Abstract

This study examines the performance of Indian textiles exports in a relative and holistic framework. Given the pre-eminence of the sector for India’s exports, a comparative study on its performance is called for. For the purpose, India’s key competitors in the export product categories are deduced. The primary objective of this study is to critically assess the Indian textiles exports performance using the export similarity index (ESI). Overall, the study arrives at some important conclusions with regard to this objective using the ESI for the textiles product codes HS 56–60 for the period 2013–2017. In view of the much-needed scope for improvement in the Indian textiles exports performance, there is a need to evolve a comprehensive export strategy for the sector, involving both firm- and state-led efforts so as to have a beneficent impact on exports and the overall Indian economy.

Introduction

The Indian textiles sector occupies an important position within India’s socio-economic landscape. It is one of the largest in the world with a huge raw material base and manufacturing strength across the value chain. To support the pre-eminence of this sector for the country, some basic statistics on the same would be of help. Tellingly, the textiles and clothing industry contributes 2 per cent to India’s gross domestic product and accounts for 14 per cent of its industrial production, 27 per cent of its foreign exchange inflows and 13 per cent of its export earnings. India is the second largest exporter of textiles in the world. Moreover, the sector is a major employment generator, second only to agriculture, giving direct employment to 45 million people, with a major portion of these employees being women (Ministry of Textiles Annual Reports for 2014–2015, 2015–2016 and 2016–2017).

The very motivation to undertake this study stems from the fact that the Indian textiles sector is too vital to be ignored in the Indian economic landscape—be it trade or socio-economic. It is in this context that the export similarity index (ESI) shall serve as a useful tool to assess the growing threat of export competitors in the textiles landscape, a novel approach as far as the Indian textiles exports studies are concerned, for a majority of them do not study exports competitiveness in the sector from the point of view of exports similarity.

On the basis of this preliminary information, it is prudent to state the objective of this study. The proposed analysis intends to critically assess India’s exports performance in the textiles sector with regard to the ESI. ESI serves as a useful tool to assess the export competitiveness with regard to an exporter’s major competitors. Greater export similarity indicates the possibility of future clash of export/trade interests (Finger & Kreinin, 1979; Wang & Wang, 2007).

Review of Literature

Finger and Kreinin (1979), Kellman and Schroder (1983), Shi (2003) and Wang and Wang (2007) contend that ESI could be employed in adjudging the similarity in exports of different countries. It is a useful measure of ascertaining the convergence or divergence in the exports structure of different nations over time. Also, it is a potent tool to assess the substitutability of exports in the international markets, for a high exports similarity index value entails a higher possibility of exports substitution among nations exporting almost similar commodities. Likewise, substitutability entails greater challenge from the competitors and the need to enhance the competitiveness profile in a particular commodity group over time.

Data and Methodology

The period of the study is from 2013 (the peak year of the Indian textiles exports) to 2017, as international trade data for all the countries included in this analysis are available until 2017. The study follows a secondary data analysis approach in the following manner.

First, international textiles trade data from sources such as Trade Map (2019) and WITS (2019) are drawn. On the basis of the same, five key products at HS six-digit level are identified for the HS two-digit level (e.g., HS code 560121 within HS 56). Second, for each HS six-digit level product thus identified, five key markets are recognised based on trade flows for the five-year period 2013–2017. It must be mentioned here that the basis for choosing the top five product categories and markets is the average values. The entities with the highest values over 2013 to 2017 qualify for the analysis. Third, the trade index for identified products over the five-year period is computed for comparing the competitiveness of Indian textiles and apparels exports with other countries in each identified potential market. The index to be used for this competitiveness analysis is the ESI.

Whether there could be any future rivalry among India and her export partners in textiles could be gauged with the help of the ESI as follows (Nag and Chakraborty, 2019):

Here, ESIjk is ESI between country j and country k; xijw is the export of commodity i (at HS four digits within the HS two-digit code under consideration) by country j to the world; and Xjw is the export of country j to the world in the corresponding HS two digits.

Specifically, the paper employs the ESI method by dividing the ratio of Indian textiles exports to the partner country (each of the top five markets identified) to the total exports of all products to those countries by the ratio of partner’s exports of textiles to total exports of all products to India. Thus, the entire exercise is based on the ratios of bilateral trade flows between India and her major textiles exports competitors as a consequence of which, during reporting the results of the ESI, only the values of partner countries are considered and not of India, thanks to the very nature of the definition of this index.

Higher values of ESI in exports over time indicate increasing similarity between exports basket of a country (India) and its trade partners. Increasing ESI values underline possibility of future conflict in export interest of the trade partners. Values nearing ‘100’ indicate perfect export similarity, whereas values nearing ‘0’ indicate perfect export dissimilarity.

The key hypothesis that this paper seeks to address is:

H0: The Indian textiles exports are not competitive in terms of the ESI.

Intuitively, if the ESI values are high for India’s key exports competitors, then the degree of Indian textiles exports competitiveness is low and the competition faced by the sector is considerable (Fan & Chang, 2010; Kellman & Schroder, 1983; Shi, 2003).

The next section discusses the results and analyses of this study based on the methodology elicited in this segment.

Results and Analyses

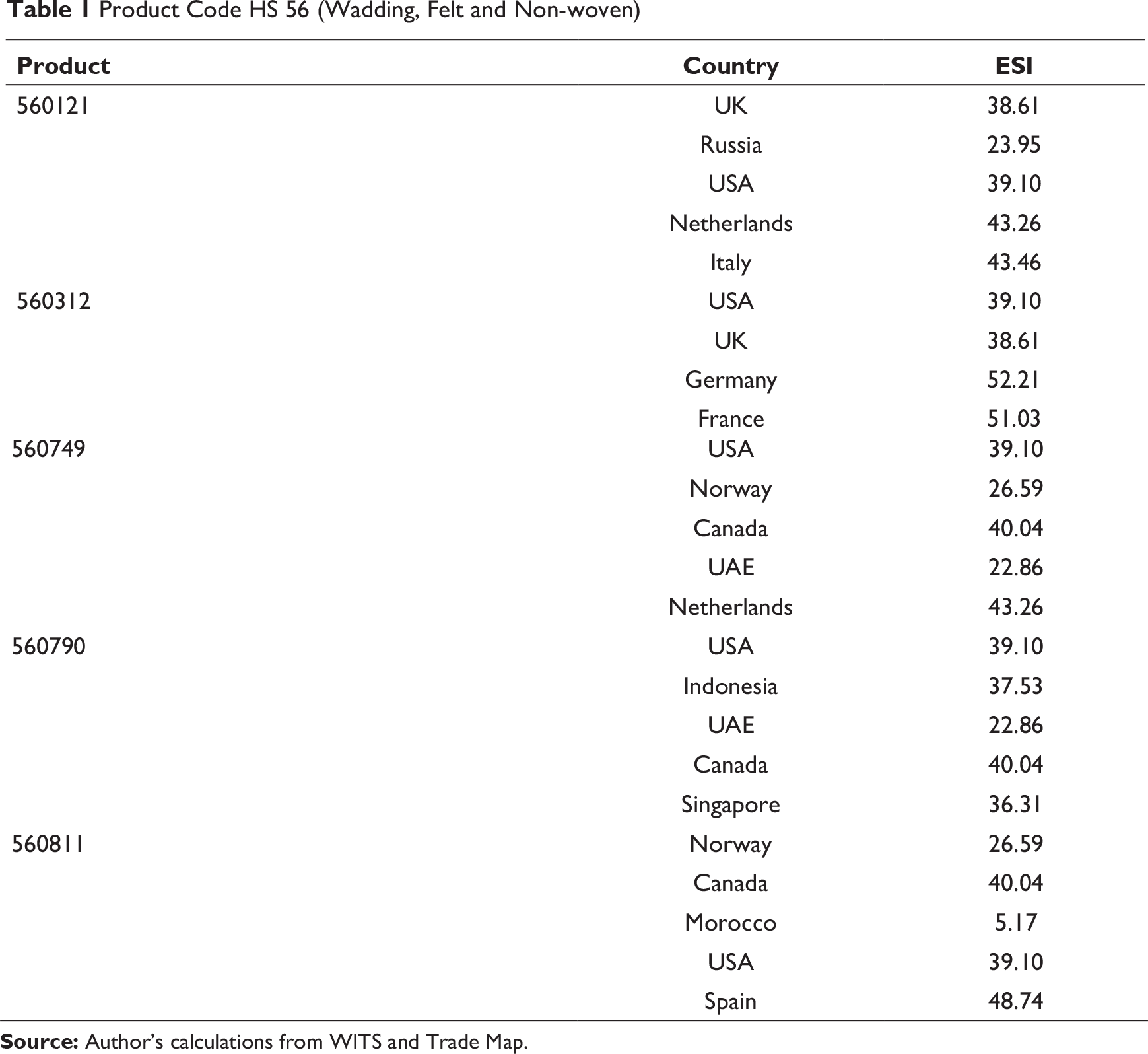

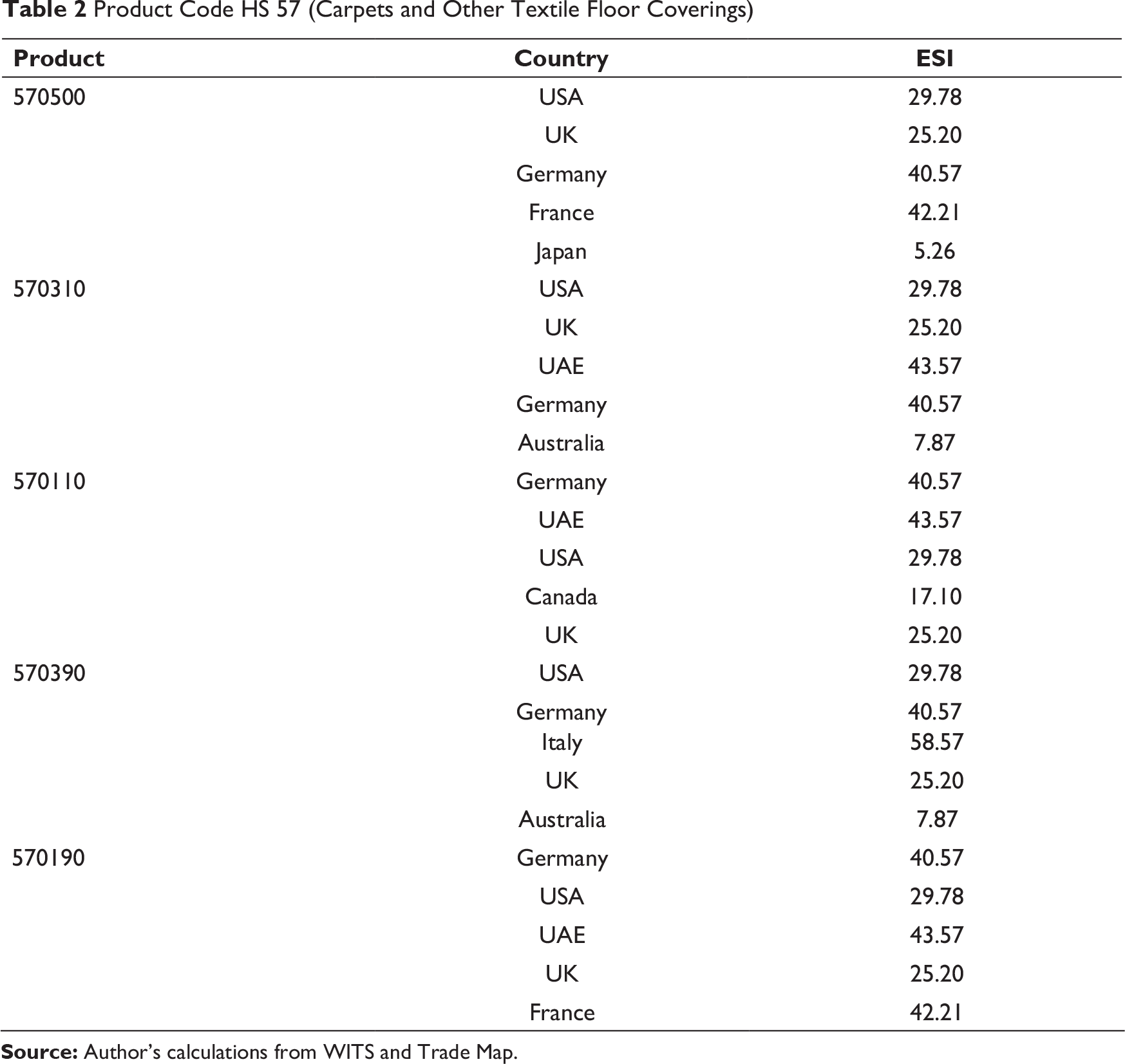

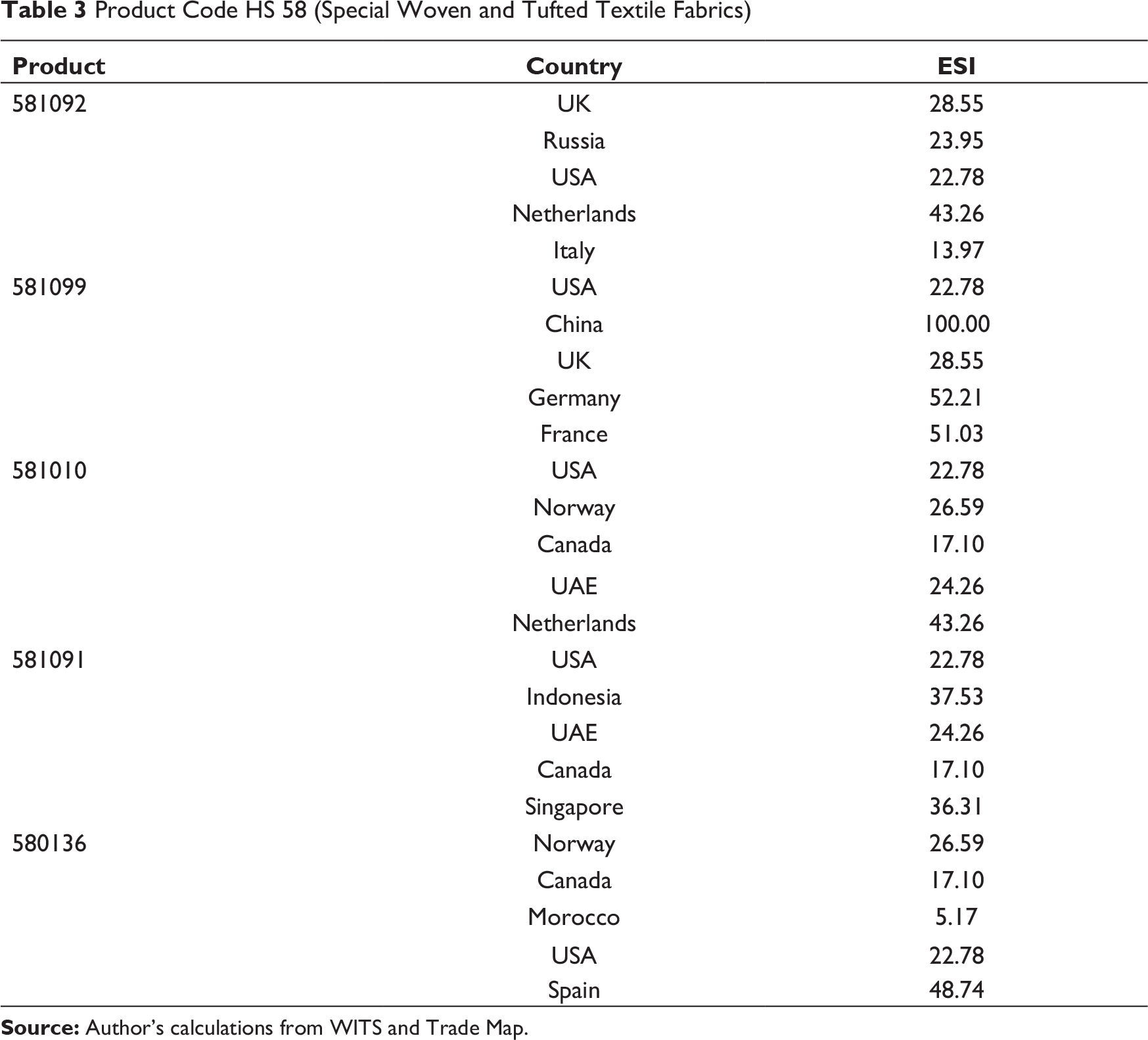

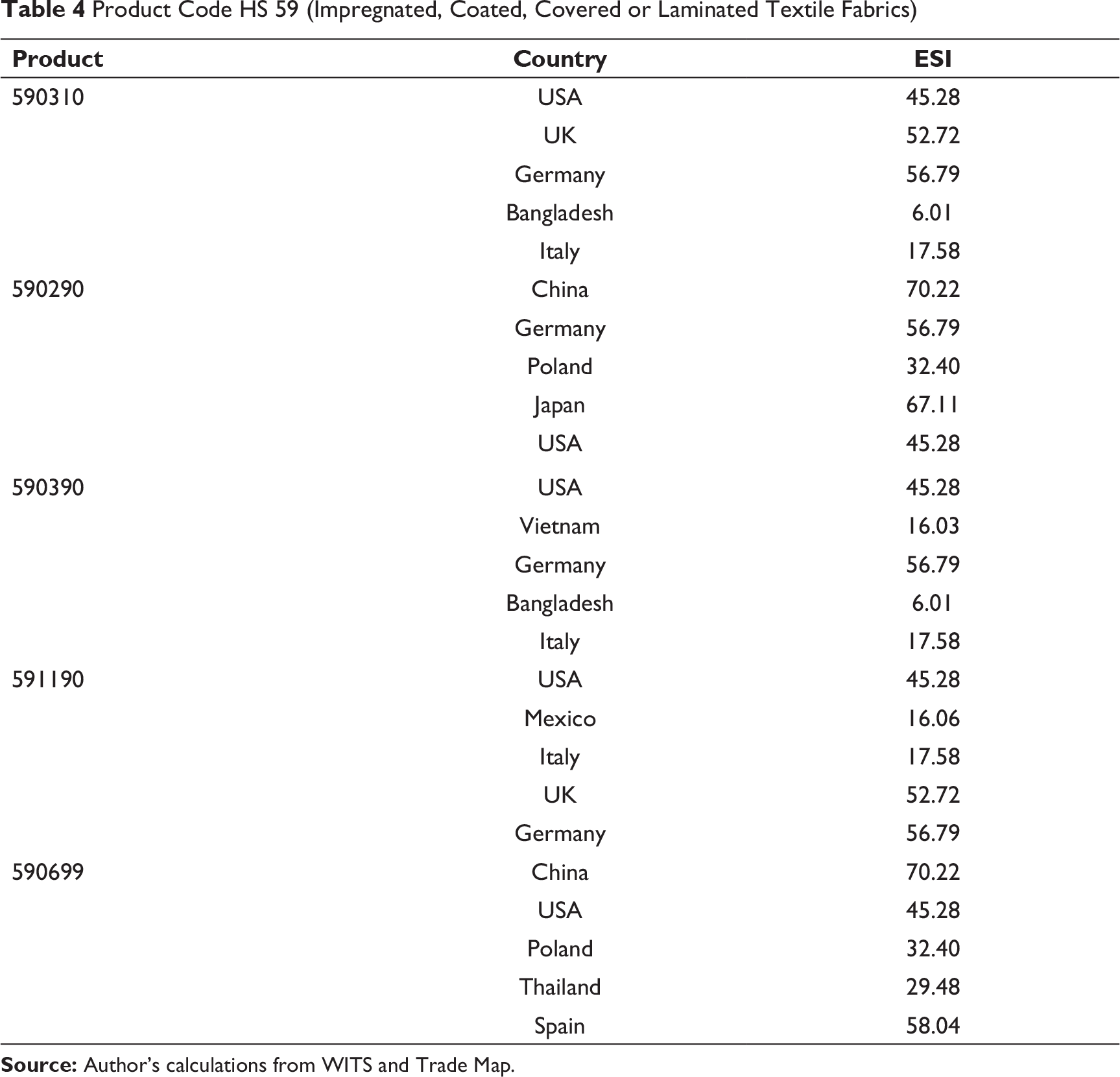

Based on the data and methodology enunciated in the previous section, ESI values for the relevant export product categories and markets are calculated. It is found that for all the major export product categories, HS 56–60, the degree of exports similarity is high.

Product Code HS 56 (Wadding, Felt and Non-woven)

Product Code HS 56 (Wadding, Felt and Non-woven)

Product Code HS 57 (Carpets and Other Textile Floor Coverings)

Product Code HS 58 (Special Woven and Tufted Textile Fabrics)

Product Code HS 59 (Impregnated, Coated, Covered or Laminated Textile Fabrics)

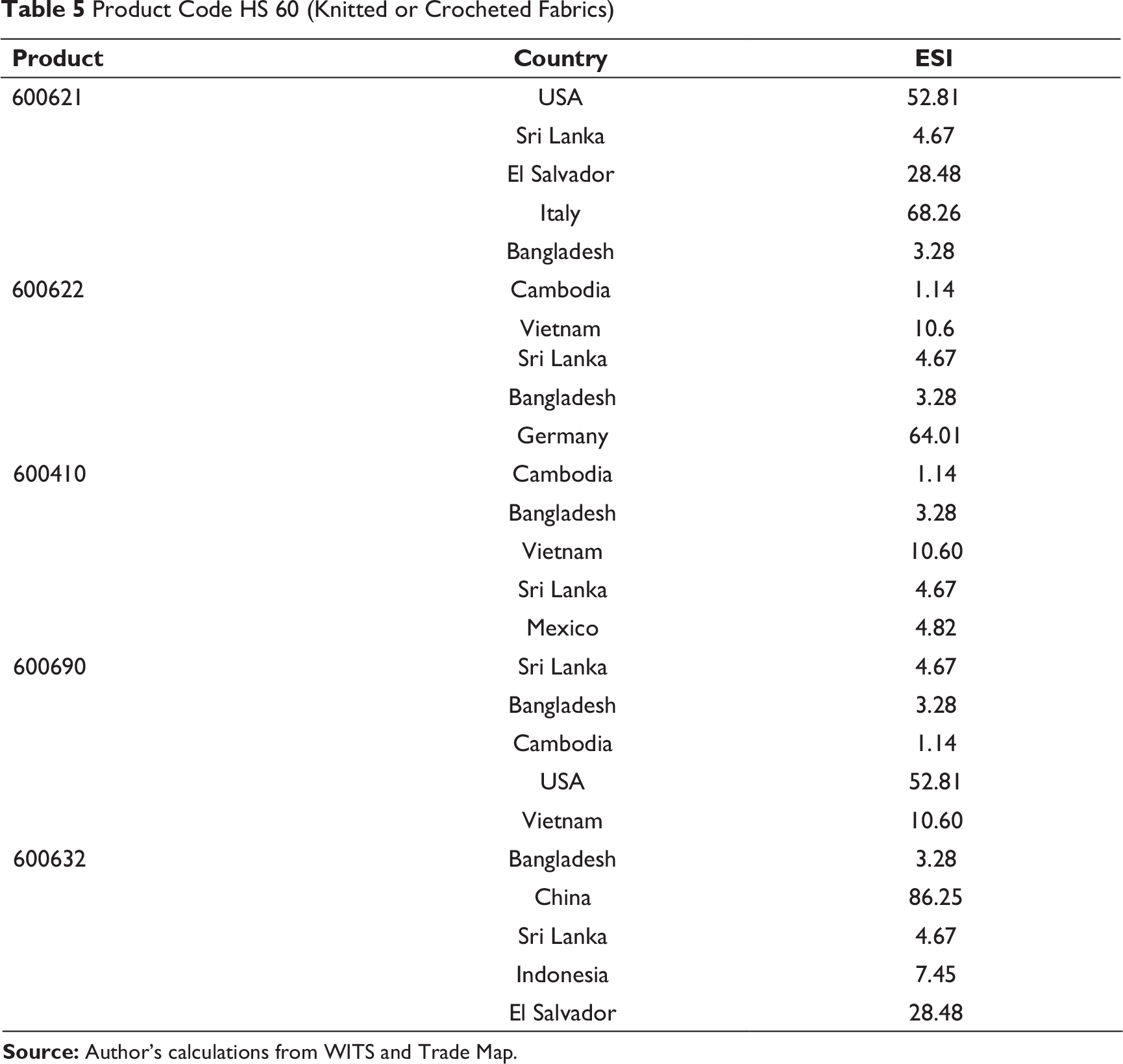

Product Code HS 60 (Knitted or Crocheted Fabrics)

Quite evidently, one cannot reject the hypothesis propounded at the beginning of the paper. India is facing a significant challenge in the textiles export product categories discussed in the section and must take urgent steps to raise her competitiveness profile in the same.

It is concluded from the analysis that the Indian textiles exports need improvement on the competitiveness front. This needs a careful assessment and solution of its probable challenges.

First, high manufacturing costs in the sector. Second, the duty disadvantage faced by the country’s exports in major markets such as the USA and the EU thanks to the lack of Generalised System of Preferences. Last but not the least, a lack of technological upgradation (Ministry of Textiles, 2016–2017). These challenges must be met with an appropriate mix of policies, consisting of both firm-level and government efforts. Some of these policies could be successful negotiation of ongoing preferential trade agreements and improving the logistics performance of the Indian textiles industry, as also reaping the benefits of scale economies through technological upgradation of small and medium enterprises (Gambhir & Sharma, 2015).

To conclude, the conversion of challenges into opportunities for the Indian textiles sector is the need of the hour, not just for the industry but also for the nation.