Abstract

The authors investigate the role of the physical store in today’s multichannel environment. They posit that one benefit of the store to the retailer is to enhance customer value by providing the physical engagement needed to purchase deep products—products that require ample inspection for customers to make an informed decision. Using a multimethod approach involving a hidden Markov model of transaction data and two experiments, the authors find that buying deep products in the physical store transitions customers to the high-value state more than other product/channel combinations. Findings confirm the hypotheses derived from experiential learning theory. A moderated serial mediation test supports the experiential learning theory–based mechanism for translating physical engagement into customer value: Customers purchase a deep product from the physical store. They reflect on this physical engagement experience, and because it is tangible, concrete, and multisensory, it enables them to develop strong learning about the retailer. This experiential knowledge precipitates repatronage and generalizes to future online purchases in the same category and in adjacent categories, thus contributing to higher customer value. This research suggests that multichannel retailers use a combination of right-channel and right-product strategies for customer development and provides implications for experiential retail designs.

Keywords

The online channel has assumed a dominant role in many industries, the result of a 15% annual growth in e-commerce (U.S. Census Bureau 2020). In this environment, retailers seem ambivalent about the role of physical stores. Industry surveys show that many consumers still prefer them: “Half of the shoppers surveyed stated that they preferred to shop with online retailers who also operated physical stores” (Squire Patton Boggs and Kantar Retail 2015, p. 7; see also Creswell 2017; PwC 2017). However, many retailers such as Macy’s, Walgreens, and Bath & Body Works are closing physical stores (Peterson 2020). At the same time, digital-native online retailers such as Amazon, Alibaba, Blue Nile, Warby Parker, Bonobos, Google, and Indochino are opening them (VanStory 2019). Given these mixed messages, we find it natural to ask, “What in fact is the value of the physical store?”

To answer this question, we first recognize that consumers buy products, not channels. They must decide which products to buy in which channels. Neslin et al. (2014) advocate for studying this joint product/channel decision. They maintain that the product and channel choice processes are “intertwined” (p. 320) and that “there is significant academic and managerial motivation for the studying the interrelationships between brand and channel choice” (p. 320). Although, strictly speaking, they discuss channel and brand choice, their message can also be interpreted as calling on academics to research “the consumer’s decision of where and what to buy” (p. 329).

Our research draws on this call to action and the seismic shifts in the retail landscape to propose and empirically examine a central hypothesis: physical stores can enhance customer profitability by providing the physical engagement that customers value when purchasing “deep” products. We argue that products differ in the amount of inspection customers need to make a purchase. Some products require relatively “shallow” inspection, where a picture and written description suffice (e.g., a mobile phone charger), whereas other products require “deep” inspection, such as touch and physical interaction (e.g., a shirt). Drawing from experiential learning theory (ELT), our thesis is that customers value physical engagement when buying deep products and that the store provides such physical engagement, creating a favorable learning experience that increases repatronage. The lesson is that the product/channel purchase combination—deep product purchases in-store—develops more profitable customers.

Our research objective is therefore to investigate the following questions: (1) Does buying deep products in the physical store 1 enhance customer value more than other product/channel combinations? (2) If so, what are the implications for the customer’s future channel choices?

We adopt a multimethod approach to answer these questions. In Study 1, we analyze customer-level transaction data for 50,387 customers of a large multichannel retail chain that sells outdoor recreation gear, sporting goods, and clothing. We first classify products as “deep” and “shallow” on the basis of the novel concept of product inspection depth that builds on Lal and Sarvary’s (1999) concept of digital and nondigital attributes and Peck and Childers’ (2003b) findings around the importance of haptic information to consumer experiences. We then use a hidden Markov model (HMM) to examine consumers’ product/channel choice dynamics and uncover two latent states: (1) a low-value state characterized by lower purchase frequency and profitability and (2) a high-value state characterized by higher purchase frequency and higher profitability. We find that customers are more likely to transition to the high-value state and remain there to the extent they have purchased deep products in the physical store.

To replicate these findings and understand the underlying process, we conduct two lab experiments. Study 2 verifies that the deep product/physical store combination produces the highest repatronage intentions. Moderated serial mediation analysis supports the following process proposed by ELT: concrete experience → reflection on physical engagement → hypothesized learning → repatronage. This finding suggests that purchasing deep products in-store provides consumers with concrete, tangible, multisensory experiences that enable them to reflect on and then generate hypothesized learning that encourage them to repatronize the retailer, thus enhancing customer value.

Experiential learning posits that on gaining experience, consumers generalize their learning beyond the contexts they have experienced. Study 3 verifies that once customers have purchased a deep product in a physical store, they are more amenable to purchasing the same as well as adjacent deep products online from the retailer in the future. They thus generalize from the retailer’s store to its website and to adjacent deep product categories.

Our findings support the trend of online retailers establishing an offline presence to enhance customer value by providing customers with concrete, tangible, multisensory experiences. This corroborates that many consumers still prefer to buy in-store. A recent survey found that “if given the opportunity, 71% of consumers said they would even prefer to shop at an Amazon store over Amazon.com” (Taylor 2015). Another survey revealed that “50% of shoe buyers, 64% of sports equipment buyers, 59% of furniture buyers and 68% of jewelry buyers still prefer the physical store” (PwC 2017). Thus, despite two decades of innovation aimed at making e-commerce more engaging, many consumers still perceive the benefits of buying deep products in physical stores.

Practitioner quotes support consumers’ needs for concrete, tangible, multisensory experiences, which facilitate physical engagement, for why online retailers seek physical store presence: [Alibaba’s physical stores are] providing an option for consumers to physically inspect, touch and feel products before purchase. This appears to be the right strategy. The physical store should attract … online shoppers, who want a more human shopping experience Many stores will be giving customers an experience and providing insight and information. Want new pants? Find your size and the style you like in the store. Looking for a new smartphone or tablet? Try them out at a store and have a clerk walk you through the different features With certain products, seeing and feeling makes a difference … even the most elegant descriptions and images can’t replace the feel of organic, high thread count cotton sheets

These quotes echo our proposition that the physical store provides customers with the engagement they value when purchasing deep products. The fact that online retailers are pursuing an offline presence today validates our findings and supports our physical engagement theme. In turn, our findings support this trend. Our findings also suggest that online retailers who cannot afford the investment required for a physical presence should mimic the physical engagement found in stores and make the digital experience more concrete, tangible, and multisensory.

In summary, we offer three key findings. First, buying deep products in the physical store increases long-term customer value. Second, consumers who purchase deep products in-store are subsequently more likely to buy the same and adjacent deep product categories online. Third, an important underlying mechanism is experiential learning. We also find that direct mail marketing encourages customers to purchase deep products in-store and increases customer value, suggesting that retailers can onboard new customers and revive lapsed customers via the promotion of deep products and in-store purchasing.

These findings make the following contributions. First, we empirically identify an important role of physical stores, which is to enhance customer value by providing the physical engagement needed to purchase deep products. Second, we provide evidence that physical stores fulfill this role through experiential learning. Third, we advance theory by introducing the notion of “product inspection depth” and highlighting the distinction between physical engagement and digital engagement. Finally, we expand multichannel research that has focused on channel choice (Thomas and Sullivan 2005; Valentini, Montaguti, and Neslin 2011; Venkatesan, Kumar, and Ravishanker 2007) by demonstrating that management of the joint product/channel decision is crucial for better understanding customer behavior.

Framework and Predictions

We aim to identify which product/channel purchase combination enhances customer value more than other combinations. We posit that customers value physical engagement when buying deep products. The store provides this engagement, creating a favorable learning experience that increases patronage and customer profitability.

Product Inspection Depth and Physical Engagement

We distinguish products in terms of inspection depth, defined as the degree to which customers examine the product to make an informed purchase decision. Inspection depth can be ordered along a continuum: (1) pictures and descriptions are adequate, (2) visual inspection of the product is needed, (3) touching the product is needed, and (4) interaction with the product is needed (e.g., trying on, testing). We refer to products that require less inspection as “shallow products”; those that require more inspection we refer to as “deep products.”

The concept of product inspection depth follows from the literature that examines how extensively the customer must examine a product to make an informed purchase. Sachdeva and Goel (2015) stress the importance of physical inspection in the fashion industry. Kacen, Hess, and Chiang (2013) find the inability to inspect shoes, DVD players, flowers, and food is an impediment to patronizing online stores, but not so for books and toothpaste. Ofek, Katona, and Sarvary (2011) suggest that profits for the multichannel firm decrease when consumers find it important to inspect the product before purchase. Product inspection depth is rooted in Nelson’s (1970) theory of search and experience goods. Search goods can be evaluated prior to purchase, whereas experience goods need to be consumed to be evaluated. Relatedly, Lal and Sarvary (1999, pp. 487–88) advance the concept of digital attributes, which can be “communicated online” versus nondigital attributes, which “can only be evaluated through physical inspection.”

Product inspection depth synthesizes these ideas yet differs in important ways. For example, it differs from experience/search in that a deep product does not have to be consumed to be evaluated—it just needs to be inspected. It extends digital attributes, such as appearance, into the physical domain (e.g., “I will try on this clothing to see how it actually looks on me”). Furthermore, it is not confounded with price. For instance, a pair of shoes requires deeper inspection than a (higher-priced) computer, whose specifications can be read off a product description. Inspection depth is particularly relevant to multichannel shopping, where the ability to inspect differs by channel.

To acquire product inspection depth, consumers need to physically examine, inspect, or even interact with the product. That is, the customer has to physically engage with the product. More generally, the literature defines engagement as “a behavioral manifestation toward the brand, beyond purchase” (Van Doorn et al. 2010, p. 253). This manifestation can include touching and examining the product, reading descriptions, watching a demonstration, reading reviews, and interacting with a sales representative.

The literature further delineates two forms of engagement: digital and physical (Van Heerde, Dinner, and Neslin 2019). Digital engagement entails nonphysical actions such as seeing the product on a printed image. Formally, we define “physical engagement” as when the customer goes beyond visual inspection to gain multisensory knowledge of the product (e.g., by touching and using it). Peck and Shu (2009) link physical touch to object valuation, and Peck and Wiggins (2006) link touch to persuasion, suggesting that physical engagement can increase customer satisfaction. The potential for physical engagement differs by channel. The physical versus digital distinction is important because physical stores offer both physical and nonphysical engagement, whereas the online channel only offers nonphysical (digital) engagement.

Experiential Learning Theory

The product inspection depth consumers acquire through physical engagement defines a shopping experience. What do consumers learn from this experience? This is the bailiwick of experiential learning theory (ELT). David Kolb developed ELT as a synthesis of work by Lewin, Piaget, and others (Kolb 1971, 1984; Kolb and Kolb 2005; McLeod 2017). It is relevant for our purposes because it translates experience into learning. In Kolb’s words, “Learning is the process whereby knowledge is created through the transformation of experience” (Kolb 1984, p. 38), and “Knowledge results from the combination of grasping and transforming experience” (Kolb 1984, p. 41).

ELT is a process whereby people learn in four recursive stages: experiencing, reflecting, thinking, and acting (Kolb and Kolb 2005, p. 194). People first experience something concrete or tangible. They then reflect on the experience. Reflection enables people to hypothesize what they have learned from the experience and the extent to which this learning generalizes beyond the recent experience. People then act (i.e., test this hypothesis when the opportunity arises). The action provides more experience, and the four-stage process repeats. 2

A review of the ELT literature reveals four themes we draw on in forming our hypotheses. First, experiential learning builds on concrete and tangible experiences (Kolb 1984). Kolb (1984, p. 21) notes, “The emphasis is on here-and-now concrete experience,” and “Immediate personal experience is the focal point for learning, giving life, texture, and subjective personal meaning to abstract concepts.”

Second, experiential learning is a feedback process: Consumers develop hypothesized learning from experience. They use subsequent experiences to test how well these hypotheses generalize, modifying them as needed. “Learning is described as a process whereby concepts are derived from and continuously modified by experience” (Kolb 1984, p. 26).

Third, experiential learning draws on the five senses. Under the rubric “sensory marketing,” researchers have connected experience to the five senses—touch, taste, smell, hearing, and seeing (Krishna 2012). Thus, three findings from sensory marketing prove critical to our hypothesis development. First, touch experience influences attitudes. Research has found that touch leads to more confident conclusions (Peck and Childers 2003b), is more persuasive (Peck and Wiggins 2006), generates affect (Peck and Shu 2009), and influences quality judgments (Ackerman, Nocera, and Bargh 2010). Second, multisensory experiences are more effective in generating learning than are single sensory experiences (Krishna, Elder, and Caldara 2010). Finally, touch can be an end in itself or a gateway to enhancing other senses, particularly visualization (Peck 2011). Consider the case of buying jewelry and wristwatches. Touching the jewelry or the watch to feel its texture and weight distribution is valuable in itself, but it also enhances visualization, as one can pick it up, view it in natural light from various angles, and try it on to see how it looks and feels. Touching and seeing naturally go together.

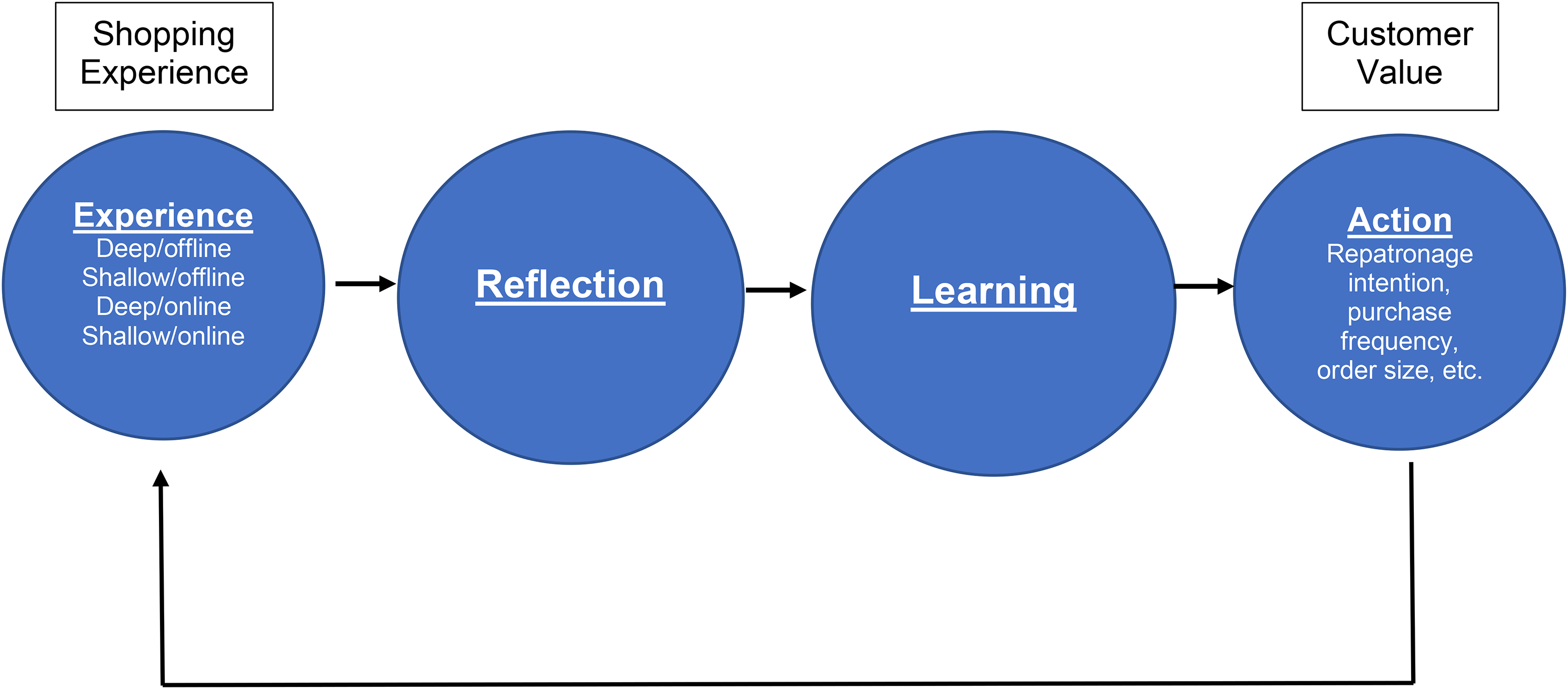

Figure 1 integrates product inspection depth, engagement, experiential learning, and customer value. The process starts with a shopping experience, characterized by the type of product the consumer buys (deep vs. shallow) and the purchase channel. This initiates the experiential learning process. Iterating through ELT yields learning that consumers want to confirm and determine if it generalizes to other contexts. These tests take the form of future shopping behaviors, which serve as the experiences that initiate future ELT cycles.

Experiential learning: translating engagement to future behavior.

Predictions

The impact of deep/offline purchase on customer value

Deep products require inspection, touch, and trial. The store provides this physical engagement, and the shopping experience therefore is concrete, tangible, and multisensory—prerequisites for effective experiential learning. These factors in synchrony encourage deeper reflection, stronger hypothesized learning and potential generalizations, and, ultimately, more action.

Importantly, we assume that providing physical engagement for a deep product purchase enables the consumer to make a more informed decision. The experience, therefore, will be positive, encouraging favorable learning that propel the consumer toward repatronage and higher customer value. We therefore hypothesize,

The role of experiential learning on the impact of deep/offline purchase on customer value

ELT contributes to the translation of deep products/in-store to future customer value. It suggests the following mechanism underlying H1: customers purchase a deep product from the physical store. They reflect on this physical engagement experience, and because it is tangible, concrete, and multisensory, it enables them to develop strong hypotheses of what they learned about the retailer. Because they are satisfied with their purchase, this learning is favorable, precipitating repatronage.

In summary, the mechanism is as follows: customers purchase a deep product in-store → they reflect on the physical engagement experience → they hypothesize favorable learning → they repatronize the retailer. This parallels ELT's process of experience → reflection → hypothesized learning → action. We thus predict:

Two assumptions underlie H1 and H2. First, the customer purchases a satisfying product. It is possible that despite the concrete experience, the customer emerges dissatisfied. Experiential learning is still at play, but the consumer learns that this retailer is not suitable, and customer value declines. Second, the customer’s favorable experience spills over to both the retailer and the brand. Thus, H1 and H2 assume the customer emerges from the deep/offline experience with favorable learning that transfers to the retailer.

Importantly, H1 is comparative; it maintains that deep/offline purchasing enhances customer value more than any other product/channel combination for the following reasons. First, the online channel entails only one sense—visual. Thus, the online experience is less concrete, less tangible, and not multisensory, and the consumer learns less. Second, shallow/offline purchasing has the potential to provide a concrete, tangible, and multisensory experience because the store offers this opportunity. However, by definition, shallow products do not require this physical engagement. As a result, the customer does not reflect enough to generate strong hypothesized learning, and repatronage is not enhanced as much.

The impact of a deep/offline purchase on future deep/online purchases

ELT posits that customers will test the extent to which their learning generalize beyond their experience to date. We consider two types of generalization. First, customers may generalize to a new channel. Consider customers buying a shirt in the physical store, and assume that they hypothesize from this experience that the retailer is a good place to buy shirts. They can then see how well this learning generalizes to another channel by purchasing deep products online from the retailer’s website. This lets them test for generalization while taking advantage of the convenience of the website. As elaborated in our discussion of H1 and H2, customers who purchase shallow products in the physical store do not learn enough to encourage them to explore whether to purchase deep products online. In other words, these consumers are less apt to experiment with the website if they need a shirt. We thus hypothesize:

Second, learning inferred by deep/offline customers can generalize not only to new channels but also to new products. Product generalization can occur because the initial purchase experience allows customers to learn about the retailer’s overall product quality and product fit—factors that are especially important for deep products. Obviously, it is easier to generalize to something that is most related to the current context, and we believe the strongest impact of buying a shirt offline will be buying a shirt online in the future. But the generalization could extend to adjacent deep products such as sweaters, coats, and other apparel, and possibly to different product categories altogether. We thus hypothesize:

Overview of Studies

Study 1 uses retail transactional data and an HMM to verify H1 and H3. We test whether the translation of product/channel into customer value is most favorable for the deep/store combination (H1) and whether this combination encourages future usage of the online channel (H3). We conduct two randomized experiments in Studies 2 and 3 to replicate Study 1’s findings. In addition, Study 2 tests the hypothesized learning mechanism (H2), and Study 3 tests product generalization (H4).

Study 1: An HMM of Customer Product/Channel Dynamics

Data

Our data are from a national retailer that sells outdoor recreation gear, sporting goods, and clothing in 140 retail stores and on its website. The data chronicle customer-level purchase occasions from January 2003 to July 2005. For each purchase occasion, we observe stockkeeping units (SKUs) purchased, price, purchase amount (dollars spent on the entire order), cost of goods sold, channel choice, timing, and returns. We know each customer’s zip code and tenure with the retailer.

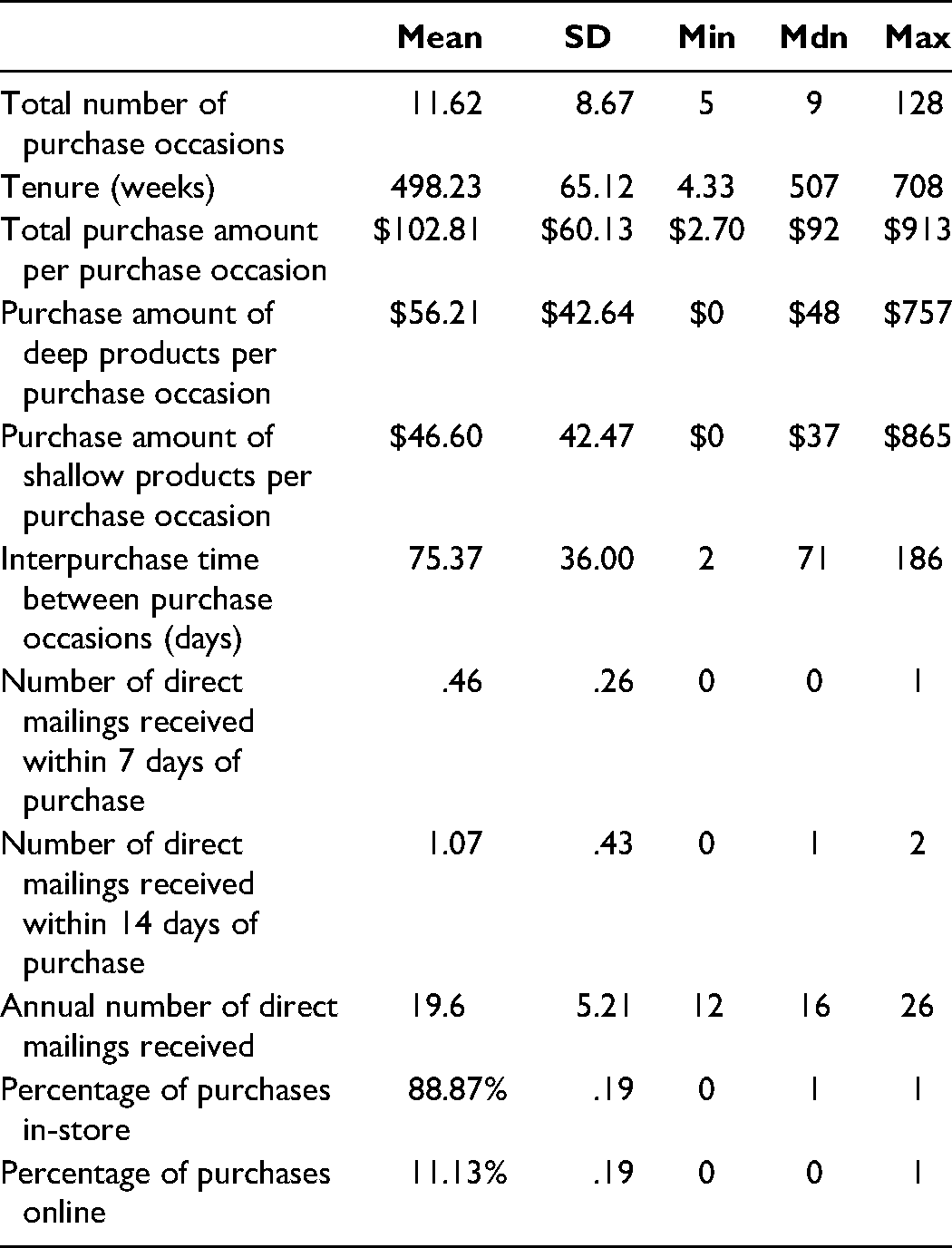

Our sample contains 50,387 customers buying more than 30,000 SKUs on 585,577 purchase occasions, an average of 12 purchase occasions per customer. Table 1 shows that online purchases make up 11.1% of purchase occasions. Because we are interested in dynamics, we select only customers who had at least two purchase occasions. Of these, 8,391 are “new customers,” with 80,751 purchase occasions, acquired after the beginning of the data set. Deep products constitute 54.7% of purchases, with an average spend of $56.21 per purchase occasion. The firm uses direct mail to communicate new styles and special events. On average, customers receive 19.6 direct mail pieces annually. The retailer does not target on the basis of past purchases. Prices and cost of goods sold do not vary between online and offline. Only 5.6% of customers purchased the same SKU more than once, either on the same purchase occasion or over multiple purchase occasions. So there are few instances of rebuying the same product. Half of the customers shop in a single channel; the others shop both in-store and online. Consistent with previous research, multichannel shoppers are more profitable (see Web Appendix Table W1.1).

Descriptive Statistics per Customer.

The retailer categorizes the 30,000 SKUs into ten “specialties,” such as camping, travel, cycling, snow sports, and clothing, followed by 373 “classes” or categories, such as jackets, pants, and shorts, and finally specific SKUs. For details, see Web Appendix Table W2.1.

Three independent judges rated each of the 373 product categories on inspection depth as well as digital or nondigital (Web Appendix W3) on a scale of 1 to 7. Intercoder reliability for inspection depth is .92. This suggests that the inspection depth concept is robust across coders and covers dimensions such as touch and interaction. The correlation between inspection and digital/nondigital ratings is .77, thus offering discriminant validity from digital/nondigital. 3 Not surprisingly, clothing and footwear generally have high ratings, but there is much variation within a specialty (Web Appendix Figure W3.1). This suggests that specialties are not perfect indicators of inspection depth. For example, within footwear, hiking boots are rated 7, women’s sandals are rated 4, and insoles are rated 2 (on a 7-point scale). Deep products are not necessarily more expensive than shallow products; the correlation between price and inspection depth is .12 and insignificant. We categorize products as deep or shallow using a median split. This enables us to model purchase amounts of each type on each purchase occasion. 4

Model-Free Evidence

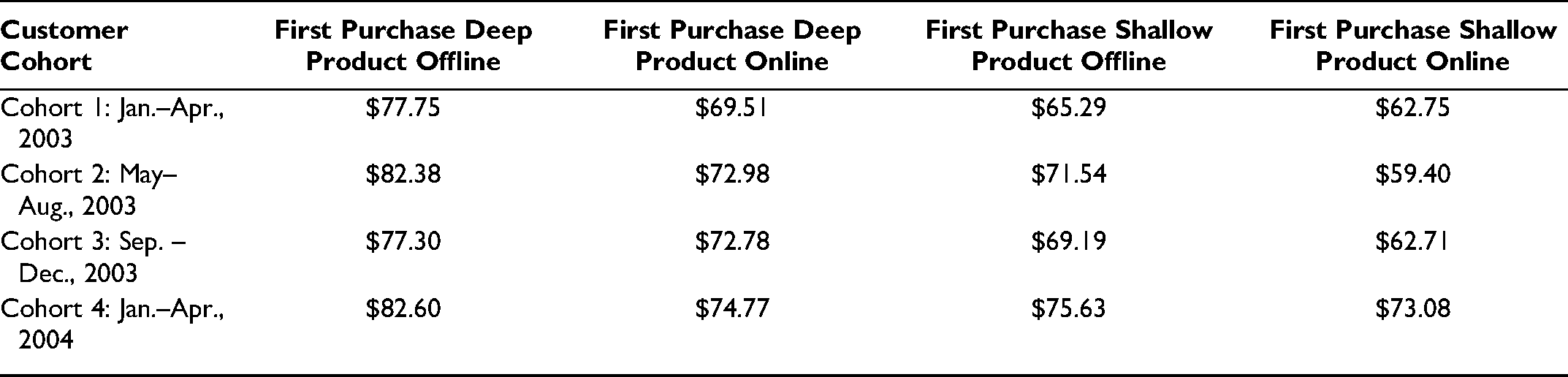

Our key hypothesis is that buying deep products in the physical store increases future customer value. New customers provide model-free evidence for this. Table 2 shows four cohorts of new customers defined by when they are acquired. Profits for the one-year period after acquisition differ depending on the first product/channel choices; buying deep products offline as the first purchase yields the highest profit, consistent with H1.

Model-Free Evidence: First Product/Channel Choice and One-Year Profit.

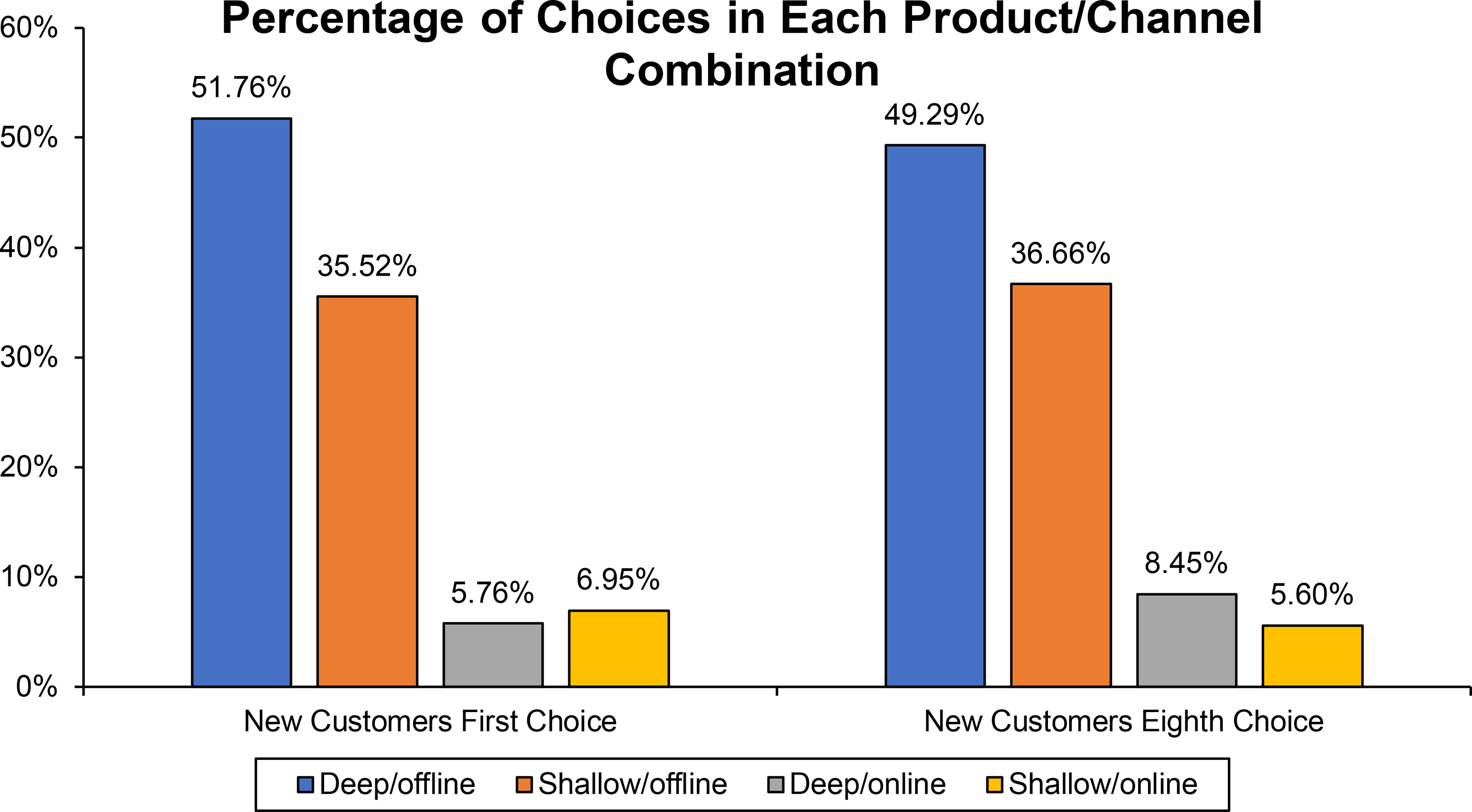

Figure 2 illustrates dynamics. It depicts product and channel choices for new customers’ first purchase and the same set of new customers on their eighth purchase. We see that 5.76% of first purchases are deep products bought online. This increases to 8.45% by the eighth purchase. This finding is consistent with H3 and shows that new customers’ buying patterns evolve and alleviates the concern that new customers’ purchase patterns are set before the retailer acquires them.

Model-free evidence of product/channel choice evolution.

It is still possible that new customers self-select into the relationship with the retailer. We address this in Study 1 by (1) developing a model designed to flexibly detect dynamics and control for unobserved customer heterogeneity, (2) separately analyzing new and existing customers via robustness checks, and (3) conducting a propensity scoring analysis. Studies 2 and 3 alleviate the self-selection concern using random treatment assignment in experiments.

Modeling Framework

We use a multivariate HMM to study customers’ joint decisions for channel choice, purchase amount, and interpurchase time. HMMs are often employed to study the dynamics of customer–firm relationships (e.g., Kumar et al. 2011; Li, Sun, and Montgomery 2011; Luo and Kumar 2013; Montoya, Netzer, and Jedidi 2010; Netzer, Lattin, and Srinivasan 2008; Schweidel, Bradlow, and Fader 2011; Zhang, Netzer, and Ansari 2014; Zhang et al. 2016). HMMs incorporate experiential learning in that they include dynamics and feedback and model changes in behavior arising from experience (reflected in “latent states”). HMMs also identify the drivers of these dynamics by studying customer transitions between latent states. A simpler model such as regression would have difficulty capturing these dynamics and rich insights. Furthermore, HMMs can distinguish temporal dynamics from customer heterogeneity. We will model time-invariant customer heterogeneity as well as dynamics.

We use the HMM to discern when the customer is in a high- versus low-value state and predict transitions between these latent states by descriptors such as customers’ previous purchases of deep versus shallow products and their use of offline versus online channels. In this way, the HMM provides tests for H1 and H3.

Specifically, we model a customer’s purchase occasion by four interrelated decisions: (1) channel choice, (2) purchase amount (in dollars) of deep products, (3) purchase amount (in dollars) of shallow products, and (4) purchase timing (in terms of interpurchase time). These four dependent variables not only paint a rich and multifaceted picture of customer behaviors beyond overall purchase amount but also enable us to calculate customer value within a particular time frame. We incorporate covariates in customers’ utility functions and thus predict customers’ decisions at each purchase occasion. We include covariates in transition functions to predict how customers migrate between latent states.

Because HMMs are popular in marketing, we detail the specific components of our HMM to Web Appendix W4. Next, we highlight the covariates in the specification.

Covariates in the HMM

Previous channel choice

H1 and H3 both predict that previous channel choices influence future customer value. We include the customer’s cumulative number of channel choices prior to purchase occasion j, offline_choices(j − 1) and online_choices(j − 1), 5 for the store (offline) and website (online), respectively. This is consistent with Kumar and Venkatesan (2005), Stone, Hobbs, and Khaleeli (2002), and Verhoef and Donkers (2005). 6

Marketing

Direct mail is the only firm-initiated marketing activity in the data and did not promote specific channels. Discussion with management revealed that communications were not customer-targeted, and we test and confirm that there is no endogenous relationship between customers’ past purchase behavior and the likelihood of receiving direct mail. Thus, it reflects a baseline advertising effect. The variable marketingj equals the number of mailings the customer received within 30 days prior to purchase occasion j. We use a squared term,

Holiday

The variable holidayj indicates whether purchase occasion j occurs within two days preceding the following gift-giving holidays: Mother’s Day, Father’s Day, Valentine’s Day, Christmas Eve, and New Year’s Day. Because last-minute online shopping risks that a gift will not arrive on time, people may be more likely to shop offline when it is very close to these holidays.

Purchase amount

We measure customer spend (in dollars) on deep and shallow products on previous purchase occasion j − 1 (deep_amount[j − 1] and shallow_amount[j − 1]). Both H1 and H3 predict that the type of product purchased is crucial for determining future customer value.

Customer tenure

Tenure (tenurej) denotes how long the customer has been purchasing from the retailer as of purchase occasion j. It represents the length of the relationship.

Product returns

We calculate cumulative returns prior to the current purchase occasion (in dollars) and distinguish between deep and shallow product returns (deep_returns[j − 1] and shallow_returns[j − 1]). Petersen and Kumar (2009) find that product returns enhance customer relationships.

Interpurchase time

We define interpurchase_timej as the length of time between the previous and current purchase occasion. Shorter interpurchase time indicates more frequent purchases and, thus, a more valuable customer. Longer times could indicate lapses in loyalty or changes in lifestyle, which could influence subsequent channel or product choice.

Specifying Utility and Transition Functions

HMMs model latent states and estimate “transition functions” that predict how the customer migrates in and out of these states over time. HMMs characterize each state by its own set of utility functions—in our case, one for each of the four customer decisions we model. Following HMM conventions, we include covariates expected to have an immediate impact in the utility functions and covariates expected to have a long-term impact in the transition functions.

Accordingly, we include previous channel/product decisions—offline_choices(j − 1), online_ choices(j − 1), deep_amount(j − 1), and shallow_amount(j − 1)—in all four utility functions to reflect ELT’s dictum that customers test what they learn from experience by taking action—all four behaviors are actions. We include marketingj and

We also include previous channel/product decisions (offline_choices[j − 1], online_choices[j − 1], deep_amount[j – 1], shallow_amount[j − 1]) in the transition functions to test our hypotheses that these influence future customer value. Direct mail is advertising that can have long-term effects, so we include marketingj and

Note that we use lagged variables in the utility and transition functions to capture dynamics (how previous decisions drive current decisions and state transitions). We are particularly interested in how previous channel and product choices determine future customer value.

We do not include current prices as a covariate. From a theoretical standpoint, including current prices in the purchase timing and channel choice models would make the difficult-to-support assumption that customers make these decisions based on prices they do not observe until after they make those decisions. As a robustness check, we included monthly fixed effects and a monthly price index of top 30 best-selling items as covariates in the utility equations. Results, most importantly those pertaining to H1 and H3, were substantively the same. 8

Heterogeneity and Estimation

Capturing customer heterogeneity is crucial for distinguishing temporal dynamics from time-invariant customer heterogeneity (Heckman 1981). We do this by adding latent class segmentation to the HMM. This allows the coefficients for the transition functions and the four utility functions to vary across segments.

We use Markov chain Monte Carlo (MCMC) methods for estimation and use the adaptive Metropolis procedure (Atchadé 2006) to improve mixing and convergence. We use the first 24 months of data for training and the last seven months for testing. We obtain our estimates from the last 50,000 draws from an overall MCMC run of 200,000 iterations. We assessed convergence by monitoring the time-series of the MCMC draws.

Interpreting the Results

Choosing the number of states and latent classes (segments)

To determine the number of HMM states and the number of segments, we consider the in-sample log-marginal density, deviance information criterion, and predictive log-likelihood on the validation sample. Drawing on these criteria, we find that a two-state, two-segment HMM exhibits the best performance. It captures dynamics and heterogeneity while keeping model complexity in check. Therefore, we adopt this model. Web Appendix Table W4.1 shows these criteria for various permutations of the HMM. The table shows that the two-state, two-segment HMM is better than models that do not include dynamics, do not include heterogeneity, or include heterogeneity but as a continuum rather than discrete segments. 9

Interpreting the states

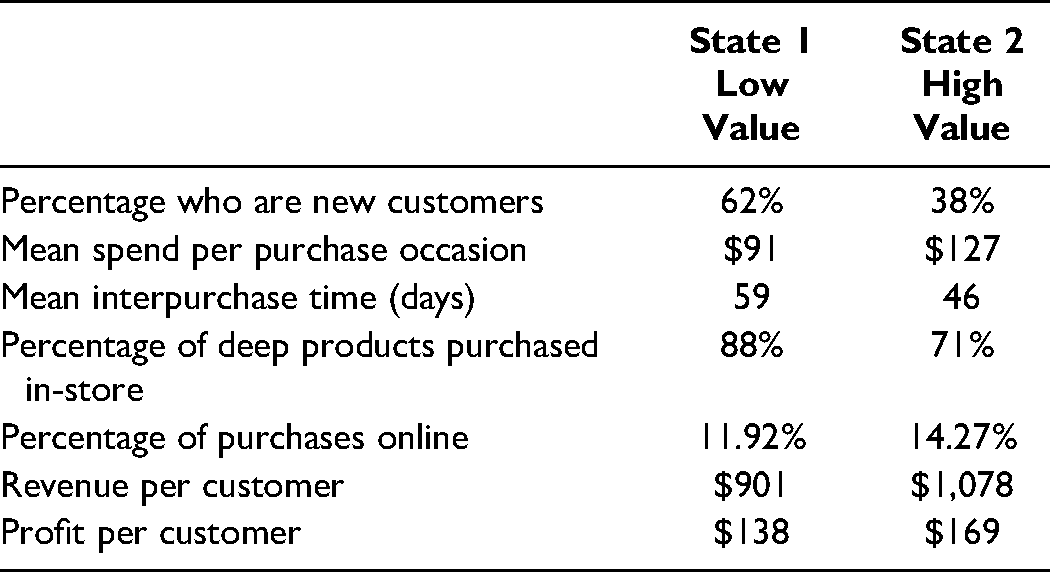

We used methods described in MacDonald and Zucchini (1997) to infer each customer

Description of the Two HMM States.

Interpreting the segments

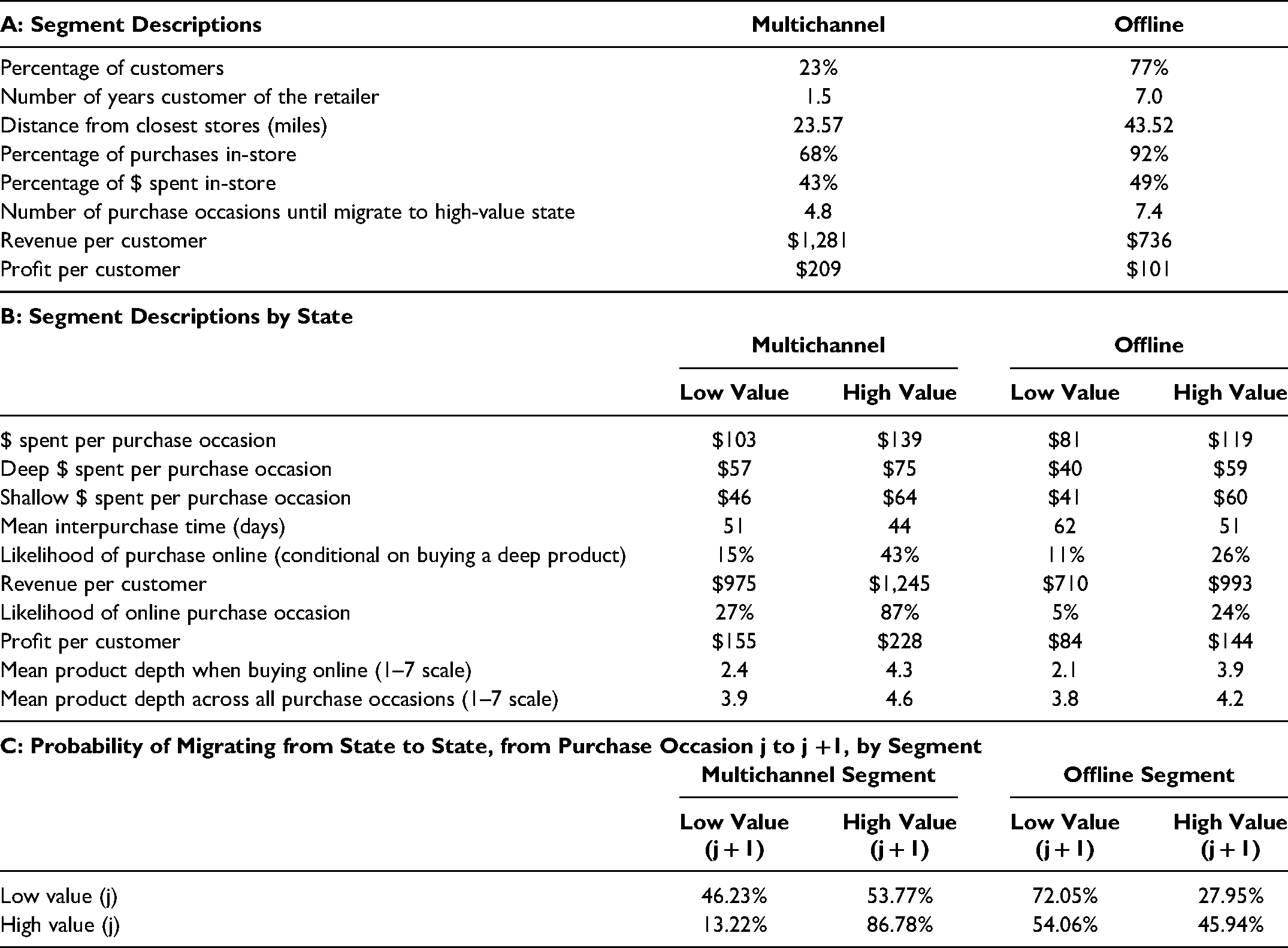

We assign customers to the latent segment to which they have the highest probability of belonging. Table 4, Panel A, shows that segment 1 is more profitable than segment 2, has a more balanced mix between in-store and online buying, transitions more quickly to the high-value state, and lives closer to the retail store. The channel mix and higher profitability suggest that segment 1 is the “multichannel segment.” Table 4, Panel B, shows that customers in this segment buy more deep products, especially when they move to the high-value state. Table 4, Panel C, shows that customers in this segment are more likely to migrate to the high-value state and remain once they get there. Segment 2 focuses on offline—92% of these customers’ purchase occasions are in-store (95% when they are in the low-value state and 76% when they are in the high-value state). Table 4, Panel C, further shows that segment 2 customers are less likely to transition to the high-value state. Accordingly, we label segment 1 “multichannel” and segment 2 “offline.”

Segment Descriptions and Migration Probabilities.

Interpreting the transition functions

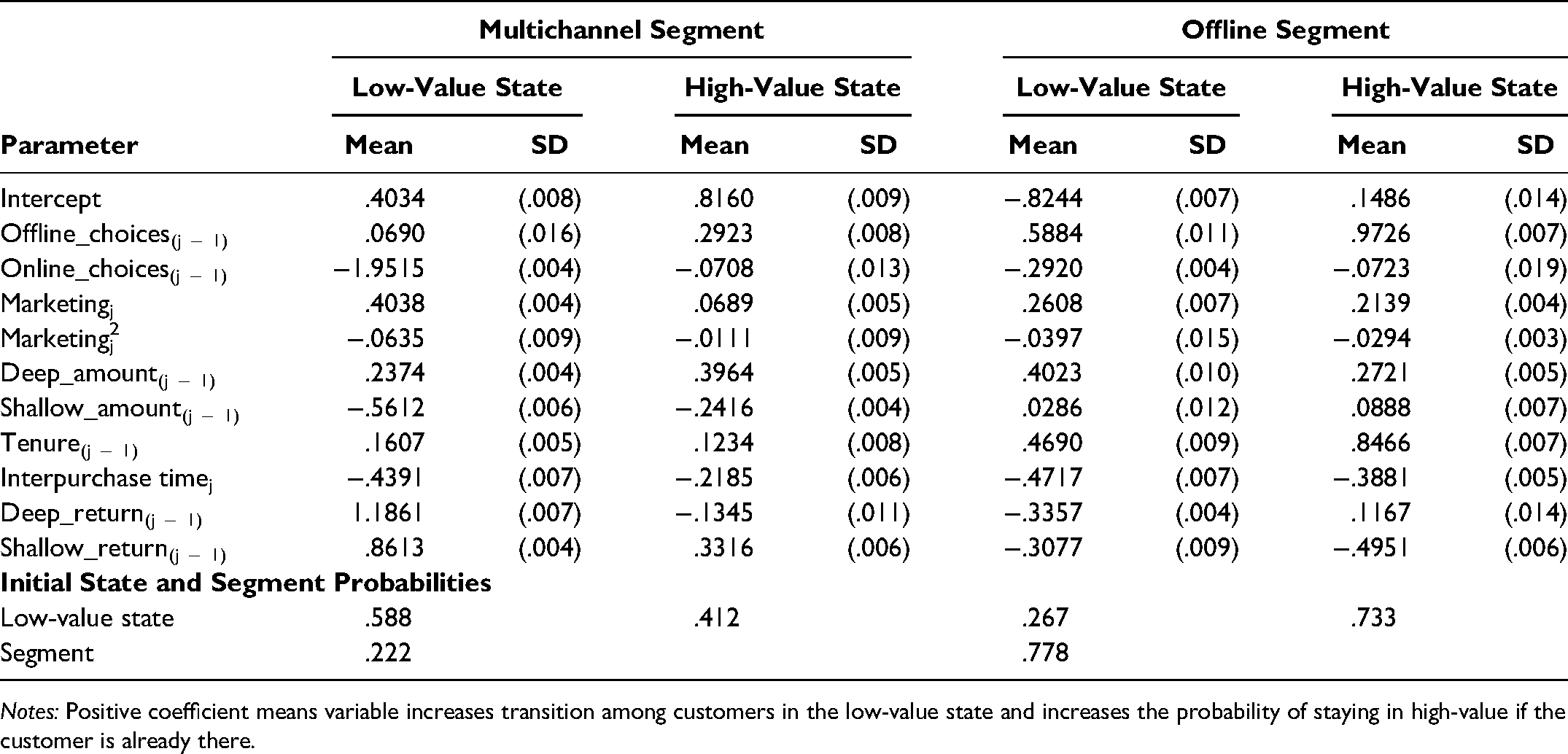

Table 5 shows the parameter estimates for the transition functions. A positive coefficient for the low-value state means that customers in that state are more likely to move from low value to high value as the covariate increases; a positive coefficient for customers in the high-value state means they are more likely to stay high value. In both segments, previous choices of the offline channels drive customers to high value or keep them there. In contrast, online choices decrease the likelihood that low-value customers move to the high-value state, as well as the chance they remain high value. Marketing drives customers to the high-value state and keeps them there. Purchasing deep products drives customers to the high-value state and keeps them there, whereas purchasing shallow products drives customers to the low-value state and keeps them there. Longer tenure transitions customers to high value, whereas longer interpurchase times move customers to low value. Importantly, the transition equations reveal plenty of dynamics that vary by segment.

HMM Transition Functions Parameter Estimates.

Notes: Positive coefficient means variable increases transition among customers in the low-value state and increases the probability of staying in high-value if the customer is already there.

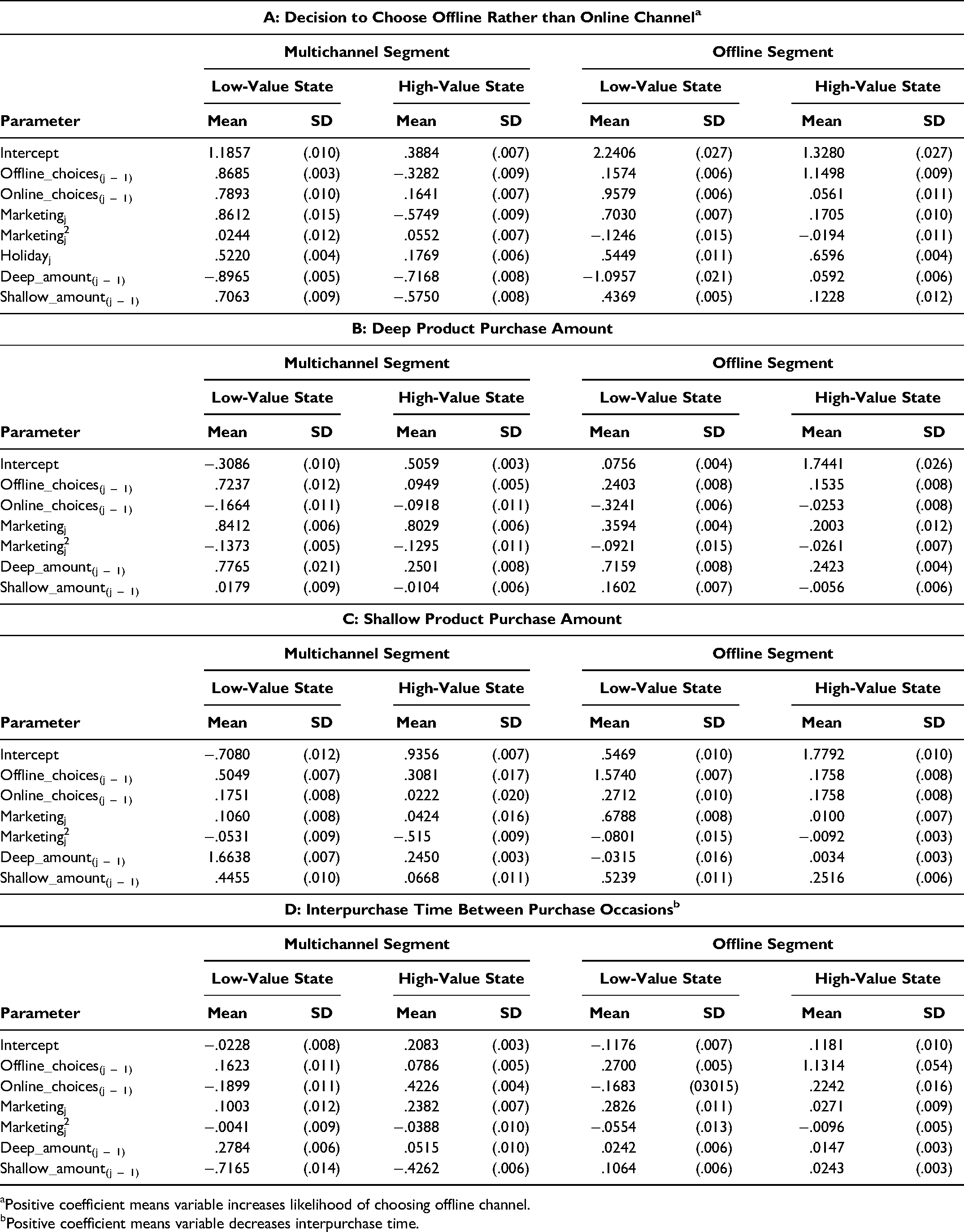

Interpreting the customer decision models

Table 6 contains parameter estimates for the four decision models (i.e., the utility functions) for both segments and both states. We also calculated marginal effects (Web Appendix W6), which are consistent with the estimates in Table 6.

Parameter Estimates for the Four Decision Utility Functions.

Positive coefficient means variable increases likelihood of choosing offline channel.

Positive coefficient means variable decreases interpurchase time.

Table 6, Panel A, displays the utility functions for the channel choice decision. The offline and online previous choice coefficients are mostly positive, suggesting that previous purchase in either channel encourages customers to buy in-store for their next purchase. Interestingly, higher previous deep product purchases mostly encourage customers to buy online, whereas shallow product purchases encourage them to buy offline. Marketing primarily stimulates offline purchases, with the exception of multichannel/high-value purchases. Holiday shopping more likely takes place in the physical store, as expected. Overall, we find strong effects of previous channel choice, previous spending by product type, and marketing.

Table 6, Panels B and C, show the utility functions for deep and shallow purchase amount. In general, previous offline purchase increases both deep and shallow spend, whereas previous online purchase has the opposite impact. Marketing increases deep and shallow spend, with a stronger impact on deep products. Previous deep product spend begets higher spend for both deep and shallow products. Shallow has the same direction of impact, albeit relatively smaller. Table 6, Panel D, shows that, for all segments and states, previous offline purchase decreases interpurchase time, possibly because the customer is more satisfied and thus buys again sooner.

Testing Hypotheses

Our model relies on temporal precedence, the association between previous and subsequent decisions, to support a causal interpretation of the results. As we show next, these estimated dynamics suggest that buying deep products in the physical store creates higher customer value and encourages customers to buy online in the future. However, as with any model of field data, we cannot claim the model unequivocally establishes causation. This is one reason we rely not only on Study 1 but also on controlled experiments that use randomization.

H1 hypothesizes that purchasing deep products offline is more likely to transition the customer to the high-value state than any other product/channel combination. The transition function estimates in Table 5 support this. Coefficients for deep_amount(j − 1) (row 7) and offline_choices(j − 1) (row 3) are positive in all four transition functions. Coefficients for online_ choices(j − 1) (row 4) are negative, so online purchases make it less likely that the customer will transition to high value. The coefficients for shallow_amount(j − 1) (row 8) are negative—or, at best in the offline segment, positive but far smaller in magnitude than the coefficients for deep_amount(j − 1). Overall, we find that buying deep products offline is most positively associated with transitioning to the high-value state (i.e., to higher customer value). Study 1 thus supports H1.

H3 proposes that customers who buy deep products offline are more likely to purchase deep products online in the future. We have shown that deep/offline purchasing drives customers to the high-value state. Table 3 then shows that these high-value customers purchase a higher percentage of their deep products online (vs. in-store) than do the low-value customers (29% vs. 11%, row 4). Table 4, Panel B, further illustrates this at the segment level: high-value multichannel customers make 43% of their deep product purchases online, compared with 15% if they are low value. The same holds true for the offline segment: these customers purchase 26% of their deep products online if they are in the high-value state, compared with 11% if they are in the low-value state. Study 1 thus also supports H3.

Robustness Checks

New versus existing customers

We ran the model only on existing customers (41,996 customers, 504,826 purchase occasions). The substantive results were very similar to those for the full data set, indicating that the evolution of customer behavior based on channel/product experiences exists for both new and existing customers.

New customers’ first channel/product choice

We tested whether the results in Table 2 are due to self-selection—that is, that new customers who start by purchasing deep products in-store already prefer the retailer. We conducted propensity score matching with new customers whose first purchase is deep products in-store as the treatment group and all other new customers as potential controls. We matched on (1) demographic variables extracted from each customer’s zip code and (2) variables calculated using data from the first two months after the initial purchase. These included distance to store, city versus rural, average prices paid, the gender category of the products purchased, purchase of children’s products, number of categories purchased per visit, and average interpurchase time. We then calculated subsequent profit, excluding those first two months.

The average treatment effect (incremental value among new customers with deep/in-store as the first purchase) is +$132.74, suggesting that purchasing deep products in-store generates higher long-term customer value (Web Appendix W7). The Rosenbaum test (Rosenbaum 2002) states that our treatment effect is significant even if the impact of an unobserved covariate were to increase the odds ratio of buying deep products offline by 50% (Γ = 1.5; see Web Appendix Tables W7.2 and W7.3).

Product definition

We ran the model with products classified as digital/nondigital instead of deep/shallow. The same substantive results hold for the digital/nondigital classification, with slightly worse model fit and prediction compared with the deep/shallow classification (deviance information criterion = 796,253 for digital/nondigital vs. 792,594 for deep/shallow, predictive likelihood = −198,237 for digital/nondigital vs. −194,899 for deep/shallow). This suggests that the deep/shallow product categorization yields a better-fitting model but similar findings to a “digital/nondigital” categorization. It also suggests that the sensory-rich inspection depth concept is particularly relevant in multichannel environments.

Use of median split for categorizing products

Our analysis categorizes deep and shallow products using a median split. We examined how much our results would change if we used different split thresholds. We reran the model using thresholds ranging from 30% to 70% (i.e., from a 30th percentile rating used to classify a product as deep up to a 70th percentile threshold). Web Appendix W8 indicates that the 50/50 (and 60/40) splits provide the best fit and performance. 10 In addition, our substantive results hold up between 30% or 70% thresholds, suggesting that the results are robust within a reasonable range of rules for classifying products as deep versus shallow. Finally, the predictive likelihood for the 30% threshold is better than that of 70% threshold, suggesting that it is safer to classify shallow as deep than deep as shallow.

Marketing Simulation for Targeting

The positive coefficient for marketingj in Table 5 (row 5) suggests that direct mail marketing moves customers to the higher-value state or keeps them there if they are already in a high-value state. A reasonable strategy is to target marketing to increase the probability that customers are in the high-value state. The question is, which customers should be targeted on the basis of their current state, segment membership, and previous product/channel choice?

We conducted a simulation to investigate this question. Details are in Web Appendix W10. We used model parameters to simulate purchase behavior over a 30-month horizon. In the base case, marketing is set so that each customer receives two direct mail pieces per month. In the “+1” case, we increased this to three per month. One could use dynamic programming to optimize targeting, but our purpose is simply to demonstrate the potential of targeting.

Profits in the base case were $127.36 per customer ($131.21 under the +1 strategy). 11 We found that the +1 strategy increased the probability of transitioning to or staying in the high-value state, “Prob(Hi),” for all customers except multichannel customers who currently are in a high-value state. They already have a high probability of staying high value (86.78%), so there is not much to gain by increasing marketing. A key result is that the gain in Prob(Hi) is largest for customers who just bought shallow products. For example, we found the gain for offline-segment low-value customers who just bought shallow offline is 29.20% − 24.67% = 4.53%, while the gain for those who just bought deep offline is 36.39% − 33.27% = 3.12%. This finding is consistent with H1: deep offline purchases naturally boost customers to a high-value state, so they have less need for marketing.

Study 2: Replicating H1 and Testing the Experiential Learning Mechanism (H2)

H1, supported by the HMM, proposes that one “sweet spot” for generating future customer value is for the customer to purchase deep products in the physical store. Study 2 employs a lab experiment to replicate H1 and test H2, the ELT mechanism we propose underlies it: deep product purchased in-store → physical engagement → favorable learning → repatronize the retailer.

Method

Our sample is 411 Amazon Mechanical Turk subjects. The average online and store patronage experience, age, and gender are statistically equal across treatment groups (details in Web Appendix Table W11.1).

We use a 2 (deep vs. shallow product) × 2 (physical store vs. online) between-subjects design with random assignment to treatment. We used “sports shirt” for the deep product and “portable cell phone charger” for the shallow product.

The survey (Web Appendix W11) instructed subjects that there is “a new sports and outdoor-gear retailer in town” and that “you have never shopped at this retailer.” We then asked, “Now, imagine that you shop at this retailer for the first time. You visit its physical store (website) and buy a sports shirt (portable cell phone charger) that costs $40. Please take a few minutes to describe in detail the specific steps you would have taken to purchase the sports shirt (portable cell phone charger) in this new physical store (on this new website).” We provided a text box for subjects to write a description of the steps they would have undertaken.

We then asked subjects to state their intention to shop at this retailer again, using the Baker et al. (2002) three-item repatronage scale (e.g., “I would be willing to buy from this retailer again in the future” [1 = “Strongly disagree,” and 7 = “Strongly agree”]). We asked subjects to rate how much they thought they would have learned about the retailer’s “product offerings and quality, as a result of this experience,” on a seven-point scale. This was followed by a question asking subjects to rate the product they bought on product inspection depth (1 = “Picture and description would be adequate,” 2 = “Visual inspection of actual product needed,” 3 = “Touch of product needed,” and 4 = “Interaction of the product needed [e.g., trying on, testing the features]”). This last step enables us to verify the deep versus shallow product manipulation.

Results and Discussion

We begin with the product manipulation check. Results indicate that the sports shirt attained statistically higher means on inspection depth relative to the portable cell phone charger (M = 2.42 vs. M = 1.64; t(409) = 6.88, p < .001).

Testing H1

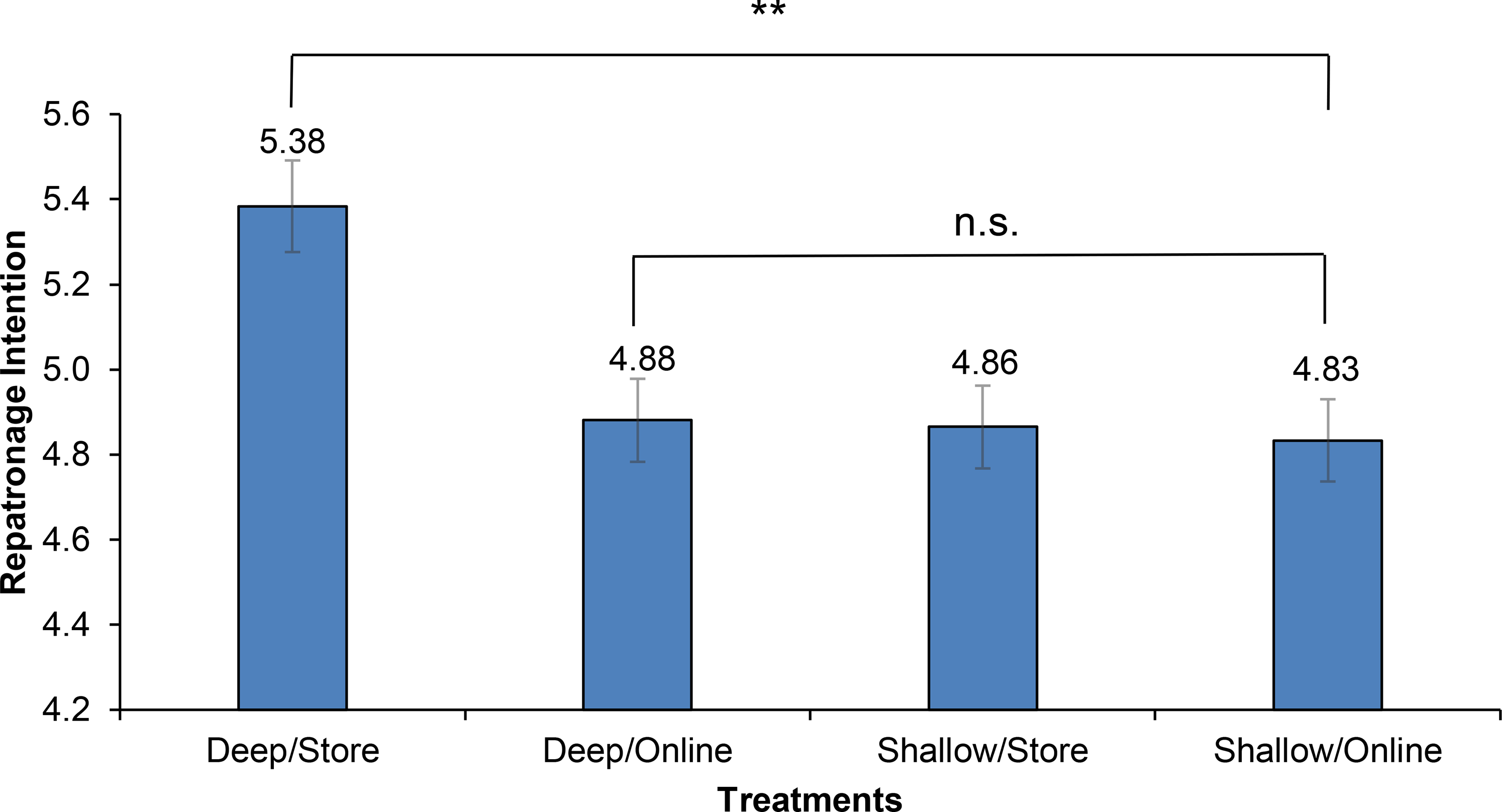

Figure 3 shows mean repatronage intentions by treatment. The 2 × 2 interaction analysis using analysis of variance demonstrates that both deep product (F(1, 407) = 6.94, p < .01) and store condition (F(1, 407) = 6.18, p < .05) positively contribute to higher repatronage. Central to our prediction, the deep × store interaction also positively contributes to higher repatronage (F(1, 407) = 4.82, p < .05). A planned contrast indicates the deep/store treatment clearly evoked the highest repatronage intentions among the three other conditions (Mdeep/store = 5.38 vs. Mdeep/online = 4.88, Mshallow/store = 4.86, and Mdeep/online = 4.83; F(3, 407) = 6.09, p < .001), consistent with H1. Web Appendix Tables 11.2A–D provide additional details of the analysis of variance and contrast tests.

The effect of first product/channel purchase combination on repatronage (Study 2).

Testing H2

We measured the extent to which subjects reflected on the physical engagement component of the experience by analyzing how they articulated the experience in their written descriptions. We recruited two research assistants blind to the research agenda to rate a physical engagement variable, “try_touch,” from each respondent’s description. We instructed the research assistants to read each description of the customers’ shopping experiences. We told the research assistants that some shopping experiences involve elements of touching, trying on, and feeling and instructed them to code try_touch as 1 if the description contains words, synonyms, or themes related to “try,” “touch,” or “feel”; alternatively, we instructed them to code try_touch as 0 in the absence of these themes. Intercoder correlation was .92.

The following are examples of subjects’ descriptions that clearly suggest physical engagement: I would look at the size of it. I would feel its texture. I would test it out. I would see how it would look on me. I would see if my favorite team is on the shirt. I would go into the store and do quite a bit of browsing first. I would allow myself extra time in this store as it is my first time going. I would familiarize myself with the brand and touch everything to test out its quality. I would go into the store and browse shirts. I might try on the shirt before buying it, unless I was sure it would fit and/or I didn’t want to spend extra time. Then I’d buy it.

We tested the proposed ELT mechanism using try_touch to measure physical engagement. We used Preacher and Hayes’s PROCESS Model 83 (Hayes 2018) for moderated serial mediation, which combines serial mediation (Model 6) and moderated mediation (Model 7). Following our theory, we used store versus online as the “X variable” moderated by deep versus shallow product (the “W variable”). 12 PROCESS generated estimates and standard errors via bootstrapped sampling with 5,000 iterations. The ELT-based mechanism we propose (deep/store purchase → physical engagement → learning → repatronize retailer) is the “indirect effect” reflecting the mediating role of physical engagement and learning on the relationship between a deep/store purchase and repatronage intentions.

We first conducted several preliminary analyses to demonstrate the value of moderation and mediation. We first regressed store on repatronage, which yielded a significant direct effect (bstore = .273, p = .013). Then, we added the deep/shallow moderator to this model, yielding a significant interaction effect of deep × store (bdeep × store = .472, p = .029) but rendering the main effect of store insignificant (bstore = .031, p = .84; bdeep = .047, p = .76). Similarly, the direct effect of store becomes insignificant once try_touch and learning are added as regressors (bstore = −.143, p = .146; btry_touch = .425, p < .001; blearning = .442, p < .001).

The results of Model 83 regarding moderated serial mediation show that the direct effect of store on repatronage is insignificant (−.143, 95% confidence interval [CI] = [−.336, .0501]). The index of moderated mediation, however, is .188 (95% CI = [.100, .293]), supporting the moderating effect of deep versus shallow product on the impact of the store versus online on repatronage. For the deep product, the conditional indirect effect for store on patronage is .219 (95% CI = [.122, .332]); for the shallow product, it is significantly weaker at .031 (95% CI = [.011, .059]). The results suggest that both the proposed moderation and mediation are at work and that store purchase increases patronage through physical engagement and learning, more so when purchasing a deep product. This confirms H2’s prediction that ELT contributes to the mechanism translating deep/store purchasing into repatronage.

We conducted two robustness checks to reinforce this analysis. First, recall that the deep/store condition stands out and the other three essentially are equal. We therefore created a deep/store dummy variable equal to 1 if the subject was in the deep/store condition and 0 otherwise. Although regressing deep/store on repatronage yields a significant direct effect (b = .524, p < .001), the direct effect becomes insignificant after we account for the proposed mediation. Serial mediation analysis (PROCESS Model 6) yields a significant indirect effect: deep/store → try_touch → learning → repatronage. Details are in Web Appendix W11 (Table W11.3).

Second, we reran Models 83 and 6, switching the order of try_touch and learning, estimating an alternative process: store → learning (moderated by deep product) → try_touch → repatronage for Model 83 and deep/store → learning → try_touch → repatronage for Model 6. While the global model fit and the total indirect effects are unsurprisingly the same across both orderings (Pieters 2017), the indirect effects of serial mediation are quite different. For instance, our proposed ordering yields .1882 (SE = .048) for the deep products’ index of moderated mediation in Model 83; the alternative ordering yields an index of .0138 (SE = .009). Model 6 highlights this difference more saliently. Whereas the proposed ordering yields a serial mediation indirect effect of .1258 (SE = .03), or 30% of the total indirect effect, the alternative ordering yields the serial mediation indirect effect of .0154 (SE = .006), which translates to 3.7% of the total indirect effect. We acknowledge that Pieters (2017, p. 698) cautions against trying to infer the correct mediation order by the aforementioned tests. He advocates that the ordering be based on “strong evidence from logic, theory, and prior research that the hypothesized casual direction is more plausible than indicated alternatives” (Pieters 2017, p. 697). We believe the application of ELT we used to specify the try_touch → learning ordering satisfies this requirement.

In summary, Study 2 replicates Study 1’s finding that the deep/store purchase combination produces the highest repatronage, in support of H1. It also tests the ELT mechanism as proposed by H2. The moderated serial mediation results, and the robustness checks, are consistent with the ELT mechanism.

Study 3: Replicating H3 and Testing Product Generalization (H4)

Study 3 tests our predictions related to generalization of learning. We aim to replicate the HMM’s support for H3, which predicts that purchasing deep products in-store increases the likelihood of purchasing deep products online, compared with purchasing shallow products in-store. Further, this study tests H4, which proposes that the impact of purchasing a specific deep product in-store generalizes to related, adjacent deep products. As noted previously, generalization is an important component of experiential learning and could be very powerful for retailers. It demonstrates the temporal interplay between offline and online channels and suggests that deep/store purchase of a particular product “spills over” to higher likelihood of purchasing adjacent deep products online when the customer repatronizes the retailer.

Method

Study 3 is a two-treatment between-subjects design. The two treatments were deep product/in-store and shallow product/in-store. We randomly assigned 414 participants from Qualtrics Consumer Panel to the two treatments. To ensure that participants were relevant for our context, we asked Qualtrics to screen them based on age (between 20 and 60 years old), household income (minimum of $30,000; 50% of sample needs to have at least $60,000 household income), and e-commerce experience (need to have purchased a product online at least once in the past six months).

We first told subjects that a new sports and outdoor-gear retailer has opened in town. We then asked them to imagine their first shopping trip to this retailer’s physical store, where they purchased either a sport shirt (deep product) or a battery charger (shallow product). We then asked them how likely they would be to purchase each of four products from the retailer’s website in the future. These four products included two deep products, a sport shirt and a sweater (a product adjacent to the shirt), and two shallow products, a battery charger and an activity tracker watch (neither of which are adjacent to a shirt). Finally, as in Study 2, near the end of the study, after the key measures were collected, we asked the respondents to rate the shirt or the battery charger for product inspection depth, depending on their assigned conditions, to enable us to check the deep versus shallow product manipulation. Details of the questionnaire are in Web Appendix W12.

Results and Discussion

Manipulation checks confirmed that the shirt was perceived to be deeper on the four-point product inspection depth scale than the charger (shirt = 2.26 (SE = .09), charger = 1.65 (SE = .07); t(412) = 5.51, p < .01).

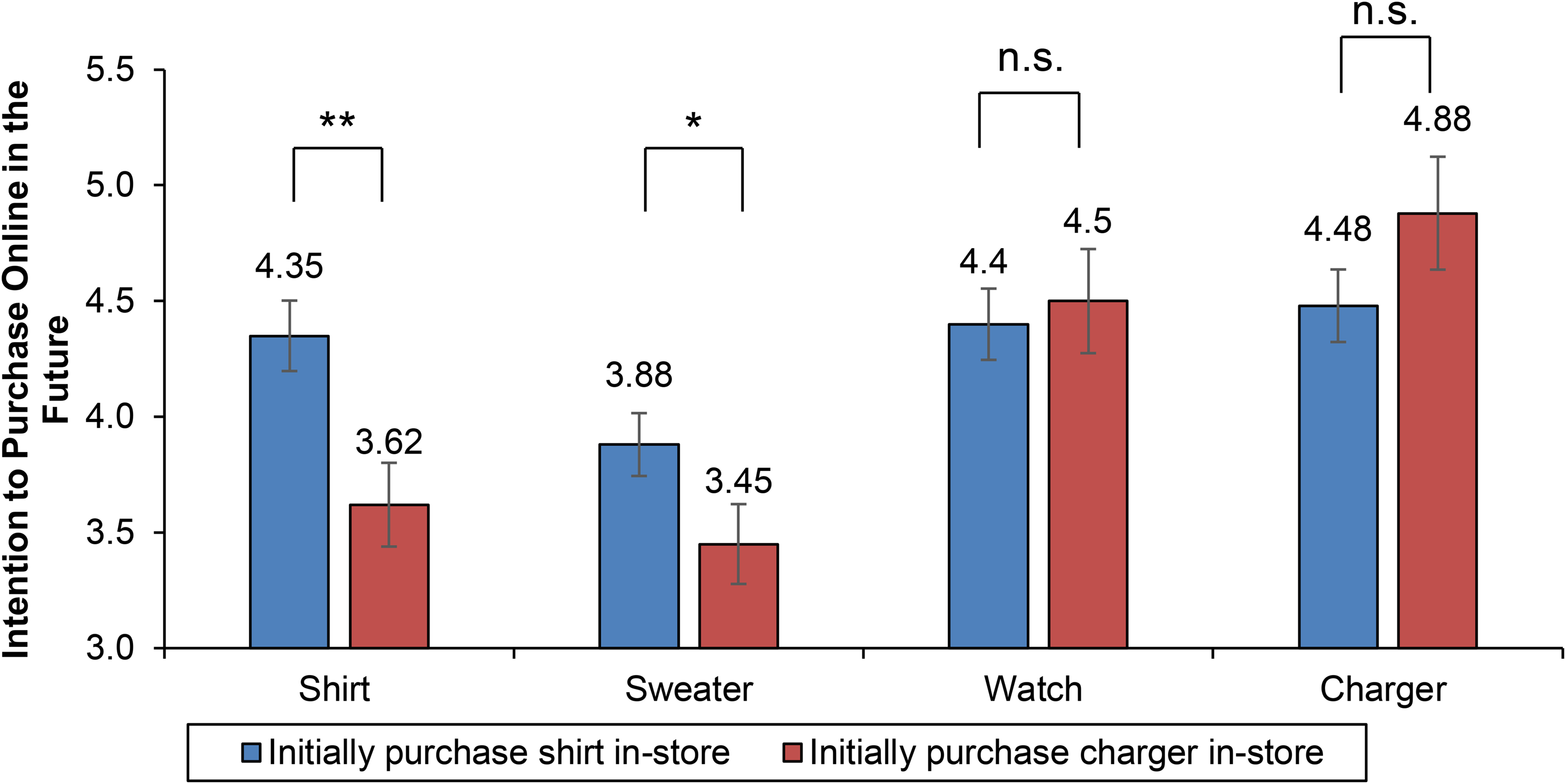

Figure 4 shows that first purchasing a shirt offline increases intentions to subsequently purchase a shirt online, compared with if the first purchase is a charger offline (Moffline_shirt = 4.35, SE = .14 vs. Moffline_charger = 3.62, SE = .13; t(412) = 3.7, p < .01), confirming H3.

The effect of first deep product in-store purchase on future online purchase likelihoods, compared with shallow product purchase (Study 3).

We next tested for spillover. H4 posits that generalization will be to adjacent products. Indeed, the results show that the shirt treatment leads to a higher online purchase likelihood for the adjacent sweater than does the charger treatment (Moffline_shirt = 3.88, SE = .14 vs. Moffline_charger = 3.45, SE = .13; t(412) = 2.3, p < .05). This supports H4. While spillover extends from shirt to sweater, it does not extend to the charger and watch—two shallow, nonadjacent products. The likelihood of buying a charger online next time is nonsignificant between the two treatments (Moffline_shirt = 4.48, SE = .15 vs. Moffline_charger = 4.88, SE = .14; t(412) = −1.9, p > .05). Similarly, the difference between purchasing an activity tracker online subsequently is nonsignificant (Moffline_shirt = 4.4, SE = .14 vs. Moffline_charger = 4.5, SE = .14; t(412) = −.5, p > .05). In conclusion, we have support for H4: buying deep products in-store generalizes to adjacent products. Additional regression analyses corroborate these findings and are in Web Appendix W12.

In summary, Study 3 demonstrates that buying deep products in-store encourages customers subsequently to purchase deep products online more than does buying a shallow product in-store, in support of H3. Furthermore, buying a shirt in-store increases the likelihood of not only buying a shirt online in the future but also buying an adjacent product (a sweater) online. This supports H4. Study 3 overall testifies to the value of ELT as a theory for understanding the impact of deep/store purchases on future customer value.

General Discussion

We set out to study the role of the physical store in today’s multichannel retailing environment. Our thesis was that the physical store increases customer value by providing physical engagement when customers buy deep products. We drew on ELT to formulate four hypotheses: H1 suggests that deep product/in-store purchases increase customer value more than any other product/channel combination. H2 suggests that ELT provides a mechanism that contributes to this effect. H3 posits that customers who purchase deep products in-store are more likely to purchase online from the retailer in the future. H4 proposes that customers will repurchase not only the original deep product but also related, adjacent deep products online. H1 and H2 follow because the store delivers a tangible, concrete, multisensory experience, which facilitates the physical engagement beneficial for buying deep products. This precipitates effective experiential learning. H3 and H4 follow from the generalization phenomenon proposed by ELT.

We evaluated these four hypotheses using an HMM applied to field data (Study 1) and two lab tests (Studies 2 and 3). The results support the following conclusions: (1) purchasing deep products in-store increases future customer value more than any other product/channel combination (H1), (2) the ELT mechanism (deep product/in-store purchases → physical engagement → favorable learning → repatronize the retailer) contributes to this increase (H2), and (3) purchasing deep/in-store increases the likelihood of purchasing the focal and adjacent deep products online in the future (H3 and H4).

Research Implications

Our work has several implications for future research. First, researchers should consider the product/channel combination in studying consumer decisions in a multichannel context. We focus on the physical store and deep products, but the bigger picture is for future research to study product and channel choices together. Not doing so may incur a lost opportunity—the insights in our article would have been diminished if we had focused solely on channel or product.

Second, the product inspection depth concept extends theory regarding product categorizations such as digital versus nondigital by incorporating details related to both physical and visual inspection. We believe this is a valuable concept for studying and comparing products because inspection depth varies appreciably across products, and channels differ in the degree of inspection they can provide. We hope researchers will apply and perfect this concept.

Third, we demonstrate the applicability of ELT to developing customer relationships. This importantly extends the domain to which ELT has been applied. The pivotal role of the customer experience (Verhoef et al. 2009) cannot be understated.

Fourth, our reliance on ELT proved fruitful, but Loewenstein et al. (2001) posit that decision making can be a dual process, drawing on cognitions and feelings. ELT prescribes an involved process of reflection, hypotheses, and repetition, by which consumers form cognitions. ELT does not directly tap feelings. Under this umbrella are concepts such as trust, commitment, affect, and emotions advanced by Pansari and Kumar (2017) and Bowden (2009). These concepts provide additional theories for our results and thus need testing.

Managerial Implications

Study 1’s data are from 2005, yet our findings are in evidence today. The last decade has witnessed a marked increase in the opening of physical stores by online retailers, despite myriad changes in the retailing environment. This attests that our findings are not ephemeral. The general lesson of our research is for retailers to create a concrete, tangible, and multisensory experience for customers buying deep products. This sets the stage for favorable experiential learning and increased customer value. Retailers can do this in numerous ways:

First, when retailers find that a customer is buying online but is decreasing in value, we suggest a promotion for deep products in-store. Our marketing simulations show that there is potential to increase customer value through direct marketing. Second, retailers should facilitate physical engagement for deep products through merchandising and training sales personnel to walk customers through the engagement (e.g., by helping customers try and use deep products in-store). Third, retailers cannot and should not infer product inspection depth solely from predefined product categories, because there is much variation in inspection depth with a particular category. Rather, management should infer inspection depth using our proposed measures or expert, independent judges. Fourth, we recommend retailers use a deep/offline onboarding strategy for new customers. They should use acquisition channels and product promotion strategies that encourage the first purchase to be deep products in-store.

Our general lesson applies to recent developments in retailing. For example, showrooming (Gensler, Neslin, and Verhoef 2017) starts with customers in-store, where the retailer can provide physical engagement. However, the retailer may lose customers who use their smartphones in-store to find the product elsewhere. There are two possible solutions. Retailers can train sales reps to attend to customers buying deep products and equip reps with a mobile device to place orders, or retailers can provide customers with an app to “lock them in.” Interestingly, Van Heerde, Dinner, and Neslin (2019) find that store-oriented customers are good targets for retailer apps. Similarly, “buy online, pickup in-store,” a form of “web-rooming,” can get customers to the store where they can physically engage with additional products to the ones they ordered online.

Our central thesis also has implications for retail loyalty program design and its real-time management. Loyalty programs may be more effective if they provide incentives for customers to shop in-store, such as extra reward points for in-store shopping, particularly when it comes to deep products. These programs need to provide the data, system, and incentives needed to route customers to the physical store when needed, such as when customer value is waning.

Limitations

Our work has limitations that suggest opportunities for future investigation. First, our hypotheses assume that physical stores provide effective physical engagement and favorable experiential learning. Our results could have turned out differently if our focal retailer’s stores did not provide satisfactory experiences. This meant that our hypotheses were nontrivial and falsifiable, and future work should investigate the store features that best provide physical engagement. Second, we could not observe and thus could not incorporate customers’ category expertise or preference evolution due to product consumption. Two customers who bought similar tents could have different camping experiences, which would partially determine future purchases that are outside of the firm’s control. Third, with transactional data typical in customer relationship management research, we assumed that customers make channel and product decisions jointly. Future work using more granular data could examine the sequence of channel and product choices and explore situations such as planned versus serendipitous purchases. Fourth, we do not know exactly when a customer makes the decision of what and where to purchase. A shopping list study would be useful for future research. Finally, our observational data were from one retailer—a specialist in outdoor products. Future work should consider other product categories.

Future Directions

Guided by our mantra to create physical engagement to enhance customer value, we next discuss additional fertile areas for research.

Store or showroom?

Is the traditional physical store, with its requisite square footage and inventory, the best way to sell deep products? As fulfillment logistics have gotten faster, more orders can be placed via in-store kiosks and staff-assisted online ordering and can be fulfilled quickly. This suggests stores do not need to allocate a large space for inventory and can use that real estate to help convert the physical store to a showroom. The question is which is best—physical store or showroom?—in terms of customer preferences and the financials.

Full or limited assortment?

As the physical store’s value lies in facilitating physical engagement through deep products, stores may not need to carry a large assortment (not all sizes and not all colors). The counterargument is that stores should carry a broad assortment because customers might want to physically engage with specific sizes/colors. Future research should study and resolve this tension.

Full or limited staff?

A trained and empathetic sales team would play a key role in delivering physical engagement to the customer. We noted this in discussing showrooming, where the sales rep was needed to keep the customer “on course” with the retailer. Kumar and Pansari (2016) also delineate an important role for staff in developing customer value. This would suggest full staffing of physical stores (see Gensler, Neslin, and Verhoef 2017). However, this strategy is expensive, and customers may be quite capable of physically engaging on their own.

The role of private label

As noted in formulating H1, we assume the favorable learning the customer gains from physical engagement transfer to the store. One way the retailer might ensure this is to emphasize its private label. Nordstrom, L.L.Bean, and Warby Parker are good examples.

Leveraging technology to create physical engagement

Physical engagement is a particular challenge for online retailers. What combination of videos, chat, user testimonials, virtual reality, augmented reality, and other interactive features should be deployed to mimic in-store physical engagement?

Although the current state of augmented reality technology is probably not realistic enough to fully capture physical engagement (Conger 2020), future work could examine how this technology can satisfactorily do so for certain product categories, consumption contexts, and consumer segments.

One recent notable example is the virtual tasting experiences offered by Wine.com, an online wine retailer. This program encourages customers to order a featured wine ahead of time, then go online and, either live or via recorded videos, taste the featured wine alongside its winemaker or renowned critics such as Steven Spurrier. This program not only can result in immediate sales of the featured wines and fills the vacuum created by the closure of physical tasting rooms during COVID-19 but, according to our theory, also has the potential to facilitate sensory engagement (in this case, visual, audio, taste, and smell). Research could investigate whether such creative digital efforts can translate into long-term loyalty towards the online retailer.

Identifying physical engagement-prone customers

Retailers might consider updating their customer segmentation schemes to reflect customers’ needs for physical engagement. Peck and Childers (2003a) show that the need for haptic (touch) experiences is an individual trait. An interesting line of future research is to investigate whether this trait evolves over time and what drives this evolution. Retailers could thus explore ways to identify physical engagement-prone customers and design their stores and websites accordingly.

Other forms of physical engagement

Retailers may want to explore other avenues to physically engage customers in-store, such as through cultural events or prosocial efforts. For example, they may celebrate ethnic holidays and dedicate a certain percentage of sales to charitable causes. Can these be turned into forms of physical engagement? A retailer can advertise online its efforts to fight COVID-19, but it can also demonstrate in-store the personal protective equipment its donations buy for the community. Future work could investigate whether these various in-store efforts generate customer interactions and affect that enhance customer value.

These speculations, along with the more direct implications stated previously, demonstrate the richness of marching to a simple yet powerful message: Retailers can increase customer value by providing physical engagement when selling deep products. We hope both researchers and practitioners will leverage this message in future work.

Footnotes

Acknowledgments

The authors thank the Editor, Associate Editor, and reviewers for their constructive, insightful suggestions. They are grateful to the retail chain for providing the data and managerial support. They also thank Tom Meyvis (NYU), Mari Romero (Colorado State University), and seminar participants at KU Leuven, Cheung Kong Graduate School of Business, Indiana University, HEC Paris, NYU, Southern Methodist University, Renmin University, the University of Miami, and the University of Washington for their comments.

Associate Editor

David Schweidel

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.