Abstract

The Tissue Engineering and Regenerative Medicine International Society of the Americas (TERMIS-AM) Industry Committee conducted a semiquantitative opinion survey in 2010 to delineate potential hurdles to commercialization perceived by the TERMIS constituency groups that participate in the stream of technology commercialization (academia, start-up companies, development-stage companies, and established companies). A significant hurdle identified consistently by each group was access to capital for advancing potential technologies into development pathways leading to commercialization. A follow-on survey was developed by the TERMIS-AM Industry Committee to evaluate the financial industry's perspectives on investing in regenerative medical technologies. The survey, composed of 15 questions, was developed and provided to 37 investment organizations in one of three sectors (governmental, private, and public investors). The survey was anonymous and confidential with sector designation the only identifying feature of each respondent's organization. Approximately 80% of the survey was composed of respondents from the public (n=14) and private (n=15) sectors. Each respondent represents one investment organization with the potential of multiple participants participating to form the organization's response. The remaining organizations represented governmental agencies (n=8). Results from this survey indicate that a high percentage (<60%) of respondents (governmental, private, and public) were willing to invest >$2MM into regenerative medical companies at the different stages of a company's life cycle. Investors recognized major hurdles to this emerging industry, including regulatory pathway, clinical translation, and reimbursement of these new products. Investments in regenerative technologies have been cyclical over the past 10–15 years, but investors recognized a 1–5-year investment period before the exit via Merger and Acquisition (M&A). Investors considered musculoskeletal products and their top technology choice with companies in the clinical stage of development being the most preferred investment targets. All sectors indicated a limited interest in early-stage start-up companies potentially explaining why start-up companies have struggled to access to capital and investors based their investment on the stage of a company's life cycle, reflecting each sector's risk tolerance, exit strategy, time of holding an investment, and investment strategy priorities. Investors highlighted the limited number of regenerative medical companies that have achieved commercial status as a basis for why public investors have been approached by so few companies. Based on respondents to this survey, regenerative medical sponsors seeking capital from the financial industry must keep the explanation of their technology simple, since all sectors considered regenerative medical technology as difficult to evaluate. This survey's results indicate that under the current financial environment, many regenerative medical companies must consider codevelopment or even M&A as nondilutive means of raising capital. The overall summary for this survey highlights the highly varied goals and motivations for the various sectors of the government and financial industries.

Introduction

Toward this end, the Committee conducted a survey of the members of TERMIS-AM to assess the hurdles faced within four major participant groups in the commercialization stream and published these results in 2010.1,2 The groups surveyed included academia, start-up companies, development-stage companies, and established companies. A significant hurdle consistently identified by the TERMIS-AM membership survey was access to capital for funding additional research and development activities necessary for the commercialization of a regenerative medical/tissue-engineering technology.

To better understand the funding challenge, a survey of governmental agencies and the financial industry was developed with input from different investment sectors coded as government, private, and public investors. These sectors generally represent funding of the commercialization continuum from academic to start-up, development stage, and ultimately established companies.

The survey was developed to understand three major characteristics of governmental agencies and the financial industry: (1) previous investment experience with regenerative medicine technologies; (2) level of continued interest in future investments for regenerative medical technologies; and (3) perceived risks and barriers regarding a future investment in this industry. Anonymous responses were received from 37 institutions representing each of the three sectors. Although the data represent only a small sample of the potential governmental agencies and financial institutions that may consider investments in regenerative medical technologies, this information provides a roadmap for future surveys and highlights the differences that exist within and between governmental agencies and the financial industries.

Methodology

Study population

A customized online semiquantitative opinion survey was created and distributed to governmental and financial organizations, including the public and private investors. Investment groups included venture capitalists, public funding groups (hedge, mutual, and other funds), banks, angel investors, and multiple governmental agencies that have disclosed publically an intent to invest in tissue-engineering/regenerative medical technologies (e.g., National Institutes of Health; Department of Defense; Food and Drug Administration; National Science Foundation).

Two online data bases (Web-Intellectuals, www.web-intellectuals.com, and Angel investor directory, www.inc.com/articles/2001/09/23461.html) were used to source public and private financial companies. Governmental agencies were identified through established Federal communication links. The survey was distributed to all available contacts with respondents entering directly into an online survey data collection Website for each question (www.surveymonkey.com). Data from all respondents were included in the survey analysis.

Survey design

The survey was designed to provide data for the assessment of three core questions:

1. Previous experience with making an investment in regenerative medical/tissue-engineering technologies—what do you see as an exit strategy? 2. Level of interest in tissue-engineering/regenerative medical technologies—have you ever invested or plan to invest in a regenerative medical/tissue-engineering company? 3. Perceived risks and barriers to making an investment decision in a tissue-engineering/regenerative medical technology—rank order the major barriers to the emerging tissue-engineering/regenerative medical industry.

Sector assignments

Participants were asked to anonymously self-identify their sector as public, private, or governmental.

Survey questions

Questions were designed to characterize each sector's investment history, risks and barriers considered to limit the amount or duration of investment, financial interests, technology preferences, stage of life company's life-cycle that would support an investment, amounts of funding available, type of exit strategy, and timelines expected for a return to the investment sectors. Choices within some questions were quantified to better understand risks and factors that would drive an investment.

Analysis of data

Data were analyzed to identify general differences between each sector and assess each sector's investment philosophy toward regenerative medicine and tissue-engineering technologies. Responses were summarized in each sector to highlight differences between groups (private, public, and government) and characterize drivers of investment choices that would highlight similarities and differences across the sectors.

Results

Respondent profile

A total of 37 investor organizations surveyed were self-assigned to three categories. Table 1 depicts the numbers of responders who were self-assigned to each category.

Percentages shown are a function of total respondents answering the question.

Previous experience investing in regenerative medicine

Respondents were asked to designate if they currently hold any investments in regenerative medical technologies. This included investment holdings in regenerative medical technologies or companies with a pipeline that includes regenerative medicine, which are shown in Table 2.

Percentages shown are a function of total respondents answering the question.

Each sector had some respondents that currently hold investments in regenerative medical technologies or had in the past; however, each group also had a substantial number of respondents that did not currently have investments in regenerative medical technology. Percentages of current investment holdings were distributed similarly across all groups.

Government sector made investments in regenerative medical technologies before the turn of the century through the time of the survey (Table 4). In contrast, a high percentage of public and private respondents have waited to observe technology advance further in the development pipeline, thus delaying capital investment (Table 3).

Percentages shown are a function of total respondents answering the question.

Percentages shown are a function of total respondents answering the question.

Respondents had a wide range of experience with investment in regenerative medical technologies with the private group being the least experienced (Table 3). A large percentage of all respondents (50% or greater) had a relatively long history (∼10 years) of providing capital to regenerative medical technology. However, approximately one in three public and private respondents has only recently (5–6 years) started to invest in regenerative medical technologies.

The number of companies that have approached the various sectors for capital illustrates a respondent's experience with this technology, as well as the industry's appreciation of the various approaches for funding regenerative medicine companies (Table 4).

The numbers of companies approaching each investor group may also reflect the relatively early stage of the regenerative medical industry and the life cycle of regenerative medical technologies (Table 4). The government sector clearly had the most companies/technologists approaching them for funding (40% have been approached by more than 10 companies). Given the robust academic pipeline of regenerative medical technologies and the experience of those seeking funds for their projects, this distribution may be expected. Private sector respondents had a wide distribution of experience with some being approached by only a few companies, while 25% had been approached by more than 10 companies. The transition from government funding to private capital may reflect the earliest step toward commercialization, suggesting that the venture capitalists (i.e., private sector) may be at the center of the transition occurring with maturation of the regenerative medical pipeline.

Public investors were approached by relatively few companies in 2011 (Table 4). This may reflect the hurdles that must be met before public investors will consider funding a particular technology (see the Perceived barriers/risks section). Similarly, few regenerative medical companies have transitioned through an initial public offering process to become publically traded. As the regenerative medical pipeline expands and the industry matures, public investors will likely be sought to a greater extent.

Level of investor interest

Previous experience can influence an investor's interest in a particular technology, and depending on the outcome of the previous experience, investor decision making can be based on many different factors. Most respondents in the current survey had invested previously in regenerative technologies and had at least one regenerative medical company seeking funds at the time of the survey (Tables 2–4). In an attempt to qualify each sector, a series of questions were put forward to determine the extent of respondent interest.

The amount of capital each group was willing to put into a regenerative medical technology was widely varied. Table 5 depicts the magnitude of investment each group was willing to make and the distribution within each group.

Percentages shown are a function of total respondents answering the question.

A majority of government (>85%) respondents were investing ≥$2MM in a particular technology. However, a majority of private and public respondents (70–75%) were willing to invest ≥$500K, indicating that smaller amounts of capital may be expected from these two groups for regenerative medical technologies. Nonetheless, both governmental and public respondents had similar amounts of capital limits with 57% and 50%, respectively, being willing to invest >$5MM in a regenerative medical technology. Notably, the stage of a company's life cycle and risk tolerance were quite different between these sectors (Perceived barriers/risks outlined below).

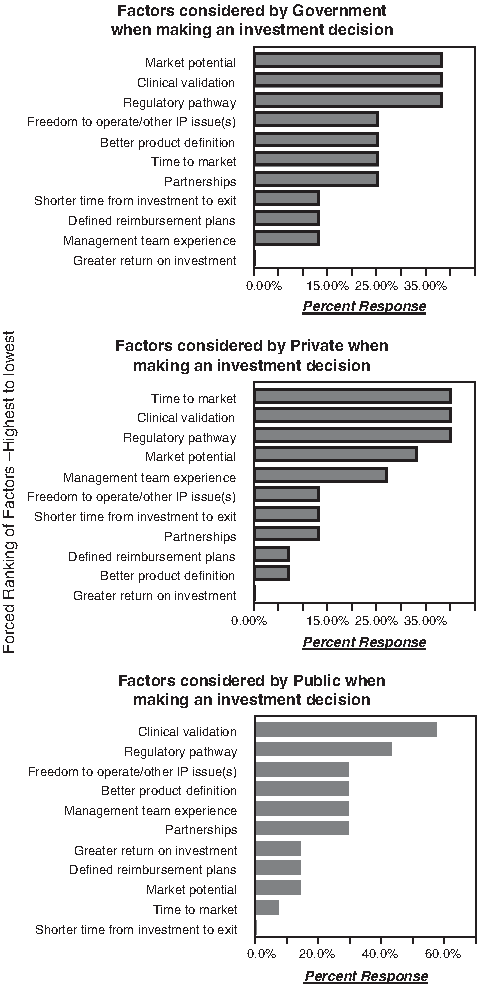

The survey respondents had a broad range of opinions regarding what factors were most important in making an investment decision that varied across the sectors (Table 6). However, clinical validation and regulatory pathway clarity were key factors considered by all three sectors before making an investment decision. All sectors considered Patent protection as an important factor to consider. Public and private respondents uniquely considered management team experience as an important factor, whereas government and public investors gave a higher ranking to potential partnerships than did the private investor (Table 6). These differences may reflect specific sector exit strategies, and each sector unique mandate to obtain a return on the investment (see the Perceived barriers/risks section).

Levels shown are a function of total respondents answering the question for each sector.

IP, intellectual property.

The duration of investment seems to be driven by many independent factors (Fig. 1), including the life of a fund, type of the grant being sought, and investor understanding of the key development milestones being targeted at the time of investment (see the Perceived risks/barriers section). Sectors varied substantially between and within groups in regard to their patience for a return on the original investment (Table 7).

Forced ranking of factors—highest to lowest. IP, intellectual property.

Percentages shown are a function of total respondents answering the question.

Generally, the public sector sought an exit from their investment in 3 years or less (Table 7). Private and government respondents were generally more patient, and a majority was willing to wait up to 5 years for a return. These differences most likely represent the stage of development for the different sectors; government and private sectors invest during the early stage of a company's life-cycle versus public investors seemed to generally wait until the technology has advanced to clinical or commercial stages of development. In the later stages of development, timelines are generally well defined with a shorter duration of time to an exit or value generating milestone.

Two investor sectors, private and public, had a common appreciation for a value generating milestone (Table 8). Such milestones frequently represent a mechanistic or clinical proof of concept when development costs are increasing and risks have been reduced, thereby attracting a broader investment population. The specific milestone that is value creating will vary generally between government and private/public investors—the private and public sectors seem to be interested in a clinical or commercial milestones, whereas the government seems to be interested in the application of a research outcome. This difference may be embedded in the distinction that these two groups have with relation to the timing for an exit—government longer duration than the private or public sectors (Tables 7, 8).

Percentages shown are a function of total respondents answering the question.

M&A, Merger & Acquisitions; IPO, initial public offering.

Each investor category had significantly different strategies to determine when they would exit the investment for another technology or technology category. Table 8 highlights the differences between sectors in what they see as an exit strategy.

Investor groups were widely disparate in their exit strategy, reflecting timing of entry into a technology's life cycle—early for government, whereas later for public sectors, possibly reflecting expected timing for returns (Table 8). Government investors clearly looked to confirmation of the technology's value with many focusing on regulatory (regulatory approval) or commercial (Merger & Acquisitions [M&A]; codevelopment partnerships) qualifications. In sharp contrast, the vast majority of public investors were looking for a return on their investment that occurs with stock price performance and M&A, when a technology is in the later stages of development.

Exit strategy preference for the private respondents may also reflect the motivation and timing of their initial investment in a particular technology (see Perceived barriers/risks section). Private respondents frequently chose companies that are in early stage of their life cycle, well before there is a market capitalization event. Consequently, M&A and initial public offering (IPO) milestones represent key transition points for a technology, with value creation during the IPO cycle or some prepublic purchase of the technology via M&A (Table 8).

Respondents from each sector had a consistent view on the therapeutic area in which they considered a higher probability of success. Table 9 ranks the therapeutic areas that each investor group would consider most likely to receive their funding.

Choices were ranked with one being the most interest in investing and six being the least interest in investing.

Government and private sectors ranked cardiovascular as the top therapeutic area for investment with bone/cartilage/muscle as the second most preferred category (Table 9). Public respondents also considered musculoskeletal technologies as an area of substantial interest. Skin and gastrointestinal approaches were considered a therapeutic area of lower relative interest for making an investment by government and public respondents, but private sector considered this in the top 50% in the forced ranking of these technologies (Table 9). Although differences in therapeutic focus varied among the investor groups, the choices may reflect maturity of the technology pipeline more than market potential, since very few regenerative products have achieved commercial success, and those currently on the market or advancing in development are in cardiovascular and musculoskeletal therapeutic areas.

Regenerative medical technologies are generally classified as device, biological, or combination (device + biological) products for regulatory purposes and clinical trial design. When investors were asked to rank order the different technology categories to establish their investment preferences for technology classification, significant differences were found in both preferred technology and investment priorities within a product technology (Table 10).

Bio, biological; Combo, combination.

Government respondents were equally split in preferring technologies classified as either device or biological (Table 10). However, 40% of respondents place combination products as their second choice. Over 50% of private respondents preferred device technologies, whereas an overwhelming majority (∼70%) placed combination technologies as a third choice of investment. Public respondents were generally more favorably inclined to select biological technologies, although both device and combination product classifications were ranked as favorable second choices by 45% of respondents in this sector. Approximately 30% of private sector respondents ranked biological and combination products as their second preference (Table 10). Government sector had a random ranking of product classification, perhaps representing a focus on the mechanism of action more than technology classification.

Perceived barriers/risks

The experience that each respondent has with successful investment decisions will vary in and between categories based on their own personal experience with technologies in their respective portfolios. To establish the perceived risks investors observe in regenerative technologies, several questions were used to define barriers that investors experience when making their decisions. Table 11 depicts how investors perceive the risks of evaluating regenerative medical technologies as compared to other biotechnologies when making an investment decision.

Percentages shown are a function of total respondents answering the question.

A high percentage of all investors consider regenerative technologies more difficult to evaluate than other biotechnologies with 50%–64% of public and private respondents, respectively, considering these technologies more difficult to evaluate for making an investment decision (Table 11). Government respondents consider regenerative medical technologies as or more difficult than other technologies to evaluate.

No respondents in the government or private sectors considered regenerative technologies less difficult to evaluate than other biotechnologies, and only 17% of public respondents considered regenerative technologies to be less difficult than other technologies, perhaps highlighting a common practice among the public sector to utilize technology-specific external experts in making their investment decisions.

Survey respondents in each sector consider different barriers when making an investment decision in regenerative medicine technologies. These barriers are outlined in Table 12.

Each sector had a different ranking for the highest barriers for investment—government respondents considered scientific basis/patents and lack of regulatory clarity as the most significant barrier (Table 12). Private respondents considered the commercial and reimbursement challenges as being most significant, and public respondents considered clinical translation as the single most challenging barrier. Respondents from the three sectors had similar perspectives on the least significant barriers—manufacturing know-how and pharmaceutical industry interest in regenerative medicine (Table 12). The differences between investor categories may reflect the stages of a company's life cycle, when each group decides to invest (see Table 13), and the experiences gained by each group as to what increases the likelihood of successful commercialization (see Table 6).

Percentages shown are a function of total respondents answering the question.

The stage of a company's life cycle determines the extent of risk and the probability of return on an investment simply by the stage of development through the pipeline (Table 13). The maturity of a technology reflects the amount of information available at the time of investment there by allowing differential risk assessment to accommodate an investor's risk tolerance.

Investor preferences vary significantly among the three sectors (Table 13). In general, government respondents would invest in a technology or a company at a much earlier stage of the technology's life cycle, whereas the private and public respondents have an overwhelming preference for clinical-stage development opportunities. The limited government interest in early-stage start-up companies highlights the challenges faced by emerging regenerative medical companies in obtaining funding (a key challenge highlighted in the first survey) and the basis for the current analysis.1,2 The limited interest in the commercial stage of development may reflect the limited number of regenerative medical companies that have actually achieved commercial status, and thus attract the public investor.

Basing their investments on the stage of a company's life cycle highlights a fundamental difference of investment priorities and underpins risk tolerance, timelines to exit, exit strategy, and the amount of money investors are willing to put forward (see the Perceived barriers/risks section). The impact of this choice influences how the regenerative medical industry will grow and mature in the future.

Each sector considers risks within the context of their fund objectives, state of the technology development, and personal experience. Current investor risks considered as barriers to future investment by each sector are broadly defined (Table 14).

Percentages shown are a function of total respondents answering the question.

Changes to governmental healthcare policy and uncertainties regarding pricing and reimbursement were considered the major barriers to new capital investments by a majority of respondents in all three sectors (Table 14). Both of these categories would be heavily influenced by changes in federal government policy more than scientific or technical advances. Nonetheless, a high percentage of investors from all sectors (20–33%) indicated that other factors would impact their decision to put more money to work in regenerative medicine (Table 14). Other factors included the high cost of technology development at early stages of technology evaluation and the relative paucity of data on various regenerative medical and tissue-engineering technologies with respect to the mechanism of action and clinical experience (data not shown).

Conclusions

To better understand the governmental and financial industry's funding environment, the Industrial Committee conducted the present survey to better define the barriers for making capital investments available for regenerative medicine and tissue-engineering technologies. To this end, a survey of investors from three financial sectors (government, public, and private) was conducted. Responses (n=37) from these groups provided insights into what may be considered before making an investment in regenerative medicine technologies. Highlights from this survey were the following:

1. A high percentage (<60%) of respondents (governmental, private, and public) were willing to invest >$2MM into regenerative medical companies at the different stages of a company life cycle. 2. The top three perceived challenges considered as barriers to making an investment in regenerative medicine technologies were regulatory pathway clarity (#1); clinical translation of the technology (#2); and commercial and reimbursement uncertainty (#3). Similarly, the most important factors in guiding respondents toward making an investment decision were regulatory pathway clarity and clinical translation 3. Investments for regenerative medicine have occurred in cycles spanning the past two decades as demonstrated by the public and private respondents putting capital into regenerative medicine before 2000 and then again in the following decade where all financial groups have increased investments after 2009/10. Duration of an investment, before exit, was relatively consistent between the groups with 1–5 years equally divided as 1–3-year (public) and 3–5-year (government and private) periods. Primary exit strategy for all sectors focused largely on M&A. 4. Respondents generally preferred the following areas for their investments: (i) Therapeutic Area—musculoskeletal>cardiovascular>dermal>renal>liver; (ii) technology classification—biotechnology>medical technologies=combination product companies; (iii) life cycle of company—clinical-stage development. 5. All sectors based their investment on the stage of a company's life cycle reflecting each sector's risk tolerance, exit strategy, time of holding an investment, and investment strategy priorities. All three sectors indicated a limited interest in early-stage start-up companies potentially explaining why start-up companies have highlighted access to capital as the primary barrier to commercialization success in the first survey.

1

Similarly, the limited number of regenerative medical companies that have achieved commercial status may reflect why public investors have been approached by so few companies.3,4

Based on respondents to this survey, regenerative medical sponsors seeking capital from the financial industry must keep the explanation of their technology simple. Notably, all sectors considered regenerative medical technology as difficult to evaluate. They also highlighted regulatory pathway uncertainty and poorly established clinical applications as barriers to making capital investments. Finally, the survey results indicate that under the current financial environment, many regenerative medical companies must consider codevelopment or even mergers and acquisitions as nondilutive means of raising capital.

Given changes in the industry over the past 12 months, including the rise and fall of various companies, 10 survey results show that the financial industry and governmental sponsors are looking for evidence of clinical impact from regenerative medical technologies. Although the ambition of all those working on development of regenerative medical technologies is to seek potential sources of translational funding, the attrition associated with any medical product development remains daunting. This challenge is amplified with new and breakthrough technologies such as regenerative medicine. In general, publically traded companies have continued to bring good market performance and potential returns to investors—some of which have increased over 100% in market value 10 ; however, price volatility, and new company start-ups bring a wide range of risks that are not equally considered by all sectors of the financial industry and government.

The overall conclusion from the current survey emphasizes significant differences within and among funding sectors in their criteria used to determine capital investments. The current survey highlights which financial sector may be most appropriately solicited for working capital based on understood risks for a particular regenerative medical technology.

Footnotes

Acknowledgments

The authors would like to thank Sarah E. Wilburn, TERMIS Administrator, for her support in the administration of the survey. We are also grateful to all respondents who participated in the survey.

Disclosure Statement

No competing financial interests exist.