Abstract

This research explores the impact of budget deficits on inflation in Sri Lanka from 1990 to 2022, examining both long-term and short-term effects. The study uses statistical methods like unit root tests and econometric models, including the Autoregressive Distributed Lag (ARDL) model and the Error Correction Model (ECM), to assess the reliability and stability of these relationships. Inflation is the dependent variable, with budget deficits as the primary independent variable, and money supply, interest rates, and unemployment rates as secondary variables. Findings indicate an inverse relationship between budget deficits and long-term inflation, while money supply and unemployment rates positively affect inflation. In the short term, previous year’s money supply, budget deficit, and unemployment rates are negatively correlated with inflation. However, the previous year’s budget deficit and the current year’s unemployment rate significantly increase short-run inflation. Interest rates do not significantly impact inflation in either the short or long term. This study, through historical data analysis and econometric techniques, aims to clarify these impacts, enhancing understanding of Sri Lanka’s macroeconomic dynamics and aiding policymakers in sustainable economic management.

Keywords

Introduction

Government policy is defined by how the government manages its budget, which involves determining revenue, expenditure, and the budget gap (deficit or surplus) within a financial year. The budget can show the implementation of all the government’s budgetary policies for the country’s social and economic development. According to socio-economic analysis, persistent budget deficits play a vital role in the causes of inflation (Catao & Terrones, 2005), and inflation is exacerbated when governments experiencing persistent budget deficits seek to print money to finance the deficit in the short run or long run (Fischer et al., 2002). Also, inflation reduces investment by increasing the nominal interest rate and affects economic growth.

Typically, many countries worldwide grapple with deficit budgets. When nations endeavour to efficiently allocate natural resources and income between public and private sectors, they often need to spend more on their income, resulting in a fiscal deficit (Onuorah, 2013). Policymakers, economists, and analysts generally advocate for increased deficit budgeting, positing it can enhance welfare and spur economic growth (Blanchard & Sheen, 2013). This viewpoint suggests that expanding government investment in public infrastructure can catalyse economic growth by stimulating private investment (Aschauer, 1989). As for Sri Lanka, the average budget deficit rate from 1990 to 2020 is 7.06 percent of GDP. The highest recorded deficit was 11.10 percent of GDP in 2020, while the lowest was 5.12 percent in 1992. Notably, the reported budget deficit for 2022 stands at 10.2 percent of GDP.

Central bank reports indicate that Sri Lanka has grappled with deficit budgets for several decades. This persistent deficit spending exacerbates inflation, particularly when the government prints currency to finance short-term or long-term deficits. Recent Central Bank Annual Reports highlight a doubling of the fiscal deficit in recent years (Central Bank of Sri Lanka, 2019 & 2020). The government employs various strategies to address this deficit, including printing money, domestic and foreign borrowing, bond sales, and utilising foreign reserves (Akinboade, 2004). The persistent fiscal deficit in Sri Lanka significantly contributes to inflation, highlighting the need for policymakers to increase revenue through taxes and curtail excessive government spending. These measures are crucial for fostering economic growth and improving citizen well-being. (Tyrone et al., 2023). However, each financing avenue impacts other socio-economic variables within Sri Lanka. For instance, foreign reserves affect the exchange rate, while borrowing domestically and abroad impacts public debt. Moreover, printing money affects the balance of payments.

The research analyzed the influence of fiscal variables on inflation in Sri Lanka from 1965 to 2018 and post-reform from 1977 to 2018. It found that fiscal policy instruments, such as public debt, budget deficit, and public expenditure, significantly impact inflation, whereas money growth does not. The study highlighted that fiscal variables are more influential in driving inflation than monetary policy variables, emphasizing the need for effective management of public debt and budget deficits for economic stability. (Biswajit et al., 2022). Despite these measures, Sri Lanka heavily relies on domestic and external debt to manage its budget deficit, with public debt reaching 90 percent of GDP, according to the (Central Bank of Sri Lanka, 2017). Consequently, a budget deficit occurs when total government expenditure surpasses revenue within a given period. Government expenditure encompasses various elements, including public sector consumption, government employee salaries, national fixed capital depreciation, and population transfers. Conversely, national budget revenues consist of multiple types of taxes. The interaction between the budget and other sectors of the national economy is evident in the definition and impact of the budget deficit.

When a country experiences economic prosperity, its budgetary revenue typically increases without imposing additional financial burdens. Despite the perception of the expenditure side of the budget as an economic policy instrument, it often remains relatively passive, even in stable economies. However, during economic stagnation, significant shifts occur in the budgetary sector. Reductions in the tax base decrease budget revenue, while increased remittances drive up expenditure.

As a result, the effect of budget deficits on inflation varies widely from country to country. Some studies, such as those by Sahin (2019) and Jafari et al. (2011), suggest a direct correlation between budget deficits and inflation, while others, like Kaur (2021) and Touny (2017), propose an opposite effect. Consequently, the impact of budget deficits on inflation fluctuates over time and across different countries. This variability underscores the importance of examining how Sri Lanka’s continuous budget deficit influences inflation – a critical national economic indicator – in the long run.

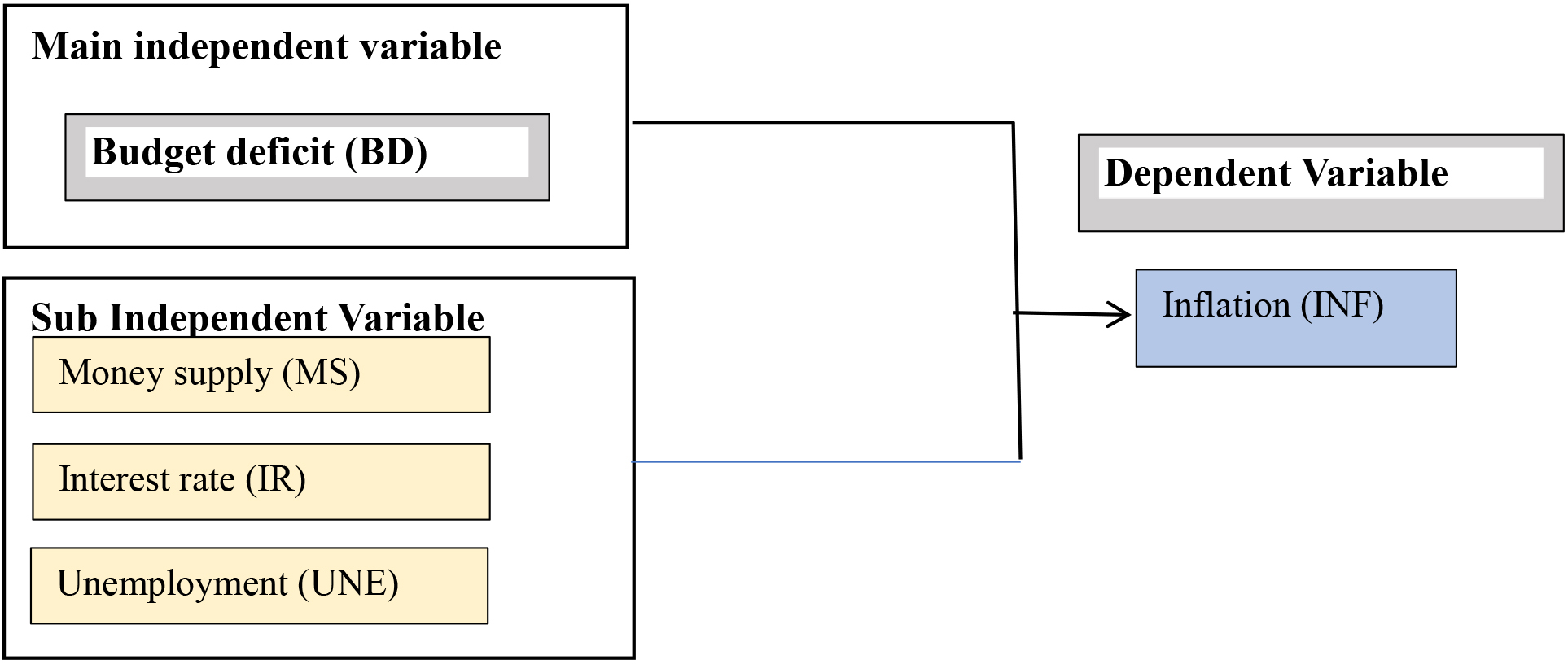

The study identifies inflation (INF) as the dependent variable, representing the general rise in prices and the decline in the purchasing value of money. The primary independent variable is the budget deficit (BD), the Difference between the government’s expenditures and revenues, which is analysed to determine its impact on inflation. Additionally, the study includes control variables: the money supply (MS), which is the total amount of monetary assets available in the economy and helps assess how changes in the money supply affect inflation; the interest rate (IR), which is the cost of borrowing money and influences inflation through its effects on consumer spending and investment; and the unemployment rate (UR), which is the percentage of the labour force that is unemployed and provides insight into economic activity and potential inflationary pressures from wage growth.

Conceptual frame work.

The research problem is that the persistent deficit budget situation in Sri Lanka has exacerbated inflation dynamics over time, as evidenced by various Central Bank reports. With the government resorting to measures such as printing currency and engaging in domestic and foreign borrowing to fund stimulus efforts, the fiscal deficit has doubled in recent years. However, reliance on these financing sources and heavy domestic and external debt has far-reaching socio-economic implications, affecting variables such as exchange rates, public debt, and the balance sheet. Despite government efforts, budgetary revenue fails to keep pace with expenditures, which include public sector consumption, employee salaries, and national capital depreciation. Economic booms may momentarily boost revenue, but stagnant periods see declines in the tax base, offset by increased remittances. The relationship between budget deficits and inflation varies across countries and timeframes, emphasising the need to assess the long-term impact of Sri Lanka’s continual deficit on national economic indicators, particularly inflation.

The necessity of this study arises from the limited research on the impact of deficit budgeting on socio-economic variables in Sri Lanka. This study aims to clarify the relationship between budget deficits and inflation, providing insights into how government funding influences inflationary trends. Understanding this relationship is crucial for devising effective fiscal and monetary policies to combat inflation. Addressing inflation necessitates a comprehensive policy approach, encompassing fiscal, monetary, and exchange rate measures, with the budget deficit serving as a vital tool for policymakers. An increase in the budget deficit typically correlates with a rise in the money supply, often leading to higher inflation rates. Consequently, clarifying the hypothesis that rising budget deficits trigger increased borrowing, thereby driving up interest rates and inflation due to heightened money supply, becomes paramount. Ultimately, this research aims to inform policymaking by providing insights into the relationship between budget deficits and inflation and their consequential impacts.

This study encompasses the following sections: Literature Review, Methodology, Analysis, Discussion, and Conclusion and Recommendations.

Studies in various countries have shown mixed results regarding the relationship between budget deficits and inflation, with some indicating positive or negative correlations and others finding no relationship. Makochekanwa (2008) highlights that the Zimbabwean economy, among others, has experienced prolonged high fiscal deficits in a hyperinflationary environment. This study examines the relationship between budget deficits and inflation in Zimbabwe.

Using Johansen’s (1991, 1995) cointegration technique, the study reviews data from 1980 to 2005 to establish a causal relationship between budget deficits and inflation rates. The findings reveal that increases in the fiscal deficit have significant inflationary effects.

Bulawayo et al. (2018), Determining whether a significant causal relationship exists between the budget deficit and inflation from 1960 to 2001. Moreover, this question needs to be sufficiently investigated by robust research in many developing countries, mainly African countries, and inflation has proved to be an intractable problem in many of these countries to certain limits. His paper investigates how the budget deficit contributes to inflation in Zambia, as policymakers must be aware of the dangers of financing public programs through excess deficit spending.

Solomon and Wet (2004) observed that the Tanzanian economy has endured a prolonged period of relatively high inflation rates alongside a substantial fiscal deficit. Their study delves into the relationship between budget deficits and inflation in Tanzania. Using pooled covariance analysis from 1967 to 2001, the research establishes a causal relationship between budget deficits and inflation rates. Dynamic simulations are employed to gauge the impact of changes in the budget deficit and GDP on inflation over time. The findings indicate that monetising the budget deficit exerts significant inflationary pressure.

Similarly, Alavirad and Athawale (2005) investigated the impact of budget deficits on inflation in the Islamic Republic of Iran using time series data from 1963 to 1999. Their analysis focused on the long-term relationship between inflation and budget deficits. Univariate cointegration tests, including Autoregressive Distributed Lag (ARDL) and Phillips-Hansen methods, were employed for analysis. An Error Correction Model was also utilised to understand the model’s short-term behaviour. The study’s results underscore the influence of budget deficits and liquidity on inflation rates in the Islamic Republic of Iran.

Jafari et al. (2011) highlight the significance of the relationship between budget deficits and inflation in macroeconomics. Their study investigates this relationship using quarterly data spanning from 1990 to 2008. The analysis evaluates the strength of this relationship concerning inflation and liquidity benchmarks. Four variables – budget deficit, monetary base, money supply, and inflation – are utilised and scrutinised. The findings reveal a significant positive impact of the budget deficit on monetary variables and, consequently, on inflation. This outcome affirms the robustness of the estimation results regarding the definitions of inflation and money supply.

In a separate study, Hinaunye et al. (2021) explored the impact of fiscal deficits on inflation in Namibia. They utilised quarterly data from 2002 to 2017 and employed the Autoregressive Distributed Lag Model (ARDL) and Granger Causal Approach for analysis. The empirical results indicate evidence of a long-run linear fiscal deficit effect on Namibia’s inflation. These findings suggest that budgetary deficits’ impact on Namibia’s inflation is positive in the long run.

A study conducted by Alwis et al. (2023) aims to explore the connection between fiscal deficit and inflation in Sri Lanka. Given Sri Lanka’s current inflationary crisis, considered the most severe in its history, and the persistent increase in fiscal deficit over the past four decades, understanding how fiscal deficit impacts inflation is imperative. Utilising annual data from 1977 to 2019, the study employs the ARDL technique for analysis. The findings indicate a positive and significant relationship between Sri Lanka’s fiscal deficit and inflation in the long and short run.

Drawing from the research of Aslam and Mohamed (2016), fiscal deficits in Sri Lanka exhibit a positive relationship with inflation, significantly accelerating it at a one percent level. According to Abeygunawardana (2017), budgetary influence plays a crucial role in determining inflation, emphasising the importance of phasing out fiscal impact for the success of inflation targeting in Sri Lanka. Maitra et al. (2022) also discovered that budgetary policy instruments in Sri Lanka generally contribute to increased inflation, while money growth does not significantly impact inflation.

His summary succinctly captures the study’s essence, delving into the relationship between deficit budgeting and inflation. Despite existing gaps in research, this study endeavours to address this by investigating how government funding impacts inflationary trends. Recognising this link is pivotal for devising effective fiscal and monetary policies to tackle inflation. The study posits that a surge in the budget deficit prompts heightened borrowing, consequently elevating interest rates and inflation through increased money supply. By elucidating these dynamics, the research aims to give policymakers valuable insights to navigate and alleviate inflationary pressures in Sri Lanka’s economy.

Methodology

Study Period and Data Sources: The research investigates the impact of budget deficits on inflation in Sri Lanka from 1990 to 2022. Ensure data reliability and accuracy, and annual time series data is sourced from reputable secondary sources. Specifically, data is obtained from the World Bank’s World Development Indicators (WDI), the Ministry of Finance of Sri Lanka’s Annual Report of the Central Bank of Sri Lanka. These databases provide essential information on variables such as inflation and unemployment rates, budget deficits, money supply, and interest rates, which are integral to this study.

Variables and Data Types: The variables considered in this study include the inflation rate, measured as the annual percentage change in the consumer price index (CPI), sourced from the World Bank’s WDI. The Unemployment Rate is also sourced from the WDI. Budget Deficit data is extracted from the Ministry of Finance’s reports, representing the variance between government revenue and expenditure. Money Supply data is sourced from the Central Bank of Sri Lanka, while Interest Rate data is also obtained from the Central Bank of Sri Lanka.

Stationarity Testing: Prior to model estimation, it is imperative to conduct stationarity tests on the variables to prevent spurious regression outcomes. The Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) tests are employed to ascertain the stationarity of the time series data. These tests aid in determining whether the variables exhibit a unit root, indicating non-stationarity, or if they are stationary at their Level or after differencing.

ARDL Model: The Autoregressive Distributed Lag (ARDL) model is selected for this study due to its versatility and resilience in accommodating varying orders of integration among the variables (i.e., I (0) levels and I (1) first differences. ARDL model along with its formulae and explanations of I (0) and I (1):

I (0): A variable is said to be integrated of order zero (I (0)) if it is stationary. Stationary variables have constant mean, variance, and autocovariance over time. I (1): A variable is integrated of order one (I (1)) if it is non-stationary but becomes stationary after differencing it once. In other words, I (1) variables have a stochastic trend and require differencing once to become stationary.

The ARDL model is used to analyse the relationship between variables that may have different orders of integration. It typically takes the form of a regression model where the dependent and independent variables are in levels or first differences, depending on their order of integration.

The ARDL methodology entails the following steps:

Model Specification: The ARDL model incorporates the budget deficit, money supply, interest rate, and unemployment rate as independent variables, with inflation as the dependent variable. Lag Selection: The optimal lag lengths for the ARDL model are determined based on criteria such as the Akaike Information Criterion (AIC) or the Schwarz Bayesian Criterion (SBC).

Bounds Testing Approach: The ARDL bounds test investigates long-run relationships among the variables. This entails testing the null hypothesis of no long-run relationship against the alternative hypothesis of a long-run relationship. The bounds test establishes critical value bounds, and if the computed F-statistic falls beyond these bounds, conclusions can be drawn regarding the existence or absence of long-run relationships.

Short-Run and Long-Run Dynamics: Upon confirming the presence of a long-run relationship, the long-run coefficients are estimated to elucidate the enduring impact of budget deficits on inflation. Furthermore, an Error Correction Model (ECM) derived from the ARDL specification captures short-run dynamics, illustrating how variables adjust to equilibrium swiftly following a change.

Model Stability and Diagnostic Tests: this validates the robustness of the findings, and several diagnostic tests are executed. ‘Model Stability and Diagnostic Tests’ ensure that the statistical model accurately reflects the data and provides reliable insights into the relationships between variables. They play a critical role in validating the findings of empirical studies and improving the overall quality of econometric and statistical analyses.

Serial Correlation Test: serial correlation is a common issue in time series data as macroeconomic variables often move together over time. In this study, the Durban-Watson test is used to examine autocorrelation. The hypotheses are:

H0: There is no autocorrelation in the model. H1: There is autocorrelation in the model.

If the probability value exceeds the threshold (0.05), we fail to reject the null hypothesis, indicating no autocorrelation. Conversely, if the probability value is lower, we accept the alternative hypothesis, indicating an autocorrelation problem.

Heteroscedasticity Test: To ensure homoscedasticity, the Breusch-Pagan Cook-Weisberg test detects heteroscedasticity. The hypotheses are:

H0: The model is homoscedastic. H1: The model is heteroscedastic.

If the probability value exceeds the threshold (0.05), we fail to reject the null hypothesis, indicating no heteroscedasticity. If lower, we accept the alternative hypothesis, indicating heteroscedasticity.

Normality Test: The normality of residuals is assessed using the Jarque-Bera test. The hypotheses are:

H0: The residuals follow normality. H1: The residuals do not follow normality.

If the probability value is higher than the threshold (0.05), we fail to reject the null hypothesis, indicating the normality of residuals. If lower, we accept the alternative hypothesis, indicating non-normal residuals.

The Ramsey RESET test detects specification errors in a regression model. The hypotheses are:

H0: The model has no omitted variables and is correctly specified. H1: The model has omitted variables and is incorrectly specified.

Stability Tests: The CUSUM and CUSUMSQ tests assess the stability of model parameters over the study period. By employing these methodologies, the study aims to comprehensively analyse the relationship between budget deficits and inflation in Sri Lanka, offering insights into both short-term and long-term economic dynamics.

Results and discussions

The result of the unit root test

The study utilised unit root test techniques, including the Augmented Dickey-Fuller Test (ADF) and the Phillips-Perron Test (PP), to assess the time series properties of the variables employed in this research. These tests were used to determine the variables’ stationarity and identify any serial integration within them. Variables, along with the results of the ADF and PP tests, are presented in Table 1.

The results of the unit root test of ADF and PP

The results of the unit root test of ADF and PP

Note: *, **, and *** refer to the significance levels of 10%, 5%, and 1%, respectively, indicating that the variables satisfy the stationarity property. Probability values are given in the table.

In the above table, Level refers to tests conducted at the Level of the variables (original data without differencing). 1st Difference means tests performed on the first Difference of the variables (to achieve stationarity).

The table above presents the summarised results of the unit root tests. The Augmented Dickey-Fuller (ADF) test was conducted on the Budget Deficit (BD) variable at a 5% significance level, with only the intercept included in the model. The test indicates that BD is stationary at the first Level, denoted as I (0). Conversely, all other variables (INF, MS, IR, UNE) are found to be stationary at the first Difference, denoted as I (1). Similarly, the Phillips-Perron (PP) test, including only the model intercept, confirms the stationary nature of BD at the Level. Therefore, based on the ADF and PP test results, BD is considered stationary at I (0), while all other variables exhibit stationary behaviour at I (1). Consequently, the ARDL Bound test method is employed to estimate the parameters in this study.

After confirming the stationarity of all study variables, an optimal lag length test was conducted to determine the suitable lag lengths for the ARDL model. This step is crucial for capturing the dynamic relationships among the variables. Various statistical criteria were utilised to identify optimal lag length, including Log likelihood value (LOGL), Likelihood ratio statistic (LR), the Final Prediction Error (FPE), Akaike Information Criterion (AIC), Schwarz Criterion (SC), and Hannan-Quinn Information Criterion (HQIC) The summarised results of these tests are presented in the Table 2.

Optimum lag length for ARDL model

Optimum lag length for ARDL model

Note: ‘*’ recommends optimal lag length level.

As per the LR, FPE, and AIC criteria, the optimal lag length level is recommended to be two-time lags. Therefore, our study has utilised two-time lags as the optimal lag level for the ARDL model. Subsequently, the results obtained using these two time lag lengths for selecting the best model through the AIC criterion are presented below.

The consistent findings highlight the effectiveness of a lag length of two in capturing variable dynamics. Therefore, the ARDL model with lag lengths (1, 1, 2, 1, 2) is selected as the optimal model due to its superior performance based on the AIC criterion’s lower error values. This model configuration effectively balances the need to capture the relevant past values of each variable while maintaining an economic structure. By adopting the optimal lag length determined through rigorous statistical testing, the study ensures robust and reliable modelling of the relationships between budget deficits and inflation in Sri Lanka over the specified period.

The bound test in econometrics aims to confirm the presence of a long-term relationship between variables through cointegration analysis, ensuring stability despite short-term variations. It validates whether economic factors move cohesively over time, which is essential for predictive modelling and policy formulation. Subsequently, upon confirming the cointegration relationship, the long-run relationship among the variables was determined using the bound test of the ARDL model. Meanwhile, both the short-run relationship and long-run adjustment were captured using the ARDL error correction model. As such, the result obtained from the bound test for the ARDL model (1, 1, 2, 1, 2) utilised in this analysis is provided in Table 3.

The results of the ARDL bounds test

The results of the ARDL bounds test

Based on this result, the F-statistic is 13.05, and the upper limit value of I (1) is 3.49 at the 5% significance level. Consequently, as the F-statistic exceeds the upper limit value, the null hypothesis stating no cointegration relationship between the variables is rejected. Thus, the presence of a cointegration relationship among the variables is confirmed.

Given the confirmed cointegration relationship among the variables, the results for the long-run relationship derived from the ARDL (1, 1, 2, 1, 2) model are presented in the Table 4.

The long-run relationship of the ARDL model

The long-run relationship of the ARDL model

The long-run relationship of the ARDL model, with inflation as the dependent variable, reveals significant coefficients for several independent variables. A statistically significant and positive relationship is observed between the independent variable of money supply and inflation at the 1% significance level. Specifically, if the money supply increases by one percent, holding other factors constant, inflation will rise by 15.9 percent in the long run. This discovery aligns with Fisher’s monetary theory and is corroborated by findings from previous studies conducted by researchers such as Fan (2016), Abdulgafar (2017), Amassoma (2018) and Akinbobola (2012).

A budget deficit negatively impacts inflation, which is statistically significant at the 1% significance level. Holding other factors constant, a 1% increase in the budget deficit decreases inflation by 0.03% in the long run. If the government uses spending effectively for investment purposes, it will increase investment and increase output. This may reduce inflation in the future. Also, the results of some studies already carried out by, Kaur (2021), Touny (2017), and Cochrane (1998) reveal the same conclusion.

The unemployment rates have a statistically positive impact on inflation at a 1% significance level in the long run. If the unemployment rate increases by one per cent, other factors remain constant; inflation will increase by 5.9 per cent in the long run. Although this finding contradicts the short-run Phillips curve, recent studies indicate that the relationship between inflation and the unemployment rate changes over time and varies across countries. (Example: Roberts, 2006; Vinayagathasan & Xiangcai, 2021; Primiceri, 2005; Gillitzer & Simon, 2015). Because most developed and developing countries have culturally, institutionally, and economically diverse backgrounds, the relationship between these variables changes over time and differs from country to country, according to Balakrishnan et al. (2011).

It can be observed that interest rates have no statistically significant impact on long-term inflation. When interest rates rise, investors and consumers adjust their strategies accordingly. Although it may affect inflation in the short term, it may not have any impact in the long run. Also, the results of some studies that have already been carried out, Brzoza-Brzezina (2002); Barsky (1987); Huizinga and Mishkin (1984), Noor (2003), Mishkin (1992) and Ghazali (2003) express the result itself.

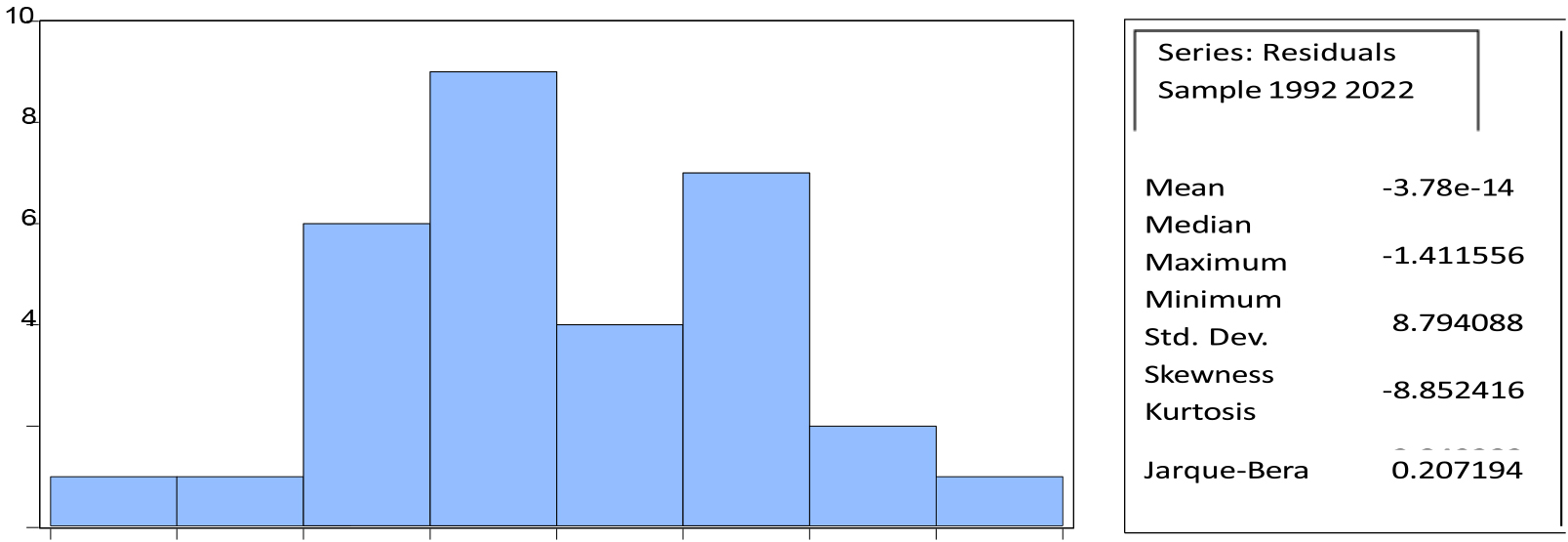

The histogram of residuals shows a roughly symmetric distribution around zero. The mean residual is nearly zero (

Histogram – normality test.

In the subsequent analysis, the results of Ramsey’s RESET test, which aims to identify potential omitted variables in the model, indicate rejection of the null hypothesis. The null hypothesis posits the absence of omitted variables, but the probability value falls below the 5% significance level (0.01

However, the consistency test outcomes show no issues related to autocorrelation; as per the LM test, the

Finally, as per the BPG Test for find out the Heteroscedasticity,

Consequently, the ARDL (1, 1, 2, 1, 2) model is deemed the best fit.

In this study, employed ARDL’s error correction model to analyse the short-run relationships among the variables and to understand how the model adjusts from short-run shocks to a stable long-run equilibrium. The results obtained using this error correction model are presented in the Table 5.

The results of the error correction model (ECM)

The results of the error correction model (ECM)

Significance levels: *, **, *** denote significance at 10%, 5%, and 1%, respectively. Probability values are given in parentheses.

In the table, “D” stands for the first Difference of the variable, indicating the change in the variable from one period to the next.

The error correction term (ECT) (

Examining the short-term relationships among the variables reveals that the current money supply, current budget deficit, and lagged unemployment rate have negative and statistically significant effects on present inflation. Specifically, a one percent increase in the money supply results in an 88.66% reduction in inflation, while a one percent increase in the budget deficit leads to a 0.01% decrease in inflation. Additionally, a one percent increase in the previous year’s unemployment rate corresponds to a 3.75% decrease in current inflation.

Conversely, the previous year’s budget deficit and the current unemployment rate positively and significantly affect present inflation in the short term. A one percent increase in the previous year’s budget deficit is linked to a 0.02% rise in current inflation, while a one percent increase in the current unemployment rate results in a 2.65% increase in present inflation. However, the current interest rate (IR) does not significantly impact inflation in the short term.

The model’s R-squared value of 0.83 indicates that about 83% of the variation in inflation changes is explained by the model. The F-statistic of 13.05 reflects the overall significance of the model, suggesting it fits the data well.

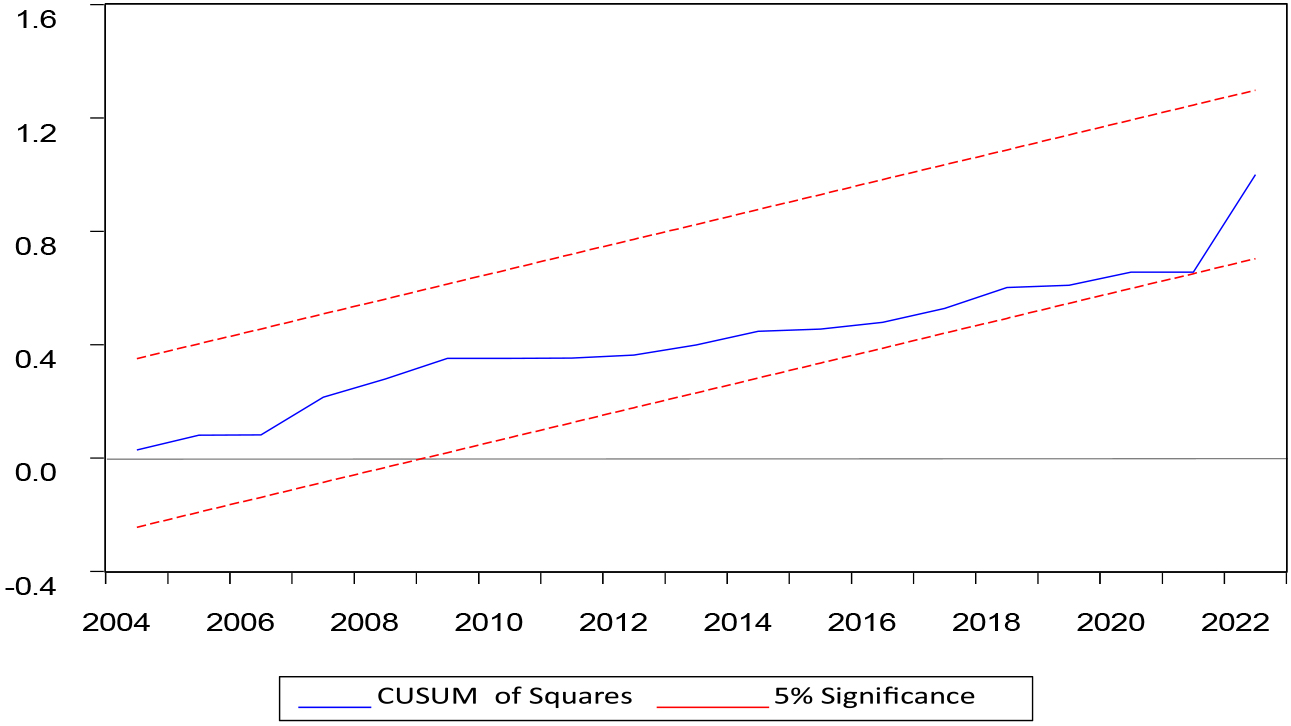

The consistency of the selected ARDL (1, 1, 2, 1, 2) model was assessed using the CUSUM and CUSUMSQ. The results are illustrated in the Figs 3 and 4, respectively.

The result of the CUSUM test.

The CUSUM test plot displays the cumulative sum of recursive residuals over time, with the blue line representing the cumulative residuals and the red lines indicating the 95% confidence interval bounds. This test aims to assess the stability of the regression coefficients in the model. In this plot, the blue line remains within the red lines throughout the sample period, indicating no significant shifts or structural breaks in the coefficients. This suggests that the model’s parameters are stable over time.

The result of the CUSUMSQ test.

The CUSUMSQ test plot shows the cumulative sum of squares of recursive residuals, with the blue line representing the cumulative squared residuals and the red lines representing the 95% confidence interval bounds. This test is more sensitive to changes in the variance of the residuals, which can indicate instability. In this diagram, the blue line also remains within the red lines throughout the sample period. This suggests that the variance of the residuals does not exhibit significant changes, further confirming the stability of the model.

The CUSUM and CUSUMSQ test results show that the blue lines (residuals) lie within the 95% confidence intervals (red lines). This consistency within the bounds implies that the ARDL (1, 1, 2, 1, 2) model is stable over time. The lack of significant deviations or crossing of the confidence bounds in both tests indicates that the model’s parameters do not exhibit instability or structural breaks, confirming the reliability and robustness of the model.

In conclusion, the research findings reveal a significant and negative long-term relationship between the budget deficit and inflation in Sri Lanka, aligning with the results of Kaur (2021), Mahmoud A Touny (2017), and Cochrane (1998). Conversely, both the money supply and unemployment rate show a positive association with inflation, consistent with the findings of Fan (2016), Akinola and Abdulgafar (2017), Amassoma (2018), and Akinbobola (2012). In the short run, the current money supply, current budget deficit, and last year’s unemployment rate demonstrate an inverse relationship with inflation. In contrast, last year’s budget deficit and current unemployment rate positively correlate with inflation. Interest rates do not show a statistically significant relationship with inflation in either the short or long run, consistent with the conclusions of Brzoza-Brzezina (2002), Barsky (1987), Huizinga and Mishkin (1984), and Ghazali and Noor (2003). Additionally, consistency tests confirm the absence of heterogeneity, non-normality, and autocorrelation in both the short run and long run, while CUSUM testing confirms the stability of the model.

Fisher’s monetary theory suggests increasing the money supply leads to inflation unless matched by output growth or changes in money velocity. Governments should direct new money to productive investments like infrastructure and technology to boost output and mitigate inflation. The positive relationship between unemployment and inflation indicates the need for policies fostering investment and growth to manage both issues. Prudent fiscal management, focusing on investment rather than current expenditures, mitigates inflationary pressures. Policymakers should prioritise food security initiatives to protect vulnerable populations. Future research should explore additional inflation factors, longer and more granular data periods, and alternative modelling techniques to enhance the understanding and robustness of findings. Incorporating unexpected shocks and policy changes in analyses can provide insights into economic resilience.