Abstract

The wave of mega-mergers sweeping the food, agribusiness, and retail grocery industry from seed to supermarket has accelerated consolidation and concentrated market power in the hands of only a few dominant corporations. Federal regulators have done little to curb the merger mania in these sectors, which will ultimately lower the prices farmers receive for crops and livestock and raise the prices consumers pay for food. But the consolidation also has significantly constrained the range of choices consumers have at the supermarket, prevented independent food innovators from surviving in the marketplace, amplified food safety problems, and presented challenges to the resiliency of the food system itself. This article examines the size, scale, and scope of recent mergers in the food, agribusiness, and grocery retail sectors and discusses the ramifications for consumers, farmers, and the food system.

I. Introduction

A powerful cabal of food and agribusiness companies has a stranglehold on the food system from seed to supermarket. These oligopolistic firms control every link in the food chain— farm inputs, commodity processing, food manufacturing, distribution, and grocery retail, separating America’s 2 million farmers from its more than 310 million eaters. These companies exert their considerable market power to the detriment of consumers and farmers and endanger the resiliency of the food system.

Consolidation has enabled companies to impose significant price concessions on farmers and consumers. Only a few companies sell seeds, tractors, and fertilizer; and a few others buy corn, cattle, and carrots. For years, this economic concentration has eroded the share farmers receive from the dollars that consumers spend on food. 1 Increasing agricultural consolidation has contributed to the current precarious economic viability of independent farmers. Steeply declining farm prices are projected to drive 2017 net farm income 50% below 2013 earnings to some of the lowest levels in two decades. 2

The increasing consolidation of the food supply also directly impacts consumers in the form of reduced consumer choices and higher grocery prices. Consumers are vulnerable to the concentrated market power of food companies that sell essential staples; aggregate consumer demand for food is largely unresponsive to price, so consumers will still buy food when food monopolists impose price hikes. According to the American Antitrust Institute, the concentration in buyers, processing, and retailing has “undoubtedly contributed to the increased cost of food.” 3

The steadily rising price of food has significantly outpaced the growth in household earnings. Since the Great Recession took hold in 2008, real consumer food prices have risen about three times faster than typical wages. 4 The concentrated agribusiness and food industries have capitalized on the spread between declining farmgate prices and rising food prices, and the difference ends up in corporate coffers. 5 The biggest food, beverage, and grocery retailers pocketed $75 billion in profits in 2016. 6

But already high and increasing levels of economic concentration in the agricultural and food sectors impact far more than consumer and farmer prices. Consolidation has substantially curtailed the choices available to consumers and farmers. Grocery stores now teem with an illusory cornucopia of different products, but the vast majority of the supermarket items are manufactured by a few firms with dominant market positions.

Horizontal and vertical concentration in the agriculture sector has constrained farmers’ choices and autonomy. Concentration in the seed and fertilizer industries has significantly limited farmers’ cultivation options. Perhaps more importantly, the larger, vertically integrated agribusinesses have pushed farmers to increase the size, scale, and intensity of their farms in order to sell their crops or livestock and maintain economic viability. This limits farmers’ options and autonomy to control production decisions on their farms.

Concentration can also reduce quality and compromise safety. According to the U.S. Department of Agriculture (USDA), high concentration levels allow the largest companies to extract more economic value from food purchases, but “consumers typically bear the burden, paying higher prices for goods of lower quality.” 7 The substantial scale combined with highly concentrated chokepoints make the food system vulnerable to potentially larger, more widespread food safety problems.

The scale of plants in a heavily consolidated industry means that a single problem in one larger plant can now impact the entire food chain. In 2011, Cargill voluntarily recalled more than 36 million pounds of ground turkey after an illness outbreak caused by antibiotic-resistant salmonella. 8 The recall represented several months’ worth of production from a single plant in Arkansas in an industry where the top four firms processed 55% of turkey meat. 9 In total, 136 people across thirty-four states were infected, causing thirty-seven hospitalizations and one death, disproportionately caused by the bacteria’s resistance to antibiotics. 10

Food safety problems at even modestly sized suppliers can infiltrate a significant portion of the food system, when ingredients pass through the highly consolidated food processing sector. In 2007, the Food and Drug Administration (FDA) received reports of 17,000 pet illnesses, including 4,000 dog and cat deaths, believed to be the result of melamine contamination in imported Chinese gluten ingredients used to make pet food. 11 Sixty million packages of over 150 brands of pet food were recalled in the United States, the largest recall in history—and all the pet food originated from one Kansas facility that had used the contaminated wheat gluten. 12

A year later, the problem of consolidation and chokepoints struck the human food supply. A 2008 peanut butter salmonella outbreak led to nine deaths and more than 700 illnesses in forty-seven states. 13 The problem began at a single company’s filthy plants that manufactured 3% of peanut products—but the company’s peanut ingredients passed through a highly consolidated food industry, leading to a recall of over 3,600 products. 14

The corporate control of farmers’ production practices contrasts with the growing consumer demand to know where their food is from and how it was produced. The important questions consumers ask about the food system are fundamentally related to economic power and equity. Food and agribusiness consolidation has hindered access to locally grown, organic, sustainable, and equitable food in a marketplace that rewards only scale but not innovation. In recent years, mainstream food processing companies have snapped up organic and natural food brands, sometimes even concealing the corporate ownership on the labels to prevent rejection by loyal customers.

There is also a growing consensus that consolidation has contributed to widening economic inequality in America. 15 At its most simplistic, monopolies can impose higher prices on consumers, eroding their incomes. 16 Dominant monopolies drive smaller rivals out of business and make it harder for new businesses to gain root, harming not only entrepreneurs but also their workers. 17 Entrenched and dominant firms are also more likely to extract economic value for investors rather than lowering prices or raising wages or benefits. 18

This economic consolidation can widely erode the vibrancy of rural economies. In a comprehensive study of concentration in the pork processing industry, Food & Water Watch found that as the four-firm pork packer concentration doubled between 1982 and 2007, the economic value of Iowa hogs fell and the number of hog farms fell by 80% (even as the number of hogs sold in the state doubled). 19 The impact was felt well beyond the farmgate. The counties with the highest number of hogs had rising income inequality (with a growing gap between per capita and median incomes) and a declining number of small businesses, even though the number of small businesses increased overall in Iowa. 20

The merger-driven consolidation throughout the food supply has amplified the market power of a handful of companies that disadvantage consumers by raising prices and constraining choices. Section II describes the scale of the problem from the current nearly unprecedented wave of food mega-mergers. Section III explores the detrimental consumer impact of the rapidly consolidating grocery retail industry. Section IV analyzes several food industry merger trends that have facilitated different aspects of market power—horizontal mergers that raise prices and reduce choices in the pork sector; mergers that maintained dominant vertical power in the beer industry; mega-manufacturing mergers between large and diversified food conglomerates; and the conventional food industry takeover spree in the natural, organic, and good-for-you sector.

II. Consolidation and Recent Merger Wave in the Food System

The agriculture and food industry has been considerably more consolidated than most other industries for years, and many economists maintain that higher concentration levels can erode competitiveness. 21 In most sectors, the four largest firms typically control between 40% and 45% of the market, yet the top four firms in many food and agriculture subsectors have more than 60% market share. The four largest companies control 89% of margarine, 22 85% of beef packing, 23 78% of potato chips, 24 75% of peanut butter, 25 74% of frozen pizza, 26 71% of pork packing, 27 and 64% of wheat flour milling. 28

Much of the current high levels of concentration has been driven by decades of mergers, acquisitions, and takeovers, but a new wave of mega-mergers threatens to hyperconsolidate the food and agriculture industry. Prior to the Great Recession, there were about 400 food company mergers per year in both 2006 and 2007. 29 The recession dampened merger activity, but as the economy recovered, a rush of even bigger mergers swept the food and agribusiness industry. There were about 600 food and beverage mergers a year in 2015 and 2016 worth a combined $176 billion—50% more deals than before the downturn. 30

The postrecession merger surge was driven by a confluence of economic and marketing headwinds that have challenged even the biggest brands. Agribusiness firms—led by the seed companies—are combining to withstand and capitalize on the decline in crop prices and the farm economy. 31 The biggest food manufacturing companies face sagging demand, sales, and profits for processed foods, and large-scale, strategic mergers are an attempt to cut costs and revitalize traditional brand portfolios. 32 Grocery retailers have been merging to expand their geographic footprint, strengthen their position within their territories, as well as fortify their position to compete with alternative formats (including drug store chains and online retailers like Amazon). 33

Many of the recent record-breaking deals have supercharged consolidation in the manufacturing, food retailing, and agribusiness industries. The $36 billion Kraft-Heinz marriage in 2015 was the biggest food manufacturing deal of all time and created the third-largest U.S. food company. 34 The 2015 $108 billion Anheuser-Busch InBev–SABMiller beer merger was the biggest beverage deal of all time. 35 The 2015 $10 billion combination of two European grocery giants, Ahold (Giant) and Delhaize (Food Lion), was the biggest supermarket deal ever, larger than the Albertsons-Safeway deal of 2014, then the biggest. 36

Three simultaneous seed and agrichemical company mergers would consolidate an already substantially concentrated industry into an effective duopoly. 37 In 2015 and 2016, ChemChina-Syngenta, Dow Chemical–DuPont, and Bayer-Monsanto all announced deals to combine. These deals would reduce the big six seed companies to a bigger four, and the largest two, Dow-DuPont and Bayer-Monsanto, would control about 70% of the global seed market. 38 The even more highly concentrated seed industry would have further incentive to raise prices and reduce innovation; farmers would have little choice but to pay more. 39 These mergers would likely reduce the cultivation choices for farmers as combining companies pare their seed portfolio options. 40 On top of the seed mergers, the Canadian fertilizer giants Potash Corp. and Agrium Inc. announced a $26 billion deal in late 2016 that would create a company that would control one-third of the nitrogen and phosphate fertilizer production in North America. 41

The current wave of merger mania is showing no signs of abating. One Chicago Tribune business columnist described the current takeover environment as the “multibillion-dollar merger-crazy packaged food business.” 42 An analyst with Mergermarket predicted that the number and value of food mergers would rise in 2017. 43 Each merger can have tremendous ripple effects across the food chain. Mergers in one segment can justify reverberating mergers up and down the agribusiness, food manufacturing, and retailing sectors.

Ultimately, the combination of mergers along the supply chain creates a series of dominant players that each use their economic leverage to extract value from the food system. Take the humble breakfast cereal. Over the past few years, a series of mergers (or pending mergers) has consolidated the market power in every link of the breakfast cereal food chain. The pending seed, agrichemical, and fertilizer mergers would raise prices for farmers who produce the oats, wheat, and corn that are made into cereal. These raw commodities are sold to agribusiness companies for processing. In 2014, ConAgra and Cargill formed a $4 billion joint venture that milled one-third of the nation’s wheat flour, a key ingredient in manufacturing breakfast cereals. 44 In 2015, Post Holdings became the third largest cereal manufacturer with 18% of the market after its $1.2 billion takeover of MOM Brands. 45 These breakfast cereals are sold by supermarket chains that are rapidly consolidating as a result of the Albertsons-Safeway, Ahold-Delhaize, and other grocery store mergers. These cascading mergers concentrate market power all along the food chain, disadvantaging farmers and consumers.

III. Supersizing the Supermarket Erodes Consumer Choice

Supermarket mergers have transformed the grocery store. When there are fewer grocery retailers competing for shoppers, consumers pay more. Decades of academic literature have repeatedly found that more concentrated retail grocery markets raise consumer food prices. 46 A USDA research economist concluded that “the overwhelming consensus is that prices rise—and, in general, supermarkets set prices less competitively—as concentration increases.” 47 The biggest chains effectively limit where consumers shop but also what they can buy, since larger chains typically prefer to buy their grocery inventory from the largest food manufacturers rather than a larger number of smaller (independent) processors.

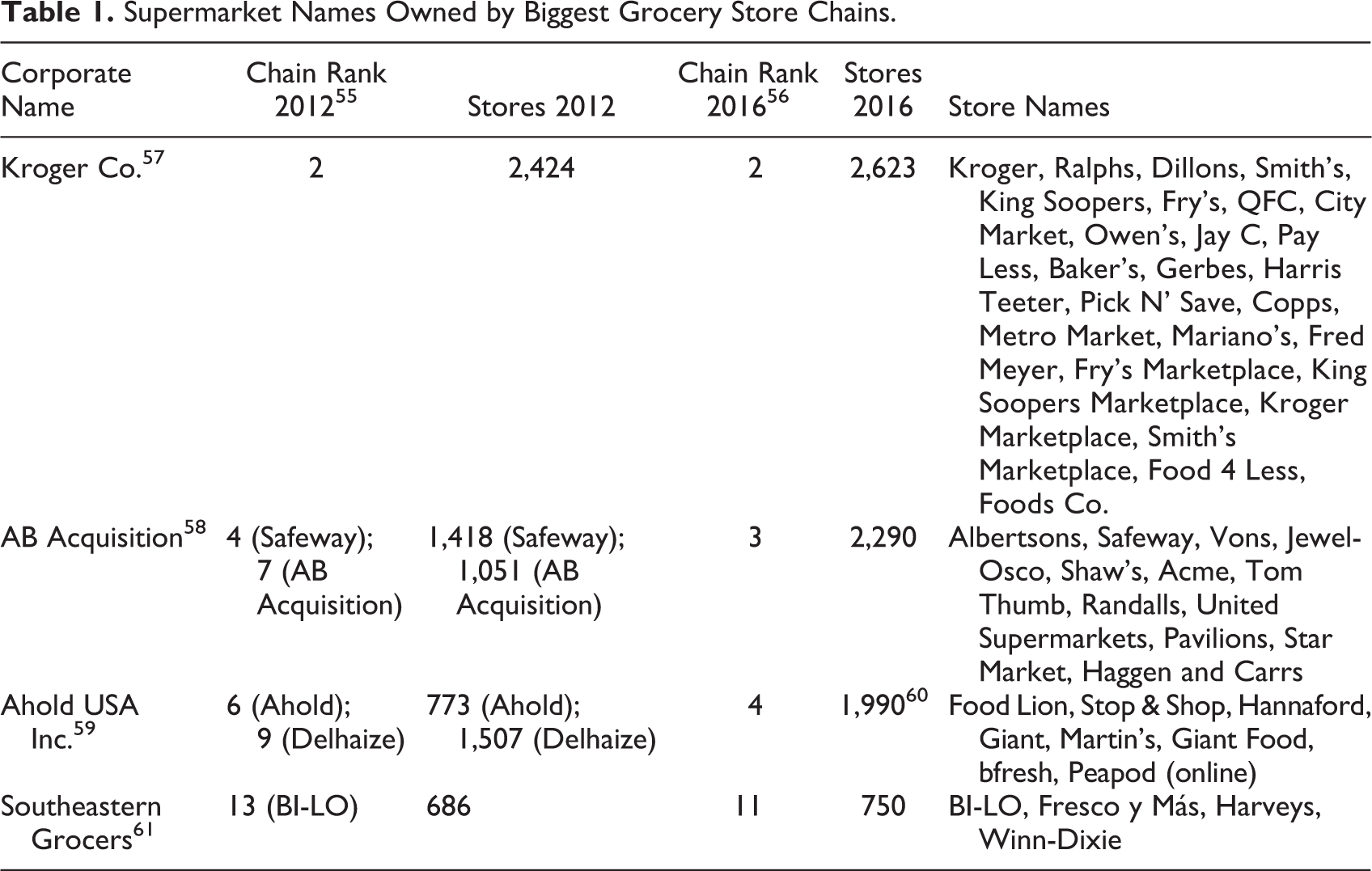

The grocery industry consolidated fairly recently. Even in the mid-1990s, the top four supermarket chains sold only about one-fifth of groceries (19.9%). 48 But the rise of big box stores selling food and mergers between regional supermarket chains rapidly consolidated the industry over the last two decades. 49 Since the end of the Great Recession, the largest wave of mergers in history has swept the supermarket industry, combining large chains that had already swallowed a host of regional stores that still display the old regional banner names (see Table 1).

Supermarket Names Owned by Biggest Grocery Store Chains.

The second largest grocery retailer, Kroger, purchased Harris Teeter in 2014 and Roundy’s in 2015, adding nearly 200 stores. 50 The third largest grocery retailer, AB Acquisition, was bulked up by a merger between Albertsons and Safeway in 2015 that joined 2,230 stores in thirty-four states. 51 In 2016, it bought twenty-nine Haggen stores in the Pacific Northwest that it had previously sold to satisfy Federal Trade Commission (FTC) regulators (Haggen went into bankruptcy after buying stores divested during the Albertsons-Safeway merger). 52 The fourth-largest grocery retailer was created in 2016 by the 1,970-store merger approved between Ahold (Giant and Stop & Shop) and Delhaize (Food Lion and Hanneford). 53 Bi-Lo (now Southeastern Grocers) purchased the 688-store Winn-Dixie chain in 2012; 22 Piggly Wiggly stores in 2013; and more than 150 Sweetbay, Harveys, and Reids stores from Delhaize in 2014. 54

This supermarket merger mania has significantly consolidated the national grocery retail industry over the past five years. The top four firms (Walmart, Kroger, Target, and Safeway) sold 54.9% of the groceries in 2012, but after the Ahold-Delhaize merger closed in 2016, the four largest (Walmart, Kroger, AB Acquisition, and Ahold-Delhaize) sold 61.7%. 62 Walmart alone sold more than one-fourth (27.2%) of the nation’s groceries, but despite the big box chain’s rapid expansion, its grocery market share from 2012 to 2016 has remained constant as the rest of the supermarket chains got larger through mergers and acquisitions. In 2017, online giant Amazon bought the dominant natural foods grocery retailer Whole Foods, bringing another powerful retailer into an already consolidated market. 63

Consolidation can be considerably higher at the local level. In 230 metropolitan areas, the four largest retailers sold more than 80% of the groceries in 2011, and Walmart made up half of all grocery sales in thirty-six cities. 64 Highly concentrated local markets have spread rapidly across the country. In 2004, the top four retailers controlled more than 90% of grocery sales in thirty-two metropolitan areas, but by 2011, there were fifty-nine markets with four-firm concentration of over 90%. 65

A. Merger Mania Reduces (and Obscures) Store Choice and Raises Food Prices

Retailers compete head-to-head in local, not national, markets, and the higher levels of local concentration can increase food prices and reduce grocery product selection and store choice. 66 Shoppers now have a diminishing choice of grocery stores as the biggest firms snap up local chains and drive others out of business. 67 Through a series of mergers, Kroger now operates stores under more than twenty different names including Harris Teeter, Mariano’s, King Soopers, Dillons, and others. 68 Shoppers are likely unaware that their local supermarket is owned by a national or even foreign grocery store chain, like the Netherlands’ Ahold chain’s Giant, Food Lion and Hannaford stores. 69

The increased national, metropolitan, and local concentration can take a bite out of shoppers. Most consumers shop at the closest store, so nearby stores have an advantage over more distant retailers. 70 Each supermarket has a nearly captive market of local consumers who incur travel and time costs to get to less convenient rivals, creating a sort of localized, one-stop-shopping monopoly. 71

In concentrated markets, the more powerful grocery chains can impose price hikes on consumers who have few other geographically practical options. 72 Retail market power allows supermarkets to charge consumers considerably more than it costs to put groceries on store shelves, and provides little incentive to pass price discounts on to consumers if they have few local competitors. 73 Price increases on specific grocery items merely induce most consumers to switch to a cheaper product in the same store, and because the large retailers can absorb these pricing shifts, they have an “inherent source of pricing power.” 74

Higher levels of concentration make it simple for competitors to tacitly collude to eliminate price competition. 75 Local supermarkets mimic each other’s pricing strategies, making it nearly impossible for consumers to comparison shop since a small number of retailers can price their foods at about the same level. 76 The widespread parallel pricing of purported competitors is exacerbated by mergers that reduce the number of rivals. 77

B. Grocery Concentration Reduces Product Options in the Supermarket Aisle

The growing size and market power of the top grocery retailers has had tremendous ripple effects across the food chain and constrained consumer choices. The increased buyer power of supermarket chains has contributed to the concentration in the food processing industry and a dramatic erosion of product choice on supermarket shelves. The grocery giants’ bulk purchases drive food manufacturing companies to merge and get bigger (see Section IV), which reduces the number of food processors filling supermarket shelves, further eroding consumer choice and raising prices.

Big retailers require large volumes of groceries to stock their shelves, and only the largest manufacturers have the capacity to meet these demands. But the biggest grocery retailers have substantial leverage over manufacturers, which can ultimately constrain consumer choice. Food manufacturers are dependent on the largest retailers, which often account for the bulk of their sales. 78

Retailer pressure on suppliers affects the variety of products in supermarket aisles. Retailers control the shelf space, they can promote store private label brands that compete with manufacturers’ brands, and they control the in-store advertising and display promotions. 79 To further cut costs, some retailers require that suppliers manage their own inventory. 80 Retailers often use exclusive purchasing agreements, long-term partnerships, and strategic alliances with manufacturers and suppliers to negotiate lower costs. 81

These factors disadvantage smaller, innovative food companies that are unable to meet the contract requirements or purchasing needs of larger retailers. Retailers also frequently mirror one another’s grocery product offerings, meaning that consumer choices are often constrained even between supermarkets. 82 Finally, two common retailer marketing strategies reinforce the partnership between the largest grocery chains and biggest manufacturers.

1. Promotional allowances and category management

Some retailers charge food companies a fee (known as slotting fees, slotting allowances or promotional allowances) to place their products in the most profitable locations in the store. 83 These charges are especially prevalent for the introduction of new grocery products and can run over $2 million for each new variety or brand. 84 These payments totaled $16 billion in 2000, the most recent aggregate national figure available (about $22.6 billion in today’s dollars). 85 The fees are likely still common and large. For example, between 2014 and 2015, Kroger alone charged manufacturers’ fees that amounted to about $7 billion annually. 86 Only the biggest manufacturers can pay these hefty fees, which keeps smaller food companies from getting onto store shelves. The FTC found that smaller suppliers believed they were “being squeezed off shelves” and that bigger companies “will pay large amounts of money to keep everyone else out.” 87

Grocery retailers and manufacturers have a symbiotic in-store strategy for marketing and inventory management that ensures that only the biggest food companies can get their products into supermarkets. Some supermarket chains have allowed key manufacturers (known as “category captains”) to determine which products are stocked on store shelves. 88 The category captain is typically a manufacturing leader in a specific grocery aisle or item (like one of the soda companies for beverages). The supermarket lets the company choose which items are available in an entire section of the store, determine the placement of brands and varieties, as well as set prices and promotions that support the products. Many retailers rely on this arrangement with manufacturers as the primary tool to manage supermarket shelf space. 89

Category captains obviously have little incentive to allow new competitors on supermarket shelves, and they can limit consumers’ choices and increase prices. 90 In 2013, an independent ice cream manufacturer sued Nestlé for allegedly leveraging its category captaincy to relegate all but the largest companies like Nestlé (including Häagan-Dazs and Dreyer’s) and Unilever (owner of Ben & Jerry’s, Breyers, and Klondike) to a tiny portion of the ice cream aisle. 91

IV. Mergers Between Food Mega-Manufacturers Constrain Consumer Choices

Rapid consolidation enabled the food manufacturing industry to corral lucrative grocery sales into fewer, larger corporate coffers. Consumers spent $649 billion on groceries in 2015—about 8% more than they spent in 2012. 92 Major food companies have pursued aggressive acquisition strategies to redouble their position in core business lines and to expand their product portfolios by snapping up new brands. The goal is to secure one of the top three positions in key grocery product lines. 93

The combination of retailer demands on suppliers and consolidation in the food manufacturing industry has significantly constrained consumer choices in the supermarket. Many food processing firms justify their own mergers as an effort to strengthen their bargaining position with large retailers. 94 Even large suppliers merge operations to consolidate their bargaining power with large retail buyers, and smaller food processors and manufacturers may exit the industry after determining they cannot bargain effectively to get fair prices from dominant buyers. 95 Mergers in the food manufacturing sector have already consolidated some of the largest food processing companies. 96

The resulting supermarket landscape is perilously deceptive for consumers. The recent wave of mergers gives fewer firms more market power, not just within product lines but throughout the supermarket. Consumers face illusory choices in the grocery store aisles—there are a seemingly endless number of product choices, but they are sold by a diminishing number of food companies.

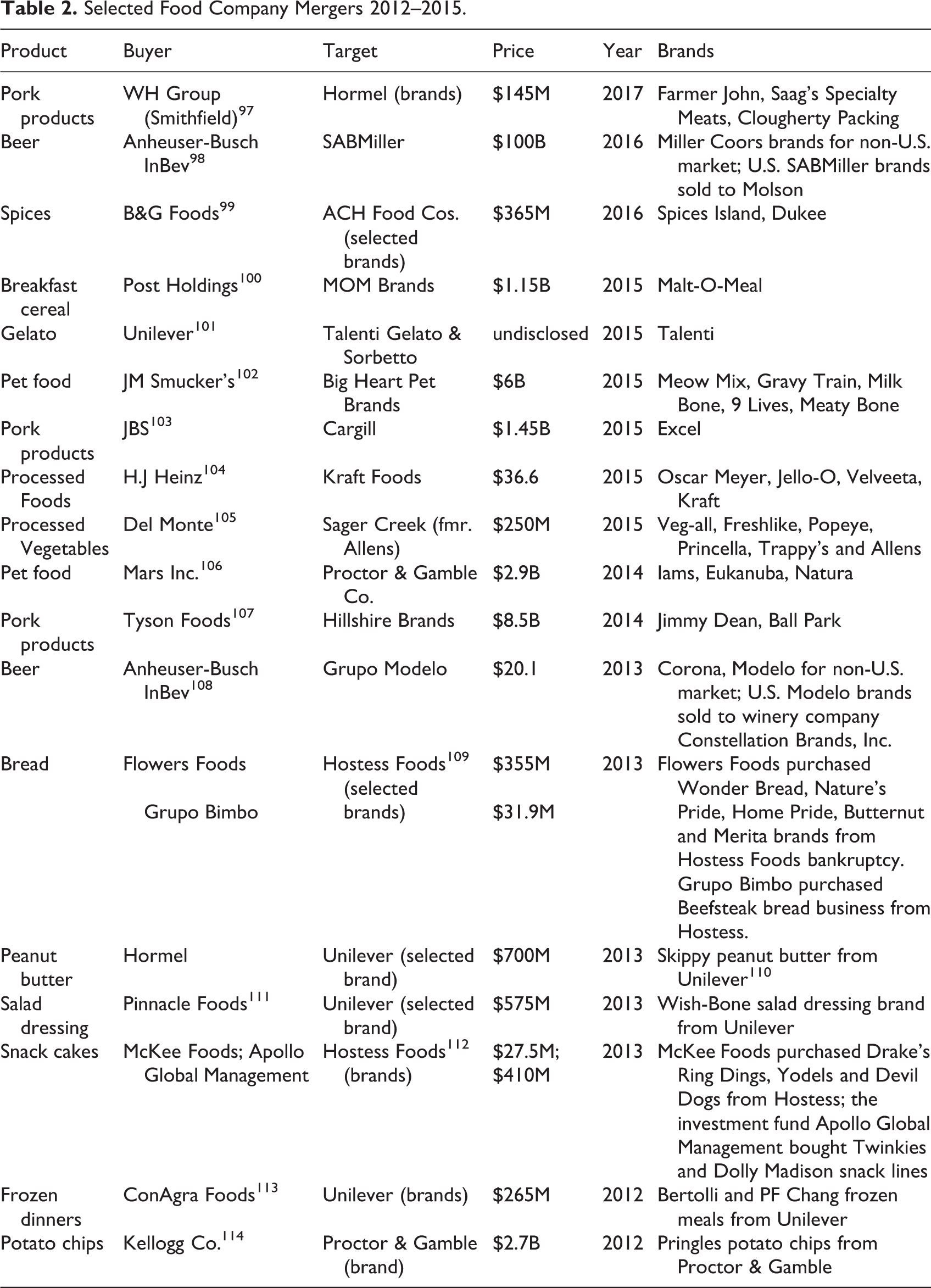

The merger wave has included significant horizontal mergers in the same market (like pork products), horizontal mergers that cemented vertical distribution power (like beer), and a host of conglomerate mergers that strengthened the reach of major food companies into more and more types of grocery products (most notably the Heinz-Kraft deal). Some companies have seized valuable brands in new segments to extend their reach—like Hormel’s $700 million purchase of Skippy peanut butter in 2013 and Kellogg’s $2.7 billion acquisition of Pringles potato chips in 2012 (see Table 2).

Selected Food Company Mergers 2012–2015.

A 2013 Food & Water Watch study found that the top few companies dominated the sales of 100 common grocery product categories. 115 The top four or fewer companies controlled an average of 63.3% of the sales these grocery products—in a third of grocery products, the top few companies controlled at least 75% of the market.

By 2015 or 2016, many of the categories had become even more concentrated. The four-firm concentration ratio rose in only a few years, including for chocolate (rising from 80.8% in 2011 to 86.8% in 2015 116 ), breakfast cereal (from 79.9% in 2011 to 85.0% in 2016 117 ), coffee (from 63.8% in 2012 to 67.5% in 2016 118 ), potato chips (from 75.7% in 2011 to 78.0% in 2016 119 ), peanut butter (from 71.6% in 2012 to 75.0% in 2016 120 ), and soup (from 67.5% in 2011 to 68.5% in 2016 121 ).

The multiple acquisition strategy has facilitated a range of techniques to exert market power over consumers. These manufacturers heavily market highly processed sugar- and salt-laden convenience foods as opposed to more nutritious options, because processed foods are bigger moneymakers. 122 Consumers have fewer genuine choices between which company made the food or whether it is a good choice in terms of price or quality.

A. Horizontal Mergers Extend Market Power That Erodes Consumer Choice

Consolidation in the food industry means that many firms sell multiple brands of the same basic products, like pork or margarine, which leads consumers to believe that they are choosing among competitors when they are actually just choosing between products made by the same firm and that may even have been manufactured at the same factory. Many food companies also manufacture generic private label (supermarket brand) products, further complicating the choices consumers face in the store. Consumers may believe they are selecting between rival food products based on price and quality, but they are often choosing between brands made by the same company. Recent mergers are only making these choices more opaque and confusing.

For example, Pinnacle Foods was the number two frozen fish manufacturer, selling both Van de Kamps and Mrs. Paul’s brands that controlled 25% of the market in 2016. 123 The two largest margarine firms sell a host of brands that dominate a very concentrated market. In 2015, Unilever controlled 58% of the market and ConAgra controlled 19%. 124 But these two firms sell a range of brands at a wide variety of price points. Unilever sells I Can’t Believe It’s Not Butter!, Shedd’s Country Crock, Imperial, Promise, and Brummel & Brown; 125 and ConAgra Foods sells Blue Bonnet, Parkay, and Fleishmann’s. 126 The prices range widely, from about $1 per package to over $3 per package. 127

Since 2014, three major mergers have further consolidated an already very concentrated industry. For most of the decade between 2003 and 2012, the four-firm concentration level for pork packing had hovered at about 64% or 65%. 128 But after Tyson Foods purchased Hillshire Farms in 2014, JBS bought Cargill’s Excel pork packing segment in 2016, and Smithfield purchased Hormel’s Clougherty Packing in 2017, the four biggest firms now control 72% of the market—a significant jump in only a few years. 129

This concentration means that hog farmers are selling into a more concentrated market, contributing to the long-term decline in the real prices farmers receive for hogs. And not only does it make it harder for consumers to know which company they are buying from, it can reduce quality. According to the USDA, the low-cost pork produced from large-scale hog operations, where the animals are bred to gain weight quickly, “may not have the flavor or texture some buyers seek.” 130

Although consumers seemingly have a wide variety of options at the meat counter, many large meatpackers sell a range of ostensibly rival or independent brands. Since the 1990s, Smithfield absorbed multiple competitors including major pork packers John Morrell and Farmland. 131 These mergers have multiplied Smithfield’s brand portfolio to include Smithfield, Farmland, John Morrell, Gwaltney, Armour, Eckrich, Margherita, Carando, Kretschmar, Cook’s, Curly’s, Healthy Ones, Saag’s Specialty Meats, and Farmer John. 132 Importantly, Smithfield and its multitude of brands are now owned by the Chinese firm the WH Group, making it significantly harder for consumers who want to buy American.

The Tyson-Hillshire Farms merger joined Tyson’s substantial hog slaughter capacity (about 17% of the market without Hillshire’s slaughter plant 133 ) with Hillshire’s popular value-added pork brands. At the time of the merger, Hillshire was the number one breakfast meat company and Tyson ranked fourth. 134 The merger joined Tyson’s brands (Tyson, “Day Starts” frozen breakfast lines, and Wright brand sausage and pork products) with Hillshire’s many pork product brands (Jimmy Dean sausage, Ball Park hot dogs, State Fair corn dogs, Hillshire Farms and Sara Lee lunchmeat, Gallo salami, Aidell’s sausage, Kahn’s hot dogs and lunchmeat, Bryan hot dogs and sausage, Rudy’s Farm sausage, and Briar Street Market lunchmeat and sausage). 135

Tyson and Smithfield’s strategy of multiple brands and labels obscures the consolidation in the meat case and makes it hard—or impossible—for consumers to see the dramatic structural changes that have taken place in the pork industry over the last three decades.

B. Brewery Mega-Merger Threatens Independent Craft Brewers and Limits Choice

The beer industry appears to offer a wide variety of choices with many independent craft brewers offering a range of options for consumers. But the reality is that the biggest beer companies determine whether or not smaller brands get onto store shelves and a series of mega-mergers over the past few years (including craft brewer takeovers) has cemented the dominance of the two largest brewery companies.

AB InBev (better known in the United States as Anheuser-Busch) and Molson Coors control about 70% of the U.S. beer market. 136 To put this in comparison, the thousands of independent craft brewers sold about 11% of beer in 2015. 137 These two companies own hundreds of brands, including Budweiser, Bud Light, Miller, Corona, Becks, Stella Artois, Coors, Michelob, Fosters, and many, many others. 138 In 2016, AB InBev bought SAB Miller, keeping the Miller brands internationally but spinning off the U.S. brands to Molson Coors Brewing. 139 This followed AB InBev’s takeover of Grupo Modelo’s global brands after selling off the rights to sell Corona and Modelo to winemaker Constellation Brands in 2013. 140 For American beer drinkers, these mergers merely rearranged the ownership of the dominant breweries, but the beer duopoly remained firmly entrenched.

The big brewers have pursued an “if you can’t beat ‘em, buy ‘em” strategy. In 2015, the four largest brewers bought nineteen craft brands for $13 billion. 141 After AB InBev announced its merger with SAB Miller, it purchased Golden Road, Four Peaks, Breckenridge, and Devil’s Backbone on top of the Goose Island, Ten Barrel, Elysian, and Virtue Cider craft brands it had previously bought. 142 When they do not buy brands, the biggest brewers can tie up raw supplies that independent brewers need, like aluminum cans and hops, driving up their upstart rivals’ costs. 143

Oftentimes, the ownership of import or craft beers is impossible for consumers to discern. In 2015, AB InBev settled a $20 million class action lawsuit for brewing Beck’s beer in Missouri but promoting the brand’s German heritage dating to 1873 while concealing its domestic production. 144

The biggest brewers have long been squeezing the rising craft brewers out of the market through vertical distribution arrangements that made it hard for independent firms to get into stores. 145 At a Senate hearing on the AB InBev-SAB Miller merger, the president of the National Beer Wholesalers Association noted that the biggest brewers could “exert pressure on independent distributors not to carry rival brands and on retailers to design their shelves to disfavor or remove rival brands.” 146

In 2012, AB InBev encouraged distributorships to merge to become the company’s anchor distributor—and provided financial support to sweeten the recommendation. 147 It also rewarded distributors that sidelined craft beers. In 2015, distributors that sold 98% Anheuser Busch brands were eligible for up to $1.5 million in rebates if they did not deliver some popular craft beers. 148 As the president of Dogfish Head brewery observed, “The success or failure of a beer should depend on how great that beer is…instead of artificial restraints to distribution.” 149

In 2015, the Justice Department launched a probe into AB InBev’s alleged anticompetitive distribution practices that made it hard for craft beers to get into the market. 150 Despite the investigation, the company successfully lobbied for an exemption to an Oklahoma law in 2016 that barred breweries from owning distribution operations, allowing the company to maintain its distribution centers in Tulsa and Oklahoma City. 151

Despite the widespread concerns with AB InBev’s anticompetitive meddling in beer distribution, the Justice Department approved the AB InBev–SABMiller merger with conditions. AB InBev was prohibited from buying additional craft beer brands without the Justice Department’s preapproval, and it was banned from providing financial incentives to discourage distributors from supplying rival craft beers. 152 The deal allowed AB InBev to continue owning many wholesale distributors. 153 But this “behavioral remedy” relies on the Justice Department to police AB InBev to ensure that the company does not use its market muscle to discourage distributors from carrying craft beers. 154 Independent brewers doubted that the conditions could ensure that they get their beers on store shelves. Pennsylvania-based independent brewer Yuengling said the approved merger was “one of the biggest threats to [the company’s] existence,” second only to a return to Prohibition. 155

C. Mega-Mergers Amplify Power of Food Conglomerates

Food manufacturing consolidation has created a handful of conglomerates that sell a range of products across the supermarket. Federal antitrust regulators largely turn a blind eye to mergers between companies that are not head-to-head competitors in very specific products. 156 This allows food processing companies to add to their product range through unfettered mergers and acquisitions as long as they are buying firms (or brands) that do not sell exactly the same products. These conglomerate mergers can disadvantage consumers as the biggest firms fortify their market power and are able to conceal their ownership of a broader product range through a multiplicity of brands.

Food conglomerates have been spreading their product tentacles across the entire grocery store.

In 2013, Food & Water Watch found that the six largest food conglomerates sold at least thirteen different kinds of grocery products (known as categories). 157 Prior to the Kraft-Heinz mega-merger, Kraft sold twenty-two varieties of groceries. It dominated macaroni and cheese, processed cheese, lunchmeat, and mayonnaise (79.0%, 48.3%, 34.8%, and 33.9% of sales, respectively). But Kraft also sold coffee, condiments, other dairy products, frozen cakes and pies, snack nuts, and more. Eight Kraft brands had annual sales over $1 billion in 2014. 158 Heinz sold seven kinds of grocery products, most notably ketchup, but also prepared meals and pasta sauce.

In 2015, the two companies merged their $29 billion in sales and created the third-largest U.S. food company (behind PepsiCo. and Nestlé) and the fifth largest globally. 159 The Washington Post called the deal a “household-name powerhouse.” 160 The merger joined a fleet of iconic brands. The deal joined Kraft’s Oscar Meyer, Philadelphia Cream Cheese, Kool-Aid, Jell-O, Velveeta, Lunchables, Planters nuts, and Maxwell House coffee with Heinz ketchup and vinegars, Ore-Ida potatoes, Weight Watchers meals, and Classico pasta sauce. 161 Kraft Heinz now owns more than fifty different families of brands, most of which have multiple varieties of products. 162

Although the merger joined two broad portfolios of grocery products, the companies produced almost no brands that were direct rivals. Before the merger, the two firms overlapped in a single category—meat sauces. Heinz’ Lea & Perrins Worcestershire and Heinz 57 sauce controlled 24% of the market, and Kraft’s A-1 brand steak sauce controlled 11%. 163

Mergers between firms that do not sell identical food products still give big food processing companies more economic power and leverage over other companies and consumers. The Kraft-Heinz deal created a bigger food conglomerate that expanded its footprint and power in the supermarket, reducing consumer choice and likely increasing prices. 164 Smaller, innovative food companies may find it harder to get on grocery store shelves because Kraft-Heinz has them surrounded on all sides. And bigger supermarket chains are more likely to source more of their inventory from a conglomerate like Kraft-Heinz that can supply products throughout the store than from many companies that only supply a few products.

Mergers between food conglomerates create more dominant product portfolios and advertising power that can disadvantage consumers. Companies with powerful brands can use their strong parent brand name to enter new categories or product classes—for example, a new Kraft food item. 165 Furthermore, conglomerates can offer new varieties of existing brands (such as new flavors) that squeeze competitors off of store shelves (known as product or brand extension). The Kraft-Heinz merger was designed to leverage iconic brands in a strategy the companies called “fewer, bigger, better” that aims to modify existing brands. 166

Food companies with broad portfolios of iconic brands exercise unique unilateral market power over rivals throughout the supermarket. Mergers between firms with multiple strong brands (like Kraft and Heinz) effectively create a firm where the combined market power is greater than the sum of the brand power of the individual firms. 167 Large portfolios give manufacturers greater flexibility to set product prices and cross-subsidize weaker brands, increasing profits across the product lines. 168

Bigger food conglomerates exercise unilateral market power through their product portfolio itself—the seemingly broad range of goods (products or variations) appeals to both shoppers and supermarkets seeking variety. 169 Consumers associate positive brand attributes of one segment or category with that brand’s products in related or complementary categories, strengthening the company’s position across the supermarket. 170 This portfolio effect essentially increases the demand for all the company’s offerings while reducing the demand for rivals’ products. 171 This allows firms with broad brand portfolios to build market share and market power. 172

Even when companies do not directly compete in any one product line, food conglomerate mergers can join firms that sell complementary products that can distort the market. Complementary product combinations strengthen both brands. These mega-mergers make it easier to promote both brands together, increasing the control that just one company has over a bigger piece of that grocery aisle. 173 One corporate antitrust lawyer recognized this opportunity in the Kraft-Heinz merger noting that “Heinz mustard on Oscar Mayer hot dogs would be a nice complementary product line.” 174

Promotions of complementary products strengthens brand equity and can increase product profits. 175 This coordinated marketing can increase consumer demand for both complementary products. 176 The conglomerates also have a better chance of introducing new products through brand or product extensions. 177 Bigger firms with stronger brands have lower marketing and advertising costs, which improves the odds of introducing new products successfully. 178

Even as Kraft-Heinz is implementing a drastic cost-cutting regime (it had 7,800 fewer employees in 2017 than before the merger 179 ), it is aiming to expand its supermarket footprint even further through future acquisitions. 180 In late 2016, there were rumors that Kraft Heinz would buy Mondelēz or make a hostile takeover bid for General Mills. 181 In 2017, Kraft Heinz made a $143 billion bid for Unilever, which was withdrawn after it was rebuffed. 182

These food conglomerates already have a sprawling empire in the grocery store. The biggest food companies operate across product lines and over dozens of iconic brands, and consumers are often unaware which brand families are owned by which companies. Although these conglomerate mergers have little overlapping product competition, they nonetheless fortify the market power of the biggest food companies, and further mega-mergers will only consolidate economic power, worsen consumer confusion, and limit consumer choice.

D. Consumers Vulnerable When Big Food Companies Buy Up Organic, Natural Brands

Consolidation has even started to inundate the organic and natural food sectors, which had long provided the primary alternative to the processed food monopoly. Consumers are increasingly interested in knowing what is in their food, where it comes from, and how it was made. They want fewer, more natural ingredients and more information about the foods they put on their families’ plates. A Nestlé official succinctly noted that “consumers are reacting to things like artificial. They want more naturals.” 183

For decades, consumers found these once-niche food products at co-op markets, health food stores, and organic grocery stores. The organic, natural, and healthy food innovators have long struggled to get onto traditional supermarket shelves. They could not deliver sufficient quantities or accept the often unfairly low prices the biggest retailers offered. The natural food companies that survived and flourished have become takeover targets for the largest food manufacturers, reinforcing their entrenched market power. 184

There are two coalescing trends accelerating the current merger wave swamping the organic, healthy, and natural food segment: stagnant processed food sales and soaring natural food revenues. The processed food manufacturing giants have struggled to maintain sales of the hyperprocessed, artificial ingredient-laden traditional brands. 185 One Wall Street analyst observed that “consumer packaged goods companies are desperate to find ways to grow, and they are not seeing any growth with their products internally.” 186

But natural, organic, and better-for-you food sales have been growing three times faster than conventional foods.

187

One corporate response has been to make conventional manufactured food seem less processed. Major food companies are dropping artificial colors and flavors and introducing new products with more natural ingredients and “cleaner” labels designed to appeal to consumers’ changing tastes.

188

Companies like General Mills, Kellogg’s, and Cargill also now sell organic products.

189

But conventional food manufacturers have also aggressively pursued acquisitions to vacuum up the alternative and innovative food brands that consumers crave. The Chicago Tribune explained the motivation: Large, traditional food companies are gobbling up smaller, nimbler firms already established in the coveted realm of food considered to be natural, organic and healthy. The authentic product stories and trusted brands that resonate with health-focused consumers often are easier to buy than to create in a lab.

190

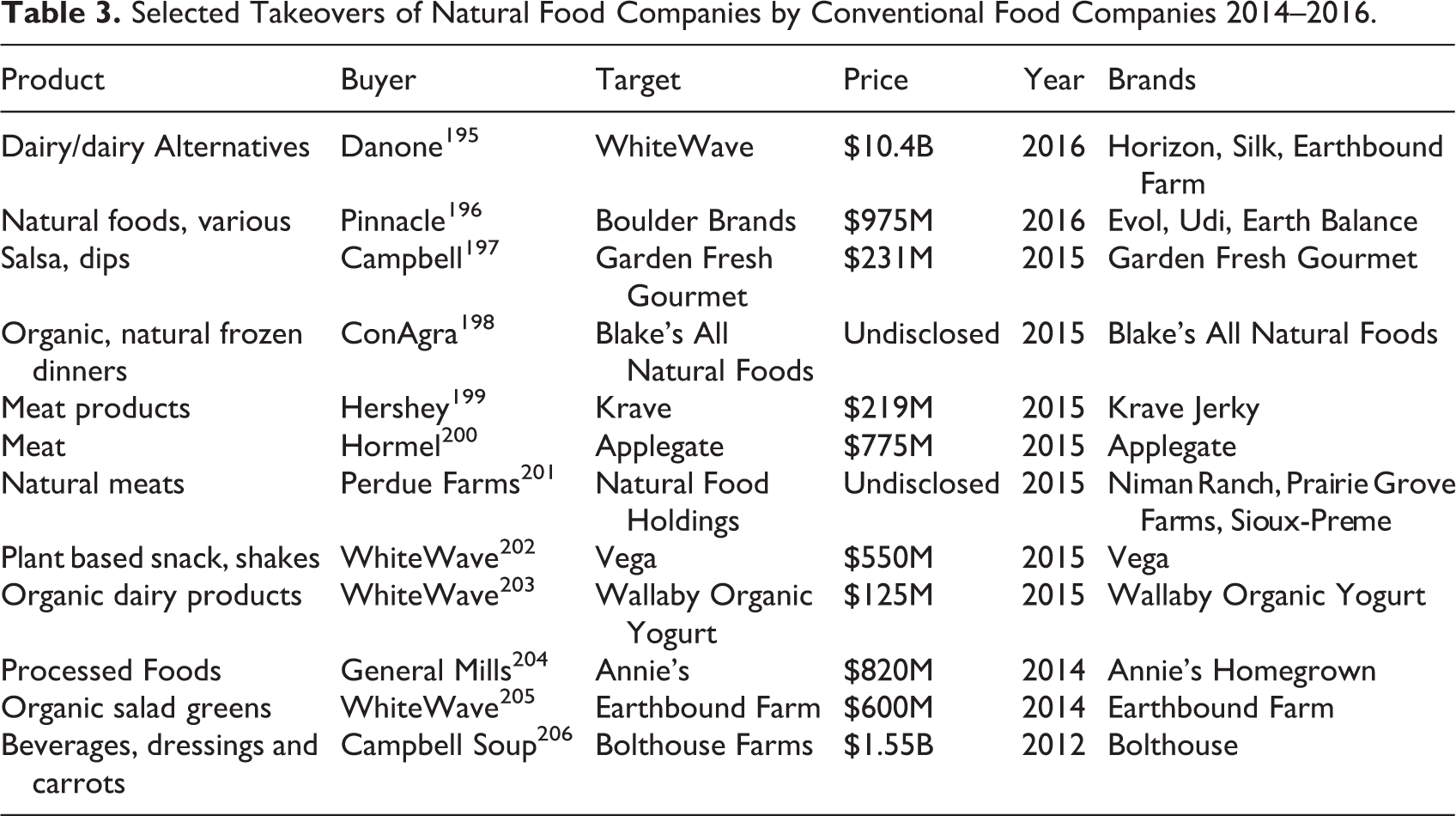

Selected Takeovers of Natural Food Companies by Conventional Food Companies 2014–2016.

Consumers can easily get lost in the shuffle when the biggest food companies buy up independent food companies that have built a loyal following. Conventional food manufacturers may not maintain the same commitment to the ideals of the organic or natural food innovators and may even weaken the company’s commitment to using wholesome ingredients. 207 The “mission and culture tend to get quickly lost in the sales and marketing machine of big food companies,” according to a recent New York Times opinion piece. 208

For example, after the biggest dairy processing company, Dean Foods, bought the WhiteWave company, 209 it subtly changed its dominant Silk organic soymilk brand. WhiteWave was motivated to sell its organic firm to a conventional dairy company to expand its sales. 210 But in 2009, Dean began selling Silk soymilk made with non-genetically engineered soybeans instead of soybeans that are certified organic, a more rigorous designation. 211 Although Dean changed its ingredient list and removed the word organic from the label, it kept the same blue Silk packaging and the same universal product code so most consumers and retailers did not know the difference. 212

WhiteWave has now been taken over by a second big food manufacturer. WhiteWave became independent again in 2013 after it was spun off by Dean, 213 and subsequently went on an organic takeover spree. It spent nearly $1.3 billion buying organic leafy greens firm Earthbound Farms, organic dairy firm Wallaby Yogurt, and the plant-based snacks and nutritional drinks company Vega (see Table 3). In 2016, the European food manufacturer Danone bought WhiteWave along with its newly expanded stable of organic brands. 214

The deal would have created a dominant organic yogurt manufacturer controlling Danone’s Stonyfield as well as WhiteWave’s Wallaby and Horizon brands with an estimated two-thirds of the U.S. organic yogurt market. 215 In 2017, the Justice Department approved the deal with the divestment of the Stonyfield brand. 216 Whether this maintains competition in organic yogurt will greatly depend on which company buys Stonyfield.

The same could happen to Niman Ranch meats. Niman Ranch was founded to produce humanely, sustainably raised livestock and protect farmers from unfair treatment by the largest meatpackers and poultry processors. 217 By 2016, more than 600 hog farmers sustainably raised free-range Niman-branded hogs that sell for premium prices. 218 The quality of the meat and narrative of the Niman brand got its products into some of America’s most prestigious restaurants. 219 Niman founder Bill Niman worried, however, that Perdue could weaken the brand’s standards without consumers understanding because “these bigger outfits have a lot of marketing power, and they’re able to spin things and create confusion in the marketplace.” 220

Consumers may not know that the seemingly independent organic, natural, and healthful brands are being bought up by large food companies. And consumers may not be able to figure it out by reading the labels, which often do not reflect the corporate ownership. For example, Kashi and Bear Naked are both Kellogg brands, but Kellogg’s ownership is concealed from consumers—the Kashi and Bear Naked labels make them seem independent, their brand websites barely reveal a relationship with Kellogg’s, and only Kellogg’s government filings clearly reveal that the company owns the brands. 221

Big Food’s takeover of venerated organic brands can have more direct consequences. Some of the largest food companies with organic brands have generously funded opposition to state ballot initiatives to label food with genetically modified ingredients (GMOs). In 2012, Kellogg (Kashi) donating $600,000, Coca-Cola (Odwalla and Honest Tea) donated over $1 million, and General Mills (Cascadian Farms and Muir Glen) donated over $900,000 to defeat California’s GMO labeling initiative, which incited a backlash by loyal consumers of their organic brands. 222 In 2013, the Grocery Manufacturers Association (GMA) trade association created a fund to oppose GMO labeling efforts designed to “shield individual companies from public disclosure and possible criticism” that opposed Washington State’s GMO labeling initiative and was funded by a host of big food companies with organic brands. 223 In 2016, GMA was fined $18 million for intentionally violating Washington’s campaign finance disclosure laws for concealing donors. 224

And the largest food processing companies have worked to weaken the rules governing organic food. Giant traditional food manufacturers and agribusinesses with valuable organic lines (like General Mills, Campbell’s Soup, Earthbound Farms, Whole Foods, and Driscoll Strawberry Associates) have had company representatives on the USDA advisory board that establishes the standards for organic farming and food manufacturing, and between 2002 and 2012 the number of approved nonorganic substances allowed in organic food tripled to over 250. 225 In 2013, the organic advisory board moved to eliminate the five-year sunset review of permissible nonorganic substances and instead require a vote to remove synthetic substances—something that would make it harder to remove nonorganic substances from the permissible list. 226

V. Concluding Thoughts on Food Mega-Mergers

The resurgent and unprecedented wave of food mega-mergers over the past five years has rapidly consolidated the entire food system. In large part, this is because of lackluster antitrust enforcement during the Obama administration. By most metrics, the Obama Justice Department and FTC took an only slightly tougher line than the historically indifferent Bush administration. 227

On food and agriculture mergers, the administration filed a single suit to enjoin a merger (the foodservice merger to monopoly between Sysco and USFoods 228 ). The Obama administration approved most deals were with few—or no—strings attached, like minor behavioral conditions on the AB InBev merger or the unconditional approval of the Kraft-Heinz deal. Some required divestitures that did not succeed, like Albertson’s sale to Haggen to get the Safeway merger approved before buying the stores back when Haggen went into bankruptcy. 229

Antitrust enforcement is unlikely to be stepped up. The Trump administration’s economic and antitrust advisors and appointees are largely sympathetic to mergers and economic consolidation. 230 An antitrust partner at Skadden, Arps, Slate, Meagher & Flom wrote that there would likely be “some tempering of the level of activity that characterized the Obama administration, particularly with respect to merger challenges.” 231 The merger wave is likely to continue with little letup in coming years. At a 2017 conference for corporate dealmakers, the JPMorgan mergers and acquisitions chairman predicted more mergers and even $100 billion all-cash takeover offers in the coming years. 232

The combination of more mergers with weaker antitrust enforcement leaves consumers more vulnerable to consolidation in the food system. It is past time for Congress and antitrust regulators to return to the spirit of the antitrust statutes and not merely a technocratic and narrow interpretation of the law—that would include more vigorous enforcement of mergers that reinforce vertical market power, conglomerate mergers that reinforce disadvantageous market power, and examining mergers more clearly in the context of the current highly consolidated landscape.

The food and agribusiness industry is capitalizing on the current low-cost environment with crashing farm prices, declining energy costs, and stagnant wages by aggressively consolidating every link of the food chain. Farmers are paying more for inputs like seeds and fertilizer but receiving less for their crops and livestock. Consumers will face this merger mania in the local supermarket, with fewer and less transparent food choices and likely higher prices.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.