Abstract

We study how messages on Twitter by large non-governmental organizations (NGOs), targeting companies from the S&P500, affect these companies’ stock prices. With a sample of 1,611 tweets between 2009 and 2017 by 18 large NGOs, we observe significant changes in the stock prices of the targeted firms. More specifically, NGO tweets stating a positive message about the environmental, social, or governance (ESG). Actions of the firm have a positive effect on stock prices, while negative tweets have a negative effect. Nevertheless, we find that the presence of institutional owners hampers this effect: firms with high institutional ownership value positive tweets more negatively, and negative tweets more positively. These results support the idea that shareholders react significantly to NGO tweets but they react differently depending on their time horizon: for shareholders who have a more short-term horizon, typically institutional owners, the reaction diverges societal expectations about how firms should contribute to society.

Keywords

We investigate shareholder perceptions of non-governmental organization (NGO). Tweets involving listed corporations. We observe examples where the market reaction to these tweets diverges from the tone of the message posted. On August 22, 2017, the NGO Ceres News posted the following on Twitter: “Major businesses like @Adobe @Nike @SierraNevada @Unilever @MarsGlobal know 100% renewable goal is good for CA.” How did the stock price of these corporations react to this positive message? Negatively. Indeed, when we compute the financial market reactions for Nike, we obtain a significant abnormal negative return of −6.65% around the day of the tweet. On April 23, 2012, Greenpeace posted the following on Twitter: “Every day tons of coal keeps the internet humming tell @Amazon to switch to renewables!.” Despite the negative tone, a positive reaction was observed on the stock market with a significant rise in Amazon’s shares following the tweet. Regarding these reactions, it appears that the news published on Twitter may have an impact on the stock price, even those tweets are about environmental, social, or governance (ESG) news.

Over the past two decades, NGOs have become increasingly important actors in the economic landscape. Indeed, they are now invited to major multinational events such as the World Economic Forum in Davos and involved in international negotiations for setting corporate social responsibility (CSR). Standards like ISO26000 or establishing the Principles for Responsible Investment. Some of them (e.g., Greenpeace) even create their own certifications for sustainable business practices. Moreover, they have significantly increased their attempts to use their influence on companies to change corporate practices. The question that we ask in this article is do shareholders even care about NGOs? More specifically, we analyze the extent to which NGO influence on corporations is valued on the stock market by measuring the effect of NGO communication on firm valuation. This question is particularly important as we live in a world that expects its citizens to behave more responsibly, including investors and shareholders.

Under the neoclassical view of the firm (Friedman, 1970), its social responsibility is to increase shareholders’ wealth (shareholder-oriented theory). There is an agency relationship between shareholders and managers whereby the latter should act in the best interest of shareholders (Jensen & Meckling, 1976). Since this view was first developed, multiple scandals and studies have largely disputed it, giving rise to the stakeholder-oriented theory. Friedman’s view can still be considered compatible with the stakeholder theory as long as we adopt a long-term perspective in the assessment of shareholders’ wealth. Bénabou and Tirole (2010) emphasized that competitive markets are driven by economic efficiency but that this mechanism may generate unreasonable social inequalities, gaps in wealth redistribution and harmful consequences for the environment. Environmental disasters such as the BP Deepwater Horizon spill in April 2010 or poor labor protection tragedies such as the RanaPlaza Building collapse in April 2013 are clear illustrations of these market failures. As a result, groups of citizens, like NGOs, seek to build a political response within the business world, pushing corporations to act not only in the best interest of their shareholders but also all other stakeholders (employees, customers, community, society at large). And social media plays a key role in this respect.

The arrival of social media changed the way in which information is processed. These information marketplaces have become a powerful tool for institutions. As a consequence, social media plays a different but complementary role in financial markets compared to the traditional media. Information relating to the CSR of listed companies is steadily attracting more attention, including from financial investors (H. Chen et al., 2014). With respect to the dissemination of CSR information, NGOs are important players. They use social media to improve the impact of their communication, especially when it relates to corporations’ activities, the purpose being to raise awareness. In doing so, they avoid the channel of traditional media via direct communication.

NGOs typically focus their communication on the impact of corporations on different types of stakeholders such as society at large. In some cases, the NGO focuses on initiatives with a negative impact. For instance, Greenpeace’s multiple campaigns against ExxonMobil for its impact on climate change, or Oxfam’s 2013 campaign on PepsiCo and Coca-Cola to stop land grabs for sugar, are two examples of the type of NGO communication that targets corporations. Nevertheless, NGOs actually most often focus on positive actions. One example is the Room to Read, which promotes girls’ education in Asia and Africa and tweeted about Google when the firm gave Brittany Wenger an award for her work on breast cancer diagnosis. Another example is this post by Ceres News: “@GM and @Ford are ramping up development of EVs. Pro EV policies and boosting access to charging will create jobs and keep our state at the cutting edge of this emerging industry,” which resulted in a negative abnormal return for GM around the day of the tweet.

As the impact on different types of corporate stakeholders is at stake, the study of NGO communication is also a way to investigate the CSR of the targeted firms, and here we focus on tweets that deal with environmental, social or governance actions by listed corporations. The existing literature shows that CSR activities relate to shareholder value (Flammer, 2013; Godfrey et al., 2009). There is a close link between the visibility of CSR actions and their impact on a firm’s financial valuation. More specifically, public perceptions and the level of stakeholder attention on specific CSR initiatives determine their effect on financial performance (Aouadi & Marsat, 2016; Flammer, 2013; Fombrun et al., 2000; Huberman & Regev, 2001; Lev et al., 2010; Madsen & Rodgers, 2015). In this respect, the Efficient Market Hypothesis (EMH) assumes that financial market valuations incorporate all relevant and available information instantaneously as it arrives. However, prior literature has shown that investors have limited time and resources to access all available information and consequently rely on a limited number of information sources (Grossman & Stiglitz, 1980; Hirshleifer & Teoh, 2003; Hong & Stein, 1999; Merton, 1987). As an illustration of the magnitude of this phenomenon, Da et al. (2011) find that search frequency in Google is a significant predictor of stock price movements. This result suggests that online tools such as Google that allow specific types of information to be targeted are used by investors to such an extent that significant effects on stock prices can be observed.

We study NGO communication on Twitter, which is one of the major players in the social media industry. Twitter was created in October 2006 to allow users to communicate via microblogging messages known as tweets focusing on concise information. They were originally restricted to 140 characters, but on November 7, 2017, the limit was doubled to 280 characters for all languages except Japanese, Korean and Chinese, in contrast to other big social networks like Facebook or Instagram, whose content scope is broader. Three years after its creation, Twitter already had 75 million unique users, and by September 2016, it had about 91.5 million unique users, according to the 2016 Nielsen Social Media Report. Twitter therefore provides particularly interesting experimental data, not only because of the concision of the information posted, but also due to its primary importance in the social media landscape. In January 2019, Greenpeace had 1.73 million followers on Twitter and Oxfam 847,000.

The existing literature suggests that Twitter messages significantly relate to financial indicators. Zhang et al. (2011) find that the percentage of tweets with “Fear” words, within the full volume of all tweets, is negatively associated with stock market indicators such as Nasdaq and S&P500. Bollen et al. (2011) use Twitter feeds to measure public mood and find a significant predictive power on the Dow Jones Industrial Average. Sprenger and Welpe (2011) develop a measure of industry peers based on the degree to which pairs of firms are associated with each other on Twitter and find that this measure of relatedness explains stock returns with the same power as SIC codes. Blankespoor et al. (2014) found that firm-initiated news via Twitter relates to abnormal bid-ask spreads and abnormal depths. Their results support the idea that firm disclosures via Twitter help reduce information asymmetry. The authors describe Twitter as a “direct-access information technology” that enables direct access to investors. Sprenger and colleagues (2014a) show that S&P500 company-related Twitter messages generate significant abnormal returns for these companies. In another article by Sprenger and colleagues (2014b), the same authors find that the “sentiment” of tweets is significantly associated with abnormal stock returns and trading volume. The results of Ranco and colleagues (2015) confirm this finding with the Dow Jones Index. Behrendt and Schmidt (2018) show that Twitter stock-related messages are associated with significant intra-day volatility for Dow Jones constituents, although the related economic magnitude is debatable. Overall, two important conclusions can be drawn from this list of results. First, Twitter undoubtedly impacts the way in which information is processed across financial markets. Second, communicating on Twitter about corporations likely affects their value on the stock market, as it may help reduce information asymmetries.

Using a sample of 1,611 tweets containing the name of a listed corporations from the S&P500, between 2009 and 2017, by one of the 18 large NGOs, we classify them into two groups to distinguish those making a positive statement about the ESG actions of the firm from those issuing a negative message, and we assess their respective impact on stock prices. NGO tweets which do not focus on any environmental, social or governance action by the firm are considered neutral. One contribution of this is that, to assess the positive or negative tone of each tweet, we developed an interpretative framework to identify whether the NGO’s message is mainly positive (or negative) from the point of view of the NGO. We voluntarily employ a manual assessment of positive and negative tones, instead of using automatic tools, to limit any mistakes in interpretation. An automatic assessment of positive or negative tone based on lexicographical dictionaries or machine learning could indeed easily lead to such mistakes given the limited number of words in each tweet. Moreover, NGO tweets are often characterized by cynicism, irony or other subtle ways to convey a message “between the lines.” The distinction between positive and negative tweets is particularly important for several reasons. As highlighted in the CSR literature, positive and negative social actions are independent constructs that must be considered separately (Mattingly & Berman, 2006). Consumers react asymmetrically to ethical and unethical actions (Creyer & Ross, 1996). This polarity also has an impact on financial valuations. Indeed, outside the CSR focus, Sprenger and colleagues (2014a) investigate more than 400,000 S&P500 stock-related tweets and find that the returns prior to good news are more pronounced than for bad news, indicating that the stock market values positive and negative news in a different way. Krüger (2015) analyzes CSR data by MSCI (formerly KLD) to identify corporate events with either positive or negative implications for the wellbeing of a firm’s stakeholders. The author finds strong negative reactions to negative CSR news and slightly negative reactions to positive CSR news. Again, this latter result sheds light on the asymmetric reaction to positive or negative CSR news in terms of stock prices. We build on Krüger’s work as follows: instead of focusing on the effect of corporate ratings such as MSCI, which are designed for investors, we investigate Twitter as another channel of communication that also concerns corporations, we look at messages that are directed toward a broader audience than investors only, and we add the NGO perceptions into the analysis. This explains why our results differ from Krüger’s findings. Our study also has important implications for business practitioners whose interest in ESG issues is clear, as illustrated by the statement by Lawrence Fink, CEO of Blackrock, in 2016: “Over the long-term, Environmental, Social and Governance (ESG) issues—ranging from climate change to diversity to board effectiveness—have real and quantifiable financial impacts. BlackRock’s push for “social responsibility,” highlights this major shift among corporations” (published January 23, 2018 on CNBC.com).

With this research, we find evidence that shareholders do care about NGO tweets but, under certain conditions, their reaction differs from societal expectations about how firms should contribute to society: NGO tweets generate significant reactions on the stock market, with shareholders reacting positively to positive tweets and negatively to negative tweets, but the effect is reversed with institutional owners. We interpret this reversal as a consequence of the short-termism of institutional investors who, in general, exert short-term pressure on firms by selling portfolio holdings following negative earnings surprises or poor stock returns, as illustrated in Starks et al. (2017). Shareholder reactions to NGO tweets depend on their time horizon and therefore vary across different shareholder categories: shareholders with long-term horizons are more likely to be in sync with societal expectations, while those with short-term horizons are more likely to react in a different way than societal expectations.

In sum, this research makes three major contributions. First, we focus on ESG information from the perspective of NGOs, in contrast with other related studies which instead use information taken from an investor’s point of view (ESG rating agencies such as MSCI). This contribution is particularly relevant given the increasing number of studies which highlight inconsistencies in ESG ratings (Bouten et al., 2017; Chatterji et al., 2016; Delmas et al., 2013; Gibson et al., 2019), and it is particularly important as the impact of CSR depends on the way it is perceived by the public, with the existing literature showing that the impact of CSR initiatives is higher when they are visible (Fombrun et al., 2000), when sensitivity to consumer perception is higher (Huberman & Regev, 2001) and when consumer awareness is higher (Servaes & Tamayo, 2013). Second, this article provides a novel interpretative framework for NGO tweets that mention listed corporations. This contribution is also important given the importance of Twitter in both the social media and the financial landscape and since, to the best of our knowledge, this article is the first to focus on tweets by NGOs involving listed corporations. Third, our results build on the debate about socially responsible investments, a steadily growing phenomenon. Our results provide nuanced arguments relating to the assertion that shareholders care about ESG issues. We show that, despite the rise of socially responsible funds and the growing integration of ESG elements in investment decisions, there is still a divergence for short-term-oriented investors between societal expectations on how firms should contribute to society and the actual reaction to NGOs’ engagement with business issues.

This divergence has important implications for business and society. Given the importance of institutional investors in financial markets, the fact that their reaction to NGO tweets diverges from societal expectations on how firms should contribute to society is problematic. This could be an indicator for how other stakeholders in the firm (i.e., other than shareholders) are prioritized by institutional investors in general. It may help explain why more and more firms now decide to become private rather than public listed companies (see the analysis by Thomas (2017) in the Wall Street Journal: “Where have all the public companies gone?”).

Theoretical Background and Hypotheses Development

NGO Activism

According to Bendell (2017), NGOs are “groups whose stated purpose is the promotion of environmental and/or social goals rather than the achievement or protection of economic power in the marketplace or political power through the electoral process.” Therefore, in essence, there is tension between the purposes of NGOs and corporations, with the former focussed on societal goals and the latter mainly focussed on economic goals. Zadek (1998) specifies the role of NGOs in regulating corporate behaviors, incorporating NGOs in the term “civil society.” From his perspective, civil society exerts pressure on companies to improve social and environmental standards, which can be considered as a kind of “civil regulatory power” which firms must comply with. With globalization, the growing power of corporations in shaping politics and the development of information technologies, the engagement of NGOs toward business has become very important (Bendell, 2017). Van den Berghe and Louche (2005) even refer to “a new invisible hand” embodied by all non-market forces exerted by NGOs, the media, and trade unions.

Tweets are not the only tool for NGO action. According to Guay et al. (2004), NGO activism can take place at different levels, and they may use a status as either advisor or advocate of socially responsible funds, and even sometimes as shareholders. Using the rights associated with share ownership, they can exert pressure on firms to encourage them to invest capital in a particular company or sector. Alternatively, NGOs can call on consumers to boycott specific products or corporations. Boycotts are among the most frequent forms of consumer expression against unethical acts by firms. Examples include the calls by multiple NGOs, including Greenpeace and Ethical Consumer, to boycott firms selling bluefin tuna, an endangered species. These calls have a clear impact: in this case, several brands stopped selling bluefin tuna. NGOs can also organize spectacular moves, at company headquarters for instance, to capture media attention. Such initiatives create images that can be broadcast throughout the media to spark interest and concern among the largest possible audience. Sometimes, NGOs also highlight positive social actions by corporations as a way to congratulate their efforts and also to invite their rivals to follow the example. Finally, NGOs can invite a list of targeted media to a press release. All of the messages surrounding these actions, from boycotts to press releases, are also likely to be posted on Twitter. The study of NGO tweets is therefore an opportunity to capture information about all topics targeted by NGO actions.

Among the existing academic studies on NGO activism, Waygood (2004) provides a general overview of NGO intervention in corporate policies. The author demonstrates that under certain conditions, NGOs can change corporate practices using capital markets and enhance general welfare. Intervention by NGOs targeting listed companies can take place at different levels, including, for example, the production of investment analysis in support of their campaigns, direct attempts to generate capital inflows or outflows for certain investment projects, communication programs targeting investors on specific ESG issues, and attempts to stimulate dialogue between investors and companies. More generally, the author places strategic alternatives to exert pressure on listed companies in one of the two categories: 1. Economic pressure on investors to influence their decisions; 2. Using share ownership to voice concerns at the board level.

Why Would Shareholders Care?

Why would NGO tweets attract the attention of shareholders? We work on the assumption that the market price of an asset is an estimate of its value. Market investors make price assessments based upon their expectations of future cash flows on the asset. They form these expectations using the available information, which can come in different forms. It can be public information available in annual reports or filings with the SEC, or information available to one or a few investors. In this setup, any additional source or information is likely to attract attention. For instance, Huberman and Regev (2001) found that the prices of biotechnology stocks reacted to the announcement of the potential development of new cancer-curing drugs only when a New York Times article was released, although the news had already been reported in the journal Nature, a publication that is less visible to non-scientific audiences than the New York Times. More recently, Focke et al. (2020) show that advertising positively affects investor attention, even if it does not significantly impact stock prices.

Existing research has produced evidence that the effect of CSR on shareholder value depends on the visibility of CSR initiatives, as well as on the perception and the level of attention from both customers and investors. Krüger (2015) argues that CSR activities allow firms to gain reputational benefits and, as a result, reduce the cost of capital. Reputation is shown to be an important channel through which CSR affects performance. Under this rationale, the visibility of CSR actions is crucial: the more visible they are, the greater the reputational impact will be. Lev and colleagues (2010) showed that charitable contributions are significantly associated with future revenue, especially for firms that are more sensitive to consumer perceptions. Servaes and Tamayo (2013) show that CSR is more positively related to shareholder value for firms with high customer awareness. The perception of CSR matters and it evolves over time. For example, public pressure to behave responsibly toward the environment has increased significantly in recent decades. As a result, Flammer (2013) found that between 1980 and 2009 positive reactions on the stock market to environment-friendly initiatives decreased while negative reactions to initiatives that are harmful to the environment increased. This result highlights the importance of public perceptions of CSR which over the last few decades have changed drastically. In the same vein, Madsen and Rodgers (2015) showed that stakeholder attention mediates the relationship between natural disaster relief efforts and financial performance. Aouadi and Marsat (2016) found that social performance has an impact on firm value only for firms that attract high levels of public attention (i.e., those which are larger) located in countries with greater press freedom, the subject of more internet searches, and followed more closely by analysts. As mentioned above, NGO communication intensifies both customer awareness and investor attention: a firm targeted by a communication campaign on social media is likely to face greater scrutiny by both, intensifying the effect of CSR on shareholder value. Given that tweets involving listed corporations are likely to increase customer awareness, visibility to stakeholders and investor attention, we posit the following:

Now that we have explained why NGO tweets would have any significant effect on firm value on the stock market, we will now focus on the direction of this effect. More specifically, we seek to identify whether corporate initiatives that are perceived positively by NGOs are perceived positively or negatively by shareholders. In other words, our aim is to identify whether NGO perceptions of ESG issues converge or diverge with those of shareholders. We define positive (negative). NGO tweets as those that convey a mainly positive (negative) message about the environmental, social, or governance actions of the firm. Appendix A provides the detailed method used to identify the tones of tweets, which can be either positive, negative or neutral.

Points of convergence between shareholders and NGOs

Several arguments suggest that NGOs and shareholders share the same interests on ESG issues. Over the last two decades, there has been an impressive rise in Sustainable and Responsible Investments (SRI). In 2014, nearly 18% of US assets under management were tied to SRI, a tenfold increase on 1995 (T. Chen et al., 2020; SIF, 2014). There is increasing demand from investors and shareholders for the integration of environmental, social, and governance aspects. The United Nations-supported Principles for Responsible Investments (UNPRI) have been very successful, with more than 1,900 signatories representing US$89 trillion of assets under management in 2018. 1 Investors therefore appear to care about environmental, social, and governance issues, such as those targeted by NGOs.

Many academic studies such as Margolis and Walsh (2003) and Fisman et al. (2005, 2006) show a positive association between CSR and financial performance, asserting that firms can “do well by doing good” by generating trust among consumers and supporting strategic differentiation. Fisman and colleagues (2006) develop a model of corporate philanthropy where firms may gain a competitive advantage by signaling their aversion to sacrificing quality, in a market where quality is difficult to observe. These arguments are supported by empirical evidence of a positive association between profits and corporate philanthropy only in sectors with high advertising intensity and high competition. More generally, the CSR effect on financial performance has long been discussed in academic studies. Under one strand of literature, ethical behavior and profit are not mutually exclusive and CSR activities may actually enable firms to be more profitable. Baron (2001) and Siegel and Vitaliano (2007) suggest that CSR can be used strategically to achieve a certain competitive advantage. Bagnoli and Watts (2003) argue that firms compete to reach socially responsible consumers. The financial literature shows that socially responsible companies have a lower cost of capital (El Ghoul et al., 2011) and lower risk (Bouslah et al., 2013). In the mergers and acquisitions context, Deng et al. (2013) show that acquirers with good CSR realize higher merger announcement returns. Lins et al. (2017) find evidence that during the 2008–2009 financial crisis, firms with good CSR had higher stock returns, profitability, growth, and sales per employee. Although none of these studies measures CSR from the perspective of NGOs, the prediction which can be derived from the theoretical perspective that firms “do well by doing good” is as follows:

Points of divergence between shareholders and NGOs

Under another strand of literature, CSR initiatives may signal agency problems in the shareholder–manager relationship. Agency problems do indeed arise when the agent (here the manager) does not act in the best interest of the principal (here the shareholders), taking advantage of a situation of asymmetric information (Jensen & Meckling, 1976). In a previous study, Barnea and Rubin (2010) investigated the relationship between ownership structure and social performance and found that when managers own a share of capital, social performance is lower. The theory underlying this finding is that managers initiate social actions only when they do not bear its cost, that managers pursue personal interests above all and that the initiation of socially responsible actions is rather explained by the fact that managers care about their personal reputation. Under the agency theory, managers may therefore not act in the best interest of shareholders (Jensen & Meckling, 1976) but rather serve personal goals such as individual reputation. CSR can signal this type of agency problem, especially when the CSR action is relayed by an NGO. This reasoning would predict the opposite of Hypothesis 2 (i.e., that positive NGO tweets have a negative effect on firm value and inversely).

One other point of divergence which may arise between shareholders and NGOs is the time horizon. What is interesting in the study of news published by NGOs is that it often relates to firms’ environmental and social performance. As a consequence, it will have a different impact depending on the investors’ time horizons. For investors operating in the short term, we expect a more negative effect of positive NGO tweets on firm value. Positive CSR actions are associated with a long-term perspective, which may be at the expense of short-term performance. As argued by Starks et al. (2017), one type of investor that typically works with a short-term horizon is institutional investors. The authors show that these investors generally sell their holdings following negative earnings surprises or poor stock performance. Consistent with this argument, Pozen (2009) argues that institutional owners exert short-term pressure on managers to beat quarterly earnings expectations, at the expense of long-term actions such as CSR initiatives.

Nevertheless, other studies tend to emphasize a higher responsibility in institutional investor holdings and the positive effect of institutional ownership on ESG performance. Dyck and colleagues (2019) provide international evidence of a positive association between ESG performance and institutional ownership. Hong and Kacperczyk (2009), Kim and Venkatachalam (2011), and Chava (2014) show that institutional owners are less likely to hold stocks that do not comply with societal norms such as those in the gaming, tobacco, and alcohol industries or those with environmental concerns. T. Chen et al. (2020) find that an exogenous increase in institutional ownership leads to better social and environmental performance. Interestingly, Nofsinger et al. (2019) argue that institutional investors engage in SRI mostly because of economic incentives and for risk management purposes, rather than for altruistic motives. More specifically, the authors show that institutional owners are tilted away from stocks with environmental or social concerns but they do not invest in stocks with higher environmental and social strengths.

To disentangle these different arguments, we test whether the presence of institutional investors is likely to induce a more short-term horizon, leading to a stock market reaction that diverges with the NGO message (i.e., negative reaction to positive tweets and positive reaction to negative tweets):

NGO tweets are particularly relevant to the study of how investors’ time horizon affects firm value. If we consider that firm-related news can be of three types: news in traditional media (reaching a broad audience), news published by NGOs (also targeting a broad audience), and news published by rating agencies (targeting firms and investors). We also consider that news published by NGOs is the type for which investors’ time horizons will be most salient. News in the traditional media targeting a large number of people is likely to have a similar effect on firm value whatever the investors’ time horizons: if the news is positive it is likely to be positively perceived and vice versa. In contrast, positive news published by an NGO will have a positive effect only for investors with long-term horizons, as this news is more likely to relate to CSR actions, themselves associated with a long-term perspective at the expense of short-term performance. As a consequence, positive news by NGOs paradoxically has a negative effect on firm valuation, and conversely, CSR news issued by rating agencies (such as MSCI or Thomson Reuters Asset4) is characterized by a change in ESG scores. However, the effect of investors’ time horizons is barely apparent with this news type because ESG ratings are specifically intended for investors and measured on a yearly frequency, resulting in a dilution of any short-term effects, which is why existing studies actually provide evidence that the presence of institutional ownership (even though indicative of investors with short-term horizons) is associated with higher environmental and social performance (T. Chen et al., 2020; Dyck et al., 2019). Finally, the investigation of the specificities of NGOs’ impact on firms with institutional owners is also particularly interesting because the literature demonstrates that the attempts by these organizations to change corporate practices are more likely to succeed when they target institutional investors (Waygood, 2004).

Data and Methodology

Sample

Our sample contains 1,611 tweets involving 18 unique NGOs and 80 unique firms. To select our sample of firms, we focused on the top 150 on the S&P500 index and ended up with 80 companies actually targeted by NGO tweets. We consider an NGO as a not-for-profit organization or voluntary citizens’ group which is organized on a local, national, or international level and addresses issues in support of the public good. We study NGO communication from the Twitter activity of 18 large NGOs worldwide. We extracted our NGO sample from the “NGO Advisor” ranking at the beginning of our project in 2017. NGO Advisor is an independent media organization that highlights innovation and impact in the nonprofit sector through its Top 500 NGO rankings, in which NGOs are assessed on different dimensions which include innovation, impact, and governance. We selected the top 20 NGOs from this list. This means that our sample of NGOs contains those with the highest levels of innovation, impact, and governance quality. The focus on large NGOs is relevant to our case, as we observe that the largest NGOs are actually those who post the most tweets involving listed corporations.

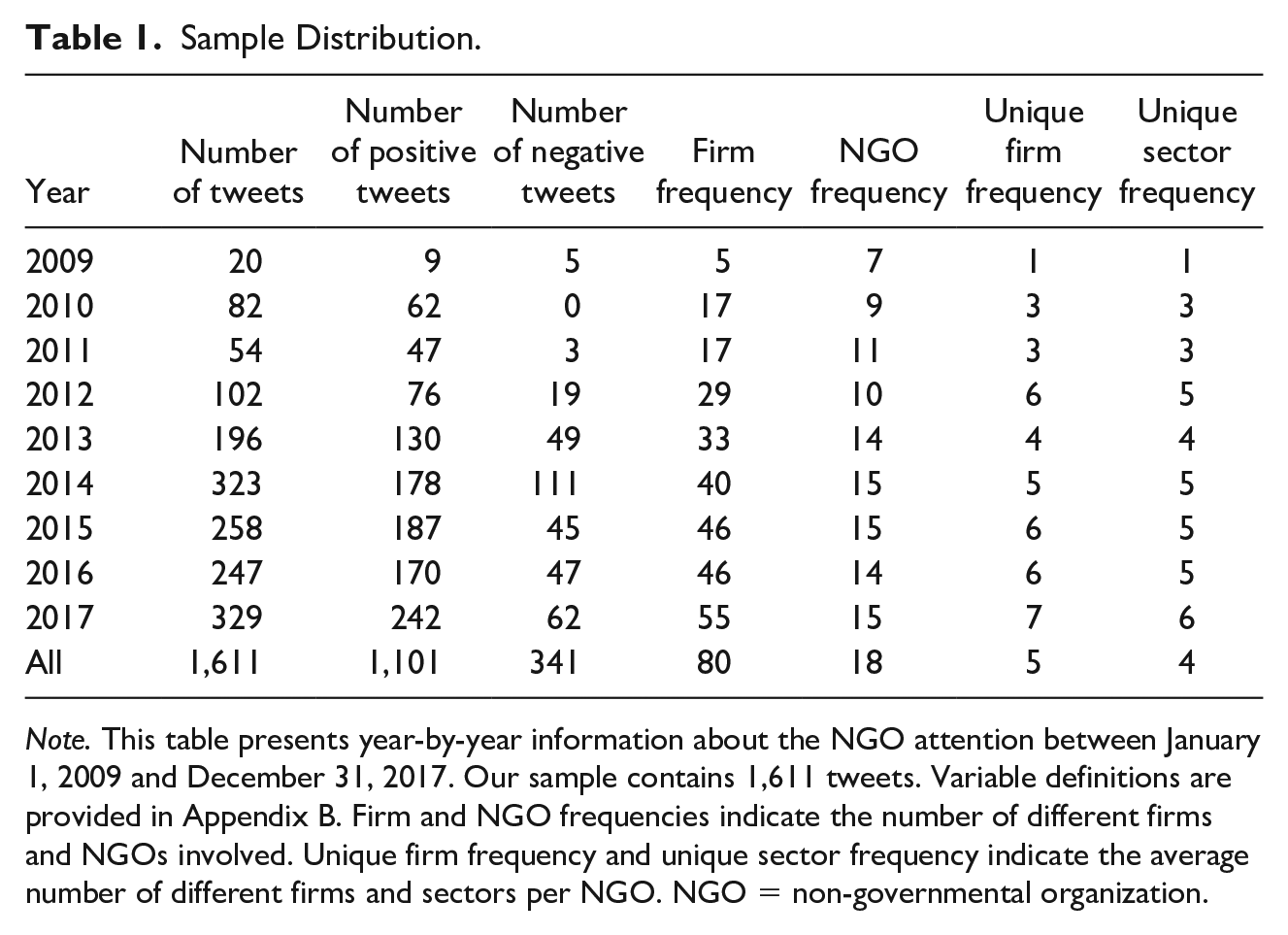

We started with a list of 20 NGOs, but two had to be deleted because of the absence of any activity on Twitter (they were also the smallest). Here is the list of NGOs used: Acumen, Amnesty International, Ashoka, BRACworld, CeresNews, GrameenFdn, Greenpeace, HIUnitedStates, HeroRATs, LandesaGlobal, MSF, OneAcreFund, Oxfam, Room to Read, Skoll Foundation, Mercy corps, Saudecrianca, and Save the Children. All of these released at least one tweet over the 2009–2017 period (from January 1, 2009 to December 31, 2017) containing the name of a corporation listed on the S&P500 index. Table 1 presents the year-by-year breakdown of the 1,611 tweets in our sample.

Sample Distribution.

Note. This table presents year-by-year information about the NGO attention between January 1, 2009 and December 31, 2017. Our sample contains 1,611 tweets. Variable definitions are provided in Appendix B. Firm and NGO frequencies indicate the number of different firms and NGOs involved. Unique firm frequency and unique sector frequency indicate the average number of different firms and sectors per NGO. NGO = non-governmental organization.

To retrieve messages from Twitter, we used the Twitter API to obtain the NGO tweets. This API provides a Search API where, upon entering a seed word, Twitter returns all tweets matching this pattern. We used the NGO twitter name to retrieve tweets. This focus allowed us to investigate only the most relevant news items and avoid “noise.” The sample exhibits two peaks in the number of tweets in 2014 and 2017. The number of NGOs and firms involved in this type of communication steadily increased over time.

One of the major contributions of this article is that we developed an interpretative framework for classifying the tone of NGO tweets. A manual assessment of the variable message tone is more appropriate in our case than automatic textual analysis, because the interpretation of tweet tones is often too subtle to be coded with a machine learning algorithm. To properly evaluate the tones of tweets, it is necessary to develop a precise interpretative framework that can be used to identify tweet types and establish a decision-making rule as to whether a tweet tone should be considered positive or negative. This interpretative framework was developed in two stages. First, we read a subsample of 600 tweets and classified them into two groups: those with a positive tone and those with a negative tone. While reading through the tweets, we fine-tuned the tone definition to set decision-making rules for ambiguous cases (i.e., where it was not straightforward to identify the tone). Next, we used the definition from stage 1 to classify all the tweets. To avoid any errors resulting from the fact that the definition evolved during stage 1 from the moment when we started reading the first tweets to the moment when we read the last ones, in stage 2 we re-classified the subsample of tweets that were analyzed in stage 1 to use a single identical definition across the whole sample of tweets.

We decided to assign a positive, negative, or neutral tone based on the following definition (see Appendix B for a full description of the variables): From the point of view of the NGO, we classify a tweet as “positive” (“negative”) when the NGO issues a mainly positive (“negative”). message about the environmental, social, or governance actions of the firm, and as “neutral” otherwise.

This concise definition reflects the decision-making rules adopted for cases where the tone was not straightforward. One important decision rule is that we strictly focus on tweets conveying a message about environmental, social, or governance dimensions; tweets that did not relate to any ESG aspect are classified as neutral. In Appendix A, we provide the details of the decision-making rules employed. By way of illustration, Appendix A also provides examples of ambiguous tweets with their classification for each decision-making rule.

Using our manual classification, we determined each tweet’s tone (positive/negative/neutral). Positive (negative) is a dummy variable equal to 1 if we consider that the tweet tone is positive (negative) and 0 otherwise. Table 1 also presents information about the number of positive and negative tweets. As shown in columns 3 and 4, the number of positive tweets (1,101) is higher than the number of negative tweets (341), regardless of the year considered. The fifth column displays the number of different firms targeted in the sample’s tweets while the seventh column provides the average number of different firms which have been targeted by one NGO. We see that the whole sample (last row) contains 80 different firms, and we record an average of five different firms per NGO over the whole period. The last row of Table 1 gives the average number of different sectors targeted per NGO. Across the whole sample, we see that one NGO tweets on average about four different sectors. A total of 416,480 tweets were initiated, of which 1,611 mentioned one of our 80 firms of interest. Further statistics on the number of tweets are provided in Appendix C, where we display the top 5 firms, top 5 NGOs, and top 5 industries in terms of numbers of tweets. Our sample contains some firms which are the subject of more positive than negative tweets such as Google or Microsoft, while the reverse is true of others such as Procter & Gamble. At the NGO level, we see that some NGOs only post positive tweets such as Save the Children while others like Greenpeace instead use Twitter for negative messages. Finally, at the sector level, we see that in the top 5 only the “Chemical and Allied Products” sector has slightly more negative than positive tweets, but the other sectors benefit from more positive tweets.

Variables of Interest

We use Cumulative Abnormal Retuns (CARs) to capture the market reaction to the release of a tweet (CARi). We calculate the returns using a traditional event study methodology and use the market-adjusted returns model to estimate the abnormal component of returns (AR) of stock i on day t:

where

This window of five trading days helps us avoid being contaminated by possible news leaks.

With H3, we examine whether institutional investors affect the impact of NGO tweets on stock prices. To measure institutional ownership, we use institutional holdings data from the FactSet database.

Control Variables

We control for firm size and growth opportunities with the logarithm of total assets, expressed in dollars (Firm size) and the book-to-market ratio from Compustat (Book-to-Market). The effect of NGO tweets on firm value may indeed vary for small/large firms and low/high growth opportunities.

Second, the effect of NGO tweets on stock performance also likely differs from one sector to another. One potential determinant is the pollution intensity of the sector’s core activity. Belonging to a pollution-intensive sector, such as mining or chemicals, will make it difficult to claim good environmental performance. As a result, those who invest in this type of firm are probably less sensitive to such aspects, and CSR news can be expected to have less impact in this context. As the investors who buy firms in polluting industries care less about CSR, CSR-related information likely affects stock returns in a different way compared to other industries. We control for sector specificities by including a polluting sector variable (Polluting Sector) if SIC codes are 1000–1499 (Mining and Chemicals) and 2800+2999 (activities related to Mining and Chemicals).

Third, the effect of NGO communication should be more pronounced in sectors that are more scrutinized by the media, and therefore by the market, typically the case for business-to-consumer (BtoC) sectors (Dupire & M’Zali, 2018; Flammer, 2015). BtoC sectors are particularly relevant to our case because these sectors, which are characterized by the fact that they sell directly to end consumers rather than other corporations. It is particularly interesting to study the specificities of these industries because, as the marketing literature highlights, social media plays an especially important role in these sectors. This is because it fosters brand awareness, loyalty, engagement, and sales (Rapp et al., 2013; Swani et al., 2014). We follow the same list of BtoC SIC codes as in Flammer (2015), which includes the following: 0000-0999, 2000-2399, 2500-2599, 2700-2799, 2830-2869, 3000-3219, 3420-3429, 3523, 3600-3669, 3700-3719, 3751, 3850-3879, 3880-3999, 4813, 4830-4899, 5000-5079, 5090-5099, 5130-5159, 5220-5999, 7000-7299, 7400-9999.

Fourth, as mentioned earlier, we control for whether the firm belongs to the first highest quartile in terms of numbers of tweets (variable “Serial Tweeted”) to account for the fact that CARs may be different for firms most targeted by NGO tweets.

Finally, we include additional variables to control for tweet and NGO characteristics. We control for the fact that some NGOs publish several tweets on the same topic for several consecutive days. As a result, it might be that the latest tweet in the series has less impact on CARs than the first. We therefore include the variable After 7-day dormant period which is a dummy variable equalling 1 if the tweet was first released after a 7-day dormant period and 0 otherwise. We control for the fact that the age of the NGO may impact its visibility and interact with the effect of NGO tweets on CARs. We use the log of NGO tenure which captures the age of the NGO as the number of years since its creation (NGO tenure). We were not able to use either the number of followers or the number of re-tweets as proxies for impact because the official Twitter API only returns the most current follower count and the most current number of retweets, which are cumulative values over time and were not recorded at the time of the tweet. Nevertheless, since our sample only includes NGOs with the highest impact, the impact of tweets by these specific organizations is likely to have a low variability in the cross-section, making it reasonable to omit the number of followers and retweets as controls. However, to proxy the potential impact of NGO, we control for the size of the NGO with the total assets, expressed in Euros (NGO Size). We additionally control for the log of the number of followers (NGO Followers). A tweet by an NGO with a very large number of followers is likely to have more impact than a tweet with fewer followers. However, measuring the number of followers at the moment the tweet is posted is difficult because Twitter only displays the latest number of followers. We therefore use the number followers as displayed in August 2020 by Twitter, although the tweets in our sample cover the period 2009 to 2017.

Results

Univariate Statistics

Table 2 displays the descriptive statistics of each of our variables of interest and controls. Out of 1,611 tweets, the average CAR is 0.13% with 68% of tweets positive and 21% negative. The remaining tweets were classified as neutral because they contain neither a mainly positive nor a mainly negative message about the ESG actions of the firm. Interestingly, 61% of tweets were sent after a 7-day dormant period, which indicates that the majority of tweets in our sample are not part of a series of similar tweets over several consecutive days; 46% of tweets target firms in BtoC sectors and 20% in polluting industries. Valuation is proxied by the book-to-market ratio and the average value is 0.5. The percentage held by institutional owners is 75.25%. The average NGO tenure is 43.04 years and ranges between 8 and 98 years. Finally, the average of total assets at NGO level is more than 210 million Euros.

Descriptive Statistics: All.

Note. This table presents descriptive statistics for our sample. Our sample contains 1,611 tweets announced by NGOs between January 1, 2009 and December 31, 2017. Table 2 describes each variable of interest. Variable definitions are provided in Appendix B. SD = standard deviation; NGO = non-governmental organization.

Table 3 provides the descriptive statistics on the number of tweets at the year, firm, NGO, and sector levels. At the time level, there are 9 years of observations, with an average of 179 tweets in each one. At the firm level, we see that out of the 80 firms in the sample, each one is the subject of an average of 20 tweets, while the median is 8. The difference between the mean and the median indicates that a few firms are the target of many more tweets than others; this is also characterized by the highest quartile being above 29 tweets (Q3), while the lowest is below 3 (Q1). (i.e., 25% of firms are the subject of more than 29 tweets, and another 25% are the subject of fewer than 3). At the NGO level, we observe that each NGO posts 90 tweets on average while the median is 53 and that 25% of NGOs post more than 86 tweets (Q3), while for another 25% the figure is below 12 tweets (Q1). Finally, at the sector level, there are 21 different sectors with each one targeted by an average of 77 tweets, while the median number of tweets per sector is 42, so the sample is again characterized by some sectors which are particularly targeted by NGO tweets. The highest quartile is more than 74 tweets per sector (Q3), while the lowest is below 9 (Q1).

Descriptive Statistics: Tweeting Activity by Subsamples.

Note. This table presents descriptive statistics for our sample. Our sample contains 1,611 tweets announced by NGOs between January 1, 2009 and December 31, 2017. Table 3 focuses on the number of tweets per year, per firm, per NGO, and per sector. Variable definitions are provided in Appendix B. SD = standard deviation; NGO = non-governmental organization.

In our multivariate analysis, we account for these sample characteristics by including year and sector fixed effects in our regressions, controlling for a number of NGO characteristics (tenure, size, number of followers), as well as for a “Serial Tweeted” dummy indicating whether the firm belongs to the highest quartile in terms of the number of tweets.

Table 4 provides the average CARs of NGO tweets for a 5-day event window ([−2days:+2days]). The mean CAR for the whole sample is reported in the first row, as well as the number of observations involved and the t-stat assessing whether the CARs are significantly different from 0. Table 4 displays the results for the subsamples of tweets with positive and negative tones. We also provide average CARs for a subsample of firms with low institutional ownership as well as a subsample of firms with large institutional ownership and test the difference in means. We derive subsamples based on all other control variables and we split our sample into two subsamples for dummy variables (e.g., BtoC sector, after 7-day dormant period, polluting sector, Serial tweeted) and for continuous variables (e.g., IO, firm size, book-to-market, NGO tenure, NGO size, and NGO followers) according to their median. Table 4 also indicates the difference of mean CARs according to tweet tone (positive or negative).

Stock Market Reactions Around Tweets From Non-Governmental Organizations (NGOs).

Note. This table presents the average cumulative abnormal returns [−2 days; +2 days] for all tweets and according to tweet tone and tweet characteristics. Our sample contains 1,611 tweets announced by NGOs between January 1, 2009 and December 31, 2017 variable definitions are provided in Appendix B. NGO = non-governmental organization.

**, and *indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Across the full sample, the average CAR of NGO tweets is significantly positive (0.125%), which indicates that NGO tweets have a significant impact on stock returns. While the average CAR for the subsample of positive tweets is insignificant, it is positively significant for the subsample of negative tweets. However, as these univariate results do not take important covariates into consideration, it is difficult to draw any conclusions at this stage. Nevertheless, when we look a bit deeper into the subsample analysis, we see that when IO is larger, overall shareholders react more negatively to NGO tweets (Diff: −0.029), the reaction to negative tweets is more positive (Diff: +1.094) and the reaction to positive tweets is less positive (Diff: −0.116). These results are consistent with the idea that institutional owners exert short-term pressure on managers and react in the opposite direction of the NGO message, in contrast with other types of shareholders.

Concerning control variables, we observe that shareholders react differently for firms in BtoC sectors, with reactions to NGO tweets less positive overall, reactions to positive tweets less positive, and reactions to negative tweets more positive. For firms with low growth opportunities (high book-to-market), where agency problems can be stronger, shareholders react more positively to NGO tweets. Negative tweets targeting smaller firms, where agency problems can also be stronger, also have a more positive effect on firm value. For tweets occurring after a period of 7 days without any tweet about the firm (surprise), shareholders tend to react more positively; we also observe that for tweets with no surprise (where there have been prior tweets about the firm in the past 7 days), the reaction to negative tweets is significantly more positive. In polluting industries, the effect of NGO tweets on firm value is more positive than in non-polluting industries. Finally, the positive effect of NGO tweets on firm value is more pronounced when the NGO has more followers, a lower tenure, and smaller size.

However, we need to sharpen our analysis with multivariate statistics to fully account for all interactions, controls, time, and sector effects that may distort the interpretation of univariate statistics.

Multivariate Statistics

To address our testable hypothesis, Table 5 provides the results of the following specifications:

where one observation, with i in subscript, represents one tweet from one NGO about one firm. CARi indicates the CAR of that firm around the day of the tweet. Tone refers either to Positive, a dummy variable that is equal to 1 if the tweet has a positive tone, and 0 otherwise, or Negative, a dummy variable that is equal to 1 if the tweet has a negative tone. A tweet can be neutral (neither positive nor negative). X is a vector of control variables that include log Firm Size, BtM, Serial Tweeted, After 7-day dormant period Polluting sector, BtoC, logNGO Tenure, log NGO Size, and log NGO Followers.

Explaining Stock Market Reactions Around Non-Governmental Organizations (NGOs).

Note. Tweets. This table presents the results of a OLS regression analyses of the cumulative abnormal returns calculated on an event study [−2 days;+2 days]. Our sample contains 1,611 tweets announced by NGOs between January 1, 2009 and December 31, 2017. All regressions control for year and sector fixed effects. Standard errors are adjusted for heteroscedasticity. Variable definitions are provided in Appendix B. NGO = non-governmental organization.

**, and *indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

In Table 5, Models 1 and 2 indicate that positive and negative tweets have no significant effect on CARs. However, in Models 3 and 4, the coefficients for the positive and negative dummies are statistically significant and indicate that the general reaction to positive tweets is positive and negative to negative tweets. This result supports H2. Interestingly, Model 3 indicates that the interaction between positive (negative) tone and institutional ownership has a negative (positive) effect on CARs. In other words, shareholders value positive NGO tweets more negatively when there is institutional ownership, in support of Hypothesis 3. Conversely, in Model 4, we see that the interaction between negative tone and institutional ownership has a positive effect on firm value, again in support of Hypothesis 3. Overall, multivariate statistics serve to sharpen the interpretation of the results obtained in the univariate analysis: while NGO tweets lead to an aggregate significant effect on stock prices (H1), positive tweets are on average positively perceived by shareholders, and negative tweets are negatively perceived (H2), but the effect is reversed with institutional owners (H3): negative NGO tweets are more positively perceived when institutional ownership is higher, and positive tweets are more negatively perceived, consistent with a stronger divergence between the NGO message and the stock market reaction. Institutional owners therefore appear to induce a more short-term horizon and lead to a more negative perception of CSR initiatives.

Discussion

We now propose a discussion of the above results from a broader perspective. After a disengagement of governments in the 1980s, corporations faced less and less regulatory pressure. Nevertheless, after many scandals, numerous actors, including NGOs, engaged under different manners and attempted to denounce the deviations from what the society expects from corporations and to modify their deviant behavior or their negative externalities.

Our results show that tweets by well-known NGOs, regardless of tone, have an impact on the financial performance of the corporations targeted. This illustrates that social media allows NGOs to reduce information asymmetries and provoke adjustments on the stock market. However, these stock market reactions depend on the type of shareholders concerned. Our results are consistent with a large body of literature on investor heterogeneity, where divergent investor opinions have implications for asset prices and returns. On the one hand, we find that one type of shareholder reacts positively to positive tweets, and conversely, another type of shareholder (institutional investors) reacts in the opposite way. On the other hand, investors with a long-term horizon react positively to a positive tweet and vice versa.

The impact of NGOs on stock price via social media, relative to a positive externality or a deviant behavior by a firm, illustrates the socio-economic and political context in which firms now operate. To better understand this linkage, it is important to study the process which allows an NGO to transform a deviant behavior into a challenge and politicize it, sometimes resulting in a regulatory framework with which the corporation will have to comply.

This influence by NGOs and interest groups is well documented in other disciplines. In political science, prior research has investigated whether these influences on public administrations are positive or harmful (Ornstein & Elder, 1978). In sociology and in management, for example, Pasquero (1985, 1993) studied the contribution of NGOs and interest groups in turning a corporate concern into a political challenge. For these authors, a concern can remain silent (for example, the working conditions in the textile industry). It can only grow and emerge if several actors, interest groups, or NGOs decide to denounce it, dramatize it in the media (Gamson, 1988), and crystallize it as a societal stake. The pressure on the government becomes strong enough for political parties to consider regulating it. Such regulation may not be a law: it could be sanctions or a code of conduct incumbent on multiple stakeholders. In cases where the implementation of a regulation is not achieved, there is a possibility of “reactivation,” whereby the concern remains in a dormant state until other interest groups or other more favorable conditions, like elections, for example, once again bring it into the spotlight. Initially, firms are likely to resist these potential social and environmental norms. But then they begin to engage in negotiations to reduce the changes induced by the implementation of these norms, until finally responding unwillingly by adhering to the minimum legal requirements (Logsdon, 1985).

An illustration of this is the environmental catastrophy caused by Exxon-Valdez and the pressure from NGOs and the media which led the United States to require the petroleum sector to use double hulls. The Exxon accident in Alaska occurred when maritime safety was an environmental concern, one targeted by several NGOs, and allowed this concern to be crystallized, amplified by the media leading to more regulations.

During this process, companies which would not otherwise have taken heed of NGO warnings on social media could be compelled to comply with the regulations. In other words, an externality targeted by an NGO can lead to an obligation to comply rapidly at high cost, to the loss of clients who insist their providers follow specific codes of conduct, or to a deterioration in the reputational capital of firms who do not comply, resulting in an increase in their cost of capital. Being targeted by an NGO could represent a “dormant” debt which a firm can no longer ignore. Until recently, moving from the emergence of a concern to its formalization, amplification and politicization or attenuation was constrained by the availability of resources (time and money) to denounce the problem (Hilgartner & Bosk, 1988). Nowadays, the development of social media reduces certain constraints and offers NGOs the opportunity to mobilize the followers of their causes at both the local and international levels.

Therefore, it is important for companies that want to be legitimate and in touch with the various stakeholders that may hinder their activities to strategically monitor the publications of the most influential NGOs. This way, they can get ahead of potential scandals and be proactive.

Conclusion

Social media has changed the way in which information is processed on the market. Our article investigates the perception of CSR by the financial markets based on NGO tweets. Using an event study approach, we measure the impact of NGO tweets on firm valuation, distinguishing between tweets conveying a positive or negative message about the Environmental, Societal or Governance actions of the firm. We find that NGO tweets significantly affect firms’ CAR, with shareholders generally reacting positively to positive tweets and negatively to negative tweets, but this effect is hampered by the presence of institutional owners. We find that when institutional ownership is higher, shareholders react more positively to negative tweets and more negatively to positive tweets. All in all, these results show that the presence of institutional owners leads to a stronger divergence between the NGO message and its perception by the stock market. While prior literature shows that institutional owners exert short-term pressure on management, this article shows that such pressure induces a divergence from societal expectations about how firms should contribute to society. When the investors have a short-term horizon, they value ESG initiatives more negatively than when they have a long-term horizon.

Social media is a new channel for NGOs to communicate their message. The results of our study, which focuses on one social media platform, Twitter, and on the largest NGOs, illustrate this new environment and show that denouncements or encouragements on social media now have an impact on the financial performance of companies. Ultimately, corporations need to take into account not only their shareholders but also their stakeholders, including NGOs which can target and influence financial results or cost of capital. Firm strategy should include monitoring of the main social media platforms, and especially those used by the largest NGOs, to anticipate emerging concerns or even start a discussion with the NGO to better understand the concerns being voiced and implement appropriate changes, just as firms do with their financial backers. Moreover, given the reaction of institutional investors, the targeted firm should adapt its reaction to the actions of NGOs depending on the ownership structure. Companies with a high proportion of institutional ownership should thus communicate with the NGOs that target them.

This research contributes to the existing knowledge in different ways. The focus on the NGO’s point of view is particularly relevant as a growing number of studies emphasize the limitations of existing ESG ratings which are often designed for financial investors and may therefore not properly reflect the connection with societal expectations. Our research is also novel as it develops an interpretative framework for NGO tweets which allows us to assess the tone of the message with respect to its ESG dimension. Maybe more importantly, our works provide nuanced views relevant to the steady development of socially responsible investment initiatives by showing that there is a persistent divergence between the interests of short-term-oriented shareholders and all other stakeholders. This finding is particularly important as we live in a world that expects its citizens to behave more responsibly, including shareholders.

Although this study provides novel results, it leaves room for further investigation. Since we focus on large firms and large NGOs, our results may not be applicable to smaller, less visible institutions. In addition, we focus on the U.S. context, and the results may differ in different geographical and cultural settings. This research points to avenues for further research, especially given our focus on Twitter which is one among many other social media channels. It would be interesting to study NGO activity on other social media and evaluate whether the shareholder reactions differ from one social media platform to another. It would also be useful to evaluate the effect of NGO tweets on other stakeholders, for example, by studying changes in revenue or employee satisfaction in relation to tweets to evaluate customer or employee reactions. Finally, it would be interesting to extend the analysis and compare the impact of NGO tweets that relate to ESG dimensions with other NGO tweets which do not relate to any ESG dimension.

Footnotes

Appendix A

Appendix B

Variable Description.

| Variables | Description | Source |

|---|---|---|

| CARi (%) | The cumulative abnormal returns for acquiring firms over the five trading days that surround the tweet dates [−2 days;+2 days] | CRSP |

| Positive (Dummy) | 1 if the tweet tone is positive according to our interpretative framework for NGO tweets presented in Appendix A, 0 otherwise | Manual |

| Manual | ||

| Negative (Dummy) | 1 if the tweet tone is negative according to our interpretative framework for NGO tweets presented in Appendix A, 0 otherwise | Manual |

| Manual | ||

| IO (%) | Percentage of share ownership held by institutional investors | Factset |

| Size (Dollars) | Market Capitalization (in 1000s) is a measurement of the size of a security defined as the price multiplied by the number of shares outstanding | Compustat |

| Book-to-Market (%) | Ratio of book value to market value (Compustat variables CEQ/MKVALT) at the beginning of the year | Compustat |

| Serial tweeted | 1 if the firm belongs to the highest quartile in terms of numbers of tweets | |

| After a 7-day Dormant Period (Dummy) | 1 if the tweet is released after a 7-day dormant period, 0 otherwise | Manual |

| Polluting Sector (Dummy) | 1 if the firm SIC codes are 1000–1499 and 2800–2999, 0 otherwise | CRSP |

| B to C Sector (Dummy) | Dummy variable equaling 1 when the firm belongs to a B2C sector based on their 4-digit SIC codes, including the following: 0000-0999, 2000-2399, 2500-2599, 2700-2799, 2830-2869, 3000-3219, 3420-3429, 3523, 3600-3669, 3700-3719, 3751, 3850-3879,3880-3999, 4813, 4830-4899, 5000-5079, 5090-5099, 5130-5159, 5220-5999, 7000-7299, 7400-9999. | CRSP |

| NGO Tenure (years) | The difference between the tweet release date and the NGO creation | NGO Website |

| NGO Size (in million) | Total assets of NGO (in million) | NGO Website |

| NGO followers | Number of followers (in thousands) |

Note. NGO = non-governmental organization.

Appendix C

The Top-5 Firms, Top-5 Non-Governmental Organizations (NGOs), and Top-5 Industries in Terms of Numbers of Tweets.

| Number of tweets | Number of positive tweets | Number of negative tweets | |

|---|---|---|---|

| Top-5 Firms | |||

| ALPHABET | 140 | 108 | 0 |

| PEPSICO | 104 | 57 | 45 |

| MICROSOFT | 102 | 84 | 14 |

| PROCTER & GAMBLE | 102 | 27 | 74 |

| CITIGROUP | 76 | 68 | 7 |

| Top-5 NGOs | |||

| CeresNews | 468 | 411 | 20 |

| SavetheChildren | 266 | 212 | 0 |

| Greenpeace | 230 | 22 | 201 |

| Oxfam | 117 | 26 | 79 |

| SkollFoundation | 86 | 68 | 4 |

| Top-5 Industries | |||

| Business Services | 403 | 299 | 24 |

| Chemical & Allied Products | 252 | 116 | 123 |

| Food & Kindred Products | 226 | 120 | 93 |

| Depository Institutions | 192 | 176 | 11 |

| Transportation Equipment | 82 | 70 | 4 |

Note. NGO = non-governmental organization.

Acknowledgements

We thank Eric de Bodt, Jean-Gabriel Cousin and Amal Aouadi for their valuable comments and suggestions. We have also benefited from remarks received during the AFFI Conference (Paris, France) 2018 and the Business & Society Conference (Mannheim, Germany) 2018. Remaining errors are the sole responsibility of the authors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.