Abstract

This fascinating publication is an excellent contribution on State-Owned Enterprises (SOEs) in China, dissecting their changing role and importance as an instrument of State Capitalism and Economic Statecraft. Divided into nine chapters, the book is interspersed with rich data and case studies on SOEs and their operations in China. The study is the result of several years’ research at the Hongkong and Sanghai Banking Corporation Limited, Business School of the Peking University. The book dispels many accepted assertions regarding SOEs in China beginning from their wholesale privatisation to their passivity in contributing to China’s economic rise. It reveals that the total number of enterprises numbering more than 150,000 is still owned by the Central and local governments. Their share of industrial assets amounts to 40% of the Chinese GDP, besides their share of the pie in Bank credits which is a halfway mark. Despite budget constraints and difficult economic scenario, the state keeps SOEs afloat. SOEs are often called the ‘eldest son’ of the Chinese economy. In the larger scheme of statecraft, they are the most trusted players in Chinese strategies which intend to continue to have these enterprises as the last outpost of the Chinese State (p. 3).

The introductory chapters highlight extensively the role of SOEs. They are not just simple binary systems but a vital part of the Chinese economy. They are controlled not by the State but by an empowered regulatory body known as State-owned Asset Supervision and Administration Commission (SASAC). SOEs are under ownership by the people. The State ensures the consolidation and growth of SOEs. According to SASAC, administratively, SOEs are divided into ‘Central Enterprises’ (SOEs supervised and managed by local governments). The Central SOEs are economic giants. They are sub-divided into four categories: Central Industrial SOEs, Central Financial SOEs, Central Cultural SOEs and Central Administrative SOEs (p. 55). The responsibilities of individual Central enterprises in the national social and economic development are relatively unique. They belong to the management of the State Council and function at the ministerial level. SOEs have entered sectors such as chemicals, construction, shipbuilding, mining, utilities and energy. To be ahead of their rivals, SOEs sail on technological strength, creating high-quality services, effective overseas partnerships receiving the Government support on guarantees, relying on team talent and establishing brand goals. These enterprises have numerous subsidiaries functioning in the various provinces of China. There are provincial enterprises too besides the local-level enterprises. China continues to work through SOEs to build its might globally in essential sectors such as energy, finance, infrastructure, media and entertainment. The Fortune 500 list included 102 Chinese SOEs having revenue of $8.3 trillion. Chinese SOEs have been displacing Western enterprises from the Fortune 500 list of top enterprises (p. 125).

SOE reforms started with a big bang in the late 1990s by dismantling of tens of thousands of SOEs. The closure of SOEs resulted in massive suffering of millions unemployed. The restructuring process aimed to make SOEs more efficient and improving their performance. This was preceded by the first stage restructuring during 1978–1983. This initial stage focused on increasing the operational autonomy accorded to enterprise managers, mainly by allowing them increased authority over allocating their profits. The restructuring entered the second stage during 1984–1989. ‘Price and Contract Reforms’ were continued herein. Smaller State and urban collective enterprises instituted more radical measures. Market interface dominated the restructuring initiatives. The third stage, 1991–2000, focused on improving the efficiency of large and small SOEs with the objective of overcoming breakdown and problems intriguing Chinese economy. The Chinese leaders vowed to create a modern enterprise system resting on ten pillars stretching from increasing funds for product development to clearing inter-enterprise debt. Corporatisation was employed as the necessary gateway for privatisation, which strategy for ownership reform was antithetical to the Soviet Shock approach followed by the former Soviet Block (p. 102). The next phase of restructuring was devoted to intensify enterprise reforms. The main thrust was on cracking down on loss-making enterprises. The book discusses at length the methods of restructuring the units comprising decentralisation of management, reshaping of management and property rights and privatisation.

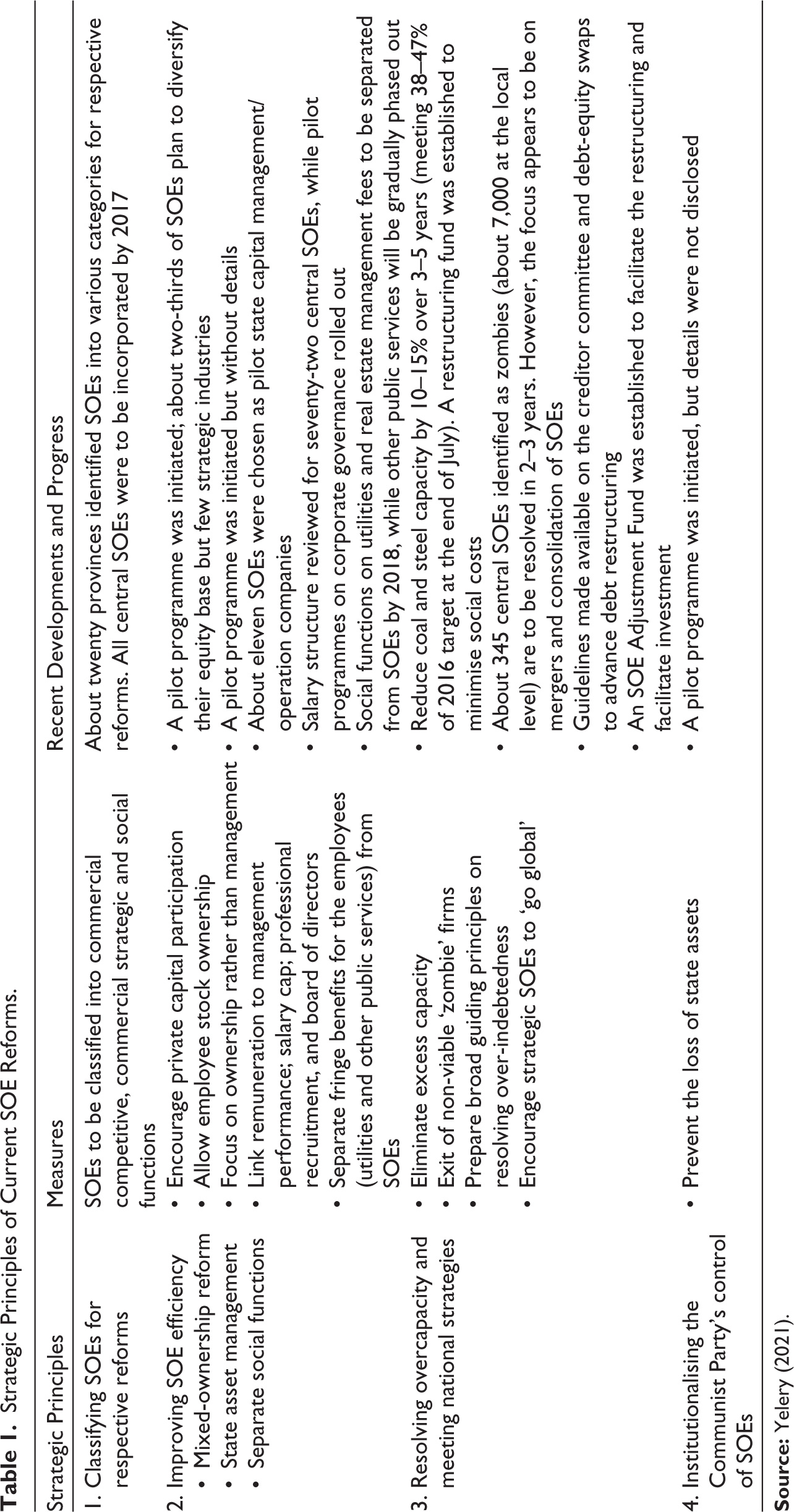

According to the author, the Chinese State continued to make strategic changes in SOEs through merging, superior known performing assets management and reorganising them into strategically organised categories. The global quest of Chinese enterprises received a great shot in arm with China’s accession to World Trade Organisation. China followed the principle of ‘grasp the big and let the small go’. China replaced its previous goal of reforming SOEs with a new one - building the world’s first-class enterprises and groups to deal with the competition in the international market. China adjusted the State-owned economic layout and structure. The governments’ role shifted from managing enterprises to capital management. The functions of owners and managers of SOEs were separated. After 2008, the operation of SOEs was gradually integrated with the market and accepted the golden rule of survival of the fittest. SOEs imbibing modernisation started doing better than their counterparts domestically and internationally. The author well describes the strategic principles of current SOE reforms in China as shown in the matrix presented in Table 1.

Strategic Principles of Current SOE Reforms.

The 19th Congress of the Communist Party of China further reinforced the need for SOEs and supported them in their emergence as China’s Poster-Child. The industrial and financial enterprises are significantly contributing to the wealth creation in China. SOEs form a major component of the machinery to implement Belt and Road Initiative and setting up enterprises jointly with private sector as a part of the Public–Private-Partnership Programme. SOE restructuring has travelled far and wide to the other provinces of China. The book describes restructuring initiatives of Provincial Enterprises of Zhejiang. SOEs as Provincial Enterprises are crucial for the Communist Party to mobilise party committees and reorganise itself internally. The local enterprises are crucial in delivering political provinces. As of 2018, there were 11,000 SOEs at all levels in Zhejiang provinces. These enterprises have performed well financially. The new goal of China is of cultivating World-Class enterprises with global competitiveness (p. 124).

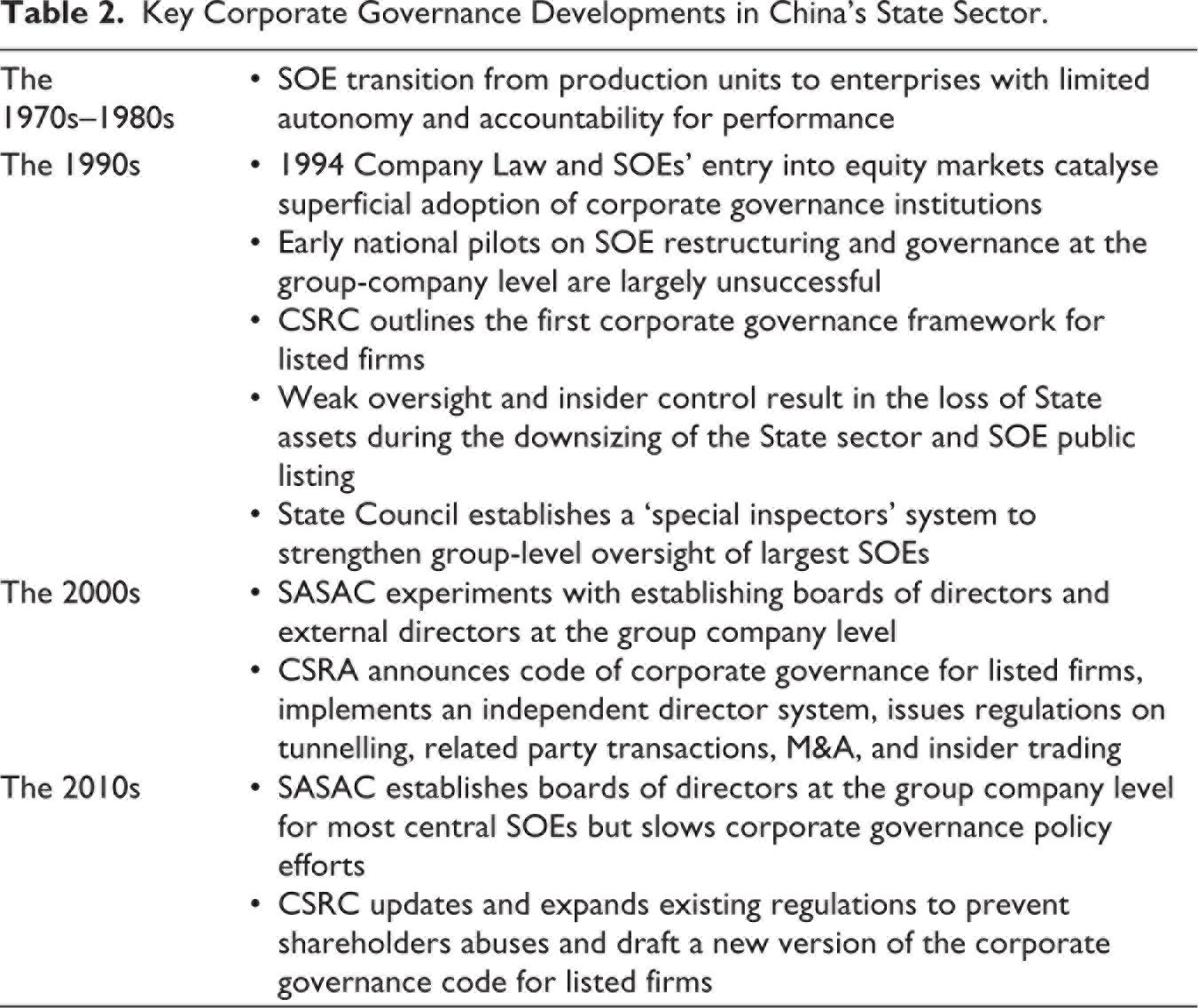

To remove major roadblocks in strengthening SOEs, China initiated many corporate governance reforms as summarised in Table 2.

Key Corporate Governance Developments in China’s State Sector.

The book under reference is first of its kind on SOEs in China which discusses in-depth the various stages of restructuring SOEs in China. It throws light on the rise and fall of SOEs in China and their emergence as phoenix at the central, provincial and local levels of administration. It chronicles the reform measures initiated during the various stages and mentions the especial features of Chinese restructuring of SOEs. The book brings out the hidden strategies of reforming Chinese SOEs and their outcomes. The modernisation of SOEs has dramatically improved their performance and made them competitive in the domestic and international markets. The controlled restructuring has reduced significantly the numbers of these enterprises but also created a few ‘global champions’ out of them figuring in the Fortune 500 list. The credit for this phenomenon is ascribed to the initiatives to establish a new regime of corporate governance. However, the book does not tell the readers the Board’s functioning at the enterprise level and about the dynamics of the business at SASAC. An important omission is not bringing in discussion the corporate democracy in SOEs and their stock market performance.

Arvind Yelery deserves rich compliments for the painstaking deep research on SOEs in China. His scholarly work clearly points out the fact that internally SOEs drive China’s brand of State capitalism while externally SOEs form part of well-crafted Chinese economic statecraft.

This is a ‘must read’ for policymakers, planners, administrators, CEOs, stock market chiefs, researchers and postgraduate students pursuing studies in international relations, economics, management, public administration and commerce and those who are working on SOEs’s reforms, restructuring and privatisation.