Abstract

Abstract

The International Space Station (ISS) is heralded as a political and engineering success that provides a firm foothold for the National Aeronautics and Space Administration (NASA) and its international partners to send crews to visit and operate in low-Earth orbit (LEO). For current NASA leadership, the future of LEO rests in the hands of U.S. private industry in which NASA is a buyer of services, including human spaceflight services, which are owned and operated by private companies. The NASA human spaceflight strategy is to send crew missions to cislunar space and to transition ISS capabilities over to commercial habitats and platforms in LEO by the 2020s. This article argues that it is unlikely that market forces and industry capabilities will be strong enough by the mid-2020s to support commercial habitats without direct NASA support. Therefore, NASA should study the costs and timelines of extending the ISS past the mid-2020s versus procuring short-duration commercial platforms. If cislunar habitats are the goal, then short-duration commercial solutions in LEO could serve as test beds for future deep space habitat concepts.

Introduction and Background

National Aeronautics and Space Administration (NASA) often refers to the International Space Station (ISS) as a “staging ground” for the development and testing of capabilities that will one day be used on human spaceflight missions out to cislunar space and eventually to Mars. For these reasons, NASA is urging its international partners to extend the current international agreements that govern ISS operations from their current expiration date in 2020 to 2024. During these discussions for an extension of the ISS, NASA and its partners are faced with questions on what comes next after the ISS. Such questions are a reminder to NASA and other space agencies around the world of just how much time, effort, and cost went into completing the ISS and the cost that goes into maintaining the station today. As the 2020s approach, many governments may not have the fiscal resources or strategic goals to embark on another large station development project in low-Earth orbit (LEO) to replace the ISS.

NASA Vision for LEO

For NASA leadership, the conversation centers on the theme that LEO is an emerging market in which NASA is to be a buyer of services, including human spaceflight services, which are owned and operated by private companies. Already, NASA is passing on traditional government activities of supply and crew transfer to and from the ISS over to the hands of private industry with the implementation of its Commercial Cargo and Crew programs. NASA is applying the same strategy when it comes to answering the question of what comes next after ISS in LEO. At a presentation in April 2015, NASA Associate Administrator Bill Gerstenmaier stated, “What we'd like to do is have the next space station…be a private space station that is driven primarily by fundamental or basic research coming from the private sector.” 1

NASA appears to see 2 scenarios for a market that drives the development of these commercial platforms. The first is sustained economic activity in LEO enabled by human spaceflight driven by private investments and commercial supply and demand. The second scenario is similar to the first except that the market would be driven by both public and private investments and public and private demand. 2 NASA believes that the ISS presents opportunities to test business cases that will empower an LEO commercial market enabled by human spaceflight.

To achieve a vision of sustained economic activity driven by human spaceflight activity in LEO, NASA has articulated 4 goals

3

:

1. Leverage ISS to enable LEO commercialization 2. Establish a policy and regulatory environment that promotes commercialization of LEO 3. Stimulate robust, self-sustaining, and cost-effective supply of U.S. commercial services that accommodate public and private demands to and from LEO 4. Foster and facilitate consortia-type activities to attract broad sectors of the economy to use LEO for commercial purposes.

NASA includes commercial platforms among the commercial services mentioned in Goal 3.

Evaluating the Potential Market in Leo

In order for commercial companies to successfully own, operate, and maintain commercial stations in LEO without NASA mission commitments, there has to be a market for commercial business cases. Today's multi-billion dollar market in LEO is primarily driven by nonhuman spaceflight activities, particularly satellite services, satellite manufacturing, satellite launch, and satellite-related ground systems. Today, investors and venture capitalists are primarily drawn to the recent successes of remote sensing companies such as Skybox, which was acquired by Google. 4 However, none of these companies has human spaceflight components to the business plans. Their businesses are simply finding ways to innovate in established spaceflight markets.

The level of investment required by NASA to enable commercial platform capabilities will depend on how strong or weak the LEO human spaceflight enabled market is in the 2020s. If a strong market forecast can be successfully argued, then NASA involvement may only be limited to the stimulation of technological development, a traditional NASA strength. However, a weak market forecast may require more of a NASA commitment, including dedicated leasing contracts to outright procurement of stations for specific missions, to stimulate commercial development.

Commercial Research and Development in Microgravity

One may ask, why does NASA have an interest in maintaining U.S. LEO platform capabilities? For NASA, the benefits of studying the effects of microgravity on the human body offer an insight into some of the physiological and psychological challenges astronauts face in long-duration spaceflight to the Moon, an asteroid, or Mars. Long-duration challenges on the human body include radiation, constant noise, unusual light–dark cycles, and sustained higher levels of CO2. 5 NASA claims that the results of missions such as the recent 1-year mission of astronaut Scott Kelly and cosmonaut Mikhail Kornienko provide a “stepping stone” to future Mars missions. 6 Furthermore, the ISS also serves as platform for testing new technologies and processes in an active mission environment in microgravity before embarking on deep exploration missions to the Moon, an asteroid, or Mars.

NASA perspective on a microgravity market

In 2011, NASA selected the Center for the Advancement of Science in Space (CASIS) to manage a U.S. national laboratory onboard the ISS and to promote the potential commercial benefits of the microgravity environment. 7 Specifically, CASIS provides seed money, expertise, access to launch, administrative support, and education outreach for commercial microgravity research. In a July 2015 statement to the House Subcommittee on Space, NASA Associate Administrator for Human Exploration and Operations, Bill Gerstenmair, stated that U.S. industry partners can “use the unique microgravity environment of space and the advanced research facilities aboard [ISS] to enable investigations that may give them the edge in the global competition to develop valuable, high technology, products and services” that will “help establish and demonstrate the market for research in LEO beyond the requirements of NASA.” 8 ISS Program Director, Sam Scimemi, also enforced this view stating that NASA envisions a future of “sustained economic activity in LEO enabled by human spaceflight, driven by private and public investments creating value and benefitting Earth through commercial supply and private and public demand.” 9

As for exactly what research or investigations that may draw industry to LEO, “protein crystallization, exotic fibers, and 3D tissues” are often mentioned as examples of markets that NASA, through CASIS, can attract broad sectors of the U.S. economy to LEO. 10 This sentiment of market opportunity within these areas of pharmaceuticals, biotechnology, and materials science is shared by others in NASA leadership and at CASIS. 11 Universities and companies already have some projects underway onboard ISS with other experiments in the planning stages. In addition, NASA has met with Department of Commerce officials about potential tax incentives for microgravity research. 12

Issues with microgravity research

While NASA claims that there is “huge potential” in LEO, few of the NASA promoted research areas are yet to be proven economically viable.

13

In 2015, NASA created an LEO economic study team tasked to study the potential for LEO commercialization. Among this team is Dr. Nicholas Vonartas of George Washington University whose research team developed a model of drug development costs from space-grown proteins.

14

Dr. Vonartas notes that key evidence on protein crystal quality improvements in space compared to Earth-based methods is still pending. Research by Dr. Lawrence DeLucas of the University of Alabama at Birmingham is currently analyzing 2,000 protein crystals grown in space versus Earth based.

15

Until Dr. DeLucas and other researchers begin to show concrete evidence that microgravity development methods improve bioscience and material production, perspective companies may be unwilling to invest in research without government support. As Dr. Vonartas writes:

The leap from earth crystals to drastically pricier (yet better quality) space crystals may be too risky of an investment to expect from private pharmaceutical companies, even with significant projected cost reductions. A government-subsidized consortium may be the best plan to alleviate some of the early-stage, precompetitive financial risk.

16

Many in the scientific community want NASA and CASIS to continue to support and conduct science research to fill in these data gaps. While there is commercial utilization onboard the ISS today, NASA leadership has been disappointed with the recent lack of other ideas presented by industry for other ISS commercial utilization opportunities. 17 Moreover, some in industry have asserted that NASA argument of microgravity research as a potential market for LEO commercialization is overly optimistic and that such a market could be 10 years out from developing. 18 Some industry experts note that part of the problem for companies that may be potentially interested in microgravity research is that there are no small steps available to try out research projects in microgravity other than going directly to the ISS and NASA, which can be a costly and time-consuming proposition despite government support. 19

Space Tourism

Out of all the potential human spaceflight markets, space tourism may be the most publicized. The attraction of the space environment becoming accessible to the general public is an enticing business case that has attracted new companies to the spaceflight market. In 2012, the Federal Aviation Administration (FAA) and its Office of Commercial Spaceflight (AST) released a statement that projected the market for space tourism to be $1 billion by the 2020s. 20 The FAA also believed in 2012 that companies would be making suborbital flights regularly by 2014. However, as of 2016, no suborbital commercial services have begun. Furthermore, this $1 billion market would primarily come from suborbital flights, not orbital flights, which is the type of spaceflight activity that would support a commercial space station business case.

Tourism market studies

The idea of space tourism is often a recurring theme of human spaceflight market studies. In 1994, 6 major aerospace companies came together to produce for NASA the Commercial Space Transportation Study (CSTS).

21

This study conducted market assessments of numerous potential commercial and government markets in space, one of which was space tourism. While tourism is a multi-billion dollar market on Earth, the study stated that space as a destination must meet the expectations of a typical tourism industry in that:

[Trips] must be available to customers on short demand; costs and pricing structures must allow a reasonable profit margin; the system must be capable of operating without a standing army of support personnel; and operating facilities must offer multiuser capabilities so that they can be more cost effective.

22

The CSTS predictions were dependent on lower launch and operations costs. Similarly, a Space Tourism Market Study published by the Futron Corporation in 2002 stated that suborbital and orbital tourism had potential markets of $700 million and $300 million, respectively. 23 Futron forecasted that by 2021, more than 15,000 passengers would be flying annually on suborbital flights. 24 However, by the end of 2015, no commercial voyages have begun. Even having a few hundred passengers flying annually by 2021 may be difficult for commercial companies to achieve. However, there does seem to be enough investment and demand in the market to eventually bring suborbital flights to fruition. One suborbital company, Virgin Galatic, already has sold more than 700 tickets at a price of over $200 thousand per ticket. 25 However, continual development delays and a recent test accident have hampered their suborbital vehicle from coming to market.

Orbital space tourism

For orbital flights, the market becomes more about destinations than experiencing microgravity, which a commercial space station could provide. 26 Nonetheless, this type of trip would be at an exceptionally higher price point than suborbital flights. Over the past 15 years, several private citizens have flown into LEO via Russia's Soyuz spacecraft to the ISS by paying $20 to $40 million through a company called Space Adventures. 27 Space Adventures facilitates and negotiates the training and transportation costs that are provided by Russia's human spaceflight program to fly on government missions to the ISS. Currently, the future of fully commercial orbital flights from U.S. providers is tied to NASA Commercial Crew Program (CCP) vehicles, SpaceX's Dragon and Boeing's Starliner, both of which will not begin flights till late 2017 at the earliest. Even during the early 2020s, any orbital tourism market will probably still be limited to multi-millionaires. Therefore, given past predictions and lack of current capabilities, NASA should not assume a vibrant commercial market for orbital tourism by the mid-2020s. Even if suborbital tourism does materialize by the 2020s, customer demand for spaceflight experience may be satisfied enough to a point where it creates a weak business case for orbital tourism.

Foreign Human Spaceflight Interests

As NASA human spaceflight ambitions shift from LEO to cislunar space, there may be continued interest in LEO human spaceflight missions from other world space programs. This includes non-ISS partners such as China, which has its own LEO space station ambitions, along with potential interests from nations that have never had manned space programs before such as Norway and United Arab Emirates. Even traditional NASA partners such as Canada, UK, and Japan may be able to expand their astronaut corps if commercial platforms became available. 28 Industry has also argued that if NASA were to commit human spaceflight missions to commercial platforms, some of these partners would readily join such missions and share the cost. 29

China's space station ambitions

A source of potential commercial competition for U.S. companies and political pressure on NASA is a Chinese owned and operated human space station in LEO. Assuming that the current station development schedule holds, China's human spaceflight agency, the China Manned Space Agency (CMSA), has stated that a core module would launch in 2018. 30 Eventually, CMSA plans to add 2 experiment modules to the core and complete the station by 2022. Like the ISS, this station would support a nominal crew of 3 with a maximum capacity of 6.

A Chinese station potentially threatens a commercial market for foreign human spaceflight. China is actively soliciting foreign participation in its planned station in the form of modules to attach to its planned 3-module core system. 31 China may leverage the station for political purposes. For example, China could send foreign astronauts to LEO at little to no cost from developing countries as part of building stronger political and economic ties with those countries. This competition may create market headwinds for commercial stations trying to entice foreign space programs to lease time for human missions in LEO, especially non-ISS partners looking to have a human space presence. Already, China has signed space station cooperation agreements with Russian and European space agencies. 32 Furthermore, European Space Agency astronauts have already begun visiting training sites in China in preparation for future collaboration.

By law, NASA is not allowed to collaborate with CMSA as result of Congressional language that first appeared under the 2011 Department of Defense and Full-Year Appropriations Act and continues to appear in subsequent NASA appropriations. Specifically, no appropriated funds may be used “to develop, design, plan, promulgate, implement or execute a bilateral policy, program, order, or contract of any kind to participate, collaborate, or coordinate bilaterally in any way with China or any Chinese-owned company.” 33 Exceptions to this restriction include hosting Chinese nationals at NASA facilities as long as prior notice and certain assurances are given to Congress. 34

A Chinese station may create political pressure on NASA to avoid a “station gap” from ISS to a commercial station or a deep space station. One could imagine Congress having concerns and reservations around a lack of U.S. human spaceflight capability and presence in LEO compared to the Chinese in the 2020s. However, NASA leadership's opinion is that China's human spaceflight developments are a positive for global exploration efforts. ISS Director, Sam Scimemi, stated that “It's very good to see many countries, including China, to be interested in going into space with humans.” 35 Perhaps a shift in policy by 2020s may allow NASA astronauts to participate in China's future LEO station, which may damage a business case for commercial platforms in LEO.

International human spaceflight visions

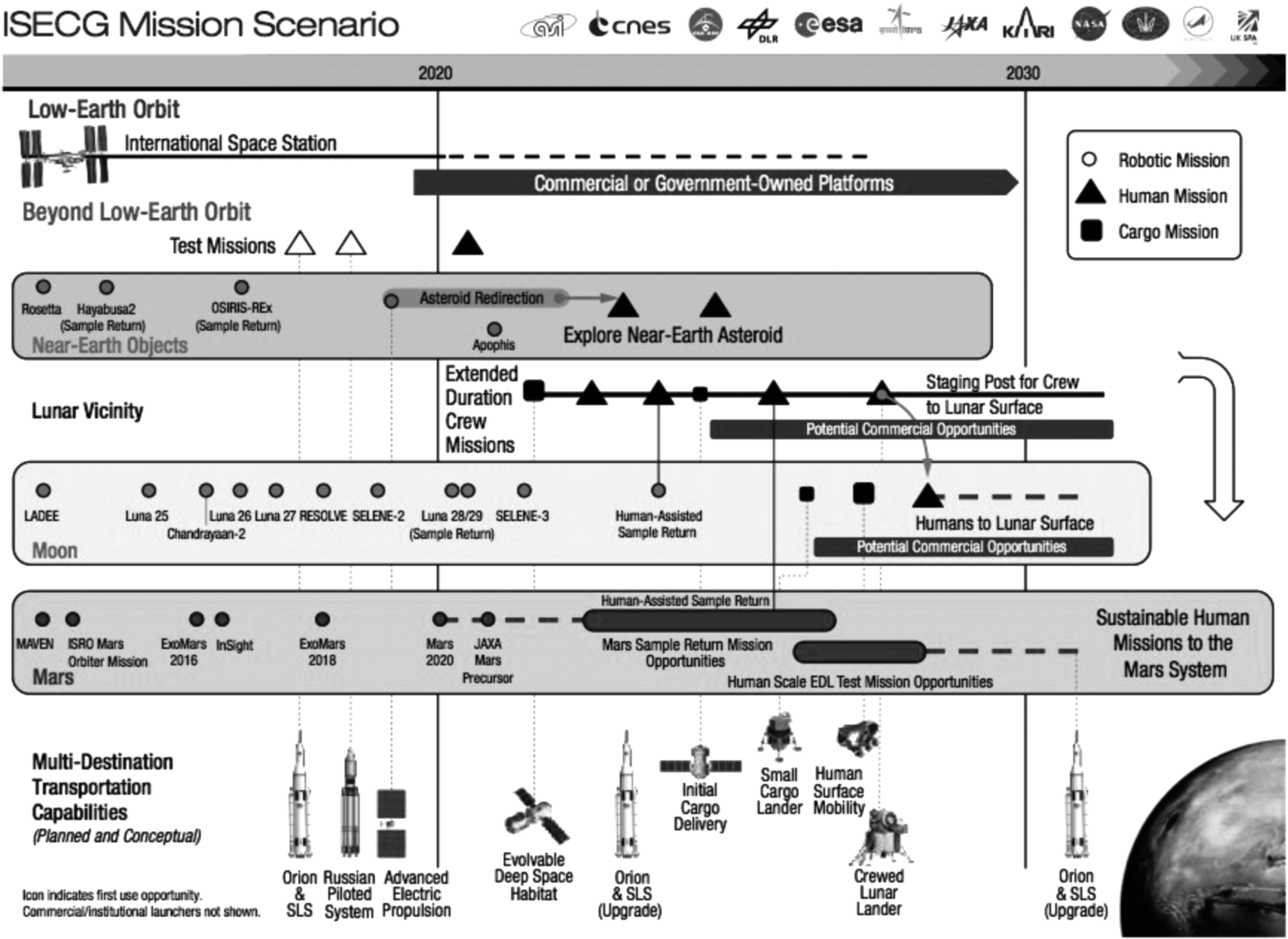

To date, no foreign space agencies have publically announced any kind of partnership with a commercial company to develop a commercial platform for human spaceflight missions. Currently, 14 world space agencies, including NASA, work collaboratively on a common vision for peaceful robotic and human space exploration to LEO, the Moon, and Mars through the International Space Exploration Coordination Group. In 2013, the group produced a roadmap for exploration activities out to the 2030s as shown in Figure 1. The roadmap includes NASA mission objectives for an asteroid redirect mission in cislunar space and potential Mars missions. However, the roadmap also shows human missions to the Moon with lunar landings. These missions represent the visions for many European space agencies and new space powers such as China. 36 As for LEO space, the roadmap does not elaborate beyond the ISS and potential “commercial or government-owned platforms.”

ISECG 2013 roadmap mentions commercial opportunities, but government focuses on lunar and cislunar space human spaceflight missions 87 Credit: NASA (www.nasa.gov/sites/default/files/files/GER-2013_Small.pdf). ISECG, International Space Exploration Coordination Group.

Regulatory Environment

Government regulation of commercial space stations may fall under the purview of the FAA and its Office of Commercial Spaceflight (AST). Currently, AST regulates all commercial launches in the United States and even launches by U.S. citizens abroad because the international treaty environment created by the 1967 Outer Space Treaty, the 1972 Liability Convention, and the 1976 Registration Convention that define space activities only in terms of state actions, therefore, placing liabilities on the United States. 37 AST also licenses commercial launch and reentry sites, also known as spaceports. The licensing process includes preapplication, interagency review, policy review, determination of financial responsibilities, environmental reviews, and safety reviews. 38 AST mission is to “ensure protection of the public, property, and the national security and foreign policy interests of the United States during commercial launch or reentry activities.” However, AST mission is also to “encourage, facilitate, and promote U.S. commercial space transportation.” Moreover, in late 2015, President Obama signed into law the U.S. Commercial Space Launch Competitiveness Act, which limits the FAA ability to regulate commercial space launch companies until at least 2023. 39 Therefore, an established regulatory environment is predicted to be a low hurdle for commercial stations in the 2020s with the likelihood of only a nascent framework to govern LEO commercial platform activities.

Although AST has no current mandate or guidance around payloads, including commercial station modules, the FAA does study launch payloads in the context of U.S. interests. As AST analyst Steph Earle states, “The FAA has become the gateway to space for payloads.” 40 The FAA continues to lead interagency reviews on payloads even though it does not have regulatory authority to authorize payloads. Other agencies that may see a greater role in commercial space station regulation include the National Oceanic and Atmospheric Administration, which regulates commercial remote sensing and the Federal Communications Commission, which regulates commercial broadcast. FAA states that the agency is supportive of these “innovative space uses” and believes that part of AST mission is to promote the space industry, especially as investors look for regulatory consistency in this new market. 41

Despite a mission dedicated to the promotion and protection of commercial spaceflight, Congress has consistently constrained AST regulation authority over the commercial human spaceflight industry to avoid regulation burden as demonstrated with the passage of the U.S. Commercial Space Launch Competitiveness Act of 2015. Thus, Congress is likely to wait on granting AST any new regulatory authority around orbital safety and commercial space stations until the industry matures. However, this policy approach is not without tradeoffs. Pressures to place minimum burden on private commercial space companies have come under criticism by a National Transportation Safety Board (NTSB) in an accident investigation report on the October 2014 accident of a Virgin Galactic's SpaceShipTwo, a suborbital spacecraft that left one test pilot dead and one seriously injured. 42 Currently, AST issues experimental permits to commercial launch providers for human spacecraft. 43 From its investigation, NTSB found that AST issued waivers to the SpaceShipTwo's developer, Scaled Composites, for an experimental flying permit after the company failed to meet regulation requirements following a hazard analysis. In addition, AST is accused of reducing the number of technical questions posed to Scaled Composites to avoid placing a burden on the company.

Whatever pathway NASA chooses in the promotion of commercial space platforms for LEO missions post-ISS, it is clear that FAA has intentions to become the safety regulatory body for commercial activities for LEO. The Commercial Space Transportation Advisory Committee (COMSTAC), the industry panel that advises AST, recommends that the FAA look at establishing a mission license for commercial space stations as a possible regulatory solution for commercial space stations. 44 Mission licenses would capture innovative activities that do not currently fit into the current categories of commercial launch and spaceports. However, this authority requires Congressional action to establish.

In this new era of space transportation, FAA often looks to NASA as a baseline for safety guidance. In 2014, FAA, with the input of COMSTAC and NASA, created a document entitled “The Recommended Practices for Human Spaceflight Occupant Safety” to facilitate safety discussions between government, industry, and academia on commercial human spaceflight. 45 The document provides a framework for industry to develop safety standards and is based on NASA requirements for its CCP. 46 In addition, the U.S. Commercial Space Launch Competitiveness Act directs FAA to consult NASA on issues of health and safety in regard to commercial launch and reentry vehicles. 47

Evaluating the Potential Organizational and Technological Capabilities in Leo

While commercial companies have worked with NASA since the earliest stages of human spaceflight and are fundamental partners in ISS operations and development, a wholly developed, owned, and operated commercial station brings about new organizational and technological challenges that are further complicated by the need to be cost-effective. Furthermore, any station will be dependent on the reliability, frequency, and cost-effectiveness of cargo and crew launches to sustain operations. Thus, the organizational and technological capabilities of cargo and crew launch vehicles from U.S. providers must be assessed as well.

Commercial Space Station Capabilities

To date, companies interested in selling commercial human spaceflight services have nearly exclusively focused on suborbital and orbital launch and return missions. The only company that has consistently committed and demonstrated a commitment to private station development is Bigelow Aerospace. However, recent NASA investments in habitat concepts for potential deep space uses could provide potential commercial spin-offs for LEO applications.

Bigelow aerospace

Founded in 1999 and based in Las Vegas, Bigelow Aerospace is diligently working to establish itself as the primary provider for a commercial platform market. Bigelow Aerospace's plan is to dominate the LEO human spaceflight market with its expandable habitat design. Such a concept was originally developed by NASA, which first started testing inflatable satellites through its Echo program in the late 1950s. 48 Bigelow Aerospace first tested their expandable concept in 2006 with the successful launch and deployment of its Genesis I station followed by another successful launch and orbit of Genesis II. These concurrent successes validated Bigelow Aerospace's expandable engineering concept and demonstrated its long-term durability as both Genesis prototypes maintained their structural integrity throughout their missions.

In early 2016, NASA launched the Bigelow Expandable Activity Module (BEAM) to the ISS under an $18 million contract through NASA Advanced Exploration Systems (AES) program to provide proof of concept for expandable habitats. 49 In May 2016, BEAM successfully attached to the ISS Tranquility node and, after some delays, successfully expanded to undergo its scheduled 2-year testing period. 50 BEAM became the first expandable module entered by humans in space. Bigelow Aerospace is confident in the habitat's safety, particularly in regard to its resiliency to space debris and micrometeorites. Often people may be inclined to associate terms, inflatable and expandable, with flimsy material like that of a balloon. However, Bigelow Aerospace is trying to change that perception by showing the public that the combination of fiber materials that comprise BEAM shell is actually stronger than steel. Through hypervelocity impact tests, the BEAM expandable material actually outperforms the current structural materials used for the ISS modules. 51

While BEAM is set to prove the viability of expandable habitats, Bigelow's flagship product is the B330, an expandable habitat that is designed to house 6 astronauts and is 330 m 3 in volume, which is much larger compared to the 16 m 3 of volume provided by the BEAM module. The B330 design allows for the connection of additional B330 modules to allow for the creation of different station configurations to meet the size requirements of a customer's needs. The docking system onboard each B330 is designed to be compatible with SpaceX's Dragon and Boeing CST-100 Starliner docking systems. Therefore, Bigelow Aerospace states that the debut of the B330 is dependent on the operability of Dragon and Starliner, which are scheduled to occur in late 2017, to begin testing and deployment of 2 B330s presently under development. 52 In addition, the B330 is advertised to have a life span of 20 years. According to the then Bigelow Aerospace's Government Affairs Chief, Mike Gold, the “B330 system would at first provide a complement to the [ISS] and then eventually be its successor.” 53 If this product comes to fruition as promised, then a station constructed from 3 B330 modules would provide more internal volume than the current ISS and take less than a 10th of the number of payload launches to assemble. 54

Technological challenges

Technologically, Bigelow Aerospace appears to be close to proving that its station designs are structurally sound for crewed missions. NASA expects BEAM to provide valuable data points for structural models on expandable materials. 55 However, even traditional space companies such as Boeing through its work on the ISS have proven expertise in rigid structure concepts to develop future station modules beyond ISS if they choose to enter the market. However, perhaps the greatest technical challenge to any potential station developer yet to be resolved is the commercial development of life support and environmental control systems. Bigelow Aerospace's BEAM does not have any of these components as it is designed to merge seamlessly with the ISS's current life support systems. Today, NASA holds significant intellectual property around ISS life support and environmental control systems that is yet to be made public or shared with industry. 56 NASA is open to transferring this knowledge to commercial industry. 57 However, for any company pursuing station development, these critical systems will take time to develop, test, and deploy. Current work by Boeing and SpaceX for the CCP may provide some insight into how industry will address life support and environmental control system issues.

Organizational challenges

Today, ISS crews have nearly continuous connection with ground controllers across the globe, who provide technical, procedural, medical, and other specialist advice to ensure operations onboard run smoothly. With such major governmental organizations in place to operate the ISS, will commercial companies be able to provide the same level of continuous support to commercial missions within LEO? Also, an equally important question is, can this support be done cost-effectively? ISS crews are constantly in communication with ground controllers asking a variety of questions on intimate details on the station's internal and external systems to maintain operations and crew safety. This communication is especially critical during times of maintenance and emergency. Commercial orbital and suborbital cargo and crew missions may be able to provide a glimpse of these organizational capabilities. However, commercial platforms would require organizational support for months or even years on end, which is far cry from launch and return missions that may only last hours or days.

The only U.S. case study available of privately run operations onboard a space station occurred in early 2000 when a private company, MirCorp, leased the Russian Mir space station for commercial activity. 58 While the company funded a private crewed mission to Mir, the company was supported by Russian ground controllers and existing government space infrastructure, including the Mir itself. The 70-day mission produced a number of firsts in human spaceflight that included a privately funded launch, spacewalk, and station operations. However, while MirCorp claimed to have significant investor interest in various potential markets that included science and tourism, ultimately the Mir station was deorbited because the Russian government shifted its efforts toward ISS development and private investors could not maintain the Mir's support costs. 59

NASA cislunar habitat goal

While NASA human spaceflight mission profile in LEO currently remains centered on the ISS, NASA long-term vision is crewed missions to Mars. However, in the next 10 to 15 years, NASA is focusing its human spaceflight program on cislunar space as a destination to achieve the organization and technological capabilities needed to endeavor on to Mars. Development is already well underway for a new heavy-lift launch vehicle, the System Launch Vehicle (SLS), and a new crew capsule spacecraft, Orion, for human missions out to cislunar space. SLS is NASA's first heavy-lift rocket since the massive Saturn rockets of the 1960s Apollo program and will be the most powerful rocket ever built. 60 In July 2014, SLS passed a critical design review, which allows Boeing, the prime contractor, to begin production of the vehicle's core stage. 61 Scheduled for delivery in time for the first Orion unmanned mission out to cislunar space planned for 2018, the initial SLS configuration will be capable of launching 70 metric tons beyond LEO. 62 On top of SLS will be the Orion crew capsule, which can accommodate a crew of 6 and last up to 21 days. 63 Orion successfully completed an unmanned flight test in LEO in 2014. However, recently a NASA review found that Orion may not be ready for crewed mission until 2023. 64 This crewed mission, the only mission currently on the books for SLS and Orion, intends to send a crew of 4 out to lunar orbit and return to Earth.

Recently, NASA has begun incorporating cislunar habitats into its human spaceflight strategy, which could help shape future crewed missions into cislunar space. In its Journey to Mars document released in late 2015, NASA states:

NASA, together with its international and commercial partners, will develop a strategy to complete “Mars-ready” habitation system testing on Earth and on ISS. NASA and its partners will also develop an initial habitation capability for short-duration missions in cislunar space during the early 2020s and evolve this capability for long-duration missions in the later 2020s.

65

Congress has been consistent in funding the SLS, Orion, and supporting ground systems for NASA cislunar missions. However, Republican Congressional leaders are critical of a NASA proposed cislunar asteroid redirect mission and its Journey to Mars outline. 66 A NASA investment into the development of deep space habitats does have the potential for LEO commercial spin-offs or at least provides NASA with potential platforms that could be deployed in LEO after the ISS is decommissioned.

NASA has already begun to invest in potential deep space habitat concepts through its AES and its Next Space Technologies for Exploration Partnerships (NextSTEP) program. NASA already funds 7 contracts, each valued up to $1 million, through the NextSTEP program related to habitation concepts to sustain an Orion crew of 4 for up to 60 days in cislunar space. 67 Four of these contracts address habitat concept development, while the other 3 address environmental control and life support systems. The 4 companies with habitat contracts are Bigelow Aerospace, Orbital ATK, Lockheed Martin, and Boeing. While Bigelow Aerospace is the most vocal about LEO applications of its habitat concept, the other company participants have expressed potential LEO applications of their concepts as well as according to AES. 68 Boeing's concept is centered on developing something low cost first and then testing and evolving the concept for cislunar space and Mars, which may indicate potential LEO application. 69 Orbital ATK concept is a modular approach based on its existing Cygnus cargo spacecraft, which is a NASA commercial supply vehicle to the ISS. Finally, Lockheed's concept will study how habitats should be designed to optimally sync with the Orion vehicle.

These NextSTEP contracts are scheduled to be completed by September 2016. AES then intends to initiate a Phase II set of contracts where the companies will begin hardware development. 70 The amount of funding for these Phase II contracts or the exact requirements is yet to be determined as AES will let the companies each scope out the costs for Phase II. AES is expecting to find around 60% overlap between the 4 companies' concepts that will lay the foundation for the Phase II contract amounts and scope. 71 This contract approach is similar to how NASA is approaching all new human spaceflight contracts, where NASA sets specific goals but industry is free to select the approach to achieve those goals. However, some in industry are curious to know if NASA intends to procure a cislunar habitat after the NextSTEP contracts.

Privatization of ISS operations

What if the next station is not really new at all but a repurposed ISS that is privately operated? Such a concept of privatization is not unknown to NASA. In the late 1990s, NASA sponsored a series of independent studies focused on potential ISS operation models, including privatization. 72 These reports included analysis and observations for different ways to organize the ISS, including creating an entity to operate U.S. modules on ISS for profit or as a nonprofit. Details included how a private entity would operate in NASA human spaceflight hierarchy and the amount of NASA personnel needed to be transferred to the private entity. Some of the nonprofit concepts mimic what the CASIS role is today running a U.S. national laboratory onboard ISS. However, NASA never acted on these studies to investigate the concept further.

One of the unique aspects of turning over ISS operations to private stakeholders is that the ISS is internationally owned and operated among 5 space agency partners. Current ISS international agreements are only in effect until 2020. In early 2014, NASA declared a desire to extend the ISS agreements to 2024, and the United States entered this language into the recent U.S. Commercial Space Launch Competitiveness Act. However, an actual agreement with all existing international partners is yet to be agreed upon. Perhaps there could be a scenario where companies may want to add modules to the ISS for commercial purposes as part of a larger private presence onboard the ISS. BEAM could provide a proof of concept for such an idea. 73

To date, NASA leadership has not embraced or promoted the idea of fully privatizing operations onboard ISS. Therefore, the probably of NASA transferring full operations to a private industry is considered low. However, ISS program leadership has stated that they foresee some operations becoming privatized in the coming years. Specifically, they point to payload integration as an area of operations to turn over to private industry. 74

Commercial Cargo Capabilities

The NASA Commercial Orbital Transportation Services program (COTS) was a 2-stage program in which NASA invested ∼$800 million from 2006 to 2012 to help industry develop, demonstrate, and eventually provide cargo delivery capability to the ISS. 75 COTS produced 2 successful providers, Orbital ATK and SpaceX, to replace cargo capabilities lost from the retirement of the Space Shuttle. NASA then created the Commercial Resupply Services contracts, which are worth billions of dollars, to purchase these capabilities. Both suppliers have had multiple successful missions until each suffered an accident in late 2014 and mid-2015. However, both Orbital ATK and SpaceX returned to flight in 2016. The assumption of an ISS extension to at least 2024 will provide a steady source of demand in addition to commercial and defense markets for cargo suppliers. For example, SpaceX valued NASA supply and return mission contracts in 2016 at $150 million per launch. 76 However, it is unclear what SpaceX's profit margin is off these flights. Orbital ATK states that these missions are a profitable part of their space systems division. 77 However, both SpaceX and Orbital ATK have diversified space launch portfolios that comprised commercial and defense satellites, which are not part of an LEO market enabled by human spaceflight.

While the capability may be there in the 2020s for cargo delivery to commercial stations, payload cost and launch frequency may continue to pose market headwinds. SpaceX is trying to reduce costs by developing a reusable Falcon rocket that launches payloads to space and then lands back on Earth for later reuse. In 2016, SpaceX released a list of fixed prices and capabilities for launch services in 2018 of its Falcon 9 and planned Falcon Heavy expendable launch vehicles. 78 The price points for these vehicles, included $62 million to launch 22,800 kg to LEO onboard a Falcon 9 and $90 million to launch 54,400 kg to LEO onboard a Falcon Heavy. SpaceX claims that it can further discount these prices around 30% once Falcon reusable technology is further demonstrated in future launches.

Given the proven technological and organizational capabilities of industry in commercial cargo and satellite launch and coupled with a stable commercial and government market for satellite launches, cargo supply capabilities should be readily available for commercial station providers. This argument is further strengthened if there is overlap between the ISS and a commercial station's deployment. Areas of possible concern include the financial stability of a commercial station to withstand launch failures and supply disruptions. In addition, ground control teams from companies such as Orbital ATK and SpaceX operate in concert with the NASA Johnson Spaceflight center ground control team, which has a long history of organizational expertise with LEO operations, to deliver cargo to the ISS. A future commercial station enterprise would also have to have a robust ground control organization that could work in concert with these launch providers.

Commercial Crew Capabilities

For over 3 decades, the Space Shuttle was the only U.S. crew-rated vehicle to transport astronauts to and from LEO. With no crew-rated vehicle to replace the Space Shuttle, NASA now relies on the Russian Soyuz to transport NASA astronauts to and from LEO. NASA decided to develop the next generation of LEO vehicles through the CCP, a program that strives to create an environment where NASA no longer procures LEO human spaceflight capabilities but invests in industry-developed, industry-owned, and industry-operated vehicles. The CCP goal is to end the United States current lack of capability to transport astronauts to and from ISS and LEO by 2017. 79 That time frame may change due to development delays, some of which NASA blames, in part, to funding gaps in the program created by Congress. 80

In late 2014, NASA awarded Boeing and SpaceX with fixed price contracts worth a total of $6.8 billion to transport NASA astronauts to and from ISS from 2017 to 2023. 81 If Boeing and SpaceX are unsuccessful, NASA will be left with difficult options, including the continuation of purchases of Russian Soyuz flights and potentially backing out from its ISS commitments. Therefore, assuming ISS is utilized to at least 2024, the probability of commercial capability to LEO is high. NASA will continue to fund these contracts and procure this capability because the political and budgetary pressures of continuing to use Soyuz seats will be unappealing and perhaps more costly. NASA already has assigned astronauts to begin training with both CCP provider vehicles.

Recommendations

As NASA enters the 2020s, much of its human spaceflight portfolio will continue to center around ISS operations. Commercial industry may still be able to provide NASA LEO capability that is more cost-effective than the ISS or for post-ISS LEO missions. This depends on the NASA mission objectives in LEO and in the scope of its overall human spaceflight strategy for the 2020s, as well as budgetary and policy inputs from Congress and the President.

Study Impacts of an ISS Extension Versus Short-Duration Commercial Platforms

Since an established habitat presence in cislunar space by the mid-2020s may be unlikely, NASA should begin studies on the cost and benefits of continuing ISS operations into the late 2020s versus procuring commercial platforms. Specifically, the studies should address commercial platforms developed for NASA for short-duration use, such as 60 days, which is the current life span goal set out in the NextSTEPs contracts. Safety, mission tradeoffs, and budgetary considerations should all be major considerations. Already, there are some concerns around NASA plans to extend the ISS out to 2024. In September 2014, the NASA Office of Inspector General (IG) released a report on NASA plans to extend ISS operations to 2024. In this report, the IG calls the NASA $3 to $4 billion annual cost estimations for ISS operations out to 2024 “overly optimistic.” 82 In addition, the IG found that NASA does not plan to maintain any contingency funds for ISS operations out to 2024. Moreover, NASA commercial cargo companies currently have limited capability to deliver large replacement parts critical to ISS operations, such as solar arrays and radiators should maintenance be required. 83 Also, NASA should be realistic about ISS costs and contingency costs should ISS partners withdraw from the ISS agreements. NASA and its commercial partners should put forward realistic time frames for procuring short-duration platforms that can integrate with commercial cargo and crew capabilities.

If short-duration commercial platforms are concluded to be a safe, feasible, and cost-effective option against another ISS extension through NASA studies, then NASA should consider a Commercial Habitat Program with corresponding Space Act Agreements that compliment or directly build off of NASA AES deep space habitat contracts. In addition, this habitat program may include procurement contracts for a commercial platform supplier for short-duration NASA LEO missions. The number of deep space platform procurement contracts should be tied to the NASA trajectory to operate within cislunar space and deployment of deep space habitats with SLS. LEO commercial platforms should serve as the test beds for the deep space habitat designs and provide an infrastructure for private utilization should a commercial market emerge.

Conclusion

In 1994, 6 major aerospace companies came together to produce for NASA the CSTS. This study conducted market assessments of numerous commercial and government markets in space, including markets for human spaceflight. Every seemly possible space market was analyzed from communications to athletic events in space. 84 Many of these markets, the companies claimed, could be untapped with lowered costs for access to space. 85 However, since 1994, commercial launches in the United States per year are consistently low with only 12 FAA licensed commercial launches in 2014. 86 Companies now participating in Commercial Cargo and Crew programs may lower the cost of launch for NASA. However, even with these new capabilities, self-sustaining commercial platforms by the mid-2020s seems unlikely. As NASA enters the 2020s, it has to consider where the priorities lie for human spaceflight in cislunar space, including a deep space habitat. NASA should study the costs and timelines associated with an extension of the ISS past 2024, the procurement of short-duration LEO stations, and the procurement of cislunar habitats to provide the next presidential administration proper data points to make a decision on the future of NASA human spaceflight strategy.