Abstract

Franchise encroachment, or the addition of an outlet in the vicinity of existing franchisees, is largely viewed as resulting in revenue cannibalization of incumbent locations. Against this backdrop, the authors consider the possibility that the addition of same brand outlets can, in fact, also create positive effects via customer utility and ultimately benefit franchisees, due to a range of mechanisms such as quality signaling, learning, or brand awareness, resulting in a positive pathway on franchisee performance. The authors unpack this possibility using an experiment and detailed proprietary and publicly available data sets from the hotel industry over a five-year period. Their results show evidence of positive effects on customer utility for same-brand outlets and stronger effects for newer brands, cross brands, and online travel agency channel bookings. Counterfactual simulations indicate that although encroachment hurts franchisees on average, it can modestly benefit same-brand franchisees in low-brand-density markets. Together, the findings illustrate the potential “sunny side” of encroachment, underscoring the need to update our view of encroachment as context-dependent. The novel emphasis on customers versus the dominant firm view suggests customer and incumbent responses to encroachment should be accounted for in the development of franchise strategy and public policy decisions.

Keywords

Franchise encroachment (“encroachment” hereinafter) is a key phenomenon in franchise management. Encroachment occurs when a franchisor places a new outlet in proximity to an existing franchisee(s). Incumbent franchisees view these actions negatively, as the new outlet increases competition and cannibalizes their revenues. This view is reflected in substantial literature in marketing, which primarily focuses on documenting this negative impact (Kalnins 2004; Nishida 2014) and managing the resulting conflict (Kaufmann and Rangan 1990). The literature also examines ways to safeguard franchisee interests through litigation (Antia, Zheng, and Frazier 2013), contracting (Kashyap, Antia, and Frazier 2012), and a range of governance mechanisms (Antia, Mani, and Wathne 2017). In broad strokes, this literature has painted a picture of encroachment as being predominantly negative for incumbent franchisees and has focused on firm roles.

We explore the possibility that encroachment might in fact be positive for incumbent franchisees by incorporating both a customer view and brand differences into this picture. Specifically, we introduce the possibility that customers may gain utility from more outlets of the same brand, subsequently increasing demand and, ultimately, franchisee performance. This utility might come about via a range of mechanisms such as quality signaling, learning, or brand awareness. While researchers have acknowledged conceptually that encroachment may improve franchisee performance (Blair and Lafontaine 2002; Kalnins 2004), little empirical evidence exists to date. The closest finding is limited: Chiou and Tucker (2012) show that multiple exposures of a trademark hotel brand name on a third-party intermediary’s website generated an overall net increase in consumer clicks. However, no studies thus far have provided evidence of encroachment activities directly improving performance via customer utility and demand.

While research has examined encroachment effects on customer demand in a static setting with endogenous franchisee pricing (Pancras, Sriram, and Kumar 2012; Thomadsen 2005), these studies do not make the distinction between same versus different brand effects on customer utility, and they focus on a single franchise brand. In contrast, we consider a range of brand characteristics within a franchise chain to inform a broader view of encroachment, performance outcomes, and a more explicit incorporation of the customer’s viewpoint. For example, an entry of a Residence Inn hotel will have same brand effects on other Residence Inn hotels and different brand effects on Westin hotels, Element hotels, and so on in the market. We examine these differing effects of brand encroachment on consumer choices.

Our context is a single franchisor, incumbent franchisee(s) of multiple brands, and a range of encroachment types across various markets. We model the net impact using publicly available data, a proprietary data set from one of the largest hotel groups in the United States over a five-year period, and an experiment. We find that encroachment effects are not only statistically significant but also economically relevant. Although the effects are predominantly negative, we nevertheless find positive effects on customer utility that are stronger for same brands, newer brands, cross brand locations (i.e., brands with overlapping monikers such as Hyatt Place and Hyatt House), and bookings made through online travel agencies such as Expedia and Kayak.

Counterfactual simulations reveal both positive and negative economic outcomes. Overall, encroachment reduces incumbent revenues and profits by 5.3% ($43,810 in revenue and $26,090 in profit per month), consistent with the historical bent of the literature (i.e., increased competition). However, this impact is not statistically significant for same-brand franchisees, suggesting the negative impact is reduced. Further analysis reveals significant positive effects in low-brand-density markets: same-brand franchisees improve performance by approximately 2% per month (i.e., $4,300 in revenue and $2,900 in profit), with 70% (30%) of these outlets realizing higher (lower) revenues as a result.

To the best of our knowledge, ours is the first study to directly model encroachment effects on customer preference and identify the conditions under which it might benefit franchisees. We find that while encroachment hurts franchisees on average, the prevailing assumption that it always results in revenue losses for all incumbent franchisees is inaccurate; we find a distinct difference in its impact on same versus different brand outlets.

The stakes for better understanding franchising phenomena are substantial. Franchising is one of the most pervasive organizational forms in the U.S. economy, accounting for as much as $890 billion, or 50% of all retail sales across 75 industries. This amounts to approximately 3% of the 2016 U.S. gross domestic product in nominal dollars. 1 Our research context—the hotel industry—accounted for approximately $660 billion in 2019. 2

In the following sections, we provide a motivating example, overview the relevant literature, and develop a customer utility model that estimates the net effect of encroachment, franchisee competition, endogenous pricing, and heterogeneous customer preferences. We next describe data, and the estimation section then applies a logit and a full demand model. We explore heterogeneous brand characteristics to gain further insights and present counterfactual simulations to consider market composition differences. A general discussion and implications for management conclude.

Background and Related Literature

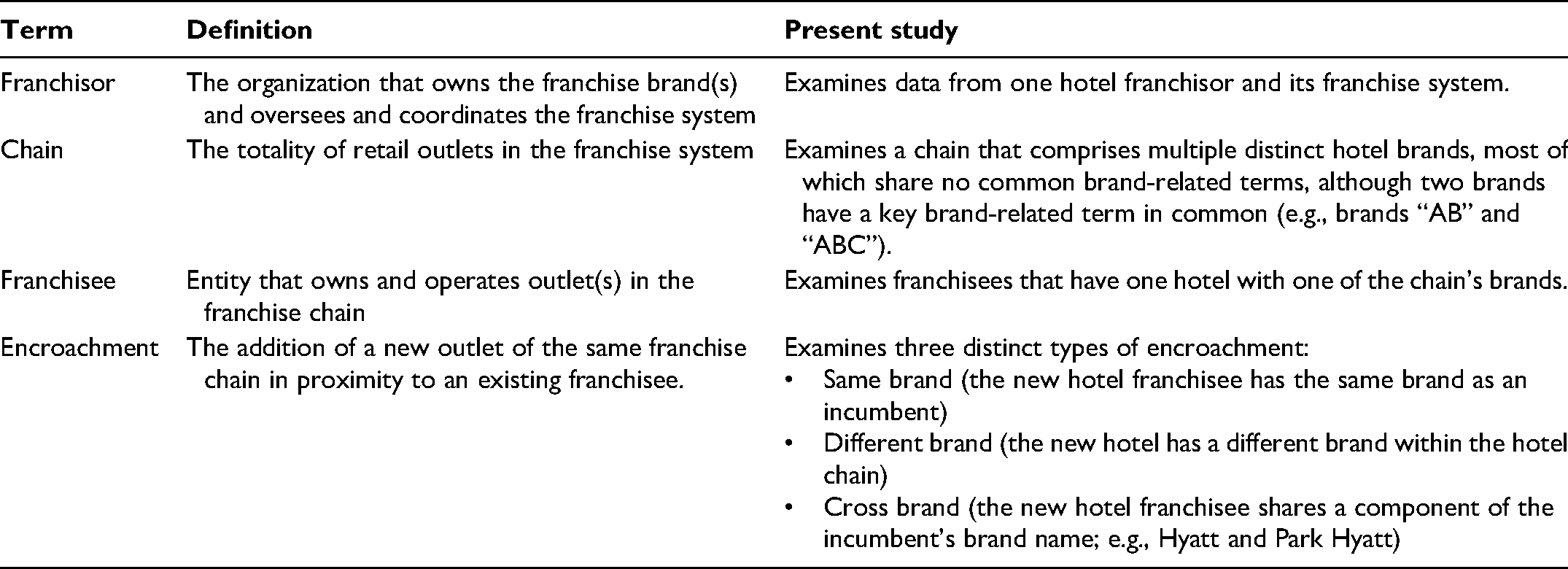

In this section, we review the related literature on franchise encroachment. Table 1 summarizes the range of terms that occur throughout the article and their definitions.

Terms and Definitions.

Sources of Conflict in Franchise Systems

Encroachment arises because franchise business models are marked by a fundamental incentive misalignment: franchisors earn a royalty rate on franchisee sales and an upfront fee (Lafontaine 1992), but franchisees are profit maximizing in their pursuits (Kaufmann and Rangan 1990). The fixed fee averages 8% of all payments from franchisees (Lafontaine and Shaw 1999), leaving 90% of the franchisor’s income from royalties. Given that franchisors cannot extract all rents via a fixed fee (see Kaufmann and Lafontaine 1994), they have an incentive to add more outlets as long as revenues are positive, but this creates a downward pressure on franchisee profits. This behavior is widely viewed as anticompetitive (Blair and Lafontaine 2002), and the incentive misalignment has led to an active regulatory context and lobbying efforts aimed to minimize the resulting conflict.

Several states have implemented measures to safeguard franchisees’ interests through disclosure requirements and relationship laws, and research has shown that such laws do in fact lower litigation incidences (Antia, Zheng, and Frazier 2013). Kashyap, Antia, and Frazier (2012) show how the franchisor’s use of ex ante contracts and extra-contractual incentives influence subsequent monitoring and enforcement, while Antia, Mani, and Wathne (2017) examine the relationship between governance mechanisms and franchisees’ motivation and bankruptcy.

Adding a New Franchisee Outlet

In a related vein, other research considers the factors that drive a franchisor’s decision to add a new location to a market. The academic literature mainly focuses on the trade-offs between increased franchisee competition and firm-side benefits such as preemption and firm size spillovers related to entry of hamburger chains (Blevins, Khwaja, and Yang 2018; Igami and Yang 2016) or new entrant sales at the expense of incumbents (Kalnins 2003, 2004; Mazzeo 2002). In contrast, practitioners predominantly talk about “demand generators,” or businesses that bring in out-of-town visitors, which seem to be less studied. Our analyses corroborate this and show the number of businesses as a strong predictor of hotel entry (Web Appendix W1). However, we find that local population characteristics are less relevant in predicting hotel entry after controlling for the number of businesses.

Encroachment Impact

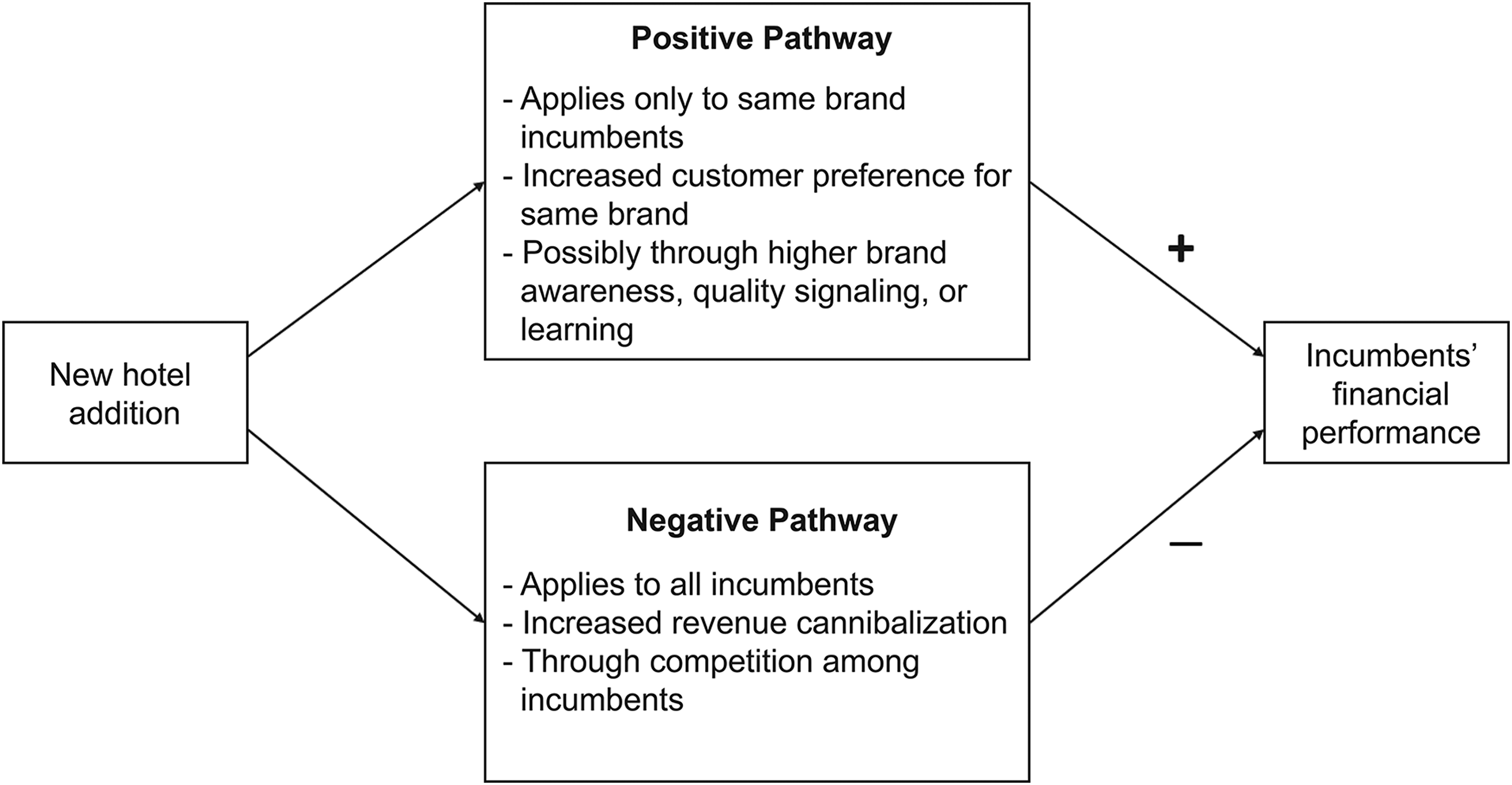

Encroachment can have positive and negative effects on incumbents. Herein, we consider potential theoretical mechanisms that drive positive and negative pathways and their performance impact, although we are not able to empirically tease them apart due to data or modeling limitations. Figure 1 displays an overview of the pathways.

Positive and negative pathways of encroachment on franchisees’ financial performance.

Negative Pathways

A long-standing prediction of industrial organization is that an incumbent’s prices and revenues will decrease if new firms enter the market through business stealing (Anderson and Renault 1999; Narasimhan and Zhang 2000; Perlo and Salop 1985; Tirole 1988). This prediction is easily extended to a franchising context: the entry of additional franchisees will lead to greater revenue losses for incumbent franchisees.

Ample evidence supports the resulting negative pathway from competition. For example, Kalnins (2004) finds that encroachment leads to significant decreases in hotel franchisee revenues per room ($51–$66.81 per quarter). Ingram and Baum (1997) show that a hotel in Manhattan was less likely to survive as the number of chain units in the area increased. Nishida [2014] shows the presence of competing convenience stores in the same market, regardless of their chain affiliation, reduces store-level revenues significantly. In fast food franchise settings, evidence for negative pathways approximates on average an 18 percentage point decrease in revenues (Yang 2012). Pancras, Sriram, and Kumar (2012) show that incumbents’ revenues are decreased by 1%–2%, but distance can help mitigate this negative pathway; for every one mile increase between stores, revenue loss is stemmed by as much as 28.1%. Collectively, these results show that encroachment generally hurts incumbent performance via negative pathways by increasing competition.

Positive Pathways

An alternative point of view is that a cluster of same-brand locations can be useful for customers, while simultaneously benefiting incumbents (Blair and Lafontaine 2002; Kalnins 2004). This possibility has been understudied. We next consider three possible drivers of positive pathways that can arise from customers.

Brand awareness

More same-brand outlets can increase awareness of the brand or simply make options more noticeable. Franchisee locations can act as a “living billboard to build awareness and positive brand association” (Avery et al. 2012, p. 97). Although most hotel customers are not local, this effect might be operative in online choice settings in which a consumer sees multiple same-brand locations available in a specific area (cf. Chiou and Tucker 2012). One extension of brand awareness impacting positive pathways is via cross-brand effects. In our context, an example of cross-brands is hotel locations with overlapping monikers, such as Hyatt Place and Hyatt House. Given the prominence of the Hyatt chain name, its use in multiple locations might boost demand for these outlets. This may increase brand awareness via multiple exposures and market prevalence.

Brand quality signaling

Multiple locations can also act as a quality signal, much as advertising communicates quality (Ackerberg 2001; Kihlstrom and Riordan 1984). When multiple products share a common brand name, this acts as a nontrivial “performance bond,” a credible indicator assuring consumers that products are of high quality, thereby lifting sales of all products under certain conditions (Wernerfelt 1988). Costly brand and infrastructure investments communicate a pledge to a prespecified quality level for both existing and new hotels.

This logic might be moderated by brand type and booking channel. For example, a quality signal might be more diagnostic for newer than for older, more established brands because consumers may perceive greater purchase uncertainty associated with new brands, and the quality signal acts as an assurance in the consumer’s choice process. Similarly, the signal might be more pronounced in channels in which customers do not have strong brand loyalty or product experience. As an example, when a consumer sees multiple Marriott locations in a purchase channel that overviews multiple brands, the cluster of outlets may be a more diagnostic quality signal (i.e., the brand’s commitment to a market area) than for a customer using Marriott’s booking channel. A prominent avenue for quality signaling is online travel agency (OTA) channels: platforms such as Expedia and Kayak rely heavily on sponsor advertising, and these efforts are another means by which firms can signal brand quality to customers.

Consumer learning

Consumer learning across similar brands occurs (1) at a point in time, such as when a new brand enters a market, and (2) over time via consumption and exposure to firm communications (Janakiraman, Sismeiro, and Dutta 2009). Thus, the first scenario can be purely cognitive: consumers form a quality perception, and existing brand quality inferences spill over to the new, similar brand entrant. In this context, online reviews from other guests may enable a customer to pool their experiences to infer hotel quality, potentially improving utility for specific brands. In contrast, the second scenario may involve a gradual process over time owing to consumers’ experiences. Learning can be particularly valuable with experience goods such as a hotel stay.

The net effect of positive and negative pathways on incumbent franchisee performance is not obvious. The new outlet may increase customer preference for franchisees and benefit their performance but, at the same time, heighten competition, which can put pressure on prices and decrease revenues. Thus, a model is needed to quantify the net effect on incumbent performance. While we attempt to rule out as many alternative explanations as possible, completely distinguishing among the positive pathway mechanisms—quality signaling, consumer learning, and brand awareness—remains a fertile ground for future research.

Model

We employ a structural model to examine customer response to encroachment in the presence of franchisees’ endogenous prices as well as subsequent outcomes, such as whether their sales increase or are cannibalized. Berry, Levinsohn, and Pakes (1995) provide a useful starting point in their model of an individual customer choosing a product with the greatest indirect utility out of a discrete set of differentiated goods that compete on price; this is a natural framework of static competition. We build on their model and account for a positive pathway effect on customer utility, customer heterogeneity, and price competition as a modification to the standard model.

Past research models the addition of a new franchise outlet via reduced form analyses using revenue data and estimates costs related to the firm’s decisions (e.g., Blevins, Khwaja, and Yang 2018; Hollenbeck 2017; Igami and Yang 2016; Suzuki 2013). In contrast, we micro-model customers’ heterogeneous demand response to encroachment while abstracting away from modeling the firm's dynamic entry. Further, we control for the firms’ entry decision using fixed effects and uncertainty in the exact timing of hotel entries. A more comprehensive approach would be to micro-model both heterogeneous demand response and a firm’s dynamic entry decision with endogenous prices accounting for the demand response to the number of same brand outlets, but we leave this to future research.

Customer Preference

Consider a geographic market m in time t, in which H (or

We further model

For the kth observed product characteristic

By grouping demand parameters into

The Supply Side

The franchisee sets its own hotel price (per night) without restrictions from the franchisor. Thus, we assume that hotel h in market m at time t decides on the room price to maximize the following profit function:

Data

Data Overview

We obtained a unique data set from one of the largest hotel franchisors in the world with multiple distinct brands, which provides substantial variation for investigating encroachment. More than 98% of the hotels are run by independent franchisees that set their own prices and pay a royalty fee to the chain. The royalty rate is assumed to be 10.61% of the gross franchisee revenue, which is the average for the focal chain in HVS Global Hospitality Services studies without much variation across brands. 3 Due to confidentiality concerns, we cannot disclose the number of brands in the focal chain. Suffice it to say that the individual brands are distinctive with unique logos, brand names, and service quality. The data include each hotel’s brand, price, monthly demand data, and so on.

Price and demand

We have monthly revenue and room demand of the franchisor’s hotels operated between September 2007 and March 2012 (55 months), from which we derive price (revenue per room night), consistent with previous work such as Chung and Kalnins (2001), Kalnins (2004), and Suzuki (2013). The data include information on the percentage of business stays at each hotel in a given month, providing some insight into customer heterogeneity. Publicly available data on industry cost shifters, such as the median hourly wages of hotel employees from the U.S. Bureau of Labor Statistics, serve as instrumental variables for price.

Market share and potential

Market share is defined as the demand (nights × rooms sold) divided by the monthly market potential. Market potential is defined as the maximum of the sum of a franchisee’s demand and the demand of its competitors (including other hotels in the chain and hotels that are not part of the focal chain) in a particular market over the data period; this value is constant across time periods. The competitor demand information was collected by the chain to ensure that a relevant, competitive set determines each franchisee’s market; this value is verified via mutual discussion with the franchisee. For example, suppose two franchisees are in a given market: franchisee 1 and franchisee 2. Also suppose that the demand for month t is 10 and 20 for the two hotels, respectively. Additionally, assume that the surveyed competitors’ demand for the period is 30 and 35, respectively. Market potential in month t is then max(franchisee 1 market potential, franchisee 2 market potential) = max(10 + 30 = 40, 20 + 35 = 55) = 55 hotel nights. We then again take the maximum of such market potential across time periods for the market. This information is likely more accurate than an industry association such as Smith Travel Research might provide.

The outside market share is defined as staying at hotels that are not part of the focal chain or not staying at any hotel. Web Appendix W3 provides further justification of the market potential being constant over time and discusses the outside option related to time trends.

Defining and cleaning the geographical market data

To properly assess encroachment and its impacts, our definition of a market needs to correctly capture the true local competition faced by each franchisee. One constraint is that the data do not include the address or location of each hotel. The location information provided is a geographic tract, which is defined by the combination of a metropolitan statistical area designation and location type (e.g., near an airport, highway or resort; suburban). For example, in the San Francisco-Oakland-Fremont metropolitan statistical area, the Oakland airport and San Francisco downtown area are provided as two separate tracts.

One problem is that some tracts may encompass multiple local markets. For example, three major highways crossing the state lie within the “Wyoming Interstate” tract. It would be erroneous to assume that all the hotels along these highways compete against one another (for a map of this area, see Web Appendix W4.1). Their inclusion could result in unreasonable parameter estimates, and more importantly, they do not reflect local franchisee competition, which is crucial to correctly specify Equation 5. We exclude rural metro/towns and suburban areas citing a similar argument. Therefore, we exclude such tracts (i.e., suburban, rural metro/town, and interstate locations) from estimation and retain tracts that are more likely to reflect a single market: airports, resorts, and urban areas. Absent more granularity and location information, we are unable to accord all the excluded tract data to the necessary unit of analysis. We also exclude markets with a single hotel of the focal chain during the entire period, as they may not be representative markets where our counterfactual simulations are relevant.

Web Appendix W4 details the process of tract exclusion and considers various empirical tests to justify their exclusion. Logit model results suggest that our main model results are robust to the inclusion of single hotel tracts 4 and tracts with missing variable information such as wages. Importantly, including suitably matched excluded suburban and rural metro locations that are likely small, well-defined markets yields similar results (see Web Appendix W4.4), which suggests that our findings are not limited to urban, airport, and resort locations but can generalize to suburban and rural metro/town locations.

The final estimation sample consists of 21,644 hotel-market-month observations of 447 unique hotels in 128 geographic markets across 34 states. Although the data set spans 55 months, we do not necessarily observe 55 months for every tract, depending on the chain’s presence in a market. Out of 447 franchisees, 127 entered the market during the data period. Forty-three percent of the entries (54 hotels) involved one or more instances of same brand encroachment, whereas the remainder did not. The data include 6,924 market-month observations.

Descriptive Statistics

The focal chain consists of a mix of multiple economy and luxury hotel brands; we are prohibited from revealing each brand’s market share and price point for reasons of confidentiality. Instead, we provide summary statistics of monthly demand, market share, mean hotel size and more in Table 2. The total market share of the chain is approximately 28%, which is generally consistent with its known overall market share in the industry. The average room price is $107.45 (SD = $39.05) per night. The large standard deviation is driven by the fact that the chain has multiple brands: the highest-end brand has a 9.19% market share with the average price of $192.79, whereas the lowest-end brand has a 6.84% market share with an average price of $73.68 per room per night.

Hotel Summary Statistics.

Notes: Summary statistics are calculated across 21,644 hotel-month observations.

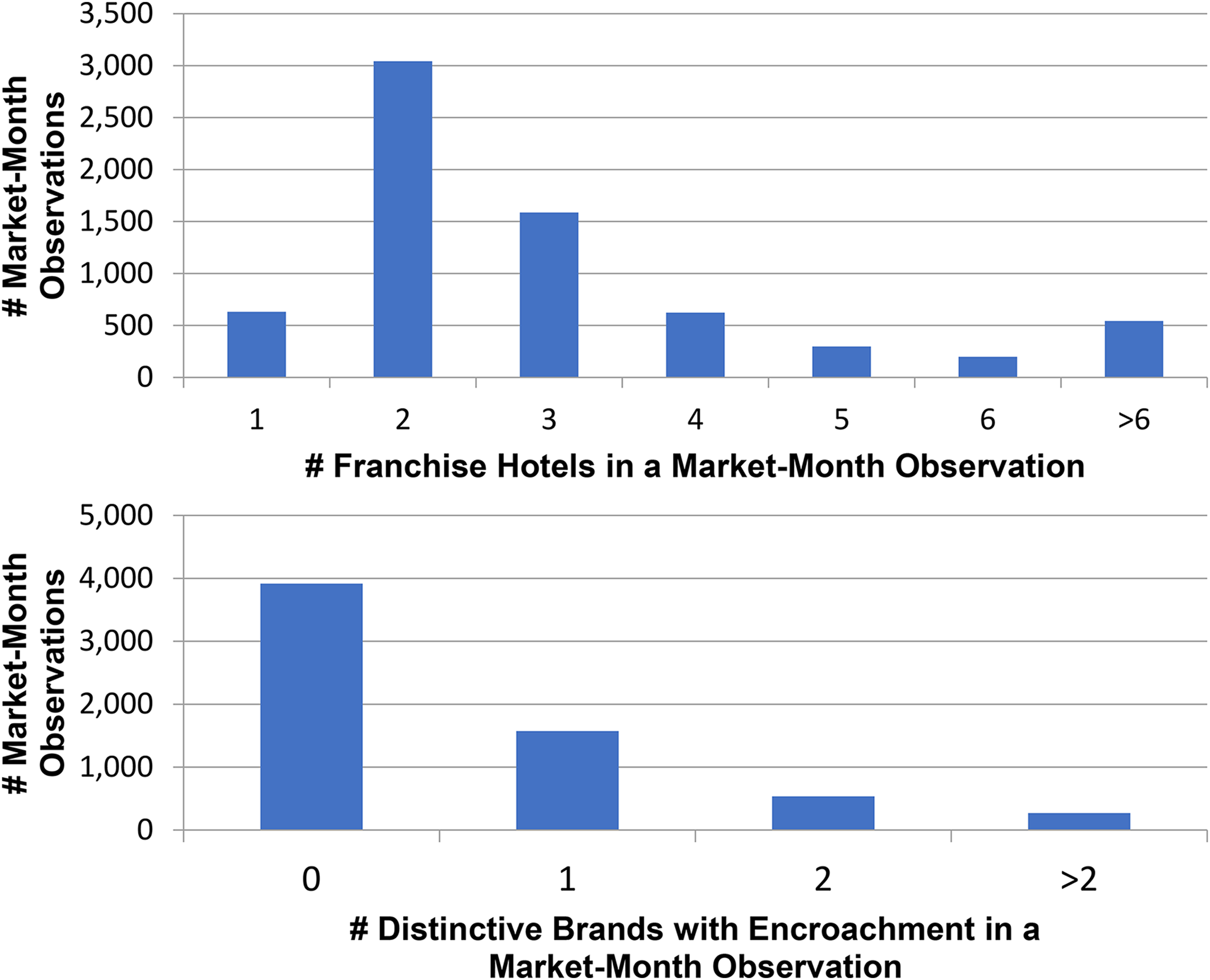

Based on the 6,924 market-month observations, the average number of hotels is 3.13 per market in a month (SD = 2.13). All brands have at least one market with same brand encroachment (.99 hotels on average per market). Figure 2 overviews the distribution of this chain’s hotels across market-month observations. The top graph shows that approximately 90% of market-month observations have multiple hotels, and the bottom graph indicates that approximately 38% of the market-month observations with multiple hotels have at least one brand with same brand encroachment. Some market-month observations even have two or more such brands.

Distribution of market-month observations.

Customer Heterogeneity, Moderators, and Supply-Side Data

Business stays account for 52% of hotel visits, and we use this proportion to estimate different demand response types. We employ multiple moderators to understand brand heterogeneity (e.g., brand type and age) and the number of cross brands (two brands in the chain that share a common moniker in the market). Overall, 21.8% (SD = 41.2%) of the 21,644 hotel-month observations represent luxury brand hotel observations, and 16.2% (SD = 36.9%) represent newer brands (introduced after 1997). The average number of cross brands is .76 hotel (SD = 1.14) across hotel-month observations. We use wage data from the U.S. Bureau of Labor Statistics: the mean of median wages of desk clerks (maids) was $10.20/hour ($9.66/hour) with a standard deviation of $1.38/hour ($1.52/hour) during the data period.

Estimation

Berry, Levinsohn, and Pakes (1995) and Identification

The first component of the estimation matches the predicted market shares

We then construct moment conditions by assuming that demand shock

Another endogeneity concern involves the positive pathway variable as defined by the number of same-brand hotels in a market. Part of

While individual hotel dummies control for endogeneity from time-consistent demand heterogeneity, concerns remain about market-specific time-varying unobservables. Because the positive pathway is proxied by the number of same-brand hotels and its change in a market, if such unobserved heterogeneity is correlated with different hotel entry patterns, it can ultimately bias the estimate (Manuszak and Moul 2008; Pancras, Sriram, and Kumar 2012). We address this issue in several ways. First, we include fixed effects specified at the market × six-month level to flexibly control for the unobservables that may influence hotel entry and, thus, the change in the number of same-brand hotels. The fixed effects also account for time-changing outside options to some degree by allowing them to have different intercepts.

Second, we exploit the institutional knowledge of the industry regarding the timing of hotel entry. This entry decision may be decided at large time intervals (e.g., hotel entry planned in the second half of 2015); interviews with chain executives reveal that the exact timing of entry is difficult to predict due to the nature of the commercial real estate development process. This timing varies within a six-month window, depending on many unpredictable external forces, such as financing commercial real estate mortgages, passing inspections, and obtaining permits from local government. Therefore, we assume that the variation in the number of same hotel brands is exogenous within a six-month window.

This approach is consistent with the precedent of Ching (2010), who similarly assumes exogenous entry timing of generic drugs due to unpredictable FDA approval processes. We first checked the validity of this assumption by showing that the month in the six-month window cannot predict entry (see Web Appendix W2.2). We checked robustness of the results with additional control variables (see Web Appendix W2.3). Additionally, we examine incumbents’ demand and price surrounding the entries of same and different brands and find that both increase only for same brands post entry (Web Appendices W6 and W7, respectively). These results corroborate our modeling approach that customer utility or willingness to pay increases only in the case of same brand encroachment.

Since we only observe hotels from one chain, it is difficult to completely rule out the possibility that the entry timing in this chain may coincide with entry/exit of unobserved nonchain hotels. Two factors mitigate this concern. First, the uncertainty in the commercial real estate development process equally applies to unobserved hotels. Thus, it is unlikely that their entry/exit patterns will systematically coincide with our chain’s entry timing within the six-month window and result in an overestimate of our results. 6 Second, we do not observe the full range of competitive options, which can lead to an attenuation bias via measurement error (i.e., our estimates may be conservative; for a similar setting in the airline industry, see Orhun and Guo 2018). Finally, we consider other endogeneity concerns (e.g., the granularity of our fixed effects, independent hotels rebranding as new hotels in our data) in Web Appendix W8.1.

Other Details of Estimation

The estimation strategy is based on the generalized method of moments estimation combined with micro moments (e.g., Berry, Levinsohn, and Pakes 1995 2004) to estimate customers’ heterogeneous demand response in terms of the percentage of business stays. Supply moments are estimated to evaluate the degree to which an economies of scale explanation might be operative after controlling for hotel and time-varying market factors. Technical details of the estimation are included in Web Appendix W8.

Results

Logit Results

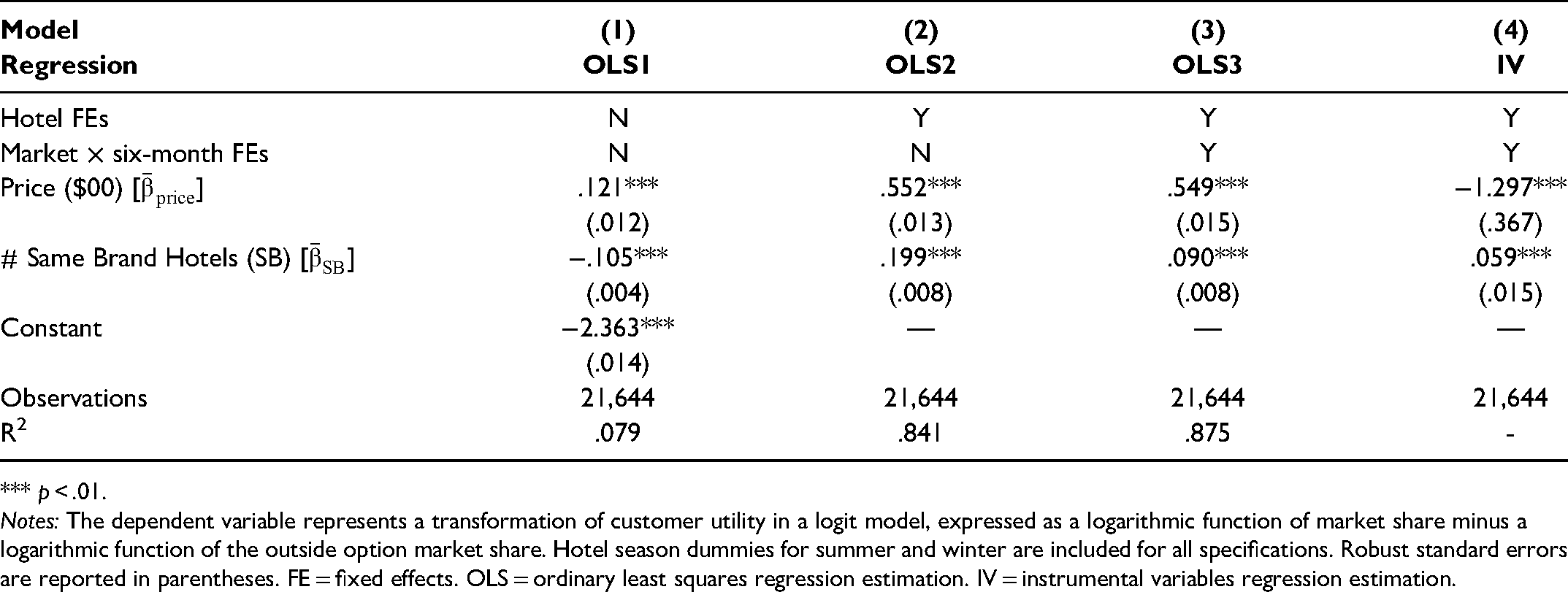

We estimate a homogeneous logit demand model (

Logit Model Results.

*** p < .01.

Notes: The dependent variable represents a transformation of customer utility in a logit model, expressed as a logarithmic function of market share minus a logarithmic function of the outside option market share. Hotel season dummies for summer and winter are included for all specifications. Robust standard errors are reported in parentheses. FE = fixed effects. OLS = ordinary least squares regression estimation. IV = instrumental variables regression estimation.

The results of the logit regression using price and SB in Model 1 imply that customers prefer higher prices and dislike having more of the same-brand hotels in a market, as SB is negative and significant. When we include hotel fixed effects in Model 2, a positive pathway emerges, and the number of same-brand hotels increases customer utility, suggesting that demand is positively associated with same brand encroachment. The price coefficient remains positive and statistically significant, an unconventional finding. Including additional market × six-month fixed effects in Model 3 substantially reduces the SB estimate (from .199 to .09, although still significant at 1%), underscoring the value of controlling for time-varying market-specific unobservables.

However, after instrumenting price with the average size of the focal chain’s other hotels and that of different brand hotels in the market, the price coefficient in Model 4 is now negative (−1.297, p < .01); this suggests that an instrumental variable approach results in more reasonable results (i.e., hotel demand decreases as price increases). The first-stage regression results show that the instruments have enough explanatory power with the first-stage F-statistics of 112.9. Collectively, the logit results suggest consumers respond positively to same brand encroachment—a positive pathway that can create revenue benefits among same brand franchisees if the negative pathway or market competition is not severe.

The results are robust to different functional forms of SB, such as a log function of the same-brand hotels (see Web Appendix W2.1). In comparison to the log specification, the linear function of same brand hotels results in a better fit (

Full Model Parameter Estimates

Demand-side parameters

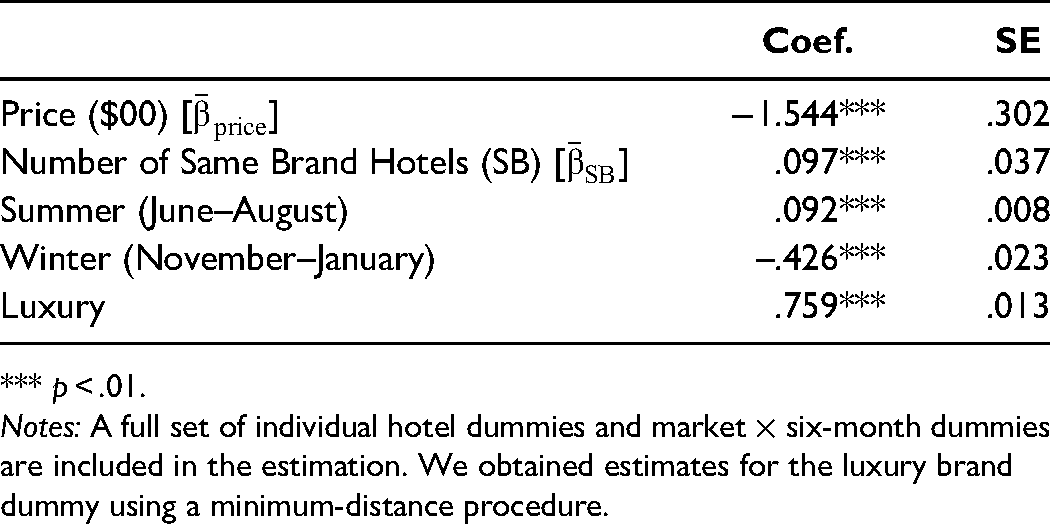

We now estimate the full model with heterogeneous customer preferences (

Demand Macro Parameter Estimates in Equation 3.

*** p < .01.

Notes: A full set of individual hotel dummies and market × six-month dummies are included in the estimation. We obtained estimates for the luxury brand dummy using a minimum-distance procedure.

The mean price parameter estimate is negative and significant (−1.544, p < .01), implying that customers have a preference for lower prices. Combined with the price heterogeneity estimates in Table 5, this results in an average own-price elasticity of −1.33. Seasonality has a significantly negative (positive) effect for winter (summer), which suggests that demand peaks in summer. We draw additional insights on customer taste by running a generalized least squares regression (Chamberlain 1982; Nevo 2000) in which we regress hotel dummy estimates on a luxury brand dummy (=0 if economy brand). As expected, customers prefer luxury over economy hotels (.759, p < .01). Parameter estimates for all dummy variables (

Customer Heterogeneity Parameter Estimates in Equation 3.

Notes: *** p < .01.

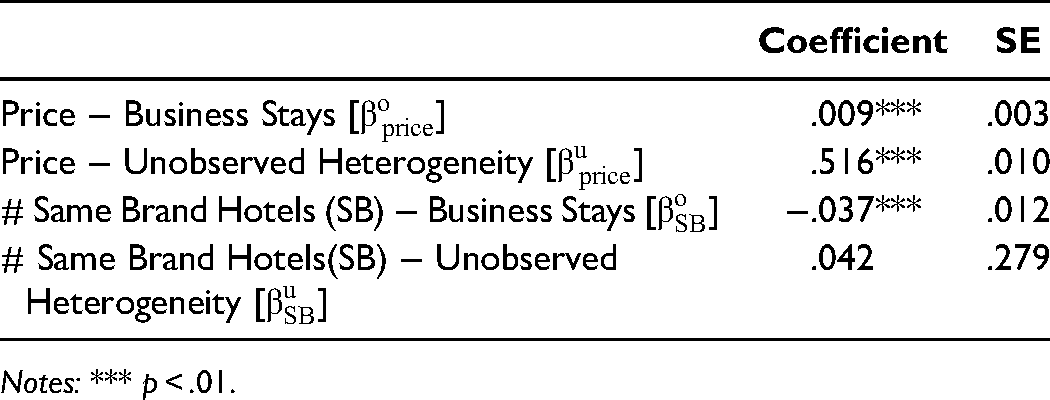

Customer heterogeneity coefficients (

Supply-side parameters

The estimation of the supply side (Equation 8) shows that the effect of SB on marginal costs after controlling for hotel and market-time fixed effects is slightly negative but not significant (–.008, p = .233), suggesting a lack of economies of scale (for detailed estimation results, see Web Appendix W9). An alternative covariate is the number of same-brand hotels in the nation in a given time period if the level of economies of scale is at the national as opposed to local markets. Our analysis shows that the economic significance of such an effect is very close to zero. The estimated marginal cost is $27.11 per room night, which approximates the marginal cost found in the hotel industry (e.g., Hollenbeck 2017).

Economic Value of a Positive Pathway Effect

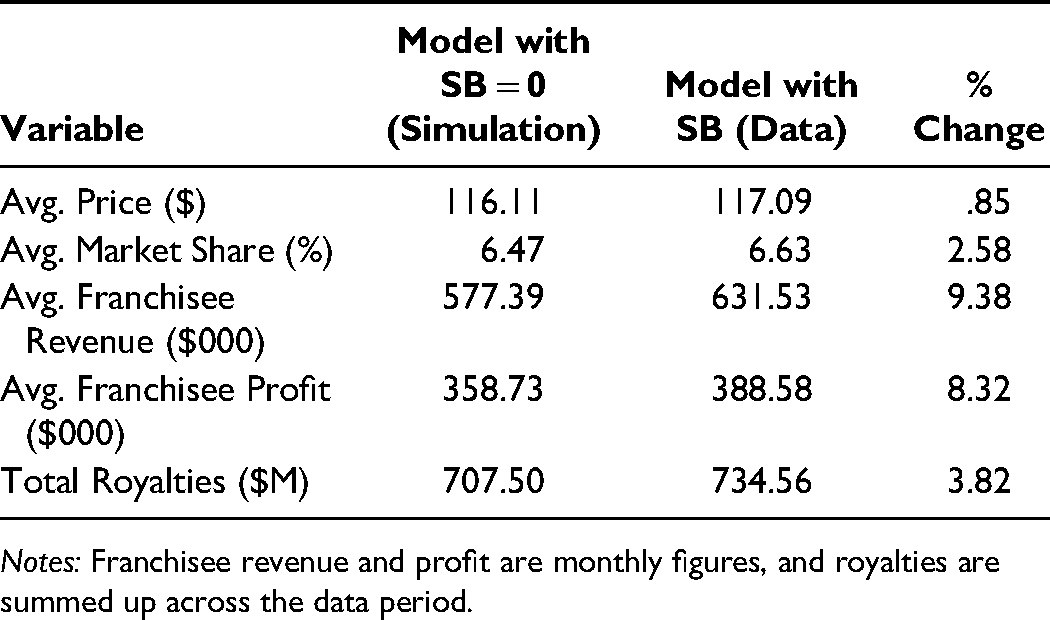

We can estimate the economic value of this effect by comparing the observed data with a scenario in which the SB parameter is set to zero; conceptually, this approximates a scenario in which consumers are not responsive to an increase in the number of same brand hotel outlets (i.e., no positive pathway effect). Note that in this scenario, franchisees may set different optimal prices. The first-order conditions defined in Equation 6 allows us to recalculate the new optimal price. We then compare the scenario’s outcome against our data in Table 6. The results suggest that a positive pathway contributes to a slight increase in average price and accounts for approximately 9.4% (8.3%) of the average hotel franchisee monthly revenue (profit) in the focal market. Also, 4% of the $707.5 million gross royalty income is estimated to result from the positive pathway effect. Therefore, the positive pathway is not only statistically significant, but also economically relevant regarding the franchisee’s economic welfare.

Positive Pathway Economic Value.

Notes: Franchisee revenue and profit are monthly figures, and royalties are summed up across the data period.

The Impact of Brand Characteristics on Encroachment Outcomes

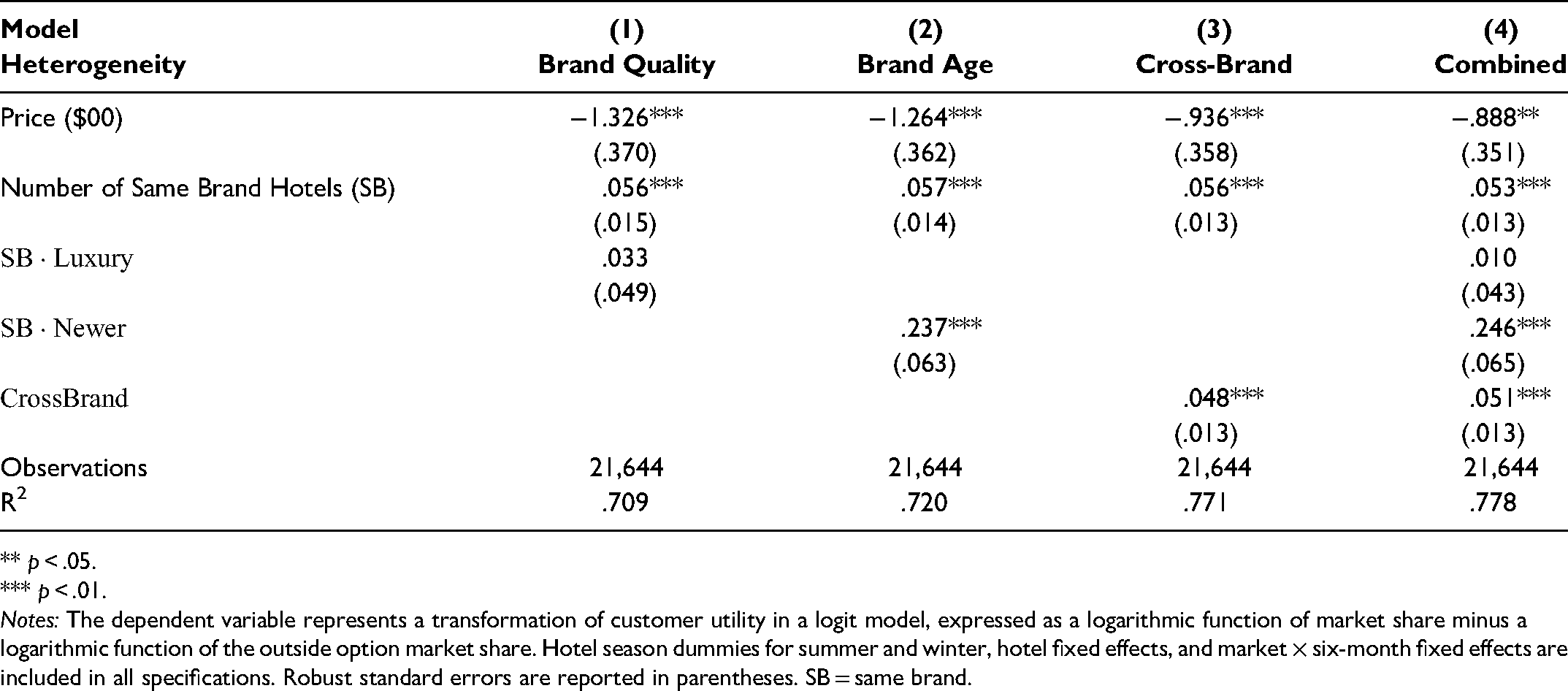

In this section, we investigate whether the positive pathway varies across a range of brand dimensions such as quality (luxury vs. economy brands), brand age (more vs. less established brands), and cross-brands (brands with an overlapping moniker).

Brand quality

In Model 1 of Table 7, we reestimate the logit model (Model 4 in Table 3) with an interaction term between

Heterogeneous Effects of the Number of Same Brand Hotels.

** p < .05.

*** p < .01.

Notes: The dependent variable represents a transformation of customer utility in a logit model, expressed as a logarithmic function of market share minus a logarithmic function of the outside option market share. Hotel season dummies for summer and winter, hotel fixed effects, and market × six-month fixed effects are included in all specifications. Robust standard errors are reported in parentheses. SB = same brand.

Brand age

Prior to 1992, the chain was composed of 57% of the chain’s brands relative to the data period. Three or more brands were added to the chain’s portfolio after 1997, and then the full set of brands developed together. We define a dummy variable

Cross-brands

We consider the possibility of additional positive pathways through cross-branding, in which two outlets share a common aspect of the brand name. For example, a “Hyatt Place” hotel may benefit whenever another hotel outlet incorporating “Hyatt” (e.g., “Hyatt House”) is added to the market. Among the chain’s brands, two have similar names (e.g., brands A and AB): brand A’s moniker is one word, and brand AB has two words starting with brand A. The second word (B) does not directly signal superior overall quality but refers instead to the speed of service. If positive pathways are generated via the number of outlets with same brand monikers, we may observe a positive pathway not only between two outlets of the A brand, but also between A and AB brands. We assess this possibility by adding

Placebo test

To further assess robustness, we conduct a placebo test to see if a cross-brand effect is no longer observed for the count of the number of hotel brands with dissimilar names. For instance, in place of brand A’s

Booking Channel Analyses

Booking channels offer varying forms of product comparison and purchase convenience in the customer’s purchase process. We consider positive pathway effects across booking channels that support varying degrees of purchase intent and brand loyalty. One advantage of OTA channels such as Expedia or Orbitz is that they allow customers to compare across brands and options in terms of price, dates, and locations, which may be particularly valuable to customers who are seeking a specific type of deal and are open to a range of brands. OTA customers may be more likely to make occasional purchases and may not be brand loyal. In contrast, customers who book through a chain’s official website are likely to have a preference for the brand and may not need an array of brand options for their purchase; they may be brand loyal or repeat customers. A positive pathway for demand may be less likely for this group due to saturation or ceiling effects, relative to OTA channel customers. Put differently, OTA consumers are more likely to benefit from a positive pathway, and this impact should be observable via heightened demand as encroachment increases.

We investigate this possibility by estimating a series of ordinary least squares (OLS) regressions for different online channel demand over brief windows (±3 months) around hotel entries for incumbent hotels, excluding the entered hotels. Details and results of the estimation are included in Web Appendix W11. We find that the incumbent’s demand (9.946, p < .10) and the proportion of demand (.013, p < .05) through OTAs increase relative to other brands when a same-brand hotel enters the market. However, there is no significant corresponding effect through the chain’s website channel. These significant interaction terms support our contention that same brand encroachment spurs a positive pathway effect and increases customer preference in OTA channels. Thus, incumbents benefit more from purchases in the OTA channel than the chain’s channels. We evaluated the price response to determine whether a demand increase in the OTA channel decreases the overall price (hotel revenue per room). We find an increase in price for same brand incumbents post-entry, suggesting higher willingness to pay in customer utility (see Web Appendix W7 for further details).

We conduct similar analyses with offline booking channels associated with the chain, namely, traditional travel agents and call centers, but did not find any significant results. We conjecture that because travel agents are experienced in hotel bookings, they are less influenced by the addition of same brands. In addition, customers who book through the chain’s call centers, like those who book through the chain’s website, may have brand loyalty or preference that would make them less sensitive (i.e., a ceiling effect) to same brand encroachment.

Explanations of Observed Positive Pathways

We next consider various explanations for the observed positive pathways. Although we are not able to unequivocally isolate their effects, a careful consideration of the empirical evidence can suggest which explanations might be operative.

Potential Explanations

Brand awareness and quality signaling

Our results in prior sections suggest that brand quality signaling and awareness mechanisms are likely operative. Evidence of an additional positive pathway on customer utility for cross-brands and a moderating effect of newer brand outlets further corroborates this possibility. Additionally, the demand patterns show that consumers who purchase through the chain’s booking channels (as opposed to OTA channels) are less likely to reflect a positive pathway effect, possibly due to brand loyalty and familiarity. Online advertising in OTA channels may also result in greater exposure of same brand hotels, which would increase brand awareness and quality signaling. This is consistent with our finding in Table W22.

Consumer learning

We have suggested that a possible positive pathway might arise if consumers learn from the presence of multiple brand outlets. Although our hotel-level data prohibit us from isolating this effect at the customer level, we explore this potential mechanism via an online experiment. If learning improves as the number of hotels in a market (i.e., brand exposure) increases, consumers may learn about hotel quality more accurately (i.e., correct quality association of the brand with more outlets), absent more information such as budget constraints, pricing, location, and so on. Better learning would thus be evidenced by greater accuracy in markets with more hotels regardless of the hotel quality level.

We test this possibility using a design in which we manipulate hotel quality (high vs. low) and number of hotels in a market (two vs. five) in a 2 × 2 between-subjects design. The dependent variable is the recall accuracy of the focal hotel brand quality. If the consumer learning mechanism holds, one would expect that recall inaccuracy would be higher in the two-location condition than the five-location condition. Web Appendix W12 contains more details regarding data collection, stimuli, and analyses.

The results are supportive: inaccuracy is significantly higher in the two-location than the five-location conditions across both high- and low-quality hotels. When there are fewer hotel outlets, the inaccuracy is mainly driven by the participants’ reported ratings gravitating toward the condition mean, consistent with an explanation of not learning well. As a result, for higher-than-average hotel quality (i.e., as in our data), more same-brand hotels are associated with higher perceived quality. Collectively, these results provide evidence for the possibility that more outlets can increase preference via consumer learning, supporting a positive pathway effect.

More broadly, our results suggest that customer utility and market demand can be positively impacted by the addition of a new outlet when the addition is of the same brand, a newer brand, a cross brand, or purchased in an OTA channel.

Unlikely Explanations

Scarcity

If consumers prefer scarce boutique hotels (e.g., Hotel Indigo) over more standard hotel offerings with wide market coverage (e.g., Hilton Garden Inn), then the existence of multiple establishments of the same brand would decrease utility for the encroached brands. Research on luxury goods consumption is consistent in this regard, showing that scarcity and exclusivity creates value for customers (Stegemann 2006; Wiedmann, Hennigs, and Siebels 2009). However, our results do not support differing pathway effects for luxury hotel brands compared with economy brands, suggesting that scarcity is an unlikely explanation.

Television advertising

Television advertising is difficult to target or tie to a specific outlet opening, given the difficulty of predicting a hotel opening even within a six-month window. Unlike fast food customers, hotel customers are not necessarily local, which can complicate advertising targeting. Therefore, we consider television advertising unlikely in our context.

Other supply-side explanations

Although our focus has been on demand-side mechanisms for positive pathways, several supply-side mechanisms have often been discussed in the franchise literature as well, such as co-ownership, cost agglomeration, economies of scale, and capacity constraints. While these mechanisms are useful, they cannot adequately explain the positive pathway effects on customer utility or are irrelevant in our research context, as explained in Web Appendix W13.

Counterfactual Simulations

A key advantage of a structural modeling approach, relative to regression analyses, is the ability to conduct counterfactual simulations. In this section, we explore two counterfactual simulations. The first simulates the impact of encroachment reduction, which has implications for shaping policy and represents a possible action for conflict reduction. It illustrates how removal of an encroaching outlet impacts the remaining hotels’ optimal pricing and customers’ subsequent hotel choice. The second counterfactual explores a key boundary condition of intrabrand competition: markets with varying same brand density. These counterfactuals have both practical and theoretical implications, and they allow us to explicitly illustrate the role of positive and negative pathways on incumbent performance.

Counterfactual 1: Encroachment Reduction and Incumbent Performance

We simulate encroachment reduction by removing one same brand franchisee and allowing the remaining franchisees to reoptimize their prices through Equations 6 and 8. We compare this simulated market outcome to the current model estimates and quantify the net aggregate effect on the remaining franchisees’ performance. Because we do not have data on hotels outside the chain, our results assume that such hotels would not respond to the simulated policy changes.

We consider all combinations of the removal of a single same brand hotel using the following process: first, in each market, one same brand hotel is removed. If there are three brand A hotels, then one is randomly selected (A1) for removal. Second, the remaining hotels (A2 and A3) reoptimize their prices, according to Equations 6 and 8. Third, market outcomes—including franchisee price, demand, revenues, and profits, as well as franchisor revenues and profits—are then recalculated. Finally, the foregoing three steps are repeated for each remaining hotel (A2 and A3) and across all markets.

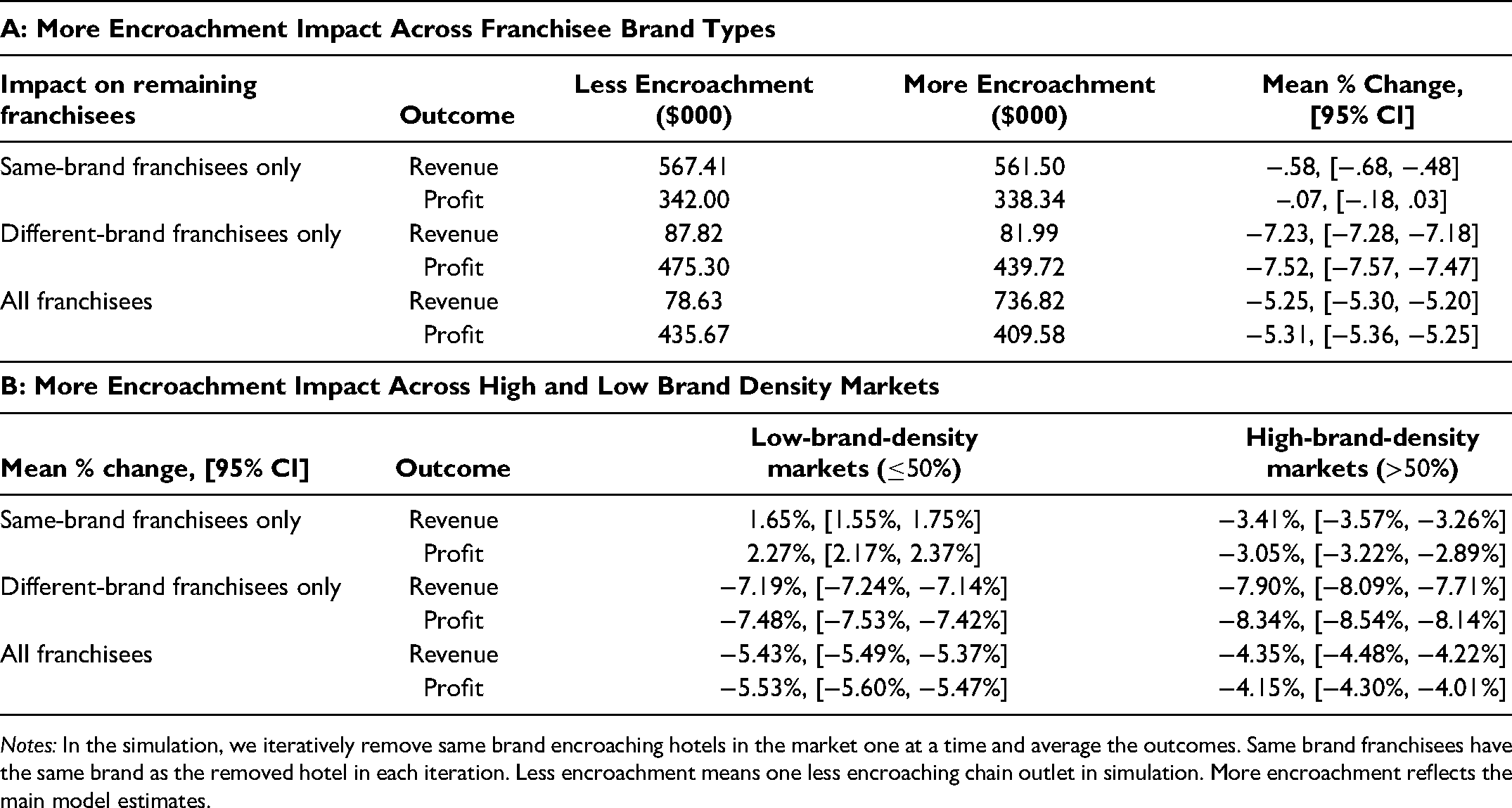

We further decompose the impact of encroachment reduction by considering its effects on same and different brand outlets. Table 8, Panel A, reflects the performance impact on revenues and profits with one fewer same brand outlet. The first column reflects the simulation results (i.e., less encroachment), the second column reflects our model estimates (i.e., more encroachment), the third column reflects the mean percentage change between the foregoing, and the fourth column reports 95% confidence intervals. The overall impact of more encroachment results in an average revenue and profit loss of 5.3% (i.e., −$43,810 in revenue and −$26,090 in profit per month) for all incumbents. This result is consistent with the negative pathway findings in the empirical literature. This value is meaningful, as the “impact threshold,” or the minimum drop in revenue that must be observed for a franchisee to bring suit for encroachment in Iowa, is 5% (Iowa Code 523 H, 1995).

Decomposing this further for same- and different-brand incumbents, we find that the effect is even greater on different-brand franchisees in the franchise system, with revenues and profits declining significantly by 7%–8% (i.e., −$59,834 in revenue and −$35,586 in profit per month). In contrast, more encroachment has little to no impact on same brand franchisees: although revenues decrease significantly (i.e., −$5,914 per month or −.58%, 95% CI [−.68%, −.48%]), the impact on profits is not statistically significant (−$3,659 per month or −.07%, 95% CI [−.18%, .03%]). Given that franchisors earn a royalty rate on revenues and franchisees are profit maximizing, these effects are economically meaningful. The results suggest that while a negative pathway dominates for different brands, a positive pathway seems to mostly offset a negative pathway for same brands (i.e., mitigation). This represents a critical contribution to our understanding of encroachment.

Counterfactual 2: Brand Density Market Conditions

Another dimension to consider is the number of existing brands, or a brand’s “density,” in a market. The fewer the number of same brand outlets, the lower the brand’s density, and potentially, the weaker the negative pathway from adding yet another outlet. Positive pathways might then dominate negative pathways in the case of same brands, potentially improving franchisee performance. In contrast, in markets in which brand density is high, firms have more competition for customers; thus, we are likely to observe that negative pathway effects prevail.

Suppose there are two markets that vary in terms of the number of A hotels:

Low-density market (“Market L”) consists of two A hotels, one B hotel, one C hotel, and one D hotel. In this market, we can calculate a brand density ratio for A hotels to be 40%. High-density market (“Market H”) contains three A hotels, and one B hotel, and one C hotel. In this market, the same-brand density ratio for A hotels would be 60%.

If one A hotel is removed, we would expect its impact on the remaining A hotels to be smaller in Market H because the marginal positive pathway is likely lower. We divide the data set into low (≤50%) and high (>50%) same brand density ratio markets.

7

Note that the brand density ratio reflects the number of same-brand hotels over the franchisor’s total number of hotels in the market. We provide further evidence that the brand density ratio is a good proxy for the same brand concentration with respect to all hotels, including hotels that are not part of the chain, in Web Appendix W14.1.

Table 8, Panel B, displays the performance impact. Consistent with a negative pathway mechanism, encroachment generally hurts franchisees, reducing average revenue and profits by 4%–6% regardless of the market’s brand density. This performance decrement increases for the remaining different brand franchisees, resulting in a reduction in revenue and profits of 7%–8% and replicating results from the previous counterfactual. In contrast, the performance decrement is minimized and can even be positive for same brand franchisees. In high-density markets, they experience only a 3% reduction in performance (−$18,954 in revenue and −$12,011 in profit per franchisee per month). In low-density markets, incumbent performance improves by approximately 2% ($4,349 in revenue and $2,914 in profit per franchisee per month).

Counterfactual Simulations of More Encroachment on Franchisee Monthly Performance.

Notes: In the simulation, we iteratively remove same brand encroaching hotels in the market one at a time and average the outcomes. Same brand franchisees have the same brand as the removed hotel in each iteration. Less encroachment means one less encroaching chain outlet in simulation. More encroachment reflects the main model estimates.

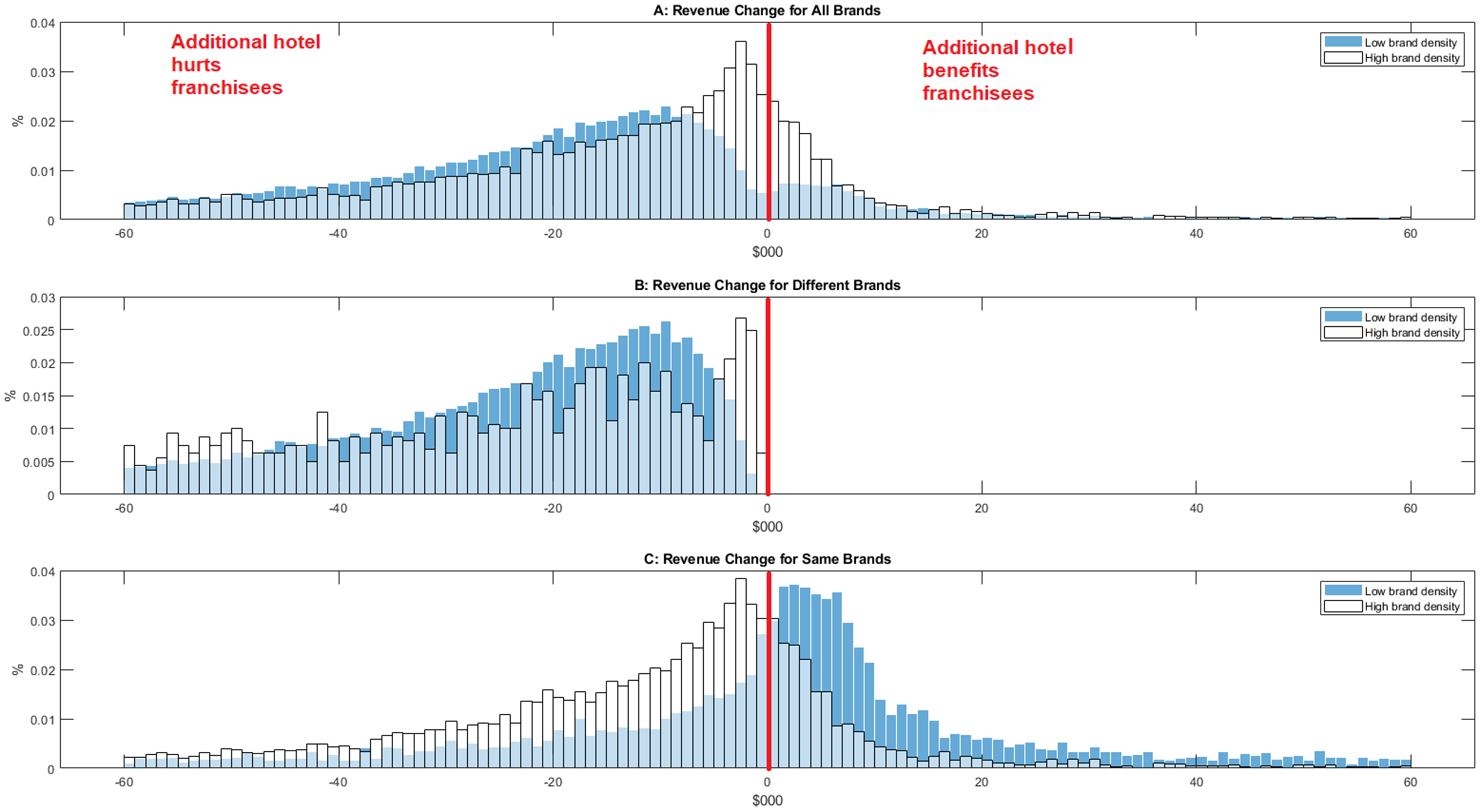

Figure 3 sheds further light on these point estimates by illustrating the distributions of franchisees’ monthly revenue change: the midpoint of the graphs reflect no change, while areas to the right reflect the net outcome of a positive pathway dominating a negative pathway, reflected in higher franchisee revenues. Panel A of Figure 3 reflects the relative distributions for the first two cells of the last rows in Panel B. It is worth noting that the brand-density markets’ plot is bimodal. We explore this further in Figure 3, Panels B and C.

Distribution of incumbent revenue change across high- and low-brand-density markets.

Figure 3, Panel B, shows revenue change from the perspective of same brand outlets (i.e., the first two rows in Table 8, Panel B). In low-brand-density markets, a clear positive pathway impact is evident for same-brand franchisees; this plot is similar to the positive pathway impact for low-brand-density markets in Figure 3, Panel A. This distribution shift suggests that on average, 70% of franchisees benefit from having a same brand hotel added in their vicinity. With high brand density markets, revenues are generally lower, consistent with a negative pathway dominating; however, even under these conditions there is a sizable portion of revenue for which positive pathways dominate.

Figure 3, Panel C, illustrates franchisee revenues decrease from the perspective of different brand outlets (i.e., the middle rows in Table 8, Panel B). This plot suggests that the addition of a different brand hotel hurts franchisee revenues regardless of market brand density. It also suggests that there are no positive pathway gains for outlets whose brand is different from the new outlet—only a negative pathway.

Collectively, the counterfactual analyses and associated plots provide a more nuanced understanding of the impact and market conditions under which positive and negative pathways to franchisee performance occur. Web Appendix W14.2 presents histograms of selected market revenues pre- and post-simulation.

Conclusions and Implications

Substantive Implications

A chief advantage of franchising organizations is rapid growth in the number of outlets and service availability. This growth may inevitably result in more same brand franchisees being located close to one another. Prior to our research, encroachment was only considered in terms of negative pathways. However, our work provides important insights into the circumstances under which this might not be the case. Adding a same brand outlet can in fact lead to positive pathways via customer utility enhancement, which can subsequently mitigate negative pathways and even improve franchisee revenue and profits for same brand outlets in low-brand-density markets.

The reduced negative performance impact of encroachment on same brand franchisees suggests that encroachment may not be as universally harmful as once thought. Moreover, the prevailing positive pathway increasing both revenues and profits in low-brand-density areas suggests that firms should seek to encroach more in those areas (i.e., strength in numbers). To this end, we find that newer brands benefit more, holding promise for market entry strategies, as do cross brand locations and OTA bookings. Our work calls for managers and researchers to rework their view of encroachment to recognize that it may not be unilaterally negative.

Beyond the hotel industry, if encroachment involves mostly negative pathways dominating positive pathways, one may not observe any increase in performance related to same brands. Alternatively, if products are well differentiated such that negative pathways are relatively small, newer brand franchisees may achieve improved performance with same brand encroachment. On the other hand, different brand encroachment does not involve positive pathways, so we expect it to be seen as an adverse event to incumbents in other industries as well.

Marketing implications

Encroachment has been a contentious issue in the marketplace, but our research is the first to identify potential benefits and positive pathways from the addition of a same brand via a customer-centric viewpoint. Our ability to trace these pathways to improved customer utility underscores the power of the customer in a research area that has mostly focused on the franchisor’s view of the market. Encroachment can be positive through customer utility, and we demonstrate where and when these benefits occur.

Being the first to distinguish the performance impact for same- versus different-brand outlets in a franchise system adds nuance to our understanding of how franchise systems should go to market and how brand characteristics play into it. Specifically, franchisors might prioritize markets with low same brand density for more locations. In this regard, we observe that a positive pathway effect can increase franchisee revenues by 1.7%, reflecting a 2.3% improvement in profits. This illustrates the potential “sunny side” of this controversial phenomenon. Importantly, franchisors can be strategic about when and where to reduce or expand locations, particularly as it pertains to franchisee conflict or relationship improvement.

Regarding channel conflict, franchisors face a fundamental trade-off in achieving their expansion goals; prevailing in a particular conflict, such as encroachment, can come at the cost of less location expansion. Our work identifies an alternate path, suggesting that additional same brand locations can result in a win-win outcome in low-brand-density markets and with various brand characteristics.

It is also worth noting that franchise contract specifics may make it difficult to generalize our results. For instance, encroachment is irrelevant in franchise chains that guarantee exclusive territories. Also, the type of franchising may affect generalizability. While many new franchises are business format franchising (i.e., franchisees pay running royalty payments to the franchisor as a percentage of sales), the traditional franchising model is still prevalent in sectors such as automobile dealerships and gasoline stations (Blair and Lafontaine 2005). In traditional formats, the franchisor sells the product to franchisees with the right to serve a certain geographic area instead of collecting ongoing royalties. Regardless of the format differences or other unique aspects of the hotel industry such as capacity constraints, we may yet observe positive pathways if brand awareness and quality signaling are relevant. We leave these issues for future research to verify.

From a consumer welfare perspective, our research sheds a new light on how to consider hotel choice offerings across a range of markets. Our findings of additional positive pathways (e.g., cross brands, newer brands, purchase channel types) to hotel performance suggest that such offerings might enhance consumer welfare in new markets and in the creation of valued product offerings. These insights are important for policies such as those described in The Network Expansion Handbook, which is developed by the International Franchise Association’s Franchise Relations Committee to assist in establishing codes of conduct and setting expectations and compliance for encroachment practices.

Policy implications

Our counterfactual simulations help inform the fractious efforts around franchise regulation. Although franchisors may allow exclusive territories to individual franchisees, established franchisors often maintain legal rights in the final encroachment decision (for more detailed discussion, see Kalnins 2004). However, the threat of litigation motivates franchisors to maintain goodwill. Our findings of prevailing positive pathways in low-brand-density markets and the substantially reduced negative pathway impact on same-brand incumbents indicate customer utility gains from having more same brand hotels. Future research might consider how a ban on same-brand encroachment, such as the Iowa Franchise Act of 1992, would affect customers.

Theoretical Implications

Our finding that encroachment can be economically beneficial for same brand franchisees contributes to the literature, which has historically shown the opposite. Incorporating a consumer perspective represents a substantial departure from the dominant approach, which has historically focused on the franchisor’s revenue and market share. Moreover, the customer’s perspective enables us to illuminate the value of encroachment in terms of increased customer utility and demand for same brand franchisees. Although we find customer heterogeneity differences for hotel industry-specific factors such as business stays versus leisure stays, generalizability to other industries remains an area for future investigation. As an example, considering that hotel franchisees rely on out-of-town customers more than a fast food franchisee might, pathways for these two industries may differ.

We expand the scope of research in the marketing literature on franchise management, which has mostly focused on issues of governance and enforcement (Antia, Mani, and Wathne 2017; Kashyap et al. 2012), or organizational forms such as the proportion of a chain that is franchisor versus franchisee owned (Antia, Zheng, and Frazier 2013). Our research highlights the phenomenon of encroachment as a substantive direction for future research in its own right.

Our work contributes to the growing body of work on firm entry. Similar to Datta and Sudhir (2011) and Vitorino (2012), we allow both negative and positive outcomes from entry, albeit in a franchising context. Their results support the positive effects that arise from economy-of-scale gains on the supply side or a concentration of product category brand locations. We, in contrast, focus on the effect of multiple same brand outlets on customer demand as opposed to the use of multiple-store formats or category effects.

Generalizing our findings beyond the hotel industry depends on industry-specific factors that may affect pathways. 8 For example, the magnitude of negative pathways may be different in other industries. One measure of this negative pathway is own-price elasticity. For example, Pancras, Sriram, and Kumar (2012) find an elasticity of −2.09 among fast food franchisees, and Kim (2021) finds −2.82 among auto radiator distribution franchisees. Our price elasticity of −1.33 suggests weaker negative pathways relative to these industries.

The findings also suggest that one would expect stronger positive pathways with newer brands. If an industry mostly consists of long-established brands with a high degree of familiarity, positive pathways may be small or difficult to measure.

Future inquiries could consider these possibilities as well as identify additional moderating factors in which positive pathways might be operative. Historical or other secondary data analyses would assist in documenting the real financial and relational impact of encroachment for same brand outlets in low-brand-density markets. More broadly, such results could be investigated across other franchised service industries.

Limitations and Future Research

We acknowledge several considerations in the summation of our results. First, the data limitation on location information of hotels led us to mainly focus on well-defined markets such as downtown areas, airports, and resort towns to isolate encroachment effects. Can we observe the effect of encroachment in other markets? Including suburban and rural metro locations that are likely small, well-defined market yields similar results (Web Appendix W4.5), suggesting that our findings are not limited to downtown, airport, and resort locations. Further information on hotel location data in the excluded markets would allow us to break them into local markets for inclusion in our analyses.

Second, while consumer learning remains a possible explanation for our findings, our static model is unable to fully capture potential dynamics. A dynamic model based on individual choice data and experience would be required to determine that learning has occurred. We leave this as an avenue for future research.

Finally, from a modeling perspective, while our results are robust with more granular fixed effects, our market × time fixed effects may not fully capture all unobserved demand shocks, which can bias results. Individual-level customer panel data would have been useful for determining which demand side explanations—consumer learning, brand awareness, or quality signaling—dominate. Although our study focuses on the presence of same brand hotels, the role of online advertising and consumer search behavior would further shed light on this topic. These topics remain fruitful directions for the future.

Footnotes

Acknowledgments

We thank our industry contact and the firm that provided us with the data, our review team for their feedback and suggestions, Ryan Hamilton, Arturs Kalnins, Francine La Fontaine, Steve Shugan, Raphael Thomadsen, and Miguel Villas-Boas. We also thank participants and discussants for their comments and suggestions at the Marketing Science Conference, Bass FORMS Conference at the University of Texas at Dallas, McGill International Conference on Marketing, Georgia Research Symposium, Institute for the Study of Business Markets Academic Conference, and marketing seminars at the University of Rochester, the University of Colorado at Boulder, Hong Kong Baptist University, Hong Kong Polytechnic, University of Bocconi, Koç University, and City University of London.

Associate Editor

Hari Sridhar

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.