Abstract

This article investigates the existence and extent of a gender gap in satisfaction with the Bank of England’s performance in controlling inflation. Descriptive data and previous research report gender gaps in attitudes towards monetary institutions and outcomes. Much of this research, however, disregards potential biases arising from women’s lower propensity to express an opinion, and to answer ‘don’t know’ instead. Using the Bank of England’s Inflation Attitudes survey (2001–2025), and modelling selection into substantive answers, I find a statistically significant – yet, substantively small and not persistent – gender gap in satisfaction with the Bank of England. This gender gap remains after controlling for inflation perception and monetary knowledge. I also find that women do not overestimate inflation, and they do not seem to ‘punish’ more harshly the Bank for high inflation or deflation. Therefore, variance in this gender gap can be attributed to a different propensity to report ‘extreme’ opinions, and to different reactions to high inflation or deflation. These findings highlight gendered dimensions for the understanding of monetary institutions and finance, contributing to the literature on satisfaction with the performance of institutions.

Introduction

Globally, independent central banks are facing a legitimacy crisis (Bateman and van ‘t Klooster, 2024; Bergbauer et al., 2020; Roth et al., 2014). Many politicians and scholars question the extent of central banks’ powers, and the timing and wisdom of their decisions (Bianchi et al., 2023; Binder, 2021; Bodea and Garriga, 2024; van ’t Klooster and Fontan, 2020). In addition, citizens report increasing levels of distrust and dissatisfaction with central banks (Ehrmann et al., 2013; Garriga, 2025), which could further undermine the legitimacy of these institutions.

Research on citizens’ attitudes often finds a gender gap in public satisfaction or confidence in central banks: women report lower trust in and satisfaction with central banks than men (Blanchflower and MacCoille, 2009; Brouwer and de Haan, 2022; Ehrmann et al., 2013; Niţoi and Pochea, 2024; van der Cruijsen and Samarina, 2023). This is consistent with more general findings regarding gendered attitudes towards inflation and monetary policy. Much of this research, however, disregards the fact that women tend to be less likely than men to express an opinion – that is, they are more likely to select the ‘do not know’ option – which may bias the results and affect the interpretations (Hansen and Goenaga, 2024). Is there a gender gap in attitudes towards central banks?

This article analyses the existence and extent of a gender gap in satisfaction with the Bank of England’s performance in controlling inflation. Although descriptive data and some studies find a gender gap in attitudes towards central banks, there are conflicting findings regarding its extent and direction even for the case of the Bank of England. 1 I suspect that these differences may result from selection bias. Therefore, to assess the extent of gender differences in satisfaction, I first examine whether the reported gender gap in satisfaction with the Bank’s performance is influenced by a different propensity to express a substantive opinion and to express more extreme evaluations about the Bank’s performance. In addition, I empirically examine two channels that, according to the literature, may explain gendered differences in satisfaction with the Bank. First, women may overestimate inflation and believe that the central bank is not doing a good job at controlling prices. Second, women may suffer more directly the consequences of inflation, and thus ‘punish’ more harshly (via negative evaluations) than men central banks’ failure to achieve their inflation target. Although these channels have been explored in the literature, methodological reasons suggest the need to account better for selection into providing an answer before analysing the resulting sample.

I test these explanations using quarterly data from the Inflation Attitudes survey (2001–2025), published by the Bank of England. This survey directly asks respondents about their satisfaction with the central bank in performing the task of controlling inflation – and not merely trust or overall satisfaction – using the same phrasing to a representative sample of respondents. The temporal coverage allows users to disentangle the effect of ‘atypical’ years. I first deal with potential selection issues that may affect answers used in this article. The results suggest that, although there are gendered differences in attitudes to monetary policy and outcomes, the extent – and even existence and direction – of a gender gap is affected by a different propensity to express opinions and strong opinions between men and women. I find that women are less likely to express opinions and more extreme opinions – i.e. ‘very’ (dis)satisfied – than men, and to report lower perceived inflation. Failing to account for this selection effect introduces important biases in the estimations. Second, I show that there is a gender gap in satisfaction with the Bank of England’s performance that goes beyond standing explanations regarding gendered differences in inflation perception and financial literacy. This gender gap is less pronounced and less prevalent through time than previously assumed – characterizing 16 years (64%) in the sample. Furthermore, when respondents perceive high inflation or disinflation, the gender gap disappears.

These findings are important for the study of monetary institutions, finance and beyond, contributing to the literature on satisfaction with, and potentially trust in, institutions, and the extent of gender gaps in public opinion. Understanding the determinants of satisfaction with political institutions and public policy, in general, is important for several reasons. First, citizens’ satisfaction indicates a positive evaluation of the performance of institutions vis-à-vis their expected role (Footman et al., 2013; Kelly, 2002; Van de Walle, 2018). Both from utilitarian and normative perspectives, public management scholars emphasize the importance of maximizing satisfaction with public services and institutions (Van Ryzin, 2007). Second, several scholars connect perceived competence with trust in institutions (de Blok et al., 2022; Christensen and Lægreid, 2005; Dahlberg and Linde, 2018; Levi and Stoker, 2000; Mishler and Rose, 2001; Torcal, 2014; Zhang et al., 2022) and even more broadly, with the government or democracy (Bouckaert and van de Walle, 2003; Norris, 1999; Weitz-Shapiro, 2008). 2 This article’s findings contribute to the literature analysing gendered evaluations of political actors and institutions (Schneider and Bos, 2019), adding evidence to discussions around the interpretation of substantive answers in the presence of extreme options, and prevalence of ‘do not know’ responses (Goenaga and Hansen, 2022; Hansen and Goenaga, 2024; Lizotte and Sidman, 2009; Luskin and Bullock, 2011; Sturgis et al., 2008).

Understanding the correlates of satisfaction with monetary authorities, in particular, is key for central banks. Satisfaction is regularly used as an indicator of public confidence in central banks among academics (Bergbauer et al., 2020; Brouwer and de Haan, 2022; Ehrmann et al., 2013; Garriga, 2025; Kaltenhaler et al., 2010), practitioners and specialized press. 3 Negative views and dissatisfaction regarding independent central banks’ performance not only threaten their legitimacy (Baerg and Cross, 2022; Binder, 2021; Burgoon et al., 2012; DiGiuseppe et al., 2025a; Jones, 2009), but they are also likely to translate in low confidence in central banks’ policies. Given that monetary policy hinges on the ability to anchor inflation expectations, low confidence in central banks may challenge the effectiveness of monetary policy (Blinder et al., 2008; Christelis et al., 2020; Coibion et al., 2020; De Haan and Sturm, 2019) and increase central banks’ exposure to politicization (Binder, 2021; Bodea and Garriga, 2023). This reasoning has led central banks to work on their communications and try to regain public support (Blinder et al., 2008; Ehrmann et al., 2013; Goutsmedt and Fontan, 2024).

Importantly, this article contributes to growing research on the gendered nature of finance (Clarke and Roberts, 2016; Nallari and Griffith, 2011), that challenges the ‘strategic silence’ about gender in financial institutions, including central banks (Bakker, 1994; Young et al., 2011). From a policy design standpoint, disentangling the factors that may contribute to a gender gap in satisfaction is important because they suggest different communicational strategies to increase satisfaction with the institution (Bholat et al., 2019; Blanden, 2024; Clarke and Roberts, 2016; McMahon and Reiche, 2025), and may contribute to central banks’ efforts to anchor inflation expectations (Baerg et al., 2025; Blinder et al., 2024). Furthermore, these findings may inform communicational strategies to increase satisfaction with public institutions beyond central banks (Amin and Ritonga, 2022; Christensen and Lægreid, 2005; Ho and Cho, 2017; Lewis and Pattinasarany, 2009; Luoma-aho et al., 2020).

The rest of the article proceeds as follows. The next section briefly reviews the literature on gendered views on monetary policy and outcomes. Section ‘What Women (Really) Think’ presents the hypotheses to be tested, the following sections describe the data and methods, and present and discuss the findings. The last section concludes and describes avenues for future research.

Gendered Views on Monetary Policy and Outcomes

Research on citizens’ attitudes often finds a gender gap in public satisfaction or confidence in central banks. For example, both aggregate and individual level data suggest that women report lower trust in the European Central Bank (ECB) (Brouwer and de Haan, 2022; Bursian and Fürth, 2015; Ehrmann et al., 2013; Kaltenhaler et al., 2010; van der Cruijsen and Samarina, 2023). Other work shows similar results regarding satisfaction with the Bank of England (Blanchflower and MacCoille, 2009; Garriga, 2025). 4 These findings map on broader studies regarding attitudes toward monetary institutions (Banducci et al., 2003; Farvaque et al., 2017; Favaro et al., 2023; Hayat and Farvaque, 2012). Yet, there is little research regarding what could explain this gender gap.

The literature suggests there are gendered views on important issues regarding monetary policy and outcomes. Two consistent findings are relevant for this article. First, a significant literature suggests that women perceive higher inflation than men (Armantier et al., 2016; Blanchflower and MacCoille, 2009; Bryan and Venkatu, 2001; Coleman and Nautz, 2023; Detmeister et al., 2016; Jonung, 1981). There are several explanations for this gender gap in perceived inflation. Some highlight that women have biased inflation expectations because of insufficient information (Bruine de Bruin et al., 2011; Corduas, 2022) and lower levels of financial literacy (Bucher-Koenen et al., 2017). Other stress differential exposure to inflation: women tend to engage more in grocery shopping, which exposes them more to price volatility than men (D’Acunto et al., 2021), and women are more likely to spontaneously think about prices of specific goods (Bruine de Bruin et al., 2011). Reiche (2024) combines these explanations and shows that shopping behaviour alters inflation expectations but only among low-financial literacy women. Other studies find that men have a higher probability of correctly reporting level and changes in the official inflation rate (Blanchflower and MacCoille, 2009), and that men tend to make smaller errors in their inflation forecasts (Ehrmann et al., 2017).

Second, research consistently finds that women have lower levels of financial literacy (Angino et al., 2022; Armantier et al., 2015; Bucher-Koenen et al., 2017; Haag and Brahm, 2025; Lusardi and Mitchell, 2008, 2023; McMahon and Reiche, 2025). In particular, studies find ‘significant differences in the number of correct answers and ‘Don’t know/Refused’ responses to basic financial questions between women and men’ (Aristei and Gallo, 2022). The roots of gender differences in financial literacy seem to exceed education and numeracy skills (Cupák et al., 2018; Fonseca et al., 2012). More recently, however, some researchers have questioned a tool generally used to proxy literacy for this widespread finding: Many studies use the answer ‘Do not know’ to indicate lack of knowledge. However, the determinants of, and behaviour associated with, incorrect and ‘Do not know’ answers to financial literacy questions seem to differ (Aristei et al., 2025; Cucinelli and Soana, 2023). Furthermore, there might be systematic reasons for why women choose the ‘Do not know’ answer more often than men – for example, many attribute this gap to underlying traits related to gender stereotyping (Ferrin et al., 2022) self-confidence (Bucher-Koenen et al., 2021; Coffman, 2014; Hansen and Goenaga, 2024; Wolak, 2020), higher uncertainty (McMahon and Reiche, 2025), dissatisfaction with the political system (Goenaga and Hansen, 2022), or a mere artefact of the ways in which knowledge is measured (Dolan, 2011; Ferrin et al., 2018; Frazer and Macdonald, 2003; Kraft, 2024; Mondak and Anderson, 2004).

Therefore, the use of the ‘Do not know’ answer may artificially increase the reports of a gender gap in financial literacy (Bucher-Koenen et al., 2021; Conte et al., 2024), as research shows regarding political knowledge (Fortin-Rittberger, 2016; Lizotte and Sidman, 2009; Luskin and Bullock, 2011; Miller, 2019; Mondak and Anderson, 2004; Tsai, 2023). 5 This research suggests the need to revisit the findings in the literature summarized above – that is, to what extent the gender gap found in inflation perception and in financial literacy is sensitive to selection processes affecting the likelihood of providing an answer (instead of ‘Do not know’).

Both factors – inflation perception and financial literacy – are important for the analysis of central banks’ performance evaluation and for trust in central banks (Garriga, 2025; Niţoi and Pochea, 2024). Regarding inflation, there is evidence that those who perceive higher levels of inflation also tend to have lower trust in the ECB (Hayo and Méon, 2024; van der Cruijsen et al., 2025) or the Federal Reserve (Binder and Skinner, 2023; DiGiuseppe et al., 2025a). This finding is confirmed in experimental settings (Dräger and Nghiem, 2023). Therefore, if women perceive inflation to be higher than it is, they may reach the conclusion that the central bank is not doing a good job at controlling prices and thus, express less satisfaction with the Bank’s performance.

Regarding financially literacy, evidence suggests that knowledge about the European and New Zealand’s central banks (Hayo and Neuenkirch, 2014; Hayo and Neumeier, 2020) seem to foster citizens’ trust. In fact, Hayo and Neuenkirch (2014) find that specific knowledge about the ECB is more important than general monetary policy literacy to explain trust in the institution. Dräger and Nghiem (2023) find that a literacy treatment ‘improves respondents’ comprehension about monetary policy and inflation’ and increases their reported trust in the central bank. This positive correlation between knowledge and trust seems especially strong during the Global Financial Crisis (Ehrmann et al., 2013).

Overall, the literature suggests that gaps in inflation perception and in monetary knowledge may explain gendered differences in satisfaction with the central bank. It is not clear, however, whether there are gendered differences in satisfaction with monetary institutions beyond inflation perception and financial literacy. The literature also suggests that a different propensity in expressing substantive opinions on monetary matters may have an effect even on accurately assessing financial literacy. The effect of this differential propensity to provide substantive answers on other variables is yet underexplored.

What Women (Really) Think

This article investigates the existence and extent of a gender gap in satisfaction with the Bank of England’s performance in controlling inflation. Although the literature and descriptive accounts show different levels of satisfaction between men and women, I argue that the magnitude of this gender gap has been overstated as a consequence of disregarding men’s and women’s different propensity to express an opinion. This insight, discussed above regarding financial literacy, is likely to exceed knowledge questions, as shown in a broader literature on political behaviour (Berinsky, 2002; Goenaga and Hansen, 2022; Hansen and Goenaga, 2024). If women are more likely to select the ‘Do not know’ option, and the correlates of this choice overlap with the correlates of satisfaction, this may bias the results (Berinsky, 1999).

I therefore expect the gender gap in satisfaction with the Bank of England to be affected once the propensity to manifest an opinion is taken into account – that is, when the ‘Do not know’ responses are not just considered missing data or indifference for the satisfaction question. Therefore, the first set of hypotheses this article tests is the following:

H1a. There is a gender gap in performance evaluation of the Bank of England.

H1b. The gender gap in performance evaluation is affected by a differential propensity to manifest an opinion on the Bank of England’s performance.

Second, if women are less likely to manifest a substantive opinion, it is likely that when they do provide an evaluation, they are more likely to manifest less extreme opinions than men. Women’s lower likelihood to select ‘extreme’ opinions than men – that is, a lower propensity to select the ‘strongly agree/strongly disagree’ options, and responding instead ‘agree/disagree’ – has been documented in other fields (Bunting et al., 2021; Hansen and Goenaga, 2024; Peterson et al., 2014), even among highly educated female economists and political scientists (Entringer García Blanes et al., 2025; Sarsons and Xu, 2021). However, the evidence on the link between gender and extreme responses is mixed (Batchelor and Miao, 2016; Greenleaf, 1992).

A different propensity to choose extreme answers can be a result of differences in self-confidence, given reported overconfidence among male respondents (Barber and Odean, 2001; Exley and Nielsen, 2024; Moore and Healy, 2008; van Veldhuizen, 2022), or higher uncertainty (McMahon and Reiche, 2025). If that is the case, the observed gender gap in descriptive data may be affected by women’s reluctancy to express an evaluation – and thus, choosing the ‘Neither satisfied nor dissatisfied’ option – than by their negative views of performance. I expect this gender gap to be present even after accounting for a differential propensity to manifest an opinion on performance. This expectation is consistent with Sarsons and Xu’s (2021) findings among female economists working in top universities, and among international relations scholars (Entringer García Blanes et al., 2025).

H2a. Women are less likely to express extreme evaluations about the performance of the Bank of England.

H2b. The gender gap in expressing extreme evaluations is affected by a differential propensity to manifest an opinion on the Bank of England’s performance.

In addition, I test two hypotheses to explore channels that, according to the literature, may explain gendered differences in satisfaction with the Bank. First, it is possible that women overestimate inflation. An erroneous perception of inflation may drive lower levels of satisfaction that we observe in the aggregate descriptive data. However, based on the discussion above, selection issues may affect previous estimations of women’s inflation perception. I hypothesize that the previously observed gender gap in inflation perception is affected by the propensity to provide substantive answers.

H3a. Women estimate higher inflation than men.

H3b. This gender gap is affected by a differential propensity to provide a substantive answer regarding the current level of inflation.

Second, and independently from women’s perceptions of the level of inflation, women may ‘punish’ more harshly the central bank for poor performance in controlling inflation, and thus, show higher dissatisfaction than men when inflation is higher. This expectation is consistent with two findings in the literature: first, important research shows that monetary policy has gendered effects (Braunstein and Heintz, 2008; Chundakkadan, 2023; Couto and Brenck, 2024; Young, 2018). 6 Second, other research suggest that women may be more conservative regarding inflation preferences – see for example research showing that female central bankers are more conservative than male in similar positions (Diouf and Pépin, 2017). Therefore, I test the following hypothesis:

H4: The gender gap in satisfaction with the Bank of England’s performance is conditional on perceived inflation.

Data and Methods

The data for this article come from the Inflation Attitudes survey, conducted by the Bank of England across the United Kingdom. It includes quarterly surveys (2001–2025) 7 on a quota sample of residents between 15 and 75 years old. Except for the questions regarding monetary literacy, the other questions used in this article have been asked in all quarters.

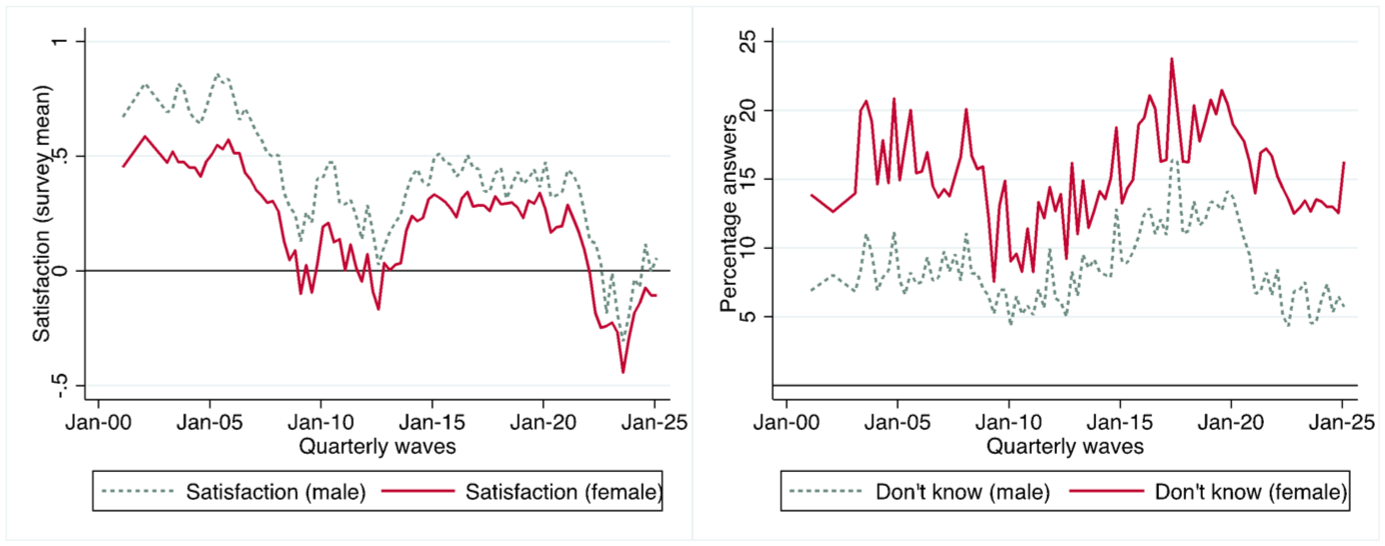

For the first hypotheses, the dependent variable is Satisfaction and is built from the answers to the question ‘Overall, how satisfied or dissatisfied are you with the way the Bank of England is doing its job to set interest rates in order to control inflation?’ These answers are ordered from -2 (very dissatisfied) to 2 (very satisfied). ‘Neither satisfied nor dissatisfied’ is coded 0. A sixth option, ‘No idea’, 8 is coded as missing in the five-category ordered variable. In the full sample, this variable’s mean is 0.28 and its median is zero. The left-side panel in Figure 1 plots the sample mean per survey wave of Satisfaction, by gender. To test the second set of hypotheses, I use the absolute value of Satisfaction. Satisfaction (absolute) ranges from 0 ( ‘Neither satisfied nor dissatisfied’) to 2 ( ‘Very dissatisfied’ or ‘Very satisfied’).

Satisfaction With the Bank of England’s Performance Average Sample (Left) and Rate of ‘Do Not Know’ (Right), by Gender. Quarterly Data.

Out of 240,133 respondents, 28,763 individuals (11.98%) answered ‘Do not know’ to the question about satisfaction. 9 The share of respondents choosing the ‘Do not know’ option varies by gender and is systematically higher among women (15.11%) than men (8.45%). The average gap between these figures is 6.8 percent points, and ranges between 2.4 and 11.8 percent points (excluding the May 2020 wave, when this option was not included). The right-side panel in Figure 1 plots the percentage of respondents who chose this option, by gender and wave. The ‘Do not know/No idea’ answer, coded as missing, is the basis for the selection models.

The main independent variable is Female. It is coded 1 if the answer to Sex is female, and zero otherwise. Of note, the variable Sex has four alternative answers for self-identification (female, male, in another way, prefer not to answer). The survey included the non-binary options in 2022, with further changes in 2023. 10 To maintain male as a consistent baseline category, I recoded the non-binary options as Other/NA.

Inflation perception is the response to a series of questions asking, ‘Which of these options best describes how prices have changed over the last 12 months?’ Answers are constrained to set options, varying by one percent-point interval. Of note, respondents do not have a choice below -6% or above 16%, which constrains the answers. Therefore, the Bank reports perceptions middle of bucket (-5.5 to +15.5 scale). 13.3% of respondents answered ‘No idea’ to this question.

Knowledge reports correct answers to questions asking to identify who sets the interest rate, and what is the degree of independence of the Monetary Policy Committee from the government, following Garriga (2025). See Supplemental Appendix 2 for coding. These questions were asked only in the first quarter of each year, except for 2010, when it was asked in all quarters.

I control for all demographic variables included in the surveys. Age classifies respondents in 10-year groups (from 15 to 24 years, to 65 years and up). I recode this variable as a series of dichotomous variables, and include the discrete variable, ranging from 0 to 5, in selection models. Class codes social grade. 11 It is included as a set of dichotomous variables per category, and as a categorical variable (0 = DE, 1 = C2, 2 = C1, 3 = AB) in the selection models. Education is a ordinal variable ranging from 0 (low, GCSE), to 2 (high, degree). Working is coded 1 for those working full- of part-time, and zero otherwise. To control for housing tenure, I include two dichotomous variables: Owner and mortgage holder (Mortgage). The excluded category includes those renting from the council and people letting or living in other people’s houses. Models also include a set of dummy variables identifying five regions (Scotland, North & NI, Midlands, Wales and West, and South-East used as the baseline) and the wave of the survey. Finally, selection equations include Inflation (observed), the consumer price index (CPI inflation) in the 12 months prior to the survey. Data come from the Office of National Statistics. Descriptive statistics for the full sample (Table A3.1) and for the first quarter-only sample (Table A3.2) are in Supplemental Appendix.

I estimate one-stage (pooled ordinary least squares (OLS) and ordinal probit) and two-stage (Heckman OLS and Heckman ordinal probit) regressions using the survey weights to make the sample UK-representative. For the selection models, I include gender self-identification, education and class as categorical variables, employment, age, and the observed inflation in the quarter of the survey.

Findings

Gender and Satisfaction the Bank’s Performance

Table 1 shows the estimates of multivariate analyses of the effect of gender on satisfaction with the Bank of England’s performance. Given that these models include a control for Knowledge, the analysis is based on pooled surveys conducted the first quarter of each year. 12

Gender and Satisfaction With the Bank of England.

Year-fixed effects not reported.

Standard errors in parentheses ***p < 0.01, **p < 0.05.

The estimates of a pooled one-stage OLS regression (column 1) suggest the existence of a gender gap in satisfaction with the performance of the Bank of England even after controlling for perceived inflation and knowledge about monetary policy (about 9.5% of a standard deviation in Satisfaction). Columns 2 and 3 show the estimates of the Heckman selection models. A positive and statistically significant transformed rho suggests that it is necessary to correct for sample selection because respondents who are more likely to be selected are also likely to report more satisfaction, suggesting the need to model the selection to produce less biased and more efficient coefficients. This provides support for hypothesis 1b.

Consistent with the literature, the first stage of the selection model (column 3) indicates that women are significantly less likely than men to express an opinion regarding the Bank of England’s performance. 13 This provides support for hypothesis 1b. Several other factors associated with higher satisfaction are also significantly associated with expressing a substantive opinion instead of selecting the ‘Do not know’ option: Education, Class, working part- or full-time, and age are positively associated with both outcomes. At higher level of observed inflation, respondents are more likely to provide an answer. 14

Once accounting for selection (column 2), the gender gap persists, providing support for hypothesis 1a. This coefficient suggests a slightly larger difference between men’s and women’s satisfaction than in column 1. Substantively, the gender gap represents about 11% of a standard deviation in Satisfaction. Other factors associated with higher Satisfaction are knowledge about the Bank of England, having a degree, class status, working part- of full-time, housing tenure and age. There are regional differences regarding overall satisfaction: respondents in the South-East of the country (the omitted category) express mores satisfaction than respondents in other regions, particularly in Scotland and Wales.

Although models in Table 1 include year-fixed effects, I further test whether this apparent gender gap is a persistent phenomenon or the artefact of some years/survey waves. I re-estimate these models in each survey. 15 The left-side panel in Figure 2 shows that, although the estimates for Female are generally negative, they are not consistently statistically significant. Between 2001 and 2025, the difference in satisfaction between female and male respondent was statistically significant only in 16 years – that is, 64% of the surveys reveal a gender gap. The coefficient for Female does not achieve statistical significance in 2001, 2003, 2006, 2015–2016, and after 2021. The largest gap is in 2011 (0.23), followed by 2005 and 2004 (0.22 and 0.19, respectively).

Gender Gap in Satisfaction With the Bank of England’s Performance. Estimates From Non-Pooled Data.

The non-pooled regressions show additional evidence regarding hypotheses 1a and 1b. The estimates for Female in the pooled sample (columns 1 and 2, Table 1) look quite similar in magnitude. In fact, a simple comparison of the estimates suggests that holding other things constant, after accounting for selection the gender gap is larger than the one revealed in simple OLS regressions. However, the importance of modelling selection into substantive answers becomes more evident when comparing the estimates from each year. The right-side panel shows the estimates for Female produced by OLS regressions on each wave. Results that do not model selection into substantive responses suggest that a gender gap in Satisfaction is far more prevalent through time: in these models, the coefficient for Female is always negative and achieves statistical significance in all but 3 years (2015, 2022 and 2025).

Altogether, these results provide support for the first set of hypotheses: controlling for a host of factors, including inflation perception and knowledge about the Bank of England, women generally express lower levels of satisfaction with the Bank. This result, however, is generally overestimated if selection into substantive answers is not taken into account, and does not seem to be persistent across time.

Gender and ‘Extreme’ Evaluations

The second set of hypotheses expected women to be less likely to express ‘extreme’ evaluations about the performance of the Bank of England. Columns 4 and 5 show the two stages of ordered probit selection models estimating the likelihood of providing stronger opinions regarding satisfaction with the Bank. 16 The dependent variable ranges from zero (neither satisfied nor dissatisfied) to 2 (very satisfied/very dissatisfied). The positive and statistically significant rho indicates that in these models too, selection matters: respondents who are more likely to be provide a substantive answer are also likely to report stronger opinions regarding satisfaction.

The negative coefficient associated with Female suggests that women are less likely to express more intense satisfaction/dissatisfaction. Given that ordered probit coefficients cannot be directly interpreted, Figure 3 shows the difference in the probability of each of the three outcomes between men and women when all other variables are held at their median and the non-binary option held at zero. 17

Absolute Satisfaction With the Bank of England’s Performance, by Gender.

Women are more likely than men to select the ‘Neither satisfied nor dissatisfied’ option (Predicted margins = 0.43 and 0.34, respectively). In contrast, they are less likely to express satisfaction or dissatisfaction (Predicted margins = 0.49 and 0.54), and to choose the more ‘extreme’ answers (Predicted margins = 0.08 and 0.12, respectively). All these gender differences are statistically significant. This provides support for hypothesis 2a. A comparison of the predictive margins obtained with and without modelling the selection shows also support for hypothesis 2b. Although the magnitude of the bias is very small (between 0.2% and 1.7%), margins estimated after a one-stage ordinal probit underestimate the probability or women selecting the ‘neither satisfied or…’ option, and incrementally overestimate the probability for women choosing the other two options.

Gender, Inflation Perception, and Satisfaction With the Bank

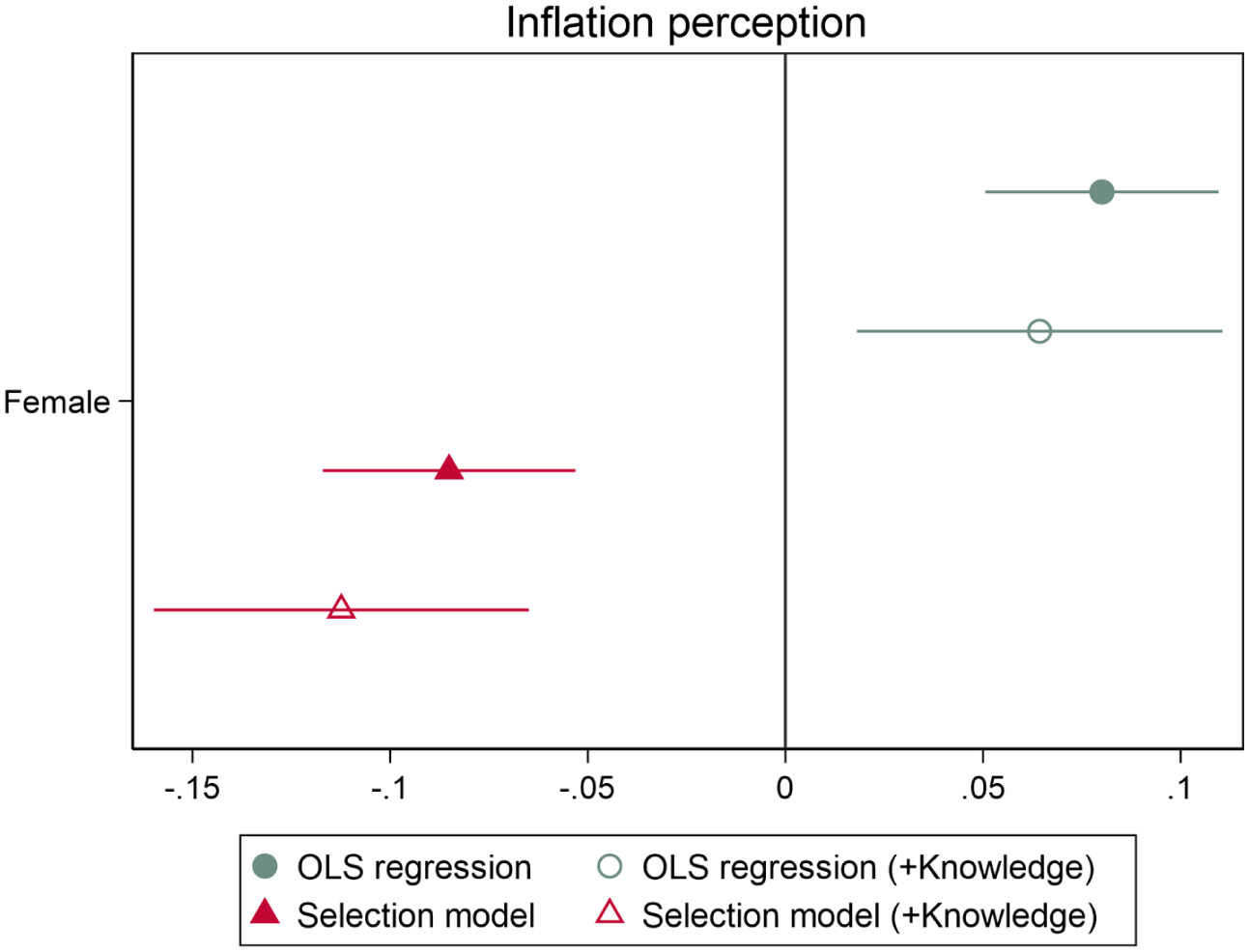

The last hypotheses explore whether gender conditions inflation perception and the effect of inflation perception on satisfaction with the Bank. To test hypotheses 3a and 3b, I estimate two sets of models, excluding and including a control for monetary knowledge, a variable that significantly reduces the sample size (full table in Table A4.5 in Supplemental Appendix).

A simple OLS seems to provide support for the literature stating that women provide higher estimates of inflation than men, although by a small margin (between 0.06 and 0.08 percentage points). However, results from the selection estimations present a very different picture. 18 After modelling selection, the coefficient associated with Female is statistically significant but negative, suggesting that women perceive lower inflation than men. The magnitude of this coefficient is between -0.09 and -0.11 percentage points, depending on the inclusion of Knowledge the models. Figure 4 shows the estimates for Female from one- and two-stage OLS models, excluding and including a control for Knowledge. 19 Controlling for Knowledge, and after modelling selection into providing an estimate of inflation, women on average estimate inflation to be 0.11 lower than men. 20

Inflation Perception. Comparison of Coefficients in One- and Two-Stage Regressions, Including and Excluding a Control for Monetary Knowledge.

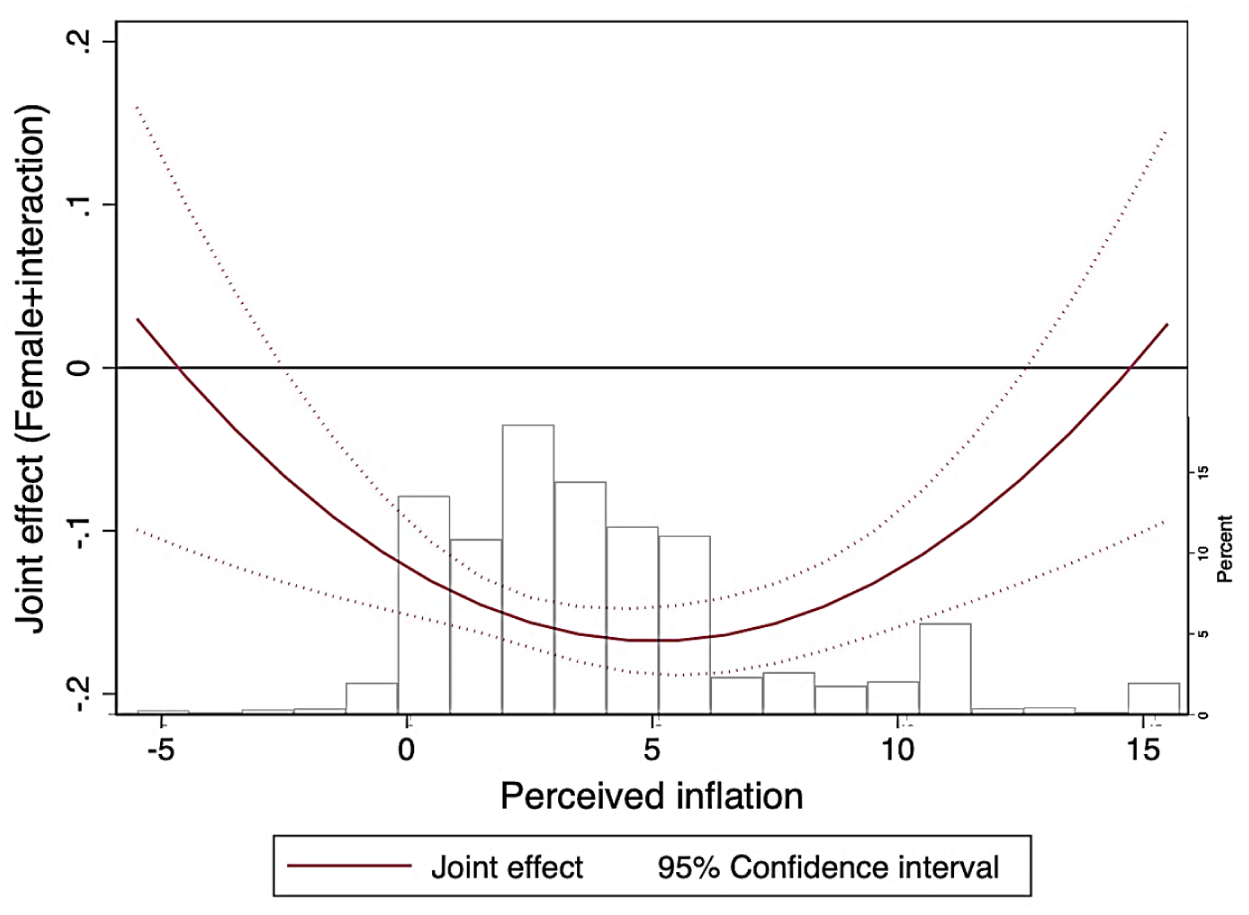

Finally, I test whether there is a gender gap in reaction to perceived inflation that gets reflected on satisfaction with the Bank of England’s performance controlling inflation. Figure 5 presents the estimates for Female at different levels of perceived inflation. Assuming that the reaction to inflation is not linear because of periods in which perceived deflation may have affected satisfaction negatively, the model includes interactions with Perceived inflation and its squared term (full model in Table A4.7 in Supplemental Appendix). Results indicate that there is a significant gender gap in satisfaction when perceived inflation ranges between -2.5% and 13%, but not in the extreme values of the distribution. It is possible that the different propensity to express ‘extreme’ (dis)satisfaction across genders has a ‘ceiling’: once individuals perceive (relatively) extreme levels of inflation/deflation, where the Bank of England seems to be very far away from their inflation target, women are less hesitant in expressing extreme views, and this blurs gender differences. Women tend to report more dissatisfaction at higher levels of inflation, but the gender gap narrows down when Perceived inflation exceeds 5.5%. This threshold represents the top 25% of this variable distribution in the pooled sample, and the mean of it for years 2020 to 2025. This may explain the absence of a statistically significant gender gap in the last 4 years of the survey (see Figure 2).

Gender Gap in Satisfaction With the Bank of England’s Performance, at Different Levels of Perceived Inflation.

Conclusions

In this article, I analyse the extent and limits of gender gaps in assessment of monetary institutions and outcomes, using data on public satisfaction with the Bank of England’s performance in controlling inflation. Because I use observational data, I do not attempt to make any causal claim. Furthermore, because the data have been collected by a third party, there are limits to the variables I am able to include, and I am constrained by their measurement choices and available variables. Yet, several findings are noteworthy.

First, I show that, generally, there is a gender gap in the satisfaction with the performance of the Bank: Women generally exhibit lower satisfaction with the performance of the Bank of England’s job at controlling inflation, as show in previous studies (Blanchflower and MacCoille, 2009; Garriga, 2025). This gap cannot be attributed to inflation perception or financial literacy alone, factors that were already included in the estimations. However, at least in the past 25 years in the United Kingdom, this has not been a persistent trait: in over a third of the years covered by this study, there is no significant gender gap in satisfaction with the Bank. Importantly, these years include the inflation surge in the United Kingdom. I find that this gender gap is less apparent and even disappears at higher levels of perceived inflation or deflation, suggesting the possibility that once respondents perceive relatively extreme levels of inflation/deflation, where the Bank of England seems to be very far away from their inflation target, women are less hesitant in expressing extreme views, making the gender gap become insignificant. Interestingly, the direction of the observed gender gap in inflation perception contrast with expectations in the literature. Female respondents do not seem to overestimate inflation – or to perceive higher inflation than men. Taken together, these indicators, combined with a different propensity to express extreme evaluations, may explain why in context of high inflation, men express stronger discontent and blur gender gaps in satisfaction.

Most results tend to be sensitive the way in which the ‘Do not know’ responses are treated – either as missing data or as a sample selection dynamic. This is key because the likelihood providing a substantive answer significantly varies by gender. After controlling for selection into a substantive answer, the estimated gender gap for some outcomes differs in magnitude, direction, and statistical significance. This is specially the case for respondents’ perception of the level of inflation. Future research can further explore the characteristics of those who choose the ‘Do not know’ answer, and why these characteristics vary across questions in the same survey setting.

Variance in the gender gap in satisfaction with the Bank of England indicates deeper factors at play, suggesting that assessments of the Bank’s performance may be influenced by broader monetary preferences and concerns that transcend mere economic indicators (Croson and Gneezy, 2009; Diouf and Pépin, 2017; Masciandaro et al., n.d.). 21 Because monetary policy has gendered effects, women may assess the performance of the Bank of England beyond the perceived level of inflation. In other words, the assessment is not expected to come exclusively from the perceived price stability but also from the boarder decisions the Bank makes regarding the interest rate. McMahon and Reiche (2025) speculate that gender gaps may increase during crisis periods.

This article’s findings suggest to look not only at objective economic data but also at potential biases in the perception of economic realities (Binetti et al., 2024; DiGiuseppe et al., 2025b). Research should further explore the underlying motivations for these differences, particularly looking into how gender influences perceptions of monetary policy and its socioeconomic implications. Understanding the factors that affect attitudes to central banks is important because satisfaction with the monetary authority’s performance is a key component of trust in the institution. As trust in central banks becomes increasingly crucial for effective monetary policy, addressing the nuanced reasons behind a gender gap in satisfaction seems imperative for enhancing communication strategies (Bodea and Kerner, 2022, 2025; Haldane and McMahon, 2018; McMahon and Reiche, 2025).

Supplemental Material

sj-docx-1-psx-10.1177_00323217251399528 – Supplemental material for A Gender Gap in Attitudes Towards Monetary Policy? The Case of Satisfaction With the Bank of England

Supplemental material, sj-docx-1-psx-10.1177_00323217251399528 for A Gender Gap in Attitudes Towards Monetary Policy? The Case of Satisfaction With the Bank of England by Ana Carolina Garriga in Political Studies

Supplemental Material

sj-docx-2-psx-10.1177_00323217251399528 – Supplemental material for A Gender Gap in Attitudes Towards Monetary Policy? The Case of Satisfaction With the Bank of England

Supplemental material, sj-docx-2-psx-10.1177_00323217251399528 for A Gender Gap in Attitudes Towards Monetary Policy? The Case of Satisfaction With the Bank of England by Ana Carolina Garriga in Political Studies

Footnotes

Acknowledgements

This paper was presented at the 2024 annual meeting of the European Political Science Association. I thank Daniel Devine, Andreas Kern and Brian Phillips for their comments on previous drafts of this paper.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Additional Supplementary Information may be found with the online version of this article.

Contents

Appendix 1. Number of respondents per survey wave Appendix 2. Variables constructed from the survey: Knowledge. Questions, answer options, and coding Appendix 3. Descriptive statistics Table A3.1. Descriptive statistics. Full sample Table A3.2. Descriptive statistics. First quarter only. Appendix 4. Additional tables and figures Table A4.1. Introducing controls sequentially to Model 1, Table 1 (OLS) Table A4.2. Introducing controls sequentially to Model 2, Table 1 (Selection model) Table A4.3. Gender and ‘extreme’ opinions regarding satisfaction with the Bank of England. Comparison one- and two-stage ordered probit coefficients Table A4.4a. Predicted margins after one-stage oprobit (from column 1, Table A4.3) Table A4.4b. Predicted margins after two-stage Heckman oprobit (from column 2, Table A4.3) Table A4.5. Perceived inflation. Table A4.6. Crosstabulation of responses and non-responses for Satisfaction with the Bank of England and Inflation perception. All quarters. Table A4.7. Conditional effect of Inflation perception on Satisfaction

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.