Abstract

This article outlines the hallmark of a new phase in the evolution of space activities and the changing role of space agencies. The growing affordability and ease of technological advancements, alongside a shift toward more business-oriented political leadership, and the increasing participation of commercial companies in public programs have been reshaping strategies, approaches, and modes of engagement of space agencies. Levels of analysis include both legacy and emerging space agencies. In terms of methodology, this study primarily relied on desk research, utilizing publicly available documents, external and internal databases, conference proceedings, and other bibliographic sources. To document the new strategic orientation, after discussing the transition patterns for legacy space agencies, the authors report and illustrate four taxonomy-based cases of emerging space agencies.

INTRODUCTION

The space sector has undergone significant changes, transitioning from being dominated by superpowers and large corporations to becoming more accessible and inclusive. This shift has been driven by the emergence of new actors, including both public and private entities, as well as the rise of emerging space countries. As a result, space agencies and governments play a crucial role as enablers within the space sector.

Over time, the space sector has experienced various stages of evolution, 1 as depicted in Figure 1.

Stages of evolution of the space landscape.

Initially, with the organized study of the Universe by early astronomers such as Galileo Galilei, the initial stage came into being. In the 20th century, the pursuit of expanding human presence in space led to the launch of stage 2. This phase was characterized by the space race between the United States and the Soviet Union, culminating in the historic Apollo moon landings and continuing throughout the Cold War. Subsequently, as competition between nation states decreased, stage 3 emerged, marked by collaborative efforts such as the International Space Station (ISS) that required partnerships.

However, space activities were still primarily limited to a small number of powerful states and a handful of large private enterprises. Today, the space industry is undergoing a paradigm shift, transitioning from stage 3 to stage 4. This shift is driven by changes in motivations, actors, roles, and technologies. Stage 4 represents a more democratized and accessible space industry, characterized by increased public–private and private–private collaborations. It has seen the rise of numerous small- to medium-sized private companies in the sector.

The emergence of private participants in the space industry has significant implications for traditional players, particularly for established space agencies.

As the industry evolves, space agencies must redefine their roles within the changing landscape. In the early days of stage 2, when the first space agencies were established in the 1950s, they were the primary champions, actors, and investors in their respective national space sectors. However, in the present context, a space agency is just one of many participants in the space industry and must adapt to its evolving position within the national space sector.

The National Aeronautics and Space Administration (NASA) serves as a prime example of the dramatic changes that space agencies have undergone. 2 During the peak of the space race, NASA's budget accounted for 4.5% of the U.S. federal budget. However, in recent times, it has decreased to below 0.5%, reflecting the transformation that NASA has experienced.

In this perspective, we explore the current dynamics within the space industry and discuss the evolving roles of both legacy and emerging space agencies.

THE SPACE INDUSTRY

In 2021, the global space economy witnessed a turnover of ∼469.3 billion U.S. dollars, reflecting an increase from 446.9 billion U.S. dollars in the preceding year (Fig. 2).

Global turnover of the space economy from 2009 to 2021 (in billion U.S. dollars). 3

Within the global space economy, the commercial space products and services sector emerged as the most prominent, constituting nearly 48% of the overall turnover amounting to 224.2 billion U.S. dollars (Fig. 3).

Global space economy from 2019 to 2021, by sector (in billion U.S. dollars). 3

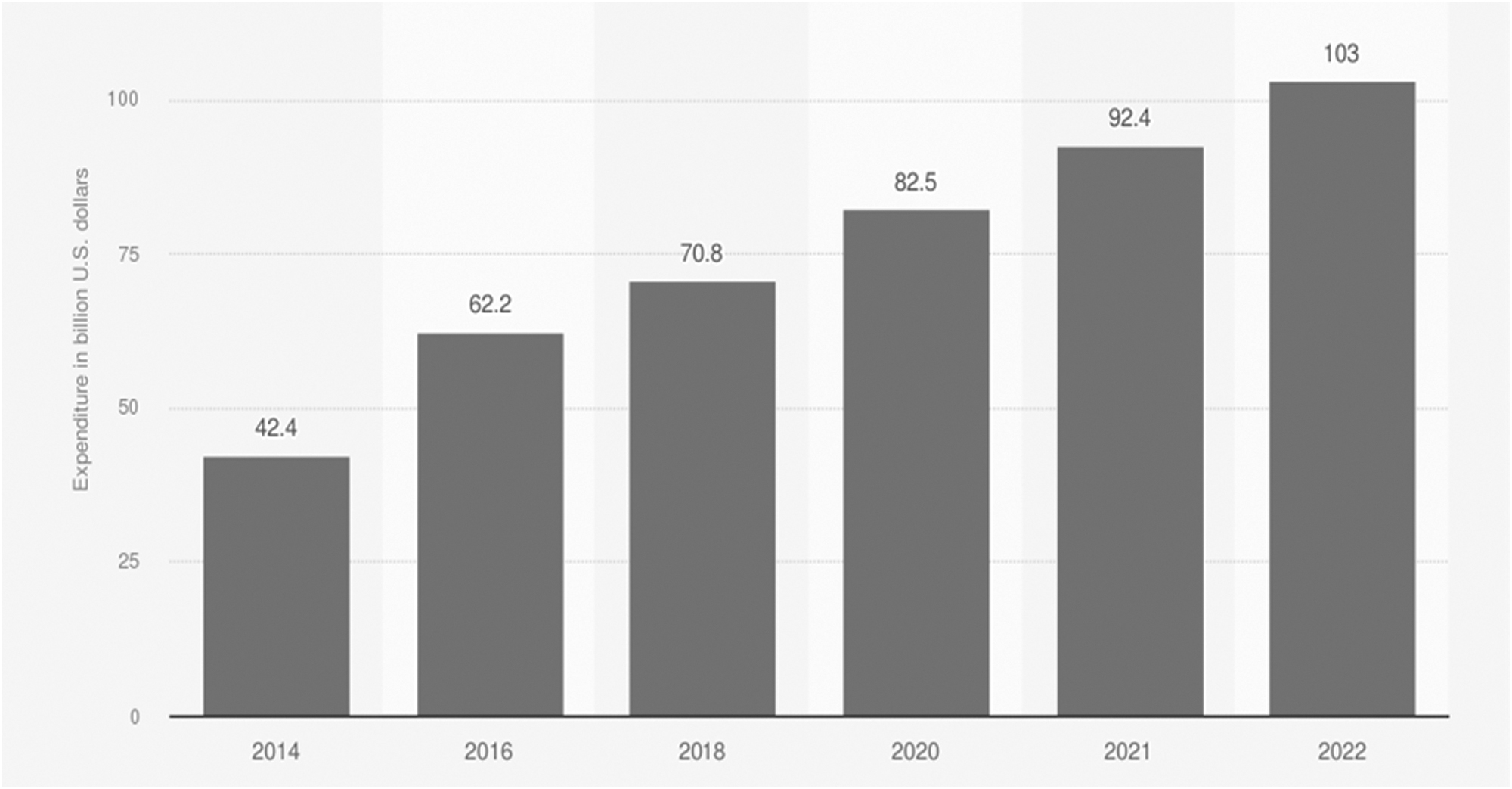

Despite the ongoing COVID-19 pandemic, government expenditures on space programs worldwide have continued to rise in recent years. In 2022, global government spending on space programs reached a total of 103 billion U.S. dollars, indicating a notable increase of ∼11.5% compared with the previous year (Fig. 4).

Government expenditure on space programs worldwide from 2014 to 2022 (in billion U.S. dollars). 4

Looking ahead, it is anticipated that government space budgets will experience sustained growth in the upcoming years, gradually tapering to an annual growth rate of ∼1%–2% between 2024 and the end of the decade. While regional defense rivalries and the increasing militarization of space are expected to sustain budgets, macroeconomic conditions may place strain on public budgets, exerting downward pressure on civil space expenditures. 5

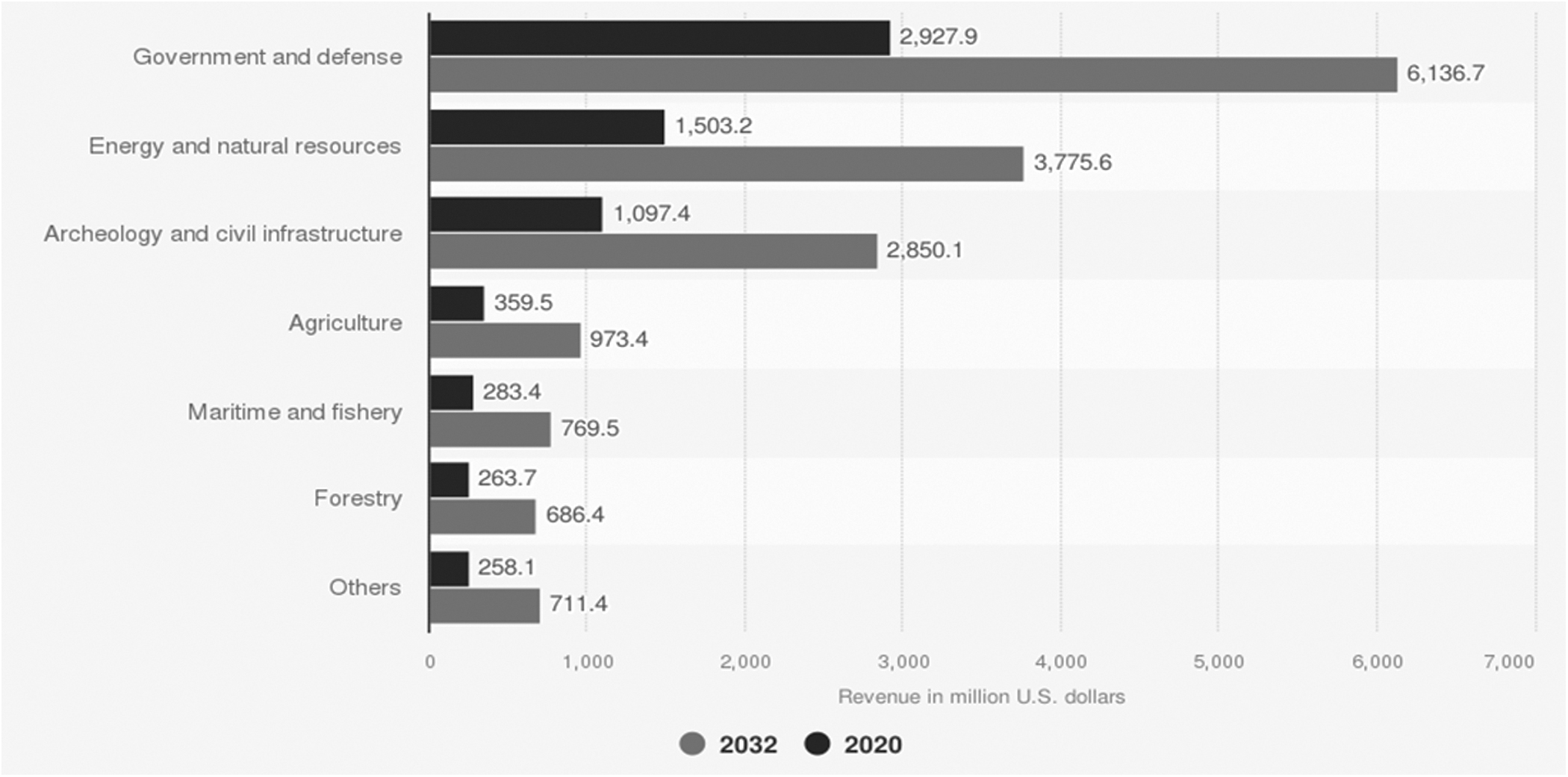

In 2022, civil budgets amounted to $55 billion, representing 54% of total spending, whereas defense expenditures rose to $48 billion, accounting for 46% of total spending. Civil expenditures are driven by ambitious projects undertaken by leading spacefaring nations, such as space exploration and launchers. These budgets are further inflated by post-COVID recovery plans and the short-term effects of inflation. In 2022, governments worldwide allocated the highest amount of funding, reaching $14.5 billion, to human spaceflight, making it the most heavily funded space application. Following closely behind is Earth observation and Meteorology, which received an investment of $12.7 billion this year. 5 This revenue is projected to climb to some 15.9 billion by 2032 (Fig. 5). In this area, the growing trend has addressed natural disaster forecasting and management, transportation and logistics, water and crop management, land and urban planning, telemedicine applications, education programs, and so on. 6

Projected global satellite earth observation market size in 2020 and 2032, by end user (in million U.S. dollars). 6

Public investments in Space Science and Exploration, totaling $10.2 billion, are closely linked to human spaceflight, as these two applications often complement and support each other.

Conversely, investments in defense-related space programs have reached a new record, spurred by escalating geopolitical tensions and the necessity to develop advanced space capabilities. In recent years, the domain of space has evolved into a crucial battleground and a fully fledged operational theater for the implementation of hybrid warfare tactics on the defense front. The militarization of space has reached unprecedented levels, with notable increases in investments directed toward “traditional” space applications such as Navigation, Telecommunications, and Earth observation. However, the primary growth driver now lies within the realm of Space Security and Early Warning. This particular field has witnessed a significant 5-year compound annual growth rate of 32.4%, resulting in a total value of $9.5 billion in 2022. 4

The gap between civil and defense spending continues to narrow, and according to projections from Euroconsult, it is expected to achieve a 50/50 parity by 2031. This shift will be driven by sustained growth in defense budgets throughout the decade.

The sharp and steady market growth (production and commercialization of space products and services) has also supported and boosted the growth of new space ventures.3,7

The United States now has 5,582 space-focused companies, almost 10 times more than the next country, the United Kingdom, which has 615. And there are more than 10,000 total, globally. 7 Most of them operate in the downstream segment, but there have also been a number of leading new ventures involved in the construction and launching of space vehicles, such as Blue Origin, Virgin Galactic, and SpaceX. It has already been proven by launch services (including crew and cargo transportation), satellite remote sensing, Research & Development (R&D), and media to support the activities of commercial enterprises and to enable companies to capture some significant value.

In addition, some segments of the value chain that do not presently yield high market value could become sources of commercial business as low Earth orbit demand grows.

Legacy Space Agencies in Transition

Parallel to the increasing involvement of the private sector in a diverse range of space-related initiatives and programs, the role of space agencies has also evolved over the years. During the initial 60 years of global space activity, national space agencies played a predominant role in driving the majority of space ventures. Within this framework, the private sector served as contractors for public programs, relying on public funding for their inception and continued operation. However, in the past decade, developments had been occurring concerning the growing affordability and ease of technological advancements, alongside a shift toward more business-oriented political leadership and a favorable financial landscape. This shift, accompanied by the increasing participation of commercial companies in public programs and a transformation in the dynamics of the public–private sector relationship, signifies a paradigm shift that is receiving heightened attention from governments and space agencies.

This evolving landscape, often referred to as the “New Space” dynamic, 8 presents new and emerging space actors with expanded opportunities to contribute significantly to the space sector. Although a precise definition of this dynamic remains elusive, it has been described as a disruptive sectorial transformation characterized by a variety of end-to-end efficiency-driven concepts that propel the space sector toward a more business- and service-oriented trajectory. In this emerging ecosystem, the future trajectory of the “New Space” dynamic is heavily reliant on the effective implementation and success of new public strategies. Consequently, most agencies have begun or are currently adapting their strategies, approaches, and modes of engagement with the private sector to align with and foster the emergence of private endeavors. This involves forging new types of partnerships and, to some extent, redefining their own roles to accommodate these changes.

One notable aspect of this emerging ecosystem, among several others, is the ability to share costs and risks between the private and public sectors, 8 potentially alleviating the financial burden on the public entity. This approach is most prominently observed in the United States. 5 Since its establishment in 1958, NASA has primarily focused on government-owned and operated space missions. During the Mercury, Gemini, Apollo, and Space Shuttle programs, the space agency enlisted private contractors to develop launch vehicles and spacecraft. In these instances, the involvement of the industry was predominantly as contractors through cost-plus contracts, which were based on the actual production costs and agreed-upon rates of profit or fees.

However, with the turn of the century and the retirement of the Space Shuttle, NASA seized the opportunity to explore new mechanisms that built upon previous initiatives aimed at seeking alternatives to traditional public–private relationships. These efforts included the exploration of new contracting schemes and procurement approaches. In recent years, both U.S. public policies and NASA itself have actively supported the development of public–private partnership (PPP) schemes. These schemes aim to achieve cost-effective means of accessing the ISS for cargo and crew by implementing cost-sharing contractual arrangements. The milestone payment-driven Space Act Agreements have been utilized as a strategy to facilitate these partnerships and achieve mutually beneficial outcomes.

In 2005, the establishment of the NASA Commercial Crew and Cargo Program Office introduced two significant programs aimed at enabling the national private sector to transport cargo and crew to the ISS. This marked a tangible shift in the U.S. space policy, which has now paved the way for a vibrant and innovative ecosystem with increased involvement of private actors. As a result, NASAs role has transitioned from one of orchestration and direction to a more facilitative approach driven by commercialization needs. These new policies in the United States have already contributed to the development of more accessible and cost-effective space programs. However, moving away from the traditional public procurement framework and accessing space-related services on more affordable terms requires more ambitious PPP schemes.

Private actors such as SpaceX, Blue Origin, Orbital ATK, and others are pursuing a risk-sharing approach based on the assumption of long-term government commitments. This approach enables them to provide optimized offerings for commercial customers and creates conditions favorable for private market adoption. With its new procurement approach, NASA has shifted the responsibility for design and delivery to the private sector. By departing from the traditional cost-plus system procurement process, the agency has facilitated the growth of commercial space capabilities. This approach benefits from cost-sharing and encourages innovative practices in commercial system development. As a result, the United States is currently at the forefront of the New Space movement, with the majority of these pioneering endeavors being led by American companies.

Regarding Europe, it is important to highlight the continent's notable achievements in the realm of commercial space. Since the late 1970s, several private European companies have made significant strides in exploring the potential of commercial space ventures. For instance, Arianespace, established in 1980, became the world's first private space launch operator, while SPOT Image, founded in 1982, emerged as the pioneer commercial operator and dealer for space imagery. In addition, satellite communication company SES commenced operations in 1985 and has since become one of the leading players in global TLC (telecommunications) services. Alongside these success stories, the European space agencies and relevant institutions have increasingly engaged in ambitious commercial initiatives and PPPs 5 across various fields. Examples include the ARTES program, TerraSAR-X, RapidEye, and the Hylas project, among many others.

While direct comparisons between the U.S. and European space sectors and their operating models may not be applicable due to inherent differences, it can be argued that the European space sector is also undergoing a similar transformation. In light of this, new opportunities are being cultivated to foster innovative forms of collaboration between the public and private sectors. The European Space Agency (ESA) and national space agencies are already taking significant steps in this direction, aiming to promote entrepreneurship and empower private actors to assume more prominent roles in space programs.

At the ESA Ministerial Council in Lucerne in 2016, ESA Member States allocated €10.3 billion for space programs, based on the vision of a “United Space in Europe in the era of Space 4.0.” Space 4.0 represents the evolution of the space sector into a new era, characterized by a transformed landscape. In ESAs context, “Space 4.0i” describes how the agency envisions its role as a space agency for Europe in the future. This concept combines global space developments with ESAs specific interpretation, encompassing four key actions: innovation, information, inspiration, and interaction. The ESA aims to realize these actions through disruptive and risk-taking technologies, strengthening connections with public and user communities, launching new initiatives and programs, and forging enhanced partnerships with member states, European institutions, international players, and industrial partners.

Ultimately, the policies introduced in the early 2000s to foster the development of a robust and sustainable commercial space sector have achieved their objectives, particularly in the United States. As a result, public space agencies now face programmatic opportunities and strategic challenges within this evolved context, acknowledging the necessity to adapt their approaches further to effectively fulfill their mandates.

EMERGING SPACE AGENCIES IN CONTEXT

In the last 5 years alone, more than 10 countries have established their own national space agencies, as depicted in Figure 6. The proliferation of space agencies or administrations dedicated to space has experienced exponential growth in recent decades.

Creation of space agencies since 2000 (European Space Policy Institute database). 1

The relative standing and global position of countries in the field of space depend on the combination of “Capacity” (referring to a country's ability to implement space strategies to achieve its economic, political, or social objectives) and “Autonomy” (referring to the country's capability to formulate space-related interests independently, regardless of divergent political interests).1,9 For instance, the Luxembourg Space Agency (LSA) can be considered an example of a limited space agency with low capacity and autonomy. On the contrary, the United Arab Emirates Space Agency (UAESA) can be categorized as an autonomous spacefaring nation, characterized by higher autonomy compared to capacity. Other notable examples of emerging spacefaring nations include Argentina, Brazil, and Mexico in Latin America, South Africa, Egypt, Saudi Arabia, Iran, United Arab Emirates and Turkey in Africa and the Middle East, as well as Australia, New Zealand, Indonesia, Vietnam, Malaysia, and South Korea in the Asia-Pacific region.

When examining the rationales for newly formed space agencies, Kommel et al. 2 have identified six types: economic, socioeconomic, coordination, centralization, geopolitical, and regulatory (Table 1).

Main Rationales for the Establishment of Space Agencies

From Kommel et al. 2

Economic rationale: When examining the functions and objectives of these recently established space agencies, significant importance is placed on enabling and facilitating the expansion of the national space industry to stimulate economic growth. However, this support operates in a reciprocal manner. Just as emerging space agencies are fostering the growth of the private sector, the primary motivation behind the establishment of modern space agencies is often the commercialization of space. The rise of the “new space” sector has provided smaller and developing nations with the opportunity to implement space programs without requiring exorbitant budgets as in the past.

Socioeconomic rationale: Governments worldwide are experiencing a growing impetus to engage in space activities, recognizing the multitude of opportunities they present for enhancing the well-being of their societies. These opportunities encompass a wide range of areas, including climate and food security, as well as educational and professional prospects.

Coordination and centralization rationale: In the past decade, the establishment of space agencies by many countries has often been driven by the need to streamline and centralize the administration of their diverse space programs and activities. Previously, these initiatives were dispersed across different government departments. It is noteworthy that emerging space nations typically do not create space agencies as their initial step in space involvement. Instead, they tend to establish these agencies after already engaging in various space endeavors, such as satellite launches, scientific research promotion, or participation in international space organizations.

Centralization rationale: By adopting a more centralized structure for their space sectors, countries aim to reduce redundancy, raise awareness of available opportunities, encourage participation, and optimize resource utilization.

Geopolitics rationale: While less prevalent than in the past, the establishment of a few emerging space agencies still serves the purpose of enhancing a nation's geopolitical position. Governments of these nations often aim to formalize their space endeavors through dedicated agencies to engage with the global space community and strengthen international relationships. Furthermore, the space agencies of emerging space nations can serve as a platform to establish themselves as prominent players in space exploration, showcasing their clear goals, strategies, and policies. Taking a leading role in space endeavors enables these nations to demonstrate political stability, financial security, societal development, as well as scientific and technological expertise to the international community. For space agencies involved in military space activities, such organizations also contribute to promoting national security.

Regulation rationale: Finally, certain countries have established space agencies with the specific purpose of regulating their national space activities. These countries usually have a well-developed space sector involving various players from domestic industries. By creating a dedicated space agency and assigning it regulatory responsibilities, these nations have been able to consolidate their regulatory frameworks and streamline processes, such as licensing, while ensuring compliance with international laws and regulations.

THE “PROFILING” RESEARCH

For the purpose of our research, we defined “emerging space agencies” as those civil agencies at the national level dedicated to the development of space science and technology, the exploitation of space data and applications for governance and the betterment of society, or the development of a commercial space economy.2,9,10

An in-depth literature review of four emerging newly formed space agencies was conducted to provide practical exemplification of the profiling taxonomy of emerging space agencies. This review includes open-source data from articles, books, contracts between space organizations, government archives, and other publicly available sources. These sources encompassed a wide range of sector-specific and general contributions, providing a comprehensive basis for the study. Results were then compiled to identify trends and draw general conclusions about the birth and development of emerging space agencies.

The Socioeconomic Rationale of the African Space Agency

The agency is expected to begin working closely with South Africa and Nigeria, whose national space programs are among the most advanced on the continent, and based on the African Union's Agenda 2063, the African Union intends to establish the African Space Agency in 2023.

In article 4 of the statute of the agency, 11 it is stated that “The main objectives of the African Space Agency are to promote and coordinate the implementation of the African Space Policy and Strategy and to conduct activities that exploit space technologies and applications for sustainable development and improvement of the welfare of African citizens. In particular, the Agency shall:

a. harness the potential benefits of space science, technology, innovation and applications in addressing Africa's socio-economic opportunities and challenges….”

The Agenda 2063 program is the African Union's long-term framework for socioeconomic development, regional integration, and preservation of history and culture.

The Agenda has 15 flagship projects, including the Africa outer space program. It has a direct or indirect impact on the other flagship programs. It focuses on Earth observation, meteorology, satellite communication, satellite navigation, and astronomy.

A number of application projects that may benefit from the availability of communication satellites are being considered and targeted:12–14

- The goal of the African Single Air Transport Market is to connect Africa's major cities and create a unified air transport market in Africa. This goal rests on the security of space and airports on the continent. In this context, satellite communications are needed for all phases of flight, weather information, communications, and in-flight services.

- The goal of the integrated high-speed rail network is to connect all African capitals and commercial centers by rail. To facilitate the movement of goods and people throughout Africa, satellite communications should provide the information the rail network needs: location, navigation, weather, and communication.

- The Pan-African Virtual and Electronic University project, run from Yaoundé, Cameroon, is proposed as an open, distance, and electronic learning tool of the Pan-African University. This project requires communication satellites for students and their teachers to access the internet.

- The African Commodities Strategy, another of the flagship projects, assumes the use of satellites for communications. Communication satellites are indispensable for the real-time transfer of price information on commodities and processed products from around the world.

- The Secretariat of the African Continental Free Trade Area in Accra, Ghana, needs communication satellites to maintain the African Trade Observatory, share information on trade and tariffs, and for its payment and settlement system.

- The African passport project was launched to remove restrictions on the free movement of Africans everywhere in Africa. This system also needs communication satellites to transmit information about travelers.

- The Grand Inga dam project will produce more than 40,000 megawatts of electricity to increase power supplies across the continent. The monitoring of the dams is based on weather information provided by meteorological satellites. Earth observation satellites are also indispensable for surveying rivers and plains.

- Other projects, such as the Great Museum of Africa and the African Encyclopedia, could potentially leverage the potential of the internet to increase visibility and usability globally.

The Economic Rationale for the LSA

The LSA was established in 2018 as a Joint Venture (private and public) and placed under the supervision of the Minister of Economy. It is an associate member of the ESA and has as its mission the development of industrial and service activities in the space field. 15 The birth of this organization is to be placed in the context of a long-term strategy adopted by the country's government, which since the 1960s has reduced or even replaced, the economic weight of traditional sources of income consisting of Agriculture and the Steel Industry. Today, in fact, 30% of the country's income comes from the financial services sector. Luxembourg's ruling class has come to believe that Space can be an important opportunity for economic and social undertaking after having successfully operated in the field of telecommunications. Indeed, the first European Enterprise (the Societè europèenne des telecomunications-SES) was born in Luxembourg in 1985 to market the “continuous operation” of satellite connections for radio and television broadcasting.16,17

In 2016, the partnership between the government and the ESA enabled the establishment of the European Space Resources Innovation Center. The Center is in charge of providing information and assistance to private players wishing to enter into space business (construction of satellites and their components, new satellite services, exploratory missions to asteroids, etc.). 18 The LSA true to its mandate not to undertake space missions itself or to implement related tools is in the business of empowering private companies to address these opportunities. Among various other initiatives, the Agency established 3 years ago an Investment Fund devoted specifically to the business of Space. 19

Luxembourg, thanks to its tradition of developing a commercial satellite communications industry (which currently accounts for about 2% of its Gross Domestic Product), has been dedicated to expanding its commercial space sector. The country has leveraged its legal framework to attract private sector investors. Luxembourg's 2017 Space Law, similar to the Commercial Space Launch and Competitiveness Act of 2015, provides that companies doing business within the territory of the Grand Duchy (e.g., having offices in Luxembourg) can legally own resources from celestial bodies. This favorable regulatory framework has allowed international space mining companies such as Deep Space Industries to establish their operational headquarters in Luxembourg.

The Coordination and Geopolitical Rationale for the UAESA

The agency established in 2014 emblematically expresses the strategic design of a country that aims to develop space activities as an important source of income and thus economic growth. 20 Investments in Space along with other uses of resources in industrial activities and technology intensive services are expected to replace the country's current main source of income consisting of hydrocarbon extraction and commercialization. 21 The UAESA is within the decision-making sphere of the government as it is part of a Section of the Prime Minister's Cabinet. This is in charge of Economic Development and the country's future. Members of the Agency's Board are representatives of each individual Emirate while the Advisory Council includes experts professionally connected with major international space agencies. 22

Thus, it is a group of advisors capable of capturing the most interesting technological innovations and experiences that are being developed in major countries at the forefront of space technology transfer programs. The Agency has a very large budget, approaching $5.2 billion in 2020. Operating alongside the UAESA is a Space Research Center that employs 150 engineers, of which 30% are women. This group of engineers built the MARS-Hope probe with the collaboration of JAXA. The probe launched in July 2019 with the Japanese rocket H-IIA is currently orbiting Mars. Its mission is to analyze the planet's atmosphere and surface. Thus, this mission has a reconnaissance function, and according to UAESA's plans, it could precede other more challenging missions. Finally, it is worth mentioning the commitment placed by the agency to create a Master Course in Space Science and Technology.

The UAESA is strengthening the United Arab Emirates space sector by establishing international partnerships in the space sector and committing to represent the country in space conventions and international forums, along with other activities. 23

The future agency aims to pursue international cooperations (e.g., with major space agencies, governments, aerospace companies, and academic institutions) to be fully integrated into the international space ecosystem, join major projects, and build local know-how.

The Centralization and Regulation Rationale for the Australian Space Agency

The Act that established the Australian Space Agency in 2018 explicitly refers to its mission as a structure to promote industrial development. Also consistent with that mission, the Act provides for the organizational placement of the Agency under the Minister of Industry, Science, Energy, and Resources. In truth, the country, since the mid-1970s of the last century, had organized radio and television transmissions via geostationary satellites and had used for this activity, the Australian Space Center, which was later closed in 1996. In its short life, the agency has drawn up a 10-year program (2019–2028), the main points of which focus on providing substantial support for space research and training activities.

Reference is made in this regard to the expertise that exists in the field at the Universities of Canberra and Melbourne. Mention is also made of the Project for the utilization of networks of small satellites functional for the development of Blockchain-based financial systems. For future considerations on the Agency's activities, it is worth mentioning that it, in addition to cooperation with NASA, has signed a number of “Memoranda of understanding” with the agencies of France, the United Kingdom, and Canada.

The Agency has the function of regulating Australia's space and high-power rocket activities, also overseeing international agreements affecting space regulation.24–26

The Space Act 2018 establishes a system for regulating space activities in Australia or carried out by Australian nationals outside Australia. The main activities that must be approved under the Act include:

- the launch/return of a spacecraft or a satellite from/to Australia; - the launch/return of a spacecraft overseas or a satellite (for Australian citizens who have an ownership interest); - operating a launch facility in Australia; - launching a high-powered rocket from Australia.

Australia's creation of a space agency came after having previously been involved in the space sector to varying degrees, such as by launching satellites, producing scientific research, or participating in international space initiatives.

By creating a more centralized structure for their space sectors, the country aimed to reduce dispersion, increase awareness of available opportunities, encourage participation, and enable more rational use of resources.

CONCLUSIONS

The increasing opportunity for new and emerging players in the space sector to make significant contributions is commonly referred to as the “New Space” dynamic. While a precise definition of this dynamic is elusive, it has been described as a disruptive trend driven by various efficiency-focused concepts that steer the space sector toward a more business- and service-oriented approach. The future of this dynamic is heavily reliant on the successful implementation of new public strategies. As a result, many established space agencies are adjusting their strategies, approaches, and interactions with the private sector to accommodate and foster the rise of private endeavors. This involves forging new partnerships and, to some extent, redefining their roles. One notable aspect of this emerging ecosystem is the sharing of costs and risks between the private and public sectors, potentially alleviating the financial burden on public actors.

In the past decade, there has been a significant increase in the number of emerging space agencies. These agencies primarily focus on the management of space activities rather than executing their own scientific missions or developing hardware. Their roles typically include the development and implementation of national space strategies and policies, promoting international cooperation through agreements with other spacefaring nations, and participating in international forums. In addition, they play a crucial role in promoting and coordinating the growth of their national space sectors, aligning with the previously mentioned rationales. Some of these agencies also prioritize tasks such as promoting research and education, establishing regulatory frameworks, enhancing defense capabilities, utilizing space technologies for national development, supporting launch programs, and guiding major research directions.

In conclusion, emerging space nations are driven more by commercial considerations, opting to support private companies' space ventures rather than pursuing their own independent endeavors. This shift can be attributed, in part, to a changing perspective on the potential benefits of space for life on Earth. The previous Cold War mindset, which viewed space access as a means to demonstrate technological superiority and national sovereignty, has gradually given way to a more pragmatic approach. Governments and citizens now recognize the potential of space to promote sustainable socioeconomic development, address existing challenges, and provide competitive advantages for businesses.

Footnotes

AUTHORs' CONTRIBUTIONS

The submitting author is responsible for ensuring that contributions of all authors are correct.

AUTHOR DISCLOSURE STATEMENT

No competing financial interests exist.

FUNDING INFORMATION

No funding was received.