A recent application in machine learning has introduced a novel approach, complemented by big data sources, aimed at providing precise estimates for small geographical areas. This method employs a dual strategy: (a) hybrid estimation, involving the integration of big data sources with imputed values derived from nearest neighbours (KNN) to address missing target variable values from the big data source; and (b) calibration of the collective sum of small area estimates to an independent yet efficient national total. Evaluating its efficacy using simulated data from the 2016 Australian population census, the calibrated KNN (CKNN) method demonstrated superior performance compared to the Fay-Herriot method based on area-level covariates.

This paper enhances the comparative analysis by contrasting the CKNN method with a hierarchical Bayes method using the logit-normal model (LN) relevant for binary data. Broadly speaking, the LN method can be viewed as the Bayesian equivalent of Battese-Harter-Fuller (BHF) method, which incorporates unit-level covariates. Our results demonstrate the CKNN method’s superiority over the LN method. However, the application of hybrid estimation to the LN method significantly diminishes this superiority. Although CKNN estimates maintain better precision, they are not as accurate as the estimates from the hybridized LN method.

The estimation of variables in small geographic areas, known as small area estimation (SAE), is recognized as a crucial yet inadequately addressed requirement by national statistical offices (NSOs) and is particularly pertinent to the needs of statistical users. While “small areas” typically refers to sub-national or local geographical regions, it is important to note that the same principles and methodologies for national estimates are equally applicable to the estimation for small population groups.

The unmet demand for SAE arises due to the inherent limitations of direct estimates for small areas, primarily stemming from the challenges associated with small, or non-existent sample sizes, leading to substantial sampling errors. To overcome this hurdle, NSOs employ a “model-based approach,” utilizing statistical models to leverage information and enhance estimation accuracy across areas [1, 2], over time [3], or resort to synthetic estimation techniques [4]. The Fay and Herriot (FH) and Battese, Harper and Fuller (BHF) models, which use area-level and unit-level covariates respectively, are commonly used by NSOs and are considered to be the industry-standards for SAE.

For a comprehensive understanding of the various methodologies employed in small area estimation, one may refer to the extensive literature, including [5, 6, 7, 8, 9, 10, 11, 12, 13, 14].

The FH model enhances the precision of SAE by “borrowing” strength across areas, employing what is known as “linking” models – refer to, for instance, equation 4.2.1 of [14]. This improvement is achieved by assuming shared regression coefficients in the linking model for area totals. By amalgamating the sampling error model (equation 4.2.3 of [14]) with the linking model, a mixed linear model (equation 4.2.5 of [14]) for the survey estimates (which are appropriately weighted) of the areas is derived. Subsequently, model parameters are estimated through this combined framework. Empirical Best Linear Unbiased Predictors (EBLUPs) for the small areas are then computed by plugging the estimated parameters into the mixed linear model, along with the area-level covariates.

The BHF builds upon the aforementioned concept by employing a mixed linear model, focusing not on the survey estimates of the areas, but on the survey units directly. An essential condition for implementing the BHF model is the presence of unit-level covariates, not only for the observed units in the survey sample but for the entire population. Through simulation studies [15, 16], it has been demonstrated that SAEs derived from BHF models surpass FH estimates in terms of precision and are less susceptible to bias. This superiority arises from the more granular information available in unit-level covariates, providing more informative estimation compared to the FH models operating at the area level.

In this paper, we employ the LN model instead of the BHF model for comparison. The LN model can be considered as the Bayesian equivalent to the BHF model as it also uses unit covariates for prediction, offering a compatible framework for our analysis. The principal reason for choosing the LN model instead of the BHF model is that, using Monte Carlo Markov Chain (MCMC) for computations, the LN model facilitates more efficient number-crunching compared to the BHF model.

The subsequent Sections of this paper are organized as follows. Section 2 provides an overview of the calibrated KNN (CKNN) methodology, elucidating its application in generating small area estimates and the associated computation of mean squared errors (MSE). Moving forward, Section 3 summarises the outcomes of a comparative analysis between CKNN estimates and those derived from the FH method. Section 4 reports the findings of a parallel assessment, contrasting CKNN estimates against both LN estimates and hybridized LN estimates. Our concluding remarks are presented in Section 5.

Harnessing big data for SAE

As big data gains prominence [17, 18], the question arises: Can we unlock its potential for SAE? The response is in the affirmative, as demonstrated in [19]. Addressing the well-recognized under-coverage bias associated with relying solely on big data for SAE, [19] mitigates this limitation by mass imputing the missing data using survey data as donors and counters the constraints posed by the small sample size in SAE by complementing the imputed data with big data. This symbiotic relationship between the two data sources underscores their complementarity in achieving robust SAE outcomes.

In what follows, we provide a bird’s eye view of the methodology used in [19] for SAE with big data.

Notation and the underlying idea

Suppose we have a finite population, , comprising units with the following values, and , , where is a vector of auxiliary variables and is fully observed, and is the variable of interest. We assume that , where , of size , comprises the labels of the big data set and , of size , is the complement of . We assume further that , are observed without error. Finally, we also assume that we have a probability sample, , with known design weights of the sample, , Thus we have the following data available to the analyst for SAE: (a) ) for ; (b) for ; (c) and (d) information on where these units are located in the small area. Finally, let denote the big data inclusion indicator which is 1 if unit and 0 otherwise. We assume that (e) , , is fully observed. Note that is observed for In addition, note that the case when is subject to nonresponse and not fully observed was addressed in [20] and [21] respectively and will not be repeated here.

Suppose further that and and where and denotes the small area. For SAE, we are interested to estimate . As and because and are fully observed, the SAE problem boils down to estimating , using the information available from (a) to (e) above. Let and denote the estimate of and respectively. Then

Denote the population total by . [21] showed that the data integrator, perhaps better referred to as a hybrid estimator, is equivalent to a generalised regression estimator and hence is approximately designed unbiased They also showed that when is sufficiently large, is a more efficient estimator than , where and denote the size of the Big Data, population and sample respectively. As is an efficient estimator of the population total, [19] uses it to calibrate the imputes for the missing values in using a KNN algorithm with the donors coming from . In other words, and the methodology is called the CKNN algorithm.

The KNN algorithm

For a description of the KNN algorithm, refer to [19] and the references therein. To ascertain the optimum number of nearest neighbours, the number, , and selection of the covariates in to be used in finding the nearest neighbours, the following two steps are applied [19]: (a) a grid search on all possible combinations of and all combinations of the covariates from ; and (b) a 5-fold cross validation methodology. The objective is to identify the combination of , and the specific covariates that minimises the aggregated sum of absolute prediction errors across all the small areas from .

Furthermore, [19] utilizes the HasD distance metric [19, 22] to find the nearest neighbours in , i.e. extending beyond the boundaries of the specific area to encompass the entire donor pool. This approach ensures a thorough exploration of potential matches, transcending the limitations of a localized focus. Conceptually, by sharing the donors across all areas in , this mirrors the assumption of shared regression coefficients used in the FH and BHF models. Finally, the HasD metric, which can handle continuous and multinomial data, is bounded between 0 and and offers the important characteristic of being scale invariant.

The CKNN algorithm

Let the subscript denote the unobserved unit in and , be the nearest neighbour of , where Denoting by , an estimate for the population total in area from the donors is given by . In KNN, . In CKNN, we define where is chosen to minimise subject to the following conditions: (a) ; and (b) . The Chi-square minimisation criteria follows those of [23] and ensures that each , , , , is as close as possible to whilst condition (b) ensures that entire sum of the estimates across all the areas is calibrated to the independent estimate of the overall population total, . To simply notation, we shall henceforth use to denote , and refer as a CKNN estimate or a hybrid estimate signalling its combination of big data and survey data. The are also referred to as calibration weights.

For an analytic solution for the calibration weights, the reader is referred to the Lemma in [19].

Estimating the MSE of

The MSE of can be decomposed into variance and a squared bias components as follows:

where . The error, , is due to the use of nearest neighbours to impute the missing values in and is the imputation bias. Hence, is the relative imputation bias.

The variance component, , does not have a closed form, but can be estimated using the “fixed – K asymptotic bootstrap” of [19, 24]. How many bootstrap samples are required? According to [19, 24], to have the coefficient of variation of the “width” of the bootstrap confidence interval of about 7%, the number is 500.

To estimate the relative imputation error, the following steps are used [19]: (a) sequentially, each observed data point in undergoes imputation using the CKNN algorithm as outlined in Section 2.3. This entails (a1) using HasD to find the nearest neighbours for each simulated missing data point in ; (a2) applying calibration weights to the nearest neighbours for each simulated missing data point to calculate the imputed value; (b) the imputation error is calculated by summing the difference between the imputed value and the actual value of the data points in ; (c) is calculated from dividing the imputation error derived in step (b) by the sum of the imputed values in Finally, is estimated by

Performance of the CKNN algorithm

To illustrate the methods, [19] used the 1% public use micro data file from the 2016 Australian Census (Australian Bureau of Statistics, 2016) (available at https://www.abs.gov.au/statistics/microdata-tablebuilder/log-your-accounts to authorised users) to simulate the population, big data, and the probability sample. The variable of interest for SAE is the number of volunteers for 56 small areas as defined geographically by the Australian Bureau of Statistics.

The population, has 173,021 personal records. With 56 areas, there is an average of 3,089 personal records per area. Among the 173, 021 personal records, there was a total of 35,742 volunteers, giving an overall average volunteer participation rate of about 21%. The number of volunteers ranged between 46 to 1,236 amongst the 56 small areas, and the volunteer participation rate varies between 11% to 31%.

From , a simple random sample of 1,730 (i.e. 1% of ) of the personal records and a missing-not-at-random big data sample of 103,438 personal records (i.e. 60% of ) and 18,548 volunteers (52% of all volunteers) were created. For further details on how these samples were created, refer to [19].

Covariates available at the unit record level for computation of the HaD metric are: labour force status (employed, unemployed and not in the labour force), birth region (6 groups), age (7 broad groups) and sex (male, female).

Using the methods outlined in Section 2.2, [19] found that the optimum combination of the covariates is comprising the labour force status, birth region and age variables.

In addition, was 36,312 as compared with the actual number of 35,742 volunteers.

Estimates for , , , , and

Area

1

910

811

104

832

182

828

120

2

426

401

55

493

136

444

82

3

728

641

83

632

151

788

127

4

1014

879

111

879

201

949

143

5

839

676*

78

626

161

694

111

6

383

404

59

320

103

350

72

7

529

468

62

524

130

521

91

8

730

741

88

700

160

773

113

9

447

387

55

411

122

352

78

10

433

364

43

350

101

398

74

11

544

630

93

506

161

519

111

12

751

733

87

773

207

730

124

13

1236

1119

122

1083

232

1197

148

14

650

636

87

684

179

665

117

15

350

400

62

423

123

359

80

16

499

521

64

552

143

495

80

17

312

392

58

449

128

371

81

18

768

701

88

904

181

842

108

19

507

436

52

535

122

475

74

20

857

714

91

1041

202

834

121

21

1026

990

119

925

207

1005

139

22

732

698

73

653

152

790

117

23

706

708

86

854

203

806

140

24

584

646

91

723

170

561

105

25

412

462

62

644

158

548

98

26

800

813

101

708

176

779

125

27

896

968

121

1142

218

980

148

28

794

859

110

777

184

906

146

29

391

438

56

287

97

372

74

30

607

596

76

526

128

602

101

31

632

698

90

615

144

664

107

32

543

561

65

435

120

635

114

33

920

861

95

670

165

806

112

34

445

457

65

340

102

408

86

35

670

641

84

493

128

676

107

36

685

798

110

708

172

677

117

37

741

739

94

770

174

741

115

38

387

406

56

383

116

379

81

39

515

563

78

571

148

586

110

40

611

692

87

634

161

692

112

41

589

639

37

460

120

609

48

42

459

504

32

358

103

452

36

43

898

970

54

766

176

929

62

44

570

657*

43

499

134

631

59

45

633

690

41

630

160

645

52

46

847

904

46

705

166

820

49

47

702

770

46

757

168

756

64

48

681

740

44

639

166

708

57

49

763

844

48

720

169

798

56

50

716

774

44

735

185

758

66

51

548

637*

40

522

130

607

44

52

359

390

23

195

67

368

33

53

853

948

59

736

179

888

66

54

289

324

22

250

78

305

30

55

779

818

43

572

148

792

59

56

46

55*

4

44*

16

50

6

Total

35,742

36,312

34,158

36316

Average absolute estimation error

57

89

42

Average relative root mean squared error

11%

26%

15%

Estimated coverage rate

93%

98%

100%

Notes: (1) * denotes is not within , or not within i.e 95% Credible interval, where denotes the actual size of the small area , the superscriptsHY, LN1 and LN2 represent hybrid, logit-normal and hybridized logit-normal estimates respectively, and RTMSE and SD represent root mean squared error and standard deviation respectively. (2) Estimated coverage rate (# of true counts within the 95% confidence interval) divided by 56. The coverage rate of 98% and 100% are not statistically significantly different (95% confidence) from the nominal coverage rate of 95%.

The actual and CKNN estimates, denoted by their root MSEs, denoted by , for the 56 areas are tabulated in Table 1, where the superscript HY denotes hybrid estimates The CKNN estimates have an average absolute estimation error of 57, average relative root MSE of 11% and an estimated coverage rate of 93% against a nominal coverage rate of 95%.

To assess the performance of hybrid (CKNN) estimates in comparison to FH estimates across the 56 areas, both estimates, accompanied by their respective error bars, are depicted against the actual number of volunteers in Fig. 1. In this representation, the black dots denote the hybrid or FH estimates, and the vertical lines denote the 95% confidence interval. The proximity of the black dots to the red line indicates the accuracy of the estimates relative to the true values. Additionally, shorter vertical lines signify greater precision in the estimates.

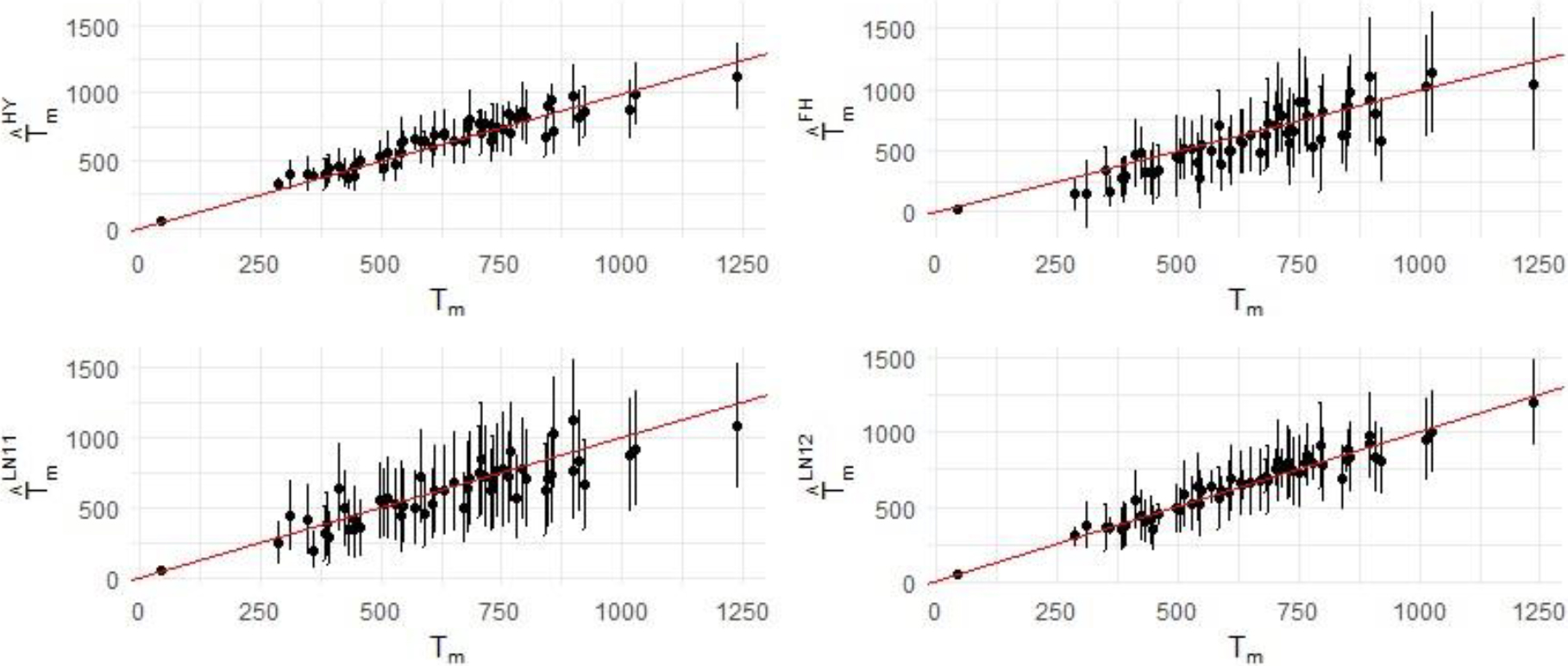

Plot of and their 95% error bars against . Notes: (1) Data are sourced from Table 1 (left plot) and [19] (right plot). Error band is defined as where or FH. (2) denotes the actual size of the small area , the superscriptHY represent hybrid estimate.

As observed in Fig. 1, [19] concluded from this analysis that CKNN estimates outperform FH estimates. Specifically, the CKNN estimates exhibit better accuracy (closeness to the red line) and reduced uncertainty (shorter vertical lines) compared to their FH counterparts.

Levelling the playing field

The juxtaposition of CKNN estimates with FH estimates, as illustrated in Fig. 1, presents an inequitable comparison for two key reasons. Firstly, CKNN estimates are derived from unit-level covariates, while FH estimates are based on area-level covariates. This inherent difference in the granularity of covariate information disadvantages the FH estimates in the performance comparison.

Secondly, the CKNN estimates employ a hybrid approach by integrating big data, survey data and predicted missing data (due to the under-coverage of big data) to generate SAEs. In contrast, whilst they can be hybridized as shown by the hybridized LN estimates below, FH estimates do not currently adopt a hybrid estimation strategy, relying solely on the survey data without taking advantage of the information available from big data.

Given that, at the unit level, volunteer status is a binary variable, the application of the BHF model, designed for continuous variables, is not suitable. In their book, [14] delineate an Empirical Best Linear Unbiased Prediction (EBLUP) approach (Section 9.5.2) and a Hierarchical Bayes (HB) approach (Section 10.13.2) specifically tailored for binary variables. The EBLUP approach is also extensively discussed in [26]. However, for the purposes of this paper, we opted for the LN model under the HB approach, because it can be considered the Bayesian equivalent of the BHF model, it is applicable for binary response variables and software exists to facilitate with number crunching for HB models.

From a computational standpoint, the preference for the Hierarchical Bayes (HB) approach is substantiated by the availability of version 0.7.7 the R package, mcmcsae in the Comprehensive R Archive Network. Developed by Dr. HJ Boonstra of the Central Bureau of Statistics in the Netherlands. This package provides pre-built MCMC methods. These methods facilitate the generation of samples from the posterior distribution of SAE estimates, accommodating both continuous and binary target variables. With mcmcsae, users can efficiently compute posterior mean (and quantile) estimates along with their credible intervals, thus simplifying one’s computational burden.

For the 1% 2016 Census data, we use the LN model (equation 10.11.7 of [14]) for the volunteer data as follows:

Bernoulli (

Logit ( with

and are mutually independent with and where denotes the Gamma distribution with parameters and .

Utilising mcmcsae, Gibbs sampling was applied to the posterior distribution of to generate 2,000 non-burned-in MCMC samples of with the Gelman-Rubin’s R_hat of each of lying between 0.9999 and 1.0017 demonstrating convergence. These are then plugged into (ii) to compute 2,000 estimates of, from which the posterior mean and credible intervals of are computed. For further details, refer to [14].

Using the LN model, we generated two sets of LN estimates for the small areas, denoted as and respectively, along with their credible intervals by and respectively. The is compiled without incorporating the big data in the estimation process, while employs a hybrid estimation approach akin to the method employed in CKNN estimates with the exception that calibration to the independent national total which is based on pro-rata, as the LN estimates is only 0.2% higher than the independent national benchmark total. These estimates were tabulated in the last four columns in Table 1, and visually represented in Fig. 2. The diagram on the left of the lower panel in Fig. 2 plots the LN1 data, and the diagram on the right plots the LN2 data.

Plot of , and their 95% error bars against . a. Notes: (1) Data are sourced from Table 1 (upper left, lower left and left right plots) and [19] (upper right). Error band is defined as where denotes root MSE (upper panel) and credible interval (lower panel). (2) denotes the actual size of the small area , the superscripts HY, FH, LN1 and LN2 represent hybrid, Fay-Herriot,logit-normal and hybridized logit-normal estimates respectively.

Without calibration, the national sum of the small area estimates from both LN estimates are further away (i.e. less accurate) from the actual number of volunteers of 35,742 than that of the CKNN estimates.

The average absolute estimation error of CKNN estimates is smaller (i.e. more accurate) than the LN1 estimates, but higher (i.e. less accurate) than the LN2 estimates, suggesting the LN2 estimates are slightly more on target than CKNN estimates – an error of 42 for the LN2 estimates as compared with 57 for the CKNN estimates.

The average relative root mean square error of the CKNN estimates is the smallest (i.e. the most accurate) and is 11% compared with 15% for LN2 estimates.

The coverage rate of LN1 and LN2 estimates are numerically (but not statistically) higher than the CKNN estimates.

From Fig. 2, the following observations can be made:

The CKNN (i.e. the hybrid estimates) plot (diagram on the left on the top panel) is better than the LN1 plot (diagram on left of the bottom panel), both in terms of numerical accuracy of the prediction, and reduction in uncertainty.

The CKNN plot is worse than the LN2 plot (diagram on right of the bottom panel) in terms of numerical accuracy but better in terms of reduction in uncertainty.

The performance of LN1 estimates is comparable with that of the FH estimates. At first glance, this contrasts with findings in the literature [15, 16]. However, those studies assume the linking model – specifically, assumption (ii) of the LN model – perfectly explains the target variable. The 2016 Census data, however, does not substantiate this assumption.

Comparing the LN1 with the LN2 plots, it is evident that hybrid estimation is superior to no hybrid estimation.

Conclusion

The key results outlined in this paper underscore the superiority of CKNN estimates over LN and FH estimates, albeit with a notable reduction in this superiority when juxtaposed with hybridised LN estimation. Regardless of what methods one may choose for SAE, this result underpins the importance of adopting hybrid estimation.

It should be noted that the methods outlined in this paper require certain assumptions to be fulfilled [19]. They are:

The target variables, which are also collected in the survey, are observed throughout the big data set without measurement errors – this condition is more likely to be satisfied when using administrative data for hybrid estimation than using many other types of big data. Where this condition is not satisfied, can be used as a training data set to construct a measurement error model to adjust the target variables in big data [28];

there are no over-coverage errors in the big data. Where this is not the case, can be used to estimate over-coverage rates in the small areas to remove the bias from ;

the donor set, which depends on the size of and has to be sufficiently large, to support the imputations;

is fully observed for the units in the survey data set, – this can generally be made possible by matching the units between and through direct matching or probability matching [29]. When is not observed, or observed with error, one may use a semi-supervised classification technique to compute an EM estimator for [21]; and

associated with each unit of the population, there is a set of covariates which are available and known to the statistician. The assumption presumes the existence of a database with covariates covering the whole of the population.

The drawback of nearest neighbour methods arises when the dimensionality, i.e. becomes too large [27, p. 22]. In such cases, the methods are susceptible to the curse of dimensionality, wherein the donors are positioned so far apart that they no longer genuinely qualify as nearest neighbours. In our numerical example, with 3, the CKNN estimates of the total number of volunteers in small areas are not affected by this phenomenon.

An attraction of the CKNN method is in the variable-agnostic nature of the KNN algorithm. Put differently, this singular algorithm, configured only once, can be seamlessly applied to a spectrum of target variables. In contrast to the LN method, there is no necessity to construct variable-specific linking models for each target variable. This attribute allows the NSO to swiftly generate SAEs across a wide array of target variables. Additionally, in scenarios where unit record files are generated by the NSO for subsequent secondary analysis by researchers, the imputed data over this diverse array of target variables exhibit internal consistency across them without the need for further statistical processing.

Footnotes

Acknowledgments

We would like to thank Dr HJ Boonstra for his helpful advice on using mcmcsae to run the logit-normal model, and the two referees for their helpful comments on an earlier version of this paper.

Disclaimer

Views expressed in this paper are those of the author and do not necessarily represent those of the Australian Bureau of Statistics.

References

1.

FayRHerriotR. Estimates of Income for Small Places – An Application of James-Stein Procedures to Census data. Journal of the American Statistical Association. 1979; 74: 269-277.

2.

BatteseGEHarterRMFullerWA. An Error Component Model for Prediction of County Crop Areas Using Survey and Satellite Data. Journal of the American Statistical Association. 1988; 83: 28-36.

3.

PfeffermannD. TillerR. Small area estimation with state-space models subject to benchmark constraints. Journal of the American Statistical Association. 2006; 101: 1387-1397.

4.

LehtoneRVeijanenA. Design-based methods of estimation for domains and small areas. In PfeffermannDRaoCR. editors. Sample Surveys: Inference and Analysis Handbook of Statistics. Amsterdam: North-Holland; 2009; pp. 219–249.

5.

DattaGS. Model-based approach to small area estimation. In PfeffermannDRaoCR. editors. Sample Surveys: Inference and Analysis. Handbook of Statistics. Amsterdam: North-Holland. 2009; pp. 251-288.

6.

GhoshMRaoJNK. Small area estimation: An appraisal. Statistical Science. 1994; 9: 55-93.

7.

GhoshM. Small area estimation: its evolution in five decades. Statistics in Transition New Series; 21: 1-22.

8.

JiangJLahiriP. Estimation of finite population domain means – A model-assisted empirical best prediction approach. Journal of the American Statistical Association.2006; 101: 301-311.

9.

JiangJLahiri,P. Mixed model prediction and small area estimation. Test.2006; 15: 1-96.

10.

PfeffermannD. Small area estimation – New developments and directions. International Statistical Review. 2002; 70: 125-143.

11.

PfeffermannD. New important developments in small area estimation. Statistical Science2013; 28: 40-68.

12.

RaoJNK. Inferential issues in small area estimation: Some new developments. Statistics in Transition. 2005; 7: 513-526.

13.

RaoJNK. Some methods for small area estimation. Revista Internazionale di Siencze Sociali. 2008; 4: 387-406.

14.

RaoJNKMolinaI. Small Area Estimation. New York: John Wiley & Sons; 2015.

15.

FayR. Further comparison of unit – and area – level small area estimators. Proceeding of the Survey Research Methods Section. 2018; 2057-2070.

16.

HidiroglouMAYouY. Comparison of Unit Level and Area Level Small Area Estimators. Survey Methodology. 2016; 42: 41-61.

17.

DaasPJHPutsMJvan den HurkPAM. Big data as a source for official statistics. Journal of Official Statistics2015; 31: 249-262.

18.

TamSMClarkeF. Big data, official statistics and some initiative by the Australian Bureau of Statistics. International Statistical Review. 2015; 83: 436-448.

19.

TamSMSharmeenS. A Calibrated Data-Driven Approach for Small Area Estimation using Big Data. Australian and New Zealand Journal of Statistics.2024; 66: 125-145.

20.

TamSMKimJKAngLPhamH. Mining the new oil for official statistics. In HillCBiemerPPBuskirkTJapecLKitchnerAKolenikovSLybergL, editors. Big Data Meets Survey Science: A Collection of Innovation Methods. New York: John Wiley and Sons; 2020.

21.

KimJKTamSM. Data integration by combining big data and survey sample data for finite population inference. International Statistical Review. 2021; 89: 382-401.

22.

HassanatAB. Dimensionality Invariant Similarity Measure. Journal of American Science. 2014; 10: 221-226.

23.

DevilleJCSärndalCE. Calibration estimators in survey sampling. Journal of the American Statistical Association. 1992; 87: 376-382.

24.

OtsuTRaiY. Bootstrap inference of matching estimators for average treatment effects. Journal of the American Statistical Association. 2017; 112: 1720-1732.

25.

EfronB. Better boostrap confidence intervals. Journal of the American Statistical Association. 1987; 82: 171-185.

26.

HobzaTMoraleD. Empirical best prediction under unit-level logit mixed models. Journal of Official Statistics. 2016; 32: 661.

27.

HastieTTibshiraniRFriedmanJ. The Elements of Statistical Learning: Data Mining, Inference and Prediction. New York: Springer; 2008.

28.

MediousEGogaCRuiz-GazenCBeaumontJFDessertaineA. PuechP. QR prediction for statistical data integration; 2023; [cited 2024 Aug 8]. Available from: https//www.tse-fr.eu/publications/qr-prediction-statistical-data-integration.

29.

FellegiISunterAB. A theory for record linkage. Journal of the American Statistical Association1969; 40: 1183-1210.