Abstract

The study examined the crowding in or out effect of public investment on private investment in Botswana from 1980 to 2018 using the autoregressive distributed lag bounds testing approach. The findings of the study indicate that infrastructure public investment negatively affects private investment while non-infrastructure public investment has a positive impact on private investment in the short run. The study concluded that infrastructure public investment crowd out private investment while non-infrastructure public investment crowds in private investment only in the short run. The recommendation emanating from the study is that the government should spend more on non-infrastructure public investment in order to crowd in private investment, especially in the short run, and introduce more initiatives to promote the role of the private sector in growing the economy.

Introduction

Although numerous studies have been conducted to establish the impact of public investment on private investment, it is still uncertain whether public investment crowds in or crowds out private investment. The literature reveals three views on the crowding in or out effect of public investment on private investment. The Keynesian approach suggests that public investment crowds in private investment, while the neoclassical approach holds that it crowds out private investment, and the Ricardian equivalence theorem suggests that government spending will leave private investment unchanged (Kuştepeli, 2005). Studies such as those conducted by Odedokun (1997), Pereira (2001), Ramirez and Nazmi (2003) and Erden and Holcombe (2005) found public investment to crowd in private investment, while those of Karagöl (2004), Acosta and Loza (2005), Mitra (2006), Bint-e-Ajaz and Ellahi (2012) and Dash (2016) indicate that public investment crowds out private investment.

Although a number of studies have examined the impact of public investment on private investment, the majority of these studies consider the impact of aggregate public investment and not that of infrastructure and non-infrastructure public investment (see Ouédraogo et al., 2019). Furthermore, previous that have examined the dynamics of private investment in sub-Saharan African countries largely focused on (a) the relationship between financial sector and private investment (Fowowe, 2011; Misati & Nyamongo, 2011), and (b) whether poverty plays a role in private capital mobilisation (Dominik & Narayanan, 2023). Moreover, the specific studies that have focused on the impact of infrastructure and non-infrastructure public investment on private investment are scant and inconclusive. In Botswana, the government has played a role in promoting investment by the private sector in particular. Since private investment has been identified as one of the factors contributing to the growth of the economy, the study will attempt to examine whether it is infrastructure or non-infrastructure public investment that crowds in private investment. The findings will enable the government to know which type of public investment they should focus on in order to stimulate the level of private investment. Although studies on the crowding in or out of public investment have produced a significant amount of discussion for several years, there has been no consensus whether public investment crowds in or out private investment.

In light of this, the present study will examine whether public investment crowds out or in private investment in Botswana using the autoregressive distributed lag (ARDL) methodology for the period from 1980 to 2018. The study will disaggregate public investment into infrastructure and non-infrastructure public investment. Theoretically, public investment can have either a positive or a negative impact on private investment. When public investment increases, the expectation is that this will lead to an increase in private investment due to the provision of infrastructure such as roads, railways, ports and technology. Moreover, an increase in public investment can lead to a decrease in private investment if the government invests in non-infrastructural goods and services, such as health, education, transport and security, which are in competition with the private sector. Infrastructural public investment crowds in private investment, as the provision of infrastructure by the government reduces the cost of production and saves the private sector money, which could lead to an increase in private investment. However, crowding out could also occur due to the shortage of credit available to the private sector. The increase in public investment leads to an increase in the fiscal deficit, which is financed mainly by domestic borrowings, which could reduce the availability of funds and have a negative impact on the private sector investment. Sakr (1993) has found public non-infrastructure investment to have a negative impact on private investment, and public infrastructure investment to have a positive impact on private investment. Therefore, the study aimed to establish whether this is the case in Botswana.

The rest of the paper is organised as follows. The next section “Public and Private Investment Dynamics in Botswana” discusses the policies and trends in public and private investment in Botswana. Section “Literature Review” reviews the empirical literature on the crowding in or out of public investment. Section “Methodology” presents the methodology used in the study. The section “Empirical Results” provides and discuss the empirical findings of the study, while the last section contains the conclusion.

Public and Private Investment Dynamics in Botswana

Botswana is one of the fastest growing economies in Africa. Economic growth averaged 8.43% for the period 1980 to 1999, and 4.21% for the period 2000 to 2018 (World Bank, 2021). The impressive growth achieved was due mainly to the exploitation of the country's sizeable diamond deposits, sound macroeconomic policies, political stability, as well as good governance (Bank of Botswana, 2012). In order to boost economic growth, the government in Botswana has been working on the diversification of the economy. Furthermore, by creating an environment that is conducive to the sector, it has also encouraged the private sector to invest in the economy.

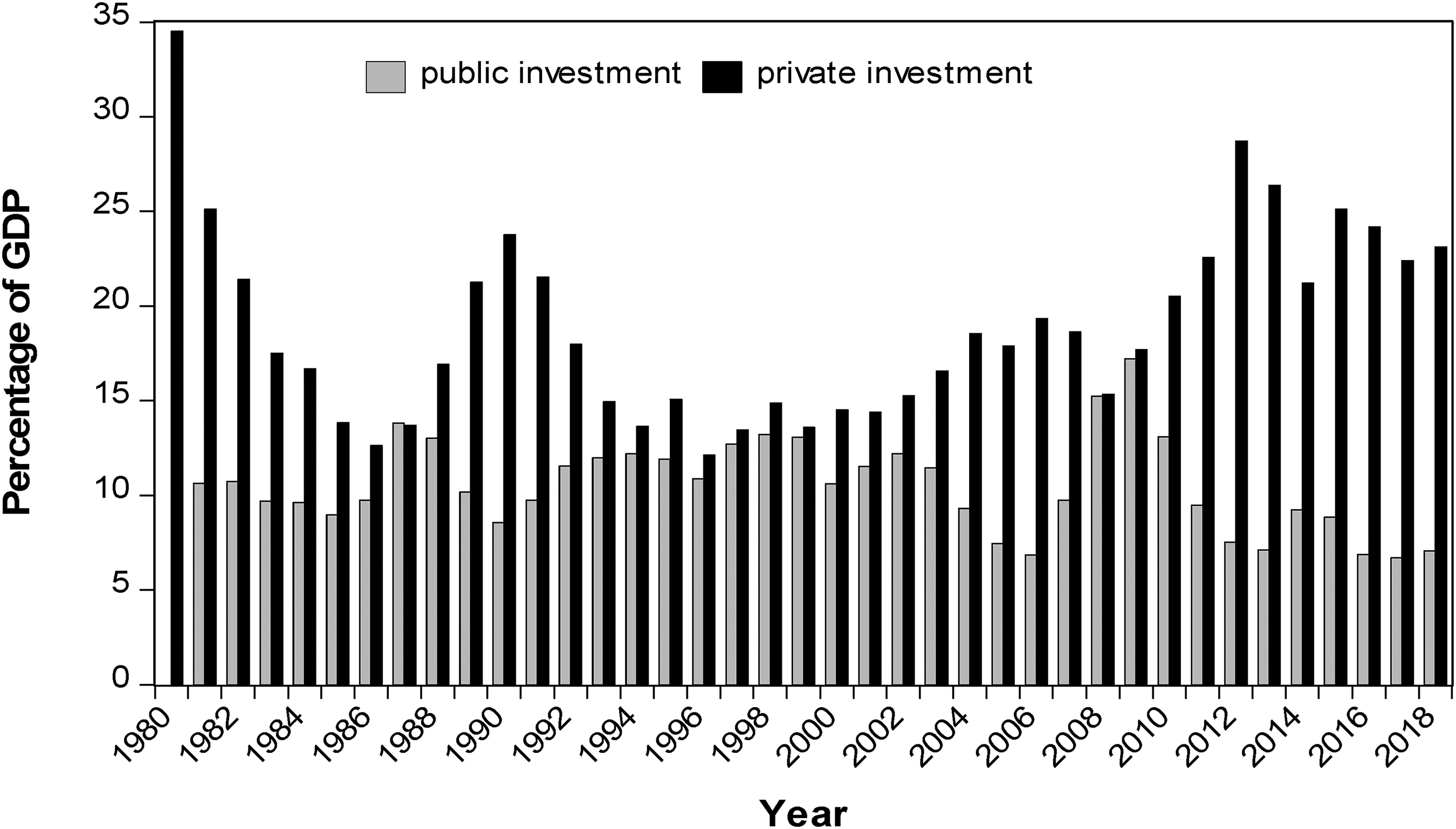

This can be seen through the policies and initiatives that have been developed over the years. One such initiative is the privatisation of state-owned enterprises (SOEs), through which the government aimed to include the private sector in the diversification of the economy and creation of jobs. According to the Republic of Botswana (2009), the privatisation of SOEs is a good indicator to investors, as it shows that the government has reduced its involvement in economic activities. In 2009, the Government of Botswana adopted the Public Private Partnership strategy as another way to finance the government's infrastructure projects, to fast-track and improve the development of infrastructure, and to build an environment that is conducive to a stronger partnership between the public and private sectors (Ministry of Finance and Development Planning, 2009). Public investment as a percentage of GDP decreased from 17.21% in 2009 to 7.54% in 2012, while private investment as a percentage of GDP increased from 17.70% to 28.69% during the same period (World Bank, 2021).

The government further emphasises the attraction of the private sector and the provision of infrastructure through policies such as National Development Plans (NDP) 10 and 11. During the implementation of NDP 10, which spanned April 2009 to March 2016, the government planned to become less dependent on government spending and to promote the private sector as the driving force for economic growth (Republic of Botswana, 2009). NDP 11 was launched in 2016 and was scheduled to run from April 2017 to March 2023. In order to achieve the objective of NDP 11, the government will create a conducive environment that will enable the private sector to play its role in the economy. According to the Republic of Botswana (2017), macroeconomic stability, the availability of infrastructure, and information and communication technology will enable the government to provide a conducive environment for private sector investment. Figure 1 presents the trends of public and private investment as a percentage of GDP in Botswana from 1980 to 2018.

Public investment and private investment in Botswana (1980–2018). Source: Own compilation from World Bank Development Indicators (2021).

Over the period 1980 to 2018, the level of private investment in Botswana was higher than public investment as a percentage of GDP (World Bank, 2021). For the period 1980 to 2018, private investment as a percentage of GDP averaged 18.9%, while public investment as a percentage of GDP averaged 10.3% (World Bank, 2021). Figure 1 provides evidence of a positive co-movement between private and public investment for the period 1980 to 2018. It shows that for the majority of the period between 1980 and 2018, when public investment decreased, private investment increased. This suggests that public investment crowds in private investment. However, it is unclear whether it is infrastructure or non-infrastructure public investment that crowd in private investment, which will be established in this study.

Literature Review

Crowding in states that government spending increases private investment while crowding out means that government spending reduces private investment in the economy. The literature shows the Keynesian approach to suggest that public investment crowds in private investment, and the neoclassical approach to suggest that it crowds out private investment (Kuştepeli, 2005).

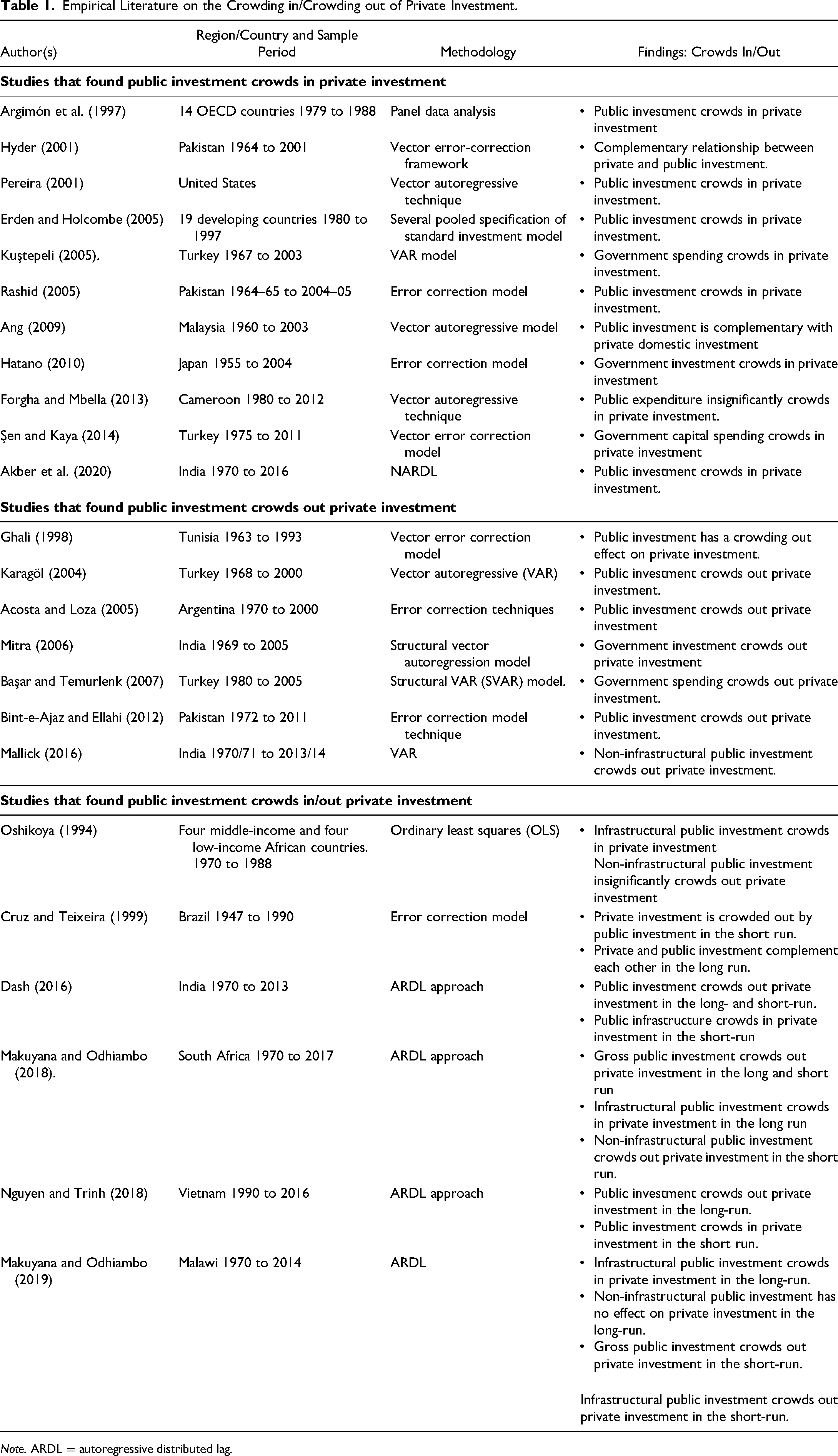

The relationship between private investment and public investment has been the subject of ongoing debate for some time now, and the empirical findings on whether public investment crowds private investment in or out have been inconsistent. Some studies have found that public investment crowds private investment in, while others have found it to crowd private investment out. Some of the studies that find public investment to crowd in private investment include those by Argimón et al. (1997), Pereira (2001), Erden and Holcombe (2005), Kuştepeli (2005), Rashid (2005), Hatano (2010), Şen and Kaya (2014) and Akber et al. (2020). The studies that are in support of the Neoclassical and found public investment to crowd out private investment include those of Karagöl (2004), Acosta and Loza (2005), Mitra (2006), Başar and Temurlenk (2007) and Bint-e-Ajaz and Ellahi (2012). Table 1 gives an overview of crowding in or out of public investment on private investment in various countries. A summary of some of the empirical studies on the crowding in or out effects of public investment on private investment is presented in Table 1.

Empirical Literature on the Crowding in/Crowding out of Private Investment.

Note. ARDL = autoregressive distributed lag.

As indicated in Table 1, it is clear that the findings on crowding in or out of public investment on private investment remain inconclusive. The effects are found to differ as a result to the type of government expenditure used, the methodology, the region and the period of the study. However, the majority of the reviewed studies examining the effect of government spending on private investment found the opposite, namely a crowding out effect.

Methodology

The ARDL bounds testing approach developed by Pesaran et al. (2001) is used to examine the cointegration relationship between private investment and disaggregated public investment. This approach is selected because it has some empirical advantages over other cointegration techniques such as the Engle-Granger and the Johansen-Juselius approaches. The key advantages are that the ARDL makes it possible to determine cointegration irrespective of whether the variables are integrated of order zero or one. It is also efficient in the case of data with a small number of observations.

The formulation of the model to examine the impact of public investment on private investment follows Blejer and Khan (1984), Odedokun (1997) and Makuyana and Odhiambo (2019). Oshikoya (1994) has found evidence that public infrastructure has a positive impact on private investment while non-infrastructure investment has a negative impact although insignificant on private investment. Therefore, public investment is disaggregated into infrastructure and non-infrastructure public investment. The equations are specified as follows:

Model 1: Private Investment and Infrastructure Public Investment

The dependent variable is domestic private investment, which is measured by the private sector's gross fixed capital formation as a percentage of GDP. The choice of independent variables is underpinned by the theoretical and empirical literature. The model includes gross public investment, which is measured by government gross fixed capital formation as a percentage of GDP, and it is decomposed into infrastructure and non-infrastructure public investment. Infrastructure public investment includes investment in the construction of roads, railways, hospitals, schools and telecommunications, while non-infrastructure includes services such as education and health. Public investment may crowd in private investment, especially when government invests in infrastructure that only it can provide. However, it can also crowd out private investment, especially when government invests in goods that are in competition with the private sector (Greene & Villanueva, 1991). Studies such as those conducted by Pereira (2001) and Ramirez and Nazmi (2003) found that public investment crowds in private investment, while Acosta and Loza (2005), Mitra (2006) and Dash (2016) found that it crowds out private investment. Therefore, gross and disaggregated public investment is expected to have either a positive or a negative impact on private investment.

In line with previous studies, the current study uses real GDP per capita as a proxy of economic growth. The coefficient of GDP per capita is expected to be positive and to have a significant impact on private investment. This is consistent with previous studies such as that by Tan and Tang (2012), which found economic growth to have a positive impact on private investment. Credit to the private sector measured by the domestic credit to the private sector is used as a proxy for financial development and has also been found to influence the level of private investment. Oshikoya (1994) found access to credit by the private sector to increase the level of private investment. Therefore, the study expects the coefficient of the domestic credit to the private sector to be positive and statistically significant.

Another variable that has been found to determine private investment is the real interest rate, which is measured by the lending rate adjusted for inflation. The real interest rate is used as a proxy for the user cost of capital and has a negative impact on private investment. However, it also has a positive effect on private investment as some argue that higher interest rate increase the flow of bank credits, which complements the private sector savings, facilitates private capital formation and therefore private investment (Frimpong & Marbuah, 2010). Studies such as Tan and Tang (2012), Suhendra and Anwar (2014) have found a negative relationship between private investment and real interest rate, while Frimpong and Marbuah (2010) found support for the complementary hypothesis. Therefore, real interest rate is expected have either a positive or a negative impact on private investment in this study.

Inflation, which is measured by the consumer price index, is also another determinant of private investment. It is used as a proxy for uncertainty in the economy and, it is expected to have either a positive or a negative impact on private investment. Trade openness is measured by the sum of exports and imports of goods and services as a percentage of GDP. There are studies in literature such as Ajide and Lawanson (2012) and Maluleke et al. (2023) that have found trade openness to have a positive effect on private investment. In this study, we expect trade openness to have a positive association with private investment.

The study uses annual time series data for the period from 1980 to 2018 to examine the impact of public investment on private investment in Botswana. The data is obtained from the World Development Indicators. Consistent with previous studies such as Odedokun (1997) and Makuyana and Odhiambo (2019), the data on infrastructure and non-infrastructure public investment was obtained by gross public investment decomposed into infrastructure and non-infrastructure public investment. These proxies of infrastructure and non-infrastructure public investment are based on the assumption that infrastructural investment is an ongoing process that is associated with economic development and has a long gestation period (Blejer & Khan, 1984). Therefore, the infrastructure public investment is obtained following Blejer and Khan (1984) as follows:

Non-infrastructure public investment (

Following Pesaran et al. (2001), the ARDL model specification of models 1 and 2 is expressed as follows:

Model 1: Private Investment and Infrastructure Public Investment

0 = the constant term;

The first stage of the ARDL procedure involves testing for cointegration on equations 4 and 5. The null and alternative hypothesis to test for cointegration for both models is expressed as follows:

The results of the cointegration test are determined by the computed F-statistic, which is compared with the critical values reported by Pesaran et al. (2001). If the computed F-statistic is higher than the upper critical value bound, the null hypothesis of no cointegration is rejected. If the computed F-statistic is less than the lower bound, the null hypothesis of no cointegration cannot be rejected. After establishment of the cointegration, the long-run and error correction estimates of the ARDL model are obtained. The ARDL-based error correction model is specified as follows:

Model 1: Private Investment and Infrastructure Public Investment

Model 2: Private Investment and Non-Infrastructure Public Investment

0 - the constant term;

The coefficient of the lagged error correction term (

Empirical Results

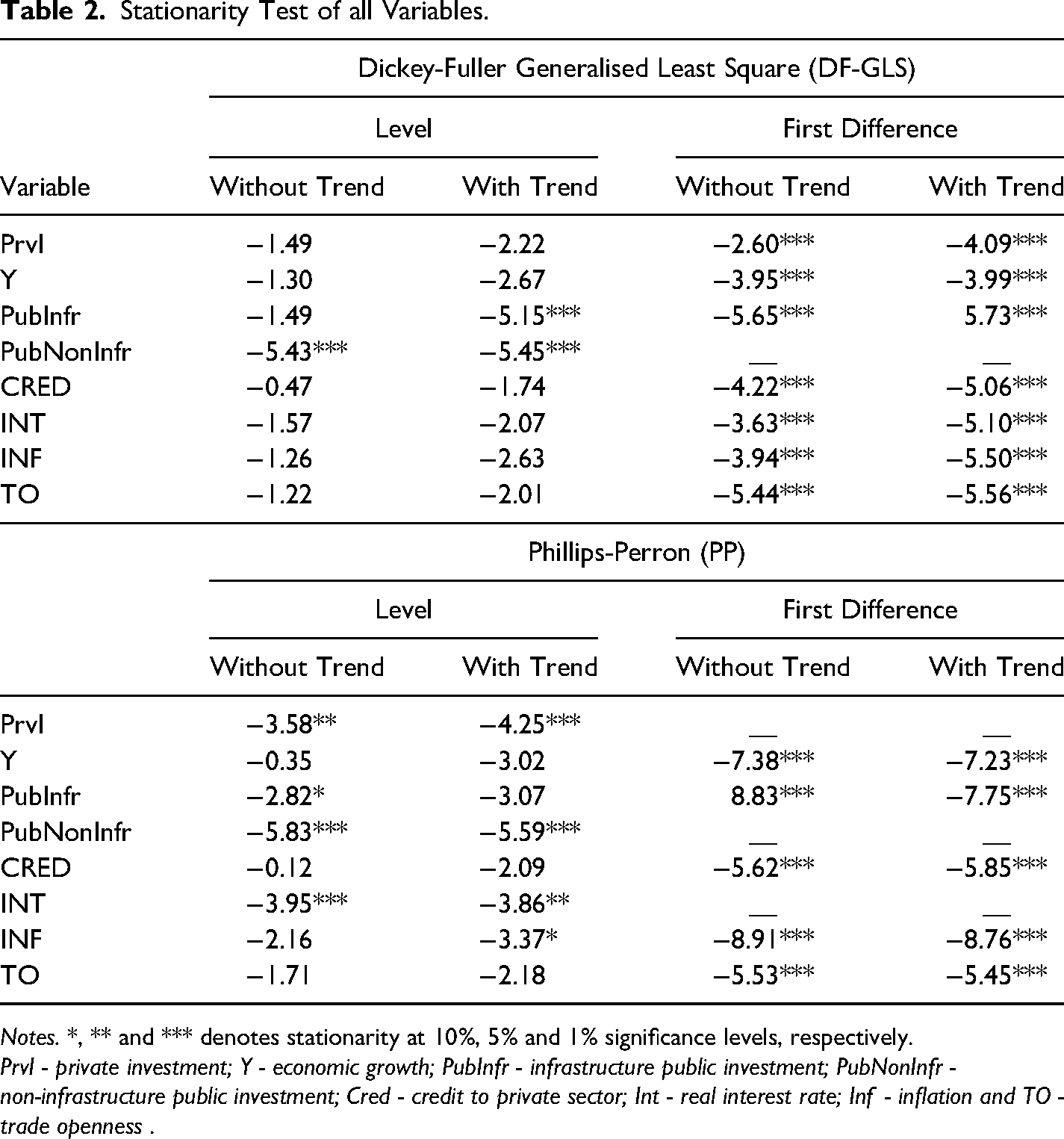

All the variables used in the analysis were first tested for stationarity to ensure that all the variables were of order one or lower. The Dickey-Fuller Generalised Least Squares (DF-GLS) and the Phillips-Perron (PP) tests were used. The results of the stationarity tests for all the variables in levels and the first difference are shown in Table 2.

Stationarity Test of all Variables.

Notes. *, ** and *** denotes stationarity at 10%, 5% and 1% significance levels, respectively.

It was concluded from the stationarity tests that all the variables were stationary and integrated of either I(0) or I(1); therefore, it was possible to perform the analysis using the ARDL bounds testing approach. Since it had been established that the variables were stationary, the next step was to perform the cointegration test, which would determine whether there was a long-run relationship between private investment and its determinants. The results of the F-statistic were 3.788 for model 1 and 4.496 for model 2. The results confirm the presence of cointegration between private investment and public investment, as the calculated F-statistic is higher than the Pesaran et al. (2001) upper bound critical values at a 1% significance level. Following confirmation that the variables were cointegrated, the long-run and short-run coefficients were estimated. The results of the cointegration test are reported in Table 3, and the long- and short-run results are presented in Table 4.

Bounds F-Test for Cointegration Results of Models 1 and 2.

Notes. ** and *** denote statistical significance at 5% and 1% level, respectively.

Results of Long- and Short-Run Estimation for Models 1 and 2.

Notes. *, ** and *** denote statistical significance at 10%, 5% and 1% levels, respectively

Long-Run Results

The long-run results reveal that infrastructure public investment has a statistically insignificant impact on private investment in the long run. The findings imply that infrastructure public investment does not have a significant crowding effect on private investment in Botswana. The non-infrastructure public investment is also found to be statistically insignificant in the long run. The findings suggest that in the long run, investment by the government, whether on infrastructure or non-infrastructure, does not influence the level of private investment.

The results of the other variables in models 1 and 2 show that credit to the private sector and trade openness have a statistically significant positive impact on private investment in the long run. This suggests that an increase in credit to the private sector and trade openness will lead to an increase in private investment in the long run in Botswana. Economic growth, interest rate and inflation are found to be statistically insignificant in the long run for both models.

Short-Run Results

In the short run, infrastructure public investment is found to be negative and statistically significant at the 1% level of significance. This suggests that an increase in infrastructure public investment will lead to a decrease in private investment. Therefore, private investment is crowded out by infrastructure public investment in Botswana in the short run. The findings concur with studies such as those by Karagöl (2004), Acosta and Loza (2005), Mitra (2006), and Başar and Temurlenk (2007) which have found public investment to crowd out private investment. The infrastructure of public investment in the previous period is also found to crowd out private investment.

The non-infrastructure public investment is found to be positive and statistically significant at the 1% level of significance. This suggests that an increase in non-infrastructure public investment will lead to an increase in private investment. Therefore, non-infrastructure public investment crowds in private investment in Botswana in the short run. The findings are supported by studies such as that by Kuştepeli (2005), which found that public spending crowds in private investment. The results further reveal that non-infrastructure public investment in the previous period tends to crowd in private investment in the short run.

The study further found economic growth, credit to the private sector and trade openness to have a statistically insignificant effect on private investment in the short run in both models. However, economic growth from the previous period has a positive impact, while credit to the private sector had a negative impact on private investment in both models. Trade openness in the previous period was found to have a negative and significant effect on private investment in model 1. Interest rate and inflation were found to be positive and statistically significant. This means that an increase in the interest rate and inflation will lead to an increase in private investment in the short run. It was also found that the inflation rate from the previous period had a positive impact on private investment in the short run for both models.

The ECM had the expected sign, which was negative for both models 1 and 2, and was statistically significant at a 1% level. This means that private investment adjusts to equilibrium at a speed of 47.18% for model 1 and 47.23% for Model 2 in the event of a shock in the Botswana economy. The results show that the R-square is 0.922 for model 1 and 0.925 for model 2, implying that 92% of the variation in private investment is explained by the independent variables in both models. Table 5 summarises the results of the diagnostic tests.

Diagnostic Tests Results.

Notes. Normality test using the Jarque–Bera test, Serial correlation using the Breusch–Godfrey langrage multiplier test, Heteroscedasticity using the Breusch–Pagan–Godfrey test and Functional form using the RESET test; and values in parenthesis are p-values.

The results in Table 5 show that there is no serial correlation, the error term of the model is normally distributed and there is no problem with heteroscedasticity. The Reset test, which shows the functional form of the model, is well specified. The Cumulative Sum of Recursive Residual (CUSUM) and Cumulative Sum of Squares of Recursive Residuals (CUSUMQ) tests are conducted to check the null hypothesis that the parameters are unstable. The CUSUM and CUSUMQ plots indicate evidence of stability among the variables as the plots are within the confidence band at a 5% significance level. Therefore, both models pass the stability test, indicating the reliability of the estimated parameters. Figures 2 and 3 present the CUSUM and CUSUMQ plots of both Model 1 and 2.

Plot of CUSUM and CUSUMQ of model 1. CUSUM = Cumulative Sum of Recursive Residual; CUSUMQ = Cumulative Sum of Squares of Recursive Residuals.

Plot of CUSUM and CUSUMQ of model 2. CUSUM = Cumulative Sum of Recursive Residual; CUSUMQ = Cumulative Sum of Squares of Recursive Residuals.

Conclusion

The study entailed an empirical examination of the impact of public investment on private investment in Botswana for the period 1980 to 2018. The objective of the study was to determine whether public investment crowds private investment in or out. To achieve the objective of the study, the ARDL bounds testing approach was used to examine the relationship between public and private investment. Public investment was disaggregated into infrastructure and non-infrastructure. The empirical results of the study indicate that infrastructure public investment negatively affects private investment in the short run. Non-infrastructure public investment has an insignificant effect on private investment in the long run, and a positive and significant influence on private investment in the short run.

It was concluded from the study that infrastructure public investment crowds out private investment, while non-infrastructure public investment crowds in private investment only in the short run. Based on the findings of the study it is recommended that the government invest more in non-infrastructure investments such as education and health, which will stimulate more investment by the private sector. Since non-infrastructure public investment crowds in private investment in the short run, the government should spend more on non-infrastructure public investment and introduce more initiatives to promote the role of the private sector in growing the economy.

It is recommended that future studies consider examining the impact of public investment on private investment using another methodology, such as the nonlinear ARDL, to determine how negative and positive public investment shocks affect private investment.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.