Abstract

The article examines the performance of cooperative credit movement in the last four decades of colonial Bengal. Despite high hopes at the beginning, the cooperative institutions proved unsustainable due to unusually high rate of loan default and consequently failed to play a role in rural wellness as promised. The article argues that the seeds of failure were ingrained in the movement as it was used as a tool to engage and contain nationalist and communist politics in the late colonial environment. The possibility of a successful experiment on the association of a global model of non-firm financial entrepreneurship with forms of local social capital that existed in Bengal was suspended by a political process which aimed at retaining the authority of the colonial state by privileging a select social group. Social capital, the cornerstone of cooperative movement, was ineffective in Bengal because it had to operate on a ground fiercely contested by political capital.

The global wave of the Raiffeisen-model cooperative credit movement reached Bengal by the turn of the twentieth century. Between 1905 and 1947, although there was substantial growth in the number and membership of cooperative credit societies at different levels of organisational structure, the movement failed as credit did not reach to an increasing number of needy rural population as it was crippled by an extreme extent of loan default. The default, in relation to both the principal and the interest, was visible before the global depression of the 1930s and reached the soaring 80 per cent in 1934–35 in most districts of Bengal. 1 Statutory annual audits, which included qualitative classification of credit societies, also showed ‘progressive deterioration’ during the years 1917–18 to 1934–35. On a comparative scale of loan default, Punjab appeared to be the best and Bengal the worst, where out of ₹40 million of cooperative loans, ₹30 million were defaulted by 1940. 2

The disproportional loan default in Bengal cooperative system was as much a failure of the institution itself as it was an indicator of the defeat of the whole Raiffeisen idea of what today is more known as ‘social capital’, trust being its cornerstone. Most regions of Europe had well-knit settled community, compact neighbourhood where people knew each other intimately, attachment to religious values and similar standard of living. Bengal seemed to have similar social ecology in which Raiffeisen model could thrive. Cooperative advocates in Bengal were well aware of this, as a commentator suggested this model was ‘suitable only for people living in a village who form a compact group, socially and economically, and who, therefore, are in a position to accept individual and collective responsibility for one another’s debt.’ 3 This view was endorsed by the government of Bengal by suggesting that this type of institutions were suitable for simple agriculturist, and no serious modification was necessary for its adaptation to ‘Indian conditions’. 4

At the initial stages, therefore, the prospect for Raiffeisen model cooperative movement in Bengal looked brighter, even by the world standard. For example, despite relative success in continental Europe, cooperative movement in Ireland failed considerably. Timothy Guinnane’s study records a number of factors existing within the specific economic and social environment of the region. These included the reluctance of prosperous local elite to get involved with their expertise and resources; lack of centralised audit systems; and the Irish ‘soft-mindedness’ in pressing on the repayment of loans by the neighbours. 5 In the USA, there were considerable doubt about the success of cooperative movement on account of its less compact rural neighbourhood and more assertive spirit of individualism. 6

So the question remains as to why, under the circumstances of relatively formative communitarian space, cooperative institutions failed in Bengal? This essay suggests that the failure in Bengal lies not so much in the difficulty of transplanting a foreign model of non-firm entrepreneurship into a new environment, but by the way existing range of social capital was unable to flourish under specific political conditions. It is argued here that the failure of the cooperative institutions to use social capital to develop a viable and effective community platform was hastened by the way the colonial state, the principal sponsor of the movement, sought to secure among the cooperative investors and organisers a political support base at a time when anti-colonial national movement was taking momentum. In other words, social capital, the cornerstone of cooperative movement, was ineffective in Bengal because it had to operate on a ground fiercely contested by political capital. To look at the performance of an economic institution from the vantage point of political process could be, it is hoped, complementary to the existing disciplinary debates about cooperative institutions. Economic historians have recently analysed the possibilities and challenges in the field of cooperative financial initiatives in term of communitarian space in which the role of neighbourhood and social collateral was crucial. 7 Yet, as the following discussions suggests, it is important also to take note of how such social capital is being thwarted by the externalities of political process.

The Structure and Impact of the Cooperative Movement in Bengal

Since the start of an organised cooperative credit union by Friedrich Wilhelm Raiffeisen and Franz Hermann Schulze-Delitzsch in 1862, following a famine in Germany, the idea and the model travelled fast across Europe and then globally. In Asia, the first quarter of the twentieth century saw remarkable growth of cooperative credit societies including in India, Japan, Thailand and China. The cooperative movement in Bengal was an extension of the global movement for micro-financing of agricultural workers and small scale entrepreneurship. In 1904, the Government of Bengal formalised the rules and regulations governing the cooperative initiatives through the enactment of the Co-operative Credit Societies Act (Act X of 1904).

Let us start with a positive note on the performance of the cooperative credit movement at the different levels of the organisational structure, in terms of accumulation and mobility of capital. At the lowest level were the ‘primary’ or village societies; in the middle the ‘central banks’; and on the top the Bengal Provincial Co-operative Bank. The primary societies were from the beginning entrusted with the task of tapping the ‘hidden wealth’ of Bengal, especially Eastern Bengal, which now constitutes Bangladesh. Within five years of the launching of the programme there was evidence of ample collection of deposits along with the ‘successful tapping of hoarded gold out of its concealment’ of which ‘some particularly striking instances’ were reported. 8 To build up a ‘corporate life’ in a semi-feudal agrarian society it was thought important to promote the ‘habit of thrift’. Efforts were taken to popularise the use of ‘home safe-boxes’, which were introduced in the fertile regions such as Magura, Barisal, Naogaon, Dhaka, Narayanganj, Gopalganj, Chittagong, Sandwip and Noakhali in Eastern Bengal and received ‘encouraging results’. 9 With these efforts, the amount of capital accumulated by 1930 was about ₹150 million.

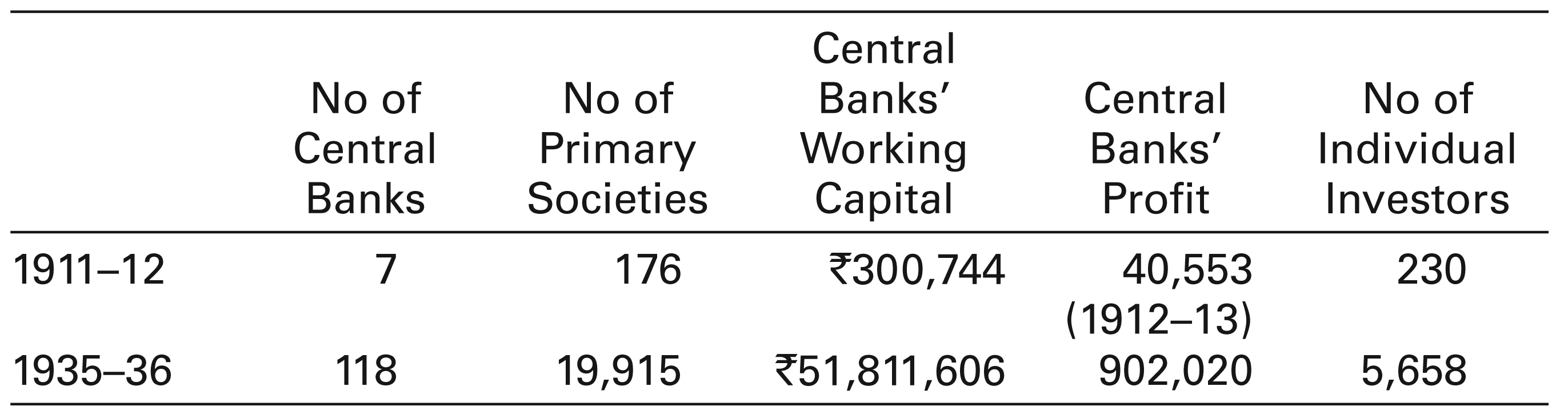

The Central Bank acted as intermediary between the Primary Societies and the Provincial Bank and other private banking institutions in Kolkata, as it linked the societies with financial market. The first Registrar of the Cooperative Department in Bengal believed that a Central Bank would be the means of ‘guaranteeing the credit of the village societies’ and it would demonstrate to the public that the small credit societies could be trusted for capital investment. Without a Central Bank, according to the Registrar, building such public trust was impossible. 10 With the first set of Central Banks in place since 1909, the government of Bengal had a policy of starting new Central Banks in areas which had a number of successful primary societies. In 1912, existing rules were modified to attract the ‘businesslike and educated people’ along with ‘non-official middle classes’ in a view to get the Central Banks working in the untapped areas. 11 As middlemen in the flow of financial capital, these banks played a crucial role in nourishing and supporting primary societies in the countryside. Between 1911–12 and 1935–36, the number of Central Banks, their working capital, profit and investors increased remarkably (see Table 1). The Bengal Provincial Bank worked as an apex body of Central Banks and a coordinator of capital flow among different central banks. The Provincial Bank started its career with a membership of 31 Central Banks in 1917–18 and the membership rose to 163 in 1935–36. 12 The net cash profit of the Provincial Bank during 1938–39 amounted to ₹81 million. 13

Growth of Cooperative Institutions during 1911–12 to 1935–36 14

In the drive for capital mobilisation, there was an appreciation of the unique agro-ecological condition in Bengal. There was usually an interval of several months between the early paddy and jute harvesting. It was usual that while some Central Banks in Western Bengal were ‘burdened with a plethora of idle funds’ from the sale of paddy, Central Banks in Eastern Bengal, which produced most of the jute, experienced scarcity of capital. Since inter-lending between these banks on a large scale was likely to give rise to the interlocking of liabilities, the Provincial Bank was envisioned as a clearing house for capital by ‘pooling the resources and channeling the surplus of one locality to meet the deficiency of another to the advantage of the province as a whole’. 15 This actually formed part of the problem for cooperative movement as much for other informal or indigenous banking sector, which Tirthankar Roy terms ‘seasonality-induced distortions in the organisation of money market’. 16

On the top of this apparent success in capital accumulation, there were high hopes of rural development in the early phase of the cooperative credit programme, but in the decades since the introduction of the credit societies agrarian credit relations actually deteriorated leading to increased poverty and landlessness. The average debt per family in Bengal increased at least threefold between 1906 and 1933 and, during the same time, the percentage of debtless families decreased from 55 to 17 (Table 2). At a gathering of peasants of Eastern Bengal and Assam held in 1937, it was reported that the papers simply listing the names of indebted peasants, collected on the occasion, weighted about 800 kg. 17 By 1940, far from wiping out debts, the cooperative credit societies had become another ‘incubus on the tenantry’. 18

Household Debt in Bengal, 1906–1933 (in rupees) 19

In Bengal, there were various problems in rural economy and well-being that were integrally connected to debt. It was mostly indebted villagers who had to sell their lands, often to non-cultivating groups who usually lived in semi-urban or urban areas. The transfer of land led to the growth of a group of landless people with greater vulnerability in terms of access to livelihood, food and nutrition. 20 Bengal plunged into a spell of poverty and destitution which ultimately prepared a ground for mass starvation during the famine of 1943. As famine literature suggests, most of those who died of starvation came from among the landless wage earners.

The question that we now turn to is: why did not the accumulation of capital at the Provincial and Central Bank levels make an impact on the efforts towards rural uplift? This requires a critical understanding of the colonial state’s politics of patronage of a group of people who were allowed to enjoy insider loans without substantial compulsion to repay at the different levels of cooperative organisation.

Political Organisation of Corruption

The perception of the failure of the cooperative movement in Bengal due the global recession of the 1930s was criticised by Niyogi as early as late 1930s when he observed that the seeds of decay had been ‘soon broadcast very early in its career by a disregard of those rules of prudent finance and efficient administration’. 21 While the recession may be partly responsible, local-level financial irregularities were quite evident from the early stage of the cooperative institutions. For instance, in the Barisal Central Bank, deposits were not accepted for more than 4 years but loans were extended for 6 years. About half of the working capital was extended in permanent loan to people other than poor cultivators. Among those who had taken loans from the then defunct cooperative societies, more than one person of the same family were given extra loans and the chairmen and the secretaries, who in most cases happened to be ‘middle class’ bhadralok (gentlefolk), laundered (attoshat) most of the assets. 22 On the Sandwip and Hatia islands near Chittagong, one Rajendrakumar Naga established 47 Central Banks whose total capital was ₹10 million in 1924. In these coastal areas, the Brahmins and Kayasthas who arrived as the ‘latest colonizers’ with little capital became ‘very rich’ in a short period of time. At the same time, three-fourths of the peasantry of Sandwip could not have full meals twice a day, regardless of the extent of agrarian production and they could not die free of debt. 23 In the Eastern Sundarbans area, specifically Bakarganj Sundarbans, which during the nineteenth century remained one of the most prosperous zones of Bengal, economic decline was clearly visible in the new century, even though earlier arrangements for leasing lands in large blocks to capitalists was discontinued in order to pave the way for dealing directly with the cultivators. 24 The visible decline in economic well-being of rural population took place despite the fact that the area was covered by many newly formed cooperative societies, at least 42 in the 13 newly reclaimed blocks in the Bakarganj Sundarbans in the early twentieth century. 25

The cooperative system, unlike the systems developed by traditional rural mahajans, had a hierarchical institutional base through which it was possible to manage financial flow. The Barisal Co-operative Central Bank Limited, for example, opened ‘hundi karbar’ (hundi trading) and advertised that anybody who deposited money in the bank could profit sitting in Kolkata only at a minimal commission and that mahajans of Kolkata could receive money securely by accepting hundi against the Provincial Banks. This way, the Bank did hundi transactions of ₹87,167 in 1928–29. 26 In another instance, in the Khepupara colonisation project in the Bakarganj Sundarbans, where all forests were reclaimed, every landed cultivator’s debt was ₹100 on average, whereas each member of the 109 co-operative societies had loan amounting to ₹200. This scenario was not warranted by the amount of working capital of the Central Banks of the neighbourhood, which stood at ₹0.6 million. 27

The Primary Societies were significant in terms of rural wellness as they directly dealt with ordinary peasantry. But corruption was rampant at that level too. For example, in the Madaripur sub-district of Faridpur, a total of ₹236,000 was due from 5,141 members in 1918–19. Out of this amount, as much as ₹70,000 as principal and ₹30,000 as interest were due from 158 defaulting office bearers. Much of these loans were benami (in fictitious names) transactions which came to light in the course of an audit. In the same year, in Rajshahi Division, the total loan due from about 1,000 societies was ₹2.7 million. Out of this amount, a sum of ₹1.6 million were appropriated by 4,221 members who were chiefly office-bearers, and the remaining ₹1.1 million were disbursed to 17,221 other members. 28 In the midst of utter mismanagement of funds, many societies could not maintain a reserve to meet urgent need of the non-influential ordinary peasant members. The task of the Government was rendered still more difficult by fraudulent activities by a number of so-called ‘provident’, ‘friendly’ and insurance societies. 29 The Chairmen and Secretaries of these societies were generally the ‘worse debtors’, who sometimes enlisted such people as members of the societies through whom they could obtain additional loan. 30

Although global depression was not the only catalyst for the decline of the cooperative movement, the depression years brought about new dynamics and intensity to the existing problems in cooperative institutions. There was an opportunity of fixing the irregularities and reviving the cooperative system with the operation of Bengal government’s Debt Settlement Board in the 1930s and 1940s, but such hope was promptly lost in the quagmire of corruption. Cooperative credit societies were found to be substantially exempted from operation of the Debt Settlement Boards in the late 1930s and early 1940s. Often a case dealing with a co-operative debt had to be kept pending for an indefinite period as no decision could be reached without the approval of the co-operative inspector who mostly saw the interest of the cooperative societies as creditor organisations.

31

Those against the Debt Settlement Board found ‘an inherent logical inconsistency’ in the effort to reduce the corpus of co-operative debts without a simultaneous attempt to address the claims of creditors of higher co-operative organisations such as Central Banks. It was noted that the mandatory provision of a notice to all creditors under section 13 of the Act would further ensure that

[c]o-operative debts are not hurriedly rushed through the machinery of Debt Settlement Boards, without the knowledge of the interested co-op societies…though co-operative credits are included within the scope of debt-adjustment scheme, in fact, especially this type of debts are safeguarded….the co-operators have got about all they wanted by the back door of the Rules.

32

The unhealthy nexus between the bending of debt regulations and a certain section of socially dominant groups is summed up by a contemporary commentator in the following manner:

Enthusiastic westernized politicians, intent on getting re-elected by showing an interest in rural welfare, directed a co-operative department whose nominal function was to help agriculture by the co-operative raising of money and lending it out to cultivators. Injections of Government ‘loans’ were to be applied as incentives to the raising of local money. Fifteen improvident, uninfluential villagers were made to join with five slightly less improvident and more influential others to form a ‘Bank’…. This stock bank was supported by the department—and there only on paper—to provide joint security by which local borrowing would be rendered possible. The Bank would then add to the money raised locally a loan it received from the department. In this way a sum of, say, ₹ 300 could be distributed among the 20 members of the bank at a ‘reasonable’ rate of interest. The stated object was to enable the recipients to pay off debts they might have incurred to moneylenders at high rates of interest or to buy much needed agricultural equipment such as seeds, cattle, implements, etc. The less improvident five were expected to have the public spirit to prevent irresponsible distribution to the more improvident fifteen…Such public spirit did not exist. No money could be borrowed locally at all. Moreover, the injection of cash into a group of villagers from outside in such quantity and on such a set of ridiculous assumptions completely demoralized the 20 and resulted in a cheerful free-for-all scramble in which the five less improvident easily secured for themselves the greatest part of the loot.

33

Credit for Unproductive Sectors

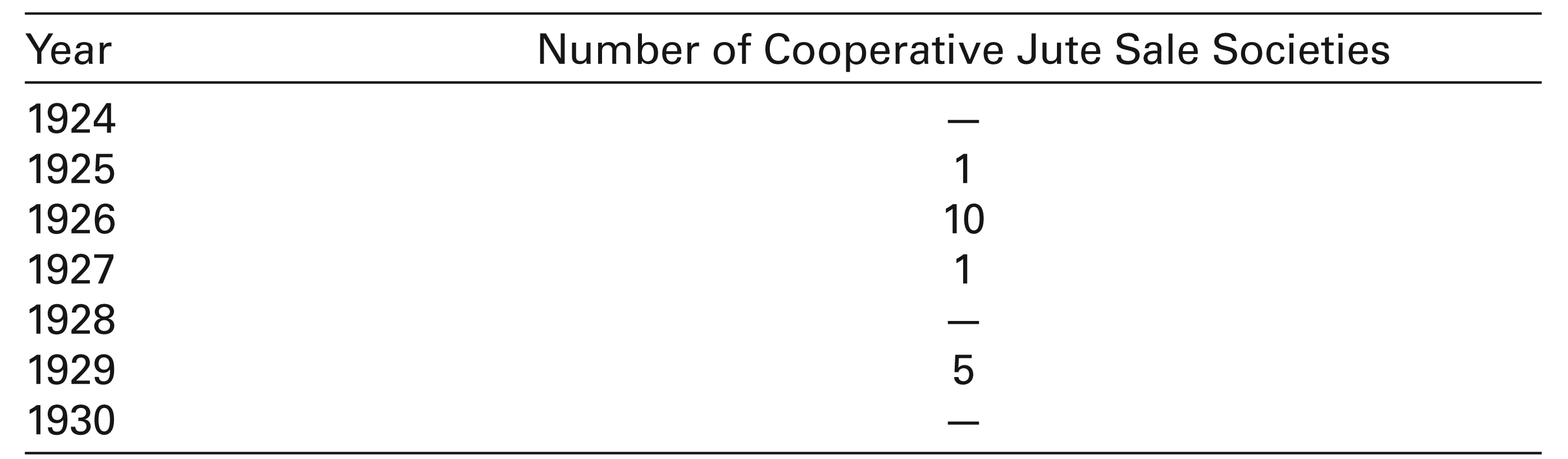

By the turn of the twentieth century, jute was a major agrarian product that was supplied to both domestic and global market. The volume of jute exports jumped fortyfold between 1838 and 1868 and during the 1860s, the value of raw jute exports increased from ₹4.1 million to 20.5 million. With only occasional and temporary slowdowns, jute cultivation, production and export was in its heyday until the early twentieth century. The same is true for rice production and export. 34 There was an opportunity for actual cultivators to make the most of the extensive market opportunities through cooperative societies and benefit thereof. But it appears that there were negligible number of ‘sale’ societies as opposed to ‘credit’ societies. There never were more than 10 cooperative sale societies in the jute sector (Table 3). For those small number of sale societies, purchase of jute was done by the managers of the societies under the instruction from the Bengal Wholesale Society. These societies were financed by the Bengal Provincial Co-operative Bank of Calcutta on the recommendation of the Bengal Wholesale Society. They sold jute to the Kolkata mills through European brokers and they got better prices than local merchants ‘on account of good assortment and jute being free from moisture’, whereas the number of ‘actual cultivators’ were negligible. 35 In the case where actual cultivators were able to form societies, they were not linked to any central organisation, nor were they assisted by outside financier: ‘the nearest central bank of credit type is unwilling to finance such societies as their liability is limited by shares, which are hardly sufficient to justify their requisite borrowings. They have, therefore, to depend on their share of capital and local deposits, if any, to carry on their business and as such are generally handicapped by their finance’. 36 There were also a considerable number of weavers who could have been a part of the cooperative movement in the region, but this did not materialise.

Cooperative Jute Sale Societies 37

It was suggested by contemporary commentators that the traditional money- lenders (mahajans) suspected a loss of credit market with the establishment of sale societies. 38 The failure of the cooperative movement to extend beyond credit relations meant that the possibility of improving the well-being of the agrarian producers in late colonial Bengal was missed out. One way of qualifying such hope could be found in the examples of co-operative management in the United States about the same time, where out of nearly 9000 cooperative organizations, 90 per cent were engaged in selling farm products worth about $2 billion. 39 Bengal’s cooperative scenario starkly contrasted also with the experience in England, where cooperative credit societies were outdriven by supply and sale societies.

One reason why the cooperative societies remained largely a liquidity machine in the form of credit societies

40

is linked with the foregrounding of collective liability to credit rather than the marketing of agrarian produces, where Raiffeisen model was tailored to fit a ‘timeless’ Oriental rural society. To alleviate the concern about the security of investment in cooperative institutions, a commentator, Sanyal, suggested that the principle of unlimited liability meant that every member of a cooperative society was ‘liable to the extent of the whole amount of his property for the debts of the society’. At the same time, a loan was granted to a member on the personal security of two other members, who were held liable for the amount borrowed.’ Sanyal further suggested that the object of such strictness was to ‘create confidence in, and attract deposits from, the investing public’.

41

Sanyal’s view reflected the official position of the Government of Bengal, as a report of the Cooperative Department agreed that

[v]illage life in India is very homogenous, and unlimited liability implies a careful selection of members and a restricted area of operations. The work of a village society does not demand any special care, and there is no difficulty in securing gratuitous management with, perhaps, the payment of a small remuneration to the writers of the books. Shares and dividends, which imply previous accumulation of capital, are not suitable to the economic conditions of villages in Bengal. All profits therefore go to the reserve fund, which is indivisible.

42

At the same time, there was no ‘very great keenness on the part of the societies to invest their reserve fund apart’. 43 Neither was the reserve fund invested, nor were the money deposited by rural population was available to the people in their need as ‘many societies could not keep money in hand to meet the sudden and emergent need of its members’. This was caused not only by the tendency of the Chairman and secretary of the societies to ‘use the cash balance for their own purposes’, 44 but also by an organised way in which savings were serving the financial market of Calcutta on a priority basis. No wonder that there were no checks whatsoever between normal working and liquidation. 45

Joint stock banks, which had close working relations with cooperative societies, extended their money to the big dealers and merchants to purchase the produce of the farmers, not reaching the farmers directly for reasons described above. The concern for security of fluidity of capital was present even before the cooperative movement took shape. From the very outset, the movement aimed at helping not the wretched of the earth but to deal with those who were still financially ‘alive’ to contribute productively in a capitalist venture. It was argued that

if the society, which knows the circumstances is willing to buy the man out of the hands of the money-lender, they will admit him, but if they consider that he is too deeply involved they must refuse to assist him. It must be admitted that there are many raiyats who will never be able to take advantage of the societies. The hopelessly insolvent raiyat cannot be aided.

46

One witness to the Banking Enquiry Committee informed that he had never come across any instances in which firms dealing in fertilisers had granted credit. 47 Money reached the peasantry, but it reached through the hands of traditional moneylenders or by those who ‘took to the profession of money lending lately’. In Naogaon in Rajshahi district, loans were extended to mahajans for purchasing jute during the jute harvesting season at favourable rates, but not to actual cultivators, as security in the form of landed property was a criterion for eligibility of obtaining loan. 48 This left an increasing number of landless and land-poor people out of the reach of the cooperative sector. In Bagerhat in Khulna, for example, the zamindars and richer people took loan on low rates of interest and lent the money to the cultivators at a higher rate. Even lawyers, government clerks and village widows started ‘business of money-lending’ supported by these cooperative institutions which were regarded as ‘no better than grocer’s shop’. 49 On the occasions when the Joint Stock banks and credit societies financed ‘agriculturist’, 50 they did it for ‘major permanent improvement and for purchase of land’, without an enquiry whether the loans were taken for productive purposes. It naturally followed that ‘middle class men’ were gradually bettering their position through joint stock banks. 51

The Politics of Cooperation

In the modern state, corruption is not merely a means to earn material gains, but also a means to secure and sustain political client bases. To understand why the cooperative institutions in Bengal were corrupted through the abusing and bending of the rules and regulations, we need to examine the conditions of late colonial politics in its specific temporality that Bengal provided. Although a number of issues in financial and operational matters as well as individual desire for profiteering existed, it was the political process which informed financial irregularities and other structural and policy issues in such a way that microfinance and political governance got into unhealthy entanglement.

A stated objective of the cooperative movement in Bengal, as in other parts of India, was to build human capacity to avert famine and poverty, which was also the case in Germany and China. But after the revolutions in the Soviet Union, imperial officials in Bengal found in it an opportunity to avert possible socialist influence among the poor. By the 1920s, communist ideals were making huge impression on the educated youth and students, which combined with nationalist feelings posed a new kind of challenge to the existing colonial order. Such development in both the global and national politics greatly influenced the performance and mechanism of the cooperative movement in Bengal.

Existing literature suggests that the government aimed to use the cooperative institutions as tools to create an environment for the microfinancial entrepreneurship for potential political actors in the country in a view to take some pressure off the anti-colonial resistance. Within a week of the introduction of the Cooperative Act 1904, the Government of India sent out the working agenda requesting the provincial governments and swadeshi leaders to establish co-operative societies. 52 In Bengal, Lord Curzon paid ‘unusual attention’ to the scheme of cooperative societies. 53 Eventually, the cooperative movement appeared to be almost synonymous with the swadeshi movement as it was suggested that the swadeshi leaders ‘should select competent leaders to promote agricultural and commercial undertakings, found agricultural associations, Co-operative societies (for the youths)’. 54

P.J. Hartog, the first Vice Chancellor of the University of Dhaka, noted that there was a tendency in Bengal to make what he called a ‘salary caste’, and he hoped that the cooperative efforts might affect a revolution in agriculture in Bengal as it had done in Denmark and Ireland. By uniting the peasantry of Bengal, the movement would boost both large- and small-scale cultivation projects and employ a large number of the bhadralok experts for the improvement of their methods of cultivation and the management of livestock. This at the same time, according to Hartog, would considerably increase the agricultural productivity and rural prosperity in the Province.

55

Thus, a section of the middle class with political clout found an avenue of rehabilitation in agrarian Bengal. And it appeared to be a combination of glocal capital and national politics both of which were now under the control of a section of the bhadralok, who were at the forefront of anti-colonial movement. In an address in 1927, the chief of the Cooperative Department suggested that

There is on the whole a perceptible tendency in the rural societies towards politics. Whether such a tendency is to be checked, it is for others more intimately connected with the movement to judge, but I would like to see the movement develop on economic lines at the present moment.

56

Catanach observes that in the Bombay Presidency there was virtually no evidence of cooperative societies being used for a political end and that while by no means it intended to eliminate the moneylender, it did aim ‘to put some fairly definite limit on his activities’. One major aim of the cooperative movement in Bombay was to prevent the transfer of land to moneylenders from cultivators. To some extent, therefore, the history of rural cooperation in the Bombay Presidency could be considered part of mainstream agrarian history, while in Bengal, it worked for expanding political space. 57 Catanach quotes an expert on cooperation, Ewbank, who believed that it was desirable to have such a rule ‘in reserve’. 58 Catanach further remarked that in Bombay most Indian businessmen looked askance at the extent to which the Bengali swadeshi movement was engaged in cooperative movement, yielding little good. This was despite the fact that in Bengal political elite ‘had the experience and capital to make the swadeshi movement into something a little more lasting than the rhetoric and flamboyant defiance of certain section of the Bengal bhadralok.’ 59

While the cooperative sector was used to contain some potential anti-colonial agitators among the middle class through a hegemony of Swadeshi patriotism, it also came to be used as a tool to control the peasantry. The zamindars were thought to be in an advantageous position with the establishment of cooperative societies, because central banks were ‘keeping special eye on the members of the village societies’. 60 Major investors and the managers of the cooperative institutions were run by both the urbanite political elite as well as rural landlords. For example, the Modern Co-operative Agricultural Associations Limited had a capital of ₹0.5 million which was divided into ₹50,000 share of ₹10 each. The first governing body included Sir Ashutosh Mookerjee as president and Maharaja Sir Manindra Chandra Nandy of Kashimbazar as secretary. There were a number of other zamindars and urban elites as members. 61

While the initial years of the cooperative movement saw the government trying to use it to contain the swadeshi political tide, later on the threat of terrorist movement, communism and economic depressions informed the government attitude towards the movement. Alexander Hamilton, a leading advocate of cooperation, suggested that a cooperative utilisation of merely ₹10,000 could eventually bring a revolution in the economy of Bengal to such an extent that 6,000 ‘White shirts’ (in the place ‘Red Shirts’) of the great peace army will pave the way for 10,000 doctors, and a hundred thousand teachers and ‘unemployment of the bhadralokh will wither and die’. Hamilton recalled his conversation with a ‘brilliant young product’ of Calcutta University, who told him, in response to the question of nationalism, that the only ‘ism’ he bothered about was the ‘belly’. Hamilton in this connection reminded the Governor of Bengal that if he could ‘apply 50,000 bread poultices to the bellies of young Bengal, the fever of unrest will abate and vanish eventually like an evil dream.’ 62

It appears that the government was moved by Hamilton’s plea and similar arguments by the likes. Governor Anderson, in a speech in 1935, reminded the bhadralok of the disadvantages of ‘perverted form of terrorism, and …anarchy in the shape of non-cooperation and civil disobedience’. Among other pieces of advice, he asked them to return to villages, to sit on the Union Boards and plan constructively for the improvement of rural areas and to take the lead in forming ‘co-operative societies for a multitude of purposes which will band the people together in small units working for the mutual advantage of their members.’

63

Eventually, these efforts led to a political programme of global proportion. As Hamilton emphatically noted:

India’s lack of funds is an imperial question, and the raiyat an imperial asset. A stronger raiyat means a stronger India and a stronger Empire—an Empire able to apply the Monroe doctrine from Suez to Singapore and beyond—an Empire which only Co-operative Credit can build.

64

Conclusions

In the late colonial conditions in Bengal, the cooperative movement was conceived as a site where both the nationalist movement and communist influence could be contained. To what extent this colonial project was successful is debatable, but the political process of appeasing a potentially threatening social group meant that less influential member of the primary societies hardly benefitted from the cooperative institutions. Unlike in Ireland, for example, where social elite were reluctant to join the movement, in Bengal it was these socially and politically dominant group which dominated the cooperative movement. This article has examined, along with economic issues, this convergence of social and political forces in order to have a better sense of the failure of cooperative movement in colonial Bengal.

Footnotes

Acknowledgements

I would like to thank an anonymous reader for detailed and thoughtful suggestions which have significantly improved the article. Useful editorial attention from the IESHR editors and conversations with Andrew Sartori and Tariq Omar Ali are highly appreciated. All limitations remain with me.