Abstract

Analysis of contagion continues to attract growing interest from both regulatory authorities and the academic world and we are witnessing the development of analytical approaches for assessing the risk of contagion in the interbank market. Indeed, given its role in financial stability and monetary policy, the Central Bank must be able to accurately determine the level of international vulnerability associated with various scenarios for cross-border contagion, both to prevent than to manage situations systemic crises. The purpose of this study is to assess the risk of cross-border contagion of the Moroccan banking system through the data of the “BIS”. The methodology is to first approximate the gross bilateral exposures using data from the banks’ financial statements. Then simulations based on contagion algorithm integrating counterparty risk are conducted to assess the risk of contagion. Also centrality of indicators and measurement of systemic importance are presented. The results were synthesized in indicators to assess the systemic importance of the French banking system internationally to Morocco; the fall of the latter is a significant risk of contagion.

Introduction

The international financial crisis has propelled the analysis of systemic risks and the importance given to the various shocks of transmission channels. Alongside the domestic risks to which is exposed the banking sector, cross-border exposures were an active channel during the financial crisis of 2008. Thus, several countries (including Germany, Belgium, the Netherlands and Switzerland) had faced the international financial crisis, despite favorable economic conditions, due to their foreign exposures to the United States.

The banking sector is exposed to two main sources of risk arising from exposures of banks, domestic or foreign, to a common risk (macro risk) and the effects of domestic and cross-border contagion. In a situation of systemic crisis, the sources of risk are mutually reinforcing and should be considered when analyzing systemic risks. Although aspects related to exposure to common risks have been widely detected, those relating to foreign exhibitions remain less explored.

The channel of interbank contagion across borders is a major shock transmission channels within the banking industry. So an analysis of this channel is essential to better understand the problem of systemic risk. Furthermore, this study is a central objective of financial stability. Compared to other transmission channels of shocks, this channel is difficult to assess due to the difficulty of approaches and techniques to quantify, compared to other channels which are known methodologies.

The interbank contagion has already been quantified by several central banks, including those with data on bilateral exposures (gross or net) of banks. Indeed, central banks, one of whose main tasks is overseeing markets continuously collect and closely follow the evolution of interbank transactions, blank and with guarantee, which facilitates the monitoring of bilateral exposures on the interbank market.

The second dimension of the risk of contagion on foreign exhibitions is against tricky to quantify, mainly due to the scarcity of data and the difficulty to follow the various international transactions. However, the Bank for International Settlements (BIS) has a database of exhibits tracing the development of each banking system abroad. On this register, this data can be very useful to quantify the risk of cross-border contagion.

The BIS provides banking consolidated data on cross-border exposures. This data is generally used by central banks and supervisory authorities to assess vulnerabilities and weaknesses that can result from a high exposure or increased interconnection between the domestic banking sector and foreign banking sectors.

In this paper, it is proposed to present some indicators to assess the risk of cross-border contagion using the BIS database and also the accounting situation of Moroccan banks. BIS statistics provide a vision on Morocco’s commitments to the outside and thus provide an overview of its exposure in terms of funding, vis-à-vis the outside. Furthermore, the review of the accounting situation quantifies foreign exhibitions in terms of having and commitment. This work is organized in four sections. The first presents a review of theoretical and empirical literature the risk of contagion. Then a presentation of the data used is performed. In a third point, the analysis focuses on the construction of cross-border contagion risk indicator. Finally, the last point presents a contagion model for measuring the potential default risk that can run the Morocco following an exogenous shock.

Empirical review

Systemic risk has generated much interest and especially in connection with the notion of contagion. The risk of contagion that Claessens and Forbes [15] turns a specific shock systemic shock to upset the analysis of financial stability and also the financial regulatory policies. Indeed, the transverse dimension of risk is at the heart of the debate because of the difficulties in implementing approaches able to provide adequate and complete answers to the risk analysis.

Due to the strong interconnection between global financial markets, a shock that affects one country generates turbulence in the financial market that could be spread to its partner countries. The effect of cross-border transmission of shocks between countries, commonly called cross border contagion was often mentioned as one of the triggers of crises in Mexico in the early 1990s and those of Asia, Russia and Brazil in late these years (Claessens and Forbes [15]). Eichengreen et al. [21], a seminal work, were the first to observe the phenomenon of contagion at the end of an analysis of the crisis of Mexico. While the analysis of cross-border contagion is the basis for understanding the financial turmoil in times of de-stresses, however, there is hardly unanimous and uniform definition of the concept (Eichengreen et al. [21]). Some researchers whose Calvo and Reinhart [12], Masson [48] and Kumar and Persaud [42] distinguish between two types of contagion mechanism or transmission of shocks: “The fundamental contagion” (fundamentals-based contagion or spillovers), dependent on real and financial linkages between countries (Glick and Rose [31], Rijckeghem and Weder [59]), and “pure contagion” (pure contagion) that cannot be explained by a change in fundamentals. This type of infection is fundamentally linked to expectations of economic agents.

In theoretical terms, the pure contagion combines the propagation of shocks to specific behaviors adopted by investors in times of uncertainty. The asymmetry of information available to investors and the degree of risk aversion can explain the behavior of gregarious qualified investors (Calvo [12]). The concrete example is that of a shock to a country which led investors to change their perception of risk in other countries because they consider that their macroeconomic fundamentals are similar, without ascertaining whether the similarities are real or just apparent.

Moreover, the existence of real and financial relations between countries can cause a transmission crisis from one country to another. In this respect, the integration of countries causing spillovers or training (spillover effects) in the terminology of Calvo and Reinhart [12]. For this purpose, it is necessary to distinguish between the real and financial interdependencies. The actual channel is usually associated with international trade and multilateral trade exclusively (Eichengreen et al. [21], Glick and Rose [31]). Indeed, Gerlach and Smets [29] were the first to model the spread of a currency crisis through this channel. In their model, a currency crisis in one country lead to a depreciation of its exchange rate by this effect and enhance its competitiveness over other countries exporting the same markets which ultimately will increase the probability of occurrence of crisis changes elsewhere. Regarding the financial channel, the plurality of actors in the financial system and the diversity of the links between the various markets such system can facilitate the spread of financial distresses. The banking system remains the most dynamic financial channel in the propagation of shocks. Indeed, two types of mechanisms are responsible for the transmission of financial crises or currency through the banking system. The first is the common effect creditor (lender common effect, Van Rijckeghem and Weder [59] and by Kaminsky et al. [41]). A banking panic generated in a country that is a common market for several creditors is able to make these markets vulnerable. Indeed, facing a massive withdrawal of deposits, banks in crisis Source country will tend to recover their capital invested in foreign markets to meet the needs of their domestic depositors jeopardizing the situation of these markets. In an analysis of the Asian and Mexican crises, Kaminsky et al. [41] compared the total loans that were granted to them before and after crises. It turns out that the loans granted by the European and Japanese banks have reached 165 and 124 billion respectively before the crisis and have suddenly been reduced by $47 billion after the outbreak of the crisis. In contrast, the second mechanism attributes the drain creditors to deregulation faced by markets. Indeed, once a market passes a distress situation, the banks that have loans granted to it must make the necessary adjustments to restore their capital and therefore their solvency ratio. Thus, they will tend to reduce their credit lines.

Empirically, the first work on the risk of contagion were interested in the analysis of domestic contagion without bypass the cross-border dimension. But the increased presence of multinational banks in different countries via subsidiaries or branches, recently raised intense debate about the risk of spread of negative shocks from the country of origin or vice versa (Roubini, 2012; Popov and Udell, 2010; De Haas and Van Horen, 2015; Giannetti and Laeven, 2012).

Indeed, the lessons of the 2008 financial crisis showed that foreign banks are potential channels of transmission of negative shocks initially triggered in the United States to spread around the world. Furthermore, transmission of financial contagion through the interbank channel depends on the level vis-à-vis the bank in de-stresses exposure. To this end, it is the creditor banks with high exposures to suffer a loss in value of their capital loss that can worsen further following the massive withdrawal of depositors (Allen and Gale [3]).

Although interest to analyze the various transmission channels of contagion is crucial empirical work remains limited. First, the lack of data on interbank exposures demonstrated the difficulty in collecting this type of information particularly in times of crisis. As a result, at the time of occurrence of a bank run, it would be difficult to return the shock transmission circuit. Apart from the data problem, the low frequency of occurrence of bank failures justifies the paucity of research on the subject since regulators have always used the bailout to circumvent bank runs. On this register Schoenmaker and Goodhart [32] concluded, following an analysis of 100 bank failures, the monetary authorities of developed countries prefer to act as lender of last resort to save institutions whose failure may lead to a crisis systemic.

From a practical point of view and apart from the difficulties discussed before, the contagion risk is evaluated on the basis of three main approaches, namely: market approach, the balance sheet approach and the simulation. The majority of empirical studies using the market approach based on analysis of market indicators to detect any contagion. They look at the analysis of asset price developments with the aim of testing whether the price change of an asset of a country will affect asset prices in another country using different techniques based on the observation that the risk aversion of investors will be the source of the contagion (Baig and Goldfajn [5]; Bae et al. [4]; Corsetti et al. [16] and Forbes K., 1999). Aharony and Swary [1], analyzed the market reaction following the bankruptcy of five major banks in the southwestern United States in the years mid 1980s by calculating the return on bank shares. It appears that banks have been affected by the contagion effect posted negative returns, this being due to information asymmetry. On a sample of European banks from January 1994 to January 2003, Reint Gropp et al. [33] use the distance to default defined by the KMV model. For each country, the authors calculate the number of banks having suffered a shock. The transmission of shocks between countries reflecting the contagion effect is emphasized by a logit model relating the variable of a given country to those delayed for other countries in addition to four variables common factors controlling them (Forbes and Rigobon [25]). These factors include systemic risk, yield curve, volatility of the domestic stock market in addition to the volatility of the US stock market. The significance of the coefficients of lagged variables attest to the transmission of shocks from one country to another.

By the same logic, Hartmann et al. [36] use the multivariate extreme value theory to prove that the contagion effect has increased gradually in Europe and the United States since the mid-1990s in a recent study, Carlos Bautista et al., 2007 is treated contagion within and between countries of Southeast Asia. They used weekly data for stock quotes 125 banks over the 2000–2005 period to build a measure of the risk of contagion. This measure is based on the average correlation residues of a market model. The results show that the average correlations significantly differ from one country to another. The likelihood of a specific shock spreads to other institutions across borders is determined by the values of indicators of risk assets and market risk (systematic risk). However, liquidity risk indicators are at the origin of domestic contagion, suggesting that market participants are rather influenced by insolvency as illiquidity across borders.

The balance sheet approach to assessing the impact of contagion explores the transmission mechanism via the interbank channel. In this regard, several studies have looked towards the analysis of depositor withdrawals during periods of crisis. These studies verify that these withdrawals are random events (Diamond and Dybvig [20]) or based on fundamental (Chari and Jagannathan [13], Jacklin and Bhattacharya [39], and Allen and Gale [3]). On this register, Allen and Gale [3], an unexpected rajoutent liquidity shock is less vulnerable in the event of full market structure, in the sense that all banks traded between them, in case of sole presence of bilateral exposures. Schumacher [55], through an analysis of the deposits of Argentina after the outbreak of the Mexican crisis of 1994 found that the withdrawals were first surveyed in banks with low strength indicators. The same in Chile and Mexico has been raised by Martinez Peria and Schmukler, 2002. Rajkamal Iyer and José-Luis Peydró [38] exploited the matrix of actual exposures to analyze the impact of an idiosyncratic shock caused by the failure of a large bank in India. At the end of their analysis, the probability of facing massive withdrawals increased by 34% if a bank holds significant vis-à-vis the failed bank exposures. In terms of assets, empirical work is based on analysis of the BIS data that transcribe aggregate foreign claims of BIS reporting banks. It appears that a contagion effect is materialized by a reduction in appropriations by the mechanism of mutual lender described above. In this context, a recent study by McGuire and Tarashev [49] was based on the analysis of the BIS data 1999–2007 to establish the link between the granting of loans to emerging countries and soundness of the banking sector. It appears that the weakening of multinational banks and the economic environment of their respective countries systematically leads to a reduction in appropriations made by their subsidiaries in emerging countries. Adam Geršl [30] examined the BIS data for the countries of Eastern Europe and Central Europe. He concluded that three factors determine the degree of risk of cross-border contagion in the region, namely the maturity of the exposure, the concentration of exposures and the existence of a common creditor (lender common effect).

In October 2010, Thierry Tressel develops a contagion model based on balance sheet identities to simulate the losses suffered by the multinational banks from 19 countries and compare them to actual losses recorded during the last financial crisis of 2008. His model also allows restore the flow of propagation of shocks across countries following the common credit effect. To do this, the author is based on BIS data that transcribe the bilateral exposures between countries and was interested in two shock transmission mechanisms, the first following a shock on the asset side the second on the liability side. The advantage of the model is that it does not require the failure of a banking system to trigger the transmission mechanism but rather assumes maintain a minimum leverage ratio. Following the first shock, the model has revealed that banks undertake to reduce their foreign exhibitions, namely credit, as they suffer a loss in assets. This impact appears the same magnitude that was observed during the financial crisis. On the liability side, if the banks do not access alternative sources of funding due to a shortage of liquidity in the interbank market, balance sheet contraction is amplified further.

Other works of interest to the transmission mechanism between multinational banks and their subsidiaries through the analysis of internal capital market. This market allows a reallocation of resources between banks and their subsidiaries. De Haas and Van Lelyveld [18] divided the impacts that could affect this market into two categories: financial shocks and real shocks. If a financial shock hits the country, where the branch office, the parent bank will allocate additional capital to the subsidiary. In the opposite case (the shock hits the country) the bank shall proceed to withdraw these funds subsidiaries to restore its financial situation. With regard to real shocks, they occur outside the banking sphere and can induce adverse effects on loans distributed by multinational banks.

For data scarcity problem on interbank exposures, several research projects have adopted an alternative approach by simulation with the aim of studying the phenomenon of contagion. In this regard, Humphrey [37] Austria uses the data to simulate the impact of a failure of a payment system. Upper and Worms [58] apply a counterfactual simulation technique on data from the German interbank exposures to conclude that the failure of a bank induces a loss of 15% of banking system assets. Elsinger et al., 2003 analyze the contagion effect in the Austrian interbank market following an idiosyncratic shock. It appears from the analysis that 75% of bank defaults were due to contagion. Degryse and Nguyen [19] explore the risk of contagion in the Belgian banking market during the period 1993–2003 and shows that the passage of a complete structure where all banks are connected together in a “monetary base” structure (money center structure) has reduced the risk of contagion. Although the simulation approach is deemed successful in analyzing the risk of contagion, several authors including Degryse and Nguyen found that it is more appropriate to the context of domestic and cross-border contagion instead.

Grzegorz Halaj and Christoffer Kok [34] recently deployed a new simulation approach based on stochastic modeling (stochastic modeling block) in order to generate inter-bank exposures, and a sample of 89 European banks. The advantage of this approach is that it allows to identify the most systemic institution whose failure will cause large contagion. This approach was confirmed by the calculation of an indicator, called Systemic Probability Index (SPI).

Data

The Bank for International Settlements (BIS) quarterly publishes statistics on international banking. These statistics are divided into two categories namely the consolidated banking statistics (consolidated banking statistics, CBS) and banking statistics (locational banking statistics, LBS). CBS based on the criterion of the country of origin or nationality of the creditor banks. However, the LBS are based on the criterion of territorial location or residence of the creditor banks. They include resident credit institutions to domestic or foreign capital (subsidiaries and branches).

The first statistics (territorial) were developed in the late 70s in order to assess exposures on the various financial markets. By cons, CBS were produced for the first time after the debt crisis in Latin America in the early 80s to assess counterparty risk and financial exposure to contagious. Thus, CBS main objective to assess the credit risk of reporting institutions by providing data on a global and consolidated basis.1 Indeed, they have been designed to facilitate the monitoring and management of total risk exposure of banking systems unlike the territorial statistics, which are based on the principle of country of residence and are intended to supplement the monetary aggregates related data credit and published by central banks.

Consolidated Banking Statistics (CBS). The CBS are classified according to two criteria: residence of the borrower, based on the risk allocation (ultimate risk basis, immediate borrower basis),2 type of risk, rather than accounting, borrower sector and maturity. The data based on the ultimate risk criterion are assigned to countries on which the ultimate risk to determine the exposure of the country credit risk. The ultimate country risk is defined as the country in which the guarantor of a debt resides and/or country where the seat of a legally dependent branch is located. The guarantor is responsible for the service of any non off payment obligation in case of failure of the direct borrower. Indeed, these statistics are the most appropriate source for measuring the aggregate exposure of the banking system towards a given country because, unlike consolidated statistics on an immediate borrower basis, they are adjusted net risk transfers this which generally helps to assess the ability of creditors to enforce their claims.

Based on the direct borrower, foreign claims cover financial receivables, risk transfers, and liabilities reported by banks headquartered in the reporting country and certain affiliates of foreign banks. However, on an ultimate risk basis, data cover the receivables from the balance sheet and certain off-balance sheet exposures of banks headquartered in the reporting country.

Furthermore, based on the direct borrower, banks report their outstanding loans and securities portfolio, classified as “receivables” in the consolidated banking statistics. On an ultimate risk basis, banks shall also communicate separately, their commitments and their derivatives contracts.

Thus, we distinguish between two types of loans namely local claims that aggregate claims on residents of the country where the bank is agreeing claims and cross-border debts which are the positions in case the counterpart country is different that of the bank granting the credit (see Table 1).

Types of CBS Claims

Types of CBS Claims

Source: BIS.

Based on the direct borrower, receivables3 are broken down into local claims in local currency and international receivables which include local claims in foreign currency and cross-border claims. By cons, on the basis of ultimate risk, a distinction between cross-border claims (on non-residents accounted for either by the office or by an agency abroad) and local (booked through an agency abroad, on residents).

Claims on the basis of the direct borrower include all financial assets in the balance sheet except for derivatives with a positive market value are excluded. For cons, the data on these (derivative contracts and commitments by signature4 which include guarantees and credit lines) are reported on a consolidated basis and ultimate risk criterion. The receivables include, on the basis of the direct borrower, deposits and balances placed with banks, loans and advances; commercial loans, certificates of deposit, promissory notes, bonds, asset-backed CDOs and asset-backed securities, banknotes and coins in assets and holdings, including holdings in non-banking subsidiaries.

In addition, receivables are disaggregated by sector of activity of borrowers namely the public sector, banking, non-banking financial institutions, non-financial private sector (households and non-financial corporations). This breakdown applies to international claims on the basis of the direct borrower and for foreign receivables, which include cross-border and local claims on ultimate risk basis. A breakdown by maturity is required for international claims on the basis of the direct borrower based on a remaining maturity (up to 1 year included between 1 and 2 years and included more than 2 years).

The claims on ultimate risk basis are equal to the sum of claims on an immediate borrower and net risk transfers. Since the place depends on whether the statements are made on the basis of the direct borrower and ultimate risk, the net risk transfers can not be obtained from the disaggregated data and are available only for total foreign claims.

The banking local statistics LBS. The banking statistics (LBS) have been designed to provide comprehensive and consistent quarterly data on international banking. These statistics include claims and liabilities vis-à-vis non-residents in any currency, as well as claims and liabilities vis-à-vis residents of countries reporting in foreign currencies. As of Q2 2012, receivables in local currency and vis-à-vis residents of the reporting country are also collected. Thus, LBS cover all financial assets and liabilities of reporting banks.

LBS are broken either by the residency of the counterparty (banking statistics by residence (LBS/R)) or the nationality of the reporting institution (banking statistics by nationality (LBS/N)).

The LBS/R provide quarterly statistics of all balance sheet positions (financial claims and liabilities) and some off-balance sheet positions. These different positions are broken down by instrument, currency, counterparty sector and country of the counterparty.

Breakdown by instrument assets are broken down into: (a) “Loans and deposits”, which include interbank deposits and loans and advances (banks or non-banks), (b) “securities holdings” and (c) “other assets” Similarly, banks’ commitments should be broken down into: (a) “Loans and deposits”, which include interbank loans and deposits received (banks or non-banks), (b) “debt securities issued” and (c) “other liabilities”.

Currency breakdown: the breakdown calculates flows from stock data, which can be used to indirectly evaluate the transactions of the balance of payments. Reporting countries are required to provide a breakdown of local currency positions (national) and in various currencies. This breakdown includes at least the local currency of the reporting country, the dollar, the euro, the yen, Swiss franc and pound sterling.

Breakdown by sector: Positions are also broken down by sector of borrowers ie the banking sector (including central banks), nonbank financial institutions, non-financial sector (general government, households and non-financial corporations).

Breakdown by counterpart country: in case the country of residence of the counterparty is not identified, the data should be allocated to: developed countries, offshore centers, Africa and Middle East, Asia Pacific, Europe and Latin America.

The LBS/EN provide information on banking activity by residence of the bank in the country of the reporting bank and by nationality. Indeed, the LBS/N are grouping the LBS/R. these statistics are broken down by nationality of the bank, currency and counterparty sector. Unlike LBS/R, the LBS/N does not contain a full breakdown of positions by type of instrument. As of Q4 2013, banks are also asked to provide a breakdown by residual maturity for their commitments.

There are many ways to exploit the BIS data for the purpose of assessing the risk of cross-border contagion. If one is in the presence of the reporting country, it can easily use these data for its positions as much as debtors with various foreign banking systems. However, non-reporting countries may only view their level of borrowing from other countries, which may facilitate the assessment of their commitment abroad. BIS Data can also monitor the dynamics of cross-border exposures due to the depth of the data available.

In order to assess the risk of cross-border contagion, it is proposed to consider the data of interbank exposures of BIS mainly referring to consolidated banking statistics. Thus, on the basis of foreign claims (cross-border claims and local claims in foreign currency and local currency), it is proposed to follow three indicators to capture the importance of cross-border contagion risks. It should be noted that Morocco is not a reporting country but it is perceived at the statistics of the BIS as a borrower.

First, the first proposed indicator captures the importance of exhibitions of Morocco vis-à-vis the outside. In this sense, the relationship between the foreign exhibitions and nominal GDP measures the importance and impact of commitments on all of the Moroccan economy.

Then, a second proposed ratio expresses foreign exhibitions compared to total assets of the Moroccan banking system. This indicator measures the balance of foreign exhibitions in the country in relation to total assets. The more this ratio the greater the risk of cross-border contagion is important and its adverse consequences will be for the domestic banking system.

A final indicator is calculated to quantify the extent of contagion risk and approximate the existence of common borrower (common lender). This is the Herfindahl–Hirschman index (HHI). This ratio measures the risk of contagion to the forefront following exposure to an ultimate borrower. Morocco is more exposed to a single borrower the greater the risk of contagion is important.

Regarding foreign exposures reported to nominal GDP, the share has increased in recent years mainly due to the increase of FDI and also to the importance of foreign-owned banks in Morocco. Thus, this ratio, describing the importance of exhibitions in the economy, reached almost 35% at end 2012, which remains a more or less important threshold because of its potential impact on the Moroccan economy in case of problems foreign countries.

Foreign exposition from the nominal GDP. Source: BIS, by author.

The second indicator pertaining Morocco’s total foreign exposures to total assets of the banking system indicates a certain stagnation between 2007 and 2012, hovering around 25%. In this sense, the share of funds from foreign banks is the fourth of bank assets, which is a very high level and more or less information about the risk of contagion that can support the Moroccan banking system in case of trouble affecting donor banks.

Foreign exeposition to total asset of banking system. Source: BIS, author.

Increased exposure to foreign largely indicates the importance of bank financing (outside) in the Moroccan economy.

HHI Index. Source: BIS, by author.

The HHI indicates a significant increase in the concentration in recent years indicating a high degree of exposure vis-à-vis the French banking system in particular. Indeed, the French banking system alone contributes more than 50% of Morocco’s commitments.

In addition to capture the ratios of exposure Morocco as abroad, other indicators have been chosen to describe the risk of cross-border contagion based on network analysis. Using the consolidated database at the BIS, the centrality and dependence measures were calculated. These include the degree of centrality, intermediate centrality and centrality by eigenvectors.

The centrality degree. This indicator measures the relationship between the different components of the network. Generally, it is broken down into two major indicators measuring inputs and outputs. Entries assess the number of flows to a network component and outputs indicate the number of outflows. This centrality indicator is calculated using the following equation:

The intermediary centrality. It quantifies the level of attachment of a component to the other network elements without considering the direct links already in place. In fact, this indicator is used to identify indirect links with other components using the direct links. In other words, this indicator provides an indication of the “exclusive” to the position of a component “i” in the global network by counting the number of paths between two nodes through ‘i’. Thus, this measure is important to identify network components whose removal would exert the strongest effect on resilience. The intermediate centrality is determined through the following equation:

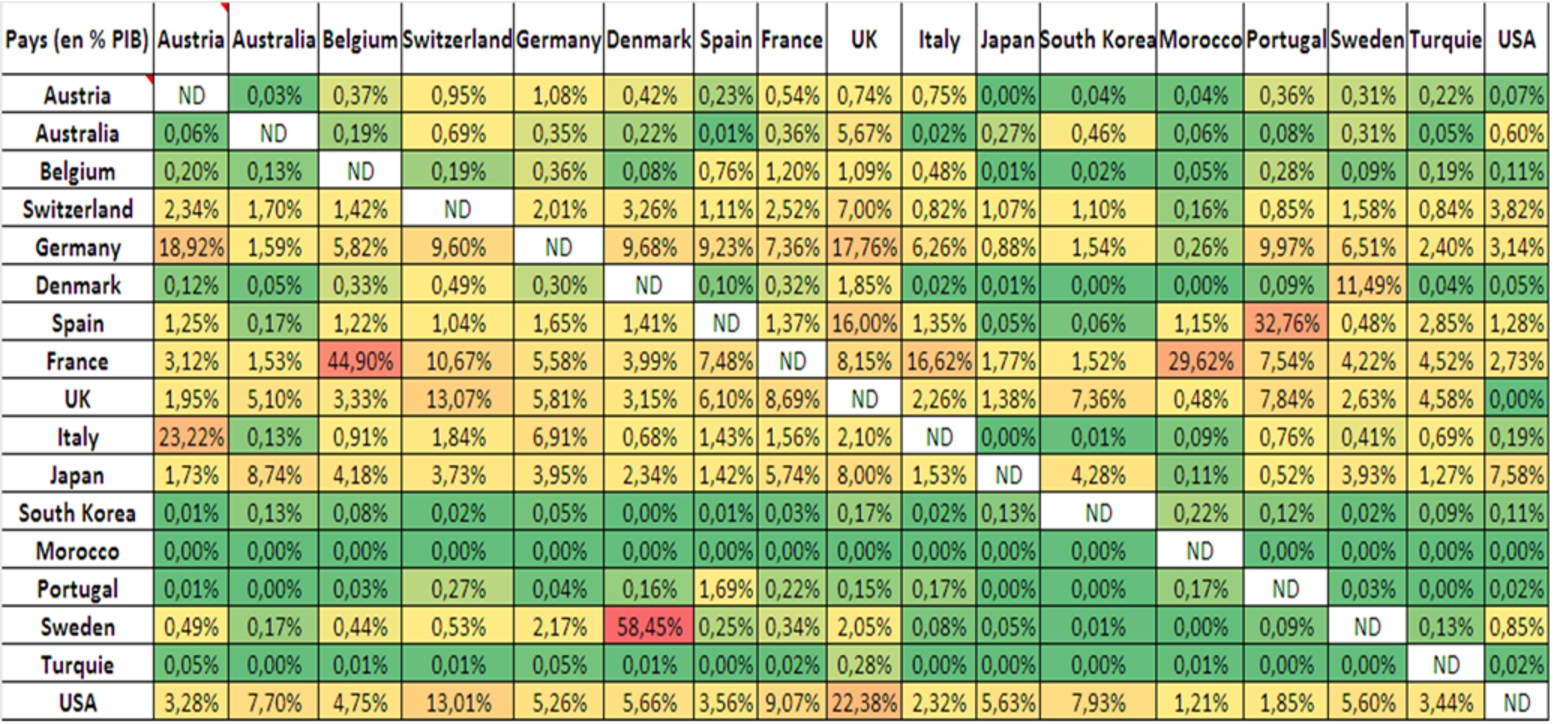

Matrix of Exposition in % of GDP

Centralization by eigenvectors. This measure gives an indication of the components that increase the spread of a shock if one takes into account the ripple effects that may occur as a result of this disruption. Mathematically, the centrality of the eigenvectors is defined as the principal eigenvector of the adjacent matrix that represents the network, indicating whether or not there is a strong link between the two elements. The equation defining a proper vector is as follows:

These three indicators are commonly used in network analysis to capture the centrality and importance of each component in the network studied. In this sense, and based on BIS data (CBS), the matrix of bilateral exposures between foreign banking systems and Morocco has been developed for the first quarter of 2013. This matrix allows to visualize the interrelations between different countries (creditors) in connection with Morocco (see Table 2).

The review of the exposition Morocco matrix as to sources of external financing from foreign banking systems indicates that the level of foreign vis-à-vis commitments Morocco is quite low in value, however, the sum of exposures percentage of GDP appears to be important in particular to the French banking system. On the basis of these two matrices, the centralities of indicators have been calculated.

The degree of centrality calculated on the basis of the network determined through fair matrices indicates that Morocco to a low centrality. Indeed, the incoming flow measuring degrees from other components and measuring degrees outgoing flows remain moderate and classify Morocco in a very satisfactory situation.

Centrality degree.

As regards the intermediate centrality, Morocco is not exposed in an indirect manner to the other system components. However, according to the matrix of bilateral exposures, Morocco is attached to the French banking system as the ultimate lender (common lender).

Intermediary centrality.

As regards the intermediate centrality, Morocco is not exposed to in an indirect Manner Reviews the other system components. HOWEVER, selon the matrix of bilateral exposures, Morocco is attached to the French banking system as the ultimate lender (common lender).

Eigenvectors centrality.

Thus, Morocco is exposed in terms of its commitments at international level to major global banking systems. However, the French banking system is the main lender of Morocco leaving a live exhibition entitled vis-à-vis France.

Trade Network (by value) of the banking systems in the light of Morocco T1-2013.

On the same lines, network analysis indicates that banking systems in connection with Morocco and France are highly interconnected what appears to be an indirect risk for Morocco.

Trade Network (% of GDP) in bank systems taking account of Morocco T1-2013.

Although the value of Morocco’s exhibition are quite low compared to all the other components of the network, it should be noted that in terms of nominal GDP exposure appears to be similar to that of other countries. Thus, the risk of cross-border contagion in the case of Morocco is reflected through the effect of “Common Lender” (the French banking system) and also by the strong interconnection of this vis-à-vis the foreign system.

Compared with the financial position of the Moroccan banking system assets and currency liabilities are currently available in an aggregated manner. The analysis of these exposures to the outside globally indicates that the risk level remains quite mastered. Indeed, changes in foreign currency assets of banks increased between 2005 and 2008. On the other hand, and from the end of 2008 they were down to only represent 2% of total assets. In another development, commitments vis-à-vis currencies outside recorded a downward trend since 2001, with a recovery to rise from 2010 to represent almost 2% of total assets.

(a) Foreign reserve and engagement with devise of Morocco. (b) Assets and engagement with devise of Morocco and HHI index of concentration.

The review of the exposure of each vis-à-vis bank abroad through assets and foreign currency liabilities can make an important conclusion. Only one bank monopolizes the majority of currency transactions and remains the most exposed to the risk of cross-border contagion. Despite the small size of these exposures relative to the total balance sheet, the degree of concentration deserves special attention (see Fig. 9(b)).

Identification of intersections and cross-border contagion network positions the banking system with its counterparts to international levels. The construction of internationally matrix of bilateral exposures to measure the systemic risk of contagion incurred by the Moroccan banking system.

In the simulation model of cross-border contagion it was inspired by the work of Espenoza-Vega et al., 2010.

Contagion model

Like the work on the risk of contagion is developed on the basis of the matrix of exposures generated in the previous section, a contagion model for Moroccan interbank market. Although most of the empirical work on the issue has brought only default risk by quantifying the impact of the advent of a default in the global interbank market, this work integrates two types of risk namely counterparty risk and refinancing liquidity risk.

First, we analyze the default risk on the international interbank market. Thus, the bank liabilities defaults cause cascading waterfalls when the core capital can fill the losses. Secondly, we associate the first risk, refinancing, liquidity risk when it is assumed that the bank, in addition to defects engaged in the interbank market, is forced to liquidate assets while accepting losses of market values “next to”. The liquidation of assets is in response to liquidity needs and the lack of other sources5 financing (due to defects in the interbank market). It should be noted that as part of this work the defect is the inability to honor commitments in the interbank market and can be interpreted as a liquidation or dissolution.

To describe the impact of these two risks (the algorithm) consider the main components of the simplified balance sheet of a bank ‘i’ (see Table 3).

Balance sheet of Bank

Balance sheet of Bank

We can write equality between liabilities and assets in the following form:

Thus, in case of default of an “h” bank on the interbank market, interbank receivables show a decrease of the amount of the recorded loss, the burden will be borne by the bank’s own funds. We denote “a” fraction lost after the advent of bank default, which results in a new formulation of the relation (4):

Credit shock in balance sheet

The losses and recorded in interbank claims need to be filled largely by the bank’s own funds. In case of their failure, it is clear that it will face solvency problems that could cause its failure. Therefore, it will not be able to honor its commitments to various other credit institutions which could generate a domino effect on the interbank market.

Besides default risk was considered an additional refinancing liquidity risk on falling prices of the assets held by the bank. We study, in fact, the situation where the bank “i” is forced to replace a fraction “b” of funds that were provided by the defaulting banks to meet its obligations through the sale of certain liquid securities. In a context of tightening liquidity, this decision will result, by hypothesis, a fall in asset prices since it is a sale in distress. In this situation one can imagine a “d” discount on the price of assets to be liquidated.6

After consideration of the refinancing risk the simplified balance sheet of the bank i become (see Table 5).

Credit and liquidity shock in balance sheet

The accounting equivalence takes the form:

To include the refinancing liquidity risk algorithm tests whether the core capital are less than the sum of uncollectible amounts and the discount on the portion of underlying assets.7

The rule used by the algorithm is as follows:

Thus, the iterations start with the fall of the first bank that can cause a failure process within the banking system. The contagion circuit is presented in Fig. 10.

Processus of cross border contagion.

In this section we analyze the effects of contagion across borders. The analysis is conducted on a network integrating the Moroccan banking system.

Banking system in default after simulation.

Figure 11 shows that France is more systemic in the cross-border network of Morocco. Thus, the fall of France induced failure to 5 countries. Furthermore, Spain and Sweden lead to the failure of two countries trimmed simulations.

In terms of losses of the banking system of cross-border network of Morocco, the simulation results indicate that the most extreme loss at the French and American banking systems, loss of Morocco remains low as the level of capital held by Moroccan banking system represents only a small fraction compared to the capitalization of other countries.

Capital loss after simulation (%).

Regarding the lack of ranking which measures the systemic importance of countries in the network containing Morocco. Thus, the banking systems which are defaults to the first occurrence of shocks are Spain, Italy and Sweden which means that the system is very sensitive to defects of other systems. By cons, France, she falls in default after the second rank of default. This can be explained by the importance of capital of the French banking system.

Number of default.

We also extracted the contagion path following the collapse of every banking system in the Moroccan network. This path says the results we obtained earlier. Thus, the risk to the Morocco is largely derived vis-à-vis exhibitions of France and this is well established in the path of contagion in Fig. 14 (in blue boxes).

Cross Border contagion: when the Moroccan banking systems fail?

The findings from these simulation exercises should be interpreted taking into account certain limits presented the methodology and data used. The estimation methodology adopted bilateral exposures. Another limitation given the difficulty of reproducing the real links between the banking systems which often are limited in their transactions some banks of the system.

Furthermore, the approach is purely static to the extent possible interventions and changes in behavior of agents (bank runs or capital increase of banks affected by a failure) and possible interventions of public authorities (the role of the bank Central as a lender of last resort) are not taken into account. Similarly, in the case of a financial crisis in the banking sector in general, it is possible that more banks find themselves in financial difficulties at the same time. While simulation exercise assumes, only, the failure of one bank alone.

Despite these limitations, the design of a realistic model of contagion remains a very complex task if not impossible, because of the complexity of interbank relations, the unavailability of data and the difficulty of identifying the different interbank contagion channels. However, in light of international experience, central banks outside the obligation to conduct macro prudential policy choose simple steps to assess the risk of contagion.

Improving the assessment of risk of contagion conducted in this work first requires the use of the matrix of bilateral exposures actual net that reflects the real risk exposures and could integrate in a second step the particularities of certain banks including those with foreign ownership or partially owned by the state. Then, to give the shock propagation process an economic base, a reflection on the interconnection of contagion model with macroeconomic variables or systemic risk models should be conducted to strengthen our macro prudential device.

Footnotes

The consolidation means that engagement by country of a declaring institution includes/understands also that of all the institutions which are connected to him, whatever their home country, including the debtor country.

Base of the direct borrower: The amounts receivable are allotted to the home country of the immediate counterpart on the other hand on the basis of ultimate risk: The amounts receivable are assigned to the country where the final risk.

On the basis of direct borrower, the foreign amounts receivable gather the international amounts receivable and the local amounts receivable in local currency. As regards the international amounts receivable, they comprise on the one hand the transborder amounts receivable and the local amounts receivable in currencies on the other hand. The transborder amounts receivable include those entered by the agencies in a country declaring, but whose seat is out the area declaring thus that those on borrowers residing in the country of origin of the declaring bank, entered by the agencies located in a country of the area. Concerning the local amounts receivable in currencies, they are amounts receivable held by the subsidiaries and foreign branches on the residents made out in a currency other than that of the country of establishment. On the other hand, the amounts receivable in local currency are amounts receivable held by the subsidiaries and foreign branches on the residents made out in local currency.

Engagements by signature indicate the share not used of the irrevocable contractual obligations which, if they are mobilized, result by the granting of a loan or the purchase of a bond.

We considere the bank don’t have the possibility to rise a capital.

With B and D variable is between 0 and 1.

For more detail methodology to see it work of: Márquez and Martinez, 2008, Espinosa-Vega et al., 2010, Upper et al., 2011 and RSF of the Bank of Luxemburg, 2014.