-making method that comprehensively measures multiple attribute factors to obtain the optimal solution [30, 31]. With the rapid development of technology and the deepening understanding of social practice, people are facing increasingly complex decision-making problems [32, 33, 34, 35, 36]. With the rapid development of computer technology, the ways and types of information obtained by people about the same thing are also gradually increasing, making attribute information gradually showing diversified characteristics. In the current context, MADM problems with single attribute values are gradually not meeting practical needs. Traditional MADM problems mainly focus on studying deterministic decision-making problems. However, due to the limitations of human cognitive level and the disturbance of objective things, data information often exhibits uncertainty [37, 38, 39, 40, 41, 42]. Multi attribute group decision-making (MAGDM) refers to a decision maker composed of multiple decision experts who jointly express opinions on multiple attributes of a set of alternative solutions, thereby ranking the advantages and disadvantages of each alternative solution and selecting the best solution [43, 44, 45, 46, 47]. At present, the core issues of MAGDM methods mainly include the following two aspects: firstly, how decision information is aggregated, namely the information aggregation operator [48, 49, 50, 51, 52]; The other is how to meet group consensus in the decision-making process, that is, the consensus reaching process [53, 54, 55, 56, 57].

Pamucar and Cirovic [58] first constructed the MABAC in 2015. Su et al. [59] extended MABAC model based on prospect theory for MAGDM under probabilistic uncertain linguistic environment. Simic et al. [60] integrated CRITIC and MABAC based type-2 neutrosophic model to cope with public transportation pricing system selection. Mishra et al. [61] chose the sustainable supplier selection by using HF-DEA-FOCUM-MABAC technique. Jiang et al. [62] defined the Picture fuzzy MABAC method based on prospect theory for MAGDM for supplier selection. Ahmad et al. [63] defined the MABAC under non-linear diophantine fuzzy numbers for emergency decision support systems. Zhang et al. [64] defined the CPT-MABAC method for spherical fuzzy MAGDM and its application to green supplier selection. Rong et al. [65] assessed the MOOCs based on multigranular unbalanced hesitant fuzzy linguistic MABAC model. Estiri et al. [66] defined the multi-attribute framework for the selection of high-performance work systems based on the hybrid DEMATEL-MABAC method. Chen et al. [67] defined the MABAC and CRITIC method under the linguistic Z-numbers environment. Su et al. [59] defined the MABAC method based on prospect theory for MAGDM under probabilistic uncertain linguistic environment. Shen et al. [68] extended Z-MABAC model based on regret theory for regional circular economy development program selection with Z-information. However, it’s obvious that the existing decision studies about the modified MABAC method [58] based on the maximizing deviation method (MDM) model [69] under SVNNs with completely unknown weight information is not existing. Hence, it’s very crucial to investigate the modified MABAC method based on the maximizing deviation method (MDM) model under SVNNs with completely unknown weight information. The main purpose of this work is to construct the SVNN-MABAC model based on MDM model to cope with MAGDM with completely unknown weight information more effectively. In this paper, the distances measures of single-valued neutrosophic sets (SVNSs) and maximizing deviation method (MDM) is used to obtain the attribute weight values. Based on the classical Multi-Attributive Border Approximation Area Comparison (MABAC) method, the single-valued neutrosophic numbers MABAC (SVNN-MABAC) method is constructed for MAGDM under SVNSs. Finally, an example for performance evaluation of microfinance groups lending and some comparative decision analysis are constructed to verify the SVNN-MABAC model.

The reminder framework of this paper proceeds. The SVNSs is constructed in Sec. 2. The SVNN-MABAC method for MAGDM is constructed in Sec. 3. An example for performance evaluation of microfinance groups lending is constructed to verify the superiority in Sec. 4. the conclusion is fully constructed in Sec. 5.

Preliminaries

Wang et al. [70] constructed the given SVNSs.

with constructed truth-membership

The SVNN is expressed as

Peng et al. [71] came up with order decision relation for SVNNs.

Let

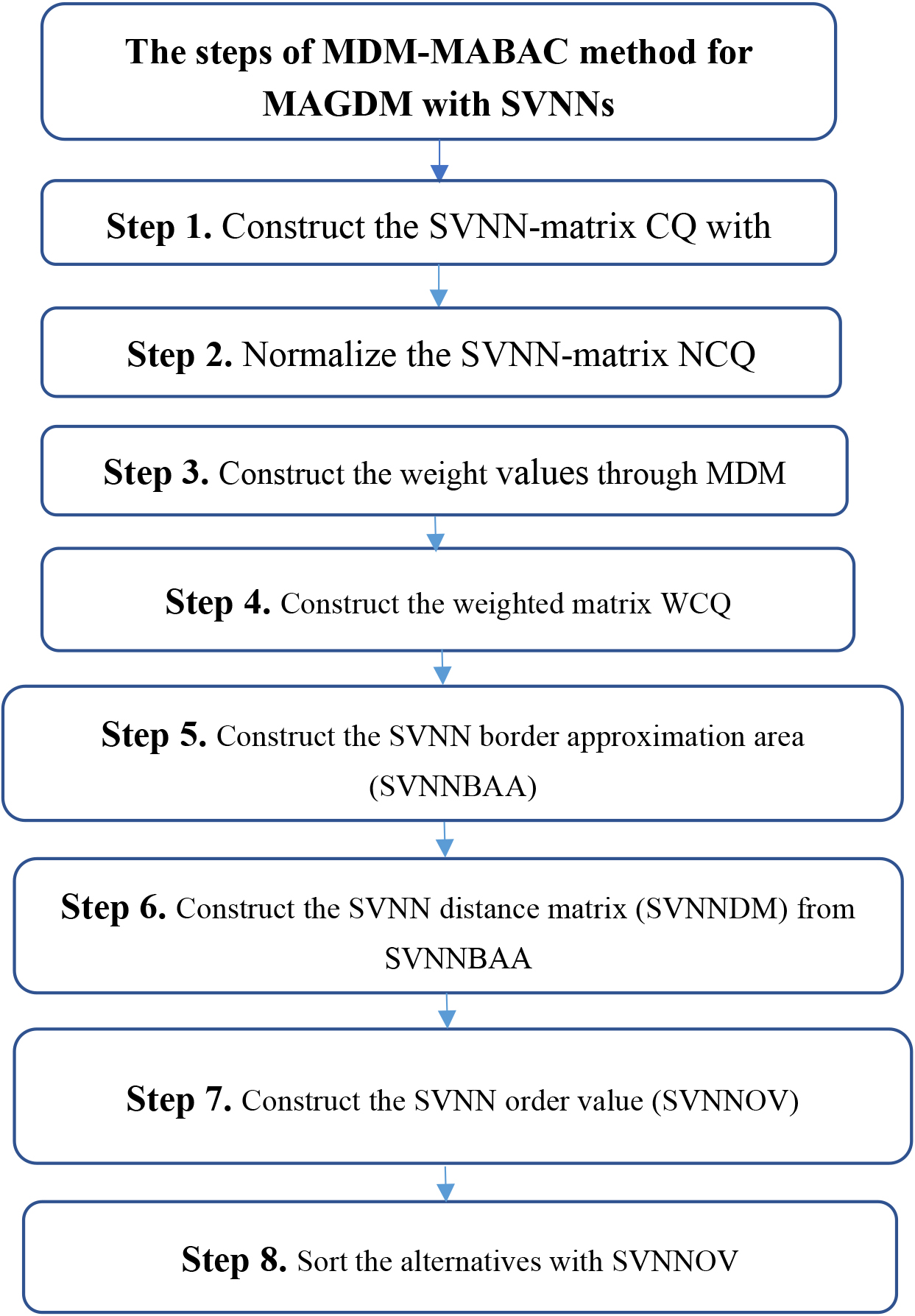

MDM-MABAC method for MAGDM with SVNNs.

The maximizing deviation method (MDM) model [69] is a useful tool to construct the weight information. Until now, the MDM model has been employed in different decision domains [74, 75, 76, 77, 78, 79, 80, 81, 82]. Then, the MDM model is constructed to obtain the weight values under SVNNs.

(1) Construct the deviation of

where

(2) Construct the weighted deviation.

(3) Construct the programming decision model.

To cope with the constructed model, The Lagrange function is employed to cope with this model.

where

And the weight information is constructed.

Finally, the normalized weight values are constructed.

An empirical example

Muhammad Yunus once said: “Complaining that the poor cannot provide loan support without collateral is like complaining that people cannot fly to the sky without wings.” More than 100 years ago, the Wright brothers invented the airplane, which successfully made human beings soar. 70 years later, Yunus and the Grameen Bank under his guidance issued loans to the extremely poor in rural Bangladesh through group lending, successfully achieving extremely high repayment rates. Group lending is the most legendary lending technology in the field of microcredit. It involves the voluntary formation of credit groups by the poor, who are jointly and severally responsible for repayment, effectively solving the repayment problem of unsecured loans. Since the 1980s to 1990s, with the promotion of institutions such as the World Bank, the Grameen Bank’s group loan technology has been promoted in rural credit markets in Asia, Africa, and Latin America. Even in developed countries such as the United States and Canada, small and medium-sized enterprise credit has adopted group loan technology similar to that of Grameen Bank. Group lending is the most legendary lending technology in the field of microcredit. It involves the voluntary formation of credit groups by the poor, who are jointly and severally responsible for repayment, effectively solving the repayment problem of unsecured loans. Since the 1980s to 1990s, with the promotion of institutions such as the World Bank, the Grameen Bank’s group loan technology has been promoted in rural credit markets in Asia, Africa, and Latin America. Even in urban credit in developed countries such as the United States and Canada, small and medium-sized enterprise credit has adopted group loan technology similar to the Grameen Bank. Due to the unique nature of organizational forms, group loans have become synonymous with microcredit to a certain extent. People often first pay attention to the unique credit groups and joint liability of group loans. In theoretical research, the joint and several liability of group loans is also considered an important guarantee for low default rates of small credit institution customers. However, the development of microcredit practices has reversed this certain trend. In other regions, the adaptability of group lending technology has been increasingly questioned. Therefore, it is of great significance to track the development and evolution of the relevant theoretical literature’s understanding of the technical performance of group loans, sort out the relevant explanations of the technical mechanism of group loans, clear up the relevant misunderstandings about group loans, objectively analyze the adaptability of group loans, and select and develop appropriate microfinance technologies. The performance evaluation of microfinance groups lending is the MAGDM. In this paper, an empirical example for performance evaluation of microfinance groups lending was constructed based on the SVNN-MABAC model. There are five microfinance groups

Four constructed attributes

Four constructed attributes

Then, the MDMMABAC method is employed to cope with the performance evaluation of microfinance groups lending with SVNNs. The built MDMMABAC method involves the following steps:

The

The

The attributes weights

The

SVNNBAA

The

The SVNNOV values

The SVNN-MABAC is compared with SVNNWA and SVNNWG operators [71], weighted singlevalued neutrosophic copula power average (WSVNCPA) operator [83], weighted singlevalued neutrosophic copula power geometric (WSVNCPG) operator [83], SVNN-CODAS method [84], SVNN-EDAS method [85] and CPT-SVN-TODIM method [86]. The order results of different methods are constructed in Table 9.

Results for different given methods

Results for different given methods

From Table 9, obviously, the order of these decision models is slightly different, however, the best microfinance group is

Due to the unique nature of organizational forms, group loans have become synonymous with microcredit to a certain extent. People often first pay attention to the unique credit groups and joint liability of group loans. In theoretical research, the joint and several liability of group loans is also considered an important guarantee for low default rates of small credit institution customers. However, the development of microcredit practices has reversed this certain trend. In other regions, the adaptability of group lending technology has been increasingly questioned. Therefore, it is of great significance to track the development and evolution of the relevant theoretical literature’s understanding of the technical performance of group loans, sort out the relevant explanations of the technical mechanism of group loans, clear up the relevant misunderstandings about group loans, objectively analyze the adaptability of group loans, and select and develop appropriate microfinance technologies. The performance evaluation of microfinance groups lending is a MAGDM issues. In this paper, the distances measures of single-valued neutrosophic sets (SVNSs) and maximizing deviation method (MDM) method is employed to obtain the attribute weight values. Based on the classical MABAC method, the single-valued neutrosophic numbers MABAC (SVNN-MABAC) method is constructed for MAGDM under SVNSs. Finally, an example for performance evaluation of microfinance groups lending and some comparative decision analysis are constructed to verify the SVNN-MABAC model.

This article studies the decision methods under SVNNs. Although some research results have been obtained, however, there are still many shortcomings that we need to further research in the future: (1) There is little research on the methods of combination weighting and further improvement is needed. (2) The current research mainly focuses on the improvement of a single MABAC method, and research on combination decision methods still needs further improvement. (3) With the further development of novel fuzzy sets, and the research on some novel fuzzy set still needs to be further investigated, such as the probabilistic neutrosophic sets [87, 88, 89, 90] and Trapezoidal Neutrosophic sets [91, 92, 93, 94, 95].

Footnotes

Funding

The work was supported by the 2022 high-level talent research start-up funding project of Liuzhou Vocational and Technical College, titled “Research on Rural Small Group Loans Based on Interval Intuitive Fuzzy Multiple Attribute Decision Method” (No. 2022GCQD14).