Abstract

In recent years, the space sector has seen an increasing number of commercial actors leveraging private and public funding to initiate innovative businesses addressing the market with new solutions. European institutions, namely the European Commission through its “Space Strategy for Europe,” and the European Space Agency through its Resolution “Towards Space 4.0 for a United Space in Europe,” expressed their commitment to foster entrepreneurship, stimulate new business opportunities, and boost investment as part of their objective to support a globally competitive and innovative European space sector. To facilitate the emergence of a dynamic entrepreneurial ecosystem backed by investors for the benefit of both public and private European stakeholders, it is essential that the different actors involved share a common understanding of the state of affairs based on tangible indicators. Although this issue has been thoroughly investigated in the United States, assessments from a European perspective have so far been limited. In an attempt to fill this gap, the European Space Policy Institute (ESPI) conducted a study with the objective to collect and consolidate relevant data and information to (1) evaluate private investment in European space start-ups and (2) examine entrepreneurship trends in the European space sector in comparison to trends observed in other sectors. This article describes the methodology and the results of this study.

A New Space Entrepreneurial Movement

The New Space Ecosystem

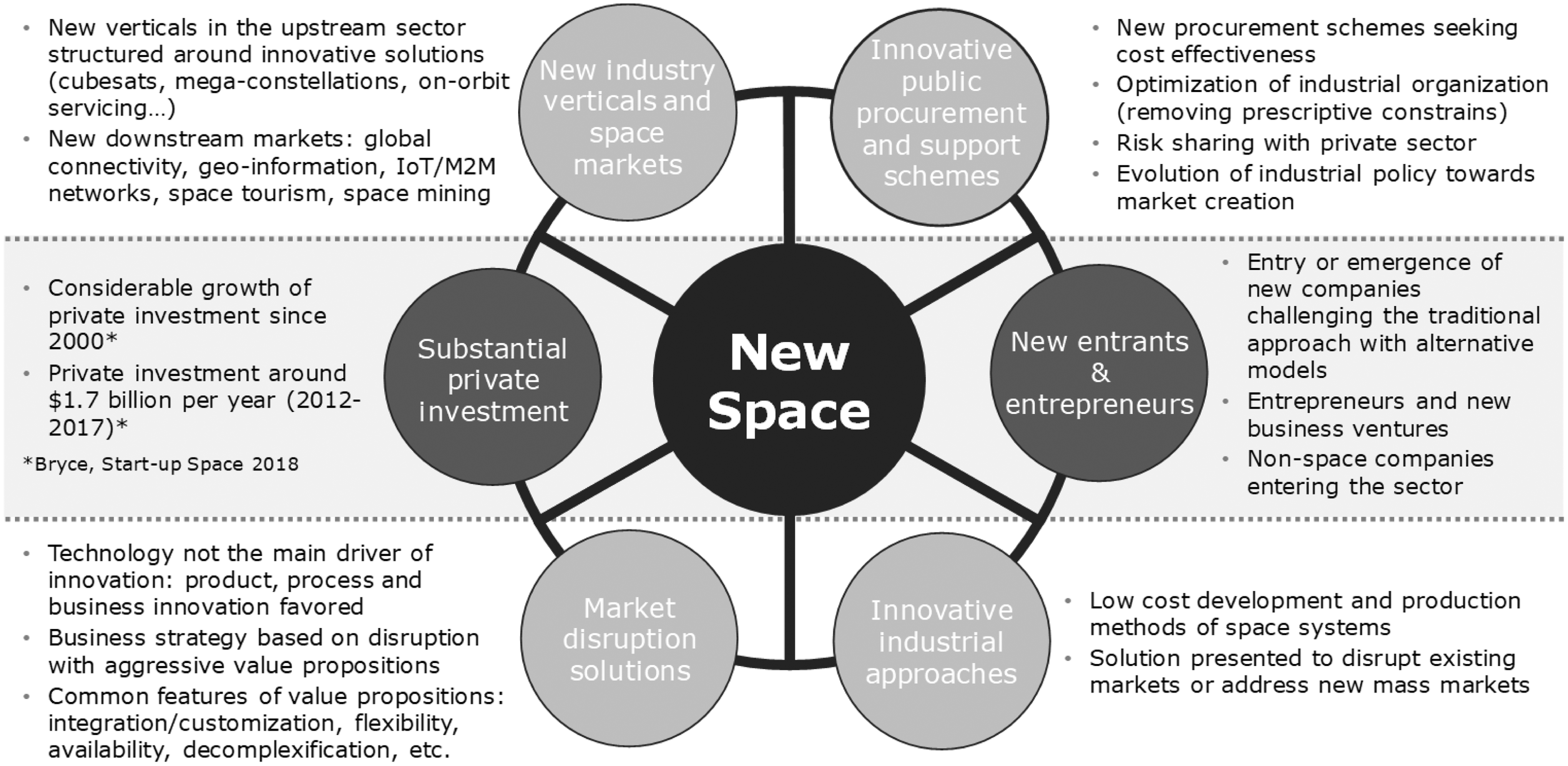

Public investment in space enabled the emergence of a sizeable and dynamic market for space-based services and products. Space capabilities are now widely considered as a key lever for multiple economic, societal, and environmental challenges. In this new context, a disruptive commercially driven approach to space has emerged marked by ambitious announcements and endeavors aiming to engage in space markets with innovative schemes and business models. In this new ecosystem, private actors play a different, more prominent, role both in the implementation of public programs and conduct of space business independently from governments. This development, often referred to as New Space, features various interrelated trends described below:

A previous European Space Policy Institute (ESPI) study 1 demonstrated that New Space trends are tangible and progressively lead the space sector toward a more business- and service-oriented step. This transformation is characterized, among other things, by a growing investment and involvement of private actors, including new entrants and start-ups.

In this context, and although the success and sustainability of the New Space model has yet to be demonstrated, new space ventures have become more attractive to selected investors. Financial markets see a strong potential: Bank of America Merrill Lynch estimated that the value of the space sector could be as high as US$2.7 trillion in 30 years. 2 Several factors are raising the interest of financial markets in the space sector. Among others (Fig. 1):

Key trends driving the New Space sectorial dynamic.

Entry of high profile companies and entrepreneurs.

Strong innovation dynamic with drastically new concepts.

Lower entry costs and quicker time to market (launch services, miniaturized systems, COTS, etc.).

Cross-fertilization of space and ground technologies (autonomous vehicles, 5G, IoT/M2M networks, precision agriculture, smart cities, etc.).

Higher penetration of space-based services and products and anticipated growth of the demand.

Fostering the emergence of a more business-oriented leadership in the space sector is nowadays a dominant consideration for governments who are increasingly eager to explore new approaches to support the economic growth of the sector and take advantage of new possibilities offered by this new dynamic for space programs.

Assessing the Trend in Europe

The European Commission (COM), 3 as outlined in the Space Strategy for Europe 2016, took a firm position seeking to foster a globally competitive and innovative European space sector.

In the same period, the European Space Agency (ESA) and the European Union (EU) issued a joint memorandum on “The future of European space”. 4 Both ESA and the EU shared the goal to “foster a globally competitive European space sector, by supporting research, innovation, entrepreneurship for growth and jobs across all Member States, and seizing larger shares of global markets.” This was reaffirmed in ESA Resolution “Towards Space 4.0 for a United Space in Europe” 5 as result of the 2016 Ministerial Council meeting.

In line with this shared strategic objective, ESA and the EU, and also European governments and their national institutions, introduced a number of initiatives including, among many others, Business Incubation Centers (BIC) to foster successful entrepreneurship in space-related business, innovative mechanisms to engage with space industry (e.g., request for ideas and public–private partnerships), instruments to support commercialization of space technologies and synergies with nonspace sectors, and cooperation frameworks with investors or adaptation of R&D programs to help new and small companies access available public funds.

The impact of these initiatives is usually monitored individually according to relevant indicators (e.g., number of start-ups incubated, funding allocated) but the overall entrepreneurship and private investment trends in the European space sector have not yet been assessed in a comprehensive study. Yet, a more complete overview of the state of affairs in Europe would be extremely valuable to evaluate the impact of public policies and to understand how the entrepreneurship and private investment dynamic can be further coordinated and supported.

It is in this context that the ESPI has initiated this study. Information provided in this report is based on two complementary tools:

The ESPI investment database gathering all available data on private investment in European space start-ups for the period 2012–2018. The ESPI space entrepreneurship survey to collect the views of European space start-ups on their business situation, on the European ecosystem and on their expectations for the future.

Methodology and Scope of the Research

Definitions and Scope

The following definitions and categories were applied to delineate the perimeter of analysis:

• Start-up: a start-up is usually defined as a company younger than 10 years, whose business tend to feature innovative concepts and models and who has not yet reached business maturity (defined according to the business stage: Public Offering, annual turnover or number of employees). For the purpose of this study and given the usually longer timeframe to reach business maturity, ESPI included companies founded after the year 2000. Business maturity (end of the start-up stage) is considered achieved if the company meets one of the following criteria 6 :

○ Acquisition or Public Offering: the company has been acquired or listed on a stock market.

○ Turnover: the annual turnover exceeds €50 million or the annual balance sheet total exceeds €43 million.

○ Number of employees: the total number of employees exceeds 250.

• Space company: For the purpose of this study, a company was considered a space company if the main business of the company (in revenue share) is part of the space value chain. For this definition, the study followed the Seraphim's Spacetech Market Map 2018, 7 which divides space activities into three segments:

○ Upstream: Build, Launch, Satellites.

○ Downstream: Downlink, Analyze, Store, Product.

○ Beyond Earth: Space Exploration, Space Resources.

• European company: For the purpose of this study, a company was considered European if the headquarters are based in Europe (EU + ESA Member States), or if a majority of its business operations is conducted in/through Europe, a feature that implies, for instance, the eligibility for EU funds.

In a number of cases, the classification of a company as a European space start-up required an arbitration because of the business setup (e.g., multiple headquarters addressing different regional markets), situation of the company (e.g., dormant company founded before 2000 but with a net business acceleration after 2000 and following a start-up behavior), or nature of business (e.g., space is part of the products and services portfolio but not a core market).

To classify sources and types of investment and ensure coherence with existing authoritative studies, ESPI selected the categories used in Bryce's Start-Up Space 8 report series.

Categories of investors include the following:

Angel investors: “individual or families (to include family offices) that have accumulated a high level of wealth and seek potentially high returns by investing in ventures during their early stages.”

Venture capital firms (VC): “group of investors that invest in start-up, early stage, and growth companies with high growth potential, and accept a significant degree of risk.”

Private equity firms (PE): “formed by investors to directly invest in companies,” typically in established ones.

Banks: financial institutions supporting investments including but not limited to loans and debt financing.

Corporations: investing in, acquiring, or merging with start-ups.

Accelerators and incubators: providing funds, knowledge, and infrastructure to early-stage companies and start-ups.

Categories of investment include the following:

Seed/prize/grant: Funding received by a start-up at seed stage/early stage of development, usually including angel and business incubators' investments.

Acquisition: Situation whereby one company purchases most or all of another company's shares in order to take control.

Debt financing: Process of raising money by selling debt instruments to individuals and/or institutional investors (e.g., banks).

Private equity: Investment consisting of capital that is not listed on a public exchange.

Public offering: Process of offering shares in a private corporation to the public.

Venture capital: funds invested by VC firms, usually with medium-term stakes, for high profit, high-risk activities.

ESPI Private Investment Database

The assessment of private investments is based on a dataset including exclusively publicly available data on announced operations and deals.

Information is collected by screening a high number of sources including investment firms', incubators', and accelerators' portfolios, articles, and specialized news outlets or specialized sources such as CrunchBase. Cross-checking was systematically performed. ESPI database includes deals for the period 2014–2018.

ESPI Space Entrepreneurship Survey

The analysis of the European entrepreneurial ecosystem is based on the results of a dedicated survey to European space start-ups. To allow for a benchmarking of results with other start-ups ESPI survey was adapted from the European Start-up Monitor 2016 (ESM16) survey, and consisted of 40+ questions organized into five main sections including:

Identity of the respondent and of the company.

Business of the company, including views on expectations for the future.

External financial support received and planned to be received in the near future.

External nonfinancial support received and planned to be received in the near future.

Views on the business environment of the company with a focus on the European entrepreneurial ecosystem, challenges, obstacles, and expectations for governmental support.

Responses have been aggregated through multiple answers questions, scores and open comments of the respondents providing additional insights on their reply.

ESPI sent this survey to 300+ companies matching “European space start-up” criteria and received a total of 64 completed responses from 16 countries.

Private Investment in European Space Start-UPS

General Overview

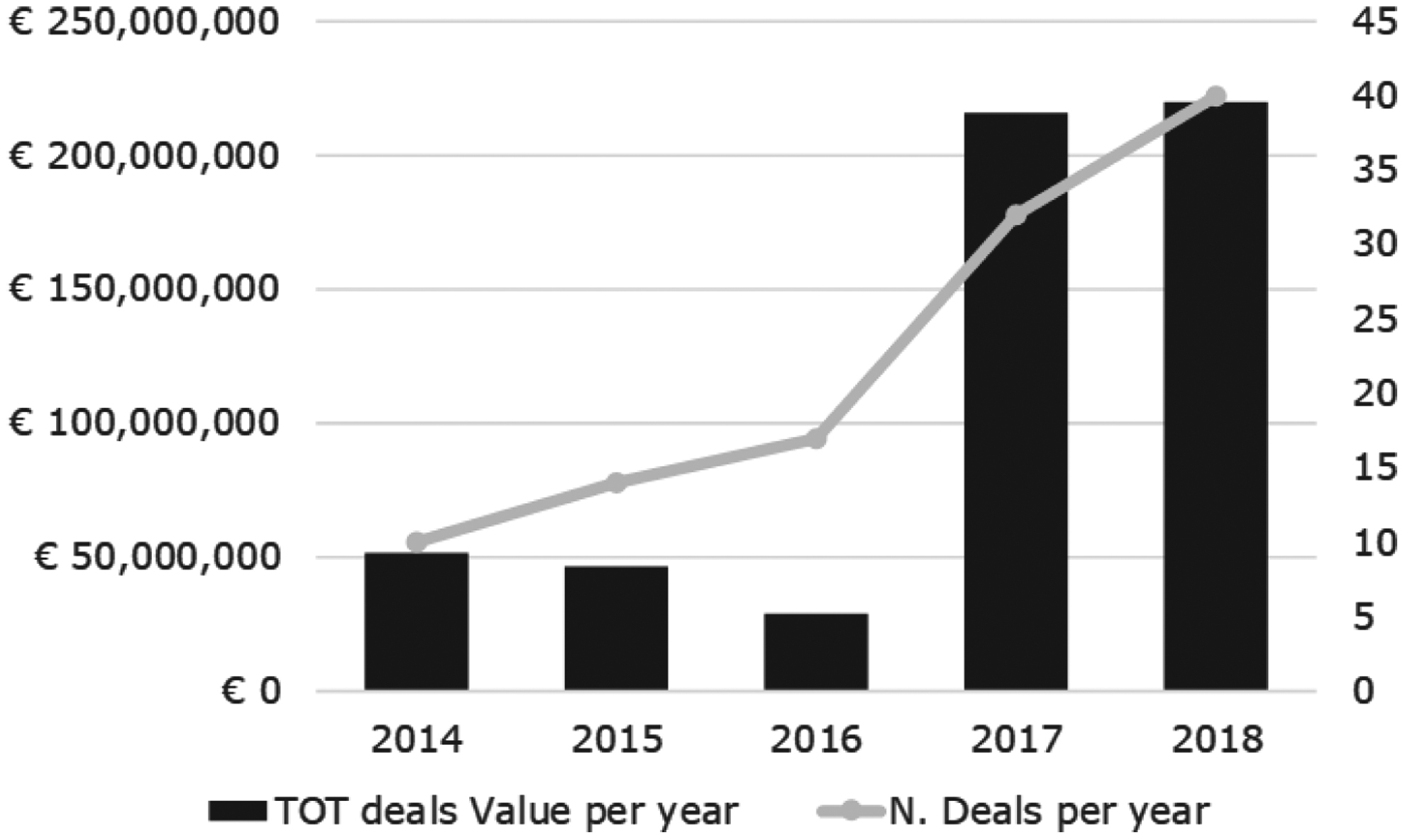

Over the period 2014–2018, 113 private investment deals concerning European space start-ups were recorded for a total amount of €562.7 million (Fig. 2). This value does not include investment in space ventures after they have successfully reached maturity (according to the definition). Involving megadeals in the tens or hundreds of millions of euros, the total value of private investment in European space ventures, including mature ones, would reach €1,783.6 million on the period.

Number and value of deals per year.

A new record high was hit in 2018 both in terms of number of deals and of total value: 40 private transactions were recorded (+25%) for a total value of €219.5 million (+2%). This is a conservative estimation as the value of some transactions was not disclosed.

A significant share of the private investment value is actually concentrated in only a few transactions. In 2017, 65% of the total investment was mobilized in only four deals greater than €20 million. Similarly, in 2018, five deals surpassed €20 million, representing 64% of the total volume private investment in European space start-ups over the year.

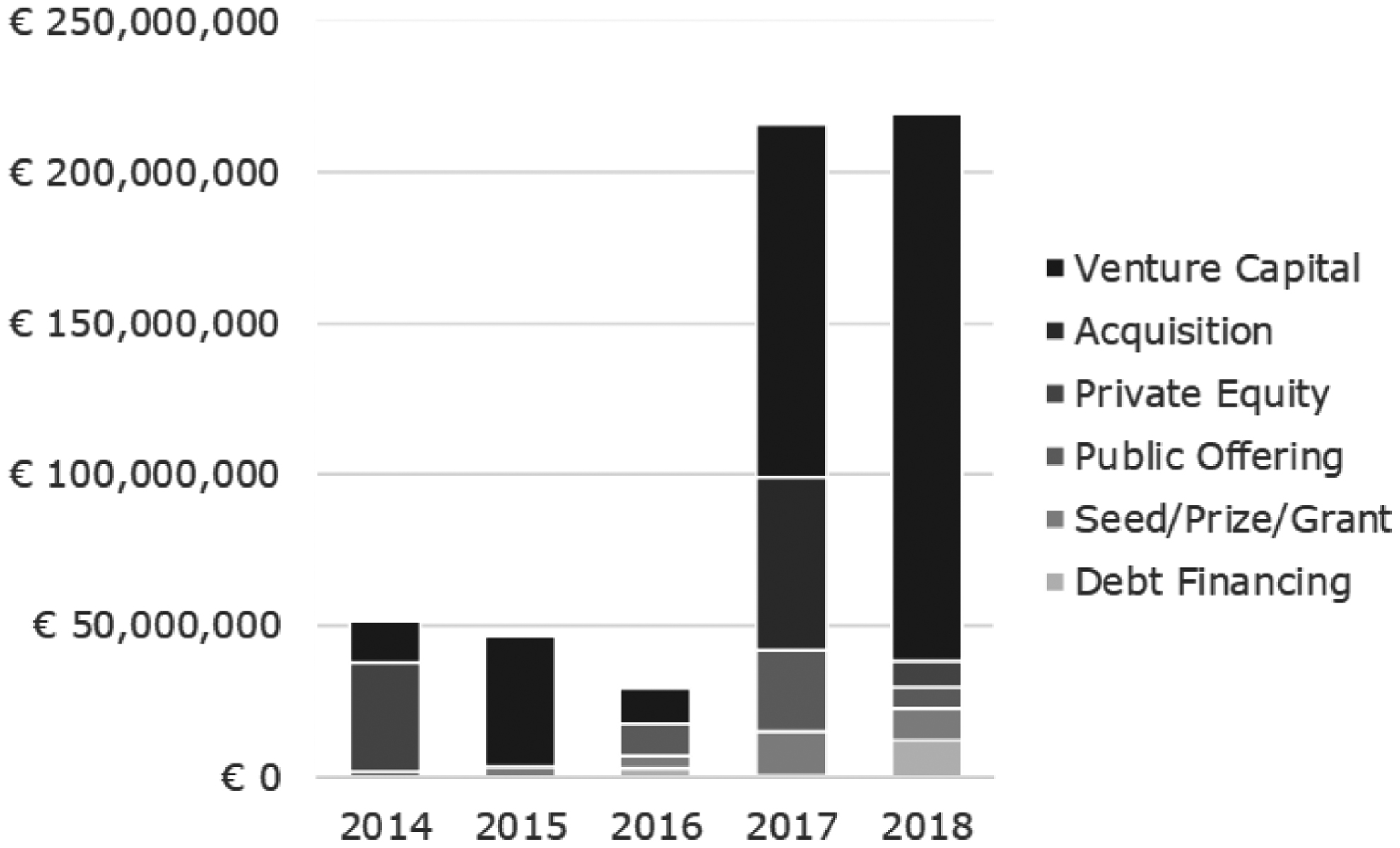

The distribution of investment value per category shows that Venture Capital (VC) remains the main form of private funding for start-ups, with a total of 48 deals and €365.8 million invested (65% of the total amount) over the 5 years. This trend was confirmed in 2018 (Fig. 3) with a total VC invested in the European space sector in the order of €181.3 million (+56%). This year, the share of VC reached 83% of the total value of private investment.

Value of investment by category and year.

On the other side of the spectrum, debt financing represented only 3% of the total investment. Seed financing, prizes, and grants (private only) involve smaller transactions for start-ups at a very early stage to help kicking-off the business. This category amounted to €34.8 million for 39 operations over the period. Other investment categories involve a few big operations. For example, acquisitions represent 10% of the total investment value with only four operations recorded on the period. The value of the deals was announced for only two of them, namely the acquisition of Wireless Innovation by Lyceum Capital and Clyde Space by ÅAC Microtec. Together these two deals accounted for €57.3 million.

Similarly, four public offerings were documented, involving ÅAC Microtec and GOMSpace in 2016, the German Mynaric in 2017 and the Luxembourgish Kleos Space in 2018, for a total value of €44.9 million. Lastly, a vast majority of private equity value on the period concern an investment in O3b Networks by SES in 2014 (i.e., O3b was still a start-up), and an investment in Unseenlab in 2018.

Overall, private investment in space start-ups is four to eight times smaller in Europe than in the United States, according to the boundaries of the assessment (i.e., definition of “start-ups”). Consistent with the difference in space budget and market sizes, this ratio confirms the good orientation of Europe toward the development of space entrepreneurship.

Distribution of Investments in Europe

The distribution of investment by start-up country (Fig. 4) shows a discrepancy between the level of entrepreneurship and public space budgets. Although France and Germany still count with a good level of investment, it is in the United Kingdom, Ireland, and Finland, three countries with much smaller space budgets, that the highest investment volumes were recorded.

Distribution of private investment value per country (location of start-up headquarters).

Many factors are at play here and each country presents a different profile. With both a strong start-ups and investors base, the United Kingdom, stands out as a clear leader of the space entrepreneurship trend in Europe. The country counts with a large number of start-ups addressing different space markets and with many investors active in the space sector. Over the period, a total of 50 deals accounting for €343.6 million were recorded in the United Kingdom. The country represents, alone, around half of the European market of private investment in space start-ups. In the case of Finland, however, most of the investment is related to a single successful company: ICEYE. Over the period, this start-up raised alone, in a series of investment rounds, more than €56 million. Ireland also owes its position to a single megadeal of €50 million involving an undisclosed consortium of Hong Kong-based investors and the Irish start-up Arralis.

Luxembourg continues to reap the rewards of its ambitious strategy to foster entrepreneurship and private investment in the country. Over the period, more than €40 million of private investment were recorded with Kleos Space and O3b leading. This is a conservative estimate that excludes private investment in foreign start-ups that set up an office in Luxembourg like iSpace.

France and Germany also reported more than €40 million of investments over the period. Although the level of private investment in space start-ups may likely be lower due to the presence of well-established players, a steady growth of the level of entrepreneurship since 2014 can be observed.

Important deals were also recorded in other countries like Spain, Denmark, Italy, Switzerland, Sweden, Austria, and the Netherlands, showing widespread entrepreneurship dynamism across Europe.

Distribution of Investments Along the Space Value Chain

Considering the position of start-ups in the space value chain, the study found that investment has been primarily directed toward the upstream segment (Fig. 5).

Investments breakdown by Space Value Chain Segment.

Major deals in this segment recorded in 2018 include Orbex (Launch, €34 million), ICEYE (Data, €29 million), and Oxford Space Systems (Build, €7.6 million). With the emergence of new vertically integrated business models, a number of investments in the upstream ultimately impact the downstream sector as well by supporting companies who commercialize services enabled by those same satellites (e.g., ICEEYE, Hiber, Earth-I). As for the downstream segment, the largest amount of investment was directed toward downlink related industries. In particular, two deals make up more than half of the investment in the downlink sector over the reporting period: Mynaric's IPO in 2017 and an investment in Goonhilly Earth Station, with the two deals amounting to more than €27 million each.

It appears that the investment in the upstream segment is more than twice greater than the investment in the downstream segment. This conclusion is in line with comparable assessments from other studies. However, it is important to note that a strong bias exists due to the difficulty to track investments in the downstream sector, which involves companies whose service and product portfolio is not entirely embedded in the space value chain. Indeed, companies providing storage or processing capabilities rarely address the space sector as a core customer. Comparably, space capabilities or data are often one input among others for companies delivering solutions to end users.

A similar situation can be observed, although to a much smaller extent, in the upstream segment for companies offering equipment, components or engineering services to customers involved in a range of different industries. As a result, a number of private investments in European start-ups with some space-related business are not included here due to the difficulty to identify these companies and establish a clear link between the investment and the development of space products and services. This also suggests that the space sector benefits greatly from investments in other sectors, particularly in the downstream segment. With a growing cross-fertilization between space and terrestrial technologies, the distinction between investment within and outside the space sector is poised to become increasingly blurred.

Start-Ups Views on the European Space Entrepreneurial Ecosystem

Overview of Survey Respondents

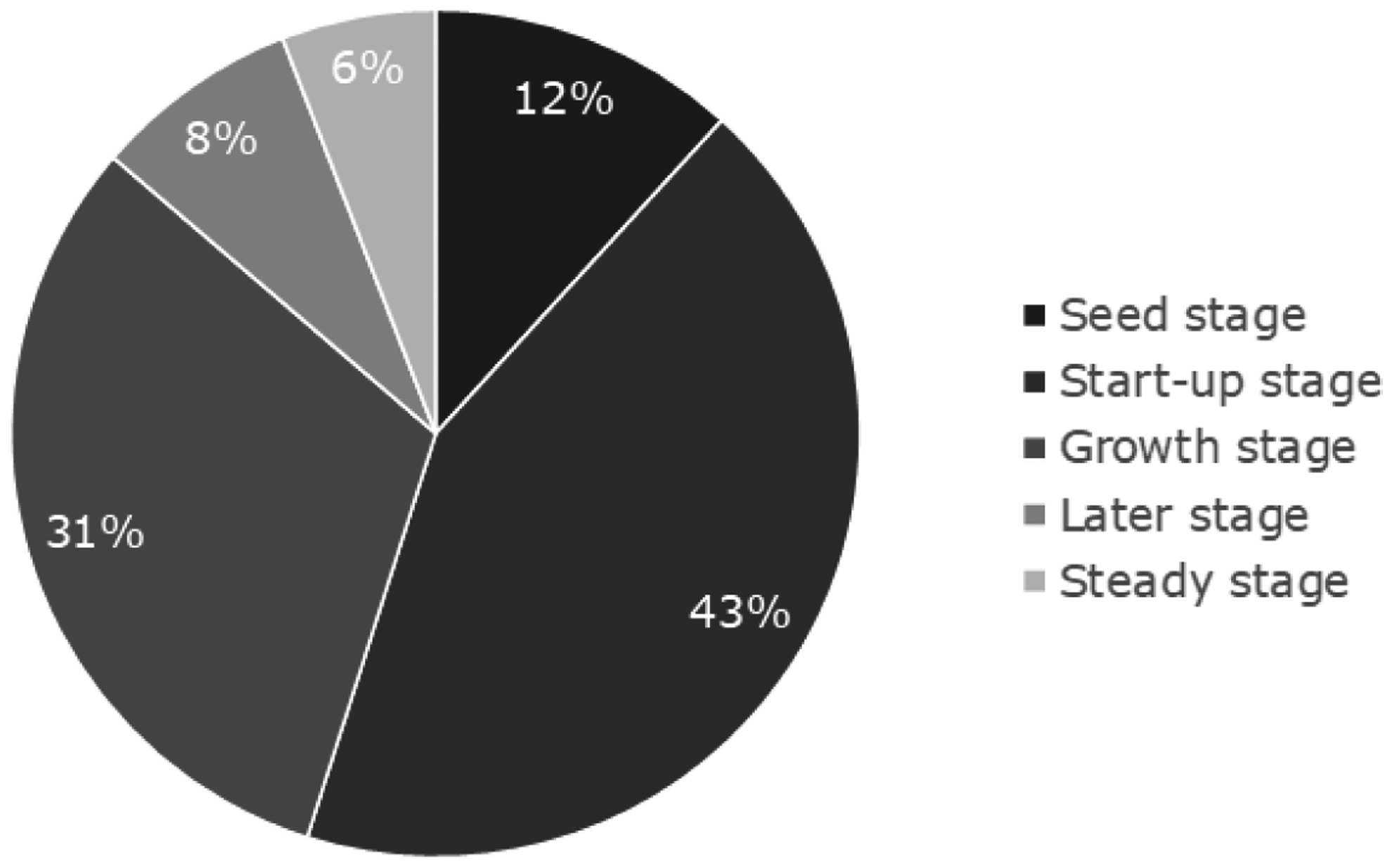

Out of 64 start-ups having replied to the survey, 56% were founded in the last 5 years, and a total of 85% of were less than 7 years old. The small number of companies older than 7 years may be explained by both the high failure rate of young businesses but also the growing number of new space ventures. In line with the average age of the companies, the majority (55%) of them is in early stage of development, with 12% at seed stage and 43% at start-up stage. More interestingly, and despite their average age, 45% of them already declares being at growth, later or even steady stages of business development (Fig. 6).

Respondents by business stage.

Focusing on the origin of these companies, 55% of them were founded as independent venture, and 35% as a spin-off, with nine companies having emerged from the academic sector. The remaining 10% includes various origins as ventures established following a company take over, and created to run nonprofit associations.

Respondents are all Small and Medium Enterprises (SMEs), with the largest one employing 78 workers while 18% of respondents have no employee, relying exclusively on the founder(s)'s workforce. Only 14% of the companies have more than 20 employees and the biggest share of the ventures (38%) currently employs between 1 and 5 staffs. A vast majority of these start-ups (84%) plan to recruit at least one additional employee within the next 12 months.

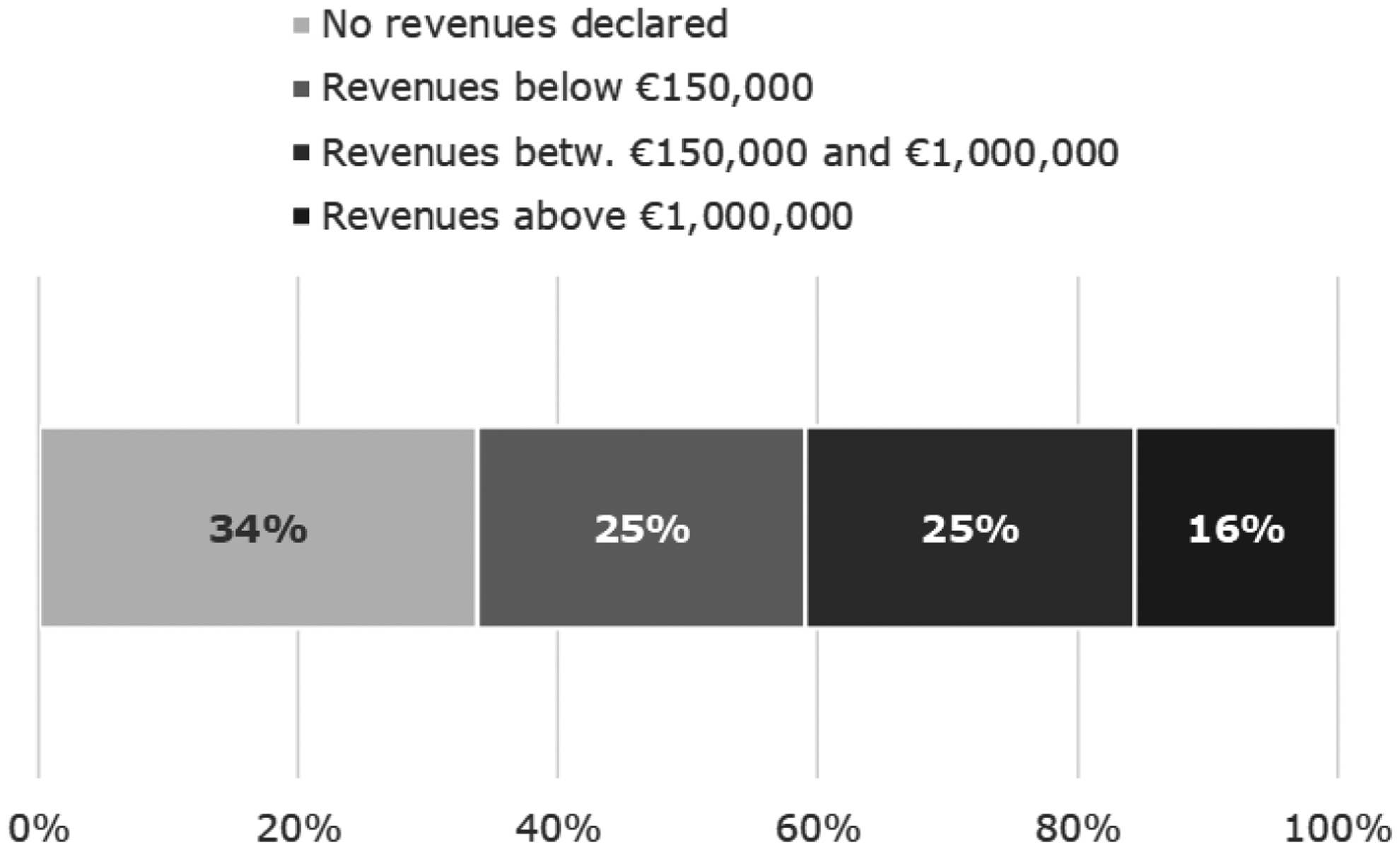

The disparity of start-up profiles can also be appreciated in terms of revenues (Fig. 7). While a majority of European space start-ups generated a revenue from their business activities over the last fiscal year, with 50% declaring a revenue below €1,000,000 and 16% above, still 34% of start-ups had no operating revenue yet. A third of start-ups rely therefore exclusively on financial support and seed investment to function.

Start-ups declared revenues (FY17).

Looking at the geographical distribution of the respondents, a majority of them (68%) are established in five countries: The United Kingdom, the Netherlands, Germany, Italy, and France. However, it is worthy to note that overall ESPI survey collected information from start-ups located in 16 different European countries. Unsurprisingly, this mirrors the overall European activities in the space sector, both commercially and institutionally, via the activities of national/supranational space agencies, and the results of the private investments database.

Perspectives on Space Start-Ups Business

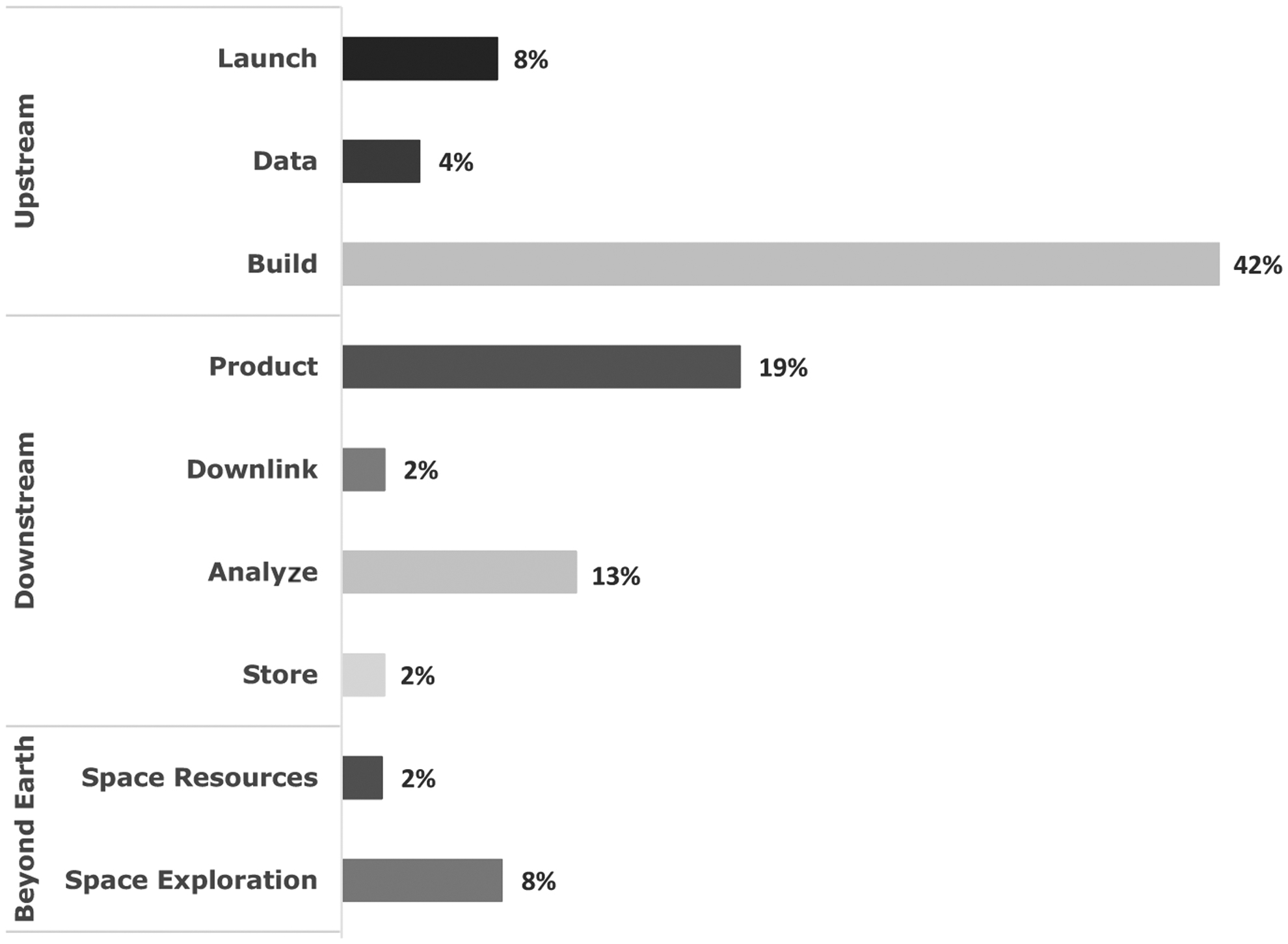

Looking at the core business (Fig. 8), 54% of the firms interviewed operate in the upstream segment of the space value chain, while 32% is focused on the downstream segment. In particular, almost 40% of the respondents are part of the Build segment, followed then by the downstream segments Product and Analyse. Hardware production and engineering for the upstream segment remain the most common space-related activities among young space ventures.

Core business, percentage of respondents.

As a matter of fact, a comparison of ESPI survey results with the findings of the ESM16, 9 which addresses all European start-ups, shows that Space start-ups are radically more innovative and international than other European start-ups.

European Space Start-ups are largely innovation-driven: 71% of these companies offer a product that is a worldwide innovation whereas only 52% of all European start-ups achieved the same result. In addition, 60% use globally pioneering technologies and respectively 47% and 41% implement innovative business models and industrial processes.

In terms of global reach, 63% of space start-ups address the global market and only 8% are confined to their domestic market, while only 24% of all European start-ups offer their solution on global markets.

With regards to their business situation, respondents shared a rather positive and optimistic evaluation with 75% estimating that their company is in a satisfactory or good business situation and 82% anticipating an even better scenario in the future (Fig. 9). Likewise, one enterprise out of two considers being in a better condition than in the past. This optimistic outlook on business development and growth mirrors the intention of a vast majority of European space start-ups (84%) to hire in the next 12 months.

Past, current, and expected business situation.

Start-Ups Challenges and Expectations from Public Actors

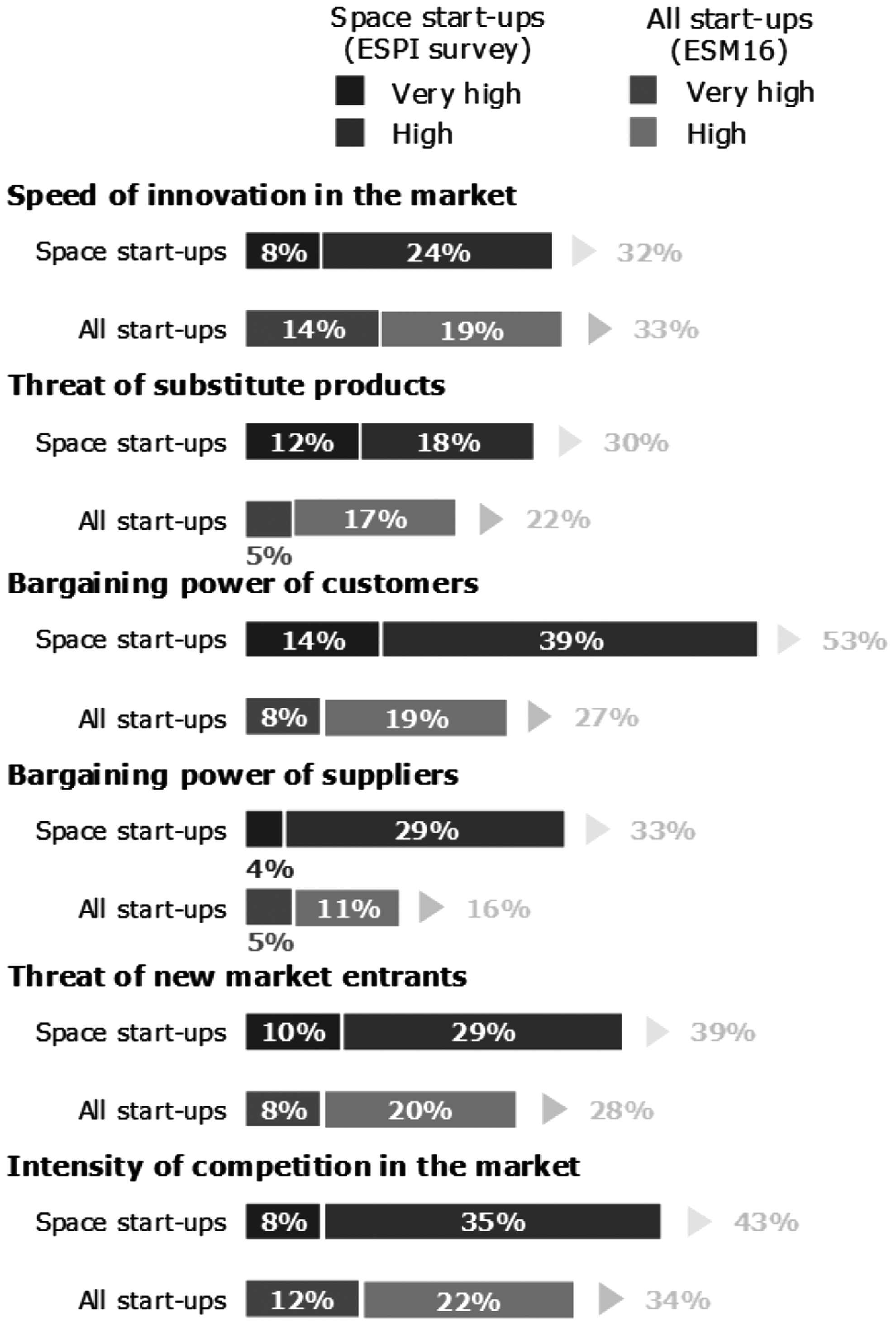

With regards to market dynamics, space ventures are less confident than other European start-ups who consider their own industry and market richer in opportunities (respectively 75% and 81% for innovation and commercialization opportunities). Difficulties faced by European space start-ups with the demand side are amplified by a strong bargaining power of customers. While only 27% of European start-ups, regardless of their industry, consider the bargaining power of their customers rather high, it is the case of 53% of space ventures. In addition to the reluctance of costumers in space markets to adopt new, unproven solutions various factors can explain this strong bargaining power: a market that is not yet mature (low demand and lack of awareness), a demand that is concentrated (core market made up of a few customers) or a situation of oversupply (offer higher than demand) among many others (Fig. 10).

Views on market forces (space vs. all start-ups).

Space start-ups actually perceive their business environment as rather hostile. A significant share of them identified additional threats including an intense competition (43%), a strong bargaining power of suppliers (33%) and the potential entry of new entrants (39%) or substitute products (30%) on the market. A larger share of space ventures is concerned by these threats than in other industries. This assessment contrasts very much with the optimistic outlook on the future of their business development and growth. This also suggests that European space start-ups consider being well equipped (or backed) to succeed, even in a complex competitive landscape.

Start-ups rely extensively on financial and nonfinancial support from various private and public actors. Overall, 89% of start-ups benefited at least from one type of backing and 38% benefited from both financial and nonfinancial instruments.

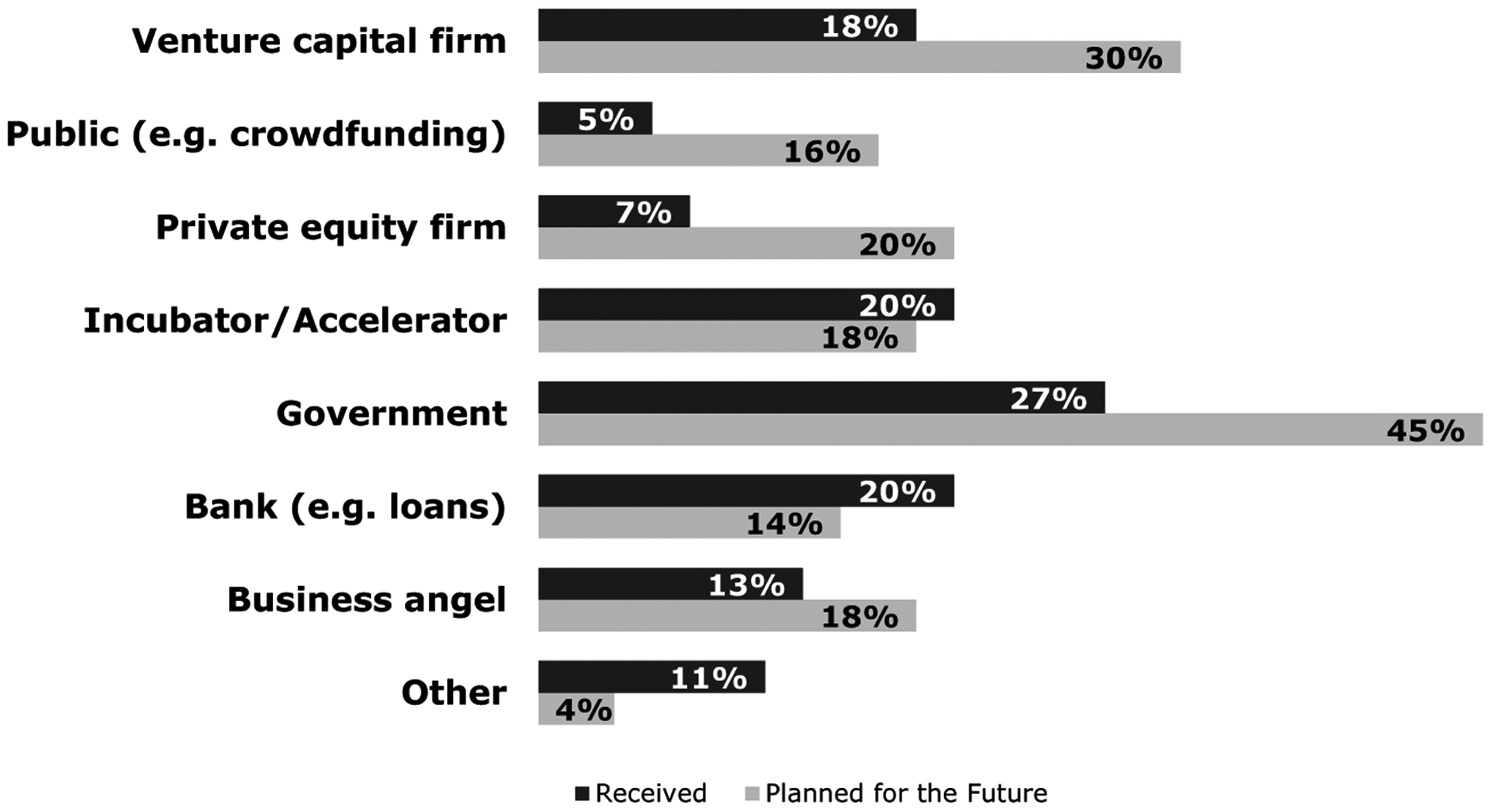

Overall, 60% of start-ups have already benefited from at least one type of financial support from a public or private organization. Survey results (Fig. 11) show that governmental support (not included in ESPI investment database) is the most common form of financial help for European space start-ups with 27% of them having already benefited from public instruments (mostly grants) and 45% planning. On the private side, banks, incubators, and accelerators are the most used sources of capital.

External financial support.

Overall, 78% of start-ups still seek financial support. Governmental support schemes are here again the favored option (45%), confirming the prominent role of public funding in the European space entrepreneurship ecosystem.

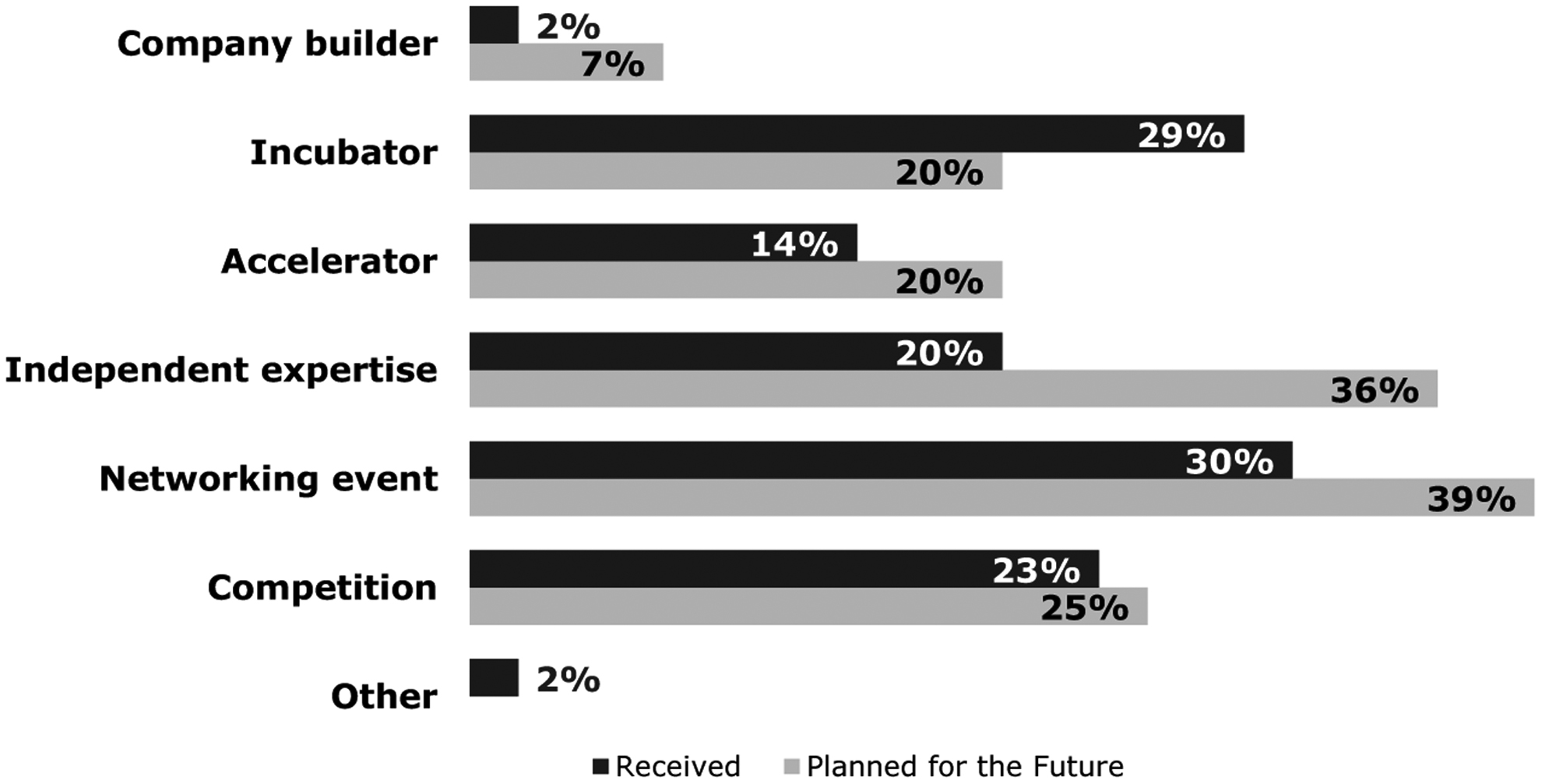

As for external nonfinancial support (Fig. 12), 56% of start-ups already benefited from nonfinancial backing including competitions (e.g., hackathon), networking events, accelerators, incubators, or independent expertise. This form of support seems, however, less sought after than financial help with only 60% of start-ups looking for it. Among existing instruments, networking events (30%), incubators (29%), and competitions (23%) are the forms of nonfinancial support most benefited from.

External nonfinancial support.

For the future, start-ups seem most interested in networking events (39%), independent expertise (36%), and competitions (25%). This mirrors the very positive opinion that start-ups have over these instruments. Eighty-two percent of start-ups consider that networking events are beneficial. This share rises to 91% for independent expertise and as high as 100% for competitions. Such enthusiasm is not shared for incubators and accelerators with 23% of start-ups considering that these instruments bring limited benefits.

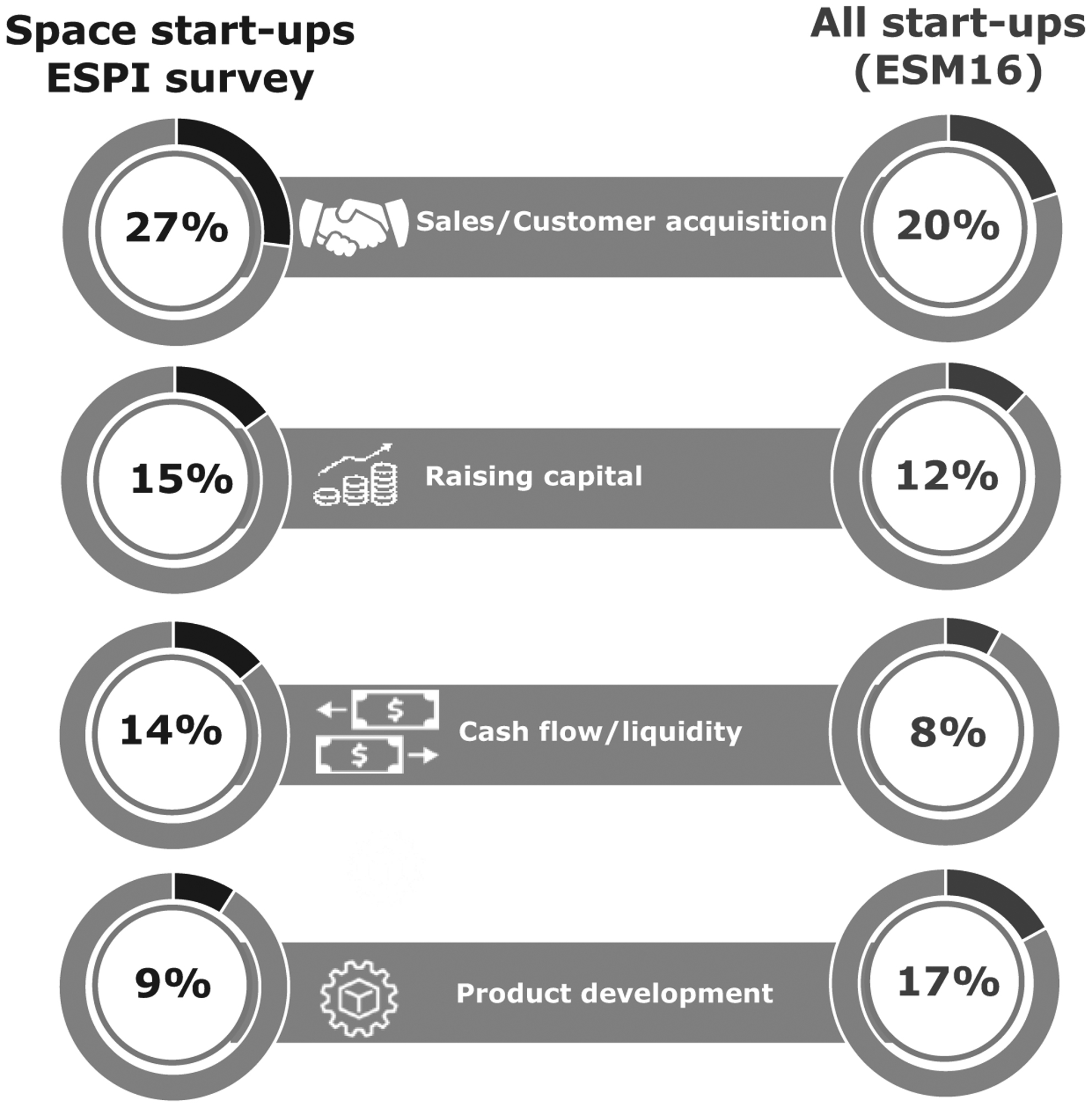

With regards to start-ups' main challenges European space start-ups highlighted their difficulty to acquire customers and sell their solution (27%), to raise capital (15%), and to manage liquidity and/or cash flow (14%). On the other side of the spectrum, start-ups tend to perceive acquisition of staff (7%), growth (6%), and internationalization (5%) as less challenging. Benchmarking space start-ups' views with other European start-ups (ESM16), underlines a profound difference in the perception of challenges (Fig. 13). Customer acquisition, also the top challenge for other start-ups, appears to be a much more significant concern for space ventures. This is also the case for capital raising and management of liquidity and cash flow, which are not even in the top three challenges of other start-ups. The challenge to raise capital reported by space start-ups is consistent with the fact that 78% of them are actively seeking financial support.

Business challenges of space and other European start-up.

Finally, Figure 14 ranks expectations of European space start-ups from politics and benchmarks them with those of all start-ups.

Expectations from public actors.

Comparably to other European start-ups, space ventures also consider that some efforts should be made in the field of red tape reduction to relieve these very small and young companies from what is perceived as an administrative burden diverting workforce from core business activities. In the same vein, space start-ups, alike others, call for a reduction of taxes.

The main difference between the space sector and other industries lies in expectations in all other fields. European space start-ups clearly have higher expectations from governments than others. At least a third of respondents estimated that improvements could be made across all themes addressed by the survey.

It emerges that space start-ups desire a much more entrepreneurship-friendly environment that would feature the following:

Improved exchanges between politics, start-ups, and established companies.

Better cultural acceptance for entrepreneurship and understanding of the need of start-ups.

Survey results also show that start-ups in the space sector need (or expect) more support from governments than others for the conduct of their business and for access to finance. More than half of space ventures expect some support from public authorities to get VC while it is the case of only 30% of other European start-ups.

Key Findings and Conclusions

Tangible Trends in Europe

The study provides evidence of a tangible private investment and entrepreneurship dynamic in the European space sector, suggesting a good orientation of Europe toward the development of new commercial space trends. However, the vast majority of space start-ups interviewed (78%) are still seeking additional funding to develop their products and they expect to be supported from public actors. More specifically, the following key findings can be underlined:

Private investment in European space start-ups exhibits a massive growth since 2014 reaching a new record high in 2018 with €219.5 million invested.

Investment value is mostly concentrated in a few large transactions. In 2018, five deals exceeded €20 million reaching together €141.3 million and representing 64% of the total investment value over the year.

Space entrepreneurship dynamism is widespread across Europe with a few top countries. Space investment deals worth >€1 million were recorded in 13 European countries. Nonetheless, among top European countries, the United Kingdom stands out as particularly successful.

There is a limited correlation between national public space budgets and the intensity of domestic entrepreneurship due to multiple forces at play, such as domestic entrepreneurial and financial ecosystems, national policies, industry, market, and macroeconomic forces.

Investment in the space sector is fuelled by synergies with other sectors particularly true for the downstream segment.

The average European start-up is led by two to three founders and employs nine people; plans to recruit five people in the next 12 months; generates an annual revenue of €500,000.

Space start-ups are radically more innovation- and global-oriented than other European start-ups; 63% of space start-ups address global markets/in comparison, only 24% of “non-space” start-ups address global markets.

The space sector offers a fertile ground for entrepreneurship; start-ups consider the space sector rich in opportunities both for innovation (62%) and commercialization (60%).

As compared to other sectors, space start-ups perceive their business environment as rather hostile but are confident in their growth perspectives. This suggests that European space start-ups consider being well equipped (or backed) to succeed, even in a difficult business environment.

Space start-ups expect financial and nonfinancial support, in particular from public sources.

Space start-ups highly value networking and mentoring; this finding supports the recommendation by the European Investment Bank to organize a dedicated annual event for space start-ups.

For space start-ups gaining customers and securing sales is a greater challenge than raising capital, mirroring the perception of a very strong bargaining power of customers in the space sector.

Space ventures expect (or need) more support from governments than other start-ups for the conduct of their business and for access to finance; space ventures also call for a reduction of administrative burden (60%) and tax (57%) but not more than other start-ups.

Role of Public Actors

European institutions have been particularly proactive to operate a cultural change and launch new initiatives adapted to the needs of start-ups. This considerable effort is shared by the ESA, EU, national institutions, and other public bodies. In line with their respective strategies, the approach adopted by public actors lies principally in the following:

Stimulating business opportunities; that is, competitions, strategic partnerships, and others.

Supporting product and technology innovation: that is, public grants, incubators, independent expertise, and others.

Helping to raise capital: that is, public funding (grants, loans, subsidies, and prizes), partnerships with investment firms/institutions, and others.

Building networks: that is, hubs, conferences, business missions, and others.

Today, European institutions actively support entrepreneurship in the space sector and, although there is still room for improvement, their effort is now yielding concrete results. Notwithstanding, existing instruments support principally the offer side: they are particularly effective in early stages of product and business developments but show some limits when getting closer to the market.

In light of the strong challenges faced by start-ups to gain customers and secure sales, support on the demand side would be recommended through three complementary actions:

Stimulate the demand for space-based solutions in Europe: Public actors already actively promote the market uptake of space-based solutions but much could still be done to leverage institutional demand. In the United States, public markets are a pillar for the business development of new space ventures. The use of anchor tenancy,* an arrangement bridging public needs and support to business, proved to be a very effective instrument to bring up the confidence of entrepreneurs and investors. It has no equivalent in Europe.

Promote a European single market: Large markets are essential for new space ventures to transform commercial opportunities into profitable and sustainable businesses. In Europe, national demand rarely offers the required critical mass. A European single market for space (based on demand aggregation and compatible regulatory frameworks) should be promoted.

Drive the demand to support innovation and growth in Europe: Benefits from an aggregated European demand would be maximized by a policy promoting a European offer when suitable. Although the relevance of such approach is undisputed, the difficulties faced by the EU to explore its application in the field of access to space highlight how much competitive partiality is contrary to the fundamentals of the EU (i.e., Open Competition, Technology Neutrality, etc.). Yet, here again, the principles of the Buy American Act, which makes an obligation to the U.S. federal administration to give preference to U.S.-made products, extensively applied in the space sector, has no equivalent in Europe.

Footnotes

Acknowledgments

The authors are grateful to the stakeholders who engaged with ESPI during the realization of this study. A special mention goes to the companies who answered the survey and dedicated part of their time to provide useful insights into their business.

Author Disclosure Statement

No competing financial interests exist.

Funding Information

No funding was received.