Abstract

Abstract

The potential of using small satellites for commercial Earth observation (EO) has successfully appraised the investment community into enabling NewSpace enterprises to launch several constellations like never before. Several of these constellations aim mostly at provisioning data at revolutionary costs and at never before achieved revisits. On one hand, these NewSpace enterprises are looking to disrupt the traditional EO data markets, and on the other, they are targeting either creation/support for big data analytics platforms through these constellations and opening up new markets for EO products. Given the sheer number of NewSpace companies and the variety of constellations that are out there, one needs to wonder whether this is going to be a game changer or is it a massive bubble. In the next 5–10 years, will there be an oversupply of EO data or is there a shortfall in supply of market-relevant data? Will big data analytics platforms driven by high-revisit data availability be a game changer in the EO marketplace? Are the NewSpace commercial EO constellations targeting only price and revisit or is there more to this story? Do these constellations cater to most of the needs of EO data users? This work makes an attempt to provide a critical analysis of the NewSpace EO small satellite platforms and the constellations to perform an assessment of the commercial exploitation of such platforms in the EO marketplace.

Introduction

NewSpace has taken the world by a storm by attracting large-scale private investments in companies with the promise of leveraging innovation in technology development to substantially reduce the cost of access to space/space products or services. According to a market research and advisory firm, there are 10,000 companies to be expected in the next 10 years seeking to commercialize space. 1

Skybox Imaging (founded in 2009) was the first NewSpace company that raised private capital in the Earth observation (EO) market. SkyBox challenged the traditional business models in EO by taking an approach of not having government as an anchor customer and with the promise to address mass market requirements for high-quality, low-cost data. 2 Since SkyBox, there are a dozen other companies that have gone on to raise private capital to build satellites for EO. Google acquisition of SkyBox Imaging 3 arguably seeded more confidence in the private capital investment community for NewSpace EO at its time.

We are in no way doubting the success of NewSpace in changing perceptions of traditional space agencies/companies. The success of NewSpace in convincing policy makers and managers of space programs to accept new methods of innovation is indeed laudable. However, the question today that looms large is whether there is room in the market for so many players in the sector and whether there is a match in demand–supply considering the upstream and downstream of the global value chain in EO.

This work provides some insights into the foundation of NewSpace EO, the advent of NewSpace commercial EO, and the dominating perceived differences between traditional and NewSpace companies. We also attempt to provide some gaps in the market requirements that NewSpace has still not addressed.

Foundation of Newspace EO

The ethos of NewSpace lay in low-cost commercial off the shelf (COTS) innovation largely; the foundation of such change in approach to space exploration possibly began with small satellites being developed by the likes of University of Surrey and TU Berlin. In fact, the very foundation of experimental satellites such as UoSAT series built by universities provides many of the bases such as cost-effective spacecraft engineering research and opportunities for in-orbit technology demonstration 4 that NewSpace argues in larger manner today.

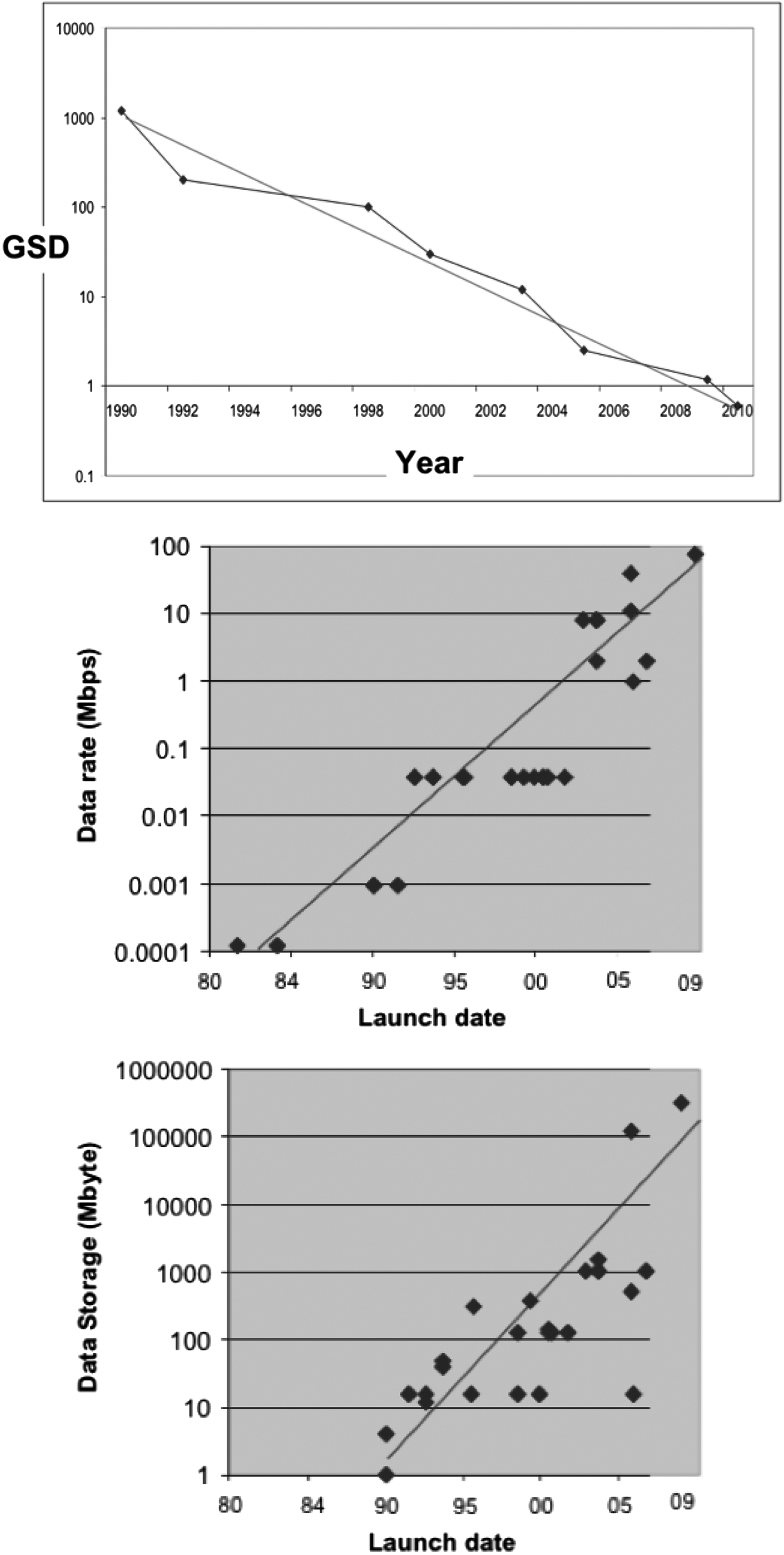

NewSpace in EO hence derives much of its inspiration from three decades of cost-effective and technology approaches to the development of satellites. It is worthwhile to note interesting observations made by Professor Sir Martin Sweeting (Fig. 1) of the close relationship of parameters such as ground sampling distance (GSD), data rate, and data storage, having a very close association with Moore's law. One could argue that the cost of satellites themselves has possibly followed the same trajectory (given the same GSD) because of factors such as reliability of COTS electronics and the decrease in launch prices.

Moore's law observed in small satellites.

Historically, the first of such major successful ventures in turning research into low-cost development of spacecraft for commercial exploitation is Surrey Satellite Technology Ltd (SSTL). SSTL aligned its business models based on capacity building for nonspace-faring nations and that emerged as a leader in the small satellite industry.

What NewSpace has done very successfully is to provide a “fundable” touch to the traditional developments (of cost-effective spacecraft development) in the small satellite world, taking advantage of gaps in traditional EO business models as well as the increase in computing capabilities fast forward 30 years from the 80 s.

The advent of CubeSats has also played a snowballing role in the interest generated by students and engineers and has turned the academic/research interest into development of NewSpace EO ventures. The most well-known example of this is of Planet Labs, which has flown >100 satellites based on CubeSat standard, and is the largest funded startup in the NewSpace EO community with $183 million in multiple series of funding. 5

Advent of Newspace Commercial EO

Table 1 provides a list of NewSpace EO companies that have flown or announced plans for a constellation of satellites for EO. One of the reasons why NewSpace EO has been so successful in raising capital may well be because it challenges traditional space enterprises at technology implementation, deployment of assets, innovation in the business model, etc., with the value proposition of opening up of new mass markets across the world. NewSpace commercial EO definitely has a value proposition that is quite unique in these counts against that of traditional EO space companies.

List of NewSpace Imaging Satellite Constellations

HS, hyper-spectral; M-IR, mid-infrared; N-IR, near-infrared; SAR, synthetic aperture radar.

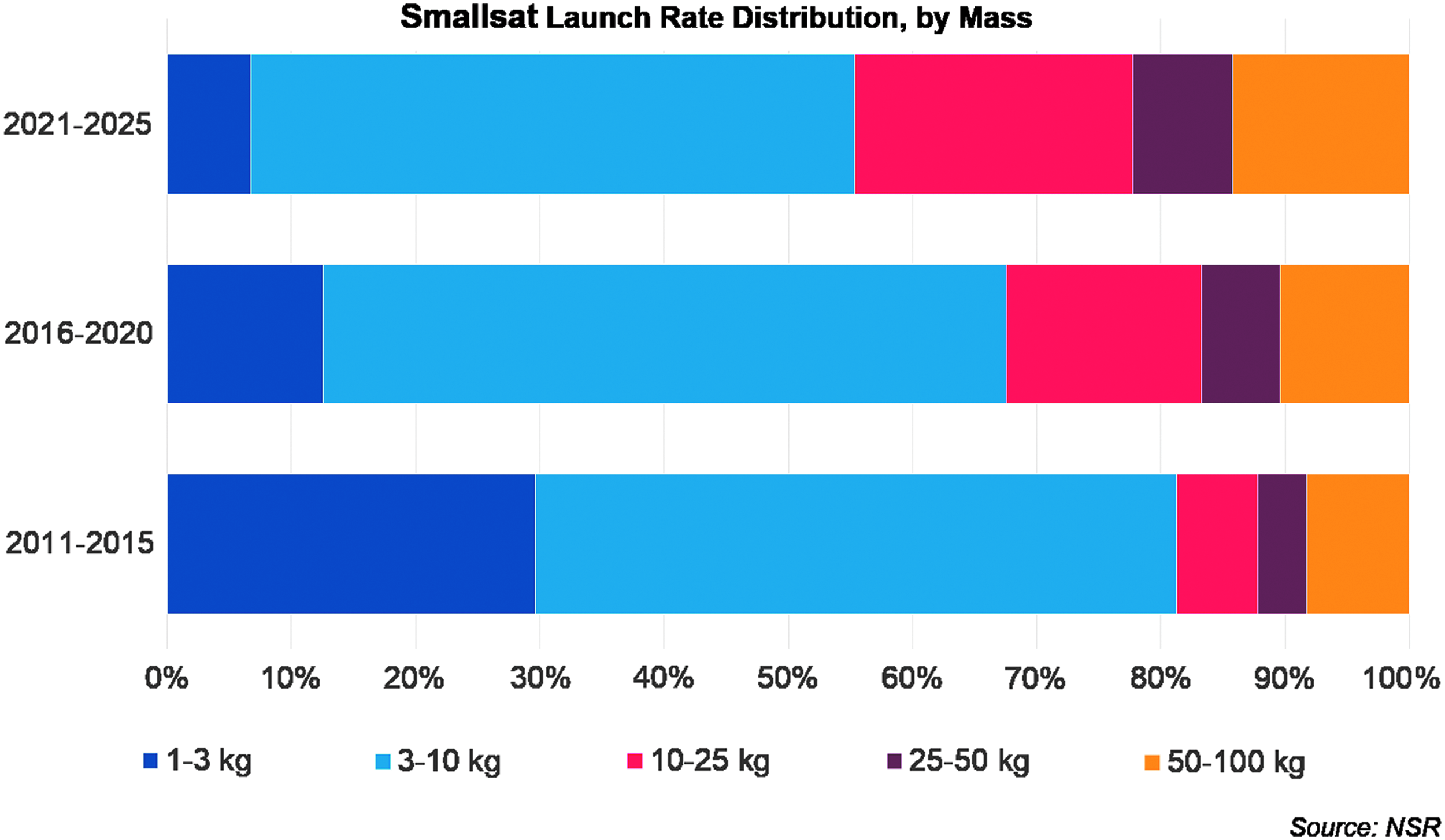

However, we are of the view that NewSpace EO models can complement traditional space business models and not disrupt them completely. From an attribute point of view, small satellites may be able to achieve similar quality output in future as the current set of large satellites. But the model for doing a satellite EO business does not drastically change because of a similar kind of customer needs for both NewSpace and traditional business models. Spatial and temporal resolution are both equally important today, and small satellites are filling the gap when it comes to temporal resolution, because the size of optical instruments will always be constrained on smaller platforms. Economics drives business model strategy, and hence a combination of small and large satellite-based imaging services (Fig. 2) is what we will be seeing in future, with National Geospatial Agency (NGA)'s decision to have both medium-resolution planet data and very high-resolution DigitalGlobe data being an example from the current industry trends.

Smallsat launch rate distribution by mass (source: NSR). Color images available online at www.liebertpub.com/space

To understand this, we explore some of the key differences and challenges that emerge between NewSpace and traditional EO satellite companies. Some of the key differences between NewSpace EO models and traditional EO business models include the following.

• Financing of EO satellites has been extremely challenging without anchor customers and, therefore, governments were acting as anchor customers to mitigate the risk of investors. NewSpace business models are mostly financed by private capital without significant anchor customer signings against the promise of mass market sales of EO products and services. Very few NewSpace companies have such sugar daddy deals. The promise of several NewSpace EO satellites is in opening new markets with disruptive pricing models.

• One of the key parameters in availability/service that NewSpace is addressing is the issue of revisit. Traditional EO satellite companies have very few assets in space that can offer revisit from a few days to even sometimes weeks. NewSpace bets big on cost/satellite and, therefore, the pitch is aligned toward providing better on-orbit availability of satellites for on-demand imaging. Some NewSpace EO companies have gone on to propose hourly/less than hourly revisits. Given the inherent constraints of optical data, the key question would be the need in the industry verticals using EO data for such frequent data. We note that the price of the data for the customer depends on both spatial and temporal resolution. Less than hourly revisits will become an expensive commercial product, which is the exact same reason that the NewSpace satellite EO industry wanted to address when it started earlier this decade. However, there are certain applications that do need such persistence, and are also having deep pockets like the government and military sector, which has traditionally been the life support of the satellite EO industry. Financial sector is an example, with commodity trading and insurance being two key areas wherein such high revisit frequency could potentially provide a lot of value.

• Traditional EO satellite data costs stand at >$10/sq km (for high-resolution satellites of ∼1 m) and can easily cost up to $50/sq km for sub 0.5 m images. They also come with tags of minimum order quantities. NewSpace EO companies rightly challenge this business model. However, the larger question is by how much. NewSpace companies have gone on to make announcements of $1/sq km pricing for fresh imaging, which if delivered is an order of magnitude less than current market practices.

• Several of NewSpace companies also plan to provide end-to-end products for several end-user applications. The pitch is to provide analytics solutions from the big data obtained from their assets in space. Traditional EO enterprises have normally provided raw images or done some basic levels of postprocessing and leave the end users of their imaging products to build derivatives on top of them.

• At an operational level, most NewSpace EO constellations are looking toward CubeSat standard-based architectures with on-orbit life ranging anywhere between 6 months to a couple of years, whereas some of them have built/proposed microsatellite platforms with lifetimes of up to 5 years. Resolution becomes the key factors in deciding the form factor and the size of the satellite. Planet Labs has pioneered medium-resolution satellite imagery of 3–5 m on a standard 3 U CubeSat form factor. Similarly, Space Systems Loral is building SkyBox's (now Terra Bella) latest satellites within a 120 kg microsatellite platform with a lifetime of up to 5 years. 6 Resolutions planned have a major say in the aperture size and, therefore, the overall size of the satellites. These constellations are definitely cost effective considering the several hundred million dollars cost of traditional EO satellites.

Challenges for Newspace Commercial EO

Although there is a lot of enthusiasm with which the venture capital community has funded several of the NewSpace commercial EO companies, we argue that the fundamental value proposition from a service standpoint for their basis is price/km and on-demand availability of satellites. However, given the limitations in imaging because of fundamental physics, most NewSpace commercial EO offerings shall be limited to range around ∼1 m, whereas traditional EO satellites are organically moving toward <0.5 m. Therefore, the competition between NewSpace companies themselves is tending to look more fierce than NewSpace versus traditional EO or the competition between traditional EO companies themselves.

To illustrate this further, it is important to understand the loyalty of anchor customers to traditional EO companies. The price of satellite imagery increases orders of magnitude between very high resolution (0.3 m), high resolution (1 m), and medium resolution (3 m+), and most of the top-of-the-chart customers are likely to be militaries/security-related organizations, who are already likely to be anchor customers. Although some of the NewSpace commercial EO companies have announced some form of anchor customer relationships, turning anchor customers of traditional EO companies may be extremely challenging, given the fact that their thrust for better resolutions is quenched by the traditional players. Recently, NewSpace commercial EO has witnessed some consolidation with a couple of acquisitions. This may be an important step and effort for NewSpace EO companies in acquiring customers. Therefore, it is vital for NewSpace commercial EO companies to deliver on the count of opening up new mass markets in sectors such as industrial monitoring, agriculture and environment, utilities, and marine transportation analytics.

It is not evident whether such an upstream–downstream structure of several of the NewSpace players (building both satellites and the analytics platforms) is commercially viable. Recently, space data-based analytics companies themselves have gone on to raise tens of millions of dollars in financing, which suggests that building analytics platforms for different industry verticals in downstream may themselves be initially capital and manpower intensive. Therefore, the question of having the bandwidth to do so versus remaining lean comes into the picture for NewSpace EO companies planning such a business model. This may well be one of the linchpins in the Google acquisition of SkyBox Imaging. Google invested in SkyBox (Terra Bella) for its “sensor in the space” offering, so that it could test its machine learning platform to derive insights from the data being generated, and run analytics. The fact that Google divested from Terra Bella goes on to support the arguments made by us that vertical integration in NewSpace satellite EO domain has necessitated the definition that a firm would need to make about its position in the industry value chain.

Although some of the NewSpace companies have published results of their imaging products, there are no substantial studies that are publicly available on the comparison of imaging products. There is definitely room to study the usability of data from NewSpace EO against traditional EO satellites for various downstream industry verticals to capture the entire scope of the possibility of NewSpace EO companies disrupting the market share of traditional EO satellites.

Another important aspect of increasing the utility of space data that remains largely in unchartered waters is the ability to sensor fuse. NewSpace EO companies have announced plans for satellites of different resolutions and bands providing a mix in the kind of data they can offer. However, from a downstream utility perspective, there is a need to support and accelerate the possibility of sensor fusion for commercial markets, for example, developing analytics solutions to combine automatic identification of ships data with that of synthetic aperture radar and ground-based observations. There is a need to explore such possible convergence of commercial EO data.

Conclusions

The potential of using small satellites for commercial EO has successfully appraised the investment community into enabling NewSpace enterprises to launch several constellations like never before. Several of these constellations aim mostly at provisioning data at revolutionary costs and at never-before-achieved revisit periods. On one hand, these NewSpace enterprises are looking to disrupt the traditional EO data markets, and on the other, they are targeting either creation/support for big data analytics platforms through these constellations and opening up new markets for EO products.

Warnings have been sounded by industry leaders 7 and investors 8 of a possible bubble with the need to promote real business plans for real markets. 9 In the next 5–10 years, will there be an oversupply of EO data or is there a shortfall in supply of market-relevant data? We believe that both traditional EO companies and NewSpace commercial EO companies are here to stay. However, it is unlikely that all NewSpace constellations shall turn out to be commercially viable. There is a need for NewSpace entrepreneurs to revisit their strategies and possibly think along the lines of the other addressable gaps including some of them mentioned in this article.

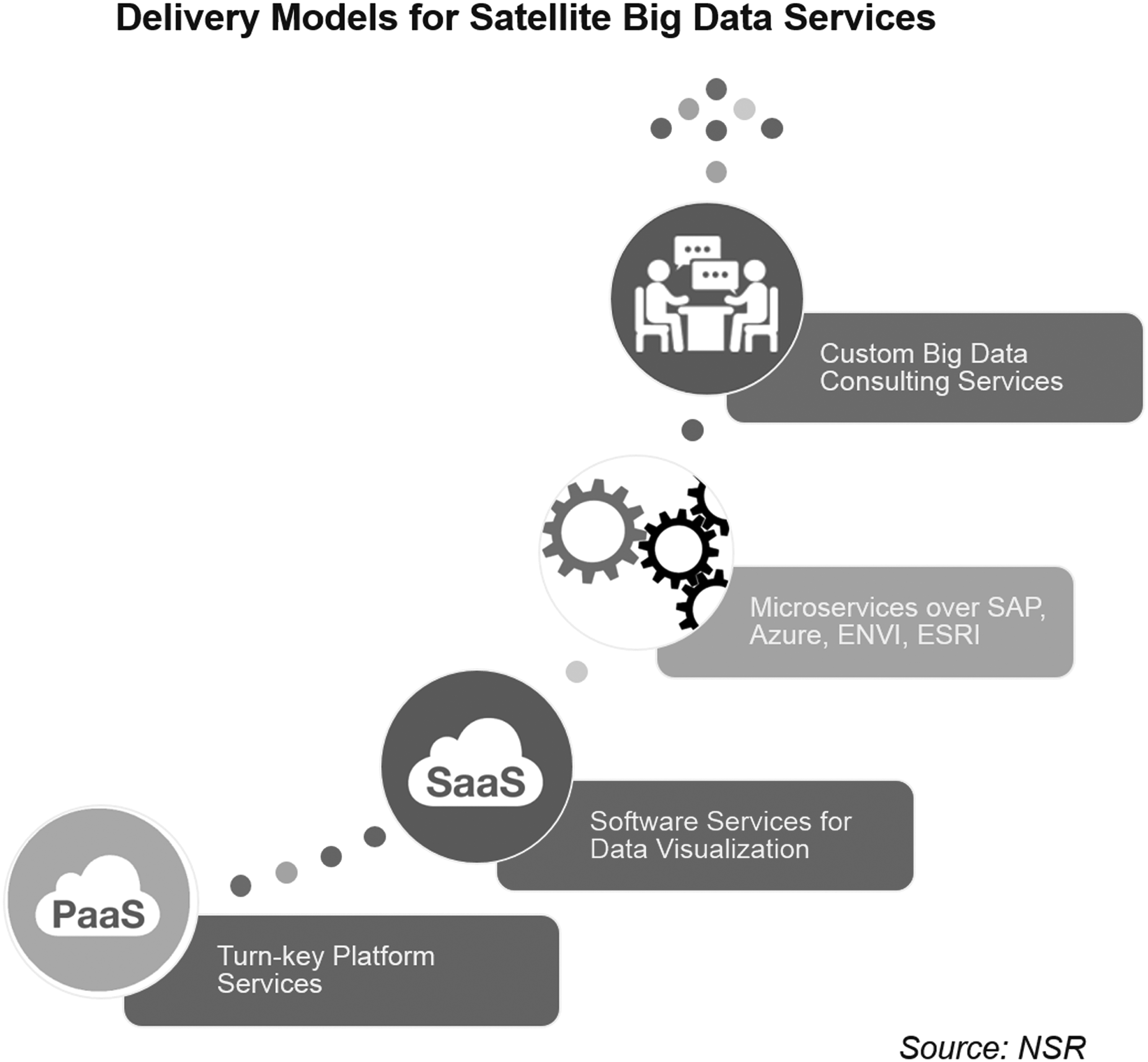

It is important to note that strategy for upstream and downstream NewSpace companies will be different and consolidation is imminent across the value chain (Fig. 3) to eliminate the inefficiencies, but focus should be initially on the core product—the satellites and the data produced by them, or the data valorization by creating a delivery platform and adding analytics. From an investment vantage point, capital raising process should be reflected by revenue-driven valuation, and not faux valuations based on inflated market data.

Delivery models for satellite big data services (source: NSR).

We believe that there is significant value to be generated for downstream end users by not just relying on satellite data but rather combining satellite data with other sources such as ground sensors, aerial sensors, and socioeconomic data to generate valuable insights that add to the increase in the overall decision making of the end users.

Footnotes

Acknowledgments

We are thankful to Sir Martin Sweeting, Prateep Basu, and Nothern Sky Research for their insights on shaping up our analysis and conclusions.

Author Disclosure Statement

No competing financial interests exist.