Abstract

Abstract

Commercial human access to suborbital space tourism as a segment within the commercial space transportation industry has been rapidly evolving. This study uses a competitive analysis approach built on the characteristics of industry structure to better understand this evolution. The overarching goal of this study is to apply economist Michael Porter's five forces model to the evolving suborbital commercial space tourism segment. Extant suborbital research, industry publications, and primary qualitative interview data were used to evaluate the role of industry stakeholders, economic and political barriers to entry, and competitive rivalry on the evolution of the industry. This study reveals that the forces being exerted on rivalry in the industry may result in the formation of an oligopoly controlled by few providers of space tourism services. Competition will evolve based on a focus on product differentiation among these firms as opposed to the reduction of ticket prices.

Introduction

Nearly 67 years after the first manned suborbital spaceflight, the suborbital space tourism industry continues to develop into what could be a self-sustaining commercially viable industry. To understand the potential for an industry to generate profit, firms and stakeholders must understand the underlying industry structure itself. This structure goes beyond just industry competitors but includes stakeholders such as customers, suppliers, governmental agencies, potential entrants, and producers of substitute products. It is the industry's structure that incentivizes new firm entrance, determines the intensity of competition, and dictates industry profitability; and it is this profitability, not the uniqueness of product itself, which drives industry growth. The goal of this study is to use Porter's five forces model, an industry structure tool developed by economist Michael Porter in his seminal work, Competitive Strategy (1980), to identify the market structure, stakeholders, and competitive forces within this emerging industry that drive innovation, competition, and profitability. The forces identified in the model guide companies to make strategic decisions about resource and asset allocation.

This study was developed as a recent call to investigate the nascent but evolving commercial space tourism industry. An important driver of commercial space tourism research is guided by the Federal Aviation Administration (FAA) Office of Commercial Space Transportation as part of the goal to promote, facilitate, and encourage the development of Commercial Space Transportation (CST). In particular, task number 305 was created as part of theme four for the FAA's Center for Excellence (COE) in CST. The overall goal of theme four is to conduct research on the industry viability of CST, including but not limited to the study of a broad set of variables that include economic, legal, legislative, regulatory, market analysis, and modeling. This research is meant to instruct and guide not only policy decisions but to aid and enhance the knowledge of the corporate participants in the competitive landscape as well. As the FAA continues to expand or contract its role as setting regulatory standards governing human spaceflight and CST, information related to the appropriate level of involvement is pivotal.

This study will review a variety of primary and secondary data sources to draw conclusions about the power of each force acting on competitors within the suborbital commercial space tourism industry. The article proceeds by first providing a brief description and history of the macroindustry—CST. As defined by the FAA, CST is the movement of or means of moving objects, such as satellites and vehicles carrying cargo, scientific payloads, or passengers to, from, or in space. The purpose of this study is to focus on suborbital space tourism, a subset of CST.

This Background section includes a financial snapshot of the overall space transportation industry as well as the details of the various market segments, which collectively make up this industry while providing a comprehensive list of active major participants. The Industry Structure Factors section provides an overview of the five forces model and how to technically apply this tool within the industry framework. The Methodology section provides information concerning the methodology utilized to gather both qualitative and quantitative data used for this study. Next, the Mapping the Industry According to Porter's Five Forces section of the article applies the five forces model to the suborbital space tourism industry and provides evaluation of the strength of each force on the attractiveness of segment entry and the potential for commercial viability of that segment. The Conclusions and Discussion section uses the model to draw conclusions about industry viability and highlights several areas of concerns that the study has identified. In addition, this section provides some discussions about these findings and some limitations of this research.

Background

History and Description of CST and the Evolving Suborbital Space Tourism Segment

In 1960, U.S. Air Force (USAF) Captain Joseph Kittinger became the first participant in the “Man High” project. This project took Kittinger up to a height of 110,000 feet by helium balloon, to which he then fell back to Earth. The USAF commissioned this project to test and develop emergency exits from high-altitude machines. 1 On May 5, 1961, Alan B. Shepard took the first suborbital flight. Shepard, who flew the Mercury Capsule at an altitude of 186 km, safely landed back to Earth in the Atlantic Ocean. By 1963, the USAF defined the edge of space being 80 km and anyone who passed that height was awarded with USAF Astronaut Wings.

Since this time, numerous individuals and companies have pursued their wings and the birth of CST ensued. 2 On April 28, 2001, Dennis Tito became the first commercial, fee-paying traveler by purchasing an orbital trip to the International Space Station (ISS) and the creation of a commercial market for human spaceflight has been evolving ever since. Tito's $20 million investment aboard the Russian Soyuz validated an unserved opportunity in the market. 3 Subsequent missions to the ISS supported these initial hypotheses for market demand; however, the retirement of the U.S. Space Shuttle Program and the limitation of physical space aboard the ISS has since eliminated the ability of serving this commercial need.

On April 1, 2004, the U.S. Office of Commercial Space Transportation issued the first license for suborbital rockets to Scaled Composites. In 2004, Scaled Composites SpaceShipOne won a $10 million prize for developing the first privately funded vehicle to cross the threshold of space. SpaceShipOne exceeded 100 km in altitude returning back to Earth and then launching again within the next 2 weeks. In additional to Scaled Composites, there have been over a dozen vehicles being developed by Virgin Galactic, Blue Origin, SpaceX, Masten Space Systems, XCOR Aerospace, Airbus, and Armadillo Aerospace that have attempted and/or continue to participate in the suborbital market. 4

The implied demand for space tourism continues to grow, and the demand for suborbital travel continues to receive validation. Initial data gathered by Futron's 2002 Space Tourism Market Study and subsequent work presented at the AIAA Space 2011 Conference in Long Beach, California, confirm the existence of demand within the suborbital tourism market.5,6 As of recent, Virgin Galactic has received over 700 registrants from participants in over 50 countries totaling more than $80 million in deposits for future human tourist flights and it has been reported that XCOR has sold over 300 tickets.7,8

Industry Financial Snapshot

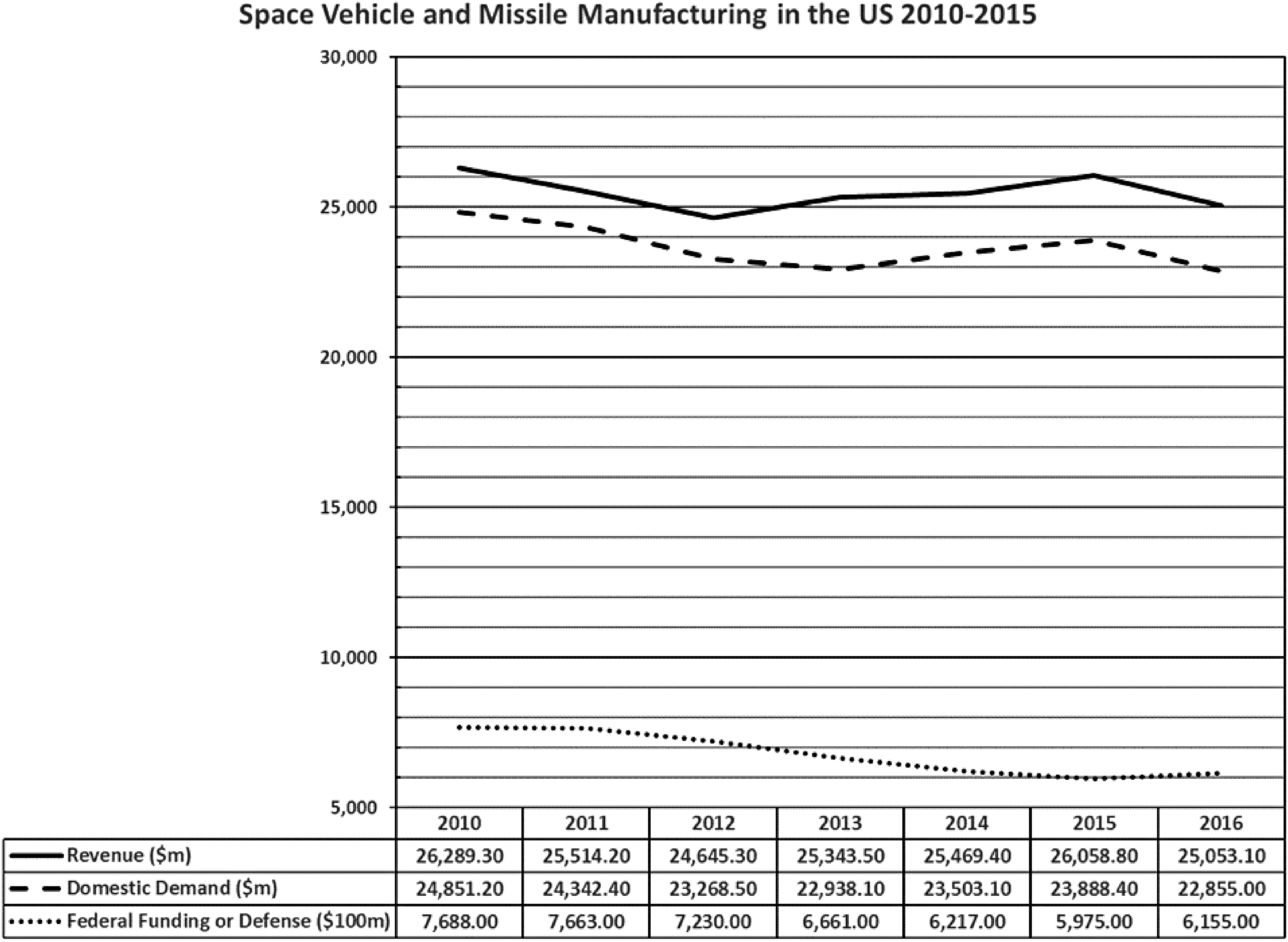

The Office of Commercial Space Transportation created in 1984 via the Commercial Space Launch Act of 1984 represents the creation of this new industrial subsegment, which involves the privatization and commercialization of space and space technology. Under the North American Industrial Classification System (NAICS), a segment for CST does not yet exist; however, NAICS code 33641b represents the space vehicle and missile manufacturing industry. Since data regarding the companies involved in CST are difficult due to the nascence of the industry, this study will begin with an analysis of the overarching NAICS code 33641b (Fig. 1).

Revenues for North American Industrial Classification code number 336414.

In analyzing historic and predictive revenue growth for NAICS code 33641b, we witness relatively flat growth in revenue. Annual industry revenue growth from 2010 to 2016 has seen an overall decline of 0.02%, which is most likely due to the decrease in government funding. Federal funding has seen sharp decreases during this period. Next to note is that there is a cyclical trend that rises and falls with the domestic demand, which is parallel in cycle with the revenue. This could be due to the increase in satellite launchings for the telecommunications industry. It is this positioning in the industry life cycle that unlocks opportunity for the privatization of subsegments such as CST.

The industry is made up of 91 primary companies. These companies manufacture products from propulsion units for missiles through the complete manufacturing of space reusable vehicles (SRV). The industry operates at a very high level of concentration with the top four producers, Lockheed Martin, Raytheon, Boeing, and Orbital ATK, accounting for 73.8% of the market share and the top six firms accounting for 83.5% of the total industry revenue predicated in 2016. However, the industry has recently seen an increase in new entrants. The new entrants have had a declining effect on the incumbent participants, thus increasing competition. These new entrants include SpaceX, Virgin Galactic, Blue Origin, and a plethora of start-up firms. The market entry by new companies is expected to cause the number of industry enterprises to climb at an annualized rate of 2.0% to 95 businesses over the 5 years to 2022. Moreover, industry employment is forecast to only climb an annualized 2.3% to 76,479 people over the next 5 years. 9

Of the total industry revenue of $26.1 billion, 32.9% or $8.59 billion are directly attributed to space systems and an additional $2.97 billion, predicted for space vehicle parts, are also part of this subset in NAICS code 33641b. Revenue for this subset known as space systems, ∼$10 billion, currently represents a relatively small but growing segment of CST. Leaders in this subset include Lockheed Martin with 31.7% and the combination of both Orbital ATK (7.5%) and SpaceX (3.3%).

The question remains if the subset of the space industry, in particular commercial space tourism, will have a significant effect on industry growth. Development and adoption of this segment have been slow. Based on early projections from Futron's October 2002 Space Tourism market study, an estimated 4,000 suborbital passengers should be flying by 2015 and revenues in excess of $700 million should be generated by the space tourism segment by 2021. * These estimates have not materialized. In 2006, the Tourism Market Study was revisited by Futron and these estimates showed a total of 4,000 suborbital passengers to materialize in 2016 with revenue in 2021 coming in shy of the previously estimated $700 million. While deposits are indeed an indicator of early interest, these estimates have been extremely slow to materialize as recent vehicle crashes and other setbacks have stymied sector growth. Predicting when, and if, adoption of suborbital space tourism is extremely difficult; however, while the overall industry is in its mature phase, commercial space tourism and transportation are expected to surge in the next 5 years.9,10

Human suborbital spaceflight has garnered the most attention and is emerging as the most viable of the segments within this industry. This segment includes the following:

• Human spaceflight as a tourist activity (up and down) and crew training. ○ Space tourism can be made up of two distinct but similar methods for experiencing suborbital flight: rocket-powered planes or stratospheric balloons. • Point to point travel for the purposes of high-speed passenger transportation and fast package delivery.

Human Spaceflight Firms

What follows are several of the more prominent firms participating in the burgeoning suborbital market. 10

1. Scaled Composites/Virgin Galactic: Founded by Sir Richard Branson, Virgin Galactic is a U.S spaceflight company within the Virgin Group that is developing commercial spacecraft. Passengers board SpaceShipTwo, a vehicle that is launched using the carrier aircraft WhiteKnight Two, which then climbs to the edge of the atmosphere using a fired rocket engine. Passengers will experience roughly 5 min of weightlessness before gliding back for the landing. The company aims to provide suborbital spaceflights to space tourists, suborbital launches for space science missions, and orbital launches of small satellites. Most recent advancements include the purchase of a new facility intended to build the new Launcher One, and research and development for a new second-generation hyperpropulsion system (an in-house production of multistage engines).

2. XCOR Aerospace: XCOR Aerospace is a small, privately held California C-Corporation founded in 1999. XCOR is developing the Lynx and the Lynx II, a small Horizontal Take-off Horizontal Landing SRV capable of transporting one passenger in addition to the pilot. The Lynx is XCOR's entry into the commercial reusable launch vehicle market. This two-seat, piloted space transport vehicle will take humans and payloads on a half-hour suborbital flight at an altitude of 330,000 feet. Then, the flight vehicle will return safely to a landing at the takeoff runway. XCOR is focused on the research, development, project management, production, and maintenance of reusable suborbital and orbital launch vehicles, and also rocket engines and rocket propulsion systems. In 16 years, the firm has developed and built 13 different rocket engines; they have also built and flown two manned spacecraft vehicles.

3. Blue Origin: Blue Origin, LLC, is developing technologies to enable human access to space at low cost and increased reliability. Blue Origin is developing a Vertical Take-off Vertical Landing (VTVL) man-rated SRV, the New Shepard. The elements of the New Shepard vehicle are currently being tested extensively, both on the ground and during unmanned test flights. The New Shepard is a fully reusable VTVL system that will take astronauts, research projects in relation to microgravity physics, gravitational biology, technology demonstrations, and educational programs, to space on suborbital journeys. The New Shepard vehicle includes a modular 530 cubic feet crew capsule capable of carrying up to six astronauts atop a separate VTVL booster that, after separating from the capsule, will return to Earth. Deploying landing gear, the booster will make a precise touchdown, enabling reusability. All of the engines are American-made and are designed, developed, and manufactured at Blue Origin's headquarters in Washington State. Advancements include completed acceptance flight tests of its cryogenic BE-3 deep-throttle engine, which will be used to power the New Shepard. The suborbital, manned space vehicle, New Shepard, has passed and received multiple preliminary design and safety certifications and has completed its first development test flight on April 29, 2015. The test flight concluded with the New Shepard achieving Mach 3 and arriving to its planned test altitude of 307,000 feet successfully.

4. WorldView: WorldView uses high-altitude balloons, as an accessible, affordable way to access suborbital horizons. WorldView's high-altitude balloon let customers soar for hours on end in a comfortable, smartly outfitted, specially designed space capsule. WorldView also provides new opportunities for research and education pursuits. This platform presents a variety of advantages over orbital and rocket-based suborbital options, giving researchers an opportunity to conduct experiments as well as an opportunity for a unique education experience. The most recent flight made by the company was a 4-h flight test where the balloon and its payloads floated at a height of 105,000 feet for an hour and 46 min. While WorldView has only been conducting cargo flights at this time, it anticipates providing human spaceflight at altitudes over 100,000 feet or 19 miles.

5. Zero2Infinity: Headquartered in Barcelona, Zero2Infinity has been launching unmanned balloons as a test for two different business ventures: stratospheric tourism and a commercial satellite delivery system. The Bloon is a version of spacecraft designed to take tourists on trips at suborbital altitudes. The Bloon's passenger pod houses a maximum of four passengers and two pilots. On Friday September 6, 2013, Zero2Infinity performed a test flight of Microbloon 3.0 from the airport of Cordoba, Spain. Microbloon 3.0 is an inflatable pod and was able to successfully ascend up to 27 km. The company is currently operational and plans to send scientific and technical payloads to near space and aims to start its manned test program within the next 2 years.

6. Space Vision: A private Beijing mainland company that plans to offer near-space tourism for private passengers in a high-altitude balloon. Passengers would ascend to 40 km in a pressurized capsule with the ability to view the earth's curvature coupled with a few moments of reduced gravity. The project is still in the “design & test phase.” The passenger capsule would be carried up by a balloon filled with nontoxic and nonflammable helium and descend under a large parachute. Passengers would also be equipped with special parachutes and jumpsuits supplied with oxygen that would enable them to bail out of the capsule at high altitude.

7. Space Adventures: Founded in 1998, Space Adventures, Ltd. is the world's premier private spaceflight company providing exclusive opportunities for private spaceflight and space tourism. Space Adventures is the first and only company to have sent self-funded individuals to space. Space Adventures curates passengers' experiences by offering views of the Earth from space at 62 miles (100 km) above Earth while experiencing moments of weightlessness. The company plans to solidify additional contracts with various space vehicle providers to provide passengers a wider variety of different space experiences and adventures.

8. Zero-G Corporation: Zero-G Corporation is a Vienna, Virginia, based company that offers passengers the chance to experience various states of microgravity aboard a modified Boeing aircraft. Zero Gravity Corporation is a privately held space entertainment and tourism company whose mission is to make the excitement and adventure of space accessible to the public. The experience offered by Zero-G is the only commercial opportunity on Earth for individuals to experience true “weightlessness” without going to space. Zero-G does not manufacture any space vehicles. 11

The eight companies listed are private companies that can either bring people into suborbital spaceflight or create the sensation of space travel. For the purposes of this study, competition and rivalry involve rocket-based tourism companies that are capable of reaching altitudes of over 60 miles. Competitors that offer high-altitude balloon rides and zero gravity experiences are considered substitutes for suborbital space tourism and referred as such in the body of this study.

In addition, on February 27, 2017, SpaceX has confirmed receipt of deposits for two individuals to be taken on a flight around the moon scheduled for late 2018. 12 Other companies have tried entry into this market and have found the capital intensity of funding to be a difficult hurdle to overcome (Fig. 2).

Competitors in human spaceflight transportation. COE, FAA's Center for Excellence; CST, Commercial Space Transportation; N/A, not applicable.

Industry Structure Factors

This study incorporates Michael Porter's five forces model for the analysis of industry structure and competition within the suborbital spaceflight industry. Every industry has an underlying structure made up of a series of influencing factors that affect competition and long run profitability of the industry. The competitive forces help to determine if an industry is attractive for firms to dedicate resources to compete.13,14 Developed by industrial organizational economist Michael Porter, this five forces model provides a framework for analyzing how various stakeholders external to a firm impact the overall level of competition within an industry. These external forces indicate the attractiveness of an industry and the possibility for long run profitability of that industry. The forces that the model evaluates are discussed in this study: (1) threat of new entrants, (2) bargaining power of suppliers, (3) bargaining power of buyers, (4) threat of substitute products or services, and (5) the competitiveness of the industry as shown in Figure 3.

Porter's five forces diagram.

These forces can be very intense within an industry, thus reducing the attractive returns on investment for the companies competing within that industry, but also can be quite mild and provide the opportunity for larger returns on investment for companies developing a strategy for entry into an industry.14,15 It is ultimately the impact and intensity of these forces, evaluated comprehensively, that shape long-term industry structure and profitability.

Porter's Five Forces Model

Threat of entry

The threat of entry can be defined by the barriers that are in place to entering the specific market at hand; when these barriers are high, investment is more difficult to come by and when barriers are low investment becomes aggressive. 15 When a particular market or industry yields higher than average returns, companies will begin to enter that market, thus creating competition and reducing the opportunity for above average returns. This is referred to as the efficient market principal. High barriers to entry reduce the threat of entry to the industry thus benefiting the incumbent firms within an industry. Since the essence of strategy is the proper allocation of resources given the available options of various investments, firms seeking to enter a new industry pay particular attention to how difficult these barriers are to overcome and how much time and capital will be required to overcome these barriers. The Porter's five forces model is used to guide these strategic decision-making options given the difficulty of these barriers to entry. Higher barriers will limit the amount of competition within a segment, thus preserving industry profitability. There are seven general barriers to entry that restrict industry competition.

These barriers to entry include the following:

• Economies of scale— cost advantages received by producing larger scale quantities. • Capital requirements—having access to the proper amount of financial resources to compete within the industry. • Intellectual property—technology, access to materials, and subsidies. • Distribution channels—ability to exclusively deliver your product to the market. • Government policy—government imposed barriers that allow or disallow a company from entering or continuing to move forward. • Product differentiation—unique competency that allows firms to be successful in a new industry. • Customer switching cost—the fixed cost that customers will face in switching to the new product or company.

Power of suppliers

The power of suppliers refers to the market of inputs required for the production of products within the industry. These inputs include labor, raw materials, technical components, and related services that become part of the completed product. When few suppliers exist or their resources are rare, suppliers can acquire power over the industry participants and subsequently increase their prices. In this case, the industry looks less attractive to participants and can stifle industry growth. There are a few methods of suppliers acquiring bargaining power. These include situations when they are the only manufacturer of materials within the industry, their product is unique and inimitable, the industry is not an important customer to the supplier group, or the suppliers can easily and credibly integrate forward into the industry's business lines. If there are many suppliers in an industry, then there is a perfect competition among suppliers and prices should subsequently remain stable.

Power of buyers

The powerful buyers can capture more value in the transaction, thus forcing pricing down, demanding better quality products or services, or demanding more services than profitable for industry participants. When few buyers exist or certain buyers represent a large portion of the market purchasing, these buyers obtain larger bargaining power with industry participants. Buyers may also obtain bargaining power by purchasing standardized products, products that are unimportant in quality to the entire project, or products that do not provide quantifiable benefit to the project. In situations where buyers possess a high level of power with the producing industry firms, profitability within the industry is driven down and the prospects of profitable growth within that industry are low.

Threat of substitutes

A substitute is a product or service that performs a similar function as the one in the industry but by different means. When the threat of a substitute is high, buyers can find an alternative solution to their needs. Subsequently, profitability within the industry will suffer. Alternatively, when the threat of a substitute is low, sellers have more power to command higher prices. If switching costs are low and the substitute has a better price-performance trade-off, then the threat of the substitute is high. In the commercial space industry, we will look into all the different products and services that can be put in place of the commercial space tourism experience and how the customer needs are relative to the costs of substitutable endeavors.

Rivalry among existing competitors

In the traditional economic model, industries that exhibit intense levels of competition among firms will drive industry profit to zero. High rivalry is measured on the intensity and the basis of which they compete within the industry. Different intensities deal with the number of competitors within the industry, the growth of the industry, the barriers of leaving the industry, commitment to the business, and the ability to read the competition. If all of these factors of intensity are high, then there is a high rivalry, which can reduce the profitability of the industry. In general, we can measure the intensity of rivalry by indicators of industry concentration. A high-concentration ratio indicates that a large percentage of the market share is held by a limited number of firms. One of the most destructive dimensions or rivalry is price competition because “price competition transfers benefits directly from industry to its customers.” 15

In summary, Porter's five forces model is generalizable to most industries; however, in interpreting this model, the current state of different industries affects the influence on overall competitive rivalry. Applying this model to an industry requires insights into the interaction among the five factors. For instance, in the airline manufacturing industry, Boeing and Airbus have a fierce rivalry in how they compete for profits in this area; however, this rivalry is mitigated by the high barriers to entry restricting the number of new entrants. In addition, the power of a limited number of buyers placing large orders for aircraft also impacts overall profitability for these producers. Taken together, these factors reduce the impact on rivalry thus driving the profit percentages to exceed typical industry standards.

Methodology

This study utilizes qualitative data obtained through primary research conducted via industry interviews and open source materials available through market studies, government publications, extant academic literature, and industry reports to apply the five forces model to the suborbital space tourism industry.

The primary source of secondary data was a compilation of over 20 industry and government reports gathered from 2002 to 2016. In general, the data had a broad consensus of information across industry, government, academic reports, and surveys. In addition, a series of interviews were conducted with venture capital firms, large industry competitors, midsized firms, and new venture start-up firms to supplement this archival data. Interviews included Virgin Galactic out of Long Beach, California, XCOR Aerospace out of Mojave, California, Altius Space Machines out of Broomfield, Colorado, Astrobotics out of Pittsburgh, Pennsylvania, and the Space Angels Network out of London, England.

Interviews with these participants were conducted over the phone with the primary author, an MBA student, and an undergraduate aerospace engineering student and through e-mail utilizing a semistructured survey to gather their perspective on the forces that affect their firm's strategic decisions. The interviews provided an inside out perspective about how participants compete in the industry. Data were gathered from a range of companies across the industry to gain several perspectives on rivalry within the industry as to eliminate anecdotal results. As predicted, similar responses were found across interviews indicating general consensus among the interview participants. Combining the information from the interviews with the quantitative results from the industry reports provided highly correlating results. By using both qualitative primary data and quantitative archival data, the conclusions reached in this study are both significant and robust.

MAPPING THE INDUSTRY ACCORDING TO PORTER'S FIVE FORCES

Barriers to Entry: Threat of Entry

The barriers to entering the commercial space tourism industry are high, making the threat of new firms entering the market very low. Several of the most difficult barriers of entry for new firms to overcome as they consider entry into the CST market include the large financial capital requirement and the economies of scale gained by incumbent firms.

Large financial capital requirements

Perhaps the largest barrier to entry into the suborbital space tourism industry is the incredibly large capital requirement needed to compete in the business. Start-up capital and upkeep research and development costs represent a major hurdle for new firms to enter the commercial space industry. In a study by Christensen and Prober in 2002, it was estimated that the costs for manufacturing and launching a single vehicle can exceed $150 million and the FAA has data showing that this number could be upward of $260 million. Started in 2002, India's GSLV Mk. 3 program is projected to cost ∼$400 million by the time development is finished. Virgin Galactic, one of the leaders in the space tourism segment, has spent over $600 million in its development. 16 These are just a few examples of the extremely high capital requirements to compete in this industry.

While this represents a very high barrier to entry, the financial markets are becoming more favorable to the industry. Principals have been the catalyst for initial seed funding for many of these upstart companies. Principals from each individual company have invested personal wealth to launch this segment of the industry. Virgin Galactic's founder Sir Richard Branson, Blue Origin's Jeff Bezos, and SpaceX's founder Elon Musk are among the 21 billionaires listed on the Forbes 500 list to have invested capital into space ventures. 17 These high-profile celebrity status entrepreneurs have played a pivotal role in the funding of these ventures, in essence, overcoming the hurdles of perceived technical and market risks. In addition, the venture capital market has been steadily warming up to space-related investment. The Space Angels Network, a uniquely positioned networking platform specializing in connecting space-related start-ups with a network of venture funders, has seen a substantial increase in invested capital over the past decade. The Tauri Group report indicated that venture capital investment in 2015 was $1.8 billion, which was more than the previous 15 years combined.

Economies of scope

Economies of scope refer to the lowering of costs by being able to utilize knowledge across different products. In the space tourism industry, firms that were able to use their research and development knowledge as well as their manufacturing experience across multiple business units are beginning to gain advantage in the marketplace. Throughout the interviews with the participating firms, it became apparent that competitors were moving toward vertical integration of their components and utilizing existing knowledge across business units. The uniqueness of the components made quality assurance difficult to monitor, and thus, firms were moving away from an outsourced relationship.

Space X is becoming a superior competitor in the launch market by producing over 70% of their components in-house. This allows them to control both the costs and the quality of production. When existing companies that are currently competing in the launch market can leverage these synergies to their space transportation business units, this provides them with an economy of scope that results in production savings that create a high barrier for new entrants. The ability for firms to amortize the expense of research and development across areas other than commercial space tourism creates substantially higher barriers for new firms to overcome. Taken together, the high capital expenditures and the economies of scope created through synergies make the barriers to entry high and the threat of new entry low.

The Power of Buyers

Understanding the potential volume of buyers is essential in evaluating any power that this group may have on the competing firms. With the prevailing price tag of over $150,000 per ticket, the average buyer will be a high net worth individual with thrill seeking behavior.5,18 According to the 2002 report by Futron, the average participant will be a male, around the age of 55, with a high fitness level, ability to enjoy a 1-month vacation, who is working full time, and has a net worth of over $1 million. The ability to pay will indeed be the driving factor of demand. Stockmans, Collins, and Maita found similar results in a survey to over 5,500 participants. Of those surveyed, 2.7% of people who were willing to travel to space would be willing to pay three times their annual salary and additional 10.6% were willing to spend one times their annual salary. 18

Early indication of the buyer's limited power is seen in the price increases of presales for tickets to travel to space. Virgin Galactic and XCOR have already begun taking deposits for their CST missions. XCOR has sold 300 tickets for its missions priced at $100,000. As of January 2016, prices increased to $150,000 per ticket and tickets for their “Founders Astronaut Program” have sold out.8,19 Consumers can still buy packages ranging from $175,000 to $235,000 to travel aboard their Lynx Mark II to over 100 km. Virgin Galactic began selling tickets in 2005 for $200,000 and by 2013 had sold ∼240 tickets. As of 2016, they had deposits from over 700 customers. 7 Since then, they have raised their price to $250,000 and are actively selling tickets. Blue Origin has not currently set a price for an adventure aboard their New Shepard spacecraft but anticipates that it will be in-line with the current providers and expects to begin offering transportation sometime in 2018. 20

With such a large contingent of initial participants and the fact that both XCOR and Virgin Galactic have increased their pricing, this would indicate that the buyers have very limited bargaining power over these firms.

Power of Substitutes

To address the threat of substitution, we must first understand the value proposition being offered through suborbital space tourism. According to the Futron Market Study, the main reason people buy a ticket for a commercial spaceflight is that they want to be pioneers. These risk takers want to be the first generation of the general public to take part in a revolutionary activity. Inherent in this definition is the need to be first. As such, there are no definable substitutes that would allow these customers to be the first to experience commercial spaceflight. For others, space travel is a lifelong dream. Seeing Earth from space is a breathtaking experience and this segment of customer places extreme value in being able to fulfill this dream.

The main substitute that could accomplish a portion of this task would be taking a voyage aboard a high-altitude balloon. While it is technically not space, these balloons travel to the edge of space, high enough to allow customers to see 99% of the earth's atmosphere. This experience allows participants to see the earth against the blackness of space, thus providing a substitute for customers seeking this as their primary value requirement. Both WorldView and Zero2Infinity are competing with this mode of transportation. These balloons do have the capability of taking participants to heights of 30–40 km. While this distance is indeed impressive and will satisfy additional components of the space traveling participants such as the view, these two companies will not be competing with the rocket-powered commercial space tourism companies. Zero2Infinity expects to collect $124,000 per trip, while WorldView is anticipating a $75,000 price.21,22

Finally, space enthusiasts seek to see space by being launched into LEO aboard a rocket. These customers need to experience not only the vision of earth from space but also the speed and force of being attached to a rocket combined with the ultimate weightlessness of zero gravity. The ability of experiencing a brief period of weightlessness is currently available through Zero-G. Zero-G uses a modified Boeing 727 to provide participants with a weightlessness experience by performing parabolic arcs. While this does meet the individual's need of weightlessness, it lacks the other elements being sought by these consumers. Pricing for this adventure is $4,950. 11

Space travel is a very unique experience; the experience of being powered by a rocket into space to experience weightlessness and to capture breathtaking views from over 100 km from earth is impossible to duplicate without buying a ticket from a space tourism company. 23 Therefore, the power of substitutes to meet all of the needs of the market is extremely low.

Power of Suppliers

With respect to the supply chain in the reusable vehicle market, participants commented on the difficulty in ensuring quality assurance and timely delivery of parts. The parts have become extremely specialized and very few suppliers are capable of delivering such small runs of customized parts to meet the needs of the limited number of buyers. While you would imagine that this has the potential to provide additional power to these limited suppliers, it has forced the industry to vertically integrate backward. Vertical integration allows firms to lower their transaction costs, control the uncertainty related to supply and ensure quality products. SpaceX is the primary example of a firm that is aggressively vertically integrating when parts cannot be produced in a cost-effective and timely manner. This capability is resulting in SpaceX being able to provide substantially discounted pricing for launches of commercial satellites. For example, ARS Technica reports that SpaceX was recently awarded two air force contract launches at $83 million and $96.5 million compared to the proposed price of $422 million by ULA. 24 However, a report by ULA indicated the price per launch at an average of $164 million for the Atlas V and $400 million for the Delta Heavy.

Regardless, the market is witnessing the beginning of a market-driven value chain in which pricing from suppliers is being driven down due to the threat of vertical integration and this power could impact rivalry among industry participants. It is interesting to note that in more mature industries, where many suppliers exist that are capable of performing nonstrategic functions, firms will tend toward vertical disintegration. We are currently witnessing this phenomenon in the airline industry where firms can externalize production functions to specialists resulting in substantial cost savings and the ability for the airlines to focus on their core competencies.

With the extremely limited number of suppliers in this market, the bargaining power of these suppliers is extremely high; however, the proliferation of backward vertical integration has allowed the competitive firms to neutralize and counterbalance this power. The power of suppliers is thus moderate.

Conclusions and Discussion

Porter's model is constructed to evaluate the impact of each force on competition within the industry. This competition, otherwise known as rivalry, indicates how aggressively firms will compete for market share within the industry and how they will choose to allocate their resources and assets among various options. A summary of the forces that are acting on rivalry among existing competitors is included in Figure 4.

Porter's five forces model for CST.

Rivalry

There are four main competitors emerging that may be capable of delivering a human suborbital experience. These companies are Virgin Galactic, XCOR Aerospace, Blue Origin, and SpaceX. Each company will be utilizing a rocket-powered vehicle. Each of these vehicles will provide the ability to rise to over 100 km with a flight duration anticipated at 10–60 min.

The barriers to entry are high, the threat of entry is low, the power of buyers is low, the threat of substitute products is low, and the power of suppliers is moderate. Taken together, Porter's five forces analysis indicates that this industry and the competitive rivalry within it are evolving to be low to moderate intensity for rivalry. The race to become the first company capable of delivering this experience is driving the innovation. The more advanced the leading company can become along this learning curve and the more reliable the service that it can provide, the faster it will be able to capture market share for this initial group of pioneers seeking to travel to space. As other competitors begin to also achieve commercial viability, Porter's five forces indicates that the industry will evolve into an oligopoly. An oligopoly is an industry defined by a limited number of sellers engaging in limited rivalry. Some of the characteristics of an oligopoly include tacit collusion, product differentiation, and higher prices. Consumers could anticipate having these main four competitors keeping their prices high and attempting to differentiate their services based on the overall experience of flying into space.

Future Research and Complementary Products

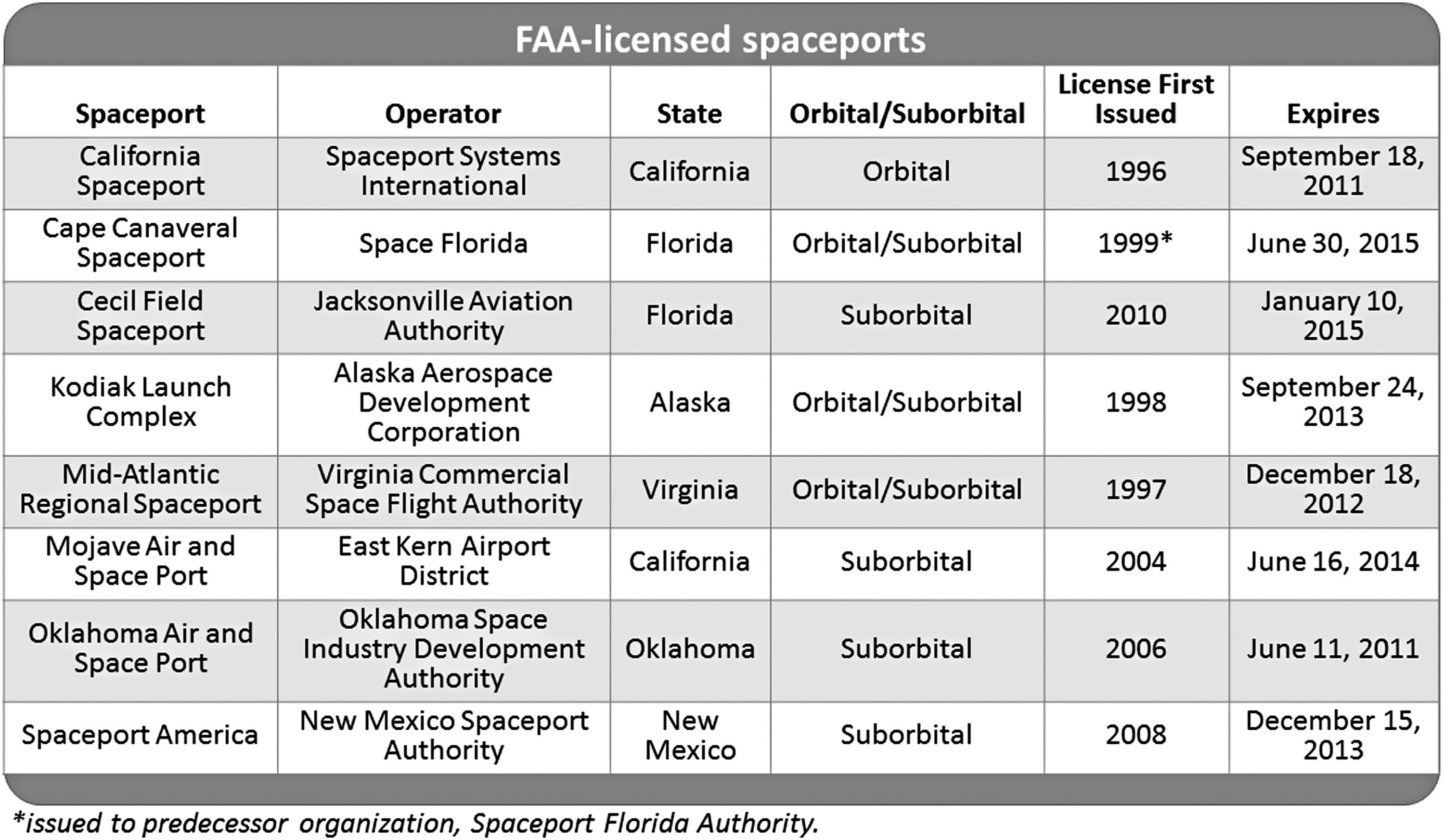

While not the focus of this study, complementary products are relevant to the proliferation of CST. Sometimes referred to as Porter's sixth force, complementary products are extremely important to the adoption of commercial space as a point-to-point method of transportation. A complementary product or service is one that is used in conjunction with the existing product or service. The value of both products operating as a system is greater than the value independently. Spaceports present a classic example of a complementary product that needs to thrive in order for point-to-point transportation to become a viable option in CST. Spaceports will dictate the availability of flights between locations and will have an impact on the demand for CST services. With point-to-point space transportation service currently under development, this “sixth” force has an incredible impact on the profitability and attractiveness of CST. While space tourism may eventually develop into a niche industry, the possibility of being able to provide point-to-point transportation will provide a larger overall revenue potential and attract a more substantial set of competitors. In order for this to happen, spaceports must proliferate. There are currently only eight nonfederal FAA-licensed spaceports in the United States (Fig. 5).

FAA-licensed spaceports. FAA, Federal Aviation Administration.

Spaceports are not an integral part for the space tourism market to grow. This experience can use a single spaceport for the entire experience; however, the availability of multiple spaceport locations will allow incumbent space tourism companies to begin to create self-sustainable spaceports and a more viable business model. Spaceports are expensive and are currently not a self-sustainable investment. The power of complementary products is low with regard to commercial space tourism but is extremely high in relation to point-to-point space transportation.

Limitations

The Porter's five forces model is a great method of systemizing a variety of variables that impact overall industry profitability and this author believes that it is a great starting point for understanding the viability of space tourism and of CST. However, industry evaluation and especially the commercial viability are impacted by a variety of factors and the Porter's model is just one model in the much larger call to action.

One of the greatest limitations of using Porter's five forces as a tool is the inexact nature of the model. The tool is meant to provide an overview of the characteristics of the industry. The evaluation criteria are somewhat subjective to the user of the tool and rely on comparisons with other industries. The tool is generalizable to other industries and the results of industry behavior tend to translate effectively. Determining power for each factor is difficult to determine based on its relativity to other markets. Many macroeconomic factors affecting future development cannot be fully integrated into the model. This study incorporates as many of these factors into the analysis as possible to create the suitable recommendation but cannot fully account for any factors that are difficult to identify or quantify. In addition, the five forces model makes the assumption that market demand exists. For the purposes of applying the model in this context, the author also makes this assumption that demand exists and will continue to exist after servicing the pent up demand for the product or service. In referencing existing data and future projections, the author is comfortable making this assumption as a predictive model.

Disclaimer

The conclusions of this study remain those of the study's author and no statement found herein should be attributed to any individual or organization. Participation in this study does not constitute an endorsement of this study or its conclusions.

Footnotes

Acknowledgments

The author thanks the following organizations: Virgin Galactic, XCOR Aerospace, Altius Space Machines, Astrobiotics, Space Angels Network and Space Florida. This report was prepared for the Federal Aviation Administration Office of Commercial Space Transportation. The program manager was Ken Davidian. (This acknowledgment does not attribute any specific statements or positions, nor does it imply an endorsement of this study or its conclusions by any organization, firm, or individual.)

Author Disclosure Statement

No competing financial interests exist.