Abstract

Governments actively court foreign direct investment (FDI) as a tool for economic growth and development. Despite the important role of FDI in the global economy, we do not know how this activity affects election outcomes. Crucially, state and local governments are often responsible for attracting FDI. Although FDI creates jobs, it also generates competition for domestic producers. Drawing on theories of global production, I argue that inward FDI increases the net welfare of voters in the local host economy. Therefore, new investment should increase the electoral success of incumbent parties in local elections. I use new project-level greenfield FDI data to test this claim in the context of Brazilian mayoral elections between 2004 and 2012. I find that the announcement of a new investment project increases the probability that the incumbent party wins reelection. The findings suggest a channel through which globalization directly affects mass politics at the subnational level.

Globalization, with large material consequences for many voters, has the potential to shape mass political behavior in a number of ways. With global inward foreign direct investment (FDI) flows of US$1.56 trillion in 2014, the activity of multinational firms has the ability to significantly influence economic outcomes in host countries. A source of job creation, productivity, economic growth, and greater tax capacity, inward FDI is widely viewed as beneficial and important to development (Moran, Graham, & Blomstrom, 2005). This is particularly likely to be true at the local level. For instance, a Kia Motors manufacturing plant employs approximately 3,000 workers 1 in Harris County, Georgia (population 33,381), 2 while PSA-Peugeot-Citroen employs about 4,000 workers in the Brazilian city of Porto Real 3 (population 18,552). 4 However, there are also costs associated with inward FDI, including increased competition for domestic producers, as well as potential negative impacts on national security, the environment, and levels of corruption (Pinto & Zhu, 2016). Do voters reward or punish incumbents for attracting FDI? Given these competing interests, it is unclear how FDI should influence domestic elections, including voting behavior and support for the government.

Existing accounts of the impact of globalization on elections generally fall into two categories. First, a large comparative politics literature on economic voting has examined the ways in which globalization shapes the accountability of elected leaders to their voters. 5 Scholars have argued that globalization limits the room of governments to manuever 6 or reduces clarity of responsibility for economic outcomes, 7 which together affect the link between economic outcomes and support for incumbents. However, this treatment of globalization as a contextual variable overlooks the fact that globalization affects the welfare of workers directly, in ways that are not accounted for by measures of economic growth or unemployment (Owen & Quinn, 2016). For instance, trade competition affects job security, wages, and the composition of jobs in the economy. To address this gap, a growing literature in international political economy examines the impact of local globalization winners and losers on local support for incumbent parties in U.S. presidential elections (J. B. Jensen, Quinn, & Weymouth, 2017; Margalit, 2011) and polarization in U.S. congressional elections (Autor, Dorn, Hanson, & Majlesi, 2016). This latter group of studies uses county-level measures of globalization winners and losers to explain county-level variation in support for office-holders in national government, highlighting the role of the geographic distribution of winners and losers in shaping mass political behavior.

However, the electoral implications of FDI differ from other aspects of globalization because policy responsibility often lies with subnational governments. Although managing capital market openness is primarily the domain of the national government, 8 subnational governments often have primary responsibility for attracting FDI to their community. Subnational leaders both engage in investment promotion, for instance, offering tax and fiscal incentives (e.g., Baccini, Li, & Mirkina, 2014; N. M. Jensen, Malesky, & Walsh, 2015; Li, 2016; McMillan, 2012; Rodríguez-Pose & Arbix, 2001; Thomas, 2007), and set local policies that shape the local economic environment and thus, the likelihood a multinational will invest (e.g., infrastructure, corruption, skill of the labor force, etc.). Indeed, research suggests elected officials have political motivations to offer incentives (N. M. Jensen et al., 2014) and that elected mayors offer more investment incentives than appointed ones (N. M. Jensen et al., 2015). This is the case even though incentives typically are an unimportant factor in location decisions, and indeed may be redundant (e.g., N. M. Jensen, 2017).

When we consider subnational politics, variation in the geographic distribution of globalization winners and losers across political units has important consequences for the impact of inward FDI on elections. Critically, there are likely to be important differences between the geographic location of winners and losers from inward FDI and political boundaries at the subnational level. 9 For example, consider how foreign auto manufacturing plants in the United States create opportunities for workers in cities in southern states (e.g., Kia in Harris County, Georgia), while simultaneously increasing competition that harms workers and capital owners in other cities (e.g., the Big Three automakers in Detroit). Located in Detroit, workers hurt by increased competition are not constituents of, and thus do not influence electoral support for, mayors in Harris County. Because of these geographic considerations, emphasis on national level aggregates may miss how globalization pressures shape domestic politics.

Although other papers have examined the calculus of offering incentives, this article is the first to ask whether voters reward incumbent parties for successfully attracting greenfield investment projects. Drawing on theories of global production, I argue that locally, the benefits to inward FDI are greater than the costs, and thus we should expect voters on net to view local FDI favorably. If state and local governments influence the inflow of capital and plausibly claim credit for attracting these investors, then we should expect to see support for local governments connected to inflows. I therefore hypothesize that inward FDI will be associated with greater electoral support for the incumbent party.

To test this theory, I evaluate how inward FDI affects electoral support for incumbent parties in Brazilian mayoral elections. Brazil is an appropriate case because Brazil relies heavily on foreign capital, and as a decentralized system, local governments have policy discretion in attracting FDI. 10 I use new data on local greenfield investment projects from the fDi Markets database in combination with data on municipal elections in 2004, 2008, and 2012. To ensure that those municipalities “treated” with an FDI project are comparable with those that are not treated and to ensure that there are not confounders driving both the prospect of reelection and the likelihood of an FDI project, I examine various subsamples of municipalities (Achen, 2002; Keele, 2015) and utilize coarsened exact matching. I find that greenfield investment has a substantively large and statistically significant effect on the electoral performance of the party of the incumbent mayor, especially in municipalities with a population below 200,000 (approximately 5,535 of Brazil’s 5,570 municipalities). The findings of this article introduce a new dimension to the literature on the mass politics of globalization, and also speak to literatures in comparative politics on Brazilian municipal elections (e.g., Brambor & Ceneviva, 2011; Brollo & Nannicini, 2012; Ferraz & Finan, 2008; Gingerich, 2014; Klašnja & Titiunik, 2017; Sakurai & Menezes-Filho, 2008) and economic voting at the local level (e.g., Dassonneville, Claes, & Lewis-Beck, 2016; Fauvelle-Aymar & Lewis-Beck, 2011; Vermeir & Heyndels, 2006).

Existing Literature: The Distributional Consequences of Inward FDI

FDI occurs when a multinational firm makes a lasting investment in the host country, either through the construction of new physical assets or the acquisition of a significant portion of the stock (at least 10%) of an existing facility. Greenfield investment involves the creation of new assets (e.g., the construction of a new facility or expansion of an existing facility), while mergers and acquisitions represent the transfer of existing assets to the multinational investor.

FDI is attractive to host countries for a number of reasons. First, the entry of multinational firms may provide spillovers to domestic firms in the form of productivity, technology, and knowledge (e.g., Göorg & Greenaway, 2004; Göorg & Strobl, 2005; Poole, 2013). 11 Second, FDI is widely viewed as an important source of economic development and growth (e.g., Organisation for Economic Co-operation and Development, 2002). The impact of FDI on productivity via transfers/spillovers of knowledge and technology is a key channel through which FDI improves local economic outcomes (Blonigen & Wang, 2005; Moran et al., 2005; Narula & Dunning, 2010).

Although there are benefits to FDI for the economy as a whole, the entrance of foreign firms also creates winners and losers. Much of the political economy literature draws on canonical models of trade to understand the distributional consequences of inward FDI. Simply put, in these models, the entrance of foreign capital changes the relative demand for factors, which impacts factor returns. First, the entrance of a foreign firm increases demand for workers, raising wages. Second, the increase in labor demand causes competition in factor markets and forces domestic firms to pay higher wages. Finally, the entry of foreign capital increases competition for domestic firms, reducing profits and therefore returns to domestic capital. In the Heckscher–Ohlin model, all factors are assumed to be fully mobile and thus inward FDI benefits domestic labor and hurts domestic capital. 12 Therefore, we would expect workers to view inward FDI favorably and domestic capital to view it unfavorably. Similar preferences are predicted by specific-factors models of FDI (e.g., Pandya, 2010; Pandya, 2014b).

The preceding models suggest the clear prediction that labor wins and domestic capital loses. However, other theories of trade and FDI offer alternative expectations. In a variation of the specific-factors model, the distributional consequences of FDI depend on whether foreign capital is a complement to or substitute for labor (N. M. Jensen et al., 2012; Pinto, 2013; Pinto & Pinto, 2008). 13 According to new new trade theory, multinationals, as the most productive firms (Helpman, 2006), will hire more skilled, high ability workers relative to domestic firms. Thus, inward FDI would benefit more skilled workers. Domestic producers would face similar disadvantages as in the above models. Yet even these more nuanced models do not fully capture the distributional pressures of FDI in the context of global production networks.

Theory: FDI and Local Elections

When subnational governments are responsible for attracting FDI, inward FDI has the potential to shape electoral outcomes at the subnational level. Within countries, the geographic distribution of winners and losers from FDI cuts across political boundaries. Thus, we must consider the composition of winners and losers within local political jurisdictions. I argue that from the perspective of local elected officials, the benefits of FDI are concentrated among voters, while the costs of inward FDI are shared across (or even located primarily in other) political units. Therefore, local inward FDI should lead to increased electoral support for incumbents.

Local Winners and Losers

Drawing on theories of global production, I argue that the distributional consequences of FDI are heterogeneous for both workers and domestic producers. With respect to labor, the entrance of new foreign firms and expansion of existing ones through greenfield investment creates new local jobs 14 and thus increases demand for workers regardless of sector or technology. 15 However, in contrast to the canonical models, all workers may not benefit from inward FDI. 16 Instead, the nature of global production is such that there are direct and indirect effects of inward FDI on the welfare of workers (Dunning & Lundan, 2008, p. 437).

The direct beneficiaries of greenfield investment are those workers employed by the multinational at its new foreign affiliate. In addition to the new employment opportunities, multinational jobs tend to be good jobs relative to jobs in domestic firms. First, multinationals tend to pay higher wages than nonmultinationals. 17 Second, working conditions may be better in the multinational affiliate compared with local plants. 18 For these reasons, greenfield investment directly benefits workers employed by the multinational, creating voters who are likely to view inward FDI favorably.

Inward FDI also indirectly benefits workers who experience an increase in labor demand through upstream, downstream, or support linkages with the investment. When a multinational enters the local economy, it often creates linkages with domestic firms, which may increase demand for intermediate inputs and contribute to the development of the industry (Göorg & Strobl, 2004; Markusen & Venables, 1999). As a result, workers employed in related industries, and especially those employed by firms that are in a contractual relationship with the multinational, will see an increase in demand for their labor. The construction of the new facility also generates demand for supporting industries. Thus, local workers not directly employed by the multinational may also benefit from the investment, creating an additional set of voters inclined to view investment favorably. 19

Finally, under certain conditions, FDI can create wages spillovers to other workers in the local labor market as a result of increased labor demand as anticipated by the canonical models. This generates additional indirect beneficiaries in the labor market. Depending on labor market mobility, this could be limited to certain markets in which the multinational is active, or spillover over to the economy more broadly if labor is mobile. Although there is abundant evidence that multinational corporations (MNCs) offer higher wages, evidence of wage spillovers is more limited, 20 especially at the local level. 21

Although the effects of inward FDI on workers at the local level are generally neutral to positive, the welfare considerations for domestic capital are more mixed. The canonical models uniformly anticipate that inward FDI will reduce the returns to domestic capital.

However, domestic producers are heterogeneous in terms of their integration in the global economy and vertical production networks, and thus domestic capital has heterogeneous preferences with respect to globalization (Crystal, 1998, 2003; Manger, 2009; Milner, 1988). On one hand, as previously stated, inward FDI creates competition for, and may crowd out, domestic producers competing in the same markets (Crystal, 1998, 2003; Owen, 2013, 2015; Pandya 2014a, 2014b; Pinto, 2013; Pinto & Pinto, 2008). Domestic capital owners facing competition from a multinational are likely to view inward FDI unfavorably.

On the other hand, some domestic producers may benefit from inward FDI through upstream or downstream linkages to the multinational (Markusen & Venables, 1999). 22 In particular, when a multinational develops relationships with local producers of intermediate inputs, this will increase profits for those suppliers. Moreover, domestic firms linked to the multinational through vertical supply relationships may benefit from spillovers of technology which improve their products and also create access to cheaper inputs (Markusen & Venables, 1999). Thus, inward FDI can create interests among domestic capital owners in the local economy both in favor of or in opposition to inward FDI. As a result, the distributional consequences anticipated by global production theory differ from both factor- and industry-based models, which predict homogeneous distributional consequences within factor groups or industries.

Aggregate Local Interests

Given that greenfield FDI benefits some individuals and harms others, how does a local constituency in aggregate view FDI? The distribution of interests across political units has important implications for the impact of inward FDI on support for the government. Although we cannot know for certain the net position of a constituency with respect an FDI project, I argue that there are several reasons to expect that local winners will outnumber losers. As a result, inward FDI is likely to be associated with increased support for the incumbent.

First, labor market winners are more likely concentrated in the local community, while domestic capital winners and losers are less restricted to a specific location. In particular, labor market winners are constrained geographically, and thus they are more likely to be a part of the mayor’s constituency. 23 Survey evidence from Latin America suggests generally favorable views of FDI; for instance, Pandya (2010) finds that support for FDI is high among skilled workers and opposition is generally low across workers of all skill levels. 24 In contrast, there is no reason to expect that domestic capital interests must be similarly geographically constrained; domestic capital interests, both winners and losers, could as easily be located outside the constituency of the local politician seeking reelection as inside the constituency. Second, it is unlikely that those negatively affected by an investment project would offset the beneficiaries locally because elected officials and potential multinational investors are strategic actors. Political leaders motivated by reelection or future office aspirations are unlikely to court investment by a foreign multinational that would harm local business interests. Similarly, potential investors are likely to try to locate foreign affiliates in welcoming rather than hostile locations, and thus greenfield investment is more likely to go where it is wanted. 25 Even if there is geographic concentration of a particular industry in a region, this does not necessarily imply there will be political concentration in one particular local political unit (Busch & Reinhardt, 1999). Together, these factors make it unlikely that losers from a particular investment project would be politically concentrated in the mayor’s constituency in such large numbers that it would shift net sentiment toward opposition to the investment.

If, as I argue, the net position of the local constituency is likely to benefit from FDI, then we should expect to see that an FDI project is associated with an increase in support for the incumbent. Unlike other policies governing globalization, subnational leaders play an important role in pursuing policies to attract investment (directly through incentives, and indirectly through economic policies). This responsibility should increase the link between the economic outcome and political accountability (Hellwig, 2014). This leads to the following hypothesis:

Alternative Explanations

There are several alternative considerations that could shape voters’ responses to inward FDI. First, there are a number of theories that would suggest a negative relationship between FDI and support for the incumbent party. Although the above theory focuses on the ways in which local FDI benefits (some) workers, inward FDI also increases volatility in the labor market, thus reducing job security (Scheve & Slaughter, 2004). Moreover, FDI can increase income inequality between skilled and unskilled workers (e.g., Dunning & Lundan, 2008; Feenstra & Hanson, 1996). Voters may also respond negatively to the proposed incentive if costly incentives are offered to the multinational firm. 26 Inward FDI can raise concerns about national security (e.g., Graham & Krugman, 1994; Graham & Marchick, 2006; Kang, 1997), 27 pollution (e.g., Waldkirch & Gopinath, 2008), or corruption (Pinto & Zhu, 2016). 28 To the extent that any of the above are true, greenfield FDI is less likely to be associated with increased support for the incumbent and thus, empirically, I would be less likely to find support for my hypothesis.

Second, we must also consider the possibility that the effect of FDI on electoral support is conditional upon the extent to which benefits to labor depend on whether foreign capital is labor-complementing or labor-substituting (Pinto & Pinto, 2008). To address this concern, I measure FDI as the number of jobs created by a project (in levels and as a share of the local population) to explicitly model the anticipated benefits to labor. I also consider the impact of only manufacturing investments on electoral support to reduce heterogeneity in benefits to workers across sectors.

Third, greenfield FDI could be associated with an electoral boost for the incumbent party if voters view an investment project as a signal that the leader is competent (particularly given competition for these projects), rather than evaluate inward FDI in terms of strictly personal pocketbook considerations. With aggregate data on vote share, it is not possible to determine the extent to which governments that attract FDI derive support from the personal material interests articulated in my theory or other considerations like a signal of competence. As I demonstrate in robustness checks, larger investment projects in terms of jobs created do generate more support for the incumbent, suggesting that the material considerations do play a role in how voters evaluate incumbents. Of course, material interests and signals of competence are not mutually exclusive. As a result, evaluating these competing mechanisms is an important topic for future research.

Finally, one may question what, if anything, is special about foreign investment relative to domestic investment, and whether we should expect domestic investment to generate similar support for incumbent parties. A new manufacturing plant regardless of firm ownership, will create jobs and a provide a boost to the local economy. Indeed, Hong and Park (2014) find targeted industrial development generated electoral gains in authoritarian legislative elections in Korea and Taiwan. As discussed above, however, attracting multinational investment specifically is expected to provide a number of extra benefits relative to the benefits from investment by domestic firms, including higher wages, greater productivity, and spillovers to domestic firms. Moreover, FDI is important source of capital for capital scarce countries, including Brazil. Thus, it is my position that there are unique electoral effects associated with attracting greenfield FDI. In the supplemental appendix, I control for local business activity as a proxy for domestic investment to address this concern.

Context: FDI and Elections in Brazil

Brazil is a good case to test this theory for several reasons. First, FDI is an important source of capital for Brazil. 29 Second, for inward FDI to influence voters’ support of the incumbent, the government must have policy autonomy and responsibility over the outcome. 30 Brazil is a multiparty presidential democracy, divided into 27 states (including the Federal District) and 5,570 municipalities. After democratization and a new constitution in 1988, the federal government of Brazil decentralized, devolving power to state and local governments to make decisions over spending, provision of services, tax rates, and other policies. Thus, subnational governments (state and local) have primary responsibility for attracting investment through direct and indirect policy measures. 31

Governments at all levels engage in investment promotion, often through the use of incentives, and Brazil is no exception. Both state and municipal governments in Brazil offer fiscal, financial and other incentives (e.g., regulatory). Summarizing existing research, Rodríguez-Pose and Arbix (2001) suggest that “the prosperity of each region and locality is increasingly perceived to be dependent on the capacity of each place to attract increasingly ‘footloose’ FDI” (p. 136). Within Brazil, state and municipal governments compete to attract FDI (Christiansen, Oman, & Charlton, 2003; da Motta Veiga, 2004; Oman, 2000; Thomas, 2007). 32 In many cases, a municipal government will cooperate with the state government to compete against cities in other states (Oman, 2000; Thomas, 2011). For example, the city of Juiz da Fora, together with the state of Minas Gerais, offered Mercedes-Benz incentives totaling approximately US$340,000 per job for an investment slated to generate 1,500 jobs; this included major infrastructure development supported by the municipal government (Christiansen et al., 2003, p. 16). Although state governments generally have greater ability to offer tax incentives (based on higher value added tax [VAT] rates) and financial incentives (larger budgets) than local governments, municipalities also offer tax incentives for local taxes (on services and real estate) in addition to financial and other incentives (e.g., land for the project site and utilities concessions).

Moreover, municipalities have a large degree of control and policy autonomy over other determinants of investment. Indeed, although incentives can be used to claim credit for investment (N. M. Jensen et al., 2014), evidence from a number of academic studies shows that incentives are not the only or even most important determinant of multinational firms’ locational decisions in general (for review, see N. M. Jensen, 2017), or in the case of Brazil specifically (Rodríguez-Pose & Arbix, 2001). Instead, the economic environment, quality of infrastructure, education of the labor force, wage costs, and market size are more important determinants of locational decisions. As a result of decentralization, municipalities have a large degree of control and discretion over these policy choices. Thus, municipalities have an important role to play in shaping the likelihood of attracting FDI. As such, it is likely that voters reward mayors for good outcomes and punish bad outcomes (Martins & Francisco, 2013).

I focus on the electoral effects of FDI at the municipal level. In addition to role that municipal governments play in shaping the likelihood of investment, municipalities are the most disaggregated administrative division 33 and the distributional consequences posited above are sharpest for local labor markets. Municipalities are governed by a mayor and city council. During the period of analysis in this article, mayors are limited to two consecutive terms in office (though it is not uncommon for ex-mayors to run again after sitting out one term). In all but the largest municipalities (less than 200,000 inhabitants), mayors are elected by plurality rule. In large municipalities (more than 200,000 inhabitants), there is a runoff between the two candidates with the most votes if no candidate receives a majority of votes in the first round. Voting in Brazil is mandatory for those between the ages of 18 and 70, so turnout tends to be higher than might be expected in local elections, compared with, say, the United States.

Anecdotal evidence from Brazil suggests that local mayors do link their ability to attract FDI to electoral support. For instance, the signing of a memorandum of understanding to invest between a municipality and a multinational is often accompanied by a ceremony, photo-op, and story in the local paper. There are additional ceremonies to celebrate groundbreaking and the opening of the facility. Investments and the associated jobs are often reported on the mayor’s website. All of these activities support the efforts of the mayor to claim credit for attracting desirable investment and facilitating the creation of jobs and local economic development. This also occurs during election campaigns. As one example, Barjas Negri, the mayor of Piracicaba from 2005 to 2012, engaged in investment promotion activities, which most notably resulted in a large Hyundai plant. When Negri ran for his old seat in 2016 (after sitting out due to term limits), he emphasized the impact of his economic development plans including industrial parks and incentives to foreign investors on the community on a number of platforms, including YouTube, 34 Facebook, and Twitter. 35

How does the research design address the possibility of that both the state and local government are responsible for attracting an FDI project? Municipal elections are held every 4 years, and are offset from national and state elections. Because elections are staggered, this reduces concerns about local mayors riding on the coattails of higher ticket offices (e.g., Fauvelle-Aymar & Lewis-Beck, 2011; Marien, Dassonneville, & Hooghe, 2015). As such, it poses a cleaner test of the performance of the incumbent party of the mayor with respect to FDI. In addition, if there is cooperation between state and local governments to attract FDI, staggered elections allow incumbent parties at both levels to claim credit without directly competing for it. In other words, voters could presumably increase support for incumbents in both elections. However, if voters view only the governor as responsible for investment, then empirically we should see no effect of FDI on local elections. In robustness checks, I look at only FDI projects announced in the year preceding the election, so there is no opportunity for competing credit claiming by the governor in the election. Furthermore, I find no evidence that the effect of FDI on support for the incumbent mayor’s party depends on whether the governor and incumbent mayor are members of the same party or different ones. 36

Data and Method

To systematically test my hypothesis that greenfield investment increases the electoral success of incumbent parties, I examine incumbent party reelection in mayoral elections for the years 2004, 2008, and 2012. In line with previous studies of mayoral elections in Brazil, I examine the likelihood that the incumbent party wins the election because term limits generate turnover of individual candidates. Thus, the sample includes those municipalities in which the incumbent party fields a candidate. 37 For robustness, I examine the impact of FDI on the likelihood of reelection, conditional on the decision to run for reelection. For additional recent analyses of incumbency advantage and disadvantage in Brazil, see De Magalhaes (2015) and Klašnja and Titiunik (2017).

Data

Dependent variable

I measure electoral performance as the probability the incumbent party wins the election. Thus, the dependent variable is equal to one if the mayor or his or her party wins the election and zero if the mayor or his or her party loses. The data are available from the Tribunal Superior Eleitoral.

Independent variable

The independent variable of interest is greenfield investment activity, collected from the fDi Markets database. Because the measure of greenfield investment is a central focus of the article, I discuss these data in detail. To my knowledge, these data have not yet been used in published political science research. Data on individual investment projects are collected from (more than 9,000) media sources, internal information sources at the Financial Times, reports from industry organizations, and investment agencies, market research, and publication companies (fDi Markets, 2015). Before projects are included in the database, announcements go through a quality control process which confirms the existence of the project using multiple sources. The data include cross-border investments in new physical projects or the expansion of existing facilities, but not cross-border mergers and acquisitions. This is appropriate for this article (a) because greenfield investment is more likely to be visible and viewed favorably than M&A activity, which is more likely to generate nationalistic concerns, and (b) also because greenfield FDI requires an explicit location decision (whereas M&A activity is limited by the location of existing assets).

I match information on announced projects to data on municipal election returns. The greenfield FDI data are available beginning in January 2003. Thus, the analysis of the 2004 election covers projects announced between January 2003 and September 2004. The analysis of the 2008 election includes projects announced between January 2005 and September 2008 and the analysis of the 2012 election includes projects from January 2009 to September 2012. Because elections are held in early October in Brazil, any projects announced in final quarter of the election year coded as zero.

There are 1,938 projects for which a municipality is identified in the database. The main measure of FDI activity is a dummy variable indicating at least one announced greenfield investment project during the mayor’s term. Attracting FDI is a relatively rare event. Of the 5,570 municipalities, only 219 unique municipalities attract at least one investment project during the sample period. A map of projects is provided in the supplemental appendix. This corresponds to a rate of investment of 2.4% in the largest estimation sample. I use a dummy variable to indicate at least one project rather than a count of projects because the number of projects is highly skewed by a few municipalities that receive a large number of projects. The primary analysis compares elections in which the party of the incumbent attracted at least one investment project to those municipalities in which the incumbent party did not attract any greenfield investment during the term.

In robustness checks, I examine three alternative measures of FDI. First, to capture the magnitude or size of the investment, I measure FDI as the number of jobs to be created by the project. 38 The measure of job creation is based on estimates made by the multinational company where such estimates are available. In cases where information is missing, fDi Markets uses an algorithm to estimate the size of these effects. For this reason, I consider the dummy variable on whether a project was announced to be a more reliable measure, with a lower possibility for measurement error.

Second, I look at the impact of greenfield investment in only manufacturing activities to reduce heterogeneity across different sectors (e.g., some sectors may be more politically sensitive or provide more benefits to workers). In my data set, investment in manufacturing activity accounts for approximately 36% of all investment in Brazil and thus constitutes the largest sector of investment.

Third, I examine the impact of FDI on reelection when only projects announced in the year leading up to the election are included. The data capture announced and verified projects, but not how long it takes to move from announcement to operational affiliate. Depending on the project, it could take several years to build a plant. For the purpose of this article, the announcement of the project itself has political value to incumbents seeking reelection. However by looking at only recent announcements, we have more homogeneity in terms of the stage of the project.

Control variables and summary statistics

I include several economic and political controls suggested by the literature on economic voting. The main economic controls are real GDP growth and local government spending. Real GDP growth during the previous year is a measure of local economic conditions. 39 These data are collected from the IBGE (Instituto Brasilerio de Geografia e Estat’ıstica). I measure total government spending at the municipal level on a per capita basis (in 2000 constant reais). This variable is logged to account for skewness and the data are available from the Ministry of Finance. I expect each of these variables to have a positive effect on the probability of reelection.

I include several political controls collected from the Tribunal Superior Eleitoral. First, I include dummy variables to indicate (a) whether the incumbent party is aligned with the president and (b) whether the incumbent party is aligned with the governor, to account for possible electoral shifts due to federal or state politics. Second, I include the partisanship of the incumbent party following the classification developed by Power and Zucco (2009) to account for possible partisan-based shifts in support. I include dummy variables for Left, Right, and Other parties, while Center parties serve as the reference category. Third, I include several election-specific control variables. I include a dummy variable equal to one if the election included a run-off and a dummy variable equal to one if the candidate is the incumbent mayor (compared with a new candidate running on the incumbent party ticket). I expect both of these variables to have a positive effect on the probability of reelection. As a measure of the level of competition, I include the number of candidates for mayor (logged to account for skewness). I expect this variable to have a negative effect on the probability of reelection.

Finally, I include a number of municipal controls suggested by the literature on Brazilian elections (e.g., Brollo & Nannicini, 2012; Ferraz & Finan, 2008; Gingerich, 2014; Sakurai & Menezes-Filho, 2008). Specifically, I include the one year lag of the following variables to account for possible unobserved heterogeneity across municipalities: the log of oil royalties received by the municipality, and the logs of population and population density. I include the log of oil royalties to control for the fact that some municipalities, primarily coastal ones, benefited from an oil price boom in the early 2000s (Gingerich, 2014). This could benefit incumbents who had larger budgets as a result (Campello & Zucco, 2016), and could also be related to the likelihood of receiving an FDI project (particularly in the resource sector). Population and population density are common controls in the Brazil municipal elections literature as a means of controlling for unobserved heterogeneity when municipal fixed effects are not appropriate. 40 In particular, large and small, as well as urban and rural municipalities may differ in a number of respects including propensity for receiving investment. Summary statistics, additional details on data sources and a correlation matrix are provided in the supplemental appendix.

Model Specification and Estimation

I estimate the probability of reelection using logistic regression. I include both year and state fixed effects and utilize standard errors clustered by municipality.

One major concern in terms of research design is whether municipalities receiving investment can be compared with those that do not receive investment, especially given that FDI at the local level is a rare event. Thus, it is important to ensure that the “treatment” and “control” groups are as similar as possible. In an ideal world, we would follow a research design similar to that of Greenstone, Hornbeck, and Moretti (2010), who estimate spillovers by looking at municipalities that received a million dollar plant, compared with those municipalities that barely lost the bid for the plant. Such a design is not possible in this context and thus I follow two second-best approaches. First, following the advice of Achen (2002) to make the sample as homogeneous as possible, I consider two subsamples of the data (and a third subsample in the supplemental appendix). Second, I examine a matched sample based on coarsened exact matching.

In the first subsample, I limit my analysis to those municipalities that have a population less than 1 million. This includes all but 13 of Brazil’s 5,570 municipalities. I exclude municipalities with a population above 1 million because all of these municipalities receive greenfield investment and thus there is no control group for comparison. This is the most general sample that still maintains common support for treatment and control groups in terms of population.

In the second subsample, I examine those municipalities with a population of less than 200,000. This includes 98.1% of Brazil’s municipalities. In Brazil, these small municipalities have different electoral rules than large ones, with mayors elected via plurality vote. Smaller municipalities are also more likely to be homogeneous in terms of propensity to receive investment.

Third, I perform coarsened exact matching (Iacus, King, & Porro, 2012) among the sample of small municipalities. 41 To determine which variables to match on, I look at the site selection literature (e.g., Greenstone et al., 2010) and the literature on Brazilian municipalities. I select several pretreatment variables: population, population density, GDP per capita, and the illiteracy rate. Each of these continuous variables is coarsened into five strata based on the 25th, 50th, 75th, and 90th percentiles. I also exact match based on the five regions of Brazil. Overall imbalance is reduced from 0.995 to 0.782, which is a reduction of 21.3%. 42 The matched sample has 974 observations, broken into 125 treatment and 849 control units. I discuss this procedure, sample, and results from additional matching procedures in greater detail in the supplemental appendix.

Results

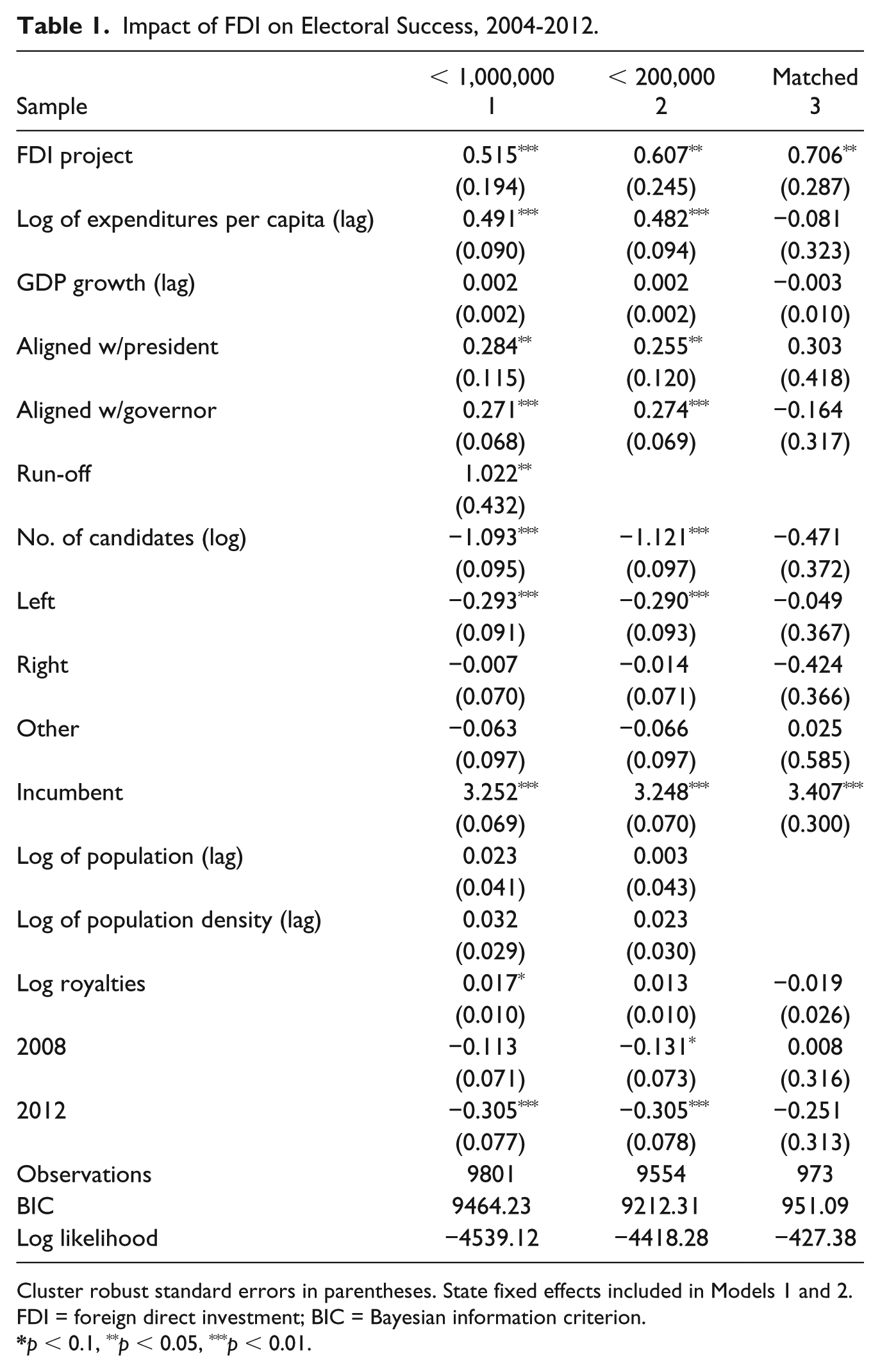

The main results for the logistic regression analysis of the reelection of the incumbent party are presented in Table 1. Before discussing each model individually, I note that the results in all samples support the hypothesis that attracting FDI increases the probability of reelection of the incumbent party. The coefficient on greenfield investment is positive and statistically significant, and of a similar magnitude, in all models. The marginal effect of FDI on the probability of reelection for each model in Table 1 is plotted in Figure 1.

Impact of FDI on Electoral Success, 2004-2012.

Cluster robust standard errors in parentheses. State fixed effects included in Models 1 and 2.

FDI = foreign direct investment; BIC = Bayesian information criterion.

p < 0.1, **p < 0.05, ***p < 0.01.

Marginal effect of FDI on probability of reelection.

In Model 1, I include all municipalities with a population below 1,000,000. The coefficient on FDI is positive and statistically significant as hypothesized. Attracting an FDI project increases the probability of reelection by 10%. This is a substantively as well as statistically significant effect. 43

In terms of control variables, the coefficient on per capita spending is positive and statistically significant, suggesting that higher levels of government spending increase the probability of incumbent party reelection, consistent with other findings in the literature (e.g., Sakurai & Menezes-Filho, 2008). The coefficient on growth in GDP is not statistically significant. This may be due to the fact that it is difficult for voters to assign responsibility for local economic outcomes to mayors, as opposed to the state or federal government.

Several of the political control variables have a statistically significant effect on the probability of reelection. The coefficient on alignment with the governor is positive and statistically significant, suggesting that mayors aligned with the governor are more likely to be reelected than those mayors that are not aligned with the governor. Similarly, the coefficient on alignment with the president is positive and statistically significant as well. The coefficient on whether there was a run-off is also positive and statistically significant. For comparison to the main effect of interest, the marginal effects of alignment with the president and governor are 0.056 and 0.054, respectively. 44 The coefficient on incumbent mayors is positive and statistically significant. The marginal effect is 0.480, which indicates a large incumbency advantage relative to mayors running for their first term on the ticket of the incumbent party. 45 The coefficient on the number of competitors is negative and statistically significant. As the number of competitors increases, the probability the incumbent party wins reelection decreases. Left parties are less likely to be reelected than Center parties, all else equal. Finally, among the remaining controls for population, population density, and oil royalties, only the coefficient on the log of oil royalties is positive and statistically significant at the 90% level. Overall, the model fits the data well, correctly predicting 79.3% of observations (modal prediction: 53.8%).

In Model 2, I limit the sample to those municipalities with populations below 200,000. The coefficient on FDI is again positive and statistically significant. Attracting an FDI project increases the probability of reelection by 0.120, 46 in other words, by approximately 12%. The control variables have a similar effect to those in Model 1, with the exception of oil royalties which is not statistically different from zero. The model again fits the data well, correctly predicting 79.4% of observations (modal prediction: 53.8%).

Finally, in Model 3, I present the results of the estimation for the matched sample. The coefficient on FDI is positive and statistically different from zero. Attracting an investment project increases the probability of reelection by 0.122, 47 or 12.2%. Among the control variables, only the coefficient on incumbent status is statistically different from zero. The model fits the data well, correctly predicting 82.5% of the observations (modal prediction: 50.3%).

Robustness

In this section, I present several robustness checks and discuss additional analysis presented in supplemental appendix. In the interest of space, I present the results only for small municipalities (those with a population below 200,000). I choose to present these results because this set of municipalities is clearly defined by having the same electoral rules. However, the findings are robust in other samples and all results are available in the supplemental appendix.

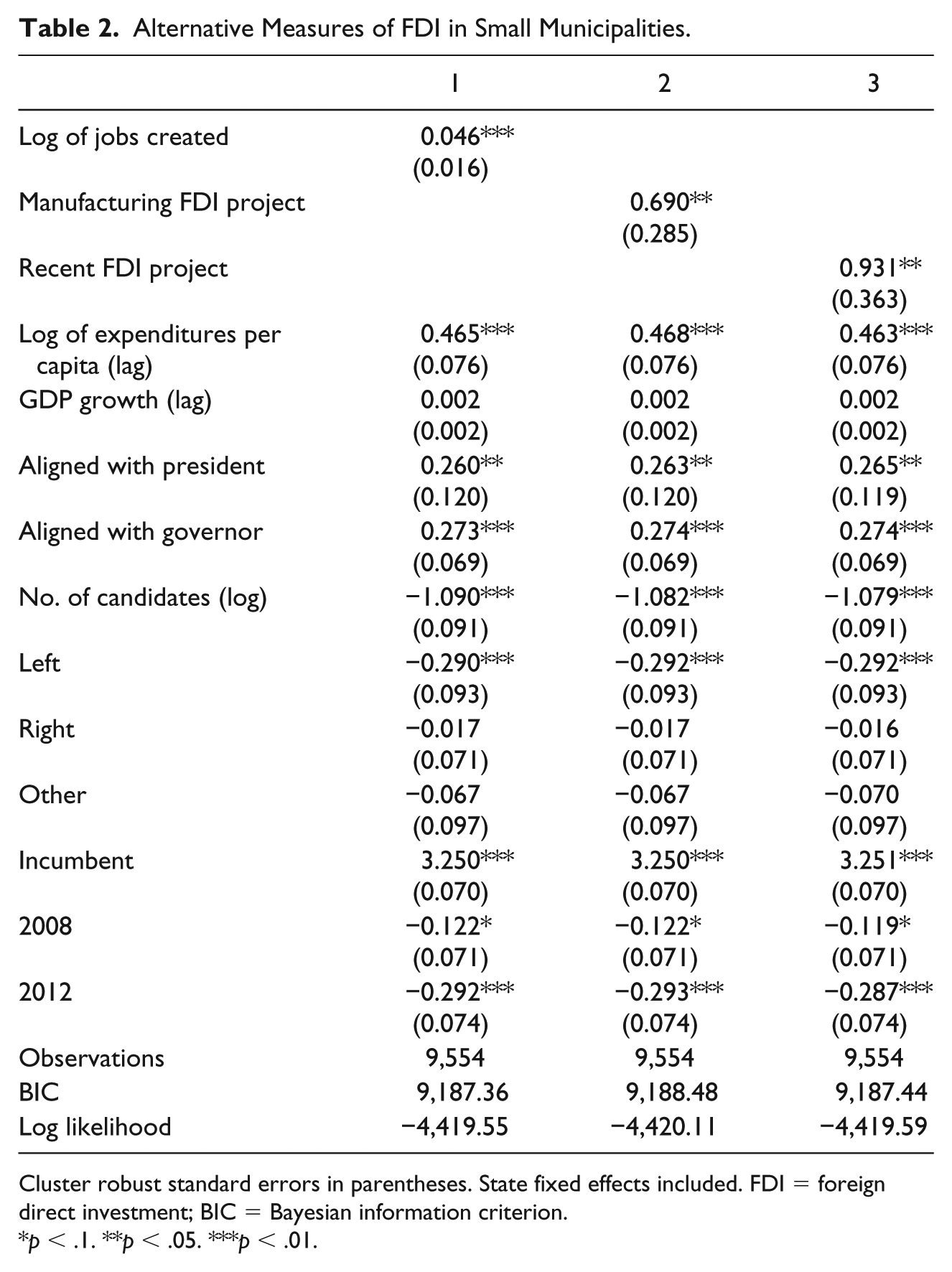

In Table 2, I examine the robustness of the findings to alternative measures of the independent variable. First, I examine the impact of FDI measured by the log of the number of jobs (plus 0.0001) created from the investment project. This allows the impact of FDI to vary by the size of the project. The coefficient on the number of jobs is positive and statistically different from zero, suggesting that incumbents who attract larger investment projects (in terms of jobs created) are more likely to be reelected. In Model 2, I measure FDI using a dummy variable equal to one for municipalities that attracted a manufacturing investment project. This controls for variation across sectors as discussed above. The coefficient on manufacturing FDI is positive and statistically significant. The marginal effect is 0.136, 48 suggesting that incumbent parties are 13.6% more likely to win reelection if they attract a manufacturing investment project. In Model 3, I measure FDI using a dummy variable equal to one for an investment project in the 12 months leading up to the election. This accounts for variation in announcement timing the stage of the project. The marginal effect is 0.184, 49 suggesting that a recent investment increases the probability the incumbent wins reelection by 18.4%. This finding also suggests that the more recent projects have a larger impact on reelection outcomes than projects announced earlier in the term.

Alternative Measures of FDI in Small Municipalities.

Cluster robust standard errors in parentheses. State fixed effects included. FDI = foreign direct investment; BIC = Bayesian information criterion.

p < .1. **p < .05. ***p < .01.

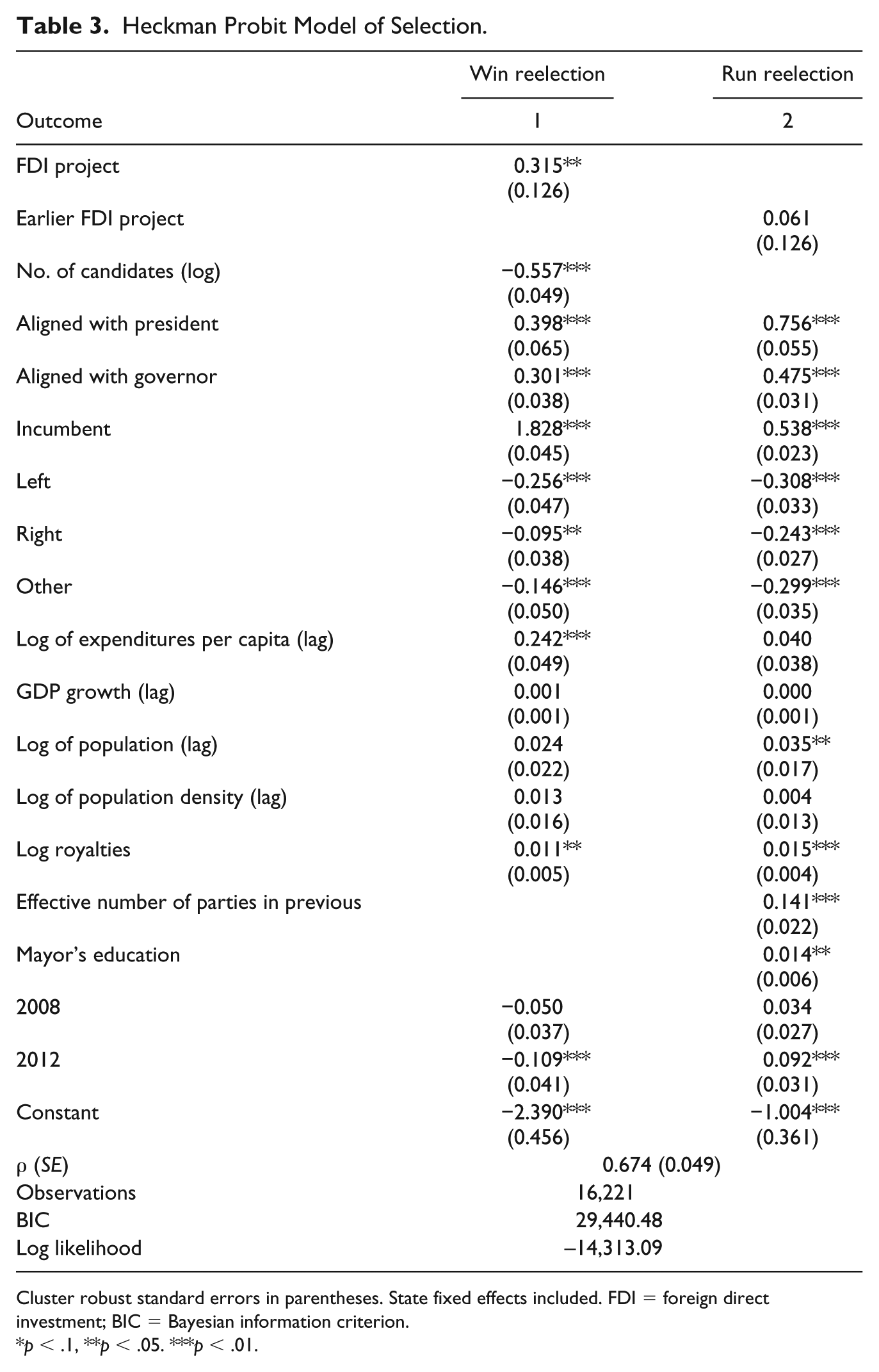

In Table 3, I present a selection model in which the impact of FDI on the probability of reelection is conditional on the decision to run for reelection; this accounts for the possibility that certain variables influence the decision to run, the likelihood of winning or both outcomes. I estimate a Heckman probit model because outcomes at the first and second stage are binary. The first stage models the decision of the incumbent party to field a candidate, while the second stage models the likelihood of winning reelection. I draw on similar models estimated by dos Anjos and Barberia (2016) and Pereira and Melo (2015) to specify the selection equation. First, in the selection equation, I measure FDI using a dummy variable equal to one if the municipality attracted a greenfield investment project in the first 3 years of the term. Thus announcements of investment before campaign filing deadlines are allowed to influence the decision of the incumbent party to run. I also control for mayors’ education as an indicator of candidate quality. Finally, I control for the municipal characteristics of population, population density and oil royalties (all lagged 1 year). I include the effective number of parties in the previous election as a measure of competitiveness of the district (dos Anjos & Barberia, 2016). This variable is also used to satisfy the exclusion restriction.

Heckman Probit Model of Selection.

Cluster robust standard errors in parentheses. State fixed effects included. FDI = foreign direct investment; BIC = Bayesian information criterion.

p < .1, **p < .05. ***p < .01.

The results for the outcome stage are presented in column 1 of Table 3 and the results for the selection stage are presented in column 2. The results suggest that the two equations are related; the Wald test rejects the null hypothesis of independence. Overall, the results in the outcome stage are similar to the models that do not account for selection. In particular, the coefficient on greenfield investment is again positive and statistically different from zero, suggesting that incumbents that attract investment are more likely to win reelection. The marginal effect of 0.069 suggests that incumbents are 6.9% more likely to win reelection if they attract FDI. 50 This effect is slightly smaller in magnitude than the unconditional estimates presented in Model 2 of Table 1.

Turning to the selection equation, the coefficient on early FDI announcements is not statistically different from zero. Eligible incumbents (compared with a new candidate on the incumbent party ticket), as well as mayors aligned with the president and governor are more likely to run for reelection. Mayors that have a higher level of education are also more likely to run for reelection, as are mayors from larger districts (in terms of population) and that received more oil royalties. In contrast to expectations, the coefficient on district competitiveness (effective number of parties in the previous election) is positive and statistically significant. Spending and economic growth do not appear to influence the decision to run.

Overall, the results provide evidence of a robust and substantively significant effect of inward FDI on the electoral success of the incumbent party in mayoral elections. In the supplemental appendix, I present a number of additional analyses. I present results without any covariates. I look at a subset of close races and a subset of municipalities based on the probability of receiving FDI. In terms of additional confounders, I control for the spatial lag of FDI and the impact of formal sector business activity as a proxy for domestic investment activity. I also employ additional matching techniques. I continue to find robust support for my hypothesis.

Conclusion

In this article, I examine the impact of inward FDI on electoral support for local governments, because responsibility for attracting FDI often rests with subnational (state and local) rather than national governments. I argue that the nature of the geographic distribution of winners and losers from individual investment projects across subnational units is such that FDI generates localized net increases in the welfare of voters in the recipient economy. Because inward FDI is likely to benefit voters at the local level, a new greenfield investment project should be associated with increased support for the incumbent party.

I test and find support for this argument in an analysis of mayoral elections in Brazil between 2004 and 2012. The results show that the announcement of a greenfield investment project increases the probability of reelection of the incumbent mayor’s party. Moreover, greenfield investment has a substantively large effect on electoral success. One contribution of study is therefore to suggest new linkages to fill the gap between literatures on mass political behavior in comparative and international political economy.

The findings of this article suggest additional questions about the electoral consequences of inward FDI. First, the extent to which the findings generalize to other countries is likely to depend on the degree to which political institutions place control for attracting FDI in the hands of local governments. This argument is particularly likely to apply in other federal systems, including advanced economies like the United States, though the same dynamics may emerge in other countries in which local governments have the ability to offer incentives. A second area of research should examine how the characteristics of different types of investment, including mode of entry, industry, and nationality of the multinational, shape how voters view inward FDI as this may have implications for whether this leads voters to reward incumbents. Indeed, relevant literatures in international political economy and international business offer theories of how the characteristics of the investment project may produce different distributional and nonmaterial considerations and newly available firm-level data can allow us to test these arguments.

More broadly, this research has important implications for the domestic politics of global production. Although this article focuses on the local impact of FDI on local elections, it raises questions about how FDI and other dimensions of globalization (a) generate within country pressures and (b) how these pressures are addressed through policy responses at different levels of government. Work by Menendez (2016) and Rickard (2012) highlights the intersection of national level political institutions and geographic distribution, but more research is needed with respect to the ways in which subnational and national institutions mitigate or exacerbate distributive tensions arising from regional inequality or competitive pressures within countries.

Supplemental Material

bge_cps_sa_final – Supplemental material for Foreign Direct Investment and Elections: The Impact of Greenfield FDI on Incumbent Party Reelection in Brazil

Supplemental material, bge_cps_sa_final for Foreign Direct Investment and Elections: The Impact of Greenfield FDI on Incumbent Party Reelection in Brazil by Erica Owen in Comparative Political Studies

Supplemental Material

eowen_cps_replication_brazil – Supplemental material for Foreign Direct Investment and Elections: The Impact of Greenfield FDI on Incumbent Party Reelection in Brazil

Supplemental material, eowen_cps_replication_brazil for Foreign Direct Investment and Elections: The Impact of Greenfield FDI on Incumbent Party Reelection in Brazil by Erica Owen in Comparative Political Studies

Footnotes

Acknowledgements

I thank Jose Cheibub, Bill Clark, Scott Cook, Songying Fang, Yoo Sun Jung, Quan Li, Rachel Wellhausen, and Guy Whitten as well as participants of the Texas Triangle IR Conference, the International Political Science Association Conference, the Politics of Multinational Firms conference at Princeton, and seminars at the IE Business School and Texas A&M University for helpful suggestions. I thank Kendall Funk and Thiago Silva for excellent research assistance and I thank Texas A&M University for funding that supported this research.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the funding received from Texas A&M University.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.