Abstract

Abstract

The concept of new space activities has gained a lot of public interest and is frequently used in discussions. However, the boundary between these new space activities and commercial space activities is not well defined and creates some confusion. Emphasis here is, therefore, placed upon a considerable difference between both, namely the entrepreneurial character of new space and equity funding. To stimulate further discussion, a definition of new space activities is proposed, putting emphasis on this entrepreneurial perspective.

By lack of a generally accepted definition, there is an ongoing debate about the differences between new space activities (and related economy) and commercial space activities. Indeed, several presenters of, for example, satellite operators are describing new space activities, and the resulting new space economy as being similar to the services they have been offering since several decades and, therefore, as nothing new.

Even if this journal is now fully dedicated to new space-related articles, there seems, therefore, a clear need for clarification. A recent article in the journal outlines the relationship between new space and the new geopolitical context or space ecosystem. 1 This approach is no doubt valid but it is felt useful to put emphasis as well to the entrepreneurial aspects linked to the search of new and novel space applications and the different steps of equity financing needed to accomplish this goal.

This article attempts to highlight the different approach and, as a result thereof, a definition of new space is proposed for discussion.

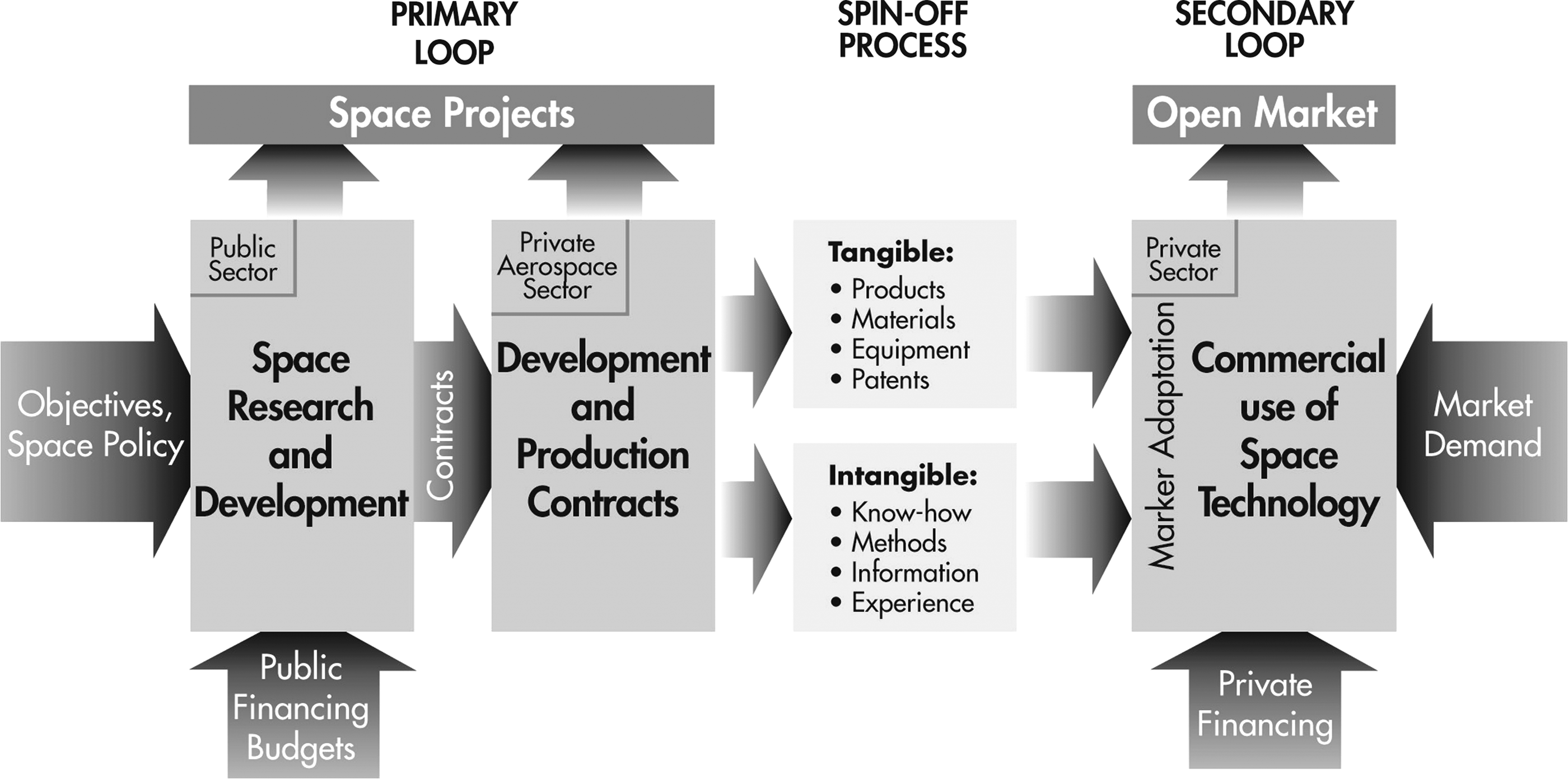

The space commercialization effect was the process that took place with the transfer of space activities from the public to the private sector, as presented in Figure 1.

Transfer mechanism from public to private space activities. 2

Let us first consider the transfer mechanism as depicted in Figure 1 in more detail.

Space activities were initially government financed, being the main driving force of national prestige. Two main players, the United States and the (then) USSR, were involved in this Space Race to put, for example, a first satellite and human in space or humans on the Moon. Two well-known astronauts, Apollo15 commander David Scott and Russian cosmonaut Alexei Leonov have described on the basis of detailed inside information the different perspectives as both of them were important actors 3 in this Space Race.

Financing of these activities was based uniquely on government (hence tax) money, and due to the Cold War effect such expenditures were never put in question in view of national prestige. This primary loop was, therefore, very prominent in the years 1945–1970, although it started already earlier with the development of suborbital rockets for military purposes.

When this public funding, mainly after the moon landing, decreased rapidly, the major space companies either directly or indirectly started to search for private space activities. An early example is the offering of commercial space telecommunication satellites-based services that started off as a public service (Intelsat, Eutelsat) but then became so profitable that they attracted easily private funding after the deregulation. The main characteristic of this, shown in Figure 1 as “spin-off process,” was that they used similar design and development methods as they were used to for governmental contracts. It is evident that also the second loop generated spin-off both to other industry as to the new space sector, as we will later also note in Figure 2, and even back to government contracts (leaner management techniques, operational procedures, smallsats,…)

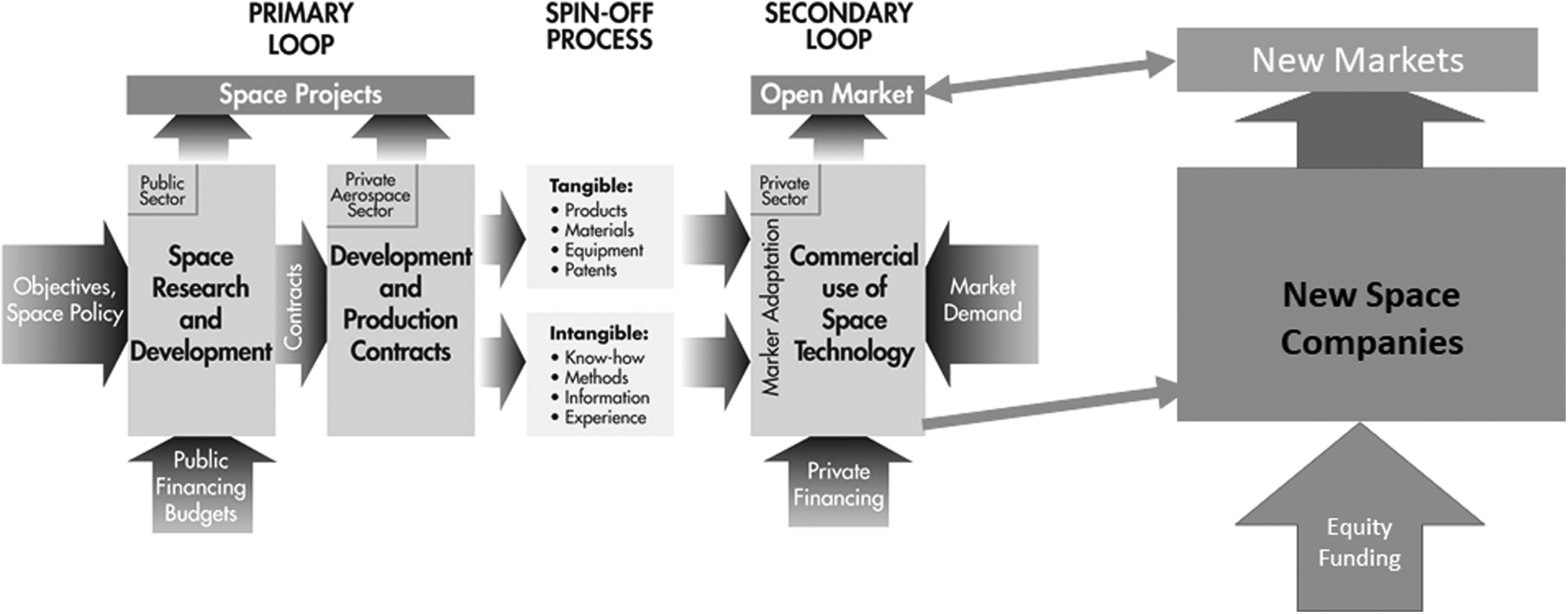

Distinction between commercial space and new space activities.

Once these activities proved to be viable, the initial public–private partnerships (and hybrid companies resulting thereof) more and more transferred to fully privately financed entities. Examples are Intelsat and Inmarsat that got access to private equity funding without public sector participation eventually.

This process created a rapid shift from governmental to more commercial activities. If we take the distribution of space activities according to the Space Foundation, we can conclude that nowadays approximately not <75% thereof are nowadays commercial activities, as we can note from Table 1.

Space Sector Distribution in 2015

Table adapted from Ref. 4

A large part of the funding was provided by traditional financing mechanisms of the large space companies (debt financing) or partial government participation. As we can note from a survey of analogue historical activities, we can conclude that such transfer happened also in the past in other areas such as shipping, railroad transport, and commercial aviation. 5

Indeed, this scenario is closely linked to the dual use of these activities.

The Indian railway system was initially developed to rapidly deploy British troops all over the country. The same rationale was given for further development of the German railway system in 1841 6 and for the U.S. and Russian railway systems.

As another example, there was a rapid development in the aeronautical sector during World War I with reuse of planes for civil transportation from 1919 onward (U.S. production lines were able to produce not <1,000 DH-4 planes monthly in 1918 7 ).

Dual use of space activities, in particular in the fields of localization (NAVSTAR, later called Global Positioning System [GPS]) and Earth observation (such as the U.S. SBIRS Early Warning system), not only justified government sources of early financing, but are also the rationale that government space activities will remain to exist.

With a solid space infrastructure in place (in terms of navigation systems such as GPS and Galileo, commercially accessible Earth observation systems, and excess transponder capacity in the field of telecommunications), young entrepreneurs are developing new applications.

A major distinction with the previously described commercialization activities is that these entrepreneurs are forced to look for inexpensive solutions to reduce the investment efforts as well as searching for cheap launch possibilities (in general as secondary payloads). Note that for launch opportunities, they have a larger freedom to do so as they are less bound by regulatory restrictions (contrary to, e.g., European Space Agency satellites where by preference European launchers shall be used).

A second important distinction is that, having limited or none collateral, the new space entrepreneurs need equity funding and financial partnerships.

The latter point, in particular, leaves the new space entrepreneurs no choice but to look for first financing rounds typically in sequential order, gathering first seed funding from family, friends, and founders sources. Initial equity funding, on the basis of a solid business plan, is then in general found by including business angels and business angel networks in the process.

In the growth phase of the activities, structured equity financing by venture capitalists is the next logic step, whereby a sharing of the ownership is a condition sine qua non, even if this step is not always popular in the eyes of the founders.

We can note here the growing interest in crowdfunding as an early funding source. In addition to well-known crowdfunding platforms such as Rockethub and IndieGoGo, Kickstarter has been most successful in the space field. We can refer to examples such as LightSail, 8 exploring the concept of solar sail propulsion (1.2 million US dollars [MUSD] pledged), Arkyd 9 promoting a space telescope (1.5 MUSD), and Lunar Mission One 10 a scientific mission to the Moon (0.9 MUSD).

For profit-making activities, this mechanism could become interesting if equity crowdfunding could become a more familiar and streamlined possibility, once the regulatory framework would have been fully established and such equity crowdfunding platforms will be fully operational.

The new space activities development, driving these companies, can, therefore, be represented as per Figure 2, as add-on to Figure 1.

The main difference highlighted is that commercial companies have mainly debt financing mechanisms and shareholders, which could also be public. They, therefore, are more focused on large applications such as remote sensing or telecommunication-based applications. New space—entrepreneurial—companies require equity financing and target completely new markets such as navigation applications and integrated services.

As an example of successful new space activities, we can refer to the relatively recent SPIRE company, 11 formed by a number of International Space University alumni of the Master of Space Studies class of 2012.

Indeed, the concept of this group is based upon a fleet of inexpensive smallsats that can be produced in a very short end-to-end in-house assembly, integration, and verification process (even in periods of 8 days only). This is done by simplified design principles and reduced lifetime requirements (typically 2 years) to allow for mass and cost reduction.

The satellites are launched seeking for cheap opportunities, mainly as secondary payloads, without constraints of origin.

The financing process followed the aforementioned equity financing process, whereby the early involvement of a strong business angel made a quick kick-start feasible.

If we combine all these considerations, a potential definition of new space entrepreneurial activities is hereby proposed as follows:

Private companies, which act independent of governmental space policies and funding, target equity funding and promote affordable access to space and novel space applications.

It is hereby acknowledged that, as each definition, there is a level of simplification imbedded in the aforementioned definition:

New space companies evidently have to abide to government regulations, but they have more flexibility, for example, in the choice of a launcher for their (secondary) payloads. New space companies will surely not refuse government contracts, but primarily they try to minimize their dependency in the long run. Affordability is a relative factor, but trying to penetrate in the markets of emerging countries requires providing solutions that are of good quality, at the same time respecting budgetary limitations.

Conclusion

Whereas there is no doubt from a macroeconomic perspective that we are evolving in space activities toward a different ecosystem, there is still a microeconomic need to distinguish between the commercial space activities as they took place during the period 1970–2010 and the new space activities nowadays. In this context we have to include the present considerations and research on commercial space companies and definitions thereof.

In this article, an emphasis is placed that financing is one of the major differences between new space and traditional commercial activities, in addition with a strong desire to develop new space applications independent from governmental motives. This also results in the need to find novel solutions to reduce mass and costs as the entrepreneurs are depending on equity financing.

Many entrepreneurs reduce their investment costs by benefitting from the systems developed by government funding in terms of satellites and launchers. They can, therefore, propose more affordable applications in specific markets, which are not the prime targets of the commercial space companies focusing on large turnovers.

It is on this basis that a proposal is made for a definition of new space activities in this article, hoping to initiate an interactive dialogue.

Footnotes

Author Disclosure Statement

No competing financial interests exist.