Abstract

Multi-sided platforms (MSPs) are becoming increasingly important in contemporary economies. This special issue of California Management Review aims to stimulate collective discussion among researchers and practitioners on advancing diverse types of MSPs and on better understanding their future development. This article analyzes five contributions to this special issue and explores the growth trajectories of MSPs. There are three types of platforms: born-platform, platform-born adjacent, and incumbent-born. And they rely respectively on three market entry strategies: market creation, market broadening, and market deepening. This article also spotlights the coopetition dynamics of the platforms.

Keywords

Multi-sided platforms (MSPs) have revolutionized models of many traditional business areas, including transportation, hospitality, and financial services. MSPs have enabled the rapid rise of a significant number of unicorns worldwide. In 2022, the global market of platforms (e.g., platform-as-a-service [PaaS] and Internet of Things [IoT]) was median $234 billion and is expected to grow to a median $2 trillion by 2027. 1 As digitalization continues to evolve, the potential of MSPs is gaining considerable weight in contemporary and future economies.

We define a MSP as a digital ecosystem for organizing collaboration and control based on software, hardware, and services, without taking ownership of the services whose exchanges it facilitates and governs through diverse inter-organizational interactions. Digital platforms create new boundaries, within which — by matchmaking, complementing, or sharing their assets and resources — customers might help each other to create new value or, in other words, innovations. 2 In that way, platforms “create strong network effects, as their relative value rises with the number of actors — users and suppliers — joining their ‘ecosystem.’” 3

Our playground is an ecosystem of social, complex, and regulated business environments with a major focus on healthcare, but not limited to it. The digital healthcare services ecosystem provides a particular context to study its transformation through the phenomenon of multi-sided markets. The digital healthcare services ecosystem can be characterized as risk-averse, non-technological, highly standardized and regulated, inert, and path-dependent, with a high-liability environment.

During the past decade, many scholars have observed that MSPs can reduce transactional costs, improve accessibility to services, manage consumerism, and thus contribute to sustainability. MSPs may help restructure entire industries and create business model innovations. 4 However, it is also true that digital economy MSPs penetrated some industries more than others. Although we can clearly name MSP leaders in the transport, hospitality, and financial sectors, only a handful of MSPs have emerged in healthcare.

The general purpose of this special issue is to stimulate collective discussion among researchers and practitioners on advancing diverse types of MSPs and better understanding the trajectories of their future development. This article aims to explore the development trajectories of the different types of MSPs and how they deal with their go-to-market challenges. We ground our observations on the explorative analysis of five selected papers that we believe contribute to the theory and practice of the MSPs.

The special issue contributes to the strategic, technology management, and platforms literature by explicating strategic choices of profiting from innovations of the three diverse types of platforms (e.g., “digital colonization” and electric vehicle [EV] platform strategy); refining technological and organizational capabilities needed to support platforms’ strategic choices (e.g., dynamic capabilities, including platform orchestration and user-engagement capabilities); and distilling three less known types of platforms based on their origin and place in the value chain (e.g., born-platform, platform-born adjacent, and incumbent-born).

Furthermore, the special issue provides advanced knowledge to the owners of three types of platforms: MedTech and automotive incumbents, Big Tech companies, and healthcare startups. Startup platform owners can benefit from adopting unique roles (community organizer, market matchmaker, and innovation manager) that help to orchestrate and boost patient innovation activities 5 ; furthermore, they can learn customer engagement mechanisms that result in successful network effects. 6 All three types of platform owners can find it useful to understand “digital colonization,” a four-stage model of the process of platform entry. 7 Finally, incumbents need to be aware of the value impedance of digital transformation and dynamic capabilities that mitigate it and help an incumbent-born platform to grow. 8 MSP strategy is beneficial to automotive incumbents that need to make strategic decisions that help coordinate a complementary network, platform launch, and openness. 9

We organize our analysis and insights into four sections:

we provide a conceptualization of the definition of the MSPs; besides well-known definitions based on the function of the platform, we propose a typology of the platforms based on their origin and place in the value chain;

we explain platforms’ go-to-market strategy based on profiting from innovations theory and distill three criteria to spotlight platform go-to-market choices;

we review the five selected papers on diverse MSP cases; and

based on the results, we discuss their impact on theory and practice, including future research avenues.

Types of MSPs

The mainstream literature provides several prevailing definitions of “digital platform.” In general terms, a “digital platform” is a connected digital system that provides a common set of design and governance rules to facilitate interactions between multiple users. Digital platforms typically change how users access markets and consume products and services.

MSPs can be differentiated based on the functions they perform. 10 Some examples of platform classification are: two-sided non-transactional versus transactional 11 ; platform providers that may or may not be platform sponsors 12 ; and exchange platforms, advertiser-supported media platforms, transaction platforms, and hardware-software platforms. 13 The most common typology of MSPs recognizes differences between product and industry digital platforms. Product platforms are organized to create product innovation by adding or removing functionalities. 14 For example, platforms such as Black + Decker, Volkswagen’s automotive platform, and Intel’s microprocessor can be regarded as product platforms. Industry platforms focus on attracting two or more types of customers by enabling them to innovate, interact, and create network benefits. 15 Platforms such as Facebook, Google, Tencent, SHS teamplay, and Philips HealthSuite are seen as industry platforms. Industry digital platforms can be classified further into either transaction or innovation platforms. Platforms also differ with respect to value propositions. Transaction platforms focus on facilitating the exchange of products or services or any other interaction on the platform, whereas innovation platforms create value by allowing innovation on the platform. 16 For example, Twitter, Uber, Airbnb, and Amazon are transaction platforms; GE Predix, Google Android, Apple iOS, SHS teamplay, and Philips HealthSuite are innovation platforms.

The less well-known typology of MSPs juxtaposes platform origin (platform-born adjacent versus incumbent-born digital platforms) and their position in the value chain (upstream versus downstream digital platforms). 17 Consequently, four types of MSP can be identified: upstream platform-born adjacent; upstream incumbent-born; downstream platform-born adjacent; and downstream incumbent-born. This classification of MSPs recognizes that there is a significant difference between the platforms based on their origin and value proposition. Platform-born adjacent platforms tend to serve end-users (most often, they are downstream platforms) and invoke a transformative service innovation. In contrast, incumbent-born digital platforms are dependent on the incumbent’s core product (and tend to be upstream platforms) and thus stumble with organizational settings and capabilities needed to assure digital platform success. 18 As a result, these two types of platforms differ in the products/services they provide, technological capabilities, and customers they serve.

Finally, there is a stand-alone type of platform—born-platform—that refers to a startup whose business model is based on a digital platform value proposition from the very start of a new venture. 19 Entrepreneurs create digital platforms to fill a particular niche and enable interactions between diverse platform users, creating a new market. 20 Furthermore, they needed to create new governance mechanisms for user participation. 21 In contrast to platform-born adjacent platforms, “born-platforms” do not yet have path dependence reinforced by the incumbent platform and thus differ significantly from them in organizational forms and governance, capabilities, and the way they address customers. 22

Go-to-Market Strategy: Platform Market Extension versus Market Creation

Numerous studies suggest that innovation alone does not guarantee commercial success. New product development efforts should be combined with a good business model that articulates value capture and go to market strategies. This was a theme in Teece’s work on “Profiting from Innovation” (PFI), which helps map business model selection to the type of innovation while enabling one to figure out how to capture value (via licensing, vertical integration, or hybrid approaches). 23 The PFI framework requires firms to ask questions such as whether a dominant design has emerged and what is the nature is of the appropriability regime. Answers to such questions impact the design of business models.

Other aspects of the PFI model inform about the timing of “windows of opportunity” for firm entry into new markets. First-movers may suffer from a nascent industry’s lack of structure, 24 while latecomers are disadvantaged by poor positioning in complementary assets. 25 The emergence of a dominant design marks the closing of a window of opportunity. 26 Christensen et al. 27 propose that the window of opportunity for entering an industry occurs “during the period just prior to the emergence of a dominant product design.” The emergence of a dominant design sometimes triggers the onset of industry maturity. 28

A stream of research in entrepreneurship examines various aspects of the optimal entry strategy of a startup (e.g., optimal timing of opportunity exploitation). 29 Studies generally suggest that a startup should focus on exploration (market creation) until it accumulates sufficient knowledge and thereafter shift focus to exploitation (market extension). Given that customer preferences and technological trajectories are revealed over time, 30 incumbents—in contrast to startups—prefer to wait until uncertainty is resolved, but then it may be too late.

A stream of strategy and platform research has stressed the importance of ownership and control of complementary assets in determining the winners and losers when new technologies are commercialized. 31 Factors include not only the supply chain inputs needed to embody the innovation in a product or service, but also other products, technologies, and services needed to produce value in consumption. Empirical support for the role of complementary assets has been found in studies of the typesetter industry 32 and the success of new entrants and incumbents in the medical imaging industry. 33

When a firm operates in a weak appropriability regime, the ownership of complementary assets (e.g., distribution channels, brand) is particularly important, as the firm still has the means to capture value from the innovation. If a firm without a complementary asset operates in a weak appropriability regime, rapid imitation would destroy opportunities for value capture. The innovator would have to either build them or form partnerships to acquire the required complementary assets.

Teece highlighted co-evolution by introducing points in time. 34 “Rents” flow to the bottleneck assets, but he acknowledged that different complementary assets could be relevant at different points in time. Rents not only are generated from exploiting bottleneck assets; they also arise from combining different technologies in unique, value-enhancing ways that lead to system-wide gains exceeding the additive nature of standard Edgeworth complements. 35 Studies on PFI have emphasized not only technological but also value chain complementarity. 36 In a multi-invention context, the bottleneck could be a technology rather than a conventional asset. The presence of different types of complementarities increases coordination issues, which makes appropriability more difficult.

Furthermore, the original PFI focused on value chain issues—whether the firm was ready to assemble the specific and general complementary assets needed to bring the innovation to market. Subsequent studies on PFI expanded the notion of business models to include the architecture of the business, including customers, costs, and likely competitor responses. 37

Consequently, we conclude that MSPs would follow the exploration of an exploitation-oriented, go-to-market strategy that aids in creating new markets (e.g., often the choice of startups) or extending existing ones (e.g., often the choice of the incumbents). The strategic choices are supported by the underlying technological capabilities of the platform owners (including orchestrating complementary assets), the novelty of the product/service (existence of the dominant product/service design), and the customers they address (value capture from boosting network effect).

Next, we present five selected papers that provide insight based on case studies of three types of MSP growth and competitive advantage in relation to their origin and market entry strategies.

The Review of the Papers on Managing MSPs

The Case Studies of Mental Health and Customer Innovation Platforms Launched by Startups

Zhou and Wan 38 examine how practitioners can develop a robust platform in a highly regulated healthcare industry. They show how mental health hybrid platforms started their businesses and operated in two different Chinese firms. Their analysis begins by referring to the need to build network effects, which manifest in both a direct and an indirect manner. These effects form the self-reinforcement feedback loop, which in turn powers more network effects. However, the network-building process poses challenges too. Findings show that hybrid platforms made efforts to deliver four types of offerings: free services, low-priced experience services, high-priced counseling services, and training services.

Six mechanisms characterize the principles and tools for the management of hybrid platforms. Social networks facilitated interactions between partners and shared needed information, while incentive mechanisms aimed to intensify and deepen the interaction and communication. The expected behaviors were reinforced by the reputational and monetary rewards for both counselors and consumers. The voting systems have several functions (e.g., giving feedback about the quality of services, and enhancing the understanding of user involvement and engagement). The remaining mechanisms deal with assurances for the platform’s counseling services and counselors’ qualifications.

Cennamo et al. 39 contend that stakeholders’ involvement produces motivated and knowledgeable partners to carry out ideas that improve the quality of life for communities and societies. The barrier to such an innovation sometimes lies in the reality that these stakeholders may be isolated from each other. In their study, Cennamo et al. bring out how, in the case of a disconnected value network and regulated industry, the platform conception enabled barriers and organizational inertia to be overcome. An MSP creates a place for the interactions and exchanges among different stakeholders, and orchestration is defined as the facilitation of a set of processes that increase MSP value to its users.

Orchestration comes to light through three distinctive roles that the platform plays in the creation of an assembly of integrated contributions. First, the community organizer position indicates the broad task of sharing innovations developed by patients and caregivers. This role differs from the traditional platform archetypes presenting the functions of knowledge exchange facilitator, information certifier, and engagement manager. Second, the market matchmaker role puts together the innovation value networks. When compared with the matchmaking activities of traditional platforms, this role emphasizes connecting innovators with the product producers who have recourses to, and interest in, new perspective ideas. Activities related to the amplification of information and bridging form the main scope of the matchmaking role-set. Third, in the case of that successful platform, the role of the innovation manager presents as a facilitator of Internet transition possibilities. The case shows that the platform can become an innovation value shaper when the motivation and capabilities are in place.

The Case Study of the “Digital Colonization” of Highly Regulated Industries by Big Tech Platforms

Ozalp et al. 40 capture large-scale movement that extends digital power across diverse markets and shows that the entry of established platforms into the highly regulated industries takes a specific form. Ozalp et al. coin the term “digital colonization” to illustrate the four-stage model of the platform entry process into regulated industries. Their analysis targets Big Tech companies (known as GAFAM: Google, Amazon, Facebook, Apple, and Microsoft) that entered the healthcare and education areas in the United Kingdom and the United States because, so far, most entry activities have happened in those countries. The variance of Big Tech entry processes depends on the level of regulation, the existence of central versus distributed systems, and the importance of private actors.

Through step-by-step analysis, Ozalp et al. discover how the Big Tech companies entered the regulated areas of healthcare and education. The findings reveal that the Big Tech companies focus on capturing data as a pathway to value-adding activities. These companies have a competitive advantage in the highly regulated industries when developing new data-driven services and products. Data are evolved to the value-adding process from two sources: first, direct data capture through using the companies’ own hardware or software for developing the datasets; and second, indirect data capture, which means using existing data. These represent the first two stages of the model of the process of platform entry to the regulated industries. The process stages that follow concentrate on how to exploit these data. The detailed analysis exhibits the generation of data-driven insights for improving existing products and services and participating in the design of new products or services for the industry. The process model shows why and how indirect data capture, combined with data-driven insights, help overcome bottlenecks related to data sensitivity, one of the most important concerns in highly regulated industries.

The Case Studies of MedTech and Automotive Incumbent-Born Platforms

Pundziene et al. 41 find that incumbents see digital platforms as a feasible way of extending their range of products and services. The organizations looking for these kinds of novel approaches also should consider whether the product/service innovation matches organizational innovation. Pundziene et al. show how MedTech incumbents cope with the digital transformation gaps when introducing a new approach to the products: the switch from delivering one product to one type of customer to offering digital healthcare services engaging multiple parties through product/service innovation.

This paper focuses on value impedance as a manifestation of complex challenges posed to the incumbent-born MedTech digital platforms, where value impedance is defined as a comprehensive expression of any form of friction or barrier to value flow within organizations. Dynamic capabilities form the lenses for the deeper analysis of the organizational strategies and choices because these enable a focus on the internal and external competencies under rapidly changing circumstances. The findings discuss digital transformation gaps and value impedance related to the mindset, business model, organizational reconfiguration, and continuous renewal of dynamic capabilities. Pundziene et al. contend that successful management of transformation gaps helped digital health platforms build a new set of dynamic capabilities. Dealing with organizational boundaries equips incumbent companies with the ability to cope with the continuous pressure to renew. This case shows that incumbent-born platforms may extend and deepen the firm’s market if the firm is committed to change and is flexible enough to maneuver between core and new business.

In their study of electric vehicles (EVs), Anderson et al. 42 discuss the potential within the car industry when the idea of MSPs appears. Although MSPs seem to be similar for gasoline and electric cars, Anderson et al. argue that two major differences between these car types affect the utility and profitability of businesses—namely, differences derive from the temporal or quantitative properties (like the size of installed bases) and from structural or qualitative differences (such as EVs being able to be recharged in various places and not only at filling [gas] stations). The station as a location and source for energy determines what and how the MSP can add to the existing business models. These questions oppose the mature refueling networks and those at the start of the life cycle and, in turn, lead to the need for an EV platform strategy. Knowledge about MSPs opens perspectives on how the automotive incumbents could expand effectively into the EV industry.

Anderson et al. present a set of five decisions firms, and managers of incumbent firms must make if they want to gain from exploiting the advantages of MSPs. First, the role of platform coordinator is a crucial component of a winning strategy. The advantages and rationality of actively coordinating all sides of the platform become obvious in the example of Tesla, especially when compared with other automakers. Anderson et al. argue that the lack of such coordination partially explains why the EV industry outside Tesla has been marked by lofty promises and unmet goals. Second, the egg-and-chicken problem occurs with the launching platform, and incumbents from the automobile industry should select either one or a combination of four alternatives: do it alone, collaborate within the consortia, impact and rely on the regulators and policymakers, or rely on market mechanisms. Two abovementioned vital questions lead to the third important decision: whether the MSP is designed to be opened or closed. The fourth conclusive theme opens the window for looking at growth. Fifth, organizing the platform strategies reveals the need to resolve how to put together the key characteristics of the EV industry and the concept of MSPs.

The analysis of the papers presented above led us to the MSPs’ typology and understanding of how they interact among themselves. The platform’s origin proved to be a significant factor affecting the platform’s performance and go-to-market strategy. Next, we provide a more profound discussion and concluding remarks.

Nexus of the Origin of MSPs and the Emerging Platform Market

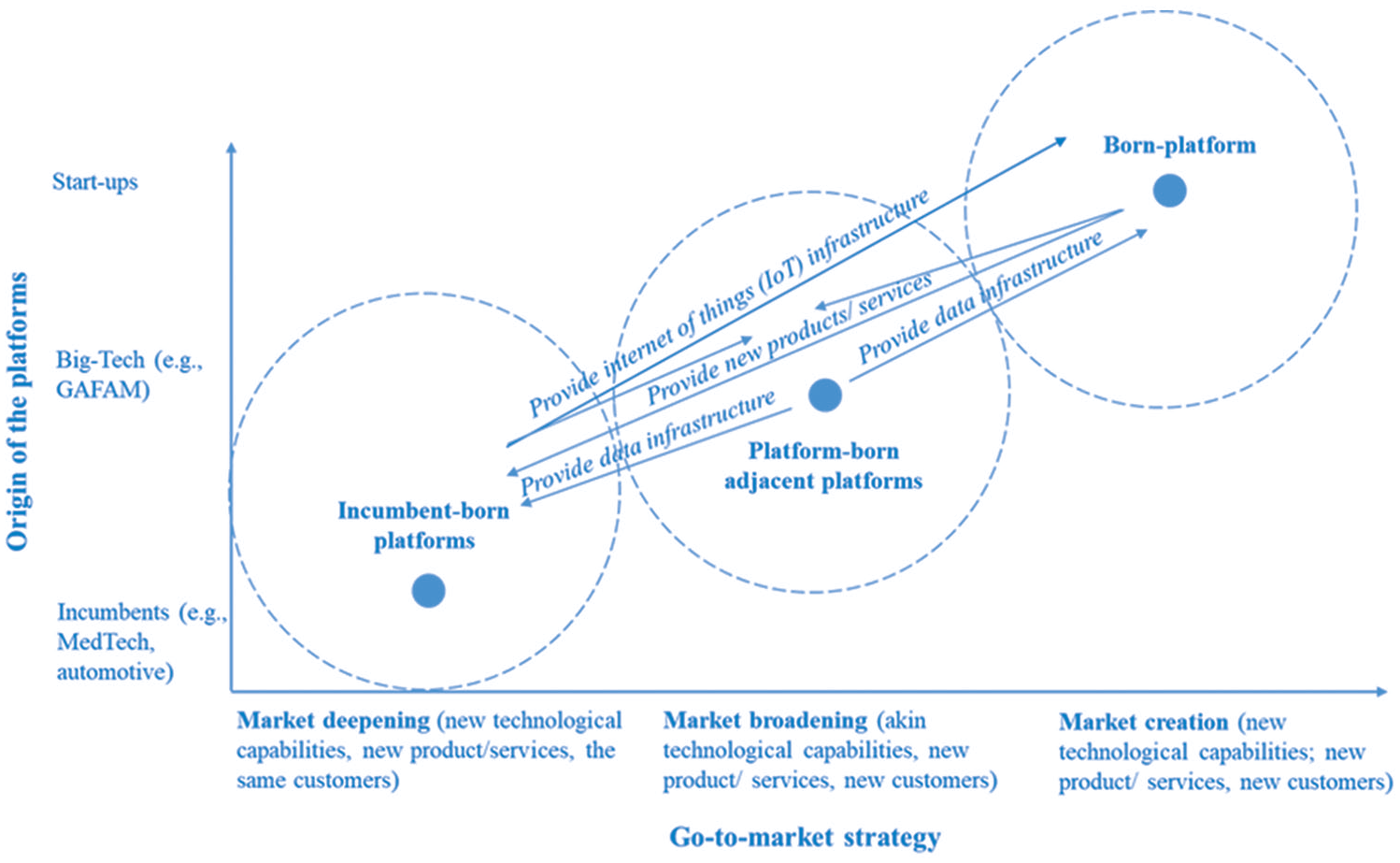

The nexus between the origin of MSPs and their position in the market and competitive dynamics can be explained by analyzing the three types of platforms (see Figure 1). First, as incumbent-born platforms sit astride an incumbent’s core products/services, they target the same customers, even though their technological capabilities often are different. 43 In that way, incumbent-born platforms deepen the market of the core products/services. In contrast, platform-born adjacent platforms address new customers by “colonizing” different business sectors (e.g., Google Health, Facebook Health, Microsoft Education) and, thus, new customers. 44 As a result, a platform-born adjacent platform broadens Big Tech incumbent platform’s market. 45 Finally, born-platform startups create unhacked markets by developing innovative products/services based on new technological capabilities and by addressing new customers. 46 The technology management scholars also support this notion: “We suggest firms pioneering these business models in their industry, such as Airbnb, often create entirely new markets based on previously untapped resources.” 47

Positioning digital multi-sided platforms at the nexus of the platform origin and go-to-market strategy.

In the case of the incumbents, the parent company’s technological capabilities play an essential role in supporting the platform’s competitive performance. For instance, the MedTech company’s IoT infrastructure is a valuable source of health data for all three types of digital healthcare platforms; Big Tech provides data infrastructure services to incumbent-born and born-platform platforms and access to and management of diverse data. 48 Based on IoT and PaaS infrastructure, both platforms can successfully harvest data and capture value by complementing each other. Born-platforms also can harvest data; however, the startup’s scale—and thus data—is relatively small and can serve as an experimental base for developing innovative products/services. 49 Often born-platforms depend on incumbents’ and platform-born adjacent platforms’ data collection and management services. On the other hand, born-platforms are a valuable source of complements (e.g., innovative products/ services), providing the other two types of platforms with niche products/services faster and more effectively than incumbent’s internal providers. 50

Regardless of their origin, all three types of platforms perform below the level of opportunity 51 due to the lack of a dominant platform design. Thus, the platform market can still be regarded as emerging and open to diverse go-to-market strategies. 52 We observe that incumbent-born platforms tend to extend existing markets with new products/services to the same customers (market deepening), while platform-born adjacent platforms tend to offer the akin technological capabilities-based products/services to new customers (market broadening). Startups can experiment with exploring and creating new markets while scouting new territories. Consequently, startups are valuable assets to incumbent-born and platform-born adjacent platforms in reducing innovation and market entry costs.

In contrast to incumbent-born platforms, first, “platform-born adjacent” and two, “born-platforms” target new customers and thus broaden or create new markets. Incumbent-born platforms enjoy a common customer base with the core business, which complicates the rapid scaling of the platforms. When the platform targets exiting customers, that creates internal competition and value impedance resulting in organizational frictions. However, when a digital transformation is commonplace, rents can emerge from combining different technologies in unique, value-enhancing ways that lead to system-wide benefits. 53 The case studies of incumbent-born platforms show that incumbents possess idiosyncratic technological capabilities; this is useful for building and maintaining IoT infrastructure and thus harvesting and processing big data while assuring the interoperability of diverse technologies and data privacy.

In that vein, the five papers illustrate the three types of platforms and their attempts to establish successfully in the emerging platform market (see Figure 2). Furthermore, Figure 2 explicates the interrelations between the three types of platforms. The case studies of the patient innovation 54 and mental health 55 platforms explicate the challenges of establishing new platform services and the unique mechanisms to engage new users and boost the network effect. The patient innovation platform utilizes interactions between MedTech firms and patient innovators, showing the value of collaboration to both parties and facilitating cooperation. The mental health platform uses Big Tech firms’ services such as social media platforms to create safe and trustworthy interactions between the users and enhance their social networking. Platform-born adjacent platforms (such as those created by GAFAM) enjoy market “colonization” by providing data infrastructure to incumbents and new entrants, such as biotech or education startups. 56 In addition, with competition shifting toward data-driven products/services, entrepreneurial activities in many industries are likely to be organized within ecosystems around Big Tech or Incumbent-born platforms that provide access to data and data infrastructure. 57 Finally, incumbent (e.g., MedTech or automotive) born platforms engage born-platform partners to serve as complementors offering IoT infrastructure and customer base. 58

Insights into the coopetitive dynamics of the MSPs of different origins.

Conclusion

The general purpose of the special issue is to stimulate collective discussion among researchers and practitioners on advancing diverse types of MSPs. This introduction aims to explore the growth trajectories of MSPs and how they deal with their go-to-market challenges. Explorative analysis of the five selected papers offers rich insights into the three types of platforms: born-platform, launched by the startups; platform-born adjacent, launched by Big Tech companies; and incumbent-born, launched by incumbent companies operating in diverse business sectors. Platform-born adjacent and incumbent-born platforms are backed by the specific technological capabilities of the parent company. Unique technological capabilities tinge the platform product/service’s design and customer base. Currently, the three identified types of platforms serve each other more as complements in different aspects (e.g., acquiring new technological competencies, data, and customers). However, with rapid market saturation, a dominant design of the platforms can emerge, the “window of opportunity” can narrow, and more intense competition can occur among the types of platforms.

Furthermore, the paper offers a new research avenues by posing some untapped questions. Can value impedance be generalized to the other two types of platforms? How to build the dynamic capabilities of MSPs, develop their competitive advantage, and successfully build alliances within and across different types of platforms? How coopetitive dynamics of the intra- and inter-different platform types, including the incumbents’ strategic choices on new platform business development contributes to the competitive advantage of the platforms? Can MSPs coopetition serve to accelerate network effect and scaling of the healthcare platforms?

Footnotes

Funding

The author(s) received financial support for the research, authorship, and/or publication of this article: The research was supported by European Social Fund (Project No. K71208006) under grant agreement with the Research Council of Lithuania (LMTLT).

Author Biographies

David J. Teece is the Thomas W. Tusher Professor in Global Business at the University of California, Berkeley’s Haas School of Business. He is also faculty director of the school’s Institute for Business Innovation, USA (email:

Asta Pundziene is the Professor of Strategic Management and Organizational Psychology at the School of Economics and Business at Kaunas University of Technology, Lithuania. She also is the Visiting Scholar at the University of California, Berkeley’s Haas School of Business, Institute of Business Innovation, USA (email:

Sohvi Heaton is a Visiting Assistant Professor at Santa Clara University and holds a PhD from the University of Oxford (email:

Maaja Vadi is the Professor of Management at the University of Tartu in Estonia (email: