Abstract

Lying is known to be endemic in a range of business settings. However, to date, studies have not analysed how lies surface, and are spontaneously managed, in ‘real time’ interaction. Drawing on video and audio recordings, in this article we analyse how actors account for false claims produced in different settings, namely sales, telemarketing and debt collection. Drawing on resources from ethnomethodology and conversation analysis, lies are conceptualized as products of interactional organization, rather than, say, products of the mind or motives of social actors. Our analysis reveals the centrality of ‘epistemics’ for understanding how people handle, and seek to neutralize, the moral risks associated with false claims. Potential accusations of ‘lying’ are shown to be defeasible in light of claims that the speaker has ‘discovered’, ‘noticed’ or ‘remembered’ some pertinent detail. We recover practices through which false claims are transformed, with varying degrees of success, from nefarious to innocent accountings. We conclude by discussing the implications of our findings for wider questions about the reproduction of work cultures that rely upon deceit.

Introduction

Lying is ‘woven into the daily fabric of business life’ (Grover, 2005: 149; see also Ashforth and Anand, 2003; Brannan, 2017; Grover, 2005; Hansen et al., 1996; Jenkins and Delbridge, 2017; Shalvi et al., 2011b). Many recent corporate scandals have revealed institutionalized systems of deceit (Markham, 2006; Rhodes, 2016). However, few studies have analysed how lies are subsumed into mundane everyday work activity. ‘Whistle-blowing’ and ‘cover-ups’ are predominantly associated with large-scale corporate scandals (Munro, 2017; Weiskopf and Willmott, 2013). This association persists even though corporate scandals such as Enron (Markham, 2006) and the VW emissions case (Rhodes, 2016) show deceit to be an everyday activity that is ‘seen but unnoticed’ (Garfinkel, 1967). This article is one of the first naturalistic studies to supply an account of everyday deceit, whistle-blowing and cover-up, revealing a repertoire of practices through which actors handle the moral accountability of ‘lies’ in ways that manage blame and responsibility.

Our use of inverted commas around the term ‘lies’ is an important aspect of the ethnomethodological approach we take in this article. Ethnomethodology is a distinct paradigm of enquiry in social science (Button, 1991) that does not provide second-order social scientific theory of how social structure is generated but instead studies how members of society, as ‘folk sociologists’ (Wieder, 1974) or ‘practical sociologists’ (Benson and Hughes, 1983), use their own common-sense knowledge of social structures to constitute the social world through their interactions. We use the term ‘morality-in-action’ (Danby and Emmison, 2014) to refer to this ethnomethodological concern with how matters of morality are oriented to and handled in everyday interaction. As Danby and Emmison (2014) argue, in everyday life we routinely infer and invoke moral versions of ourselves and each other. False claims are one such situation where issues of moral identity surface most clearly. The category ‘lying’ is only one of many potential ways of accounting for falsehoods, and crucially, as we will go on to show in this article, one that people may resist or contest.

We use the metaphor of ‘architecture’ to capture our interest in the underlying form and structure of the interactional sequences through which false claims are managed (Sacks et al., 1974). Theoretically, we do not approach lying as a product of individually motivated behaviour, but of interactional organization (Sacks, 1992). People who ‘really are’ telling the truth can nevertheless be deemed to have lied, in exactly the same way that liars can conceal deceit and be seen, publicly, to have been honest (Goffman, 1959, 1971). The question is not so much which version or ‘frame’ (Goffman, 1974) is correct but rather how the status of false claims are interactionally worked up in situ. We therefore develop an account of the public and intersubjective, rather than private and cognitive, character of ‘lies’. The term ‘morality-in-action’ sums up the basic premise of this ethnomethodological approach, drawing attention to how people account for matters of morality in the moment-by-moment unfolding of interaction. This is an important conceptual step in our view and is something that has yet to be explored in the existing literature.

Existing literature on deceit in organizational settings has sought to unearth the behavioural and cognitive manifestations of lies (Shalvi et al., 2011b), the normalization and routinization of lying at the organizational, group and individual level (Ashforth and Anand, 2003; Brannan, 2017; Jenkins and Delbridge, 2017), and the moral neutralization techniques used by those who lie (Aquino and Becker, 2005; Kvalnes, 2014). Studies have yet to analyse how particular claims are interactionally constituted as ‘lies’. Instead, ‘lies’ have been treated as taken-for-granted facts. In this article, we will draw on audio and video recordings of interactions from three different settings – sales, telemarketing and debt collection – to reveal how ‘lies’ are ‘worked up’ in the details of interaction and how lying is morally defeasible. We will show how this defeasibility hinges on ‘practical epistemics’ (Heritage, 2012): how speakers handle what they might reasonably know and what they might reasonably have forgotten or overlooked.

The article is organized as follows. In the first section, we review the literature on lying, focusing in particular on the study of deceit in business and workplace settings. Next, we outline the ethnomethodological approach we take and the distinct methodological approach this involves. We then analyse one false claim from each setting. The discussion draws together the findings to present an ethnomethodological account of ‘lying’ in interaction. The conclusion broadens the discussion to consider the implications of our findings for developing our understanding of how ‘cultures of deceit’ perpetuate in the light of the defeasibility of lies.

Lies, deceit and organizations

Lying has been extensively researched in the field of psychology. The quest to find a reliable method of detecting lies has been driven by a range of concerns, from criminal investigations to military espionage. The premise is that, because lying is a conscious activity, liars must ‘give themselves away’ and the ‘cognitive load’ (Vrij et al., 2010) of maintaining the lie will be subtly manifest in speech or behaviour. Studies have assessed the relevance of behavioural cues such as camouflaged smiling, reduced head movement, increased hand movements, increases in pitch, and speech affectations (Fielder and Walka, 1993). The lie detection industry has generated a number of techniques and technologies purporting to detect lies: polygraphs, statement validity assessment, voice-stress analysers, electroencephalograms and functional magnetic resonance imaging (Ekman and O’Sullivan, 1991; Leal et al., 2010; Stix, 2008). In some cases, these techniques are used by organizations, for example in pre-employment screening (O’Hair and Cody, 1987).

The literature on lying in organizational settings has focused on two distinct but related aspects: namely, the psychological and sociological factors influencing lying at the organizational, group and individual level and the moral neutralization techniques used by people who lie. The first body of literature focuses on the psychological and sociological causes and consequences of deceit. This literature recognizes that deceit is fundamental to work activities, including sales (Carson, 2001), business negotiations (Wertheim, 2016), job applications (Snell et al., 1999), employee reference writing (Kvalnes, 2014) and managerial reporting (Chung and Hsu, 2017). This research has produced numerous insights into the antecedents and motivations of deceit and dishonesty. Many factors influencing the propensity to lie have been identified, not only self-interest. These include emotion (Yip and Schweitzer, 2016), conflicting role demands (Grover and Hui, 1994), the type of information being falsified (Fulmer et al., 2009), the psychological cost of lying (Shalvi et al., 2011b) and the level of cognitive development (Chung and Hsu, 2017). Attitudes toward workplace deception have also been shown to be affected by perceptions of organizational fairness and equity (Gino and Pierce, 2010; Greenberg and Bies, 1992), power (Koning et al., 2011; Olekalns et al., 2014a), levels of rapport (Jap et al., 2011), social distance (Ackert et al., 2011), the degree of rivalry and beliefs about competition (Kilduff et al., 2016; Roulin and Krings, 2016), pro-socialibility (Levine and Schweitzer, 2015; Steinel et al., 2010) and perceptions of trust and integrity (Haselhuhn et al., 2017; Olekalns et al., 2014b).

In addition to these more psychologically grounded theories, which are typically based on findings from attitude surveys and experiments, other theories grounded in the organizational literature and derived from interviews and case studies have been developed. These studies have identified the role of organizational factors such as training, socialization, organizational culture, organizational identification and power relations that serve to perpetuate and sustain systems of deceit in organizations (Brannan, 2017; Fleming and Zyglidopoulos, 2008; Jenkins and Delbridge, 2017; Kenny, 2017; Lindsey et al., 2011; Rhodes, 2016; Weiskopf and Willmott, 2013).

A further body of work, most directly relevant to our focus on moral accountability, has considered strategies for moral neutralization through which deceivers lessen the psychological burden of deceit. Grover (2005) argues that people seem to be driven to rationalize their lies, lest they be morally tainted by the act of deceiving others. Aquino and Becker (2005) used an experimental simulation of lies in a business negotiation and found three techniques of moral neutralization used by those who lied: minimizing the lie, denigrating the target of the lie and denial of the lie. The selection of neutralization strategy was also found to be affected by the climate of the simulated negotiation and the consequences of the lie. Tasa and Bell’s (2017) experimental simulation of deceit in a negotiation situation also found that the person’s ability to morally disengage with and ‘neutralize’ the consequences of the deceit influenced their willingness to engage in deceit (see also Shalvi et al., 2011a).

We take up the same question as this body of work, but proceed in a different way, in line with our practice-based ethnomethodological approach. We probe how people spontaneously deal with the moral implications of deceit in situ. Our research question asks how moral neutralization is accomplished in practice through accounting work. We focus not on the pyschology of the liar but rather on thoroughly social processes through which actors manage the moral implications of their actions in the immediate aftermath of a false claim. A practice-based approach to the study of deceit is noticeably absent from existing literature. This is perhaps not surprising. It is relatively easy to study lies in experimental settings and measure attitudes to lying in surveys, but much harder to study lies in situ. There is the problem of access and finding organizations willing to let researchers study lying as it happens. Brannan (2017) has arguably got the closest to the practice of lying, studying the act of deception ethnographically from within an organization where he was an insider. We build on and advance this work adopting an ethnomethodological approach, which we will now outline.

Research approach and methods: An ethnomethodological study of ‘lying’

This article offers an ethnomethodological ‘respecification’ (Garfinkel, 1991) of ‘lying’. The concept of respecification (Garfinkel, 1991) involves three steps: firstly ‘take a methodological distinction or problem’, such as the difference between truth and lies in our case, secondly ‘treat the problem as a matter of routine local relevance for a particular kind of practical inquiry’, such as sales, telemarketing or debt collection in our case, and then thirdly analyse how ‘members make use of the distinction, and how they handle any problems associated with its use’ (Lynch et al., 1996: 273). Rather than treating lies as pre-existing entities, ethnomethodological respecification means studying ‘fact production in flight’ (Garfinkel, 1967: 79). A false claim might be treated as a ‘lie’, or it might be accounted for and transformed into something else. Any claim that is later shown to be ‘false’ can be opened to moral scrutiny, with or without anyone being directly accused of lying. Thus, we prioritize members’ accounting work through which they spontaneously establish, or deflect or deny, the moral inferences of falsehoods. The ethnomethodological approach means we do not judge whether members’ accounts are accurate and are ‘indifferent’ (Button, 1991: 86) on this matter. Our aim is not to decide whether people really were lying or not. Rather, as Heritage (1984: 141) proposes: the question of whether and how mundane descriptions are evaluated, interpreted, accepted or contested – and in terms of what criteria and considerations – is an empirical one. As such, it must be subjected to empirical scrutiny rather than determined a priori.

Ethnomethodology is based on a ‘central recommendation’ to study the ‘“reflexive” or “incarnate” character of accounting practices’ (Garfinkel, 1967: 1). Methodologically, the notion of ‘accounting practices’ is separate from the wider notion of ‘accounts’. In interpretative research, analysts collect accounts through interviews, diaries, and so on. For example, in Jenkins and Delbridge’s (2017) interview study of VoiceTel, when talking to staff about lying to customers, one HR manager produced the account that customers have ‘no real need to know’ (Jenkins and Delbridge, 2017: 60). To transform this into an accounting practice, it would be necessary to remove it from a research interview, and place it in a situated work practice. If this account was produced by a VoiceTel employee when accused of lying by a customer during their work practice, it would then be an accounting practice, in the sense that it accounts for the prior accusation in a particular way. It accepts rather than denies that a lie has taken place, and is defiant rather than apologetic. Accounts are ‘about’ work, whilst accounting practices are ‘of work itself’ (Strauss, 1985). This is why Garfinkel (1967) calls accounting practices ‘reflexive’ or ‘incarnate’, because they do not reflect upon events, but reflexively constitute them. By studying accounting practices, we therefore extend the reach of prior organizational research on lying.

This article draws on examples from three work settings where lies are typically expected to be commonplace: sales, telemarketing and debt collection (Goffman, 1971; Grover, 2005). The first study was of a sales environment is a busy high street, where a Big Issue vendor sold magazines to passers-by. The Big Issue is a magazine sold by homeless or vulnerably housed people. The second study was of a medium-sized direct marketing firm, who supply a range of services including ‘market research’, ‘training’ and ‘appointment setting’. Our data relate to ‘lead generation’ work where telephone agents call up people to book appointments for sales representatives. The third study was of recordings of phone calls between a third-party debt collection agency that acted on behalf of their clients to collect debts from companies who owed money from unpaid commercial invoices. An overview of the three datasets considered in this article is provided in Table 1, and the research consent and confidentiality process undertaken in each of the three studies is outlined in Table 2.

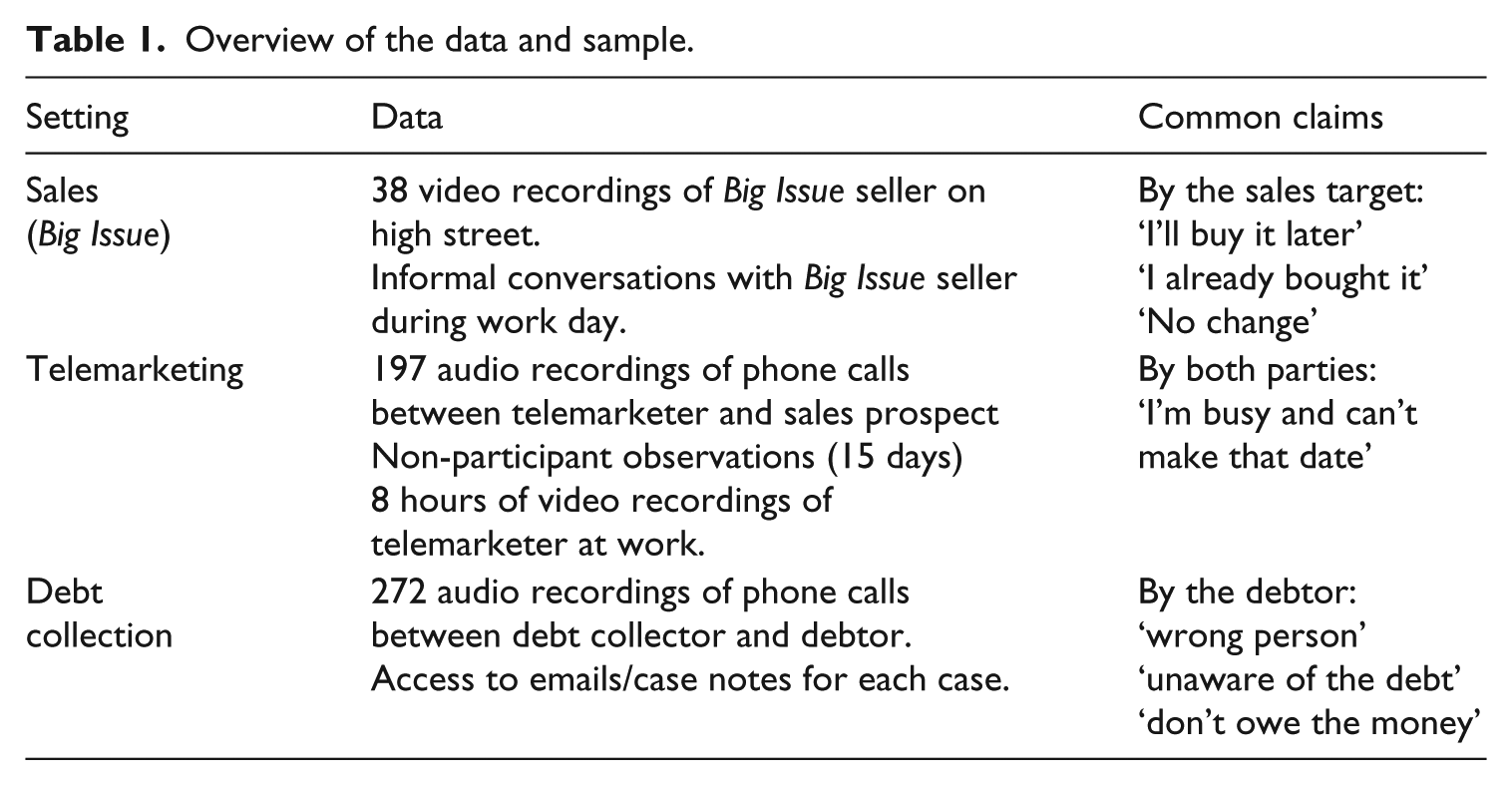

Overview of the data and sample.

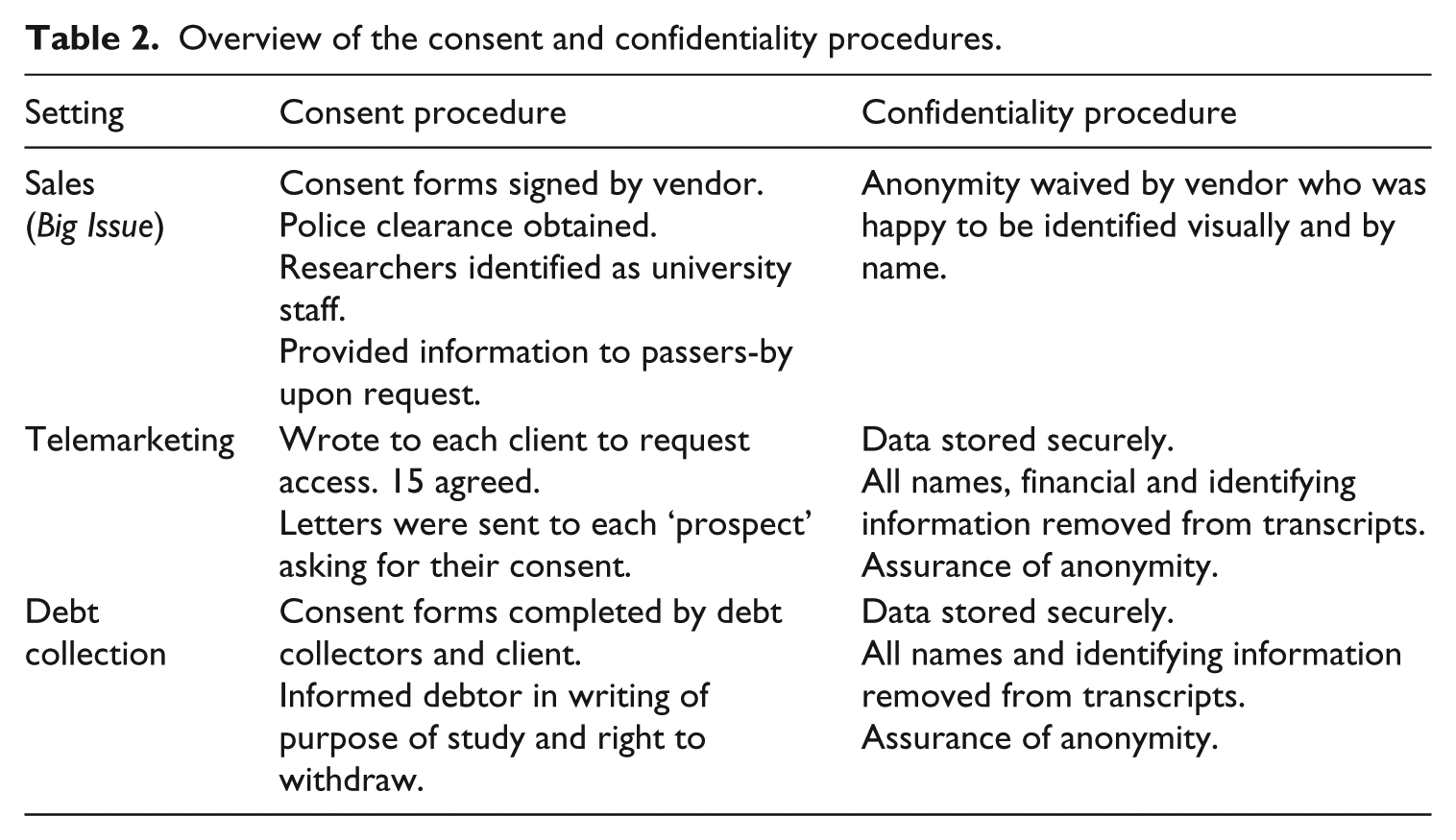

Overview of the consent and confidentiality procedures.

For this article, we analysed only the audio and video recordings of work practice, which were transcribed using the Jefferson (1984) notion system used by ethnomethodology and conversation analysis (EM/CA). Rather than searching our transcripts for the terms like ‘lies’ or ‘lying’, we looked for occasions where initial claims are later shown to be false, finding a total of only three examples, which are analysed in this article. This provided us with a suitable ‘collection’ (ten Have, 2004: 52) – a methodological approach widely used in ethnomethodology and conversation analysis, alongside single-case analysis, involving identifying a number of cases of well defined phenomena for detailed analysis (Schegloff, 1988).

False claims are a suitable site for analysing the accountability of deceit because, whilst not all false claims are lies, all lies involve false claims. False claims are ‘lies’ if the speaker knows them to be false; they may be ‘mistakes’ if they did not. Our analytic work focused on how participants both (a) held others to account for, and (b) produced accounts of, the discrepancy between the original claim and the unfolding events that rendered the original claim false. We worked through each case, drawing on methodological resources from conversation analysis (CA), a field allied to ethnomethodology (Sacks, 1992). One principle from CA is particularly important for our analysis, namely the idea that activity is sequentially organized. CA draws attention to how each turn at talk publicly displays a way of accounting for what has gone before, thereby generating a public record that is available to the recipient and the analyst alike (Sacks et al., 1974). An original claim that is later contradicted and shown to be false, for example, can be accounted for as a deliberate deceit, an innocent mistake, a realization, and so on. In line with ethnomethodological principles, then, our analysis sought to understand the ‘architecture’ of members’ own accounting work, as a reflexively embedded property of unfolding sequences of talk and embodied activity, rather than replacing this with a second-order theory of what people are doing and why (Button, 1991).

‘Rigour’ from within an ethnomethodological and conversation analytical (EM/CA) approach is not about things like sample size or the strength of correlations of variables. It is achieved by identifying an interactional phenomenon (in our case false claims) and systematically analysing the sequential structure of the talk-in-interaction (and associated non-verbal actions) in order to reveal the patterns in how people co-produce social reality in and through their interaction (ten Have, 2004). The approach demands that the researcher gets close to the ‘practice’ being studied, typically by recording it and slowing it down for repeated analysis, in order to identify the ethno-methods (members’ ‘methods’ or ‘practices’) being employed (Llewellyn and Hindmarsh, 2010).

As the analysis of the three extracts progressed, we became increasingly focused on the role of knowledge in the way actors managed the moral implications of false claims. The data began to reveal a suite of epistemic practices (Stivers et al., 2011) through which participants negotiated what they, and others, might reasonably be expected to know or might reasonably claim to have forgotten or not known. In what follows, we present our analysis of how people accomplished the transformation of ‘lies’ into ‘mistakes’ in one of three ways: by ‘discovering’, ‘noticing’ and ‘remembering’ various pertinent pieces of knowledge related to their prior claims.

Findings: The defeasibility of lies

Discovering

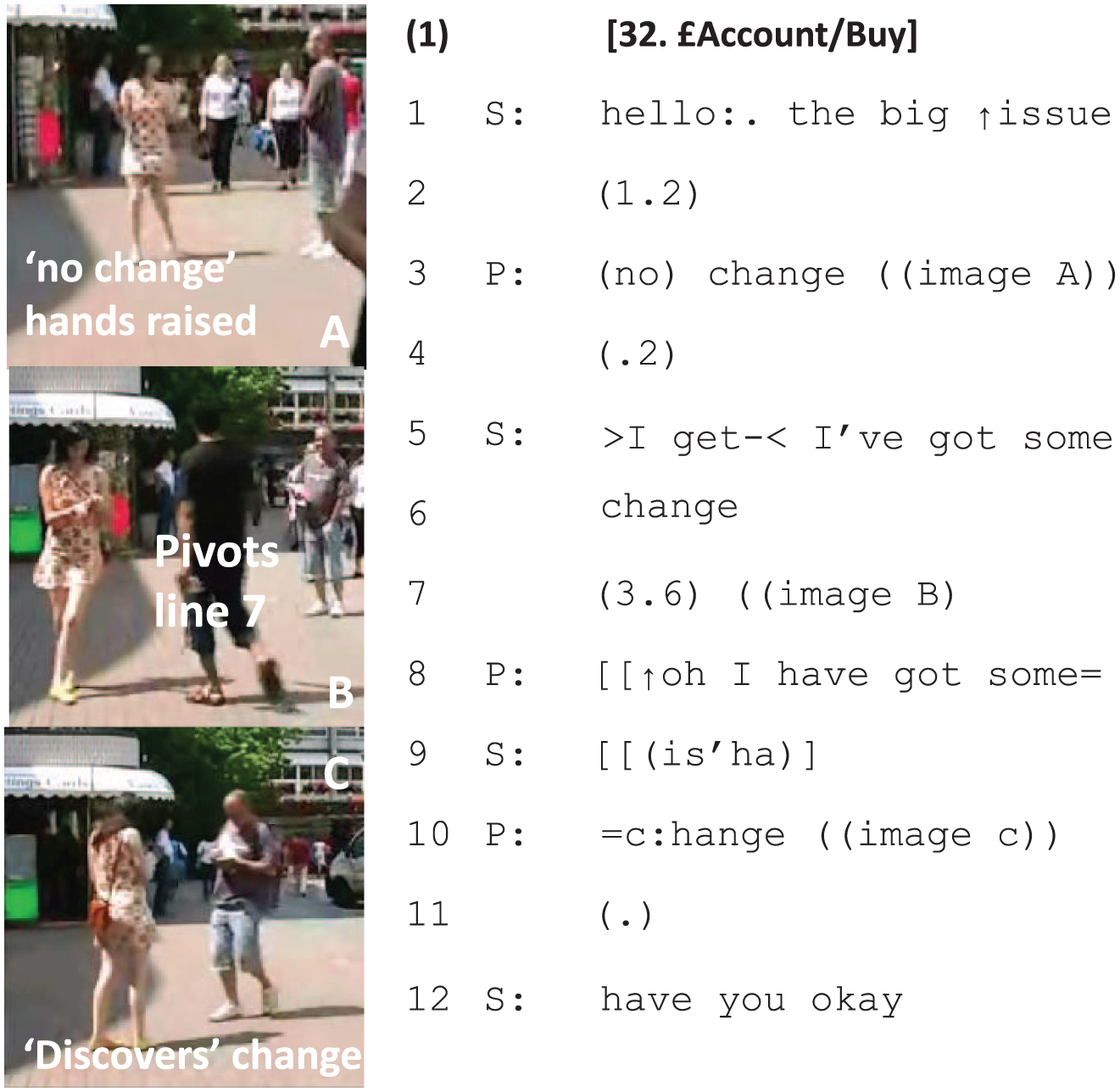

We start with two straightforward examples, where relatively little was at stake, before progressing to a more complex and consequential third case. Whilst being relatively innocuous and straightforward, Figure 1 illustrates how actors handle the moral implications of false claims through reference to epistemic states, in this case through a ‘discovery’.

Discovering.

At the beginning of Figure 1, a passer-by walks toward the magazine seller, who is selling the Big Issue on the high street of a busy city centre. The seller first ‘pitches’ his wares, saying ‘hello, the Big Issue?’ To avoid purchasing the magazine, the passer-by can either ignore the seller, decline the offer or produce an explanation of some kind. She does the latter. She says ‘no change’, rather than ‘no money’, and this implies she has a note of some denomination in the purse she is holding in her right hand. But she is walking away rather than stopping. From her embodied conduct, it seems that having ‘no change’ is a deal breaker.

‘No change’ is the target claim in this first extract (Figure 1). Is ‘no change’ a lie, something the passer-by knows to be false? It would be an understandable lie. Her private reasoning may be relatively benign: ignoring the seller might seem rude, whereas directly saying ‘no’ might be blunt (Grover, 2005: 149). Her response preserves her moral identity (Danby and Emmison, 2014) as someone who would be willing to support the homeless charity, if only circumstances were different.

What kind of ‘inferential labour’ (Llewellyn and Hindmarsh, 2013) does the seller deploy to make sense of the ‘no change’ accounting? The seller has two options. He can infer that ‘no change’ was an indirect way of saying ‘no thanks’, which he could also infer from the fact that she is walking away. Alternatively, he can make sense of it as an expression of interest: a matter of ability not lack of willingness. Although the first might arguably be the most affiliative response, the vendor also has to make a living. The seller takes the second option and says ‘I’ve got change’ (lines 5–6). The situation is now entirely changed, perhaps in a way the passer-by did not anticipate. If she does not stop and buy the magazine, her earlier response may seem disingenuous, because it implied a willingness to buy the magazine. Within a matter of seconds, the passer-by is thrust into a changed ‘situation of choice’ (Heritage, 1984). She stops, turns, and slowly walks toward the seller, opening her purse.

It is only at this point that we get to matters of potential deceit. The problem is that her purse reveals that she does have change and she does not have a note. If she is going to buy the magazine, there is no way of hiding this. To purchase the magazine, she can only use coins and thereby reveal her earlier claim to be false. She is between a rock and a hard place: she can either walk away and thereby undermine the implied willingness to buy in her initial utterance, or purchase the magazine and reveal her claim to be false.

At this point a lie has not been revealed. Certainly, her original claim has been shown to be false, but to reveal a lie, there is also the question of knowledge, and thus intent. For it to be a lie, the author of the claim has to know it is false (Fallis, 2009: 33). If knowledge is at the heart of lying, then, at the level of practice, accusations of deceit hinge on people’s ability to determine locally what speakers know, in this case about the contents of a purse. In terms of ‘practical epistemics’ (Heritage, 2012), is the presence of change in the purse she is carrying something she should have known about in advance?

Returning to the extract, the passer-by looks in her purse and says ‘oh, I have got some change’ (lines 8 and 10). That is, she discovers she has change, because you can only discover things you previously did not know. She reveals the claim to be false through an epistemic accounting device. Her utterance is prefaced with the change of state token ‘oh’ (Heritage, 1984), which artfully expresses the sense that she now knows something that, only moments earlier, she did not. Through this response, the false claim is retrospectively constituted as a ‘mistake’ and not a ‘lie’.

The vendor is now himself in a position of choice. Should he ‘go along’ with these ‘defensive measures’ (Goffman, 1974)? Or should he point to an act of deceit? Perhaps unsurprisingly, he goes along with her accounting. There is presumably no point in querying the moral identity of the passer-by at this stage, just as she is paying. Although he could take a sceptical stance toward her account, he goes along with it, treating the ‘discovery’ as a newsworthy matter (‘have you, okay’), not as an attempted cover-up.

In this initial extract, we have started to illustrate an ethnomethodological respecification of deceit. We do not see deceit as individual behaviour, or as a cultural phenomenon (Jenkins and Delbridge, 2017), but rather as a form of social practice. In this case, regardless of whether she was telling the truth, the passer-by has to ‘discover’ the change in her purse if she does not want to be seen to have lied. This constraint applies regardless of her ‘actual’ intent or knowledge. As a publicly accountable phenomenon, lies do not reflect the speaker’s inner motives, but their practical accomplishment of ‘knowing in practice’ (Orlikowski, 2002). In this first empirical case, the lyrical upward intonation used to say ‘oh, I have got some change’ (lines 8 and 10) stops this being a confession of deceit and accounts for her prior claim as an honest mistake.

Noticing

The second introductory example (see Figure 2) is taken from the study of business-to-business telemarketing. In this case a telemarketer is called-out for lying, but the telemarketer resists the accusation, treating it as defeasible, and presents an alternative accounting. As the extract begins, the telemarketer (T) is trying to schedule a date with a prospect (P) for a sales meeting. The telemarketer’s job is to fill the diary of the sales representative, Sally (all names are pseudonyms), with appointments. The telemarketer has just opened Sally’s electronic diary and she makes public her ‘reading’ of that diary. The telemarketer says there is ‘[nothing] for this week’ (line 4) and the ‘next available appointment is on the ninth of October’ (lines 8–9 in bold). This is the target claim (line 9), which is later shown to be false (line 16).

Noticing.

As it turns out, 9 October is not good for the prospect (‘not at all’, line 11), who states he is ‘off for that week’ (line 13). The telemarketer has to start again. She returns to the appointment schedule and offers a new slot, but one that is in fact earlier than the first one (which she claimed was the earliest one available), 3 October (line 16).

For Sacks, lying is ‘perfectly observable in the same way that anything else is’ (Sacks, 1992, LC1: 559). One practical resource available to actors to observe lies are contradictions. In our data, contradictions are at the centre of the mundane model people used to observe deceit (Lynch et al., 1996). Here, the telemarketer has said one thing (‘next available appointment is . . . the ninth of October’, lines 8–9) but then said another (‘I can do Tuesday the third’, lines 15–6), and crucially without accounting for the discrepancy. Moreover, she has done this in response to the prospect’s prior action (‘I’m off that week’, line 13) and so her response may seem ‘motivated’ and ‘strategic’ (Jenkins and Delbridge, 2017).

The employee has slipped up, whether she is lying or not. The prospect immediately orients to a lie rather than a mistake. He produces a mundane act of whistle-blowing – an action that makes unethical practice public (Kenny, 2017). This whistle-blowing is initially accomplished through laughter (line 17). The prospect’s laughter orients to the telemarketer’s response as a ‘lie’ rather than, say, an honest mistake. He is not laughing at her incompetence. The laughter is a ‘document’ (Garfinkel, 1967) of a ‘scam’, a stance he maintains throughout the remainder of the interaction. The phrase ‘that old chestnut’ (line 20) is often used disapprovingly to refer to a tired old joke or story that has been too often repeated, a reference here to a typical ‘sales trick’ that involves making a promotion seem more time-limited or in demand than it actually is.

But was the telemarketer ‘lying’? This again turns on the question of knowledge, and thus intent. For it to be a ‘lie’, the author of the assertion has to know it is false (Fallis, 2009: 33). In this case, the telemarketer treats the accusation as defeasible. As with Figure 1, she makes relevant her knowledge, quickly invoking a relevant detail that changes the frame. She claims to have noticed something new when re-reading Sally’s diary. She describes only now seeing an appointment that is still showing on the schedule has been cancelled, invoking the difficulty of reading the small, and thus easily overlooked, lettering saying ‘cancelled’ on her screen (lines 23, 25–27). In her accounting work, the prospect has got the ‘wrong end of the stick’. It was an innocent mistake according to the telemarketer, not a lie derived from a sales trick.

This case powerfully reveals the sequential architecture of deceit. In this brief sequence, we have five main actions:

(1) An initial claim (‘the next appointment is the ninth’);

(2) Which is declined by the prospect (‘I’m off that week’);

(3) A second and contradictory claim (‘we can do the third’);

(4) An accusation of deceit (‘hahaha, but you said’);

(5) The ‘noticing’ (‘no, no, no, I’ve just realized’).

Why does this sequential architecture matter? Suppose the sequence was re-ordered. For example, imagine the accounting device (position 5) had been produced earlier (position 1), while the prospect was pondering his availability. What if, before the prospect said ‘I’m off that week’ (position 2), the telemarketer had said ‘oh, hang on, I’ve just noticed Sally is free on the third, is that any good?’ The sense of deceit would presumably be eliminated. What if the accounting device had prefaced the second contrary claim (position 3), so it became: ‘oh, I’ve just noticed Sally is free on the third, it says cancelled here in very small letters, is that any good?’ The sense of deceit would also presumably be reduced. The telemarketer’s moral problem is that the accounting device is invoked after the second contrary claim, and after the prospect has oriented to it as a lie derived from a sales trick. It therefore sounds like she is ‘covering her tracks’. This applies regardless of whether she was actually telling the truth.

Returning to the extract, the prospect overlooks the telemarketer’s accounting work and maintains his framing of her as dishonest, laughing throughout lines 23, 25 and 27. But he is not displaying moral outrage. He orients to a ‘playful deceit’ and ‘benign fabrication’ (Goffman, 1974: 87), one of the well-known ‘bluffs’ (Goffman, 1974: 102) that are part of the rules of the game in sales settings. Despite the telemarketer’s accounting work, the prospect sustains the deceit frame right to the end of the interaction (‘oh, that was good, that was’, line 25). There is no single ‘definition of the situation’ (Goffman, 1959) in this case. The action is simultaneously accounted for in two ways: as a ‘lie’ (prospect) and as a ‘noticing’ (telemarketer). In this case, the prospect has nothing to lose by orienting to a deceit, but nevertheless does so in such a way that reflexively constitutes a ‘benign’ rather than ‘coercive’ fabrication (Goffman, 1974). They continue the interaction on good terms and proceed to book the appointment.

Remembering

The first two cases conform to a particular architecture of deceit, where one party potentially ‘slips up’. The recipient momentarily ‘sees through’ a performance. What they ‘see’ are not ‘facts’ – in Figures 1 and 2 the relevant parties could have been telling the truth – but there also existed practical grounds for orienting sceptically towards some prior action. In the next case, we move to a different kind of case, where a debt collector strategically pursues a debtor to elicit a confession of deceit. Across numerous interactions (text messages, emails and phone calls) the debt collectors build up a sense that ‘something is going on’, orienting increasingly sceptically to a series of denials. The debtor does not confess to having lied but instead produces an account of ‘remembering’.

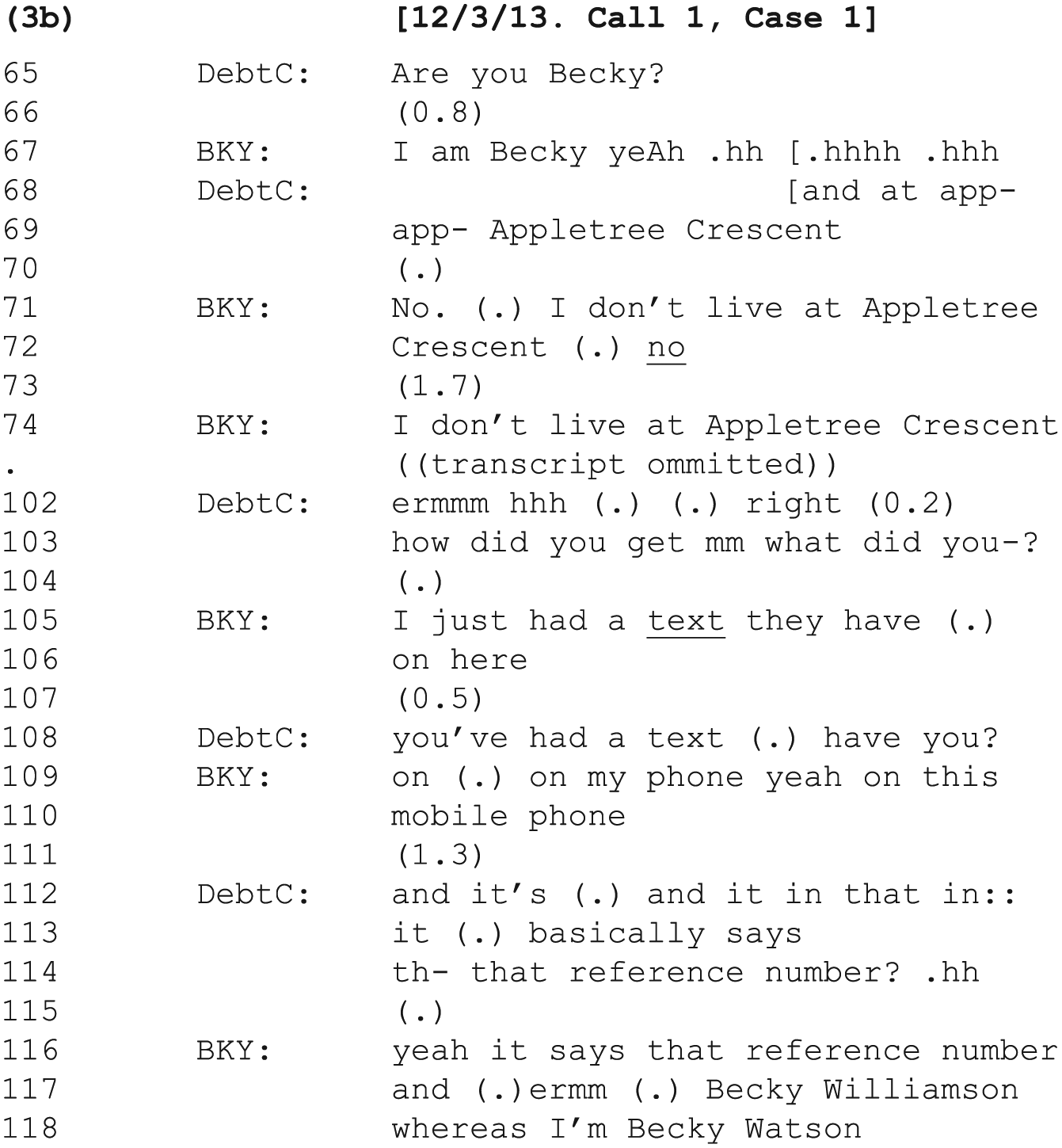

The case in question concerns the purchase of a horse saddle at a price of around £1000. The saddle was deemed faulty by the customer, a small business owner, and returned for repair without full payment being made. The seller, the client of the debt collector, pledged to have it repaired and meanwhile lent the customer an equivalent saddle to use whilst the repairs were being made. At the time of the calls analysed below, the debtor has received the repaired saddle but claims it is still unsatisfactory. She is yet to make the final payment, and she has not returned the loaned saddle.

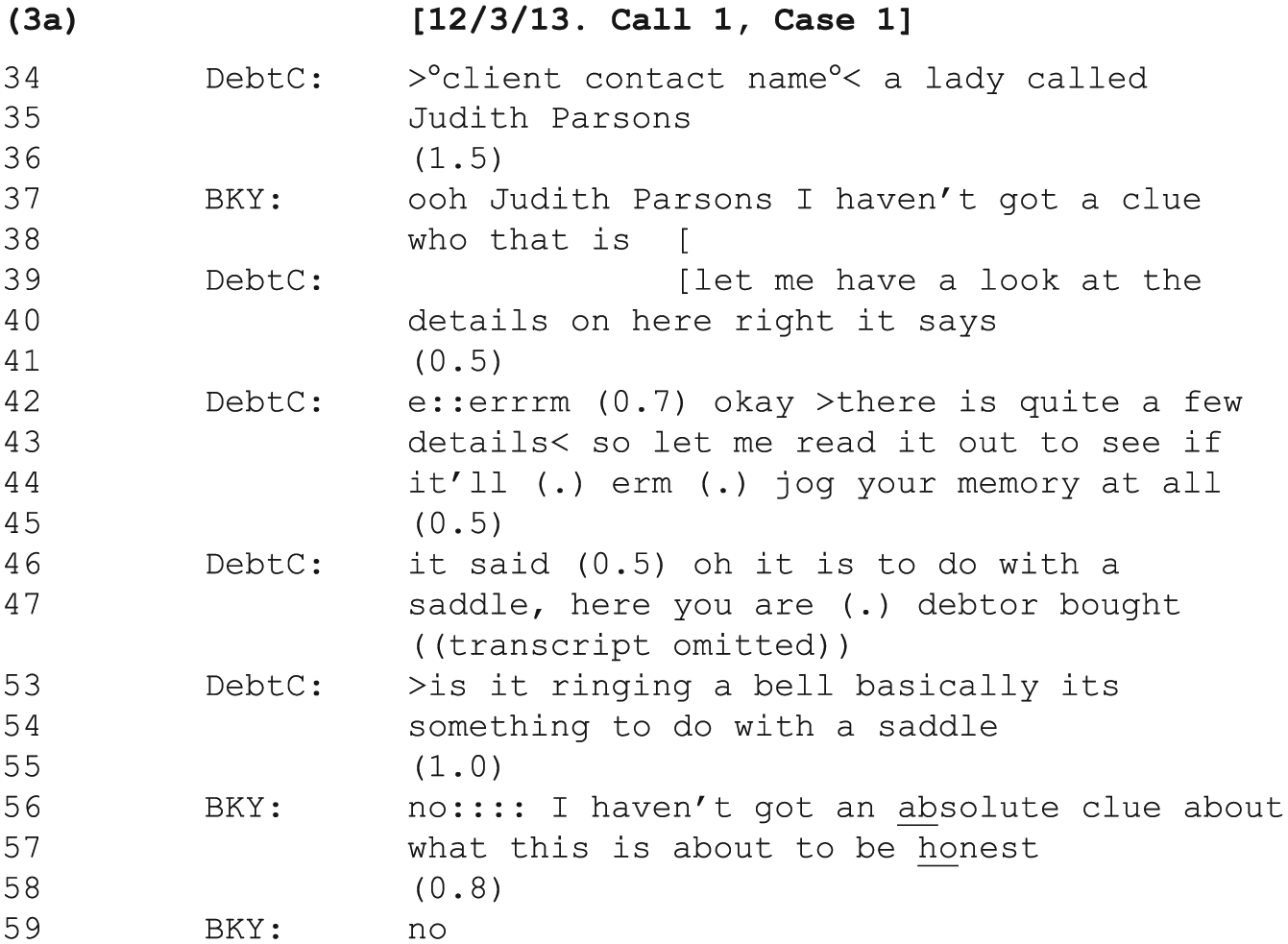

As we join the interaction, a person called Becky (all names are psuedonyms) has called the agency and is speaking to Amy (the debt collector) in response to a text message she received moments earlier (Figure 3). Becky begins by giving an account number, from the text message, which Amy inputs into the system. Amy then reads the details of the case, giving the client’s name (Judith Parsons). Amy describes a ‘saddle’ that was purchased and details some of the particular circumstances of the case. Becky is bewildered and claims to have no knowledge of the debt. Amy describes more of the details of the case to see if they might ‘jog your memory at all’ (lines 43–44). This practice establishes an interactional ‘slot’ in which the debtor can, if she is indeed the debtor, innocently claim knowledge of the purchase and identify herself as the debtor. This does not happen. Becky claims she ‘does not have an absolute clue’ about any saddle. This is the target assertion (lines 56–57). Is she telling a lie and trying to avoid responsibility for her debt, or is this in fact a case of mistaken identity?

Remembering (Amy: 3a).

Amy then proceeds to draw out three details that will eventually go on to play a role in Becky’s identification as the debtor (Figure 5). The first is the address. Becky does not live at Appletree Crescent. However, when she later gives her address to another collector, it is just a few miles from Appletree Crescent. The second detail is her name. She is not Becky Williamson, but rather Becky Watson. Third, there is the telephone number. If she is not the debtor, how did the client have her number in the first place, for the text message to have reached her (lines 102–104)? This might be an innocent error, but it seems remarkable to the debt collectors that the number should belong to another person also called Becky. Amy builds the sense of a puzzle but she also plays her role with discipline; there are no ‘unmeant gestures’ (Goffman, 1959: 210) that might ‘give off’ a sense that she is already deeply suspicious.

Remembering (Amy: 3b).

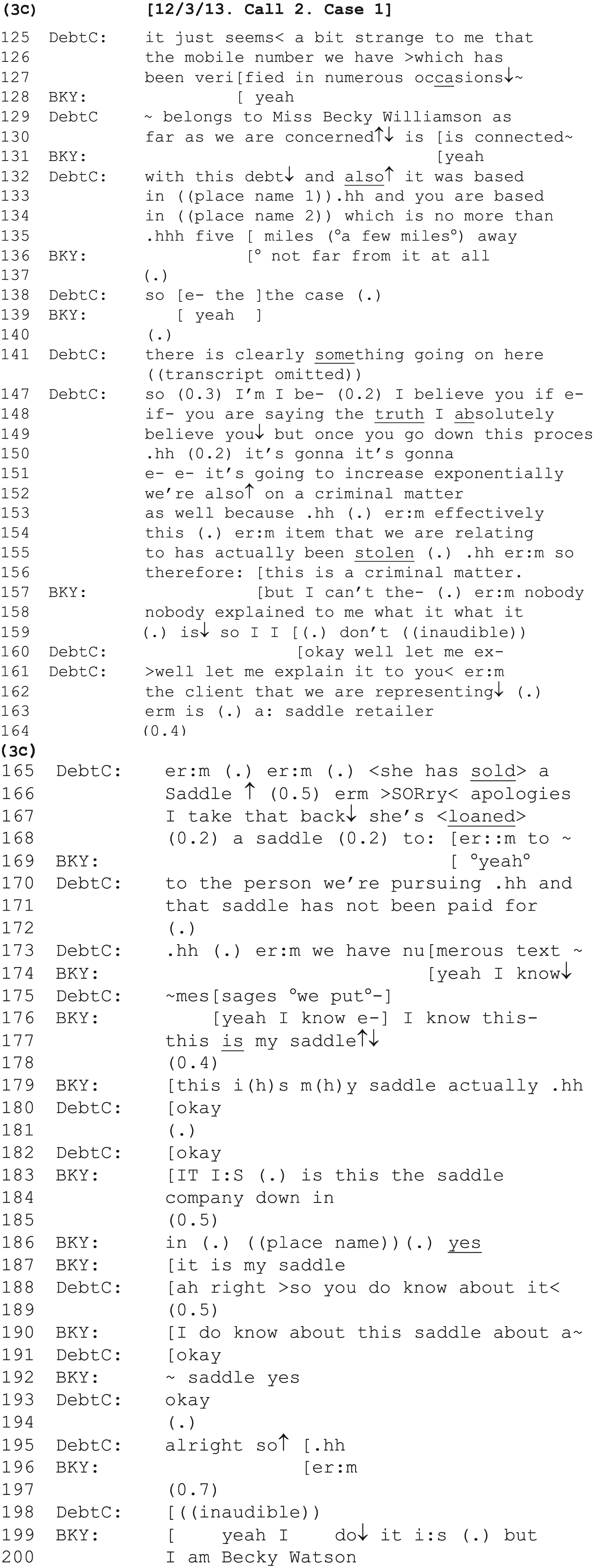

Remembering (Dave: 3c).

Amy’s work here is delicate. Notice how she does not apologize for bothering the caller, even though Becky has stated unequivocally that she knows nothing about the saddle and is not Becky Williamson. She keeps the caller on the line too, and works through the details. Amy plays the ‘good cop’. The frame is that of a ‘puzzle’ (Goffman, 1974). The caller is carefully forestalling ‘the immediate impression that [she] might be what [she] is’ (Goffman, 1959: 219), while the debt collector is carefully forestalling the impression that she is pursuing someone she believes could be lying.

The call with Amy is closed on entirely cordial terms. Fifteen minutes later, Amy’s colleague, Dave, calls Becky back (Figure 5). He has been briefed on the details of the case. Building on Amy’s previous work, Dave begins the call by orienting sceptically to her claim to know nothing about the saddle. The definition of the situation provided by Becky, that this is a case of mistaken identity, has not been accepted fully but neither has it been rejected outright. While he allows for the ‘mistaken identity’ frame (‘if- you are saying the truth I absolutely believe you’, line 148–149), he also finds something ‘strange’ in the close relationship between the details of the caller and the debtor (address, name and phone number) and concludes there is ‘clearly something going on here’ (lines 140–141). He seeks to extract a confession (from line 147) by invoking the potential financial and criminal implications of deceit (lines 151 and 156). Even then, though, he refers to ‘to the person we’re pursuing’ (line 170) and does not assume that is the person he is speaking to, allowing for the possibility of mistaken identity rather than strategic deceit.

This case is especially powerful as an illustration of our ethnomethodological approach. From our access to the details of the case as it progressed in the weeks that followed, we learnt various things. For example, the collectors learn that ‘Williamson’ was her married name, and that when married she had lived at Appletree Cresent. She did buy a saddle from the client and was involved in a protracted dispute about it. But these apparent ‘facts’ do not automatically translate into accusations of deceit followed by confessions. As we have seen, people find alternative ways of accounting of such discrepencies.

Becky begins her accounting work by claiming nobody has explained the debt to her (lines 157–159). As with Figures 1 and 2, the immediate matter of relevance then is knowledge: what the speaker can reasonably claim to know (and not know) about the matter at hand. From her account, even if she is the debtor, Becky cannot be lying because she has not been told what debt is being discussed. Perhaps she orders many saddles in the course of running her business and cannot remember the details of each one? This new accounting is thus rather neat and also suits both parties. If accepted as true, the claim ‘wipes the slate clean’ and deletes the moral implications of her previous claims. It creates a new definition of the situation out of which she can listen to the details and then remember the saddle without having appeared to have lied.

The debt collector then explains the debt, and the caller has a ‘moment of clarity’. She now ‘remembers’ the purchase. The interactional work is quite elaborate and pertains to her agency and cognition. It is not only that she now remembers she bought a saddle and then returned it and had one loaned to her while it was repaired, but also that this is surprising to her (‘this is my saddle actually’ ‘It is!’, lines 179 and 183). It is a revelation, but it is still not absolute: further checks are required. To be definitive, in her own mind, she needs to check and corroborate further details. She asks whether the debt concerns a company in a particular town in the South of England. Following the response, in further surprised tones, she exclaims ‘yeah I do it is’ (line 199).

There is one final way in which she forestalls the impression of being false. In response to her ‘moment of clarity’, the debt collector draws attention to the change in her position (‘ah right so you

Discussion

Our study has generated two main insights into the practical organization of deceit from studying the interactional architecture of false claims. Firstly, we observed a pattern of suppressing accusations of wrong doing. Sellers and telemarketers have an institutionalized incentive not to ‘recognize’ deceit publicly. Hence, the Big Issue vendor knew people ‘fobbed him off’ on a daily basis. Rather than saying ‘no thanks’, people would say ‘no change’, ‘I’ll buy it later’ or ‘I’ve already bought it this week’. In each case the vendor developed set responses, none of which oriented to the passer-by as a liar. ‘No change’ was accounted for as a problem he might solve (as in Figure 1). ‘I’ll buy it later’ was oriented to as a ‘timing issue’. ‘I’ve already bought it’ was simply met with ‘thanks’. None were oriented to as a lie. His work practice was to cultivate a body of regular customers, and accusing people of deceit would presumably be a false move in his practice. Likewise, telemarketers knew prospects would often falsely claim to be busy, rather than directly saying ‘no’ outright. Telemarketers accounted for such claims, not as lies, but as descriptions of a scheduling problem. In Figure 2, it was the prospect who ‘called out’ the lie, but also minimized its moral import: it was a mere ‘trick of the trade’, rather than a moral breach sufficient to seriously disrupt the business of the call.

The debt collector also had no interest in ‘calling out’ debtors for lying. In Figure 5, the debt collector came close to such a move when the debtor eventually ‘remembered’ the saddle (line 188). At that point, an accusation of deceit would presumably risk destabilizing the debtor, perhaps leading them to hang up just at the point they ‘remembered’ the debt and the payment negotiation could begin. The debt collector’s job, after all, is not to judge the moral identity of the debtor (although they may well have such private thoughts, just as debtors might have private thoughts about the moral identity of debt collectors as well). Their job is to recover the debt. We can conclude, therefore, that when potential ‘lies’ are uncovered, there are a series of ‘good organisational reasons’ (Garfinkel, 1967) for not labelling them as such.

Secondly, our study has shown that in situations where deceit is potentially ‘surfaced’, it is accompanied by skilful accounting work that muddies the waters of any neat classification. This is quite different from saying ‘people are good at lying’. Such an argument hinges on the idea of lies as unproblematic social facts. In contrast, we have approached lies as on-going accomplishments (Garfinkel, 1967). People who know they are telling the truth can nevertheless be seen to have lied if their public presentation or accounting work is incompetent. Goffman (1959: 219) gives the example of the honest merchant who can be falsely viewed as a con artist. In Figure 1, the customer has to ‘discover’ change, or she would be seen to have lied, regardless of whether she ‘actually’ knew she had change in her purse. From this practice perspective, the issue is therefore not one of intent (Fallis, 2009), but of the accountability of practical action. The ‘discovery’ has to be accountably ‘authentic’ for the customer to cover her tracks, regardless of her motives. Theoretically, we have introduced a new approach, one that decouples lies from agents and their beliefs and intentions, focusing instead on patterns of public accountability. This approach has enabled us to show that when people ‘slip up’, and give off a sense of potential deceit, they always found some way of re-framing the situation by accounting for a simple ‘mistake’. In each case we have analysed, although the accounting devices were different, they all made relevant epistemic matters pertaining to the speaker’s knowledge (Heritage, 2012).

As a whole, this study has opened-up a new avenue in the study of deceit, respecifying (Garfinkel, 1991) it as a lay phenomenon. Rather than presuming ‘truth’ and ‘falsity’ are stable and easily separated, we have recovered a ‘mundane model’ (Hester, 1991) of deceit. The features of this mundane model are now summarized and contrasted with existing approaches to the study of deceit:

(i) In theoretical and philosophical literature (Adler, 1997; Fallis, 2009) lies derive from motives and intent. In practice, people do not have access to the minds of others, and instead ‘see’ potential lies from the way practical actions are put together.

(ii) ‘Lies’ are conventionally contrasted with ‘truth’ (Jenkins and Delbridge, 2017; Schein 2004; Serota et al., 2010). As a lay phenomenon, in our materials, ‘lies’ are contrasted with ‘mistakes’. This is the central ‘methodological distinction’ (Lynch et al., 1996); people labour to show a claim is false owing to a mistake, rather than a lie.

(iii) The ethicality of lying is said to hinge on ‘consequences’ and ‘motives’ (see Schein, 2004: 260). But at the level of accountable action, people can be seen to have lied even when they were telling the truth (Goffman, 1974: chap. 4). Hence, ethics from this practice perspective does not hinge on motives, but upon the competency of an actor within a practice: their ability to avoid missteps and skillfully account for missteps when they do occur.

(iv) In practice, people do not orient to the repertoire of hitches, perturbations and bodily ticks described in the psychological literature as methods of ascertaining the presence of a lie (Kraut, 1978; Serota et al., 2010; Vrij et al., 2010). To understand ‘lie detection’ in practice, a different substratum of phenomena needs to be engaged, including the formulation of claims, the sequential position of accounting devices and the appearance of contradictions.

(v) In practice, lies are defeasible and are best understood as on-going accomplishments (Garfinkel, 1967) rather than stable facts. Accusations of lying can be undermined. Attempts to undermine accusations can themselves be undermined. Even when it seems there is no way of avoiding a confession, a speaker might locate some line of argument that artfully deflects the actual or potential accusation of deception.

(vi) The defeasibility of deceit hinges on epistemics in interaction (Stivers et al., 2011). In our three cases, the defeasibility of deceit hinged on the speaker’s knowledge of the contents of their purse (Figure 1), what was showing on their computer screen (Figure 2) and details of their previous purchases (Figures 3–5). Actors handled the moral accountability of false claims by retrospectively ‘discovering’, ‘noticing’ or ‘remembering’ pertinent facts relating to their prior claim.

Taken together, we propose that these findings sketch a mundane model of deceit: a suite of lay resources and reasoning practices people use to handle ‘lies’ as commonplace interactional phenomenon.

Conclusion and implications

In recent organizational literature, a number of commentators have pointed to the lack of research on lying (Brannan, 2017; Grover, 2005; Jenkins and Delbridge, 2017; Schein, 2004). This is all the more notable given that lying is known to be an endemic feature of numerous industries, but especially perhaps sales and marketing (see Brannan, 2017; Clark and Pinch, 1995; Grover, 2005) and debt collection (Goffman, 1971), the focus of our three studies. A notable absence in existing literature is the in situ analysis of ‘lies’ as they surface in talk and interaction. The practice of lying, as an empirical phenomenon in and of itself, has been largely ‘black boxed’ by the current literature. To extend organization studies scholarship further, we have taken a practice-based approach to deceit grounded in ethnomethodology that analyses ‘lies’ as observable and reportable phenomena.

The idea that lies are ‘observable and reportable’ (Garfinkel, 1967) might at first glance seem contradictory. Existing research, reviewed earlier in this article, is based on the assumption that lies are private and mysterious, only detected indirectly through sophisticated techniques and replicable only in experimental settings. This idea underpins the lie detection industry as well. Polygraphs, voice-stress analysers and electroencephalograms identify signs of deceit from people’s voices and bodies (Ekman and O’Sullivan, 1991; Stix, 2008). In contrast, the American sociologist Harvey Sacks argued that the idea that ‘lies are undetectable because they are private is a figment of educated common sense’ (Lynch and Bogen, 1997: 101). As we noted earlier, for Sacks, lying is also a publicly accountable phenomenon that is ‘perfectly observable in the same way that anything else is’ (Sacks, 1992, LC1: 559). People detect lies from the way courses of action unfold, rather than from twitches, perturbations or pupil dilation (Grover 2005: 153). Sacks gives an empirical example involving a man who called a social services agency to report an argument with his wife (see Sacks 1992, LC1: 113). Quickly, and without any prior background knowledge of the caller, the call-handler accused the caller of ‘not telling the whole story’ (Sacks 1992, LC1: 113). From the structural organization of the story, and without access to the individual or the events being reported, the call-handler recognized that a false version was being presented. She detected a ‘lie of omission’ (Lynch and Bogen, 1997: 108).

In the organization and management literature, lies have been treated as relatively unproblematic objects. Lies have been treated as claims made by speakers who know them to be false (Adler, 1997; Fallis, 2009): such as the employee who pretends to be in the client’s office when they are not (Jenkins and Delbridge, 2017) and the call centre agent who pretends to be ‘activating’ the caller’s credit card when the call is merely a cover for selling add-on services (Brannan, 2017). Our study shows that, when they are surfaced as part of interactions, ‘lies’ are not so straightforward. Indeed, perhaps the most fundamental characteristic of ‘lies’ that this study has uncovered is that they are defeasible. If a speaker is accused of lying, or simply finds themselves in a situation where such an accusation could be inferred, they can and do craft an alternative accounting that resists or deflects this. The recipient, in turn, might treat this an attempt by the liar to ‘cover their tracks’: a lie to cover a lie (Grover, 2005: 152). Or they might instead align with the accounting, and orient to a simple misunderstanding or mistake. In some cases, as our study has shown, the question of whether it really was a ‘lie’ might never be settled once and for all, with multiple accountings and definitions of the situation co-existing.

By re-thinking lying in terms of the accountability of practical action, and analysing ‘fact production in flight’ (Garfinkel, 1967: 79), we can start to gain some leverage on the interactional architecture of lies. In experimental research, truth and falsity are not ‘up for grabs’ in this way. The experimenter is the final arbiter of truth and falsehood. In contrast, our study has found that in everyday life both false claims, and accusations of deceit, are very much ‘up for grabs’. By producing an account of a change of knowledge state (Heritage, 1984) – in our three studies this was accomplished through accounts of discovering, noticing and remembering – the moral standing of the false claim is transformed and the meaning of the prior stretch of interaction is transformed from a nefarious to an innocent frame. The moral accountability of a lie is, we propose, something of a ‘slippery’ phenomenon when faced with something as apparently simple as an account that transforms the knowledge state of the speaker (Heritage, 2012). We can therefore conclude that knowledge has forms of ‘morality’ associated with it, not only through the ways in which matters of epistemic access, primacy and responsibility are handled in interaction (Stivers et al., 2011). We have shown that accounts of changes in knowledge states are also woven into sequences of action that could be framed as ‘lies’. Just as the existing literature has identified psychological strategies for moral neutralization employed to lessen the psychological burden of the act of deceit (Aquino and Becker, 2005; Shalvi et al., 2011b; Tasa and Bell, 2017), our study advances this further by showing how people also use interactional strategies for moral neutralization to lessen the moral accountability of deceit, or even more fundamentally to deflect or mitigate the notion that an act of deceit has taken place.

To broaden out the implications of our findings, we propose that defeasibility is important not only for advancing the understanding of lying as a practical action but also more broadly for advancing our understanding of the perpetuation of cultures of deceit (Anand et al., 2005; Jenkins and Delbridge, 2017; Brannan, 2017). Prior literature has drawn attention to how organizations legitimize deceit through socialization processes (Jenkins and Delbridge, 2017), the development of convenient in-group rationalizations (Anand et al., 2005), the amplifying effect of feedback loops (Fleming and Zyglidopoulos, 2008), and systems of culture management (Brannan, 2017). Our explanation from the study of work practice extends this work further by providing evidence that the morality of work arrangements, even those thought to be underpinned by deceit, has to be preserved ritualistically through daily work practices (Brannan, 2017; Goffman, 1974) and that these practices are best understood as fluid, contingent, on-going accomplishments (Garfinkel, 1967).

Ours is one of the first naturalistic studies of deceit in the wider social sciences literature (see also Lynch et al., 1996; Sacks, 1992). Having completed the research, we perhaps understand why there are so few naturalistic studies. Our dataset was large, but ‘lies’ hardly ever permeated, or came close to permeating, the surface of publicly accountable discourse. Only once, in the second extract (Figure 2), is a deceit frame sustained through the course of the interaction, and then only by one party. We can therefore conclude that although deceit is presumably prevalent in the occupations we examined, it is typically beneath the surface of publicly accountable discourse. Even when it does permeate the surface, it remains a slippery phenomenon that is readily accounted for within a more innocent frame.

Our finding that people account for actions (in our case, false claims) by re-framing them in ways that seek to reduce or remove their moral upshot also has wider implications. The approach we have developed for studying morality-in-action can also be used to study other workplace actions that attract moral evaluations and are typically viewed as disgraceful, dishonourable or deplorable, such as aggression, insults, back-stabbing or discrimination. It remains to be seen in future research whether changes in knowledge state also feature in the accounts produced in situ in these situations. If, as Danby and Emmison (2014) state, people work hard to avoid any charge of being ‘bad’ or ‘immoral’, it is important that we build a body of knowledge that can identify the methods through which moral versions of the self are assembled and managed in real-time workplace interactions. By pursuing this research agenda, a cumulative body of work can be developed that maps the interactional practices through which morality is handled in practice.

To conclude, this article represents a distinctive step toward the development of a practice-based account of deceit. We have dealt with very narrow slices of work practice, often lasting for no more than a few seconds. At this level, in the typically unexamined routine of everyday life, people become expert at using accounting devices that enable them to account publicly for themselves as acting in morally acceptable ways in the face of an apparent ‘lie’. These practices, typically ‘seen but unnoticed’ (Garfinkel, 1967), supply the ritual foundations, not only of single interactions, but also of wider institutional arrangements that are stable despite the fact that they are potentially built on deceit. In this sense, we would argue that to understand socialization into an occupation that involves lying (Ashforth and Anand, 2003; Brannan, 2017; Jenkins and Delbridge, 2017), it is necessary to reveal how people learn an apparently mundane but important skill: to be competent within a practice that requires, at all points, that any sense of deceit and subterfuge is kept from the surface of publicly accountable discourse.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.