Abstract

The study investigates long-run and short-run cointegrating relationship between stock market returns, fear index (VIX), brent crude oil prices and growth in deaths due to the COVID-19 pandemic for BRIC countries using daily data from 23 January 2020 to 24 August 2020 using Autoregressive Distributed Lag (ARDL) model. CUSUM test and serial correlation test estimates point towards the robustness of the model used. The evidence reveals that for India and Brazil, with the outbreak of COVID-19, decrease in crude oil prices and increase in volatility index, the stock returns started declining in the short run, but the impact has declined and the stock returns have regained in the long run. For China, due to the outbreak of COVID-19 and increase in fear index, stock returns declined in the short run, but the Chinese economy has recovered well due to a strong industrial and services sector. For Russia, increase in deaths due to COVID and decline in oil prices has impacted the stock returns in the long- and short run. Due to a decline of 53% for crude oil prices from January 2020 to May 2020, the Russian economy would face the consequences in the long run as well. The results suggest that though BRIC countries were impacted by growth in COVID-19 deaths, but the recovery trajectory and stability has resumed for all countries except Russia. Results of Granger Causality indicate a bidirectional causality between VIX and stock returns for the Indian market.

Introduction

On December 2019 in Wuhan, the capital city of Hubei province of China, the first COVID case was identified (Sohrabi et al., 2020; Yang et al., 2020). On 30 January 2020, the World Health Organization (WHO) declared COVID-19 as a health emergency of international concern. The virus has caused 848,557 deaths worldwide, with 25,291,896 cases reported till August 2020. The pandemic has had clear economic and financial impacts, with business failures and increased unemployment. The Shanghai stock market fell by 8% in the first week of February, with the shock spreading to other international markets. GDP growth is expected to decline by 2% in the United States and Japan and by 3% in the EU (Gormsen & Koijen, 2020).

BRIC countries are protagonists as the most promising large emerging economies in the multipolar world, covering around 25% of the global GDP. Simultaneously, they have also been attracting the most relevant investments. The progressive relevance of these countries embeds them to be placed as world leaders in the global economy. Needless to say, in the unconventional and unexpected times such as the COVID-19 pandemic, these nations deserve special attention. Critical to this discussion is testing if there is presence of any long-run relationship among stock market returns, increase in deaths due to COVID-19 and financial markets.

To gauge the market’s expectation of 30ay volatility and help the investors know about the current fear and stress that exists for the market, a CBOE volatility index (VIX) is used. It is popularly known as an ‘investor fear gauge’ (Aharon & Qadan 2017; Akdag 2019; Cheuathonghua et al., 2019; Cinar & Uzmay, 2017; İskenderoglu & Akdag, 2020; Whaley, 2000; Woodley et al. 2019). Uncertainty has a negative effect on stock returns (Bash & Alsaifi, 2019). While multiple studies existed for employing of VIX as a fear quotient for developed countries, its use for emerging countries was doubtful. A study by Sarwar (2012) convincingly assessed the legitimacy of using VIX to gauge investor fear for BRIC countries. A strong empirical evidence to support its usage for BRIC countries was found.

The pandemic led to social lockdown and travel restrictions, causing oil demand collapse. Brent crude oil price dropped from $66 a barrel in December end of 2019 to $45 a barrel in March 2020. Due to the lack of consensus between the Organization of the Petroleum Exporting Countries (OPEC) and its allies, the oil price fell to $34 a barrel. Brent oil prices signal towards the financialisation of commodity markets (Ajmi et al., 2014) and can be utilised as a factor to test the relationship between equity markets and commodity markets in BRIC nations. In this context, Ciner (2001) forayed into testing whether a relationship exists between real stock returns and oil price futures and found significant results. A rational response between stock markets and oil price changes also exists in the Norwegian market (Gjerde & Saettem, 1999).

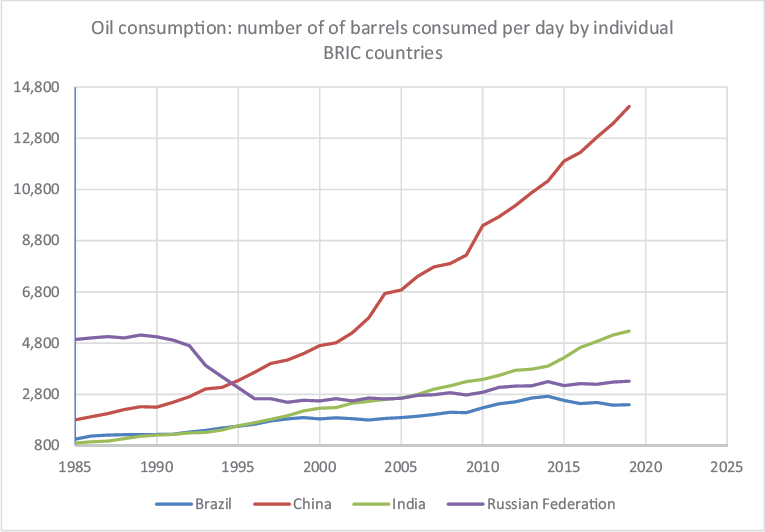

Specifically, crude oil is the most universal commodity in the sense that fluctuations in its price are strongly correlated with fluctuations in equity markets. China, due to its strong industrial presence and high population, has shown a sharp incline in consumption of oil (Figure 1) over the years, whereas for India, Brazil and Russia, the consumption has been relatively stable. Oil price fluctuations interest the researchers not only because they directly impact the economic activity but also because fluctuations in prices of oil might even affect international stability (Leigh et al., 2003).

The stock markets also responded negatively to the growth of COVID-19 cases (Ashraf, 2020). Due to the decrease in the Shanghai stock market index, the central government injected $174 billion of liquidity in the market. In July 2020, even after the pandemic, the Chinese equity market saw an investment of $7.6 billion. This could be due to the hope and uncertainty of the Chinese market during this crisis. For China, positive news improves the stock market and trading of stocks, while negative news hinders it (Li & Wei, 2018). Estimates provide ample evidence of similarities in the correlation dynamics between the crude oil and stock volatility series (Ding et al., 2017). Going beyond previous research, Ajmi et al. (2014) assess the impact of Islamic stock market indices to global risk factors (VIX) and finance systems (international crude oil market).

Investigating the relationship between equity markets returns, risk factor (VIX) and oil prices of BRIC nations in a pandemic that hampers industrial activity has several potential benefits. First, it explores the less-explored characteristics of asset markets of emerging countries, which are otherwise well-documented for developed countries. Second, it adds to valuable research using a comprehensive dataset, which may be of interest to market participants, investors and regulators. With the onset of uncertainty, such as COVID-19, many research questions arise. Are the stock returns impacted by Brent crude oil prices that have fluctuated due to COVID pandemic? Are the returns affected by growth in deaths due to COVID? The study examines if there is presence of long-run and short-run relationship between fear index, stock returns, oil prices and growth in deaths due to COVID in BRIC countries. The article adds to literature as a special case, addressing testing the long-run and short-run interrelationship during the COVID-19 pandemic, and introduces growth in deaths due to COVID as another potential variable that might affect equity returns of BRIC countries.

Overall, the motivation of the research lies in the extent of fluctuations in the equity markets, which primarily exhibit higher interrelations with other markets as well as sentiments of market participants. The paper intends to test the interrelations between VIX, brent oil prices and growth in deaths due to Covid-19 and the stock returns.

Figure 2 shows the fall in the crude oil prices during the initial months of the year, which started stabilising by second quarter of 2020. Figures 3 and 4 depicts the change or growth in deaths due to COVID in China and other BRIC countries. There has been a steady increase in the death rate, which stabilised post June 2020.

The remaining paper is as follows: Section II discusses the review of literature, Section III describes the methodology, data and variables used in the study. Section IV discusses the empirical analysis. Section V presents the discussion of the results and Section VI concludes the article.

COVID-19 has had a considerable impact on financial markets and institutions, which could be direct or indirect (Goodell, 2020). With an increase in deaths and confirmed cases of COVID-19, the US markets became more illiquid and volatile (Baig et al., 2020). Extremely large disasters have negative impacts on the outputs in the long and short run (Cavallo et al., 2013). An event like a terrorist attack effects the commodities, stocks and bonds in a negative way (Chesney et al., 2011). Pandemics bring a large loss in economic conditions of the country as well. Expected value of losses for national income varies from 0.3% for high income countries to around 2% for low middle level economies. Stock market volatility has been affected more by COVID-19 compared to other diseases like Ebola (Baker et al., 2020a, Schell et al., 2020). Ebola virus in the past brought great human and financial losses (Ross et al., 2015). Diseases like SARS, which spread rapidly from one country to another, brought a disproportionate economic impact than a health impact (Smith, 2006). Spanish Flu led to an economic decline in GDP and consumption to around 6–8% globally (Barro et al., 2020). In the United States, due to the current pandemic and business closures, there has been a loss of around $700 billion, but it saved 36,000 lives (Barrot et al., 2020). Also, the expected partisan gains were also less during COVID times for the United States (Apergis & Apergis, 2020).

Even though the virus broke out in China, the Chinese economy is in a much better position than other developing economies (Liu et al., 2020). Neither gold nor cryptocurrencies have significantly affected the stock markets in China (Corbet et al., 2020). So, though the Chinese market stabilised itself, the global market got hit during the later part of the virus spread (Ali et al., 2020). In the United States and the United Kingdom, the implied VIX rose in February, peaked in March and fell back by March end as the stock markets improved (Altig et al., 2020). VIX as an investor fear gauge index has negatively impacted the stock returns for emerging countries (Sarwar et al., 2020). High sentiment market outperforms low sentiment markets (Sun et al., 2019; Zaremba et al., 2020).

Major global and political events have impacted the oil price, and positive and negative correlations exists between the oil price and the fear index (Qiang et al., 2019). When the global activity is weak, there is a huge, unexpected rise in the oil prices (Ratti & Vespignani, 2013). Prior to the global financial crisis, there was a huge rise in the demand for oil due to disruption in the supply of oil as well as a global increase in demand for oil. Post the crisis, due to the decrease in US dollars, the oil prices crashed (Bhar & Malliaris, 2011). For the United States, the oil market became inefficient post the crisis (Gil-Alana & Monge, 2020). Volatility of crude oil improves the directional predictability of the VIX, especially when the oil volatility is high. Oil has been found to be the best hedge for emerging stock market prices (Basher & Sadorsky, 2016). Global oil and the US energy stock market’s VIX are interlinked with a long-run cointegration relationship (Dutta, 2018; Qiang et al., 2019). Implied volatility for crude oil price markets contains important information for predicting future volatility as well (Bakanova, 2010). The risk perception of the investors globally impacts the gold prices, with a long-run relationship between gold, silver and exchange rate (Sari et al., 2011). Studies conducted in developing markets like India showed a positive impact of crude oil on the Indian VIX and a negative impact of gold (Mehta and David, 2019). BRICS index returns commoved with oil prices, especially during the global financial crisis period. Gold does not comove with stock index, proving to be a hedge for countries against extreme market movements (Mensi et al., 2018). Also, during times of financial markets volatility, there is correlation between crude oil prices and stock market returns in China (Nadal et al., 2017). For Russia, external shocks such as VIX, price of brent crude oil have significantly affected the dynamics of macro-economic indicators (Shevelev, 2017). Oil fluctuations have affected the financial markets and the currencies. Lowering of oil price boosts the UK pound but hurts several sectors that are benefitted with oil supplies such as industrials and transportation (Atil et al., 2014). With the onset of COVID-19, firms that were exposed to China underperformed. Post the spread to the United States and Europe, corporate debt market emerged as a valuable driver. The effects of a health crisis were increased through the financial claims (Ramelli & Wagner, 2020).

Studies on Relationship Between the Volatility Index, Stock Market Returns and Brent Crude Oil Prices Before COVID-19 and During COVID-19

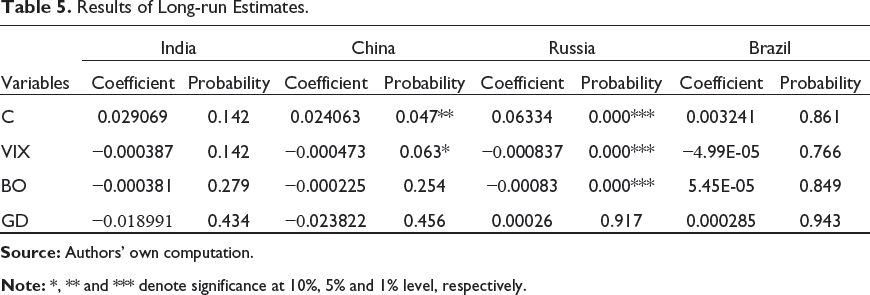

Post COVID, the results depicted that for India and Brazil, there is no long-run association between the stock returns, the VIX, brent crude oil prices and growth in deaths. For China and Russia, the fear index impacts the stock market return in a negative way. Before the COVID breakdown, a negative relationship has been found between the Indian VIX and stock market return (Chakrabarti & Kumar, 2020). For Brazil, investors could anticipate instabilities in the Brazilian market by getting indications from the fear index and could identify opportunities to enter and exit the markets (Cainelli et al., 2020). Though stock market returns and VIX move inversely, China observed them moving in tandem before the COVID crisis (Liu, 2019). Unlike the Chinese and Brazilian non-contemporaneous significant correlations between VIX and stock returns, none of the non-contemporaneous cross-correlations between changes in VIX and equity returns for India and Russia are significant (Sarwar, 2012). Before COVID, empirical evidence of time varying differential dependence between Indian stock market returns and brent crude oil have been found (Singhal & Ghosh, 2016). During COVID, for the Indian market, the variables hold a significant relationship in the short run. This implies that the stock returns are impacted by the oil price, fear index and growth in deaths due to COVID in the short run but not in the long run. Pre COVID, the corelation between crude oil and the Indian stock market returns has been found to be higher during the 2008–2014 period (Jain & Biswal, 2016). A positive causal effect from crude oil price changes to Asian market stock returns has been found (Yousaf & Hassan, 2019). Pre COVID, asymptotic dependence between Chinese stock market and crude oil prices have been concluded (Chen & Lv, 2015; Huang et al., 2015; Li & Wei, 2018). Before the COVID time period, Brazilian market has been found to be sensitive to the variations in oil prices (Teixeira et al., 2020; Nava et al., 2018). For Brazil, the brent crude oil increase and growth in deaths due to COVID negatively impact the stock returns. During COVID, the study finds that for Russia, the increase in brent crude oil prices has a negative impact on the stock returns. Pre COVID, brent crude oil price has the strongest transmission eject on the Russian stock market return (Zivkov et al., 2018).

Data and Methodology

Description of Various Indicators Used in the Study.

Description of Various Indicators Used in the Study.

The time period was chosen because COVID-19 early confirmed cases and deaths began in this time period, with growth in March and stability in August 2020. The government response curves also started declining and flattening post April 2020 (Hale et al., 2020). The data for China VIX India VIX, Russia VIX and Brazil VIX has been taken from Cboe website. Brent crude spot oil price (dollar per barrel) is taken from H1a: Is there presence of long run cointegrating relationship between the VIX, stock market returns, Brent crude oil prices and growth in deaths due to COVID-19 in BRIC countries? H1b: Is there presence of short run relationship between the China VIX, stock market returns, Brent crude oil prices and growth in deaths due to COVID-19 in BRIC countries? H1c: Is there existence of short run causal relationship from VIX, Death growth rate and Brent crude oil prices to stock market returns for BRIC countries?

In applied econometrics, several studies by Engle and Granger (1987), the Granger (1981), Autoregressive Distributed Lag (ARDL) cointegration technique, Johansen and Juselius (1990), bound test of cointegration by Pesaran et al. (1999) and Pesaran et al. (2001) have been used to establish long-run relationship among the variables and reparametrising them to the Error Correction (ECM). The present study makes use of ARDL cointegration technique to establish the long relationship among the variables.

The hypotheses are tested by the ARDL model developed by Pesaran et al. (1999) to study the long-run and short-run relationship among the variables. Cointegration is a method to study long-run relationship among VIX, stock market returns, growth in deaths due to COVID-19 and brent crude oil prices. The advantage of the method is that it overcomes endogeneity problems, computes long-run and short-run relationship together and can be estimated if the regressors are I(0) or I(1) (Pesaran & Shin, 1996). The series should not be I(2), otherwise the F-statistics computed by the model becomes invalid. So, before applying ARDL model, it is verified that none of the variables should be I(2). To check the stationarity of the variables, the study uses Augmented Dicky Fuller Test (ADF). Akaike Information Criteria (AIC) and Schwarz Information Criteria (SIC) are used to select the number of lags in the model. The null hypothesis states that there is no long-run relationship among the variables. If computed F-statistic value is greater than the upper bound, the null hypothesis is rejected, and if it is below the lower bound, the null hypothesis cannot be rejected. If it is between the lower and upper bounds, the results are inconclusive (Narayan, 2005).

The long run model is as follows:

To check presence of long-run cointegration, the following equation is run.

∇ = First Difference Operator

Once we are able to establish the long run relation with the help of the F-statistic, we can estimate the ECM.

The ECM representation is as follows:

The aim of ECM is to show the speed of adjustment to equilibrium after a shock in the short run. Diagnostic tests such as Bresuch Pagan Godfrey Heteroskedasticity and Bresuch Godfrey serial correlation tests is used. To explore the stability of the coefficients, cumulative sum of recursive residuals (CUSUM) is used. If the plot lies within the bound at 5% level of significance, the coefficients in the regression model are said to be stable (Pesaran et al., 2001).

Descriptive Statistics.

Descriptive Statistics.

The descriptive statistics (Table 2) point out interesting figures and revelations about the data. Except China, no other country experiences negative returns in the stock market index. The ratio for growth in deaths is surprisingly highest for Russia and lowest for China in the sample period. All BRIC countries also recorded high volatility in VIX, also known as fear index, with Brazil having the maximum.

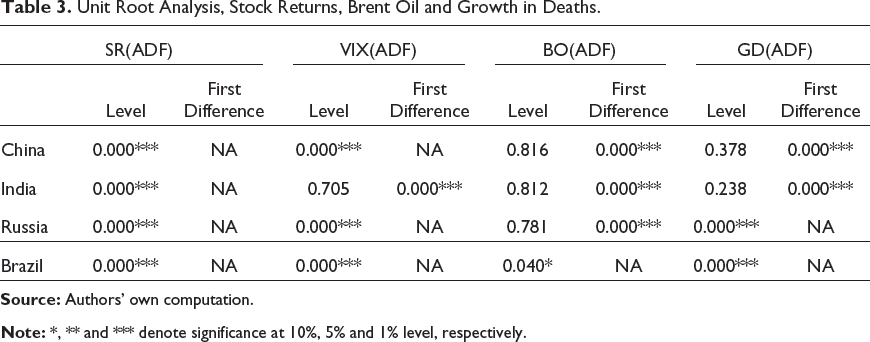

Unit Root Analysis, Stock Returns, Brent Oil and Growth in Deaths.

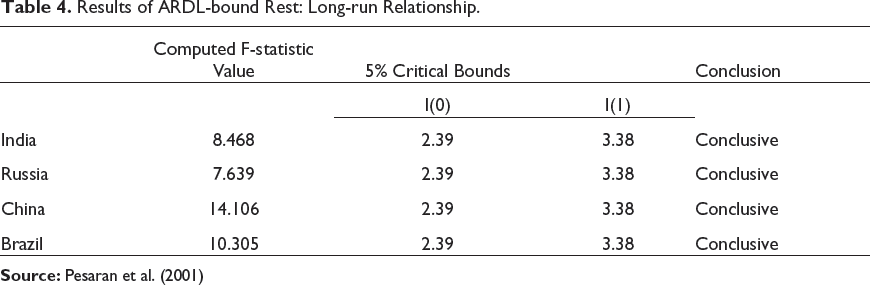

Results of ARDL-bound Rest: Long-run Relationship.

Results of Long-run Estimates.

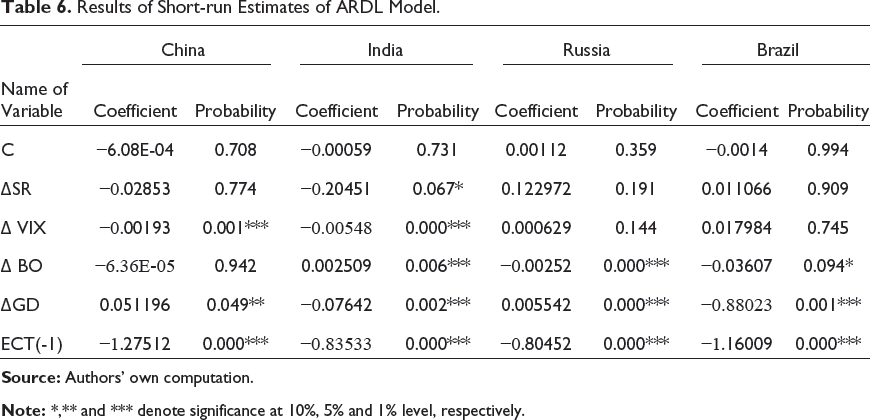

Results of Short-run Estimates of ARDL Model.

Granger Causality Results.

Although cointegrating relationship implies the presence of Granger causality, it does not indicate the direction of causality among the variables. Therefore, Granger causality is applied to check for the direction of causality among the variables (Table 7) For India, there is a bidirectional causality running between VIX and SR. With an increase in the fear index, there is an immediate decrease in the stock market returns (Sarwar & Khan 2017; Sarwar, 2014). An oil price change causes an immediate change in the stock returns (Gjerde & Saettem, 1999). Also, with an increase in deaths due to COVID, an economic uncertainty is created, which leads to a decrease in the stock returns. For China, there is unidirectional causality running from the fear index to the stock returns and from growth in death due to COVID-19 and the fear index. Also, there is a unidirectional causality running from implied VIX to brent crude oil prices (Qiang et al., 2019). For Russia, unidirectional causality has been found from oil prices to the stock returns and fear index. Also, unidirectional causality exists from increase in deaths due to COVID and stock returns. Similar to Russia, unidirectional causality runs from oil prices to stock returns and fear index for Brazil. Unidirectional causality runs from growth in deaths due to COVID to stock returns and fear index.

Serial Correlation Test.

Serial correlation (Table 8) is checked using Breusch Godfrey Serial Correlation Test. The null hypothesis states that there is no serial correlation in the residuals. As the p-value is greater than 5%, the chi-square values indicate there is no serial correlation in the model. The stability of the coefficients in the model is tested using CUSUM test.

The null hypothesis states that the coefficients are stable in the model. The null cannot be rejected, and as for the CUSUM test, the cumulative sum remains with thin the 95% confidence band limit. The CUSUM test proves that the model is not mis-specified and there would be no structural change in the model over the period of time.

For India, in the short run, with the announcement of lockdown, Sensex dropped by 40% from 42,273 points to 25,638 in January. But in the long run, over the six-month period, the market recovered by 50% to over 38,000 points. The Indian market stabilised, and inflows in the capital market by domestic and foreign investors had started. This is also because investors believe that the government and central bank will back the capital in case of any failure in the market. Capital markets have provided secure returns compared to real investments. Decrease in brent crude oil prices led India to buy crude oil worth $16.7 million, filling its strategic crude oil reserves. Brent crude oil hit a 21-year low during COVID-19 and US oil futures fell to a negative value for the first time in history. Thereby, the decrease in oil price, increase in COVID deaths and volatility impacted the stock market returns in the short run, but the markets have recovered. Even though there has been decrease in economic activity, increase in unemployment, and changing pattern of work, study and travel, the stock markets is performing well. Therefore, in the long run, the stock returns are not affected by VIX, crude oil prices and COVID deaths for India. For Brazil, growth as measured by the economy activity index has reached pre COVID levels. Brazil faced the world’s second most severe outbreak of coronavirus deaths, but due to aggressive fiscal and monetary policies and less strict quarantine measures, the economy has rebounded. As it can be gauged from the results, the stock market declined by 50% with the outbreak of COVID in Brazil. As half of Brazil exports comes from commodities, with the decline in crude oil prices the markets declined sharply in the short run. But with the passage of time, the equity markets have seen domestic investor inflows. The short-run impact on Brazilian markets was due to the fact that China exports oil from Brazil. Therefore, with COVID, increase in China’s demand for oil decreased and impacted the economy. Brazil kept some of its sectors open, with services sector’s opening leading to a revival of the stock market returns by 30%. Therefore, in the long run. the stock market returns were not affected by oil price decline, COVID deaths and the fear index. China, being the market that gave birth to the virus, experienced a surge in the volatility and a decrease in stock market returns. But over time, the Chinese economy became the first economy to grow since the COVID impact. Though there was a decline of 6.8% in GDP during the outbreak of the virus, the GDP has currently increased to 3.2% compared to 2019. This has been due to increase in exports, industrial production and plans by government to invest in infrastructure. Though the VIX impacts the stock returns in the long and the short run, but the volatility has reduced due to the revival of the economy. From the results, it is seen that the Russian stock market returns are being impacted by oil decrease, increase in deaths due to COVID and VIX in the long and short run. Energy exports account for half of Russian exports, which got hit due to price crash and low demand. There has been a loss in the tax revenue that Russia earned from oil exports as the oil price fell below $42 per barrel. Russian economy had stabilised in 2016, but the pandemic increased the VIX and destabilised the moderately growing stock markets. Stock markets fell down by 30% during COVID. The analysis of the BRIC countries depicts that India, China and Brazil are on a path of recovery, but Russia will still take time to stabilise its market and economy.

Conclusion

The study delves into the relationship between the fear gauge index, brent crude oil prices, impact of COVID-19 induced deaths and stock returns for BRIC countries using an ARDL-bound testing approach. VIX represents the feelings and fearfulness of the investors and the degree of protection they want for future investment. Though there is a short-run relationship among variables for India and China, in the long run, stock returns would not be significantly impacted by fear index, oil prices and growth in deaths due to COVID. Even though countries have decided on the policy of ‘make local and buy local’, the Chinese manufacturing market has not been impacted and has shown an increase in exports as well. For India, even though there have been rising COVID cases and weak labour market, the country is back on a growth trajectory and stable stock market returns. Energy exports play an important role in the Russian economy. Due to lockdown and recession, there was a reduction in the demand for oil, leading to loss of revenue from oil exports. The study finds that the BRIC countries would recover from the crisis in the long run.

The conclusions arrived at in the study imply that policymakers should not make any short-term regulatory changes in the market to overcome the impact of COVID-19. Due to Covid there have been travel restrictions which have in turn impacted the oil prices. This depression can be revived and made better by the OPEC deals. The hit to oil prices has impacted the stock returns for the BRIC markets by increasing the economic policy uncertainty. Therefore, a proper economic strategy to curb additional uncertainty is required by the BRIC markets. It is advised that the investors adopt a stock-specific approach while trading. International portfolio diversification strategies may be devised in tune with the results, and investors looking for investment in these emerging market economies are likely to gain from this study.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.