Abstract

Abstract

According to Wikipedia, “NewSpace” is an umbrella term for a movement and philosophy that is often affiliated with, but not synonymous with, an emergent private spaceflight industry. Specifically, the term is used to refer to a community of relatively new aerospace companies working to develop low-cost access to space or spaceflight technologies and advocates of low-cost spaceflight technology and policy. * Although this description may be arguable, the emergence of numerous start-up space ventures within the past 15 years is a fact. These start-ups cover diverse areas such as satellite communications, Earth observation, launchers, manned spaceflight and space tourism, or even energy from space as well as resource gathering in space. Companies have attracted more than $13.3 billion of investment, including $5.1 billion in debt financing, since 2000. More than 80 angel- and venture-backed space companies have been founded since 2000. Eight of these have since been acquired, at a total value of $2.2 billion. † The NewSpace movement has so far been focused, to a great extent, on the United States, namely the West Coast. Mojave in California has been dubbed “the Silicon Valley on NewSpace,” being home to several of these commercial space enterprises. The German Federal Ministry for Economic Affairs and Energy (BMWi) has launched a study for understanding the driving forces behind the NewSpace ecosystem and related chances and challenges for Germany and Europe. The study, which was conducted by SpaceTec Partners and BHO Legal of Germany, shows that at least four factors are of immanent importance for a NewSpace ecosystem to create market-driven products and services. These factors are related to: (1) Business Philosophy—creating and living an entrepreneurial spirit; (2) Financing—access to early stage risk capital and venture funding; (3) Technology Management—focus on spinning-in technologies and Information and Communication Technology processes; and (4) Framework Conditions—favorable political and legal conditions supporting commercialization. This article summarizes the insights gained and the lessons learned from success stories and failures in NewSpace. It presents the recommendations for strategies as to how NewSpace can be successful in Europe and, in particular, in Germany. Given the growing relevance of NewSpace, these insights are of high interest to stakeholders and decision makers worldwide.

Introduction

The space strategy of the German Federal Government of 2010 identified the main trends in the international space sector and in its guidelines set important priorities for the positioning of Germany. As such, it already took into consideration the impact of the U.S. space policy on the intensified commercialization and government use of private providers for carrier systems and satellite services, as well as the observation that commercialization is making fast progress, particularly in the United States. It is this foundation of new companies with a high private capital deployment, the use of new technologies and approaches, and the convergence with the information technology (IT) sector that are forming the basis for what has been referred to for some time in the professional world as “NewSpace.”

NewSpace has numerous facets, ranging from offering established services such as satellite communication and geoinformation, the manufacturing of Smallsat systems and components, positioning, navigation and timing, the operation of new launch systems to emerging business models that are centered on services related to the Internet of Things (IoT), debris mitigation, satellite servicing, manufacturing in space, energy from space, and the mining of asteroids to name but a few. Figure 1 provides an overview of today's diverse and most economically important business fields of the traditional space industry and various NewSpace business models. As can be seen by the time axis extending to the right, NewSpace is gradually developing new commercial fields beyond the traditional commercial space sector.

Current and future NewSpace Business Fields. COM, communication; EO, Earth observation; FSS, fixed satellite services; GEO, geostationary equatorial orbit; IoT, Internet of Things; LEO, low Earth orbit; MEO, medium Earth orbit; MSS, mobile satellite services.

The study is part of an action plan of the German Federal Ministry for Economic Affairs and Energy (BMWi)/DLR Space Administration, Federal Association of the German Aviation and Space Industry (BDLI), and the German Industrial Union of Metalworkers (IG Metall) to review the German framework conditions in the face of current and future developments—in particular, the rapid development of the commercial space industry in the United States.

With this study, the Federal Ministry for Economic Affairs and Energy has taken up the NewSpace thread. In an effort to better understand the driving forces behind NewSpace and thus to generate advantages for the German industry, the study was to examine the following areas:

Business and finance models of NewSpace in context; Approaches for using the resultant opportunities for the German industry; and The requisite framework conditions and political fields of activity.

The study “New Business Models at the Interface of Space and digital Economy” was finally commissioned by the BMWi and conducted by SpaceTec Partners and BHO Legal of Germany, in the timeframe from Autumn 2015 to Spring 2016.

Success Factor Dimensions for Newspace

The commercialization of the space sector is rapidly advancing—particularly in the United States. Over the past 15 years, numerous space ventures emerged, covering diverse business areas such as satellite communications, Earth observation, launchers, manned spaceflight and space tourism, or even energy from space as well as resource gathering in space.

Although some of the business concepts are not new, the pace and success rate with which these start-ups acquire their financing is. The dimension of the financial attractiveness is demonstrated by the fact that these companies have attracted more than $13.3 billion of investment, including $5.1 billion in debt financing, since 2000. More than 80 angel- and venture-backed space companies have been founded since 2000. Eight of these have since been acquired, at a total value of $2.2 billion. ‡

The NewSpace movement has so far been focused, to a great extent, on the United States, namely the West Coast. Mojave in California has been dubbed “the Silicon Valley on NewSpace,”

§

being home to several of these commercial space enterprises. In aiming at understanding the driving forces behind the NewSpace ecosystem and the related chances and challenges for Germany and Europe, SpaceTec Partners and BHO Legal have found out that at least four factors are of immanent importance for a NewSpace ecosystem to create market-driven products and services. These factors are related to (refer to Fig. 2):

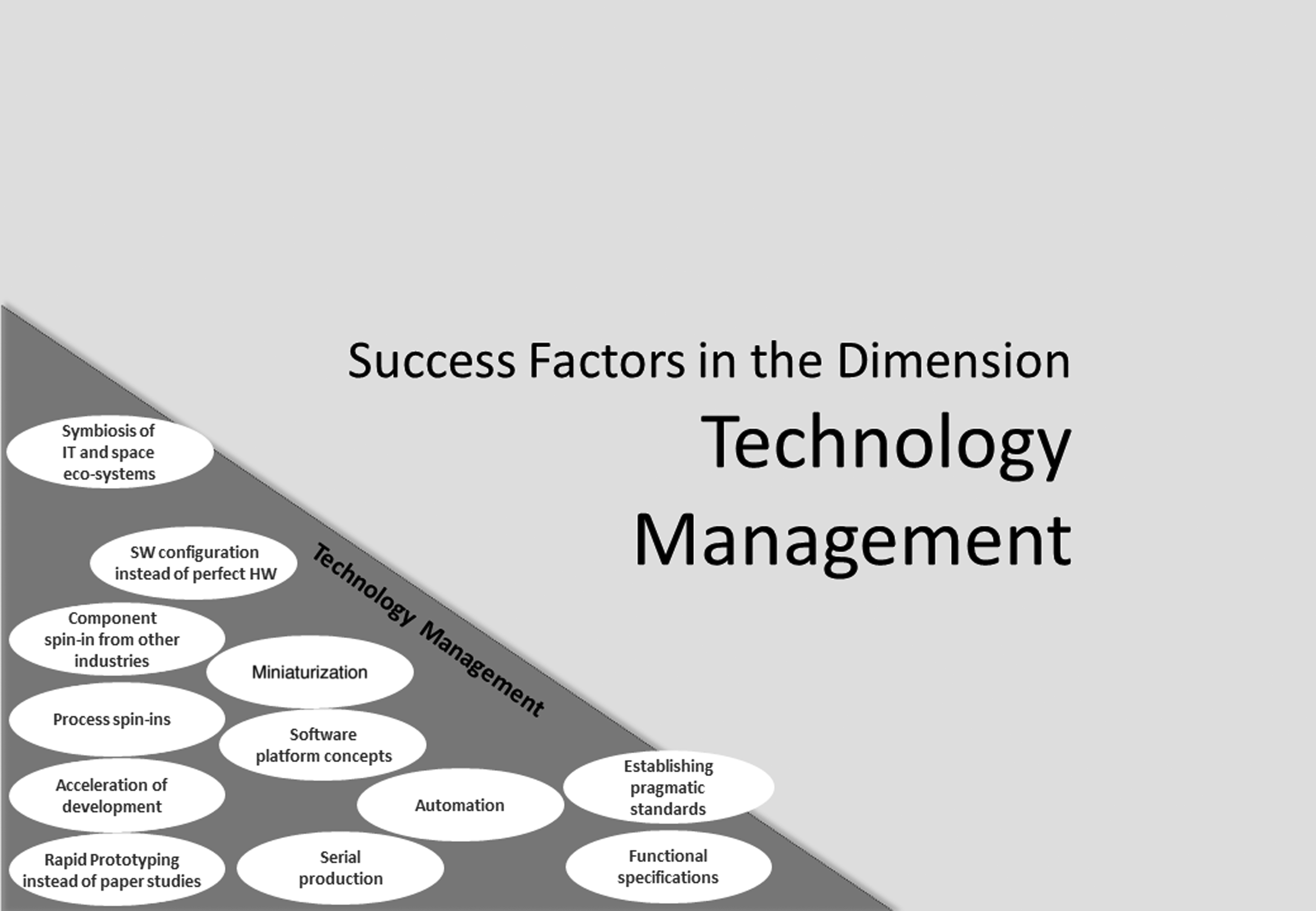

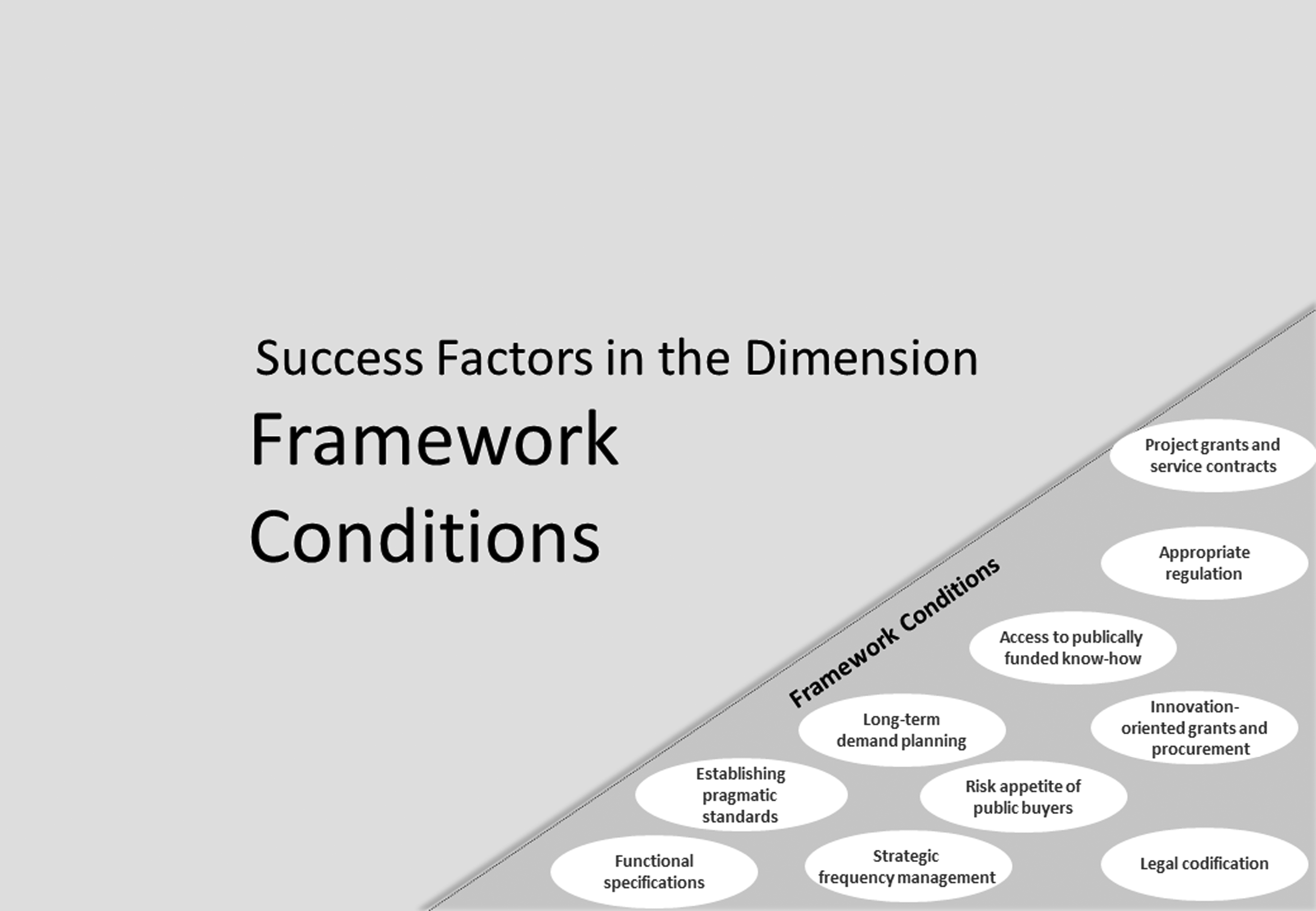

Business Philosophy—creating and living an entrepreneurial spirit (Fig. 3); Financing—access to early stage risk capital and venture funding (Fig. 4); Technology Management—focus on spinning-in technologies and Information and Communication Technology (ICT) processes (Fig. 5); and Framework Conditions—favorable political and legal conditions supporting commercialization (Fig. 6).

NewSpace success factors relevant for Germany.

Business Philosophy—Success Factors.

Financing—Success Factors.

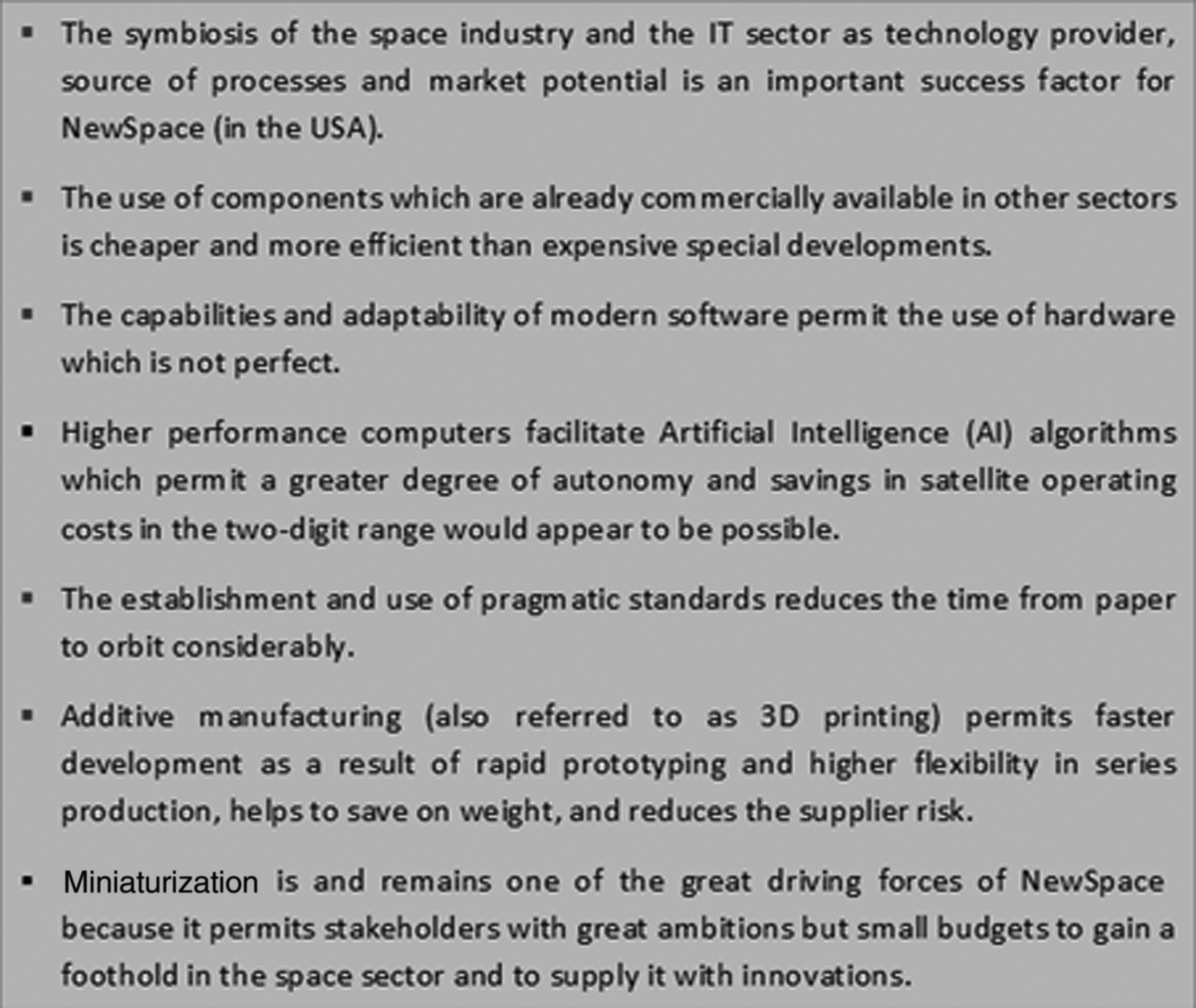

Technology Management—Success Factors. HW, hardware; SW, software.

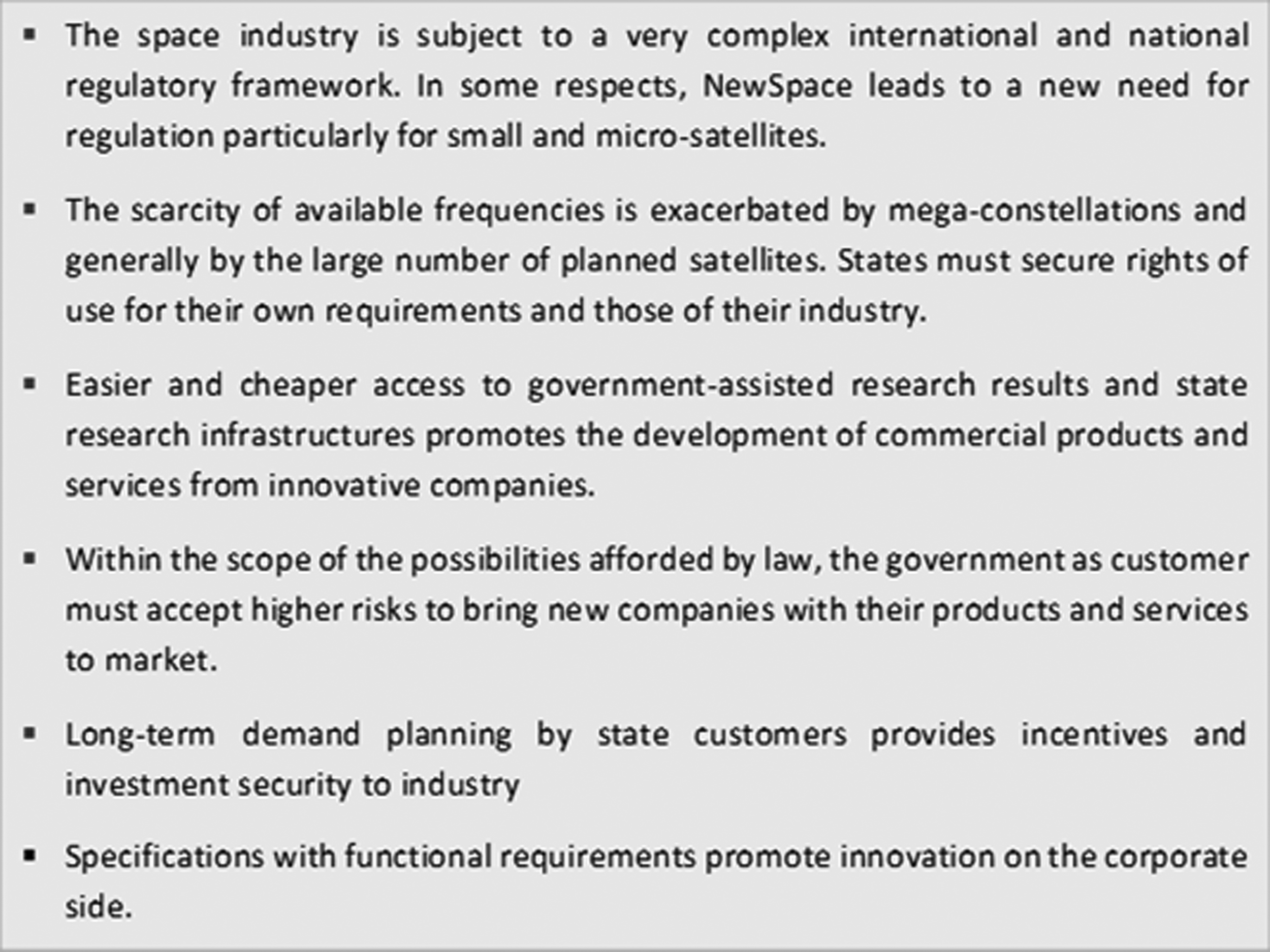

Framework Conditions—Success Factors.

These four success factor dimensions have been prepared iteratively and used throughout the study. In detail, 37 success factors have been identified, described, and analyzed in terms of their relevance for Germany (the white bubbles within Fig. 2)—we will discuss the most important factors in the following pages.

Opportunities Presented By Newspace Trends

NewSpace is driven both by new markets for services and applications and by the development of disruptive technologies and products. However, the focus is not placed on technologies as they are in the traditional space industry but on the market success that is expected for innovative applications.

Many founders of the American NewSpace companies come from the IT industry and use the experience and financial means generated from their previous start-ups. Their business philosophy is characterized by the focus on developing products and services in line with demand, challenging the status quo, promoting innovative ideas out of the box, strictly adhering to costs, and on company locations, which are attractive to highly qualified employees from all over the world.

The increasing convergence of space with the IT sector is reflected at several levels: On the one hand, the IT sector is producing great demand for global systems and services to cover the demand for broadband, for the IoT, for location-based services, or for Big Data. On the other hand, business models (e-commerce), services (cloud computing), and approaches (agile software development) are being transferred from the IT to the space sector.

Preference is given to producing critical elements in-house while remaining open to sharing ideas according to the “Open Source” principle if there is a strategic benefit. In the same way as IT, technical solutions are sought for scalable business models. Instead of insisting on customized and therefore expensive individual products—as is typical for the space industry—commercially available components are utilized wherever possible, for example, from the aviation or automotive sector.

One characteristic of the entrepreneurial initiative of the stakeholders is the willingness to assume the risk of initial funding. The foundation for this is provided by the physical proximity to venture capital (VC) investors, who provide the main share of funding. Government aid is also leveraged, for example, export loans from state-owned banks, long-term service contracts with authorities or purchase guarantees, traditional R&D grants, the transfer or use of state infrastructures, and tax relief offerings.

The legal framework conditions that are geared toward commercialization and reviewed for efficacy in short cycles constitute a favorable aspect in the United States. After commercialization of satellite communication and Earth observation was regulated at an early date, the Space Act 2015 represented a further step, preparing the way for commercial projects aimed at the extraction of raw materials in space.

A characteristic feature of NewSpace companies is the primary alignment of their business model to market opportunities. These result from:

Institutional customers such as space agencies, security authorities, or the military; New private customers, primarily from the ICT sector, and increasingly also from other industrial sectors; Global data networks, broadband coverage, and the IoT; Geo-information services for applications in the private sector, for example, in the insurance sector or in the oil and gas industry; Big Data applications that capture data with the assistance of satellites; and Autonomous systems that are based on satellite navigation and communication for the purposes of steering and control.

Newspace Success Factors of Relevance for Germany and Recommended Actions

Our analysis of the trends and drivers of NewSpace showed that the U.S. model cannot be transferred 1:1 to Germany. The differences in the characterization of the four success factor dimensions are simply too great—later, we will take a closer look at the differences as well as the commonalities.

Business Philosophy: Promoting More Entrepreneurship

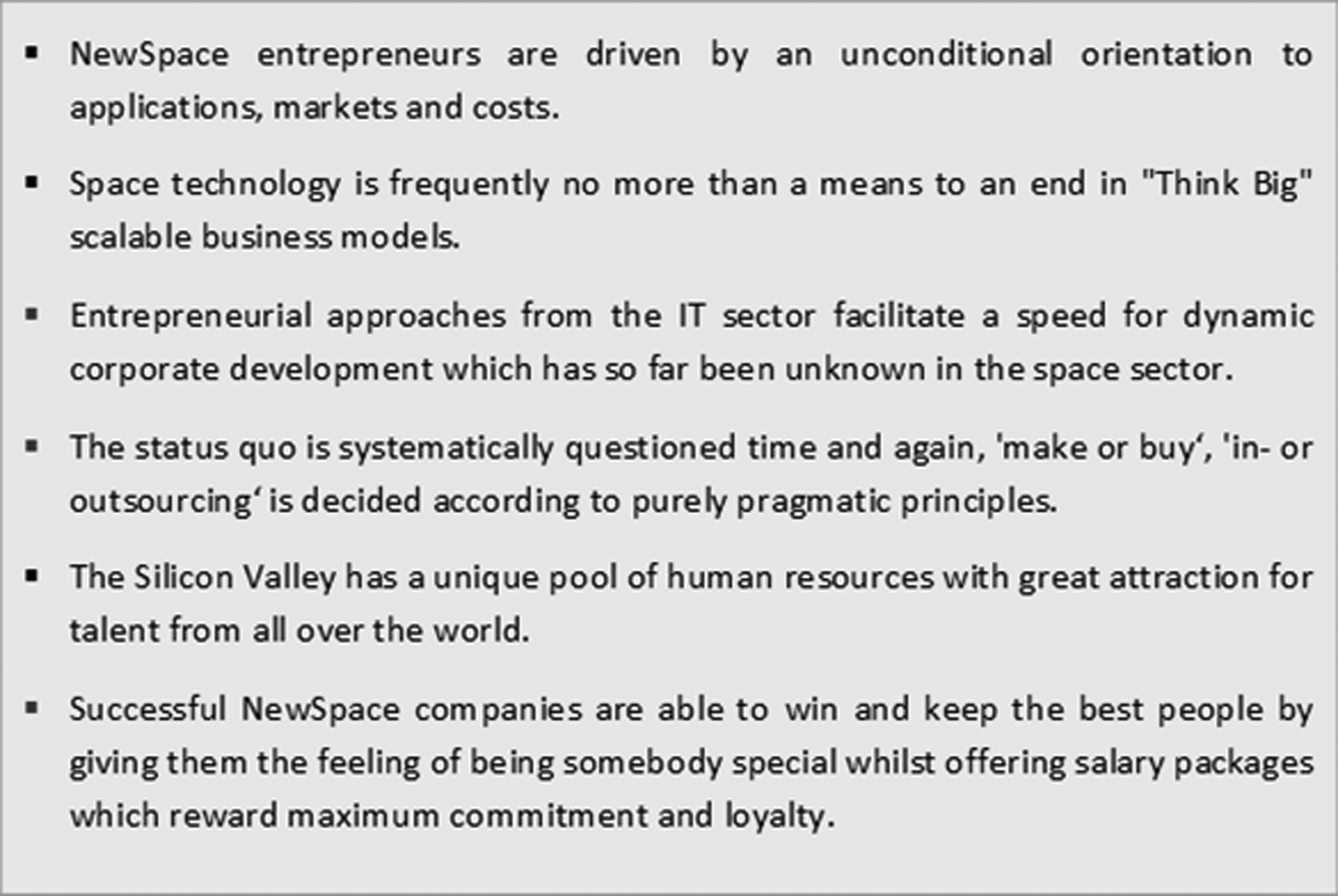

The North American NewSpace eco system à la Silicon Valley is unique in terms of entrepreneurship, innovation, willingness to take risks, HR policy, communication culture, and global market ambitions (Fig. 7). Germany lacks the entrepreneurial spirit to break free from the traditional system and to systematically focus on new markets and customers.

Business Philosophy—Key Take-Aways. IT, Information Technology.

There are also hardly any founders or investors from other industries due to the rigidity of the space sector and the required high initial investment. The species of the “Serial Entrepreneur” are not very widespread in Germany (and Europe). The “business philosophy” dimension will be difficult to emulate for the German space industry, let alone replicating it. However, sooner or later, it will have to react to the approaches and cost pressure of NewSpace.

The accelerated commercialization of space needs new entrepreneurial spirit—among all parties concerned: in the established space industry, in young companies, and also in relevant institutions. Entrepreneurship cannot be prescribed by the state; but the state can provide incentives and create framework conditions for the successful formation of new companies and the development of new markets. Industries must adapt to the market situation that has altered by digitizing space and develop an understanding for NewSpace customers or their markets (e.g., the internet economy). Only in this way can new customer groups be won.

A start-up ecosystem can support young companies, spin-offs, and technology transfer, and promote a culture of entrepreneurship. More dialogue with the entrepreneurs in the IT and internet industry and the strong industrial software sector could provide a new stimulus for NewSpace in Germany.

Institutions supporting NewSpace and wishing to use the new possibilities should provide the new companies with entrepreneurial leeway to develop creative solutions instead of confronting them with technical specifications down to the very last detail. New possibilities provided by budgetary and procurement law should also be exploited here, including the use of contractual drafting options.

Financing: Crating Financing Attuned to NewSpace

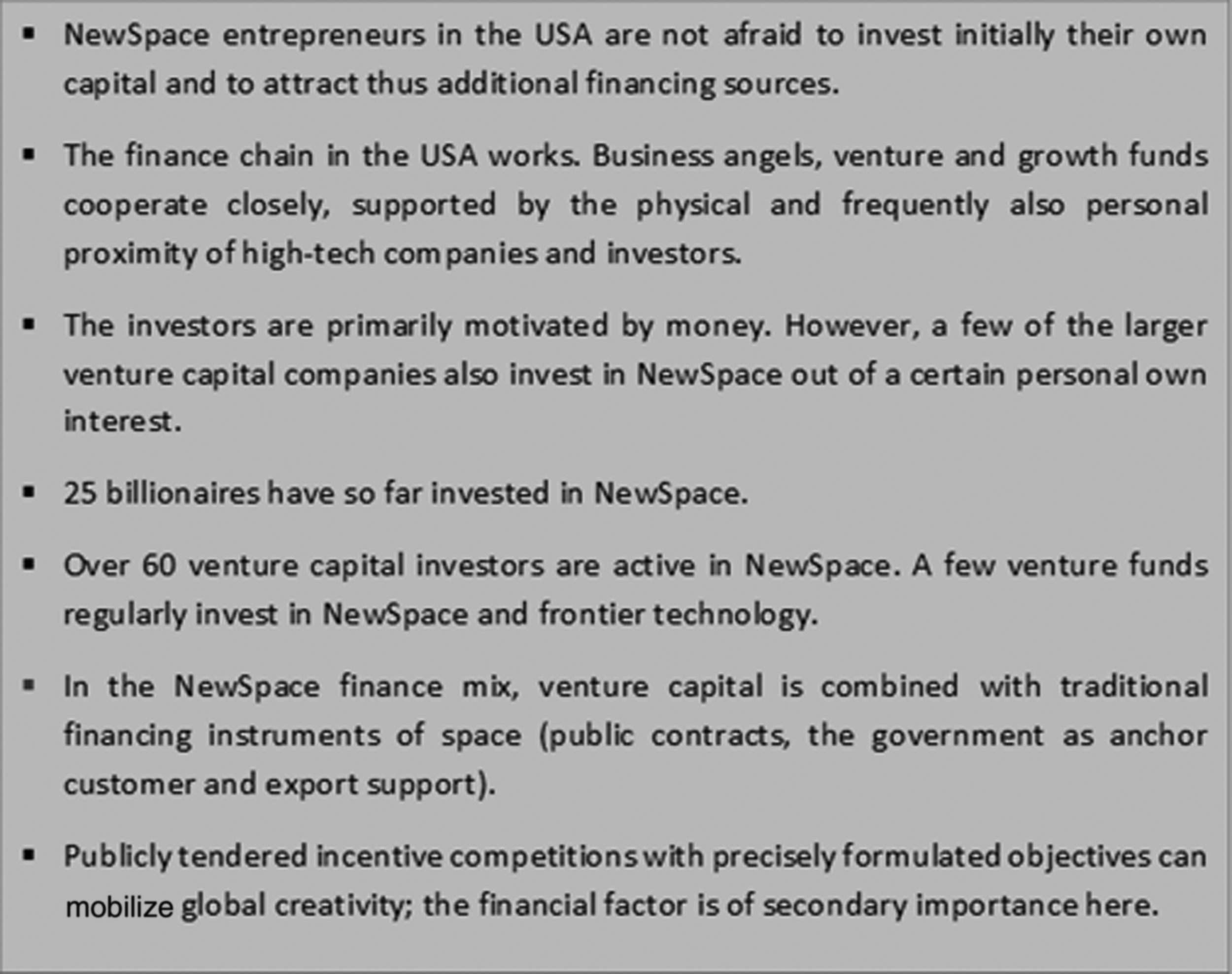

The possibilities provided by the combination of wealthy entrepreneurial personalities and well-networked VC investors in the Western United States, supported by a space policy oriented to commercialization and the huge demand from the military and security authorities, are extraordinary. Spectacular success stories (SkyBox, SpaceX, etc.) are attracting new founders, incentivizing the VC scene and facilitating the financing of so-called “disruptive” technologies and business models (Fig. 8).

Financing—Key Take-Aways.

A comparable continuous finance chain with a fast and risk-taking decision culture does not yet exist in Continental Europe. For German banks, space is fraught with risk and is exotic per se; the long development and project cycles deter the few private lenders that exist. Although VC companies are highly committed in the United States, little of this commitment is noticed in Europe.

Germany has a unique density of initiatives for the early phase, diverse high-tech hotspots, and powerful state banks. This provides the potential to support NewSpace in diverse ways and to gradually close financial gaps. The aim should be to tap a broader pool of entrepreneurs while at the same time creating a continuity in financing by multipliers advocating the “NewSpace idea” at every level of financing: prominence among Business Angles, systematic use of existing (semi-) state early phase investors, and strengthening of the VC ecosystem through specialized funds. State guarantees and well-prepared model examples could help to mobilize the banking industry for space topics.

Project funding in NewSpace should be provided in proximity to the market, for example, by financing of targeted projects that promise a successful entry to markets. Instruments such as inducement prizes can additionally promote innovation while at the same time sparking a broad-based effect. To maintain the export strength of the German space industry and extend it to NewSpace, international competitive disadvantages due to a lack of export finance instruments should be avoided. An institutional unit that is responsible for the export development of German companies could be beneficial here.

Technology Management: Living Digitalization

NewSpace is not so much about developing new technologies but rather about systematically implementing business models and approaches of the ICT sector (“patching and releasing”), making use of tried and tested products from other areas of technology (“spinning in”), and focusing on market opportunities (“surfing the trend wave”).

With NewSpace, the cards in the space industry are being reshuffled. A supplier of today can have system competence tomorrow and rise to be a global player. The strict market orientation of NewSpace permits growth of a kind that is so far unknown in the space industry (Fig. 9).

Technology Management—Key Take-Aways.

Global internet companies (Google, Amazon, etc.) with the imagination to inspire new business opportunities are absent in Europe and Germany. By contrast, we have possible synergies with other sectors (automotive, mechanical engineering, etc.), among which Germany leads the world. Intelligent transport systems, self-driving cars, and the IoT offer huge opportunities. It is important to act quickly here. The effects of scale of NewSpace go hand in hand with large hurdles to market entry if one or two companies have already filled a niche.

To be successful in NewSpace, the German space industry should open up to innovations and processes from other industries and be consistently guided by application and customer requirements. More than technology is required here. Speed is decisive to be successful in the competitive environment of NewSpace. Runners-up today may not even have a market tomorrow.

In view of the rapid technological and market developments with shorter generation cycles, development must be accelerated and closely interlinked with production. The requisite instruments—rapid prototyping, agile software models, and three-dimensional printing technology—are available.

This type of thinking may be new for traditional space companies, but it has already become established in other sectors. An overarching exchange is, therefore, necessary throughout industries, which should go in both directions, including mentoring by non-space companies and also incorporating applications-oriented NewSpace promoters in Industry 4.0 working groups. This permits an out-of-the-box approach and promotes innovation that can be successful in the market.

Framework Conditions: Securing Competitiveness

Both the political and the legal frameworks for the commercialization of space were put into place in the United States back in the 1980s. Private operators of communication satellites were established, thereby breaking the worldwide monopoly of the international satellite organization Intelsat. As a next step, Earth observation was opened to private companies. Through long-term service contracts, the U.S. authorities enabled companies such as DigitalGlobe to maintain the capital to develop and maintain efficient commercial Earth observation systems. The Space Act 2015 set the legal framework for further commercialization, primarily with launch systems, space tourism, and the exploitation of raw materials in space. The strict export control law was amended to strengthen the international competitiveness of U.S. companies. The government credit institution Export credit agency of the United States (EXIM) is used to support large export deals of U.S. companies. Some European countries have already reacted to NewSpace in terms of legislation, particularly with respect to the adjustment of approval procedures, liability regulations, and insurance duties for small and micro-satellites (Fig. 10).

Framework Conditions—Key Take-Aways.

Future German space legislation could provide the foundation for new commercial systems and the establishment of NewSpace companies. Orientation is provided by the recent amendments to space legislation in other European countries. Liability and insurance duties are to be structured such that they do not inappropriately disadvantage national industry by European and international comparisons and also include provisions for small and micro-satellites from the outset.

Based on the German Space Strategy and measures already taken, such as the Components Initiative of the German Space Agency, there should be a firm export strategy that also considers NewSpace. Tried and tested measures established in other industrial areas (delegation trips, representation at international trade fairs, bilateral cooperation agreements) should be used selectively and be specifically aligned with NewSpace. American and French companies have achieved visible competitive advantages through the massive support of EXIM and Coface. Thought should be given as to whether and how German institutes for the promotion of exports (Kreditanstalt für Wiederaufbau/German Reconstruction Credit Institute) can be effectively used to facilitate exports of the German space industry.

Germany must be in a position to obtain adequate licenses from the International Telecommunication Union for future public and commercial satellite systems. The scarcity of suitable frequencies is intensified due to the large number of registrations for new mega-constellations. German licenses should be maintained and extended where possible.

New innovation-oriented support and procurement instruments (Pre-Commercial Procurement [PCP], Public Procurement of Innovation Solutions [PPI], innovation partnership) should be tested in the space sector. ** They can contribute to ensuring that new products and services are geared to the specific requirements of public customers and reach the market from the prototype stage without having to go through the “valley of death.” Public customers can selectively control research and development in terms of their future requirements. Long-term and reliable planning is, therefore, called for.

A systematic aggregation of public demand for satellite-based services in Germany could be an important stimulus for commercialization. Through common or coordinated procurements, a critical size could finally be achieved in which companies selectively develop and offer services to meet the requirements. Long-term service agreements according to the American National Geospatial-Intelligence Agency (NGA) model would establish national authorities as anchor customers for German companies.

For new companies in the start-up phase, it may be important to be able to use the infrastructure existing in research institutes for test and validation purposes, for example, without excessively high administrative hurdles and costs. This has been given particular emphasis in a recent study for NASA.

Newspace As the Link Between Space Strategy and Digital Agenda

New space applications offer broad fields of use in other sectors. In the industrial IoT, NewSpace could win new groups of customers with more secure communication, surveillance, and navigation systems, precisely also for safety- and security-critical applications. In cooperation with Industry 4.0, Germany has the unique opportunity to counter the U.S. NewSpace with something of its own.

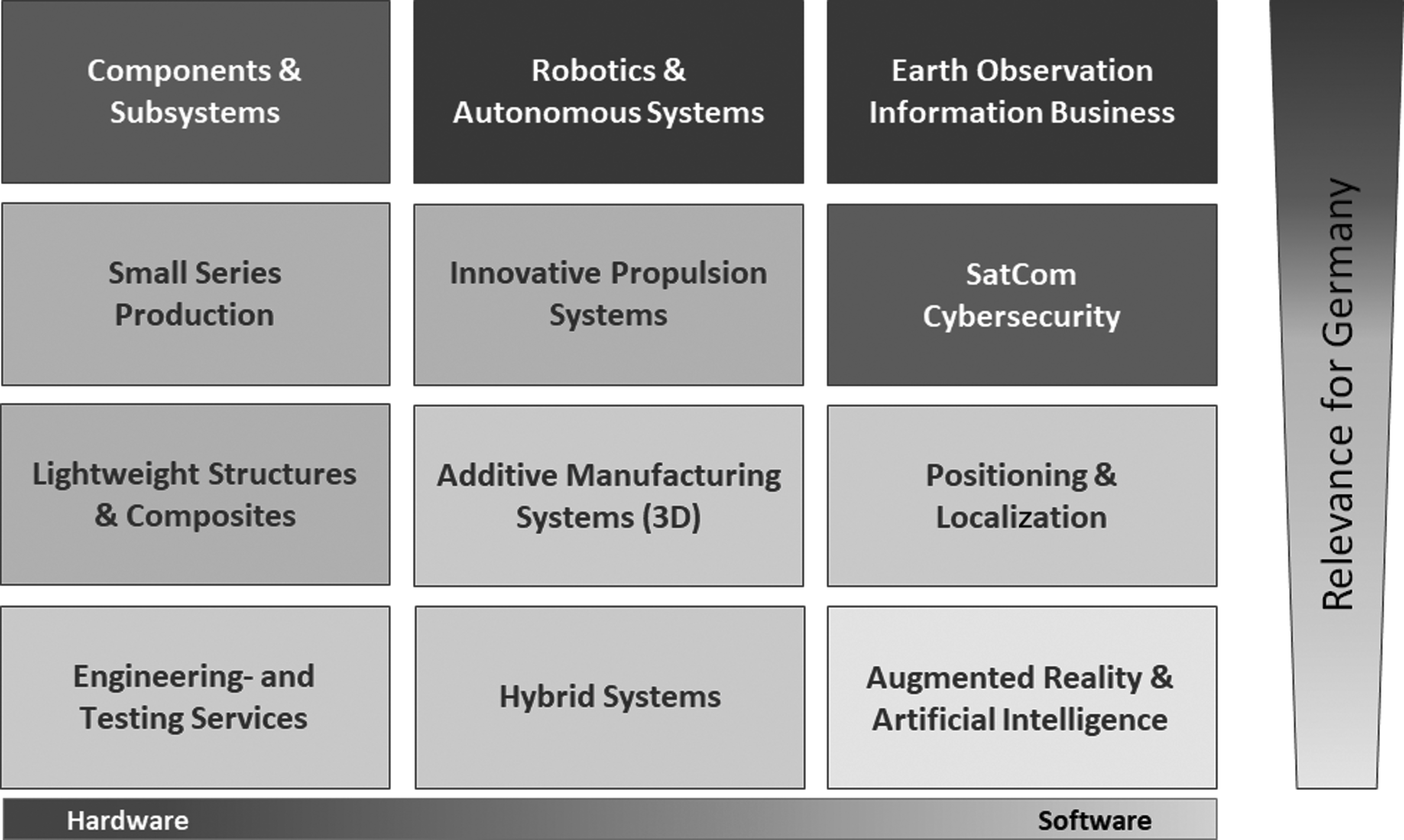

Business models in the areas of geo-information and industry-oriented broadband communication are expected to be the most attractive NewSpace fields in Germany. Positioning and navigation services are primarily developed by companies outside of the space industry in the narrower sense but should, nevertheless, be attributed to NewSpace. They are of decisive importance, above all in intelligent transport systems and self-driving cars. Further synergies result in the fields of robotics and artificial intelligence (“AI”). It is essential for NewSpace companies in Germany to seek partnerships with IT, automotive, and other relevant industries and to cooperate with them to exploit potential (Fig. 11).

Industry Capabilities as Modules for a German NewSpace Ecosystem.

There are also good opportunities for the German space industry as the supplier of components and sub-systems for NewSpace systems. This refers to small and micro-satellite components and also to sub-systems that have been developed for the defense business and that now come into question for innovative carrier systems. All in all, the following observations, assumptions, and approaches can be listed:

The excellent technical expertise and technologies in Germany can be used for many of the NewSpace trends; The industrial IoT and autonomous mobility on the ground and in the air are very promising for space applications from Germany; German companies are world market leaders in the automotive industry, in the mechanical engineering sector, and in other relevant industries; Robotics and autonomous systems are essential for the automation of industrial processes and for many security-critical applications; The industrial software sector could be a stimulus for NewSpace; German Earth observation companies are some of the best in the world. In cooperation with German IT companies (SAP, T-Systems), the potential of Big Data and Cloud Computing can be realized for new applications and markets for Earth observation; Space entrepreneurs who work primarily with space agencies find it difficult to develop new markets. Capital is often lacking as is a willingness to take risks and entrepreneurial initiative; Entrepreneurial personalities tend to be rare in the German space scene and in particular, there are no personalities with a “Think Big” mentality; Innovative business models are not thought out loud—more ambition is called for here; and A close networking of entrepreneurs and companies from different sectors is necessary to break through the closed system of the space industry and to successfully realize the potential presented by NewSpace.

The initial spark in the United States has provided industries there with the “first mover” advantage. Germany must quickly take the necessary steps if it is to assume a relevant role in NewSpace. The commercialization thrust in the space industry offers great opportunities for the export-oriented German industry, links space with general trends of the global economy (Digitization/Industry 4.0, IoT, global broadband access, autonomous mobility, etc.), and supports the meeting of the great social challenges such as environmental protection, climate change, and security.

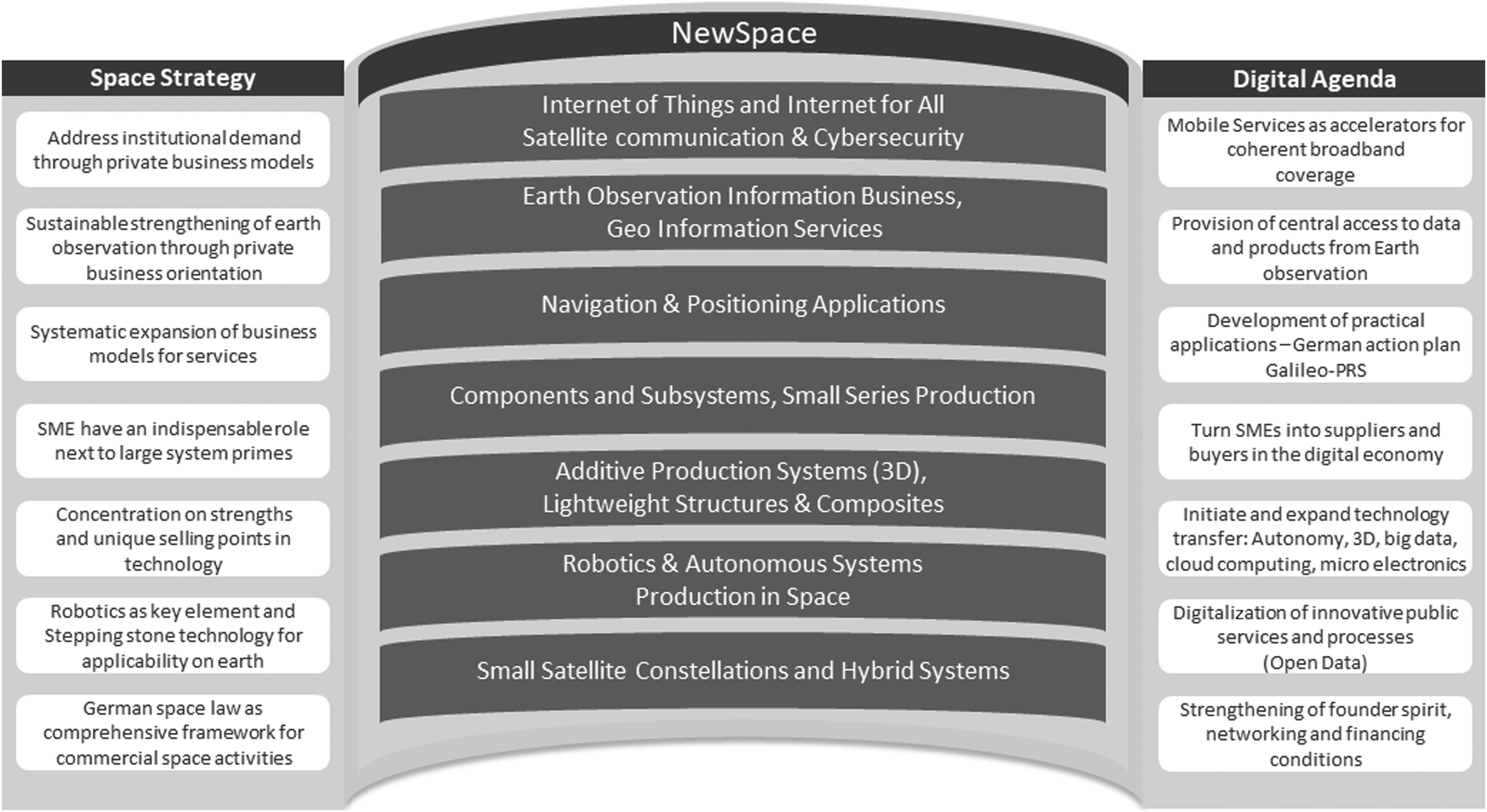

The German government has set important fields of political activity with its Space Strategy and the Digital Agenda. NewSpace could become the bridge between space and the digital economy. Great opportunities result from this for Germany and its industry.

Germany is well positioned to be successful in NewSpace. This existing industrial expertise must now be supplemented by specific digitalization know-how and transformed for the space industry so that NewSpace can also be successful in Germany. The recommended action presented in this study is intended to serve as a first marker along this path. The right track must be taken now if it is to do so.

Conclusions

“NewSpace” is an umbrella term for a movement and philosophy that is often affiliated with, but not synonymous with, an emergent private spaceflight industry. Specifically, the term is used to refer to a community of relatively new aerospace companies working to develop low-cost access to space or spaceflight technologies and advocates of low-cost spaceflight technology and policy. NewSpace has numerous facets, ranging from offering established services such as satellite communication and geoinformation, the manufacturing of Smallsat systems and components, positioning, navigation and timing, the operation of new launch systems to emerging business models centered on services related to the IoT, debris mitigation, satellite servicing, manufacturing in space, energy from space, and the mining of asteroids to name but a few. NewSpace is gradually developing new commercial fields beyond the traditional commercial space sector.

Although some of the business concepts are not new, the pace and success rate with which these start-ups acquire their financing is. The dimension of the financial attractiveness is demonstrated by the fact that these companies have attracted more than $13.3 billion of investment, including $5.1 billion in debt financing, since 2000. More than 80 angel- and venture-backed space companies have been founded since 2000. Eight of these have since been acquired, at a total value of $2.2 billion.

††

The NewSpace movement has so far been focused, to a great extent, on the United States, namely the West Coast. Mojave in California has been dubbed “the Silicon Valley on NewSpace,” being home to several of these commercial space enterprises. In aiming at understanding the driving forces behind the NewSpace ecosystem and the related chances and challenges for Germany and Europe, SpaceTec Partners and BHO Legal have found out that at least 4 factors are of immanent importance for a NewSpace ecosystem to create market-driven products and services. These factors are related to:

Business Philosophy—creating and living an entrepreneurial spirit; Financing—access to early stage risk capital and venture funding; Technology Management—focus on spinning-in technologies and ICT processes; and Framework Conditions—favorable political and legal conditions supporting commercialization.

NewSpace is driven both by new markets for services and applications and by the development of disruptive technologies and products. However, the focus is not placed on technologies as they are in the traditional space industry but on the market success that is expected for innovative applications.

Many founders of the American NewSpace companies come from the IT industry and use the experience and financial means generated from their previous start-ups. Their business philosophy is characterized by the focus on developing products and services in line with demand, challenging the status quo, promoting innovative ideas out of the box, strictly adhering to costs, and on company locations, which are attractive to highly qualified employees from all over the world. The increasing convergence of space with the IT sector is reflected at several levels: On the one hand, the IT sector is producing great demand for global systems and services to cover the demand for broadband, for the IoT, for location-based services, or for Big Data. On the other hand, business models (e-commerce), services (cloud computing), and approaches (agile software development) are being transferred from the IT to the space sector.

A characteristic feature of NewSpace companies is the primary alignment of their business model to market opportunities. These result from:

Institutional customers such as space agencies, security authorities, or the military; New private customers, primarily from the ICT sector, and increasingly also from other industrial sectors; Global data networks, broadband coverage, and the IoT; Geo-information services for applications in the private sector, for example, in the insurance sector or in the oil and gas industry; Big Data applications that capture data with the assistance of satellites; and Autonomous systems that are based on satellite navigation and communication for the purposes of steering and control.

Our analysis of the trends and drivers of NewSpace showed that the U.S. model cannot be transferred 1:1 to Germany. The differences in the characterization of the four success factor dimensions are simply too great. On the other hand, there are also good opportunities for the German space industry as the supplier of components and sub-systems for NewSpace systems. This refers to small and micro-satellite components and also to sub-systems that have been developed for the defense business and that now come into question for innovative carrier systems.

The initial spark in the United States has provided industry there with the “first mover” advantage. Germany must quickly take the necessary steps if it is to assume a relevant role in NewSpace. The commercialization thrust in the space industry offers great opportunities for the export-oriented German industry, links space with general trends of the global economy (Digitization/Industry 4.0, IoT, global broadband access, autonomous mobility, etc.), and supports the meeting of the great social challenges such as environmental protection, climate change, and security.

The German government has set important fields of political activity with its Space Strategy and the Digital Agenda. NewSpace could become the bridge between space and the digital economy (Fig. 12). Great opportunities result from this for Germany and its industry.

NewSpace as the link between Space Strategy and the Digital Agenda.

Germany is well positioned to be successful in NewSpace. This existing industrial expertise must now be supplemented by specific digitalization know-how and transformed for the space industry so that NewSpace can also be successful in Germany. The recommended action presented in this study is intended to serve as a first marker along this path. The right track must be taken now if it is to do so.

Disclaimer

This study was prepared during the period from Autumn 2015 to Spring 2016 under contract for the German Federal Ministry for Economic Affairs and Energy.

The main contractor was the consulting firm SpaceTec Partners (Munich/Brussels) with the involvement of the law firm BHO Legal (Cologne/Munich).

The authors would like to point out that the statements and recommendations contained in the studies do not necessarily reflect the opinions of the Federal Ministry for Economic Affairs and Energy in its capacity of contracting authority. Errors and defects in the study are solely attributable to the study team.

This summary contains the main core statements of the overall study, which is available at www.bmwi.de/DE/Mediathek/publikationen.html. The long version of the study explains the concepts presented and the specialized terminology.

Footnotes

Author Disclosure Statement

No competing financial interests exist.