Abstract

The imposition of restrictive trade policies and consequent fabrication of foreign trade statistics acts as hindrance for effective policy formulations in the developing countries. This article presents the trade misreporting scenario of Bangladesh in relation to major Asian trade partner countries (China, India and Singapore) between 1973 and 2018 and examines the possibilities of informal capital movements across borders. Using the vector autoregression (VAR) and autoregressive distributed lag (ARDL) models, we first build partner-level exercise, followed by a combined panel, and find that spot and forward exchange rates, custom duties and real interest rate differences between foreign and home largely affect trade misreporting rates. Interestingly, we also find that the values of past import under-invoicing might also lead to export under-invoicing and vice versa, a two-way causal relationship.

Introduction

One distinct characteristic of international trade statistics is that it can be methodically cross-checked for data falsification. Fabrications of major economic data like trade data pose enormous challenges to the economists and policymakers and hence impede fruitful governance. This study takes up the trade misreporting phenomena in Bangladesh (BD) with her three major Asian trading partners—China, India and Singapore. We show that along with creating difficulties in policymaking, falsified trade data might also lead to informal capital movements across borders. BD misreports significant values of both exports and imports with these three major Asian countries. Our findings show that BD mostly underreports both export and import values with China, and in the case of India and Singapore, we find both under- and over-reporting behaviours. Through our empirical exercises, we try to attribute intentional fabrication of trade data to policy instruments such as spot and forward exchange rates (ERs), high export taxes (ETs), customs duties on imports and interest rate differentials between foreign and home among others. Comprising both individual and panel exercises, our results demonstrate that in the case of import under-invoicing, ERs and custom duty (CD) have a positive and highly significant impact on BD’s underreporting rates with China, India and Singapore both in the short and long runs. Forward premium (FP) and real interest rate difference (IRD) between foreign and home have a negative impact on BD’s import underreporting rates with China and India in the long run. So far as exports are concerned, we get a negative relation between spot ERs and underreporting rates of BD with respect to China and India in the long and short run. We also get a positive correlation between export underreporting rates and FP of BD with respect to India both in the short and long run, but in case of China and Singapore, FP has a significant impact during the short run only. We get a positive correlation between BD’s export underreporting rates and real interest difference with respect to Singapore in the long and short run. Combining these three countries, we also run a panel to check the robustness of individual country-based exercises. Finally, we find a bidirectional causal relationship between export and import under-invoicing series at level values in the case of China. In the case of India, we have got a unidirectional causal relationship.

This article is organised in the following manner. The second Section briefly reviews the literature. The third Section discusses data, methodology and examines BD’s trade misreporting scenario. The fourth Section investigates the causal relationship between export and import misreporting series, and, finally, the fifth Section concludes the article.

Brief Literature Review

Morgenstern (1963) was the first to look into the issues of misreported domestic trade statistics by enquiring the partner country statistics. Bhagwati (1974) used the partner country statistics to cross-check the authenticity of Turkish trade data. Biswas and Marjit (2005) and Marjit et al. (2000) were the first to take up the Indian case of trade misreporting. They looked into India’s official export and import data and attributed trade misreporting to restrictive trade and exchange policies. Biswas and Marjit (2007) built a three-country trading framework to investigate cross-border illegal capital movements. Marjit et al. (2008) showed that a controlled trade environment might cause inaccurate policy projections through data fabrications. Biswas (2012) proved that export might be underreported to finance hidden import basket. Biswas et al. (2019) found that if trade statistics were distorted, the gross domestic product (GDP) might be miscalculated too. Das Subhasish & Biswas (2021a) tried to find the effects of trade and other macro policy instruments on misreporting pattern of India with the USA as partner. Using disaggregate-level bilateral-level trade data, Marjit (2022) has shown that imported inputs used to produce exportable goods might lead to causal relationship between imports and exports. Singh (2012) discussed economic integration in South Asia among Bangladesh, India and Pakistan with tariff rationalisation. Jain (2019) studied Indo-Bangla trade relationship as part of SAFTA agreement.

A large body of research also connects Chinese trade misreporting to a variety of restrictive trade policies and possible capital flight. Fisman and Wei (2004) found that China’s import misreporting was connected to the variations in import tax rates. Ferrantino et al. (2012) investigated China’s direct exports to the USA and found statistical proof of underreporting. Cheung et al. (2016) found that the Chinese capital flight was linked to trade misreporting. Biswas et al. (2022) examined bilateral trade and investment data between China and the USA and discovered that hidden capital movement might occur through both channels.

There is hardly any study on trade mis-invoicing pattern and its consequences in BD. Only recently, Das Samir & Biswas (2021b) examined the quantitative assessment of unrecorded transactions through trade misreporting between BD and its top three Organisation for Economic Co-operation and Development (OECD) trade partners. Das Samir & Biswas (2022) investigated the bilateral trade mis-invoicing scenario between BD and India.

Data, Methodology and Findings

We choose three of BD’s major Asian trade partners, namely China, India and Singapore, based on their share of trade in BD’s total trade. Following the International Monetary Fund’s (IMF) prescription (Marini et al., 2018), we use the following formulations to find the trade misreporting scenario of BD with her partners (which we assume reveal trade data truthfully).

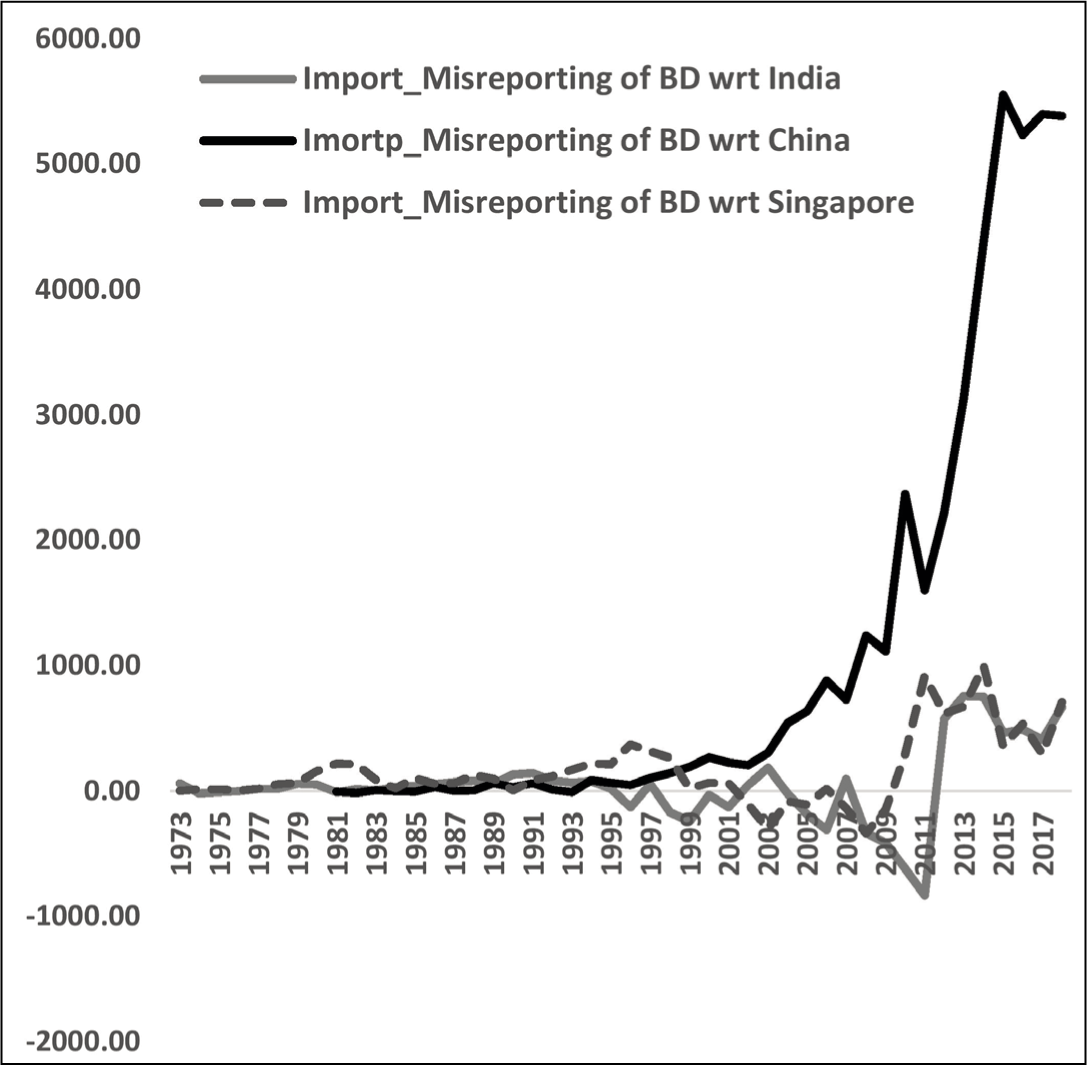

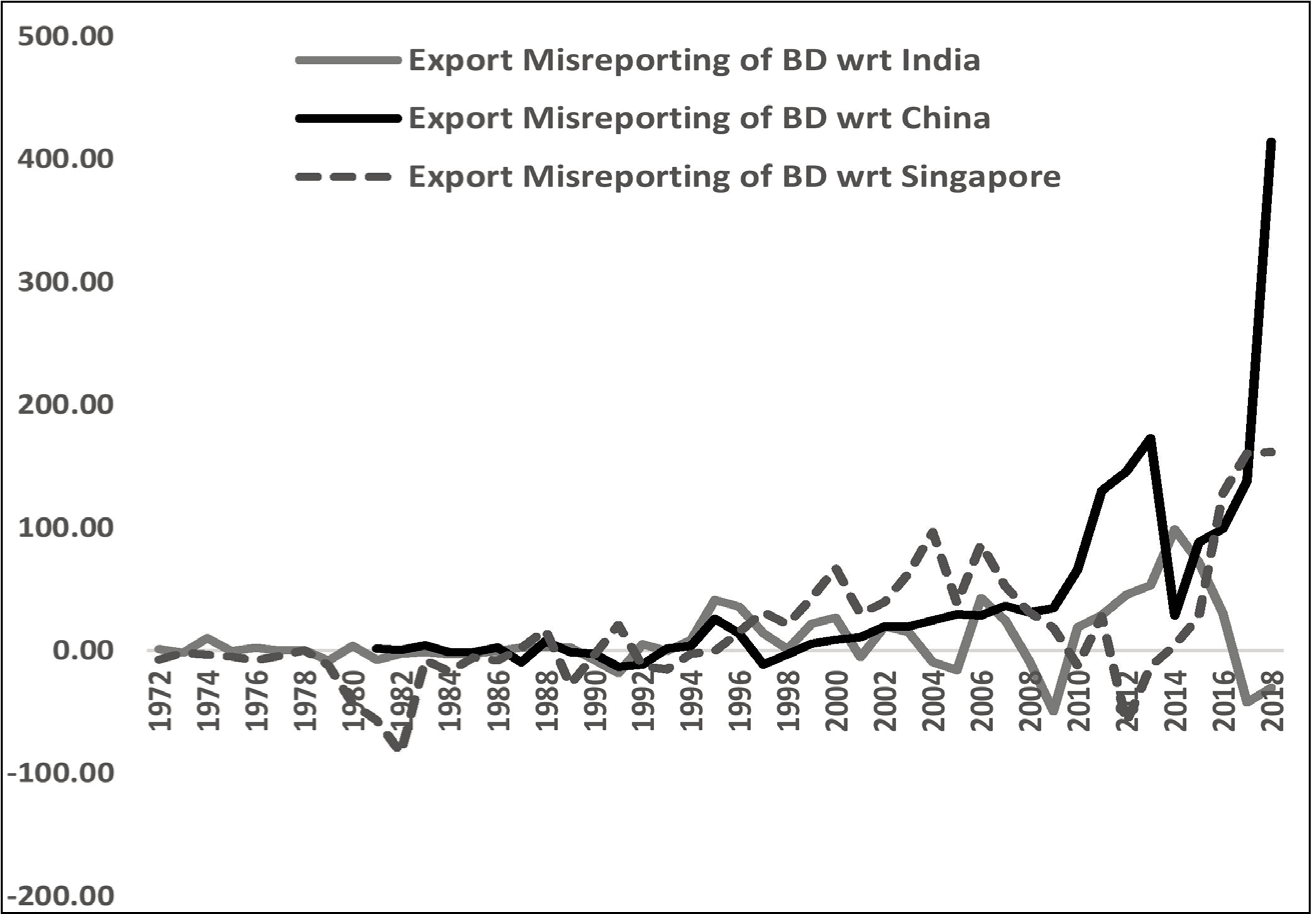

Figures 1 and 2 capture the historical trade misreporting scenario in BD with its Asian partners. By discovering the discrepancies in BD’s officially reported bilateral trade statistics, we examine the extent of trade misreporting by BD’s foreign traders and the factors that might affect their misreporting behaviour. Dishonest foreign traders usually misreport to gain from overvalued ERs, expected future depreciation of domestic currency indicated by forward rates, real interest rate differentials between developed country foreign partners and home along with ETs (for export misreporting) and import tariff or custom duties (for import misreporting). If domestic currency is overvalued, corrupt exporters might underreport and importers over-report to sell the extra foreign currency in the market for premium. On the other hand, if the corrupt traders think that the domestic currency will depreciate in the near future, the exporters and importers might under- and over-report, respectively, to send the hidden capital abroad before taking it back once the depreciation expectations are realised. Similarly, if the corrupt traders find foreign real interest rate more attractive than the home real interest rate, the dishonest exporter might underreport and importer over-report to send the capital abroad illegally. If export and import taxes are high, dishonest traders might underreport their traded values. All these variables have been incorporated in our regression exercises.

First, we run individual country-level autoregressive distributive lag (ARDL) model followed by combined unbalanced panel ARDL regression to understand the impacts of major trade policy instruments such as ER, FP, ET on BD exports, CD on BD imports, and IRD between foreign and home on misreporting rates of export

The descriptive statistics such as variance, standard deviation, skewness and kurtosis are presented in Table A2 in the Appendix. Next, we check for stationarity using Pesaran–Shin unit root tests (Table A3 in the Appendix). At the level, some variables are stationary, while others are stationary at the first difference. The Schwarz Information Criterion (SIC) is used to determine the automatic optimal lag length selection. We also check for multicollinearity among the explanatory variables. Pesaran et al. (2001) presented the ARDL bound tests, which provide t- and F-statistics to check for cointegration. The results of the tolerance and variance inflation factor (VIF) multicollinearity test are provided in ARDL regression tables. Breusch–Godfrey Lagrange multiplier (LM) test is carried out to check autocorrelation. We use the Durbin–Watson test for serial correlation. Breusch–Pagan and Jarque–Bera tests are also conducted. We also use the cumulative sum (CUSUM) test to ensure that the parameters in our model are stable (Tables A4 and A5 are given in the Appendix).

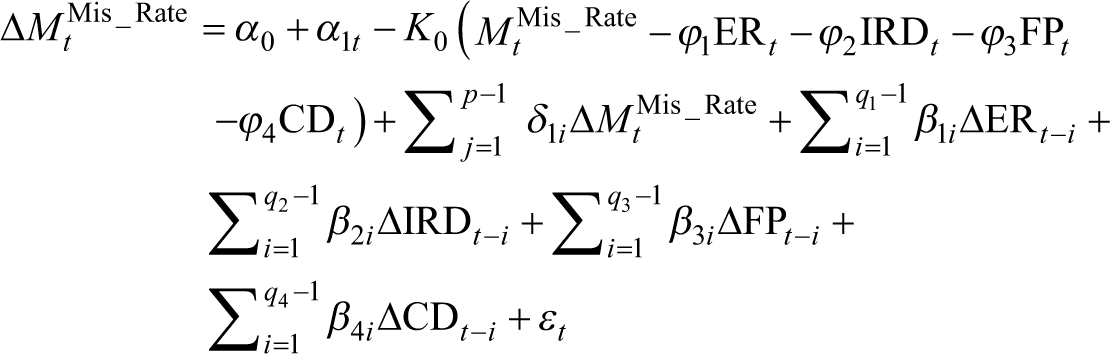

We now examine the impacts of ER, IRD, FP and CD on

where

where

The speed of adjustment parameters is connected with the EC component (i.e.

Following the findings of our empirical exercises, let us intuitively justify the results, that is, the attributes that affect BD’s bilateral import and export misreporting rates with respect to China, India and Singapore as presented in Tables A4 and A5 (in Appendix). Both in the long and short run, ER has a positive influence on the BD’s import underreporting rate with China, India and Singapore.

Assuming that the black market for foreign exchange exists in BD, if home currency depreciates, black market premium (BMP; the difference between market and official exchange rates) would fall (Biswas & Marjit, 2005). Hence, it might be cheaper for the corrupt importers to buy foreign currency in the black market to finance the unreported part of the import basket. FP has a negative impact on BD’s import underreporting rate with China and India in the long run. As FP goes up, it becomes more attractive to send the foreign currency abroad in a hidden manner to gain from future currency depreciation before taking in the foreign currency back home and converting into the domestic currency. Therefore, import under-invoicing rate would fall or import over-invoicing might go up if FP increases. Import underreporting may fall or import over-reporting may rise if the IRD goes up since it is better to send the capital abroad to gain higher real foreign interest rate as compared to the domestic real interest rate. This result is reflected in our econometric exercise as we find a negative relationship between import under-invoicing rate and IRD in the case of China and India, which are statistically significant in the long run. We get an expected positive and highly statistically significant relationship between CD and import under-invoicing rate in the case of China, India and Singapore in the long run. This is straightforward as in the face of increasing tariff rate or CD, a rational dishonest importer would always underreport to evade tariff duties.

We get a negative correlation between ER and export underreporting rates in the case of China and India again both in the long and short run. As BD’s currency depreciates leading to (possible) fall in BMP, the corrupt exporters find it unattractive to sell unreported foreign currency in the black market for foreign exchange. This causes a fall in export underreporting rate. If FP goes up, corrupt exporters would increase export under-invoicing to send capital abroad to gain from expected future currency depreciation in the long run. This result is significant for all the trade partners in the short run. Export underreporting may rise or export over-reporting may fall if the IRD goes up since it is better to send the capital abroad to gain higher real foreign interest rate. This result is reflected in our econometric exercise as we find a positive relationship between export under-invoicing rate and IRD in the case of Singapore in both the long and short run. We find no evidence of ETs on the rate of export underreporting perhaps because in BD, the ETs are not very high (Table A5 in Appendix).

We find similar results in the case of a combined country panel, which is presented in Table A6 in Appendix. In the case of export misreporting, FP and IRD have a positive impact in the long and short run, respectively. In the case of import misreporting, FP and IRD have a negative impact in both the long and short run. On the other hand, CD has a positive impact on import underreporting rate in both the long and short run.

Causal Relationship Between Export and Import Misreporting

This section takes up another interesting exercise in finding possible causal relationship between annual export and import mis-invoicing series at its level values. If unscrupulous exporters and importers develop a collaborative cartel, both of them may rationally misreport for mutual benefits (Biswas, 2012). Hence, there might be a correlation between export and import under-invoicing at level values. In order to examine a possible causal relationship between export and import misreporting, a VAR Granger causality test is carried out with a simple multi-equation reduced form (Table A7 in Appendix). At the first difference, both the import and export mis-invoicing are stationary. Hence, we employ a VAR model with lags.

We find a bidirectional causal relationship between export and import misreporting series for BD–China. For BD–India, the relationship is unidirectional. In the case of Singapore, we find no such relationship.

In the case of BD–China,

It shows that import misreporting is dependent upon the fourth lagged value of export misreporting. At the same time, export mis-invoicing is also dependent upon the second lagged value of import misreporting. These is a very interesting set of relationships in the sense that both importers and exporters are mutually dependent upon each other in their data falsification behaviours. Intuitively, the misreporting importers are financing their unreported import basket from the past (fourth period lag) foreign currency supplied by the misreporting exporters. Similarly, corrupt exporters decide about their magnitude of export underreporting based on the past (second period lag) expected demand of illegal foreign currency by the corrupt importers.

In the case of BD–India,

Conclusion

A comprehensive enquiry into any corrupt act is always a difficult task, and as these corrupt actors are international traders and investors, the exercise becomes much more challenging. Nevertheless, this exercise of ours deals with the misreporting patterns of international trade statistics by the BD traders with its top Asian trading partners and attributes the rational data fabrication to several trade, exchange and macro instruments. We have also shown that scarce domestic capital might be drained away in a hidden manner through these misreporting behaviours. Most importantly, we find that the corrupt exporters and importers might help each other for mutual benefits.

There could be several extensions of this work. One might include the foreign investment channels of BD to investigate other possible avenues of hidden capital movements. Miscalculation of domestic income (GDP) as a result of trade data fabrication could be another challenging task. Finally, a detailed exercise based on the bilateral trade data at the disaggregate level would be another interesting extension.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.