Abstract

The establishment of permanent human activities on the Moon is envisaged as a stepping stone for future space exploration and for the expansion of mankind in the solar system. Lunar in situ resource utilization (ISRU) will not only play a crucial role in extending human presence in space but also has the potential to strongly benefit life on Earth and to boost new interplanetary economy. As a recent study on lunar ISRU and commercialization, the LUnar Propellant Outpost (LUPO) envisioned a program devoted to liquid oxygen (LOX) production and selling, aiming at generating profits mainly refueling space missions, along with other minor revenue streams. The present article deepens the analysis of LUPO's business plan starting from the program's findings for the fiscal year 2018. Evidences estimating the water mass fraction inside Shackleton Crater as high as 25% are taken as new reference in updating cost and selling prices of LOX both on the Moon surface and in orbit, with respect to last projections based on a 5% fraction. All the costs related to ISRU and LOX production implementation, which are heavily affected by technological solutions, have also been revised. Competitor's analysis and breakdown are refreshed on the basis of the latest advancements in launch-related costs and refueling alternative concepts. The importance of secondary revenue streams is assessed in higher detail, particularly regarding liquid hydrogen production, gaseous oxygen and hydrogen production, water production, and infrastructure utilization by third parties. Finally, a trade-off of new income sources is carried. Selling dehydrated regolith from ISRU processes as a building material is considered. The production of multimedia and digital products based on life and activities on the Moon, such as documentaries, live-streams, and a virtual reality program based on the images sent back to Earth, is considered for outreach and profit generation perspectives. Astronaut training for future Mars missions could also be performed on the Moon, generating an additional revenue stream. This study is carried out within the framework of the 11th edition of the international Specializing Master programme in SpacE Exploration and Development Systems (SEEDS) of 2018/19 at Politecnico di Torino (Italy), in cooperation with students from ISAE-Supaero (France), and the University of Leicester (United Kingdom). The project is supported by Thales Alenia Space Italy, the European Space Agency, and the Italian Space Agency.

Introduction

In the past, space was the futuristic last frontier of humankind's dreams of exploration and one of the most exotic and fascinating subjects of curiosity and speculation.

The increasing efforts of nations and public space agencies have brought humans in close contact with space through ambitious and inspiring achievements that have contributed to Earth's prosperity.

Today, space is experiencing an exponential increase in the speed at which it pervades the realm of daily life. Sustained by unceasing technological breakthroughs and dynamic cooperative programs, marvelous futures are constantly unveiled for all the domains of human activities.

This article offers a business analysis of a LUnar Propellant Outpost (LUPO). As one of the most interesting pieces of space infrastructure currently discussed, agencies and companies alike are interested in the high technological return, business opportunities, and great mission enabling potential.

The Moon is rapidly becoming the center of numerous space initiatives for the future years, committed to providing and advancing the capabilities required for sustainable space exploration, exploitation, and colonization.

This work focuses particularly on in situ resource utilization (ISRU) on the Moon with the final goal of extracting water to produce cryogenic chemical propellant. This would be used to support future exploration missions directed to Mars, the Moon, or other destinations in the time frame 2035–2050.

The importance of this vision lies in the need to reduce the burden of Earth-based support. In fact, due to the strong gravity well, supporting numerous future missions from Earth is impractical and highly demanding on both propellant and cost requirements.

This means that one of the first steps toward breaking the chain of dependence from the cradle of humanity is enabling in-space propellant production and spacecraft refueling.

The analysis performed is a feasibility study from the perspective of a consortium of public and private entities. This consortium would be interested in implementing the lunar architecture for space exploration, and integrating this architecture with commercial objectives, to bootstrap the private space economy in Cislunar space. The initiative can transition to a privately driven, profit-generating venture in the long term, once key assets and business cases have been fully established and the risks are reduced by the acquired experience of the mission.

This study is part of the project work of the International Master in SpacE Exploration and Development Systems (SEEDS) held by 3 European universities, namely Politecnico di Torino, ISAE-Supaero, and the University of Leicester, in collaboration with the European Space Agency, Italian Space Agency, ALTEC, and Thales Alenia Space Italy.

Business Plan

Market Analysis

Exploration trends

The formulation of the strategy has been preceded by a wide analysis of the context in which the architecture shall operate and compete in.

This work starts from the International Space Exploration Coordination Group's (ISECG) Global Exploration Roadmap (GER) as a reference document in foreseeing the interests of the global community, including both public and private players. 1

The GER states that the logical next step for human space exploration shall be the Moon, for its strategic proximity to the Earth. This makes it the most suitable location to permanently extend human presence and to prepare for further exploration missions toward more exotic destinations, Mars being the next one. Of course, the Moon is also a fascinating celestial body whose scientific exploration will likely unveil many precious insights, and further our understanding of our own planet.

Many other studies on the topic 2 also confirm how the vast majority of the insiders will target the Moon both as a destination and as a stepping stone to Mars.

Subsequently, a deeper survey of the respective roadmaps of various agencies and organizations has been made, to perform a high-level assessment of the potential market needs. This research shows that from 2019 to 2030, around 30 exploration missions are planned for destinations in the solar system such as the Moon, Mars, Jupiter, and the asteroid belt. Ten more missions are planned between 2030 and 2050. Taking into account that almost 40 missions have been completed between 2000 and 2018, it is evident that there is an increasing effort in pursuing space exploration. Consequently, a conservative estimate of 2 to 3 missions per year can reasonably be assumed.

Emerging markets

The renewed interest in deep space exploration anticipates the growth of a vibrant industry part of what has been defined as the New Space Economy.

It has been estimated that by 2040 the space industry could grow from the actual value of 350$ billion to 1.1$ trillion. 3 Such growth will require new markets to emerge, sustained by the decrease in cost of rocketry and access to space. Some of the most desirable segments are expected to be broadband Internet service satellites, commercial spaceflight, and space resource mining. This latter segment, in particular, is populated by numerous companies working on harvesting water and minerals from the Moon and from asteroids.

The New Space Economy harbors great potential for new and exciting business ventures. While space is high investment, there are endless possibilities for using emerging technologies to open up new markets. Here, the role of push technologies cannot be neglected. 4 Instead, it shall be considered one of the major drivers of future developments and breakthroughs. Having fully deployed cost-effective propellant production facilities and refueling systems would make many goals more accessible, fueling exploration missions as well as entirely new ways of doing business in space. 5

These findings lead to the conclusion that there is already an existing interest in developing a lunar propellant outpost, and that the actual development would considerably extend and influence the forthcoming markets.

Stakeholder Analysis

Stakeholder requirements would provide a groundwork from which the system architectures can be designed, shaping the initial objectives and orienting the successive refinements.

Sponsors would be mainly government agencies, with an inclusion of private companies and other public institutions. The nature of this endeavor is risky and innovative. Therefore, agencies are the only institutions with the right position to address this goal, and are also interested in reducing risk for private companies that can support the initiative completing their otherwise insufficient budgets. Private companies would be interested in sharing part of the risk and investing in future lunar infrastructure for profit generation.

The operators of the mission control segment would mainly be agencies and companies with mission control capabilities. Here, the main interests are correctly and safely implementing mission operations achieving all mission goals. The space segment, on the contrary, would be operated by crew members and the Gateway.

This group of stakeholders also represents the end-users, along with the scientific community gathering knowledge from the mission. This class of stakeholders drives design and operation choices.

Finally, the last segment of stakeholders is represented by customers. Customers' fundamental interest is having convenient access to products and services capable of satisfying their need, that is, reaching a given destination in the solar system. Customer analysis is deepened in the following sections, detailing customers' needs and how this architecture can be capable of satisfying them.

Solution

System of systems architecture overview and functions

The proposed lunar propellant outpost collects icy regolith from the permanently shadowed regions of the Shackleton Crater in the lunar south pole. This area is particularly appealing for its large reservoirs of water, contained inside regolith in the form of ice with peak estimated concentrations of 25% by weight.

6

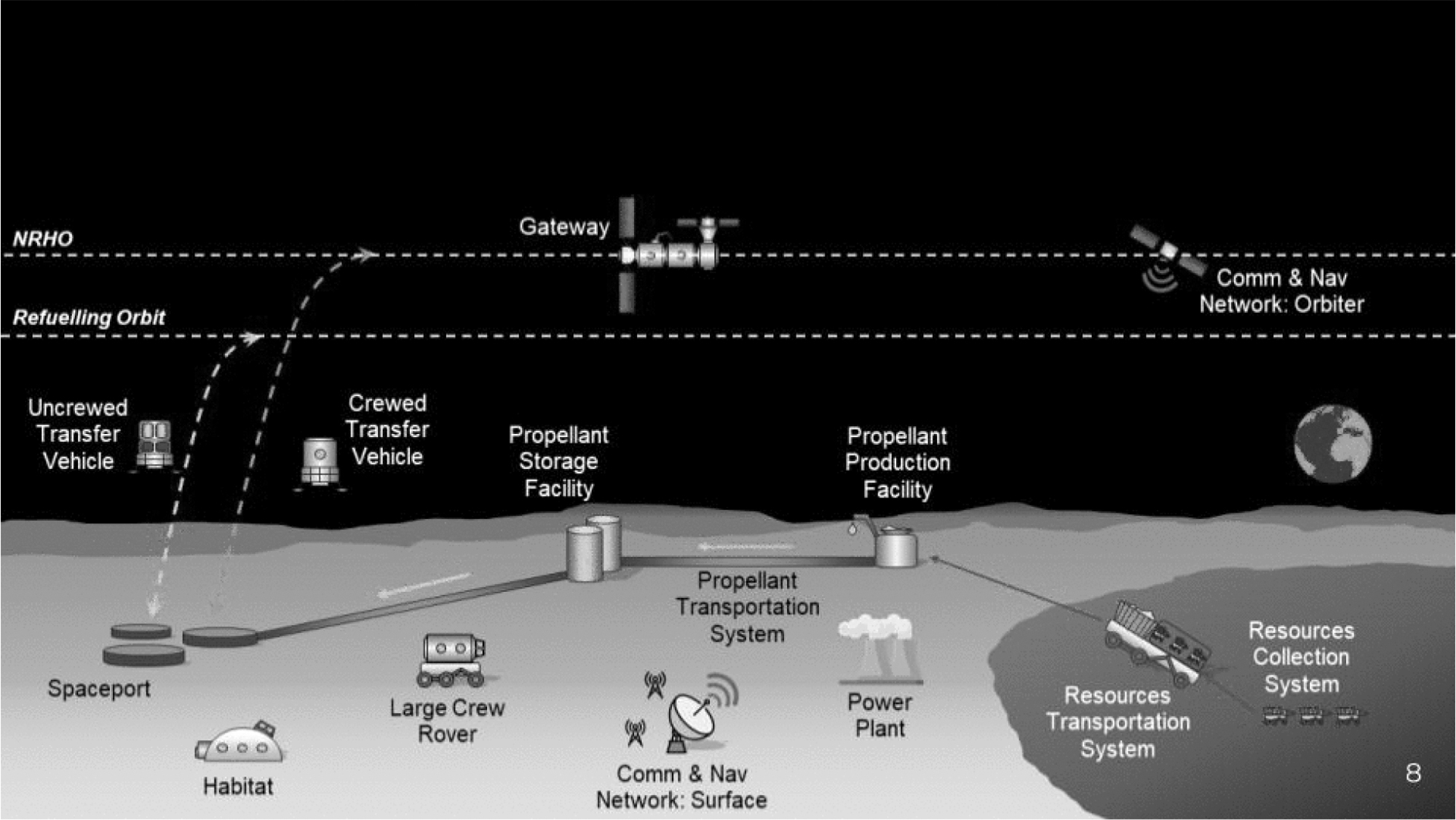

The icy regolith is then transported to a processing site, where water is separated from the minerals and either undergoes electrolysis to produce hydrogen and oxygen, or is stored for later use. Liquid oxygen (LOX) and liquid hydrogen (LH2) would be mixed with a ratio of 6:1 to be used as propellant for chemical engines, resulting in some excess oxygen. The refueling would be performed in 2 locations: lunar surface and lunar orbit. The 2 locations allow for the support of different types of customers, which is detailed in the following sections. The outpost is composed of 3 main segments:

The ISRU segment composed of a robotic resources collection system (RCS) and a resources transportation system, both feeding the propellant production facility (PPF). The products are then moved to a propellant storage facility (PSF), where they wait to be fed into the transfer vehicles through a propellant transportation system (PTS). The lunar surface infrastructure composed of a habitat (HAB) for a crew of 4 members, a large crew rover (LCR), a power system, and an assembly system (AS), used for the setup phases. AS includes a regolith sintering machine, a regolith three-dimensional (3D) printing machine, and a surface transport vehicle. Human presence is required to operate and maintain the architecture. Support to cargo operations is provided by a multipurpose lunar rover, while an astronaut transition tunnel allows for crew transfer between the LCR and a transfer vehicle. The lunar transfer segment includes a propellant transfer vehicle (PTV) to transport cargo propellant to and from the refueling orbit. It also includes a manned transfer vehicle for moving the crew from the lunar surface to the Gateway, which is assumed as an existing building block.

The architecture also includes a communication and navigation network constituted of a surface communication and navigation system and an orbiter.

An overview of the entire system is provided in Figure 1.

Outpost architecture overview.

What is shown is the outcome of last year's SEEDS master project work. 7 For the present year, a second iteration of the design has been carried, bringing deeper level of detail to the overall concept and introducing some relevant changes, as can be appreciated in Li et al. 8 An area of special focus has been the economics behind the outpost, for the many challenges it holds. Last year's business model was based on selling the excess LOX deriving from the propellant production for only self-sustainment of the infrastructure. On the basis of the vast interest in the in-space propellant production examined in this article, the business strategy has been reoriented toward a production and a distribution of both LH2 and LOX sized to satisfy an estimated market demand. This, in turn, led a scale-up of the PPF to meet the new requirements, which has revealed to be particularly convenient considering that new estimates suggesting water percentage in the regolith may be as high as 25% by mass, much higher than the 5% used previously. A 15% content has been adopted conservatively.

Value Proposition

Refueling in space does not only reduce the costs of exploration missions. Part of the value proposition is in the enabling of new space programs that would be unsustainable without a lunar propellant outpost to support them. This would also encourage new markets to emerge and potentially to drive changes in Earth's economy. At the same time, unprecedented heritage and knowhow can be built.

Selection of the refueling points

Two locations have been identified for propellant sales: the lunar surface and lunar orbit. The refueling point on the surface is bound to the area in which the outpost is built, and thus, it could only service Moon visitors interested in visiting the lunar south pole. Due to the necessity of storing propellant on the surface before transportation to the on-orbit refueling point, the implementation of surface-based refueling is advantageous. This would also provide a good starting point for a future extension of the service, perhaps facilitating refueling across a wider area of the lunar surface by means of a propellant pipeline network. Suborbital transport could also be achieved by providing refueling to lunar hoppers capable of reaching the numerous points of interests at the pole and its vicinities.

On the contrary, on-orbit refueling allows Moon visitors to reach further areas of the lunar surface and is gaining attention as staging point for Mars or other deep space missions in the solar system. Therefore, the circumstances under which this would reveal advantageous have been investigated. The most influencing factor is, obviously, the location. Many different locations could be potentially selected where propellant can be made available, ranging from low lunar orbits to Earth's orbits and other locations in Cislunar space. While relatively little effort is needed to place propellant in lunar orbits from the lunar surface, this is not the case for Earth orbits. The higher ΔVs to reach the Earth orbit mean that a much larger amount of propellant would be consumed to reach the refueling point, requiring larger amounts of propellant to be produced on surface.

This would in turn increase costs for the manufacturer while sale prices would have to be kept at the minimum to be competitive with Earth-based service providers (a number of start-ups are currently developing similar plans 9 ). This, along with the decreasing costs of rocketry and access to space, could easily make a lunar propellant outpost unprofitable and unsustainable. Potential solutions could rely on the utilization of electric space tugs supplying Moon-derived propellant to Earth orbits. In general, this path would lead to higher, undesired overall operational and technical complexity. Earth orbits have therefore been rejected.

The selection process has thus been restricted to a number of locations in the proximity of the Moon and carried through the Analytic Hierarchy Process method 10 and the Technique for Order of Preference by Similarity to Ideal Solution. 11 The adoption on these decision-making procedures allowed, respectively, to establish a preference scale among a series of decision criteria, and to subsequently process a large number of alternatives with the final goal of selecting the most similar to the ideal case.

An overview of this trade-off, including figures of merit and their weightings, is given in Table 1. In particular, the table shows the figures of merit (FoM) and their weightings if the goal is to identify the best refueling point for a human mission to the Mars. For this reason, time of flights has been given higher priority than ΔVs. At the same time, the ability to perform the refueling rapidly and flexibly is paramount: making this step slow and complex would not be convenient for customers. In the case of a martian robotic mission, weightings would be the opposite way, provided that a robotic mission would employ cryogenic propellant. The same applies for Moon missions, considering that Mars-related criteria would have zero weight.

Trade-Off of On-Orbit Refueling Locations

DRO, distant retrograde orbit; LEO, low earth orbit; LLO, low lunar orbit; TOF, time of flight.

The winning orbits are circular orbits around the Moon, ideally polar low lunar orbits with 100 km altitude. This is valid both for human and robotic missions, as a sensitivity analysis confirmed. Several ways of distributing propellant have been investigated. A direct refueling strategy, where PTV transports the propellant from the surface to the customers' spacecrafts in Cislunar space, might offer higher safety and energy efficiency compared with an architecture employing a propellant depot in orbit, 12 and has thus been adopted in the present study. This also has other advantages such as the possibility of optimizing the orbit according to customer's needs by inclination and altitude adjustments. It has been calculated that these adjustments can allow to reach up to 30° inclination and 800 km altitude from lunar surface. Going beyond these parameters would cause the ratio between the propellant used by the PTV to accomplish the task and the propellant to be sold to the customer to raise above 3, which has been set as a threshold to keep the business sustainable. It has been estimated that for a customer staging around the Moon to refuel before heading to the low Mars orbit with a payload of 70 tons, around 9% in propellant mass can be saved compared with a direct transfer case. This comes as the result of the reduced tankage and propellant masses needed to perform the journey in 2 steps. These benefits increase with increased payload or spacecraft mass. Finally, while the presence of the Gateway can potentially introduce a mandatory stop-by at the orbiting outpost in some missions, this analysis shows that its near-rectilinear halo orbit might not be the optimal site for refueling purposes, because of the intrinsic difficulties hindering rapid, repeated servicing sequences. Finally, having 2 refueling locations, on surface and on-orbit, increases the versatility of the investment for its ability to exploit the wider market opportunities.

Products and services

The LUPO infrastructure offers other advantages in addition to refueling that may lead to new revenue streams and to a wider set of useful applications. Unelectrolyzed lunar water could be used for life support, and lunar regolith could serve as building or shielding material. Habitable spaces could be leased to agencies or even to space tourism organizations, and crew time could be sold to third parties for science or training purposes. These would provide additional income and therefore diversity to the business.

Customer Analysis

Segments

An entity offering in-space refueling services shall reach the optimal compromise between the potential customer base and the cost associated with the targeting of that base. In this case, customers are characterized according to 2 factors: the type of propellant they use and the refueling point they are most interested in.

Producing only LH2 and LOX does not mean that only chemical engines using LH2 as fuel and LOX as oxidizer can be supplied. In fact, LOX is an oxidizer suitable for many other bipropellant engines, such as those using methane fuel. This means that a new portion of customers could be reached, leveraging the excess LOX deriving from the difference between the proportion of oxygen and hydrogen in water (8:1) and in propellant (6:1).

Customers can be also segmented according to their ideal refueling location. Customers performing low earth orbit (LEO)-to-geosynchronous earth orbit raising, for example, are most interested in refueling in LEO. This segment of customers has not been included among the target segments for a number of reasons explained above. Moreover, industry interest in LEO-to-GEO missions, initially required to transport broadcast television satellites into geostationary orbit, is now declining due to the increasing popularity of web-based entertainment.

In contrast, as shown in the Exploration Trends section, numbers of visitors to the Moon and Cislunar space will increase in the near future, driving up the demand for refueling on the lunar surface or in orbit, especially when return to Earth is needed, as in the case of crewed missions. Programs such as NASA's CATALYST 13 and CLPS 14 or ESA's HERACLES ascender 15 will need or seek for future refueling capabilities to sustain multiple descents.

Large missions to Mars or elsewhere in the solar system could benefit from in-orbit refueling, as assessed in the Selection of the Refueling Points section. Whether refueling in lunar orbit would be worthwhile or not for a Mars mission remains unclear, due to the lower ΔV required to reach the Red Planet without a lunar pitstop. Lunar refueling would only be a viable option if the cost saved justified a more complicated transfer and operation protocol for the customer. Here, having the Moon as an intermediate step would also be strategically important for allowing on-orbit assembly and outfitting of spacecrafts and transfer vehicles in a staging point between the Mars and Earth. 16

Channels

The entities managing a propellant outpost would act as contractor for big space agencies, or as a supplier for private companies. Groups of enterprises or institutions may want to establish agreements for the utilization of the lunar-derived propellant driven not only by mere commercial convenience but also for political reasons, or for shared interests motivated by sponsorships or other types of partnerships.

Potential demands

As previously stated, the Moon is drawing increasing attention for its potential in space exploration. The success of NASA Space Acts and COTS programs demonstrated the technological and economic benefits of partnering with the industry, fostering a strong will to extend the same approach to the Moon in preparation for Mars. 17 All this suggests a wide customer base of Moon visitors. The potential propellant demand on the surface was estimated as 50 tons/year. This amount of propellant would be sufficient, for instance, to fuel the return journey of crew or cargo lunar landers of various sizes, such as large Lockheed Martin's-like landers 18 or lighter Blue Moon Blue Origin's lander. 19

An in-orbit demand of 200 tons/year of propellant was calculated, using the following set of assumed demands:

A lunar mission, either crewed or uncrewed, every year (50 tons/year).

A large Mars mission, presumably crewed, every 2 years (140 tons/year).

A robotic mission, either to Mars or to other locations in the solar system, every 2 years (10 tons/year).

These numbers are derived from reference mission designs such as Lockheed Martin's Mars Base Camp 20 or NASA's Mars Design Reference Architecture 5.0 21 that envision a future refueling step in Cislunar space. Large lunar architectures such as those proposed by united launch alliance (ULA) Kornuta et al. 2 were used as a reference in sizing the on-orbit demand of lunar visitors.

As mentioned previously, LOX also could be sold separately as oxidizer, serving missions using other types of fuels. For example, missions to Mars may employ carbon-based fuels, and will only be interested in the LOX oxidizer. Such a demand has not been taken into account.

Finally, considering the need for self-sustainability of the outpost and its vehicles, a total of 1,050 tons/year of regolith-derived propellant would have to be produced.

Cost Breakdown Structure

Cost analyses were carried out using cost models NAFCOM99, AMCM, USCM7, and USCM8, depending on the building blocks. These models establish proportionality relationship between cost, mass, and other key parameters. Costs were spread over several years to account for incremental development cost. The final cost of the architecture is broken down as in Table 2. This cost is the output of NASA's cost models, which assume NASA having total ownership and operation authority over all the systems. However, as recent studies claim, 5 an 8-fold cost reduction can be achieved when initial investment, property, and operations are shared with private partners. Therefore, it has been assumed that the public/private consortium envisioned in the present study can achieve an 8-fold cost reduction in developing this new hardware. Overall, the final cost is estimated around 13 B$. It shall be noted, however, that the present design can be further optimized for propellant production, which could lower the total cost. Moreover, these cost models may not be accurate enough for this type of studies.

Cost Breakdown Structure

CNN, Communication and Navigation Network; ISRU, in situ resource utilization.

Revenue Streams

Propellant pricing

Selling prices for propellant both on the surface and on-orbit have been set to undercut by 25% the lowest cost a customer would have to bear to fulfill its mission objectives on its own. These costs were estimated under the assumptions listed below:

LEO is the departure and arrival point.

Cost of development of service modules (SMs): 70 M$/ton of dry mass, the average of Cygnus and Dragon capsules' development costs.22,23

Cost of development of landers/ascenders: 150 M$/ton of dry mass.

Cost of propellant on Earth: 1,000 $/ton.

Dry mass of modules: 15% of the propellant mass for SMs, 40% for landers/ascenders.

Total mass delivered to LEO: 63 tons (using Falcon Heavy, which adds 150 M$ of launch costs 24 ).

The lowest of these costs has been identified analyzing alternative mission scenarios for specific sets of customers. In particular, Moon and Mars visitors were taken as reference segments. Inside each mission category, the cheapest option for payload delivery has been compared with an alternative strategy, including refueling of lunar propellant, thus determining a potential price for each customer segment as explained above.

Moon visitors benefiting the most from refueling on the Moon surface or Cislunar space can be subdivided into 2 groups: visitors landing reusable vehicles designed to travel multiple times between lunar surface and orbit, and visitors willing to reach Luna and come back to Earth. For the first ones, the duration of the stay or the number of round trips and refuelings is widely variable. The second ones, instead, would necessitate to refuel no more than 1 or 2 times, thus setting the lower limit for the cost range.

On the contrary, 2 classes of martian scenarios were examined: one-way journeys and Earth-return missions. For the latter ones, it has been assumed that the customer is capable of producing propellant for the return leg reacting Earth-brought hydrogen with the carbon dioxide of martian atmosphere, as in the Mars Direct architecture, 25 thus narrowing the alternatives to worst-case scenarios for an LOX/LH2 provider. The last martian case considers 2 launches from Earth to land on Mars, respectively, a payload and a return vehicle. After the assembly on surface, the mission proceeds as in the other cases.

A common trait in all the scenarios is that the payload is landed on surface using an expendable lander that detaches from an SM bringing the spacecraft to a given Moon or Mars orbit. Payload is then brought back to the Moon or Mars orbit with an integrated ascender that is disposed after the payload has been attached again to the SM waiting in the orbit to perform the return leg to LEO. Opting for staging would allow the customer to optimize fuel consumption.

Tables 3 and 4 offer an overview of all the scenarios examined with their relative total ΔVs and costs per ton of payload delivered to the final destination.

Customer Mission Case Description

SM, service module.

Customer Scenario Costs for Propellant Pricing

This cost includes one SLS Block 1 launch (1 B$) due to the need to deliver around 90 tons in LEO for the return vehicle delivery on Mars.

The cheapest option is the scenario Mars no. 1. Although it would be costly, LEO refueling could be added to this scenario to allow for larger payloads to be delivered. The estimated costs apply a constraint to lunar-derived propellant price that cannot exceed 10 M$/ton on orbit and 30 M$/ton on surface.

Products

Propellant production also generates by-products that have potential for commercialization. Dehydrated regolith, discarded after water extraction, could be used as building material for shelters, antidust walls, spaceports launchpads, 3D printed or sintered structures, fundamental for future lunar bases and permanent outposts.

To use lunar regolith, customers would have to either land the extraction equipment on the Moon's surface themselves, or to buy it. Regolith extraction equipment launch and manufacturing (RCS) and its operations over 10 years have an estimated cost of 1.75 B$. Spreading a return on investment over the same period and undercutting this cost by 25%, regolith could be sold at 12.000 $/ton. If the regolith was used for a 15-m-radius and 0.25-m-tall launchpad every 4 years, the generated revenue per year would be equal to 1.1 M$.

Water is another intermediate product that plays a crucial role in space exploration. Even though it is primarily used here as a raw material to produce LOX and LH2, water could also be sold for life support or radiation shielding. Assuming the average crew member consumes 30 L/day and that 95% of this water is recycled, a 60-day lunar mission with a crew of 4 would require 480 kg of water. Radiation shielding made using water-filled walls could require, for an International Space Station (ISS) element-like sized HAB, up to 25 tons of water. 26

Using the previous approach to set water price at the lunar outpost, an estimated price of 1 M$/ton of water was obtained. If this requirement recurred every 2 years to support new crewed surface missions, a revenue of up to 12.5 M$/year could be generated.

Services

Some elements of the system could be used for additional revenue streams when their function is completed, or a standby period imposed by the operational scenario.

For example, the transport vehicle, regolith sintering system, or regolith 3D-printer used during the setup phase of the outpost could be leased to customers interested in building infrastructures on the lunar surface, perhaps even using the wasted regolith as feedstock.

The yearly lease prices have been calculated by setting the price equal to 75% of the initial cost, and distributing the cost over a period of 10 years. These result in 100 M$/year for the sintering machine, 50 M$/year for the surface transportation vehicle, and 32 M$/year for the regolith 3D printing machine.

Considering that this machinery would represent a cheap and effective test bed for agencies and companies to test technologies, it has been assumed that each piece of equipment would be lent once every 2 years, generating a total revenue of 91 M$ per year.

The HAB is uncrewed for 10 months per year and, as a consequence, the LCR is also unused most of the time. These elements could be leased to Moon visitors, simplifying their mission architecture and reducing the need for new elements to be developed only for temporary use. The cost of renting the elements has been determined considering estimates for the private transition of the ISS 27 and assumed to be 230 M$/year for the HAB and the rover.

Crew time could also be a relevant source of income. Scientific experiments or hardware testing could be carried by the crew on behalf of third parties, such as nonspace companies. Assuming an average price of NASA crew time price on the ISS of 17.500 $/h/crew member 28 and 200 h/year dedicated to experiments for commercial partners, a potential revenue is estimated of 3.5 M$/year.

The final revenue stream considered was advertisement. After a period of unpopularity due to the high investments required, space advertisement is regaining the interest of agencies 29 and private companies. 30 A permanent facility on the Moon, visited by humans on a yearly basis, would undoubtedly gain worldwide attention. This could allow for the production of media such as documentaries, virtual reality shows, or live streams, each of which harbors the potential for advertising revenue. Pricing was calculated by considering estimates made for the ISS transition into a private station 27 and companies' investments in space advertisements. 31 These considerations lead to an estimated potential revenue of 500 M$/year.

Table 5 summarizes all the revenue streams that were considered.

Revenue Streams and Related Demands

N/A, not applicable; 3D, three-dimensional; LCR, large crew rover.

Revenue streams other than propellant may generate up to 636 M$/year. A margin of 30% was applied to account for inaccuracies, leading to 445.2 M$/year from secondary revenue streams and an overall annual income of 3.94 B$.

Other products were considered, such as thorium or helium-3. The market demand for these elements is large, and their relative scarcity drives their value extremely high. However, the technology development costs required for extraction on the Moon are such that they have been rejected in this particular study.32,33

Financing

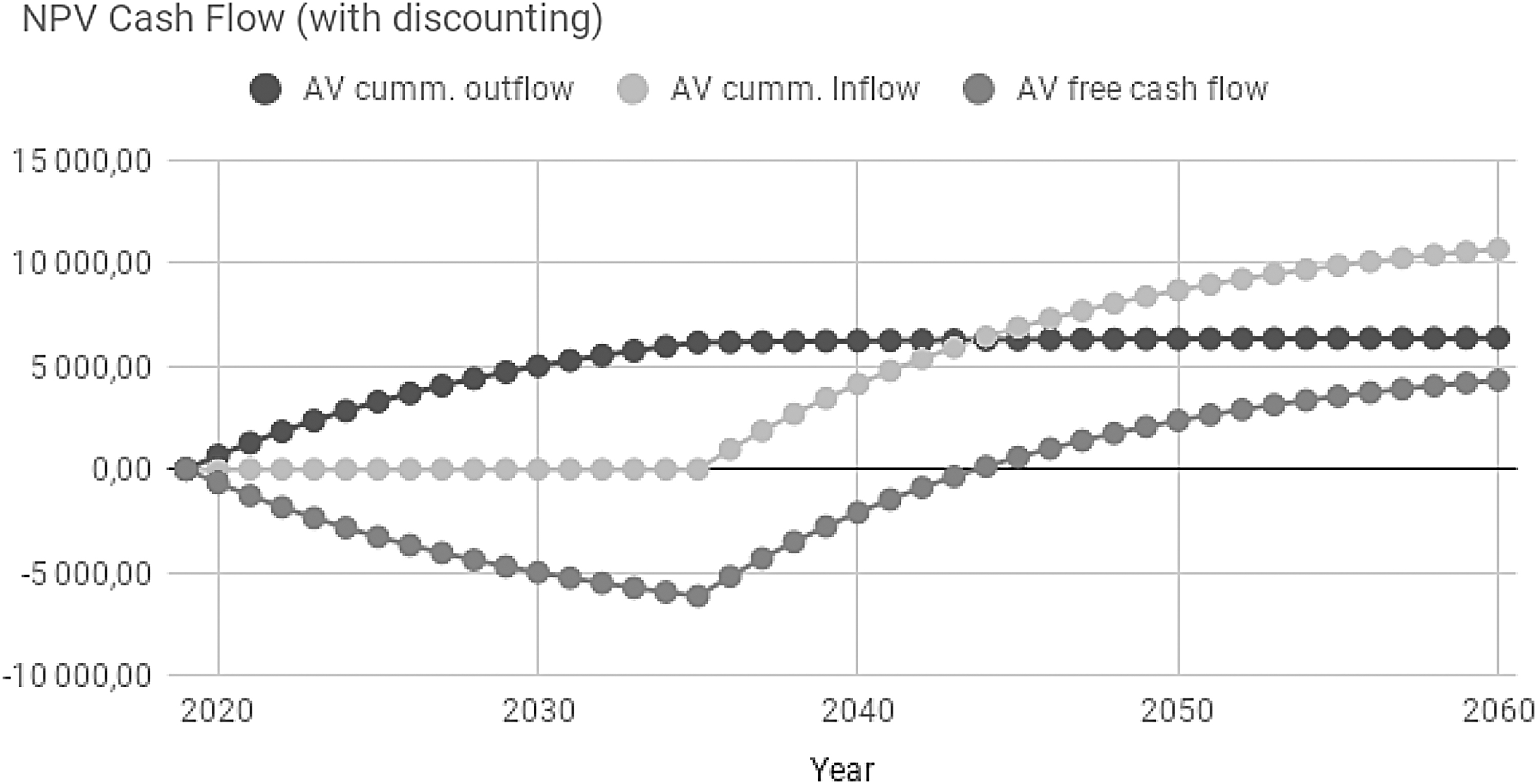

Inflation of 2.6% 34 and a risk premium of 6% were added in calculating annual free cash flow. This percentage accounts for the risk in allocating part of one agency's budget on a mission plan instead of on another one, and for risk prime of private partners. The sum is an 8.6% discount rate, the results of which over a 30-year lifetime of the outpost are shown in Figure 2.

NPV cash flow. NPV, net present value.

The break-even point is reached around 2043. Despite revenues starting to be generated at that point, these may not be enough for private investors, which for such a risky venture would not accept a return on investment lower than 8 or 10 times their initial investment. For a hypothetical private partner sharing 20% of the initial investment, for instance, almost a 3-fold increase of the free cash flow shall be achieved. A large return on investment—and therefore a business case—is not easily accomplished, but some of the required circumstances can be identified. First, cost reduction shall be implemented by simultaneously optimizing the architecture and reducing the manufacturing cost of the lunar hardware. Second, and most important, higher revenues from the surface market shall be pursued. Due to the absence of transportation costs, selling propellant on this marketplace has the largest profit margins. For the present study, demand estimates have been based on available studies, market forecasts, and present-day roadmaps, but the impact of such a mission-enabling initiative might strongly influence the status quo. A propellant outpost would enable more frequent visits aiming at emplacing the successive evolutions of Moon development, from science to in situ manufacturing, in a gradual import replacement trend that would make an off-Earth human outpost capable of wealth creation. 35 To match the requirements of the previously mentioned hypothetical private venture, 300 tons/year shall be sold on surface.

However, the value of such a propellant outpost on the Moon goes well beyond mere profit generation. The endeavor is also a large investment in technological development consistent with the GER, preparing for human exploration of Mars while fostering cooperation between players in the space industry. Deep insights into ISRU hardware, reusable transfer vehicles, and operations would undoubtedly be gained, insights that would also be hugely relevant on the Red Planet. What is perhaps equally important is that public support is fundamental in the quest for Mars. Beginning this effort from a staging point on the Moon would generate vast public interest providing a short-term demonstration of innovative and Mars-relevant space infrastructure and the knockon effect it has on the space economy.

Competitors' Analysis

Direct competition

A number of private companies, such as iSpace, Shackleton Energy, Moon Express, are currently planning to exploit lunar resources to produce and sell propellant. While some of these recently closed funding rounds, 36 little is known about their future plans.

Some of their business models foresee the gradual establishment of a settlement on the Moon, with the final goal of implementing ISRU only at the end. These companies are planning to develop cheap transport vehicles to deliver small customer payloads to the lunar surface. 37 All of them rely on robotic systems. In any case, it has to be taken into account that new ventures will emerge, encouraged by the strong support received from the public sector, especially in the United States.

The outpost described here has several advantages over these competitors. The most notable of these is the presence of humans, which enables a series of opportunities such as crew-tended experiments, operational and maintenance flexibility, and larger outreach. The drawback of the human presence would be, of course, higher risk and higher costs due to crew training, salaries, and the manufacturing and qualification of human-rated spacecrafts. All-robotic systems would be cheaper and easier to operate once available, but the technology does not yet exist for autonomous robots to fulfill the extremely challenging tasks to be carried out on a lunar base. Simpler robotics dedicated only to water collection and selling could be used, but would require customers to produce their own propellant through electrolysis, which would complicate their spacecraft design.

Indirect competition

The indirect competitors' category includes all the organizations providing propellant on lunar surface or in Cislunar space, either by harvesting it from other sources such as asteroids, or shipping it from Earth at aggressive prices. Several companies such as Deep Space Industries and Planetary Resources are currently envisioning new strategies to exploit largely available asteroid resources, water included.

The main advantage of the infrastructure presented in this report is the higher technology readiness levels (TRLs) of lunar ISRU, relative to the lower TRLs of technologies required for asteroid mining. Collection of water from asteroids is more a challenging task than from the Moon. Another major obstacle to these endeavors is the difficulty in detecting and identifying resources, which makes it particularly expensive and time-consuming to search for the most resource-rich asteroids. Furthermore, asteroid-derived propellant would be more difficult to deliver to the lunar surface and would probably be made available only in Cislunar space.

Finally, another source of LOX could be the metal oxides within rock at the lunar surface. However, oxygen extraction from oxides requires far more energy and more complex technologies than water electrolysis does. It also has the added drawback of not producing LH2 for use as fuel, but these facilities could be installed at more convenient locations than the poles, and their raw material collection would be intrinsically simpler.

Replacement competition

Replacement competitors are composed mainly of companies such as SpaceX or Orbit Fab, currently aiming at shipping propellant to LEO from the Earth. While this strategy may prove easier and faster to implement, with a smaller initial investment, the large ΔV needed to overcome Earth's gravity field makes this costly and disadvantageous in the long term. Provided that the current decline in launch costs would contribute in making such a service cheaper to implement, a well-established lunar propellant outpost might have a good opportunity to leverage the more favorable ΔV requirements.

Other replacement competitors could sell different types of propellant to support space exploration missions. Here, the primary competitive advantage is the superior performance that the LOX/LH2 propellant shows over other chemical propellants. This aspect shall be properly leveraged to compensate for the issues related to boil off and cryogenic storage. While these can be solved or at least mitigated through technological advancements, a more energetic chemical propellant is hard to find.

Particularly threatening competition would be companies achieving outstanding nuclear or electric propulsion technologies. Due to the high-thrust or high-specific impulses they could provide, these technologies have the potential to make interplanetary travel faster and cheaper, ultimately making lunar-produced chemical propellant redundant.

The main competitive advantage here is that chemical propulsion offers better options for propellant resupply, due to the possibility of producing propellant in situ on other celestial bodies. The 2 most interesting destinations for the near future—the Moon and Mars—both harbor water on their surfaces, and so, the LOX/LH2 propellant could be produced. In addition, Mars could even provide the opportunity to produce carbon-based fuels from its atmosphere. Despite the fact that nuclear or electric engines make far more efficient use of their propellant, the need for resupply will emerge sooner or later, making recurring interplanetary travels inconvenient. Furthermore, chemical propulsion currently allows higher thrust than electric propulsion, and has far more heritage and consolidated know-how than nuclear propulsion. Electric propulsion, it must be admitted, would be a major competitor for robotic missions.

Legal Aspects

Space law is a subject of great international interest. The utilization of outer space and its resources shall lead to common benefit for all mankind through responsible and peaceful development of sustainable activities.

Regulation of resource mining has to clarify delicate legal aspects about utilization and property rights. Current legal frameworks state that access to space and resource utilization shall be free and granted for everyone, in accordance with equality and mutual cooperation principles, as promoted by the United Nations Outer Space Treaty (OST). 38

Nations are currently responsible for authorizing and supervising all the space activities carried out by organizations based in or conducting launches from their territory, whether governmental or not. Institutions such as the Hague Working Group are working on outlining an international framework that laws such as OST can fit into. 39 Here, regulations are gradually defined as the context is better understood, through the concept of adaptive governance.

The Shackleton Crater, where the proposed lunar outpost is based, is of great interest for ISRU and scientific purposes. This means that regulations concerning legal claims to space resources will have to be implemented to ensure the legal recognition of the ISRU operations by the international community. Some of the proposed solutions to this include the adoption of adverse possession principle. 40 According to this principle, a possession continued for long time without interruptions, along with a constant claim of ownership, gives right to full property.

The area will be subject to restrictions that may limit the areas available for mining and the implementation of industrial activities, such as those deriving from the scientific interest in the crater. Here, the protection protocol would prohibit any industrial activity or any potential threat to the site conservation, leaving the crater contour as the only minable area. Other areas will have to be classified as safety risk areas, such as those around the PPF, PSF and PTS, and access would therefore be limited.

Finally, the location of an appropriate site for regolith disposal would need to be identified, as it would preclude access to potentially interesting regions. One solution to this aspect could be a common agreement on a not-of-interest area.

Limitations

The present work takes into account the distribution of products and services produced on the Moon for local use on the Moon itself and for space travel in the solar system, including Moon-Earth transfers. It is oftentimes suggested that other commercial opportunities might exist—such as for rare earth elements (REE) or helium 3—resulting in the distribution and selling of lunar products to terrestrial markets. 41 Although fascinating, these business cases are, however, far from being viable at the present moment, as briefly mentioned in the Services section. As pointed out by Crawford, 42 Earth's deposits have REE contents ranging from 0.1% wt to 10% wt, while lunar total estimated REE concentration is around 0.12% wt. This makes lunar REEs import unlikely, at least until mining costs on Earth become too high. As for 3He, its concentration of 20 parts per billion is so low that extraction would be impractical even to satisfy a small percentage of Earth's energy demand. In parallel to this, alternative and much more abundant fuels for nuclear fusion reactors, such as deuterium and tritium, could be sourced more easily on Earth. Other more sophisticated products that could be manufactured by taking advantage of low gravity or vacuum conditions are not mature yet and would face the competition of both terrestrial alternatives and of emerging products from in-space manufacturing endeavors in LEO.

Ultimately, the high transportation costs, scarcity of applications, and threat of substitute products currently make these Earth-based markets unattractive for lunar goods. The only exception can be represented by intangible products, such as multimedia. As stated in the Services section, videos, pictures, live-streams, or virtual reality products could be a relatively low-investment source of revenues. In addition to this, data from sensors, experiments, prospecting, and exploration could find customers among research institutions and private companies. Potential revenues from these data have not been considered for the reference scenario.

Finally, this work does not contemplate the parallel lunar development that could take place in the same time period considered for LUPO. Other initiatives might be implemented by other public or private actors at different scales, further driving an Earth-to-Moon economy offering transportation services, telecommunications, and other specialized payloads. Despite being beyond the scope of this work, a holistic vision for the Moon is fundamental to ensure a sustainable and peaceful development.

Future Work

Future work includes a deeper investigation of available cost models to deliver higher accuracy to cost estimates. Changes in the architecture to achieve lower costs or higher efficiency shall be analyzed. Further studies shall reconsider the role of a lunar propellant outpost for deep space exploration and assess potential business cases in sustaining surface-based campaigns for Moon development. In this context, the role of the Gateway shall be evaluated as it could impose major constraints on the future implementation of these plans.

Conclusions

ISRU is the key for the extension of a permanent human presence in the Universe, breaking the burdens of Earth-reliant exploration. The present work outlined a business analysis for a lunar outpost as it could be shaped to synthesize the needs and the goals of both public and private actors. By examining leverages and criticalities, this article has outlined a broad ensemble of conditions and high-level requirements that would make such a program sustainable and profitable. The establishment of a lunar propellant outpost may not be a sustainable or technically convenient solution to support deep space exploration missions. The strategic advantage stakeholders shall capitalize on lies in providing propellant on the surface, enabling frequent Moon access. In order for this capability to express its promising usefulness and generate revenues, a wider framework of lunar development initiatives shall arise that take advantage from surface refueling. In situ manufacturing and Moon industrialization, research infrastructure installation and scientific programs, exploration campaigns and tourism would be other vital organs of a new seleno-system the propellant outpost would be part of. It has then been demonstrated that the sharing of initial costs and risks between public and private players is the only way to bootstrap the establishment of such a new lunar economy, given present-day capabilities. The current state of the space industry provides good examples and demonstrations of the achievements this model can obtain. Emphasis has also been given to the additional business opportunities that emerge from the deployment of this infrastructure, such as advertisements, crew services, and the leasing of HAB, rover, and machinery. Not only would this create additional value that is key in gathering and nourishing the involvement of the tax-paying public, but it is essential in view of the long-term sustainability of the endeavor as well.

Finally, even though profits are not easily generated in the first place, settling on the Moon does not lose value if the ultimate objective is supporting Mars exploration. The path to the Red Planet is long, difficult, and expensive, but perhaps less so with a lunar propellant outpost. Fortunately, our satellite is waiting for us to make our very first step on its ground. Again.

Footnotes

Author Disclosure Statement

No competing financial interests exist.

Funding Information

No funding was received for this work.