Abstract

Indian Railways (IRs), the world’s fourth-largest network by size, has a route length covering approximately 68,155 km. It operates over 22,669 trains a day, sixty per cent of which are the ones transporting about 844 crore passengers and 123 crore tonnes of freight; two-third of its total revenue is from freight and only 27.3 per cent are passenger receipts. It is the eighth employer in the world employing about 1.227 people. It suffers from chronic under-investment, low-capacity augmentation, congestion, and over-utilisation, safety problems and poor-quality service, leading to poor morale, reduced efficiency, sub-optimal freight and passenger traffic, fewer financial resources; and deteriorating operating ratio.

The government on the recommendations of a high-level committee suggested ways to mobilise resources and restructure the Railway Board; invited private sector companies to operate 151 trains over 100 routes by April 2023 bringing in an investment of ₹30,000 crore. The committee laid down a time frame of five years for implementation of its recommendations.

The present study spread over five sections discusses observations and recommendations of the committee and suggests the outsourcing of some of its non-core functions like repair and maintenance workshops, manicuring units, washing of trains, security, and employees’ facilities like medical and education.

Keywords

Introduction

The government of India has decided to invite the private sector for railway operation and 151 trains over 100 routes will be run by the private companies by April 2023. This article analyses the introduction of reforms and restructuring of Indian railways. The article is divided into five parts. The role, significance and growth of railways over the years in the Indian economy are discussed in the first part. The second part presents, in brief, the pros and cons of the railways’ recent decision to involve the private sector in rail operations. High-level committee’s observations and recommendations for the reforms in railways have been discussed in part three. This part also presents the time frame for the introduction of the various recommended measures. The fourth section discusses the experiences of privatisation of railways abroad and lessons from that. The last section contains certain likely roadblocks and the way ahead for reforms in Indian Railways.

Indian Railways (IRs) is the world’s fourth-largest rail network by size under single management and has an established route length of over 68,155 km as on 31 March 2019. It is the lifeline of the nation, operating over 22,669 trains a day, sixty per cent of which are the trains transporting about 844 crore passengers and 123 crore tonnes of freight every day. From a very modest beginning in 1853, when the first train steamed off from Mumbai to Thane, a distance of 34 km, it has grown to a vast network of 7,321 stations with a fleet strength of 12,147 locomotives, 74,003 coaches and 289,185 wagons as on 31 March 2019. The network spans 123,542 km of track length, while route length is 68,155 km, of which 90 per cent is broad gauge. It generates 100 per cent freight output and 99 per cent of passenger output. It is the world’s eighth-largest employer employing about 1.227 million people; it contributes one per cent to GDP and is expected to add up to two per cent more to GDP. It also takes pride in its staggering numbers as 131,205 bridges, 12,147 locomotives, 74,003 passenger coaches and 289,185 freight cars. (This part is an updated version of Chapter 12, Dhameja & Dhameja, 2016; and Raghuram & Gangwar, 2008)

Originally, the railways were operating as private companies owned by Englishmen, with a certain concession such as guaranteed minimum return and free land. To guard against complaints of private ownership and poor management, the government took over a private rail company in 1925, and by 1950 the rest of the other private-owned rail companies including the ones owned by the former princely states were taken over by the government.

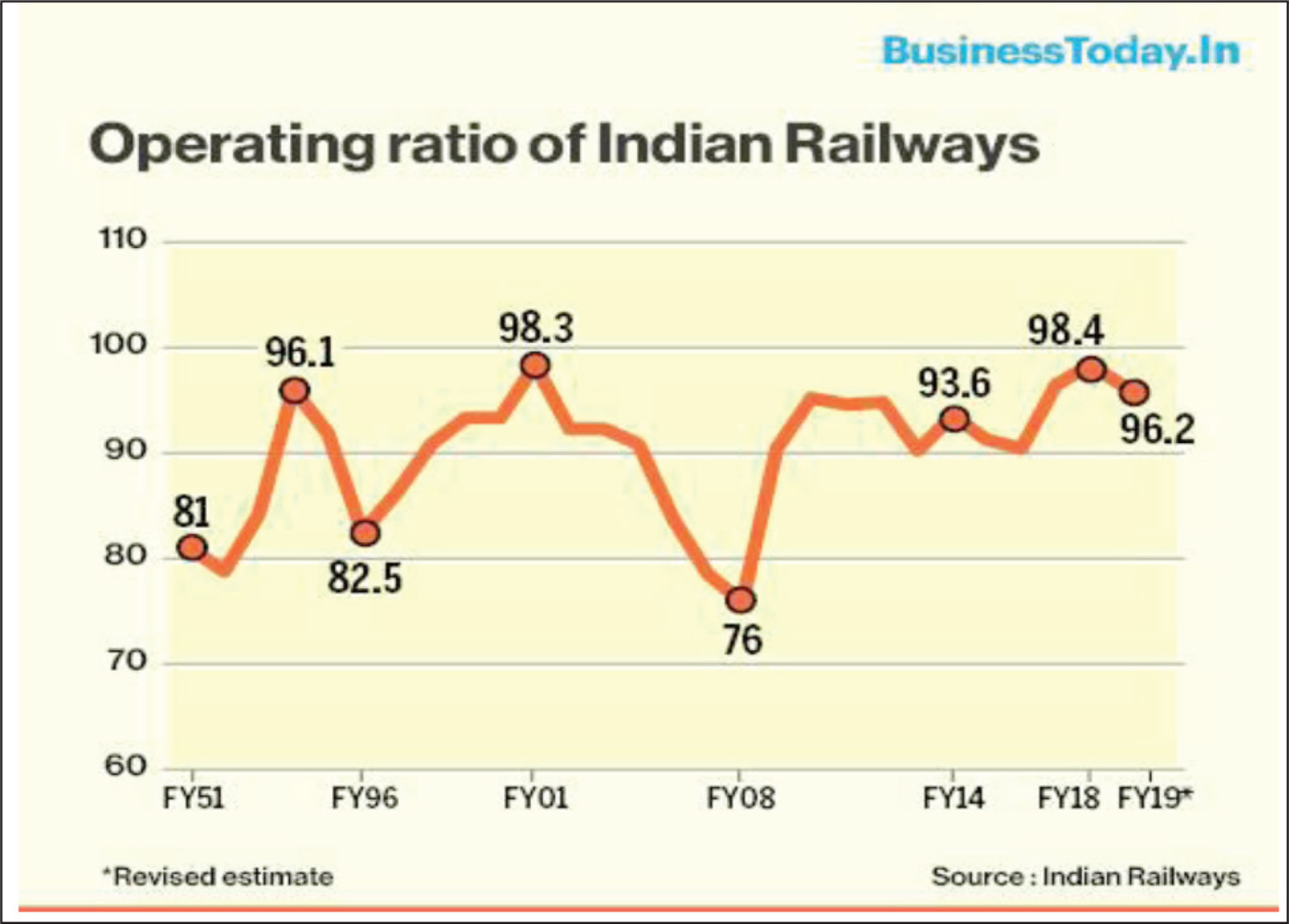

It may be noted that the route length of railways was 53,596 km in 1950 and it increased to 68,155 km in 2019, an addition of 14,559 km adding a length of only 211 km per year. As such, there was a need to move faster, to connect people and places across the nation. Despite all this, the operating performance of railways depicts a dismal picture as reflected by the operating ratio discussed later.

Organisation Structure

IRs is headed by an eight-member Railway Board which acts as a Ministry of Railway. Railway Board is headed by a chairman, and its members are specialists in functional areas. IR is divided into 18 zones, each headed by a General Manager (GM) and further sub-divided into 68 operating divisions each headed by a Divisional Manager. Station masters control individual railway stations; besides, there are eight production units, training establishments, 16 Public Sector Undertakings (PSUs) and other offices under Railway Board.

In addition, IRs offers housing and has its own hospitals, schools and sport facilities for its employees.

IRs is a vertically integrated organisation that produces the majority of its locomotives, rolling stocks at its production units. The repair and maintenance of the vast fleet of rolling stock are carried out at 44 loco sheds, 212 carriage and wagon repair units, and 45 overhead workshops across various zones.

The Indian Railway Act 1989 and the Railway Board Act 1905 allow that train operation can only be done by the public sector while all other activities of design, construction, financing and maintenance can be undertaken through private participation. Accordingly, the core activity of railway operation has to be done by the government while non-core activities can also be done through public-private partnership (PPP) initiatives. In this respect, the European Commission’s directives in 1991 provided that there should be separate accounting for infrastructure and operations. As such, it was not necessary to privatise railways; it did not matter whether the railway assets were owned in the public sector or the private sector. The matter of concern was how the railways operated, or transparency in the use of railway assets or its operations.

Emphasis on private funding and the PPP approach in the modernisation of railways and its capacity building to be a public utility of world-class would need to focus on its core business of operations and also on its performance. The government had emphasised the role of the private sector in the modernisation and improvement of railways. Economic Survey (ES) for the year 2015–2016 reads as, ‘Private investment must remain the primary engine of long-run growth. But in the interim, to revive growth and to deepen physical connectivity, public investment, especially in the railways, will have an important role to play’ (GOI, 2015–2016).

The railways’ budgets had laid great emphasis on development and capacity building and involvement of the private sector. In this regard, the Railway Minister in his budget speech for the year 2015–2016, on 26 February 2015, mentioned that:

Railway facilities have not improved very substantially over the past few decades. A fundamental reason for this is the chronic under-investment in railways, which has led to congestion and over-utilisation. As a consequence, capacity augmentation suffers, safety is challenged and the quality of service delivery declines, leading to poor morale, reduced efficiency, sub-optimal freight and passenger traffic, and fewer financial resources. This again feeds the vicious cycle of under-investment.

The Minister said that:

a number of sections are over-stretched; the same track was used for running fast trains as well as slow passenger trains or goods trains which reduced the speed of all trains on that track. The objective was to improve capacity on the existing high-density network, it is cheaper and faster and also that of gauge conversion. Further, railway transport is more cost-effective as compared to the road as the former consumes 75 to 90 per cent less energy and the unit cost of rail transport for freight was lower vis-à-vis road transport by about ₹2 per tonne-kilometre (TKM) and for passengers by ₹1.6 per passenger-kilometre (PKM).

In IRs, freight contributes about two-thirds of the total revenue and passenger receipts are only 27.3 per cent of the total. As against this, the cash working expenses account for 63.3 per cent and additional commitment expenses (pension and depreciation provision) of 22.7 per cent add to total expenses as 89 per cent. This highlights the need to analyse the cost-effectiveness of both passenger traffic and goods traffic. This emphasises the need for the adoption of accrual basis accounting to highlight the commercial viability of various business segments. This is to report price distortion in railways and to reflect to what extent freight traffic is sensitive than passenger traffic; and within passenger traffic categories, upper-class passengers are less price-sensitive and may be better placed to internalise price hikes vis-à-vis, other passenger classes. To what extent, passenger fares have been kept low and profit generated via freight services have cross-subsidised passenger services and Indian freight rates (PPP adjusted), remain among the highest in the world. This in turn has undermined the competitiveness of the Indian industry (Dhameja & Dhameja, 2016, p. 191).

In accordance with the ‘Make in India’ campaign, the government finally gave a green signal to the two much-awaited big-ticket 100 per cent FDI proposals for setting up electric locomotive plants in Madhepura, Bihar, and diesel locomotive plant at Marhora, Biharat a cost of ₹2,400 crore in 2015.

It would be of interest to note that railway finances historically were separated from the general budget. It was more due to political considerations and it usually used it to sub-serve political objectives. It was with an objective ‘to secure stability for civil estimates by providing for an assured contribution from railway revenues and to introduce flexibility in the administration of the railway finance’. Railway finances in India were separated from the general budget as per the Legislative Assembly decision in 1924. Accordingly, the first Railway Budget was presented in 1925; since then the railway budget is presented separately from the main budget though many ministries have surpassed the railways in terms of their size (Dhameja, 2013). However, the railway budget was merged with the general budget in September 2016 on the recommendation of the committee chaired by a Member of NITI Aayog, Bibek Debroy. Accordingly, the Union budget for the year 2017–2018 included the railway budget.

Further, the policy issue is whether to operate railways as a departmental enterprise or to run it as a corporation? According to an Expert Group on Indian Railways (GOI, 2001), if IRs is to survive as an ongoing transportation organisation, it has to modernise and expand its capacity to serve the emerging needs of a growing economy. In this regard, Karan Kumar (2007–2008) states that:

Corporatisation of Indian Railways is the best way to take its restructuring forward. The IRs should also adopt General Accepted Accounting Principles (GAAP), the role of the Indian Railways Regulatory Authority should be strengthened and it should be allowed to decide the fares to be charged from the passengers with a provision for adequate compensation from the Union Budget for keeping fares cheaper to fulfil its objective of social welfare. Manufacturing of locomotives and wagons should also be through the PPP Model.

Further, Dayal (2010) writes that:

A separate rail budget, termed by The Economist as a bizarre system, has done a lot of damage. It has perpetuated an orgy of populism. Potential ministerial aspirants scramble for the railway portfolio to let them have a free run across the country, doling out favours, passes, concessions, contracts, trains, lines, factories and jobs. Several non-essentials get their undeserved attention and funds. The raison d’etre of railways is lost sight of. Some of the presiding deities in Rail Bhawan have advocated a sardonic myth of rail connectivity as the panacea for inclusive growth and saddled the system with Non-performing Assets (NPA).

No doubt, the Railway Minister for the year 2015–2016, used the term ‘corporate’ and talks about the five-year Corporate Safety Plan without specifically mentioning corporatisation of railways. Though he had mentioned introducing corporate style book-keeping, the same was the objective set by the Minister in her budget speech for the year 2010–2011 by announcing the intention to bring in accounting reform to introduce accrual base accounting.

Further, in accordance with the provisions of the Indian Railways Act 1989 and the Railway Board Act 1905, core activity operation is done by the government, while some of the non-core activities have been hived off to 16 entities as public sector undertaking, corporations, or statutory authorities. Operating ratio, the ratio of revenue to cost reflects the operating performance of railways. This ratio was 98. 4 per cent in 2017–2018. It is presented below.

From Financial Year (FY) 10 onwards to the present date, the best operating ratio was 90.2 per cent in FY13. The year-wise operating ratio during the said period was 95.3 per cent (FY10), 94.6 per cent (FY11), 94.9 per cent (FY12), 90.02 per cent (FY13), 93.6 (FY14), 91.25 per cent (FY15) and 90.48 per cent (FY16). The last two years have been particularly bad for the IRs as the operating ratio has reached a level of 96.5 per cent (FY17) and 98.4 per cent (FY18). One of the contributory factors has been free and concessional free tickets/passes and Privilege Tickets Orders (PTOs) to various beneficiaries (CAG, 2019).

The IRs find themselves in under-investment resulting in lack of capacity addition and congestion below-potential contribution to economic growth, neglect of commercial objectives, poor service provision and consequent financial weakness (GOI, 2015–2016). All this highlights the need for:

greater investment in railways to boost aggregate growth and to make Indian manufacturing competitive; introducing serious reforms to rationalise tariff, to overhaul technology; and operating railways on commercial principles and to attract private investment primarily for its non-core activities.

As a process of opening up, the government decided to involve private companies in operating a certain segment of routes, and in the first phase, 150 trains on 109 routes have been identified to be opened to private companies. Private trains will be in operation in April 2023 and their freight will be decided by competitive bidding to enable them to recover their costs. These trains would cover all important cities and major tourist and pilgrimage destinations and would constitute only five per cent of the mail and express trains and the rest 95 per cent will be operated by railways. The train routes opened to the private sector would involve an investment of around ₹30,000 crore and the trains shall be designed for a maximum speed of 160 kmph to reduce journey time. According to the railway ministry, a maximum of 18 pairs of such trains are planned to be operated under Mumbai clusters (regions); followed by 13 pairs each under Delhi and Prayagraj regions; 12 pairs of such trains will be operated under Chennai region; 10 each under Howrah, Patna and Secunderabad clusters; nine each under Jaipur and Chandigarh regions; and five pairs of trains will be operated under Bengaluru region (Dash, 2020).

About twenty private companies have evinced interest to take up the operation of trains on these routes. Contract norms would include:

Concession period of 35 years; Private operators to buy and maintain the train sets, normally under the ‘Make in India’ policy of the government; Private operators shall pay to IRs fixed haulage charges, access to railways infrastructure, energy charges as per actual consumption, and a share in gross revenue determined through a transparent bidding process; and The private operator will have to conform to key performance indicators like punctuality, reliability and upkeep of trains.

The private participation would be on similar lines as of the 1990s when the economy was opened up to the private sector in areas like civil aviation and electricity to encourage greater competition, lower costs and improve service delivery. To ensure smooth functioning, and also to have the successful involvement of private companies in rail operations, there has to be an autonomous regulator with a defined role. However, for the smooth functioning and success of the proposed private sector involvement in rail operations, it necessitates:

railways should move to a complete and comprehensive system of accounting indicating the cost of each operation and activity and the finances required for the same, that is, accrual accounting instead of the current cash basis accounting; clear division between the Railway which will own and operate common infrastructure and the private sector companies which will be assigned the operation of 150 trains.

These are essential to avoid conflict of interest and to ensure good corporate governance.

The freight of other 95 per cent trains would not be increased to enable the general public to avail of rail travel facility.

The government appointed a committee under the chairmanship of Bibek Debroy (BD Committee) (Debroy, 2015) to suggest ways to mobilise resources for the IRs and restructure the Railway Board. The committee submitted its report for ‘Mobilisation of Resources for Major Railways Projects and Restructuring of Railway Ministry and Railway Board’, in June 2015, (GOI, 2015–2016). The committee reported that:

There is a wide gap between the supply and demand expectation in terms of the number of trains and their carrying capacity vis-a-vis, the quantum of traffic; Many decisions in IRs, like increase in fare, the introduction of new trains, provision of halts and establishment of new projects, are taken based on other than commercial considerations. In the absence of commercial accounting principles in the working of IRs, the costs and returns from such investments are not assessed. The sharing of the burden by the state governments and other interested parties is limited and it ends up as a burden on the nation’s economy; Since IRs is no longer a monopoly and is facing stiff competition from the road sector, the cross-subsidisation of low passenger fares by artificially high freight rates has led to a shift in favour of road transport. Most passengers are willing to pay higher fares if accompanied by better service; The entry of new operators in railways with proper regulatory mechanisms will introduce healthy competition in the interest of all stakeholders; IRs, besides its core function of the running of trains, is engaged in other activities which are non-remunerative, like provision of security to customers, medical and education facilities to employees. To state, IRs runs medical services with an infrastructure of 125 hospitals, 586 health units and 14,000 beds; there are 2597 medical officers and 54,000 paramedical staff. As regarding education, IRs runs a one-degree college and 108 railway schools; which are a burden on IRs; IRs is over centralised and departmentalisation affects working culture and results in decisions based on narrow departmental goals instead of the benefit of an organisational objective; and Apart from operations, the IRs has a wide range of off-time peripheral activities— catering, real estate development, maintenance of infrastructure, maintenance of locomotives coaches, wagons and their parts, security; besides as mentioned earlier, running of hospitals and schools, and so on. These activities are mostly unremunerative, result in a huge financial burden and skewed manpower profile—an adverse tech-to-tail-ratio.

Recommendations of the Committee

IR should be unbundled into two independent organisations—one responsible for the track and infrastructure and another that will operate trains. Further, offline activities be separated from core activities. As regards, offline activities recommendations are:

The Railway Protection Force (RPF) and Railway Protection Special Force are meant to ensure better protection and security of railway property, passenger areas and passengers, albeit with limited police powers which are mainly vested with the Government Railway Police (GRP) for which railways bear half of the cost. Since law and order is a state subject, the committee recommended two-fold actions. The state governments should ensure the cost of GRP; alternatively, the General Manager (GM)/Divisional Railway Manager (DRM) should have the freedom to choose between private security agencies and RPF security on trains. Similarly, the education needs of the employees should be taken up through subsidising alternate schooling including Kendriya Vidhyalayas and private schools; Similarly, for medical services, a multi-pronged approach has been recommended including CGHS or subsidised health care in private hospitals; Works relating to the cleaning of trains, stations, IT initiatives, at present performed by multiple agencies should be integrated to avoid sub-optimal performance; and All projects construction—whether zonal or others—should be brought under PSUs such as Rail Vikas Nigam Limited (RVNL) and Indian Railway Construction Limited (IRCON).

Board Level Policy Changes and HR Management Reforms

The three functions of policy-making, regulation and operations should not be with the same agency and should be properly split and defined. There should be a clear division of responsibility between the Government of India and railway organisations. The ministry should only be responsible for policy for the railway sector and parliamentary accountability, and should give autonomy to the IRs;

The Railway Board, an apex body of railways, should be like a corporate board headed by a chairman, like a CEO, who should be from within the Indian Railways having a minimum of three years of remaining service. He should have the power of final decision-making and a veto (in case of a divided view). In this respect, the government has recently decided that the Railway Board, besides a Chairman, will have four members (as against eight members earlier), in infrastructure, rolling stock, finance and operations and business development. Eight Group A civil services are merged into one, and should be known as Indian Railway Management Service (IRMS); lateral entry should also be allowed (Dutta, 2019);

The IRs organisation is ‘overly centralised and hierarchical’ and departmentalism has adversely affected its working culture. Each department is pursuing its narrow departmental goals, each having different priorities and measures, regardless of organisational objectives or benefits;

There are too many zones and divisions, which should be rationalised and there must be decentralisation down to the level of division. The head should be treated as an independent manager with adequate financial powers, sharing of revenues, should have the power to sanction new posts created under surrendered posts. Besides, there should be delegation and decentralistion of powers for Station Master and Zonal GM;

Employee cost including pension is the single largest component in IRs. For IRs to be competitive, for its long-term economic viability and customer satisfaction, it should focus on business/customer units like freight business, passenger business, sub-urban business, parcel business, and so on. These should be taken as separate business units to work out the cost and benefits for each unit. The BD Committee also made recommendations relating to promotion, higher professionalism, appropriate empanelment and mid-career training for IRs employees;

There should be an autonomous regulator with a well-defined role. Setting up a Railway Regulatory Authority of India (RRAI) statutorily, with an independent budget would ensure that it is truly independent of the Ministry of Railways. It would have the powers and objectives of economic regulation—including tariff regulation, safety regulation, service standard regulation, and so on. RRAI would be similar to that of the Insurance Regulatory and Development Authority (IRDA) and the Security and Exchange Board of India (SEBI);

Credible regulator will ensure smooth functioning and to have fair access to common infrastructure by private companies, it should avoid conflict of interest and ensure a fair working field for those companies;

RRAI should possess quasi-judicial powers, with appointment and removal of members distanced from the Union Ministry of Railways;

There should be an Appellate Tribunal which will hear appeals against the orders of RRAI and further appeals against the orders of the Appellate Tribunal can be directed to the Supreme Court; and

For raising resources for investments, an Investment Advisory Committee may be set up, consisting of experts, investment bankers and representatives of SEBI, RBI, IDFC and other institutions.

Accounting Reforms

With the diminishing government funding, Indian Railways has to look for non-government sources of funding. Since it is a commercial enterprise, its accounts should be structured on a commercial basis, and the accounting system must be revamped to reflect the cost of various activities and services accurately;

The traditional costing system should be revised and updated for apportionment of joint costs. A management structure should be reorganised around Line of Business (LOB) and Line of Service (LOS), and the accounting system should be reworked to align it with commercial principles. As followed by most other railways, Indian Railways should adopt commercial accounting with inbuilt depreciation accounting;

The current plan-head wise investment approach should be dispensed with as it destroys investment priorities and promotes departmentalism; rather, investors should focus on total capacity creation, including rolling stock and assets renewal technology induction. ‘Replacement and renewal of assets should be ensured, and the ad-hoc approach followed in respect of appropriation to Depreciation Reserve Fund needs to be changed to a rule-based approach that adequately takes care of this requirement’;

For the implementation of the economic reforms, a clear-cut road map may be drawn with a time frame for constituent activities, to have a responsive and transparent accounting and costing system. It should be monitored and guided at the top level and the monitoring agency, supported by domain experts from outside the railway system, should be constituted and the reforms relating to the accounting system should be carried out within an outer limit of two years;

The need for accounting reforms had been earlier recognised and accepted in the Railway Board as an accounting reform project was initiated and sanctioned in 2004–2005. However, the work has made tardy progress and the final results are far off yet. Unless IR undertakes sweeping accounting reforms, no one is going to risk putting money into it. (Sadipan Deb, as reported in Bibek Dibroy Report (Para 3.14)); and

The committee refers to the Rakesh Mohan Committee (GOI, 2001) which reported that as, the existing managerial, financial and accounting systems used by IRs have served well as a government entity operated under a monopolistic transport market and the accounting procedures were well understood within the organisation but were translucent to the outside world; and if IRs is to attract funds from abroad, it has to adopt an accounting system which communicates and interprets their policies well.

In short, the committee recommended three things for private participation in railway operation. First, railways need to clean up its accounts and move to an accrual system from the current cash accounting. Second, there must be a clear division between the part of railways which will own and operate common infrastructure, and the section which runs trains. This is essential to minimise conflict of interest. Lastly, the credible and autonomous regulator would look into the costing of common services and will ensure a fair playing field between private operators and IRs.

Other Recommendations

A Railway Infrastructure company should be created as a government Special Purpose Vehicle (SPV) (with a possibility of disinvesting in the future) that owns the railway infrastructure, delinked from IRs;

All the existing production units should be placed under a government SPV known as the Indian Railway Manufacturing Company (IRMC) under the administrative control of the Ministry of Railways. No privatisation needs to be contemplated, at least initially;

An ex-cadre post of a Chief Technology Officer (CTO) needs to be created, reporting directly to the Chairman of the Board and all IT initiatives should be integrated and brought under the umbrella of this directorate exclusive of any departmental handling in Board;

Subsidies should be targeted towards those who need them. Link Aadhar numbers for passengers when tickets are purchased. Subsidies on passenger fares to be reimbursed directly into bank accounts, for those who are under Below Poverty Line (BPL). Such subsidies must be borne by the Union government;

IRs must encourage on-board catering through large food chains and local restaurants on the payment of a modest licence fee. This can be enabled simply through web booking and thus offer customers a wide choice of local cuisine, delivered at their choice of station by the restaurant;

The committee laid down a timetable for the implementation of various recommendations and the activities relating thereof; and

The committee acknowledged that the IRs will be a humongous task, ushering a large scope of proposed changes. Thus, to implement the recommendations, the committee suggested that the ‘responsibility should vest in the Minister of Railways alone with an appropriate reporting to PMO’. In this respect, the committee recommended setting up of a strong formal implementation and monitoring mechanism to implement the enormous transformative reforms and considering the sheer size of the organisation along with the inclusion of officers with expertise and functional domain knowledge (Debroy, 2015). The committee has not recommended privatisation of IRs. It, however, has endorsed private entry, already part of the accepted policy. The committee preferred the use of the word liberalisation and not privatisation, as both are apt to misinterpretation. (Debroy, 2015).

Privatisation of Railways: International Experiences

Privatisation of railways in various countries has been discussed to draw lessons for such an exercise in India. Some countries including Japan, New Zealand, Argentina, Sweden and the UK adopted the ‘Top Down’ approach wherein the government first designed an alternative organisation structure. The ‘Bottom-up’ approach was followed in countries like the US and Canada, wherein the private sector took the initiative (Kopicki & Thompson, 1995; Debroy, 2015).

Japan

Privatisation of Japan National Railways (JNR) was preceded by restructuring it into seven separate companies—six Regional Passenger Railways and one National Freight Railway—and took about ten years to sell the stock to public. Features of Japan Railway Privatisation are as follows.

Horizontal Separation (or Regional Subdivisions)—for various islands

Functional Distinction (or Passenger and Freight distinction)

Vertical Integration (or Operation and infrastructure integration): Each Japan Railway Company owned rolling stock and infrastructure. Access to another company’s tracks for the operation was allowed on negotiations between the two companies.

The lump-sum subsidy was there for low-density companies.

There was a provision of allowance for non-rail service.

Yardstick Competition: Ministry applied yardstick competition scheme for assessment of fare revision. The performance of the operator is compared with other operators, if the assessment has low performance, then the fare revision was not approved.

New Zealand

The restructuring was carried out by multi-phase enterprise development before it was ultimately sold to strategic investors. It took about ten years commencing with the transformation of the former railway department into statutory corporation and ending with the sale of corporation shares to pre-qualified investors through a competitive process.

Argentina

As a process of restructuring of Ferrocarries Argentina (FA), the state-owned enterprise was divided into 14 concessions over five years, and these were offered to the private sector. The restructuring was carried out as the country had hyper-inflation and needed to curb deficit spending.

Sweden

Swedish State Railways were separated into two activity centres, namely:

State-owned rail operating company (Statens Jarnvagar SG): It had a monopoly for freight transport over the entire network and for passenger services over the mainline network. Banverket (BV), the national rail administration: It was responsible for providing and maintaining the country’s railway infrastructure.

British Railways Reorganisation

The period of the 1950s is known as the era of modernisation and rationalisation of British railways to eliminate the fiscal deficit. Privatisation of railways was rolled out with the Railway Act of 1990 which enabled broad reforms as:

Horizontal Separation: 25 train operations known as Train Operating Companies (TOCs) were privatised, most of these services were franchised. Vertical Separation between ownership and operation. Rail Regulator with the power to grant operating licence.

Railways Act 2005 dissolved Strategic Railway Authority (SRA) created earlier and the one which was responsible for operation—maintenance and improvement of railway infrastructure. Some of these functions were transferred to the Department of Transport. Similarly, responsibility for rail safety was transferred to the office of Rail Regulation, the industry’s regulatory authority.

Thus, rail reorganisation led to the unbundling of the railways into:

Discrete Value: adding functions such as car maintenance. Terminal operations: locomotive maintenance, track repair, unit train operation, and so on.

These were vertically connected in small enterprises that were offered for sale.

Germany

The Deutsche Bundesbahn (DB), German Federal Railway is owned by the Federal Republic. By constitution, the Federal Republic is required to retain (directly or indirectly) a majority of its infrastructure stocks.

Germany’s two state-owned passenger trains, DB long-distance and DB regional, both benefit from government financial support. DB and its subsidiary passenger and infrastructure companies are responsible for financing their operation, management and maintenance expenses entirely from revenues.

United States

There are two kinds of private carriers.

Large inter-regional carriers

Small local carriers

Since the liberalisation of Economic Regulation in 1980, the US Rail Industry has been transferred and the restructuring process has led to hundreds of small railways.

As such US railroads are separated into three classes based on their annual revenues:

Access by private contract is a predominant feature in freight management in the USA. All the Class I railways and around 90 per cent of the rest are private-owned.

Canadian experience is similar to that of the US, though the restructuring process has been slow.

China

In 2005, China adopted the Joint Venture model which was funded 50:50 by debt from local banks & equity from the Ministry of Railways.

The new China Railway Corporation (CRC) was established in 2013 to take over the commercial functions previously performed by the Ministry of Railways (MOR).

The policy is to separate government from enterprise, shift from control to regulation and supervision, reduce red tape, boost administrative efficiency, strengthen supervision of rail transport, safety, and tackle rampant corruption.

Russia

Russian Railway (RZRD) is a state-owned company in charge of the railway infrastructure, and train operation for freight and passenger. Federal Railway Transport Agency (FRTA), another unit of the Ministry of Railway regulates rail transport.

RZRD is now a joint stock holding company having 63 subsidiaries. Competition is encouraged by private sector participation.

Since 2010, RZRD transferred staff and assets to the newly formed Federal Passenger Company which is responsible for long-distance rail passengers

Following is the line of arguments favouring privatisation and the views against privatisation of Railways.

According to Nick Kingsley, Britain’s rail network is privatised, the service is abysmal, fares are stratospheric. ‘To restore our railway as a network we can be proud of, it must be renationalised. And we know that it will work because continental European railways are cheap, punctual, pleasurable and nationalised. Right?’(Kingsley, 2018).

As regards privatisation in Britain, The Adam Smith Institute has written that while it would prefer more competition within the system, privatisation has introduced competition into the system which has meant an explosion in passenger numbers (Southwood, 2014).

According to Birrell (2013) ‘on balance, rail privatisation has been a huge success’ in terms of passenger numbers, fares and public subsidy, as well as Britain having both the safest railways in Europe and ‘most frequent services among eight European nations tested by a consumer group’. ‘Forget the nostalgia for British Rail—our trains are better than ever’ .

The Guardian (2015) in its editorial reported that, despite some problems, privatisation has delivered many improvements. The editorial said that although privatisation, 20 years ago was an ideological move, to renationalise the railways at a time when they are quickly growing would also be motivated by ideology.

Again, The Guardian (2017) in its editorial reported that ‘twenty years after rail privatisation was completed, passengers put up with late, expensive and frequently overcrowded services. The state should run a few train firms or private companies would be forced to up their game’. The article further states that there are few more annoying issues for the great British public than their railways. While some cities and towns have seen stations spruced up, the public suffers from often late, expensive and frequently overcrowded train services. Further, the cack-handed rollout of infrastructure improvements has led to cancellations and delays on the network, commuters saw ticket prices rise at twice the rate of their wages between 2010 and 2016. It was also reported that rail passengers would be hit by the largest fare hikes in five years. The situation, it seemed, was one where private companies would reap the benefits, while passengers would bear the costs.

Morgo (2018) in the blog ‘European rail deregulation: UK and Sweden examples’, compared both the UK and Sweden railways privatisation and stated that the UK is the most mature privatised market but is also the most criticised one. On privatisation, British Rail, together with 28 private companies, took control of the passenger lines, paying for infrastructure and station usage. These had negative effects as follows:

Public spending on railroad subsidies doubled on privatisation; Ticket prices keep on rising, being the most expensive in Europe; There has been no innovation, or infrastructure modernisation; Due to track deterioration, there have been many security issues; and Rail passengers have decreased last year to 1.7 billion, the biggest passenger decrease since privatisation.

In short, the concession system in the United Kingdom is a complex one and involves too many actors, and ‘it needs greater collaboration between all operators and authorities, before awarding any new franchise’.

As regards Sweden’s approach to privatisation, Eve-Marie Morgo wrote that the Swedish market in 2010 was 100 per cent open to competition, to increase lines, frequencies and passenger ridership. Rail liberalisation divided Sweden’s state railway into two different companies: one responsible for the infrastructure—Banverket (BV), and one responsible for operating the trains—Swedish Rail (SR). This division led to a conflict of interests, as both companies did not share the same priorities. Since then, the rail sector experienced a dramatic job decrease and had an impact on working conditions.

As against the above, the overall result of the rail liberalisation in Sweden, despite many challenges, is positive as:

Rail passengers have increased from 10,828 to 12,373 during 2010 and 2016; The average ticket price has gradually reduced, following the entrance of Sweden’s new rail entrant, MTR Express, back in 2015; and Adoption of technology, enabled to have positive effects as under. simplify rail travel stimulate competition bring down fares

Lust (2016), reported that the privatisation of monopolistic infrastructure is economically wasteful and politically divisive. In 2000–2001, Estonia sold the passenger carrier and a portion of the track to domestic businessmen posing as a British strategic investor, and the main freight carrier and most of the track to an American-led consortium. The passenger carrier continued to receive government subsidies but closed several rail lines, which led to protests by passengers. The freight carrier earned large profits from the transit of Russian oil to Europe but invested its money in buying used American locomotives, rather than rebuilding the track. Both companies laid off about half of their workforce, provoking the first private-sector strike in Estonia since the collapse of Communism. In 2006, a new government bought back the freight services and track at more than twice the sale price, an expensive lesson in the perils of privatisation.

Since the UK’s railways were privatised in 1997, out of roughly 30 UK railways, only six are fully owned and operated by private companies or British government authorities as,

German state railway (Deutsche Bahn) operates four British railways including the London overground and the Grand Central line to Sunderland;

Seven UK railways are operated or partly operated by Dutch state railway Nederlandse Spoorwegen (NS), including Merseyrail, Scotrail and the West Midlands Railway; and

Seven railways are operated fully or partly by French state railway SNCF, including Transport for Wales and the Thameslink (Keating, 2019).

Britain’s rail network is privatised, the service is abysmal, fares are stratospheric. To restore our railway as a network we can be proud of, it must be renationalised. And we know that will work because continental European railways are cheap, punctual, pleasurable and nationalised. Right? (Kinsley, 2018)

Bowmana (2015) challenges narratives of the success of UK rail privatisation using accounting data from Network Rail and private train operating companies. It says that large government subsidies channelled through Network Rail and lower track access charges levied by Network Rail have artificially inflated train operator profits, generating returns for the taxpayer and the illusion of financial self-sufficiency has radically changed the appearance of railway finances. The study accounts for the British experiment with rail privatisation and how it has worked out economically and politically. The focus is not simply on profitability and public subsidy, but on the appearances which accounting arrangements create. This accounting fix has bolstered claims that rail privatisation has been a financial success (Bowmana, 2015).

Privatisation Abroad: Lessons Learnt

Having discussed the privatisation experiences of various countries and diverse views on such experiences, let us look into what lessons can we draw and what are the steps to go ahead:

From the experiences of privatisation in various countries, it emerges that privatisation is not a one-shot activity. It is a multi-phase activity and is normally spread over years, though some activities can be taken up simultaneously; There is a mixed reaction to privatisation, some argue in favour and many others view it negatively. On an average, rail travel is expensive in Britain than in France and it differs from country to country. As such, privatisation means different things in different parts of the world—where both the fundamentals of the economy and the purpose served by privatisation may differ. Rather, it is the management approach in managing resources and monitoring systems to attract competition which makes a difference (Goodman & Loveman, 1991). Even examples of prison privatisation in various countries have shown encouraging results (Dhameja & Dhameja, 2016, Chapter 15); To ensure good governance, and effective management, three primary functions namely, policy formulation, regulatory function and operations, should be handled by three different agencies, with clearly defined roles without any ambiguity. In the case of IRs, policy formulation would be for the transport industry including that of road, civil aviation, and port and water transport. For railways, passenger and freight operations would be a policy matter to be finalised by the Railway Board; IRs should transform from its current departmental form to a corporation, an incorporated body, as per general experience abroad, as the latter facilitates autonomy and accountability, adoption of commercial accounting, raising funds globally and marketing of shares on privatisation. It also tends to minimise political interference as it is governed by a board under a separate statute; Independent and autonomous regulator would ensure a proper playing field between different departments and also between private operators and the government departments. Independent regulators would have a role in advising on specialised tasks like powers and objectives of economic regulation—including tariff regulation, safety regulation, service standard regulation, and so on. RRAI would be similar to that of IRDA, SEBI advising on raising of resources and also working out the performance of different players; The number of departments or divisions should be rationalised and the departmental managers should be empowered to take decisions. IRs should be de-bundled by classifying its activities into core functions like the running of trains; and non-core functions that are peripheral or off-line. The core function of IRs should be the business of running trains; Of various conditions for restructuring IRs, a clean, correct and complete system of accounting is of prime importance. Current plan-head-wise accounting should be switched to accrual accounting to ascertain the cost of each product and each service on commercial principles which also incorporates depreciation cost; Emphasis should be to have an accounting and cost management system covering all elements of costs and apportionment of the joint costs and infrastructure costs for various products and services. Railways, having a monopoly, should have a system to workout the cost for each business (COB) and the cost for each service (COS). For this purpose, the management system and organisation structure should also be aligned to COBs and COSs. COBs and COSs should be set up as Separate Business Units (SBUs); No doubt, attempts have been made earlier towards shifting to commercial accounting, but the results have not been as expected, so it emphasises the need for implementation. The Report (RD, 2015) stresses developing a mechanism and system for timely implementation and also specifies the accountability of the Rail Minister and also reporting to PMO; As a policy, there should a plan for the extent of opening of the core and non-core activities to the private sector in the future; Non-core activities like medical care and education facilities for employees should be demerged from the railways by outsourcing or having arrangements, like CGHS or with private agencies, as is the practice for other government employees. Similar should be the situation towards education facility for employees and their children, that is, through Kendriya Vidyalayas; Security is another non-core area where the private sector can be involved; the state government can be taken into confidence for sharing of expense for such activity as security is a state subject; Similarly, other non-core functions or off-line activities, like maintenance of stations, repair and maintenance workshops and locomotives, production units, cleaning or washing of trains should be out-sourced. The present system of involving private organisations in such activities should be systematised with a proper control mechanism. Some of these activities are revenue-generating activities and so there should be a system to monitor revenue sharing; Running of trains, and modernisation and development of train capacity in terms of rail track should be given due importance and priority. As per the current decisions, 150 trains on 101 routes are to be run by the private companies by April 2023 with a concession period of 35 years, and the private sector is expected to invest ₹30,000 crore. This accounts for approximately five per cent of the total train routes; Policy for the remaining train routes, in particular in low developed areas having low profitability, needs to be spelled out. Two different fare structures may create two different classes and that may lead to some social differences and social problems; The restructuring plan, it is expected, will address the current problem areas like, bringing in more investment for capacity building, or over-stretched and using the same track for fast trains as well as slow passenger trains or goods trains which reduce train speed. Similarly, will the private operators be allowed to use the current rail track or new track will be laid? The production units (eight) should be taken as separate business units and should be out-sourced. These may be permitted to market their products or services; Sixteen PSUs under the ministry should be managed and governed as other PSUs; As per one view, privatisation or even partial privatisation, is not the best idea from an economic point of view. There is a need for wholesale reform to run and structure IRs as a professional management company by converting it into a holding company (Sharma, 2019); Though the committee has laid down a five-year time frame for implementation of recommendation, should we not take 2020 as the starting date? As restructuring or privatisation projects are multi-phase projects and are spread over years; many of the activities initiated earlier, like, adoption of commercial accounting, had spilled over several years. In this respect, the recommendation of the committee to have a mechanism to control such slippages and also laying down accountability has to be taken seriously; No doubt, restructuring or privatisation is a political decision, and as such in many countries separate enactments had been passed, still, administrative acumen plays an important role. With the given current strong political will, IRs restructuring could be expected to come true; and Lastly, requisite amendments in various enactments, like the Indian Railway Act, to allow levy of tariffs by private operators and the fares considering market forces would be allowed.

Footnotes

Acknowledgements

Authors express their gratitude to Dr N.C Wadhwa, IAS (Retd) and Director General, Manav Rachna Educational Institutions for his comments on the earlier draft of the paper.

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.