Abstract

Corporations are facing a growing demand for the transparency of political contributions. In the United States, this demand has largely focused on the implementation of a mandatory disclosure law. It rests on the assumption that legal enforcement can make it easier to observe the ties between corporations and political parties. In this study, I challenge this assumption. I build my case by first developing a conceptual foundation of corporate political transparency (CPT). I argue that in the absence of economic benefits, legal enforcement has a limited effect on CPT. Instead of encouraging transparency, mandatory disclosure can lead to the concealment of corporate political contributions. To develop a model of concealment, I borrow the characterizations of disguise from theatrical drama. Using the context of Indian firms, I show the limitation of mandatory disclosure and the efficacy of regulatory incentive. My study highlights the need for a broader debate on CPT to understand the relative implications of regulatory policies.

Keywords

Although the discussion of corporate political transparency (CPT) has received significant attention from the various stakeholders, it has received limited scholarly response. In fact, the concept of CPT remains to be formally introduced to the academic literature. In this study, I fill this gap by formalizing the concept of CPT and by illustrating how corporations disguise their political contributions to evade transparency. My findings illustrate the interplay of regulatory policies and corporate political disguise that underpins CPT.

Political transparency refers to the “ease with which the public can monitor the government with respect to its commitments” (Broz, 2002, p. 861). More recently, the demand for political transparency has become increasingly associated with corporations who are expected to fully disclose their “influence on elections and legislation” (Levey & Geiger, 2011). This emphasis on CPT reflects the concern of a growing nexus between corporations and elected officials (Levitt, 2010). The proponents of this nexus argue that corporations should not be restricted from political expression. Campaign contributions function as a mechanism for firms to support individuals and parties that are closely aligned with their views (Atkins, 2013; Bebchuk & Jackson, 2010; Sitkoff, 2002; Teachout, 2011). Their opponents have argued that corporate political expression, and in particular, its manifestation as corporate political contribution (CPC), distorts the economic field (Vogel, 1996). CPC leads to a more favorable environment for contributors at the cost of firms that are politically inert (Alzola, 2013; Blau, Brough, & Thomas, 2013; Kwong, 2015). At the heart of this argument is the question of observability (Bebchuk & Jackson, 2013). This argument of observability has evolved into a strong and a weak form with respect to corporate political ties.

The strong form of the argument pertains to the benefits accrued by corporations (Hillman, Keim, & Schuler, 2004), and where possible, by the politicians (Djankov, La Porta, Lopez-de-Silanes, & Shleifer, 2010). It posits a clear link between campaign contributions and the reciprocal benefits (Hill, Kelly, Lockhart, & Van Ness, 2013; Roberts, 1990; Tesler & Malone, 2008). Although some studies have suggested that politicians can get biased toward the contributors (Ansolabehere, De Figueiredo, & Snyder, 2003; De Figueiredo & Garrett, 2004; Großer, Reuben, & Tymula, 2013), there is limited evidence of a close association between CPC and firm performance (Aggarwal, Meschke, & Wang, 2012; Bebchuk & Jackson, 2010; Coates, 2012; Hadani & Schuler, 2013). Although this discussion remains an active field of academic research, the failure to observe the impact of corporate political ties has shifted the social momentum toward a greater emphasis on the weak form of the argument for observability. It has led to the expectation that at the very least, corporations should be legally required to fully disclose their political contributions (Bebchuk & Jackson, 2013; Earley & Vandewalker, 2013). Mandatory disclosure can allow stakeholders to make more informed choices (Winik, 2010). It may also help uncover more specific instances of political bias that are otherwise diffused among the general trends (Whitmore, 2012). Even though this demand for CPT has received significant attention from a number of stakeholder groups (The Conference Board, 2012; Earley & Vandewalker, 2013), it is largely absent from analytical discourse that is the cornerstone of academic research (Garrett & Smith, 2005). Thus, it remains to be understood whether the threat of punishment, or a mandatory disclosure law, is sufficient for CPT or whether it may need to be complemented by a reward, such as an economic incentive that offers tax rebates or other benefits, to ensure effective compliance (Besley & Case, 2003; Doshi, Dowell, & Toffel, 2013).

I answer this question by building a conceptual foundation of CPT by focusing on recent developments in the United States. These developments have largely focused on the enactment of a mandatory disclosure law. I then focus on the limitations of a mandatory disclosure law by examining how corporations disguise their political contributions and circumvent legal constraints. To this end, I borrow the characterizations of disguise from theatrical drama to illustrate three different forms of disguise and test them in the context of Indian firms. Given that Indian firms have gone through a regime that initially focused on legal enforcement and was later complemented by a regulatory incentive, it offers a valuable setting to test my arguments. It is particularly salient to this discussion as despite institutional differences, the U.S. and the Indian political environments “share the goal of timely and accurate disclosure of [political] campaigns’ financial activities,” which is central to CPT (Weintraub & Brown, 2012, p. 241). I use this setting to empirically examine the effect of mandatory disclosure on CPT in the absence, and subsequently, in the presence of regulatory incentive. I find that a regulatory policy focused purely on legal enforcement has a limited effect, and economic incentive plays a stronger role in CPT. My study makes two contributions. First, I introduce the concept of CPT and show that the existing debate can benefit by recognizing the role of regulatory incentive. Second, I illustrate the approaches adopted by firms to evade transparency. They offer insights into how an understanding of corporate political disguise can facilitate the development of an effective policy for CPT.

Theoretical Development

CPT captures the idea that firms ought to fully disclose their material political ties to the stakeholders. Although political ties can be built around both monetary as well as non-monetary contributions, with the latter including a variety of personal and professional interactions that occur behind the scenes, my focus in this study is limited to the former (i.e., monetary contributions). The two biggest challenges in understanding CPT include the definition of an effective disclosure (i.e., what type of political contributions should be disclosed?), which I tie to the weak form of observability, and the identification of corporate political activities with material consequences (i.e., what benefits do firms receive in return for their contribution?), which I associate with the strong form of observability (The Conference Board, 2012, p. 18). Most scholarly research has focused on the strong form of observability by examining political actions that yield favorable outcomes (Blau et al., 2013; Hillman et al., 2004; Holburn & Vanden Bergh, 2014; Li, He, Lan, & Yiu, 2012; Ozer & Alakent, 2013; Sun, Mellahi, & Wright, 2012; Zardkoohi, 1985). However, the findings have failed to clearly identify a nexus between corporations and political parties (Aggarwal et al., 2012; Hadani & Schuler, 2013). To the extent that there may be a connection, the scholarship in law as well as in management has highlighted the potential of agency costs (Coates, 2012; Hadani, Dahan, & Doh, 2015; Hadani & Schuler, 2013). At best, CPC may offer no benefits to the firm, but at worst, political contributions can harm shareholder interests by decreasing firm performance and diverting resources, including managerial attention, to non-productive avenues (Bebchuk & Jackson, 2010; Sobel & Graefe-Anderson, 2014). This makes the weak form of observability necessary for effective governance.

To safeguard stakeholder interests, policy makers generally rely on two broad classes of instruments that help influence social and economic behavior (Berliner & Prakash, 2015; Delmas, Montes-Sancho, & Shimshack, 2010; Hess, 2007; Karp & Gaulding, 1995; Kolstad, 1986; Newell & Stavins, 2003). The first instrument focuses on legal enforcement and it is commonly viewed as the command-and-control approach. Mandatory disclosure falls into this category. It focuses on the threat of penalty and encourages compliance by highlighting the legal consequences of deviance. 1 A second instrument relies on offering economic benefits and it functions as the market-based approach. Regulatory incentive falls into this category. The focus in this case is on motivational conformity, generally through the use of financial rewards such as tax rebates or subsidies. 2 The command-and-control and market-based approaches are independent. That is, the two instruments can be used in isolation and if implemented jointly, the order of introduction is not critical.

Among the two instruments, mandatory disclosure is the obvious choice. The threat of legal penalty is widely accepted as a strong reason for effective compliance, and hence, transparency (Doshi et al., 2013; Mobus, 2005). Moreover, legal enforcement can function as an official reminder for firms to avoid an undue influence on the political process (Vogel, 1996). But at the same time, it is not difficult to imagine that firms may prefer to limit the disclosure of their political ties to maintain social legitimacy (Kim & Lyon, 2014; Laufer, 2003; Lyon & Maxwell, 2011). Transparency evasion can include approaches that help disguise political contributions, and where possible, portray them in forms that are more acceptable to the society (Tesler & Malone, 2008). This potential of political disguise suggests that regulatory incentive can be a more powerful instrument than mandatory disclosure. It can expose firms to a choice between future political benefits for secrecy vis-à-vis immediate guaranteed returns for transparency. Thus, an understanding of CPT requires an evaluation of the extent to which mandatory disclosure or regulatory incentive can be effective in limiting corporate political disguise.

I first discuss how mandatory disclosure is viewed as an instrument of choice for CPT in the United States. Following that, I develop a model of corporate political disguise to understand how firms can avoid CPT. I then test my model of political disguise in the Indian context to understand the effect of mandatory disclosure in the absence, and subsequently, in the presence of regulatory incentive to assess the relative efficacy of the two instruments. 3 Although an ideal test would have been to observe the effect of each instrument in isolation. However, I was unable to find a national setting where this has been the case (e.g., see Norris & van Es, 2016).

The Case for CPT

CPT has become an active social concern. In part, the expectation of corporate political disclosure has become stronger since the U.S. Supreme Court abolished the upper limit on CPCs. 3 It has led to a growing concern that corporations may now be freer to gain an undue influence over the political process. These concerns have been raised by several stakeholder groups including members of the civil society, investors, the Securities and Exchange Commission (SEC), politicians, and to some extent, members of the academia.

The most vocal critique of CPC has been the general public. Their demand for CPT stems from the concern that the democratic process may be violated by corporate political influence (Alzola, 2013; Anastasiadis, 2014; Vogel, 1996). The possibility of violation is not limited to only one side of the equation: the corporation. Public distrust also pertains to biased political responses (Großer et al., 2013; Kapur & Vaishnav, 2011). Political representatives are viewed to be increasingly concerned about their own interests. Although it is no surprise that corporations prioritize their economic returns over the general welfare of the society (Gordon & Hafer, 2005; Keim & Zeithaml, 1986), the wider availability of information has made it evident that the political machinery is also focused on self-preservation. This can be seen from the following example:

[T]he publicly traded CCA and GEO [two dominant players in the private prison industry] also have made national headlines in recent months because of safety and security problems in some of the prisons they operate . . . According to OpenSecrets.org, which tracks campaign giving and lobbying influence, CCA and GEO have contributed a combined $20.9 million to federal candidates in the last decade. (Beyerlein & Bischoff, 2011)

Beyond public distrust, such reports have escalated the demand for political transparency, and in particular, for the disclosure of all forms of CPC. In conjunction, the demand for CPT is now also echoed by the shareholders. Once the proponents of CPC (Torres-Spelliscy & Fogel, 2011), they have started to question campaign contributions given the lack of substantive evidence regarding the strong form of observability. Individual as well as institutional investors have become increasingly concerned that campaign contributions may be shaped by managerial interests. Rather than the corporation, it appears to be the executives who gain the most out of corporate political relationships (Aggarwal et al., 2012; Bebchuk & Jackson, 2010; Coates, 2012; Hadani & Schuler, 2013). As Public Citizen, a non-profit organization focused on public advocacy, explains,

Corporate political spending requires particular investor protections because it exposes investors to significant new risks. Investors have a right to know what candidates or issues their investments are going to support or oppose. (Corporate Reform Coalition, 2015)

One important measure of investor concern is the number of shareholder proposals seeking political transparency. According to the Conference Board, there were 430 shareholder proposals between 2010 and 2014 (110 in the year 2014) seeking the disclosure of corporate political spending. It stood as the “single most frequently submitted and voted proposal type across all subject categories” (The Conference Board, 2016).

The growing pressure by investors and the general public led the SEC to take interest in examining the enforcement of CPT through a mandatory disclosure law. In this vein, a group of former SEC officials also wrote to the current chairman that “mandatory disclosure of corporate political activities should be a ‘slam dunk’ for the Commission” (Ballhaus, 2015). It may have contributed to the SEC seeking public comments on petition 4-637, which required “public companies to disclose to shareholders the use of corporate resources for political activities.” 4

Interestingly, a fourth group that has become skeptical of CPC includes the politicians themselves. They have argued that unless the nexus between corporations and politicians is made visible to the public, a few contributors can become extremely influential. Deep pockets may start dictating the choices that emanate from the political process. In one such letter to the SEC, 14 U.S. senators wrote,

[W]e urge the SEC to use its rulemaking authority to issue rules that would require corporations to disclose their political spending to shareholders. The disclosures should include spending on independent expenditures, electioneering communications and donations to outside groups for political purposes, i.e., Super PACs. (Whitehouse, 2012)

Even President Obama joined into this discussion. Using the term “dark money” to refer to the lack of transparency in CPC, he recently stated that “[w]ith each new campaign season, this dark money floods our airwaves with more and more political ads that pull our politics into the gutter. It’s time to reverse this trend” (Gilbert, 2015).

The academic community has not been completely absent from this discussion. In fact, it was a team of law professors who initiated the rulemaking petition 4-637 to SEC requesting the need to enforce the disclosure of CPCs (Bebchuk & Jackson, 2013). They identified that in addition to the social and the economic costs, the absence of corporate political disclosure makes it difficult to establish any evidence of the strong form of observability. The information reported by the recipients (political parties) or the third parties (lobbyists, super political action committees [PACs], and others) offer limited insights into the nature of corporate political influence. They stated,

Disclosure of corporate political spending is necessary not only because shareholders are interested in receiving such information, but also because such information is necessary for corporate accountability and oversight mechanisms to work. (Committee on Disclosure of Corporate Political Spending Petition for Rulemaking, 2011)

Another academic initiative has been the Center for Political Accountability (CPA). The center has developed the CPA–Zicklin Index that functions as a scorecard to rank the leading S&P firms on their policies and disclosures regarding political activities. 5 But despite these initiatives, the scholarly discourse has failed to offer much in terms of empirical insights. Consistent with the broader consensus, researchers have echoed the view that mandatory disclosure is salient to CPT. This has strengthened the conclusion that a legally enforced requirement for the disclosure of political contributions can fully reveal the corporate influence in politics (Atkins, 2013; Bebchuk & Jackson, 2013; The Conference Board, 2012; Earley & Vandewalker, 2013). My focus in this study is to examine the validity of this assumption by investigating whether mandatory disclosure law is sufficient for CPT.

The Weak Form of Observability

An answer to the above question requires an empirical investigation of the weak form of observability. It suggests understanding the extent to which mandatory disclosure can be sufficient for CPC transparency. Yet, despite the apparent simplicity of this proposition, the expectation of sufficiency is difficult to establish in the scientific domain. This is because it cannot be falsified (Popper, 2002). If the implementation of a mandatory disclosure law leads to an increase in CPC, it does not establish sufficiency. It is difficult to ascertain the extent to which corporate political spending continues to be concealed. However, the opposite argument is falsifiable and it can form the basis of an effective empirical investigation. If I hypothesize that mandatory disclosure law fails to fully reveal CPC, then any evidence of a significant increase in CPC (after controlling for other effects) due to a subsequent event 6 can establish the limitation of legal enforcement. Such an investigation poses two major challenges. The first pertains to the nature of the shock that can provide a comparable motivation as legal enforcement, and the second challenge relates to the identification of mechanisms that can facilitate the lack of corporate disclosure. Both these challenges represent different sides of the argument for CPT. A failure of mandatory disclosure indicates the use of mechanisms that help conceal CPC, and the revelation of previously hidden political contribution suggests a strong motivation for disclosure. My interest in exposing mandatory disclosure to a subsequent shock leads me toward regulatory incentive as the focal instrument. That is, if regulatory incentive leads to a significant increase in CPC subsequent to the mandatory disclosure law, this can demonstrate the limitation of legal enforcement as well as of the current debate on CPT. However, a failure of regulatory incentive in increasing CPC can lead to two potential conclusions. The first possibility is that mandatory disclosure law is sufficient for CPT. The absence of any significant increase in CPC over and above the previous trend can substantiate that mandatory disclosure is highly effective and additional policy emphasis is unnecessary. This conclusion would empirically validate the currently accepted view of the command-and-control approach for CPT. A second possibility is that neither mandatory disclosure nor regulatory incentive is effective in the political domain. Both of these instruments fail to encourage corporations to reveal their political ties. This would suggest the need to search for non-regulatory options for CPT. In sum, a significant effect of regulatory incentive on CPC disclosure can establish the limitation of mandatory disclosure. However, the absence of a significant effect would point toward the need for further investigation to identify whether it is the success of mandatory disclosure or the failure of both instruments (i.e., legal and economic) that is responsible for the empirical result.

Corporate Political Disguise

A discussion of transparency requires us to understand the mechanisms that can help evade transparency. This, in turn, demands a theoretical model that can offer insights into how firms succeed in concealing their political contributions. Although such a model is currently lacking, the discussion of disguise is not new to organizational research. Several studies have identified that the visible face of a corporation may be inconsistent with the underlying aspirations. These studies can be separated into two theoretical perspectives: the institutional theory and the theory of corporate disclosure. Institutional theory illustrates how organizational choices can be influenced by external considerations (Scott, 2014). It recognizes that firms may sometimes maintain a disconnect between their formal face and the actual practices (Meyer & Rowan, 1977). This discussion portrays decoupling as a successful tactic that remains hidden from the external environment (Boxenbaum & Jonsson, 2008). Disguised actions are successfully concealed from investors and other stakeholders due to the difficulty of their observation by the external environment (Westphal & Zajac, 2001). However, decoupling is an inappropriate lens in the case of monetary expenditures. In particular, publicly traded firms are required to have their financial transactions endorsed by external auditors. Auditors’ access makes it necessary that practices that may otherwise be shielded from disclosure become visible. Successful concealment, therefore, requires such expenditures to be recorded in forms that cannot be associated with CPC. This raises the following question: If corporations conceal their political contributions from those that have sufficient access to internal processes, what forms of disguise do they deploy? Institutional theory is unable to answer this question.

The theory of corporate disclosure offers another perspective. It explains the implications of information asymmetries that arise from the lack of dissemination of critical information. They lead to lower investor confidence, a decrease in the price at which securities are bought to compensate for adverse selection, and consequently, diminished market value of the firm (Leuz & Wysocki, 2008; Simon, 1989). These implications can have economy-wide effects through misleading signals that, on one hand, make it difficult to have a clear assessment of the opportunities available in the market, and on the other hand, they can lead to ineffective and possibly harmful regulatory policies (Shleifer & Wolfenzon, 2002; Sidak, 2003). However, this stream of research also offers limited insights into how firms conceal their financial choices.

One area that offers valuable insights is theatrical drama. It offers a comprehensive characterization of the various approaches that can be enacted to evade transparency. In theatrical drama, disguise is an important mechanism of concealment, which is accomplished through obfuscation. That is, rather than avoiding disclosure, the focus is on disclosing choices but in a form that is symbolically or operationally non-representative of the focal activity. It encourages audiences to accept what is otherwise an act of non-compliance through misinterpretation. Even though external acceptance is largely an outcome of obfuscation, audiences’ difficulty to monitor each facet of an activity also plays some role in the successful enactment of a disguise.

Theatrical disguise is instrumented through two different elements of performance: intention and identity (Freeburg, 1915; Wendt, 1994). A basic form of disguise is the change in an actor’s intentions without a material change in his or her identity. The actor appears to be socially compliant but shields his or her true intentions which embody an alternative pursuit. This cognitive form of disguise is only evident by the disparity between actions and goals (Stuart & Wang, 2016). The unmasking of the cognitive disguise requires the actor to be exposed to a social or an economic dilemma where the alignment between intentions and actions becomes more beneficial. The actor is made to evaluate and subsequently select a course of action that eliminates internal inconsistency (Tilcsik, 2010).

Disguise can also combine the change in intention with a change in identity. It accentuates the effect of a cognitive disguise by combining it with physical distortion. Such changes in identity can be evoked in two different ways. The first involves actors’ substitution of their identity with another established identity (Bradbrook, 1981). It maintains the visibility of the otherwise undesirable actions by relabeling their functionality to attain social acceptability (Meyer & Scott, 1983, p. 46). In organizational research, this functional form of disguise has been found to manifest through the incorrect classification of corporate expenditures (Gramlich, McAnally, & Thomas, 2001; Sweeney, 1994). A second type of transformation is the structural disguise, which involves the introduction of a new persona that is so distinct from the existing identity that it circumvents the potential of inferential comparison (Baker, 1992). It leads to a “legitimacy façade that facilitates noncompliance” by maintaining a physical separation between the organization and its choices (MacLean & Behnam, 2010, p. 1515; Westphal & Graebner, 2010). One of the most common ways to enact a structural disguise is through boundary segregation—the use of a separate organization, which can serve as the public view of the corporations’ political practices (Hermalin & Weisbach, 2012; Mayer, 2012). Even though the separate organization may be subservient to the parent firm, it allows the potential to isolate specific choices from the corporate boundary. I discuss below how cognitive, functional, and structural disguise can help conceal corporate political ties. 7

Cognitive disguise

The cognitive disguise for CPC suggests that corporations may hide their true political intentions by failing to disclose campaign contributions. The enactment of this disguise can help evade the disclosure of political ties. Because cognitive disguise is dependent on the fulfillment of the underlying interests, it is easier to retain the disguise as long as the economic benefits are secured by the confidentiality of CPC. The disguise can allow corporations the freedom to convey their preferences to the politicians without any concern for social reprisal, and at the same time, the absence of a formal disclosure can make it easier for the politicians to return favors without the fear of public scrutiny. Thus, an absence of political transparency can be beneficial for the corporations as well as the politicians.

Mandatory disclosure laws are designed to curb this tendency. They impose legal penalties on the corporation for a failure to disclose material political contributions. Although they may lead to the transparency of some of the political contributions, the difficulty of identifying “materiality” makes it possible for the corporate-political nexus to be transformed into mechanisms that can transgress the legal constraint. For example, corporations can use their administrative budget to pay for politicians’ traveling expenses, “hire” politicians as technical consultants, or pay for campaign events by recording the associated expense as a public relations exercise (Kaiser, 2010; Pavarala, 1996). Although I later discuss two specific manifestations of the disguise, it is not difficult to see that mandatory disclosure may have a limited effect on CPT. Although the requirement for disclosure can succeed in making some of the contributions visible to the public, it is quite possible that corporations may use limited disclosure as a smokescreen to continue to conceal the underlying reality (Gowda & Sridharan, 2012; Kochanek, 1974; Neiheisel, 1994). Thus, instead of encouraging complete transparency, mandatory disclosure may induce the need to transform the corporate-political nexus into forms that can successfully evade the requirement of political transparency (Kapur & Vaishnav, 2011).

However, when mandatory disclosure is complemented by a regulatory incentive, it can discourage the enactment of a cognitive disguise. Competing economic benefits impose a calculus of comparative evaluation. Corporations are exposed to the choice of relying on political ties to secure future and somewhat uncertain economic opportunities or capitalize on the regulatory incentive for immediate returns. This trade-off is more favorable toward transparency because the present value of benefits is often more substantive for managerial wealth (Narayanan, 1985) and shareholder interests (Bushee, 2001), and it can also allow the corporation to eliminate internal practices, which make them vulnerable to potential social penalties (MacLean & Behnam, 2010). Although the discussion of CPT has largely focused on mandatory disclosure laws, I argue that it is the regulatory incentive that is likely to encourage greater compliance. In the absence of economic benefits, corporations will continue to disguise a significant portion of CPC, and this will only change in the presence of a regulatory incentive. Although corporations may not suddenly become fully transparent, it is likely that over time regulatory incentive can turn CPT into a viable alternative to concealment (Tilcsik, 2010). 8 The enactment of a cognitive disguise in the presence of mandatory disclosure but the subsequent revelation of this disguise in the face of economic benefits suggests that regulatory incentive can have a positive effect on CPC. The resulting increase in CPC would represent the disclosure of previously concealed political contributions reflecting greater political transparency. This potential trade-off between a cognitive disguise and the immediate economic benefit of disclosure leads us to predict the following:

Functional disguise

The discussion above focused on corporate intentions without discussing the physical manifestation of the disguise. Increase in CPC after regulatory incentive is only one part of the story. The other part relates to the avenues that can contribute toward CPT. In this vein, one may argue that the increase in CPC may not be a result of the revelation of disguised contributions but a reflection of greater corporate interest in improving political ties. That is, firms do not just disclose more of their contributions but actually increase their total political expenditures to benefit from the regulatory incentive. Although this possibility cannot be completely ruled out, it is unlikely to play a significant role. This is because corporations without existing political ties are unlikely to receive significant economic favors through newly established ties that are highly public (Kroszner & Stratmann, 2005; Leuz & Oberholzer-Gee, 2006). In fact, the visibility of CPCs can jeopardize the credibility of the associated politicians (Pavarala, 1996), making it difficult for them or the corporation to rapidly intensify an embryonic relationship. This is consistent with the work that suggests that established political ties are more effective than the ones that are newly set into place (Kroszner & Strahan, 2001; Kroszner & Stratmann, 2005). The credibility in this relationship is largely a function of the extent to which the corporation and the politician are aware of each other’s true intentions, which only happens over time. Moreover, a regulatory incentive does not diminish the need to evaluate CPC as an expense that affects the bottom line. It remains a cost that needs to be justified, possibly more so because of its contentious economic and social value (Coates, 2012; Hadani & Schuler, 2013). It therefore appears reasonable to speculate that a significant increase in CPC is likely to be more strongly representative of the elimination of some form of disguise that was previously enacted to shield political contributions (Gray, 1992). 9

Kim and Lyon (2014) used the term “greenwashing” to refer to the transformation of illicit practices into legitimate choices. They argue that firms are inclined to use socially acceptable choices to frame non-compliant practices (Berliner & Prakash, 2015; Laufer, 2003). I propose that such a practice may, to a large extent, be similar across firms and be observable for significant effects for two major reasons. First, corporations will be skeptical of greenwashing political contributions if they see others to be completely complaint, especially if the focal CPC is materially significant (Lim & Tsutsui, 2012). It can increase the vulnerability to exposure and to its possible negative consequences (Westphal & Zajac, 2001). In other words, corporations attempting to disguise political contributions will follow the practices of others to diminish the potential of legal reprisal. Although legitimate choices are generally found to diffuse rapidly among the population, the effect is not too different for choices that fail to become legitimate. Greve (2011) explained that “disappointing innovations do spread widely but temporarily” (p. 950). Because political disguise requires the enactment of a legitimate façade to cover illegitimate choices, it is likely that even when concealment practices are a common mechanism to balance political ties with social reputation, firms will continue to seek ways for a more legitimate solution. In that case, regulatory incentive can provide the necessary impetus.

A second major reason includes political exigency. Politicians often suggest the avenues of contributions, which are convenient to them, particularly because as public servants they are under significant legal and societal scrutiny (Kaiser, 2010; Kochanek, 1974). Their success in distancing themselves from any accusation of bias rests on the capacity for denial (Gowda & Sridharan, 2012). Consequently, a commonly used approach is for the concealed CPCs to be directed toward charitable organizations that are closely associated with focal politicians’ immediate or extended family. For instance, Tesler and Malone (2008) observed that “Philip Morris explicitly linked philanthropy to government affairs and used contributions as a lobbying tool against public health policies” (p. 2123). They further explained that the staff at Philip Morris tried to “secure invitations and support their [legislators’] philanthropic events and causes,” invited “legislators to Philip Morris–sponsored charitable events,” and the company “also made donations to favored causes of 3 governors’ spouses” (Tesler & Malone, 2008, p. 2127). More recently, Hadani and Coombes (2012) found that political contributions and philanthropy may be used as “complementary strategies” to deal with political uncertainty experienced by firms in their industrial environment. The charitable face of political activities can be a safer means to build social reputation. In turn, it helps attain greater legitimacy from the political environment. Thus, in addition to being a safe disguise for CPC, charity also provides corporations with a reason to claim higher social consciousness when negotiating political favors (Den Hond, Rehbein, de Bakker, & Lankveld, 2014; Milinski, Semmann, & Krambeck, 2002; Williams & Barrett, 2000).

But as regulatory incentive decreases the use of alternate outlets for political contribution, CPC disclosures are likely to diminish the need for a functional disguise. This suggests that an increase in CPC in the presence of a regulatory incentive will coincide with a decrease in the magnitude of charitable contributions. This does not imply that all the corporate charitable contributions are a cover for political connectedness. Instead, I argue that once economic benefits minimize the need to enact a functional disguise, we should find that the increase in CPC, to some extent, benefits from the revelation of funds that would have otherwise been disguised as charity. Larger the decrease in charitable contributions, higher would be the increase in revealed political contributions, and stronger will be the relationship between regulatory incentive and CPC. Thus, the possible use of a functional disguise leads us to speculate the following:

Structural disguise

Another effective form of disguise pertains to structural separation. In the context of political contributions, it is often more convenient for firms to use third parties to relay their contributions (Hermalin & Weisbach, 2012; Mayer, 2012). In their report on the “Transparency for Corporate Political Spending,” Earley and Vandewalker (2013) identified three major transparency loopholes that make it difficult to observe CPCs. They include shell corporations, trade associations, and social welfare organizations. Rather than exposing the corporation to functional misrepresentation, these loopholes offer structural obfuscation for CPC disbursement. Similar to the functional disguise, structural disguise allows a mechanism to conceal political ties (Garrett & Smith, 2005). But instead of misrepresentation, a structural disguise enables the possibility of complete denial. This is because even though third parties generally serve as a conduit and are subservient to the wishes of the donor organizations, they can be portrayed as independent entities whose political choices are completely autonomous (Szper & Prakash, 2010, p. 122; Torres-Spelliscy & Fogel, 2011). Consequently, material ties between third-party contributors and political parties help cushion the corporation as well as the politicians by facilitating the assertion of mutual independence (Geis, 1988; Moore, Tetlock, Tanlu, & Bazerman, 2006).

However, as regulatory incentives can make corporations more willing to reveal their political contributions, it is likely that firms reliant on third parties will disclose greater contributions. This suggests that corporations that relied on a structural disguise would reveal a larger increase in CPC corresponding to contributions that would have otherwise been concealed in the name of trade-related transactions, association dues, or other forms of inter-organizational transactions (Earley & Vandewalker, 2013). This increase in CPC will represent the magnitude of disclosures that become observable in the face of an economic benefit. As a result, subsequent to regulatory incentive, we should find a larger increase in CPC for firms associated with a third-party political contributor than for firms that make their political contributions directly. This can be stated as follows:

Data and Method

Empirical Setting

Given my focus on understanding the efficacy of regulatory incentive relative to mandatory disclosure, I needed a national context that had implemented both of these instruments. In this regard, India offered a valuable empirical setting for several reasons. First, Indian firms are required to disclose their political contributions in the annual reports. This mandatory requirement for disclosure came into effect in 1985 (Amended Companies Act of 1985, Section 293A). 10 However, subsequent social pressure for CPT led to the passage of the Election and Other Related Laws (Amendment) Act in September 2003, which allowed 100% tax deduction on contributions to political parties (for more details, see Gowda & Sridharan, 2012). Although Indian firms were earlier required to report their political contributions, it was only after 2003 that they were economically incentivized to do so whereby “any contribution made to a political party would be deductible from an Indian company’s gross total income” for tax purposes (Murlidharan, 2008). 11 Although it is unlikely that the regulatory incentive may have led to complete transparency. 12 I believe that the incentive is likely to have made it possible to observe at least some of the political contributions that were previously disguised. A second advantage of the Indian context was that charitable contributions are also part of the mandatory disclosure law. The availability of data on political and charitable contributions directly from the source eliminated the need to rely on alternate sources, which can be vulnerable to omission and truncation errors (Brown, 2011). And third, similar to most other emerging market economies, the link between firms and political parties has been relatively strong due to India’s historical dependence on centralized administrative policies (Stuart & Wang, 2016). This offered an important context to observe the effects that may be somewhat diffused in the other national environments.

Sample

I constructed my sample by using the introduction of regulatory incentive as the center point for my panel with an equal number of years prior to and subsequent to this point. At the time of this study, data were available until 2012, which gave me a period of 9 years after the implementation of the regulatory incentive (i.e., 2004-2012). I, therefore, chose the starting point of the sample as 1995 for a comparable period of 9 years prior to the change (i.e., 1995-2003). To collect the data on CPCs, I first studied the annual reports. Although most financial indicators are available from electronic data sets such as the Center of Monitoring Indian Economy’s Prowess, they do not record political contributions. Because it was impractical to collect and code the annual reports of all the publicly held companies in India, which at the time of this study counted to more than 20,000, I relied on a longitudinal sample of 18 years for a limited number of firms. I began with the random identification of 100 firms from the Bombay Stock Exchange. But after coding their political contributions, I realized that this approach was ineffective as only 13 of these 100 firms had at least one political contribution during the sample period. The remaining firms either did not report or did not make any political contribution. This lack of observable political activity eliminated the potential to analyze the implications of a regulatory change. A firm with no political contribution before or after the regulatory change cannot reveal the implications of mandatory disclosure or when the disclosure is combined with a regulatory incentive. Although it remains important to understand the reason underlying political inactivity, the question goes beyond the scope of this study. My intent was to examine whether a politically active firm revealed higher contributions in the face of regulatory incentive than in the past when it was only exposed to mandatory disclosure. This led me to an alternate sampling approach. I referred to the list of politically active firms identified by the Association for Democratic Reforms (ADR). ADR is a non-profit organization that is working toward political transparency in India. Based on the reports from political parties regarding campaign contributions, ADR has compiled the list of all contributors that made at least one political donation during the years 2004 and 2012. This list is, therefore, the Indian equivalent to the Federal Election Commission (FEC) reports commonly used in U.S.-based studies (Aggarwal et al., 2012; Chin, Hambrick, & Treviño, 2013; Hadani & Schuler, 2013). 13 The identified sample included a total of 109 firms. I followed this sample for the period 1995 to 2012. Because some of these firms were incorporated after 1995 or were either acquired or reorganized before the end of the sample period in 2012, my panel is unbalanced and it comprises of a total of 1,229 observations.

Measures

Dependent and independent variables

My measure for CPC includes all corporate donations to political parties made directly or through a third party. Third parties were identified from the ADR lists and they included politically active not-for-profit organizations. 14 I identified their corporate ties through the newspapers and annual reports. I operationalized third-party contributor as a binary variable, which is 1 for firms that used a third party to disburse political contributions and 0 otherwise. My measure for charitable contribution includes all philanthropic donations with “the object of promoting commerce, art, science, religion, charity or other useful object” excluding political donations (Amended Companies Act of 1985, Section 293B). To measure regulatory incentive, I coded the period 2004 and onwards with a binary value of 1 during which political contributions were tax deductible and 0 for the years 2003 and earlier when there was no regulatory incentive. Because the incentive was announced in September 2003 and the fiscal year for Indian firms ends in March 2004, it is possible that some of the escalation in political disclosures may have taken place in the base period (i.e., 2003). This makes the test of my argument more conservative by increasing the difficulty of demonstrating a significant effect. However, I also checked by shifting the anchor year from 2004 to 2003 and found the results to be substantively similar.

Control variables

I control for firm sales, return on assets (ROA), and age, which can lead to stronger political ties and, therefore, higher political contribution. Because firms may be historically predisposed to charity, I also test the model after including the lag of charitable contribution. Due to the strong correlation between charitable contribution, the moderator variable, and its lag, whether with a simple 1-year lag or with an average for the last 3 years of contribution, I operationalized the lag of charitable contribution as a weighted average of the last 3 years of charitable contribution. It is computed as (2 / 10 × charitable contributiont−1) + (3 / 10 × charitable contributiont−2) + (5/10 × charitable contributiont−3). It helped overcome the concern for multicollinearity. Previous studies have suggested that slack resources can increase the potential of political influence (Schuler, 1996). I control for this by incorporating unabsorbed slack, which is the ratio of cash and bank balance to current liabilities, and potential slack, which is the ratio of total debt to total equity subtracted from 1. I could not operationalize a third type of slack, absorbed slack, which is the ratio of selling, general and administrative expenses to total sales. This is because Indian firms do not share a standard for the reporting of administrative expenses. Although listed firms are legally independent even if they are part of the same business group, there remains the possibility that business group ties may influence the magnitude of political contributions as well as the extent of transparency because such firms experience a dual governance hierarchy corresponding to oversight at the firm as well as the group levels. I include business group affiliation as a binary variable (Vissa, Greve, & Chen, 2010). It is 1 for firms associated with a business group and 0 otherwise. I identified the business group affiliation from Prowess. Previous studies have also suggested that industry competition can have a strong effect on political contributions (Grier, Munger, & Roberts, 1994; Salamon & Siegfried, 1977). I control for this effect by including market concentration as the Herfindahl index. It is operationalized as the sum of the squared values of market shares of all firms in an industry. In defining the industry, I followed Chacar and Vissa (2005) and used the National Industrial Classification equivalent to Standard Industrial Classification (SIC) classification commonly used in the United States. I checked the robustness of my findings by using broader industrial classes and they produced substantively similar results. Because political contributions can also be associated with the election cycle, I used a dummy variable to control for the election years (Kozhikode & Li, 2012). They included the years 1996, 1998, 1999, 2004, and 2009. 15 Finally, I included a dummy variable to control for firms with missing observations to eliminate any potential effect of firms’ delayed entry or premature departure from the sample. All values are in millions of Indian rupees (except for the binary variables) unless otherwise indicated.

Analytical Model

My analytical approach investigates the potential of a difference in CPC before and after the regulatory incentive. This can be best accomplished by a difference-in-difference (DiD) model that examines changes in political contribution for each firm before and after the regulatory incentive taking into account their charitable contribution and ties to third-party contributors. In particular, it enables me to test whether political contributions changed after the introduction of regulatory incentive (Hypothesis 1) and whether this change was affected by charitable contribution (Hypothesis 2) and third-party political ties (Hypothesis 3). This is illustrated by the following equation:

Here y represents CPC, the outcome variable, and the interaction variables capture the joint-implication of regulatory incentive and charitable contribution/third-party contributor. The coefficients β3 and β5 are significant only if the outcome variable is significantly different after the introduction of regulatory incentive for firms with lower charitable contribution or with third-party political ties. Using the latter as an example, the model yields the estimated effect by distinguishing between R1, the pre-regulatory incentive period, and R2, the post-regulatory incentive period, as

However, multiple observations per firm can violate the ordinary least squares (OLS) assumption of the independence of errors. The resulting correlation between firm-specific errors can lead to biased estimates (Greene, 2007). To overcome this constraint, I used the generalized least squares (GLS) model with random effects. Although fixed effects model can also be used, one of my key variable, third-party contributor, is static across time, which is excluded in fixed effects. This made random effects most appropriate for my analysis. Nevertheless, I reran all models with fixed effects after excluding the time-invariant variables and controls and found the results to be substantively similar.

Results

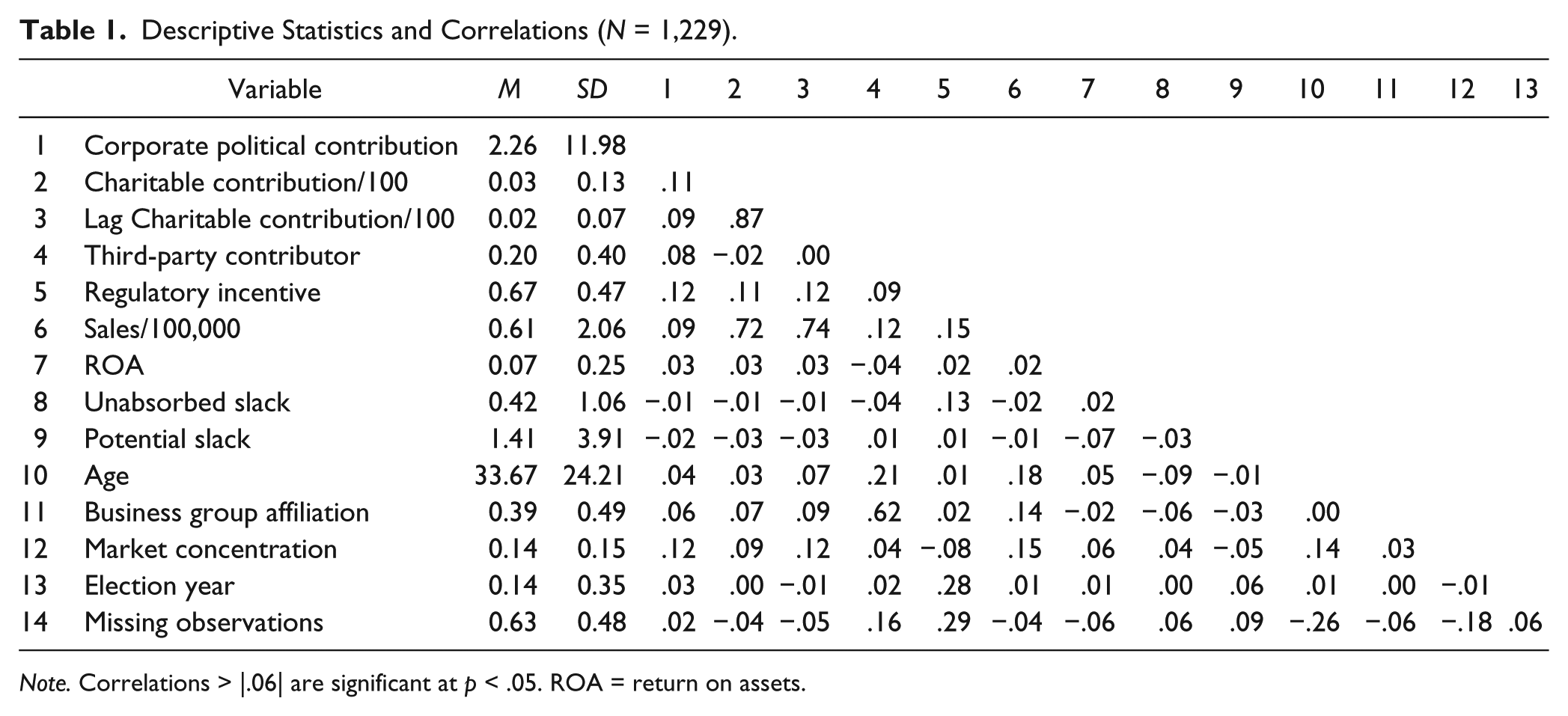

Table 1 shows the descriptive statistics and Pearson correlation. Although most correlations are small, charitable contribution is strongly correlated with sales, and a weaker but relatively large correlation can be observed between third-party contributor and business group affiliation. This was a potential concern because a large correlation between independent and control variables can make it difficult to observe the predicted effects due to multicollinearity. To examine the extent to which this could affect my findings, I checked the variable inflation factors (VIFs) and found all values to be below the threshold of 10. The maximum VIF was 2.29 and the average value was 1.47, which suggested that multicollinearity did not pose a critical concern for my analysis. 16

Descriptive Statistics and Correlations (N = 1,229).

Note. Correlations > |.06| are significant at p < .05. ROA = return on assets.

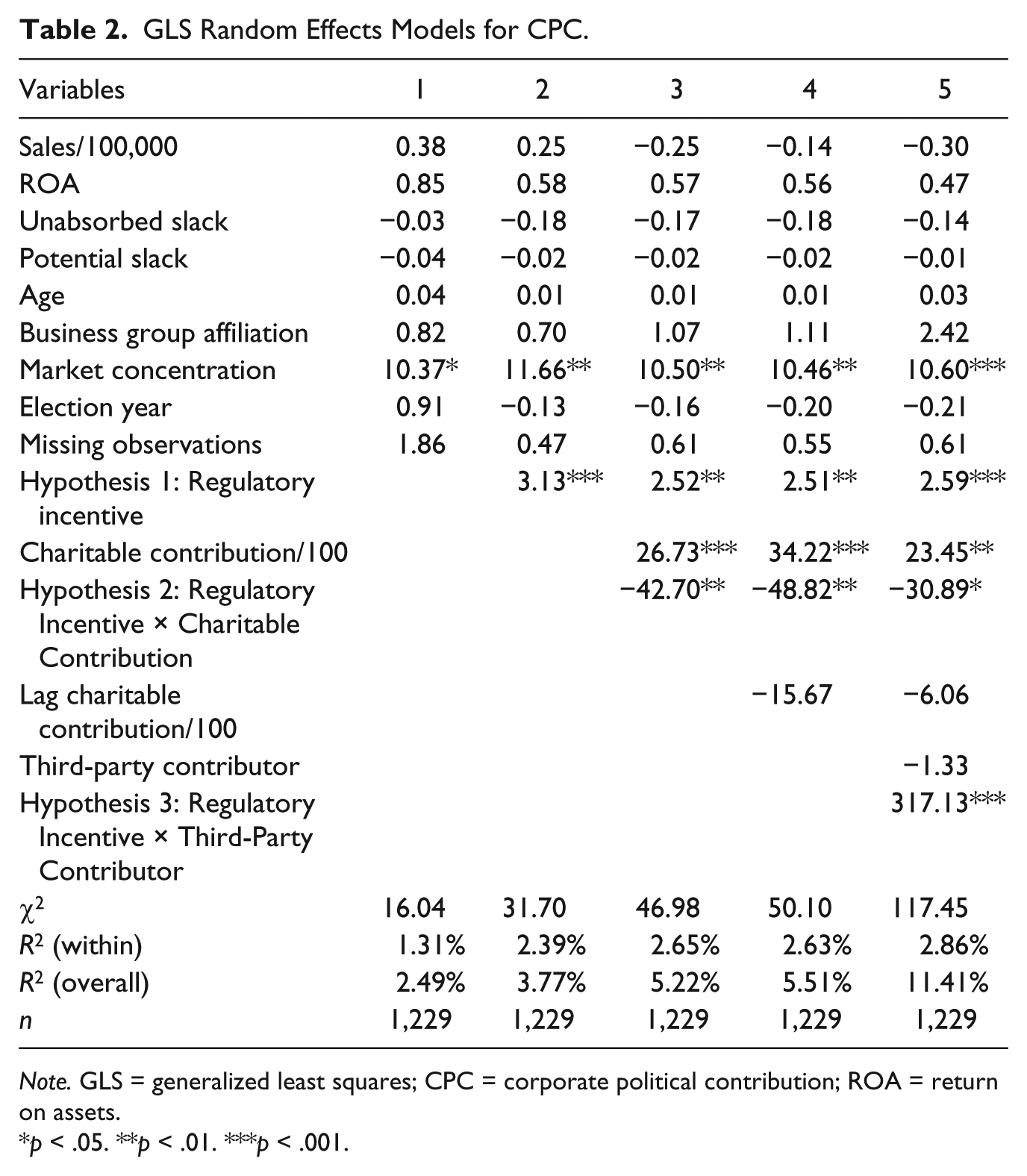

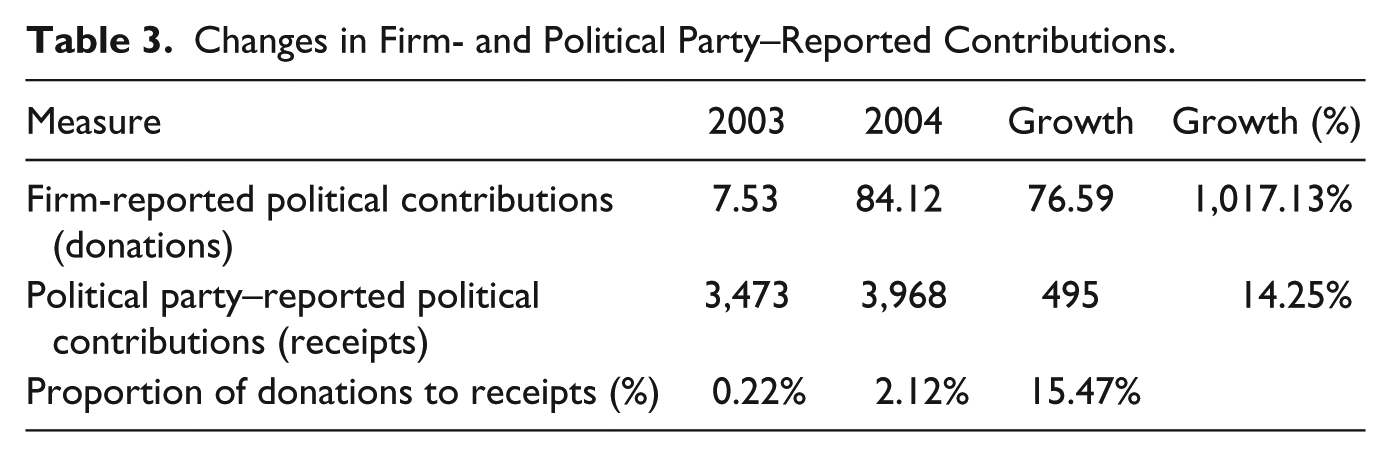

In Table 2, I report the tests of hypotheses. Model 1 includes the base-line controls where market concentration is the only variable that exhibits a significant effect. Model 2 tests for the effect of regulatory incentive. The effect is highly significant (β = 3.13; p < .001). It supports Hypothesis 1 that the introduction of a regulatory incentive led to a significant increase in CPCs. Because regulatory incentive is binary, its coefficient can be interpreted directly. It suggests that the increase in firm-level contributions was more than 3 times, on average, the contributions prior to the regulatory incentive. This validates my argument for cognitive disguise and demonstrates that in the absence of an economic shock, firms’ political intentions remained masked. However, it is not difficult to imagine that the increase in CPC may partly be associated with the corporate intention to capitalize on economic incentives that can help forge strong political ties. It is therefore important to identify the extent to which the change in CPC represents a net growth in political disbursements versus an apparent increase due to the transparency of previously disguised contributions. This requires the identification of an alternate source of data that can offer insights into the change in political contributions regardless of corporate disclosure choices. For this, I collected total political party receipts reported by ADR for the year before the regulatory incentive (i.e., 2003) and after the regulatory incentive (i.e., 2004). The comparison of political receipts with corporate contributions is reported in Table 3. 17 It shows that although there was a modest increase of around 14% in total political receipts between 2003 and 2004, the increase in firm-reported political contributions was more than 1,000%. This suggests that most of the increase in CPC may be fictional. The increase, it appears, captures the disclosure of corporate contributions that were previously reported elsewhere.

GLS Random Effects Models for CPC.

Note. GLS = generalized least squares; CPC = corporate political contribution; ROA = return on assets.

p < .05. **p < .01. ***p < .001.

Changes in Firm- and Political Party–Reported Contributions.

In Model 3, I examine if the decrease in charitable contribution facilitated the increase in political contribution. This can be observed through the interaction between regulatory incentive and charitable contribution. The effect turns out to be significant and in the predicted direction (β = −42.70; p < .01), which supports Hypothesis 2 that the introduction of regulatory incentive appears to have discouraged the use of charity for political purposes. This is consistent with my argument for functional disguise. Notice that the direct effect of charitable contribution is positive and significant, suggesting that the increase in political contribution is generally associated with an increase in charitable contribution. It is only after the regulatory incentive that an increase in political contribution was significantly likely to be accompanied by a decrease in charitable contribution. In Model 4, I add lag charitable contribution and the focal effects are unaffected. It validates that firms that were historically predisposed to charity did not respond differently. Model 5 tests my final hypothesis regarding the use of third parties as political intermediaries. This effect is associated with the interaction between regulatory incentive and third-party contributor. As predicted, the effect is highly significant (β = 317.13; p < .001), suggesting that subsequent to the regulatory incentive, firms associated with a third-party contributor demonstrated a much larger increase in political contribution compared with firms with no third-party association. This supports Hypothesis 3 that in the absence of economic benefits, third parties may be an effective mechanism for structural disguise that allow political disbursements to be disassociated from the corporation.

The results show a consistent and significant increase in the explanatory power of the model. The overall R2 for the base-line model (Model 1) is 2.49%, which increases to 11.41% in the fully saturated model (Model 5). This shows an increase of almost 4 times over and above the base-line effect. Similarly, the within-firm explanatory power of the final model is also quite significant. The R2 increases from 1.31% to 2.86%, suggesting that even for the same firm, more than twice the variance can be explained over and above the base-line effect. These values show that my hypotheses make a highly significant contribution to the discussion of CPC.

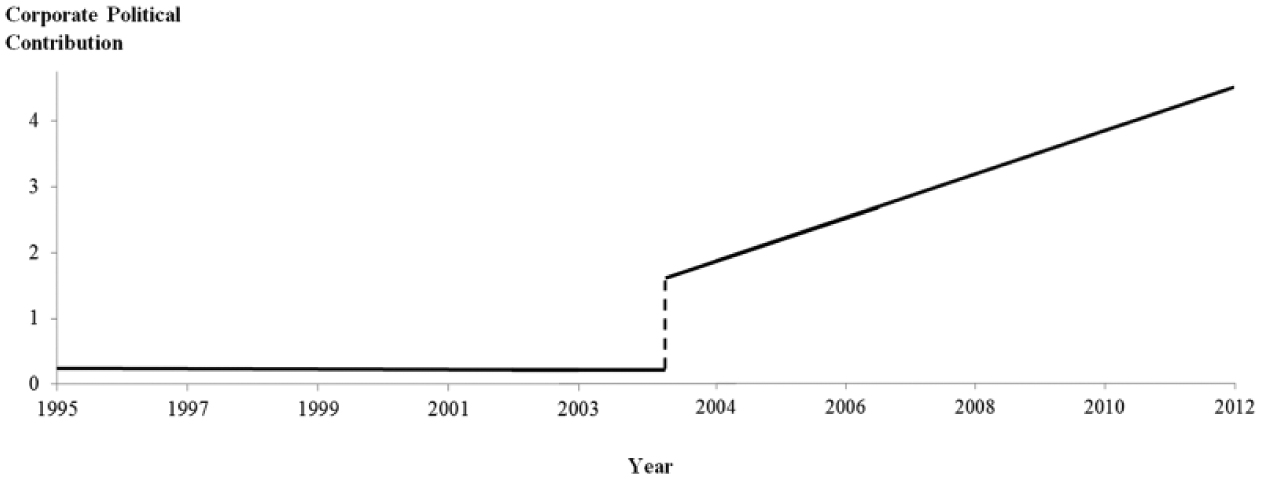

To develop a visual understanding of the effect of regulatory incentive on CPC, I plotted CPCs before and after the regulation in Figure 1. It illustrates that political contributions were largely static until 2003. However, as soon as the regulatory incentive was introduced, CPCs experienced a dramatic rise, and this trend continued until the end of the sample period. This demonstrates the significantly larger influence of economic benefit over mandatory disclosure on CPT. Notice that the regulatory incentive not only led to an immediate jump in political contributions but also led to persistent growth. This suggests a cautious approach toward disclosure with firms continuing to evaluate the evolving legal, economic, and competitive landscape vis-à-vis their political choices.

Corporate political contributions before and after regulatory incentive.

Discussion and Conclusion

This study has presented a conceptual foundation of CPT. I have argued that the discourse on CPT in the United States, which is primarily focused on mandatory disclosure, may benefit from the economic dimension. Corporations are more likely to trade off long-term financial benefits arising from political ties when incentivized with short-term economic benefits of transparency. Although economic incentives can take various forms, using the context of India, I have shown that the tax deductibility of corporate political spending has been successful in enhancing CPT. The dramatic increase in the disclosure of CPC following regulatory incentive identifies the limitations of the command-and-control approach.

In conceptualizing CPT, I have argued that the absence of transparency is due to the enactment of various forms of disguise that shield the visibility of CPCs. To develop a formulation of corporate political disguise, I borrowed the characterizations of disguise from theatrical drama, which manifests in three different forms. First is the cognitive disguise that pertains to concealed intentions. I showed that the significant escalation in CPC subsequent to a regulatory incentive is consistent with this formulation. It establishes that in the absence of the economic benefits, firms conceal a significant portion of their political contributions. A second form of disguise combines the change in intentions with a change in the visible functional identity. Using charitable donations as a mechanism for functional disguise, I showed that in the face of regulatory incentive, firms that increased their CPC significantly reduced the contribution to charity. It suggests that charitable contributions were previously used as a conduit for political contributions. Contextualizing the third form of disguise, the structural disguise, which pertains to corporate attempts to formally distance themselves from socially controversial activities, I showed that regulatory incentive led to a much larger increase in CPC for firms associated with a third-party contributor relative to firms that contributed directly. This suggests that in the absence of economic benefits, firms may use apparently independent organizations to relay their political contributions and avoid visible political ties. The strong support for my arguments substantiates that corporations prefer to disguise their political contributions when exposed to mandatory disclosure in the absence of a regulatory incentive.

My study makes two important contributions to the literature. First, I introduce the concept of CPT and demonstrate that empirical insights can significantly advance the debate on the regulation of CPC. I show that the expectations of society and of the various stakeholder groups can be more effectively channeled through policy decisions that recognize the implications of economic benefits. Regulatory incentives can provide an avenue for engagement whereby the interests of the general public, investors, politicians, and corporations are closely aligned. This, in turn, suggests that rather than viewing CPT as a model of enforcement, it may be more appropriate to view it as a negotiation between multiple goals that need to be harmonized (Freeman, Harrison, Wicks, Parmar, & de Colle, 2010). Of course, this is only possible when corporations are viewed as active participants in this discussion (Hess, 2007). Although further research is needed to more clearly understand how corporate concerns can fit into the CPT equation, it is evident that an effective balance is necessary between governance, accountability, and economic value. In this regard, the evidence from this study offers a strong endorsement of the greater viability of a market-based approach in yielding political transparency.

The second contribution of this study is the discussion of corporate political disguise. I have advanced a theoretical model of corporate disguise that can be used to build insights in areas such as institutional theory, information disclosure, and mandatory regulation, and to some extent, corporate misconduct. It extends our understanding of the obfuscation mechanisms that are available at the disposal of firms when attempting to evade transparency. Further refinements to this model can open new avenues of research, facilitate more informed regulation, and identify how the focus of CPT should expand beyond the corporation to include other entities such as external auditors and third-party contributors.

Of course, these findings need to be contextualized to understand their broader implications. The results of this study are based on the Indian economy, which is significantly different from the more developed economies including the United States. In fact, the various economies around the world offer an effective laboratory to examine the different manifestations of regulatory change (Djankov et al., 2010; Torres-Spelliscy & Fogel, 2011). It is therefore necessary to acknowledge that any model that is successful in one part of the world may not be completely applicable to another region. All regulatory forms need some modification to incorporate the unique nuances of the focal institutional context (Leuz & Wysocki, 2008). However, I also believe that the implication of regulatory incentive on CPT observed in this study is too strong to be ignored. Despite the social and the economic differences, the evidence from India offers valuable insights into the limitation of mandatory disclosure, the efficacy of regulatory incentive, and the mechanisms through which corporations disguise their political choices. Furthermore, I have ignored the costs associated with regulatory incentives. The development and implementation of viable economic benefits can be a costly undertaking for the government. It can lead to lower tax revenues and, therefore, substantive social implications as well as the politicization of regulatory change. To deter disclosures, firms may divert some of their funds toward activities that can help maintain the veil of secrecy over their political choices. This in itself may induce costs for firms and eventually for the investors. Thus, regardless of whether a regulatory change is enacted or politically subdued, there are likely to be some underlying costs. A clear understanding of such costs can help develop a broader appreciation of how CPT is tied to the economic environment.

My study also raises some critical questions. In particular, it needs to be understood whether CPT is always beneficial (Hermalin & Weisbach, 2012). This leads back to the earlier discussion about the recognition of corporate interests (Leuz & Wysocki, 2008). For example, how do the ties between corporations and politicians evolve when CPC is visible to the public? It could be that firms are reluctant of making this information public (Fung, Graham, & Weil, 2007), partly because their chosen parties may not always win and the visibility of corporate ties to a losing party can lead to an adversarial relationship with those who subsequently come to power (Gowda & Sridharan, 2012). CPT also makes corporations somewhat vulnerable by making their historical contributions public. This can have a negative effect on the negotiation power of a firm against the future recipients of political largess. Furthermore, although agency costs have been identified as a critical shareholder concern regarding political transparency, they can also have significant implications for regulatory agencies. The authority vested in executives allows them to manipulate expenditures, and in turn, raises the barriers against an effective environment for corporate governance (Bebchuk & Jackson, 2010). Even though the magnitude of CPC is significantly smaller in relation to other financial items, and correspondingly, it receives limited regulatory attention, it can have a large cumulative effect. This opens up an important avenue for further research, that is, to understand how regulatory agencies can respond to the challenge for CPT in the absence of economic incentives. I hope answers to these questions will continue to improve our understanding of the mechanisms that facilitate and limit CPT.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.