Abstract

In the aftermath of the recent recession, the percentage of households facing rent burden in the USA reached historically high levels, while cost burden for owners has shrunk. This study uses two panels from the Survey of Income and Program Participation (SIPP) to compare the prevalence, distribution and household responses to the phenomenon of rent burden in the USA in the years immediately before and after the Great Recession. Results suggest that rent burden has become more prevalent after the recession and that income, household composition and location are major drivers of this phenomenon, both before and after the recession. Results also indicate that exiting rent burden was more difficult in the years after the recession and that an increasingly common coping mechanism for rent burdened households is to increase their household sizes. These results indicate that renters have experienced increased financial stress related to their housing. This finding is notable given the lack of policy responses that address hardship among renter households in contrast to the privileged status enjoyed by homeowners in the policy domain.

Introduction

While the US government response to support homeowners during the recent housing crisis was anaemic (Immergluck, 2009), policy responses to aid renter households have been virtually non-existent. The lack of attention to the plight of renters continues a policy legacy that has rewarded homeowners rather than renters (Krueckeberg, 1999) and has helped to deepen the class cleavage that exists in the USA (Shlay, 2015). One example of uneven policy support by housing tenure is the ability for homeowners to deduct mortgage interest and property tax payments from their incomes when calculating income taxes, a benefit not typically provided to renters. Lack of support for low-income renter households is also evident in other policy domains as there has been a decline in other means-tested social programmes in the USA that scholars describe as selective welfare retrenchment (Mettler, 2007).

The lack of a policy response to aid renter households has grown more conspicuous in recent years as housing cost burden, a condition in which a household pays over 30% of its income on rent and utilities, has become more pronounced for renters and less pronounced for homeowners. Nearly 50% of all renters in the USA were housing cost burdened in 2014 compared with about 47% in 2005 (Fernald, 2015a, 2015b). The rate of housing cost burden among homeowners has moved in the opposite direction. In 2014 about 25% of homeowners were in a cost burdened state, compared with almost 29% in 2005 (Fernald, 2015b). American Community Survey (ACS) data from 2014 indicate that the number of housing cost burdened renter households exceeds that of housing cost burdened homeowner households (about 21.7 million compared with 18.9 million). As a result, renter households are more likely than homeowner households to experience threats to their viability and health that are associated with living in a housing cost burdened state. For example, housing cost burdened households spend far less on essential expenditures such as food and healthcare (Fernald, 2015b), and may compel household members to work additional hours, change their residence or alter their household composition. The affordability of rental housing takes on increasing importance as the share of US households that rent has reached the highest level since the 1960s (Fernald, 2015a).

The purpose of this study is to compare the phenomenon of housing cost burden for renter households in the USA in the years immediately before and after the Great Recession. Specifically, we focus on three related research questions. First, how did the prevalence and distribution of housing cost burden for renter households change in the years before and after the Great Recession? Second, what factors are associated with housing cost burden at the household-level for renters and how does the magnitude of these factors compare before and after the Great Recession? Third, what renter household behavioural responses are associated with experiencing housing cost burden and how have these responses changed since the Great Recession? In answering each question, we focus our analysis on a period prior to the Great Recession (2004–2005), as well as the period immediately following the official end of the recession (2009–2011). We rely on data from two distinct nationally representative panels from the US Census Bureau’s Survey of Income and Program Participation (SIPP) to provide a detailed picture of housing cost burden for renters, which we refer to as rent burden hereafter. By using panel data that cover pre- and post-recessionary periods, this study improves upon the findings of other research that use cross-sectional data from single years.

Our findings provide a deeper understanding of rent burden and how it changed in the aftermath of the Great Recession. Although descriptive statistics suggest that experiencing rent burden is unequally distributed along racial, national origin and gender lines, regression analysis demonstrates that rent burden is associated with income, household composition and location far more than with other demographic factors. In keeping with other recent research on this topic, our analysis of pre- and post-recession periods shows that rent burden has become more prevalent after the recession and that higher-income households are at greater risk of rent burden in the aftermath of the crisis. Our results also indicate that exiting rent burden became more difficult after the recession. Finally, the analyses suggest that increasing the number of adults in a household is an important mechanism by which rent burdened households exit that state.

Dynamics of the US housing market and rent burden

In the years following the Great Recession, housing in the USA became a tale of two very different markets. It is not uncommon for the owner-occupancy and rental markets to diverge, and this split was evident in the aftermath of the financial crisis (Kroll, 2013). The tepid demand for owner-occupancy housing stood in stark contrast to the sustained growth in the number of renters and the prices they paid for housing (Fernald, 2015b; Kroll, 2013). These housing trends produced a post-recession rental market with decreasing vacancy rates and higher rents (Fernald, 2015a).

Higher demand for, or lower supply of, rental housing has the potential to push market rents higher. In the years immediately after the recession, the strength of the rental market was largely attributed to increased demand (Collinson, 2011). Supply factors also played a role as Collinson found that while overall supply may have been sufficient, the stock of affordable unassisted rental housing was inadequate. According to Collinson and Winter (2010), from 2001 to 2007 the affordable unassisted rental stock fell 6.3% while the supply of high-end rental housing increased by 94.3%. The under-development of affordable unassisted rental housing continued after the Great Recession as mortgage market dislocations constrained the construction of multi-family units (DiPasquale, 2011). For extremely low-income households (those earning 30% of area median income or less), the housing choices were even more limited. In 2013, 11.2 million extremely low-income households competed for only 7.3 million affordable units, implying a significant supply and demand imbalance (Fernald, 2015b). Although rental housing market dynamics paint a grim picture for renters, an analysis of rent burden is not complete without considering income dynamics. The long-term trend of income levels for renter households suggests that household incomes are not keeping pace with the rise in rents. According to Collinson (2011), real incomes for renters fell from 1990 to 2009, and, when combined with higher rents, produced rent burden levels in 2009 that were 16.6% higher than in 1990 (Collinson, 2011).

The challenging market conditions in the years after the Great Recession produced an unprecedented amount of rent-burdened households, nearly 50% according to many studies (Bean, 2012; Collinson, 2011; Kroll, 2013). This phenomenon is particularly acute among the low-income segment of renters where 75% of households face rent burden (Bean, 2012). While low-income households are disproportionately burdened, moderate income households also faced increasing rates of burden in the years following the recession (Fernald, 2015a).

Some studies have focused on behavioural responses to economic or housing hardship, such as rent burden. Susin (2007) found that many rent-burdened households were successful at exiting rent burden after a short spell in that state, by finding housing with lower rent, increasing earnings, securing housing assistance or moving into another household (doubling up). Multiple studies have investigated household responses to hardship stemming from the Great Recession. These studies have found that in response to the recession, housing mobility fell, but among movers there was a marked increase in local moves (Stoll, 2013); household formation fell sharply (Lee and Painter, 2013); more complex households were formed (Mykyta and Macartney, 2011); and household spending fell (Hurd and Rohwedder, 2010).

Data and methods

In this study, we use data from the US Census Bureau’s 2004 and 2008 Survey of Income Program Participation (SIPP). The SIPP provides panel data on approximately 40,000 households in the USA over the course of three years. By design, the SIPP oversamples low-income households and, therefore, we apply household weights in our analyses to make the sample more nationally representative. Respondents provide household attribute, demographic, income and programme participation data during interviews conducted every four months. Housing and utility cost data are collected on an annual basis in each year of the panel. The longitudinal nature of SIPP data provides an opportunity to assess changes in the prevalence of rent burden over time, as well as determine how households react to rent burden. Based on the timing of housing and utility cost data collection in SIPP, the 2004 panel provides two data points (2004 and 2005) and the 2008 panel generates three observations (2009, 2010 and 2011). No observations exist for the recession years of 2007 and 2008.

In constructing the data set used in this analysis, we imposed various restrictions on the SIPP data to create two samples of households that were renters in the private housing market for the duration of the years in each panel. Households that entered late or left early from a panel or received government assistance for housing at any time in the panel were dropped from the analysis. In addition, households that changed tenure status during the panel (i.e. moved from renter to homeowner, or vice versa) were also excluded from the analysis. Following previous research, households that reported zero income or zero rent costs were dropped because of concerns over data validity (Steffen et al., 2015; Susin, 2007). We establish a householder for each household unit based on the reference person designation in the SIPP. In this construction, each household assumes the race, gender and age of the householder.

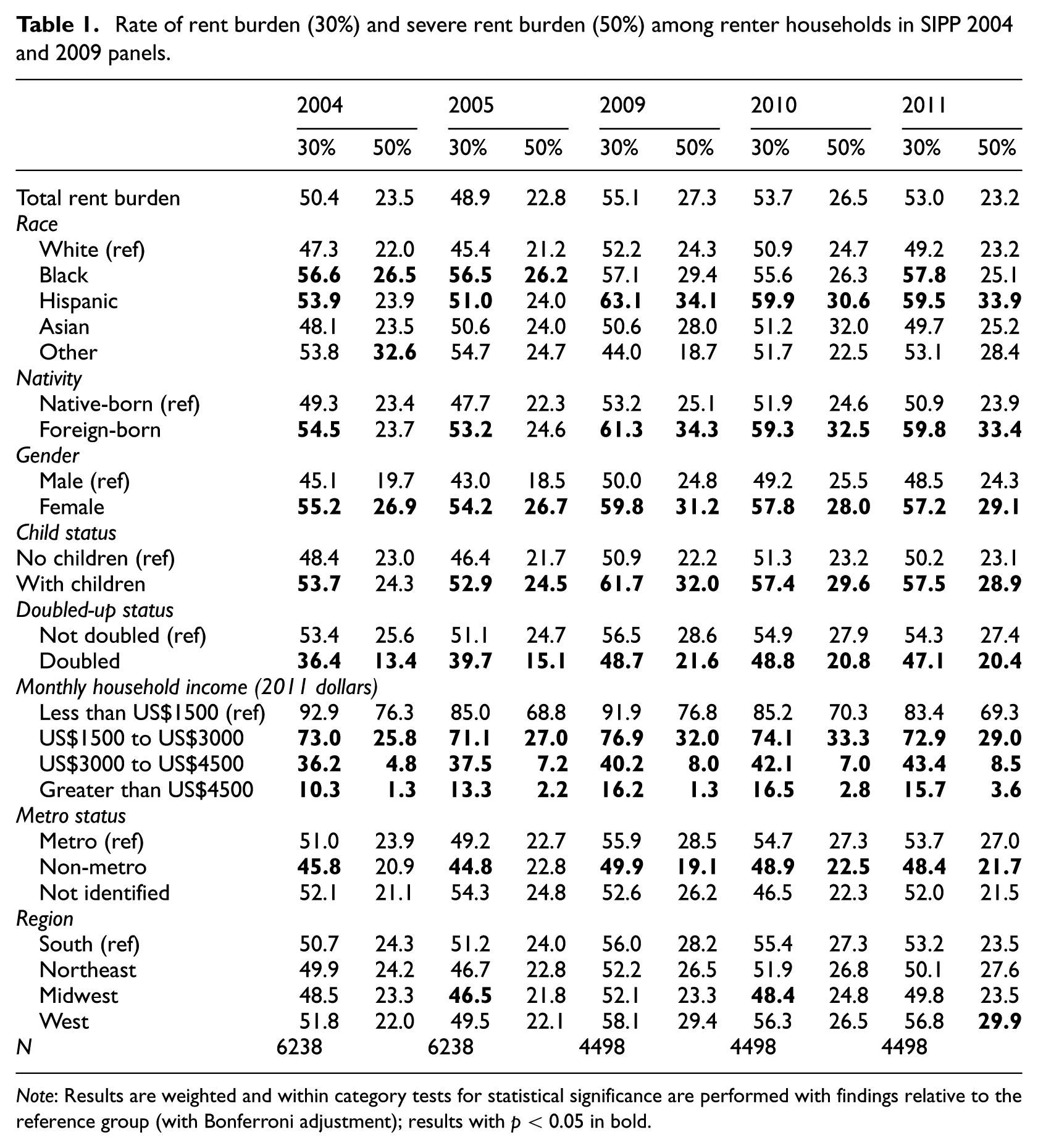

In a study on rent burden that is comparable in some ways with our own study, Susin (2007) used the 2001 SIPP panel and adjusted reported data on utility costs, which he believed to be inflated, by a factor generated from reported utility data from the American Housing Survey. Despite some potential concern that SIPP respondents may inflate their utility costs, we do not alter reported data on utility costs in SIPP. Instead, we use reported utility costs to construct a gross rent for each household. We conduct subsequent sensitivity analyses where we exclude utility costs from our construction of our rent burden measure to ensure that our results are not unduly influenced by potential systematic errors in the reporting of utility costs. We use a ratio of the gross rent and reported household income to construct a dichotomous rent burden variable for each household in each year of the data that is equal to 1 if the ratio of gross rent to household income is equal to or greater than 0.30 and 0 otherwise. In Table 1, we also provide descriptive statistics for the prevalence of severe rent burden in which gross rent accounts for at least 50% of household income. Given that the patterns and disparities for rent burden are very similar to the patterns evident for severe rent burden, we restrict our subsequent analyses to rent burden.

Rate of rent burden (30%) and severe rent burden (50%) among renter households in SIPP 2004 and 2009 panels.

Note: Results are weighted and within category tests for statistical significance are performed with findings relative to the reference group (with Bonferroni adjustment); results with p < 0.05 in bold.

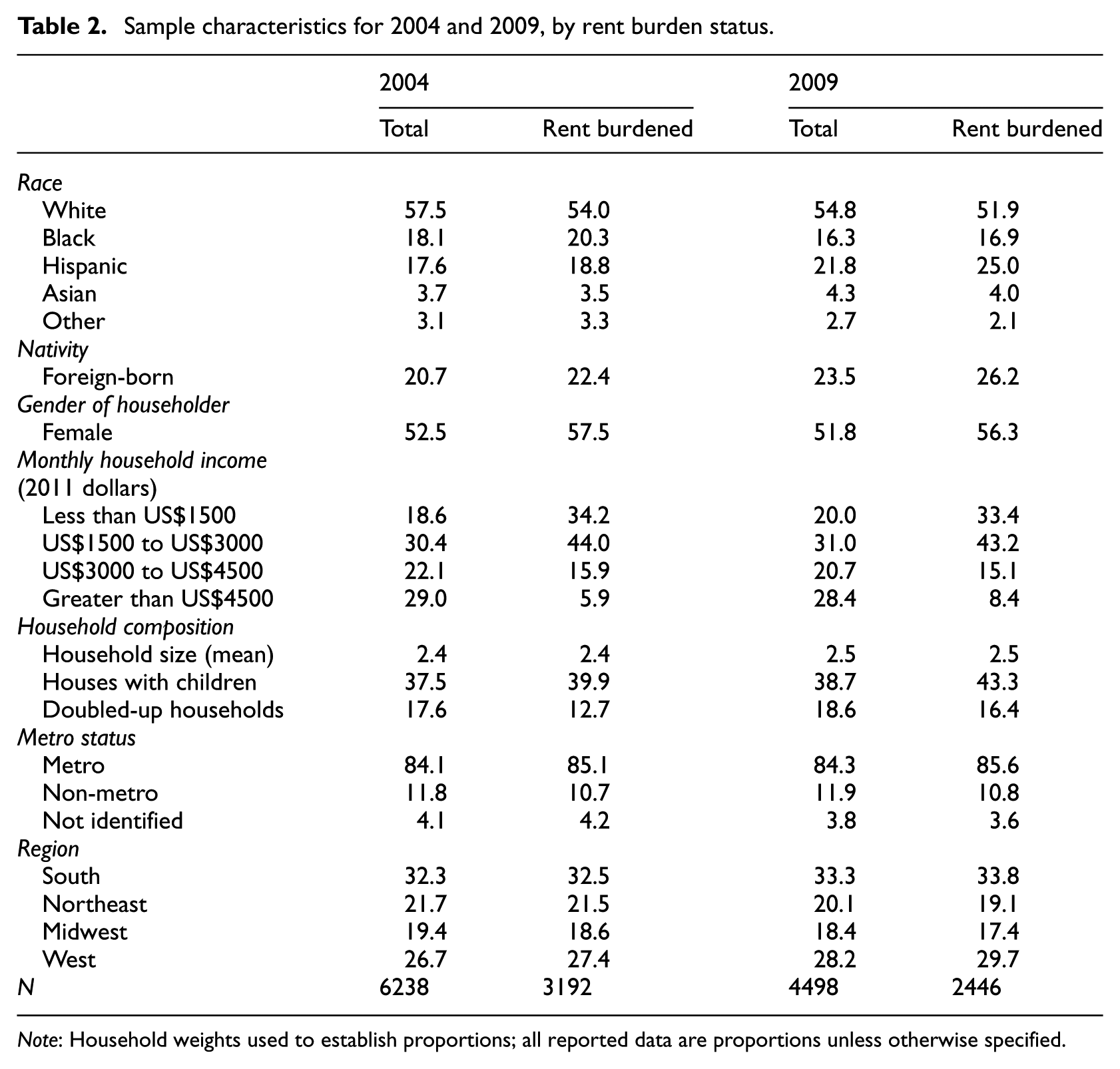

Table 2 provides a summary of the data used in this study. Although there are some slight differences in the samples within the years of each panel, we only present data from 2004 and 2009 in the interest of brevity. After data cleaning, the 2004 panel and 2008 panel include 6238 and 4498 households, respectively. The smaller sample in 2008 is largely due to the fact that more observations were excluded because of sample attrition, changes in tenure status or receiving housing assistance in the three years of this panel in comparison to the two years in the 2004 panel. Comparing the two samples reveals some minor differences. Specifically, the proportion of the sample that was non-white increased between 2004 and 2009, with an increased proportion of Hispanics in 2009 driving this change. Foreign-born households also had a larger representation in the 2009 sample compared with the 2004 sample. Each of these differences is consistent with increasing ethnic diversity and the proportion of the foreign-born in the US population over time.

Sample characteristics for 2004 and 2009, by rent burden status.

Note: Household weights used to establish proportions; all reported data are proportions unless otherwise specified.

In addition to the descriptive analysis described below, we use logistic regression models to assess the association of certain traits with a household being rent burdened. The logistic regression model we use has the following general specification:

where demographic characteristics include race, nativity, gender and age; household attributes include marital status, household income, household size, presence of children and household composition; and geographic factors include metro status and region of the USA. To facilitate comparisons across time, income categories for each year are based on 2011 real incomes. We incorporate robust standard errors to guard against potential misspecification in the model. To ease interpretation of results of these models we also calculate average marginal effects for each predictor and report these alongside odds-ratios. We selectively calculate predicted probabilities for experiencing rent burden for representative households and present the results of this analysis in a separate table.

Results

Prevalence and disparities in rent burden

The descriptive statistics shown in Table 1 demonstrate how rent burden (30% of income) and severe rent burden (50% of income) changed before and after the Great Recession. Across the population, and in most demographic categories, rent burden increased meaningfully between 2005 and 2009. The prevalence of rent burden was greatest in 2009 while the effects of the recession were most acute. In 2010 and 2011, the prevalence of rent burden moderated slightly, but still remained at elevated levels when compared with the pre-recession period. By 2011, over half of all households were rent burdened. Rates of rent burden in this study are slightly higher than other studies that use ACS data have found (Bean, 2012; Fernald, 2015b; Kroll, 2013). One potential explanation for the higher rates of rent burden is the rules that we employ to create our longitudinal data set. We constrain our sample only to households that were renters in each year of the panel, which necessarily excludes households that entered the rental market after being homeowners or exited the rental market in favour of homeownership during the course of the panel. We also exclude households that obtained government-subsidised housing during the panel, resulting in a reduction of roughly 20% of the rental sample. This relatively high figure is likely due to the oversampling of welfare programme participants in the SIPP.

The data presented in Table 1 also highlight the disparities of rent burden and severe rent burden based on a variety of demographic characteristics. First, black and Hispanic households had consistently higher rates of rent burden and severe rent burden for each of the years in the study than did white households. The proportion of Hispanic households experiencing rent burden and extreme rent burden increased dramatically after the recession, making Hispanics the ethnic group most heavily impacted by rent burden in the USA in the post-recession era. Second, in all periods, US native-born households had lower rates of burden than did foreign-born households, and foreign-born households were disproportionately affected in the post-recession period. Third, female-headed households have a persistently higher rate of rent burden and severe rent burden than do male-headed households. Finally, households that include at least one child have significantly higher rates of rent burden and severe rent burden than do households without children.

An analysis of the distribution of rent burden is not complete without considering income disparities among renter households. As Table 1 indicates, lower income renter households are far more susceptible to rent burden and severe rent burden than are higher income renter households. The vast majority of households at the lowest level of monthly household income experienced rent burden and severe rent burden in every year included in this analysis, clearly distinguishing them from wealthier households in the analysis. Among wealthier renter households, rent burden became more prevalent after the recession. This increase in rent burden among higher income households stands in contrast to the steady or slightly declining rate of rent burden among households with lower incomes.

Predicting rent burden

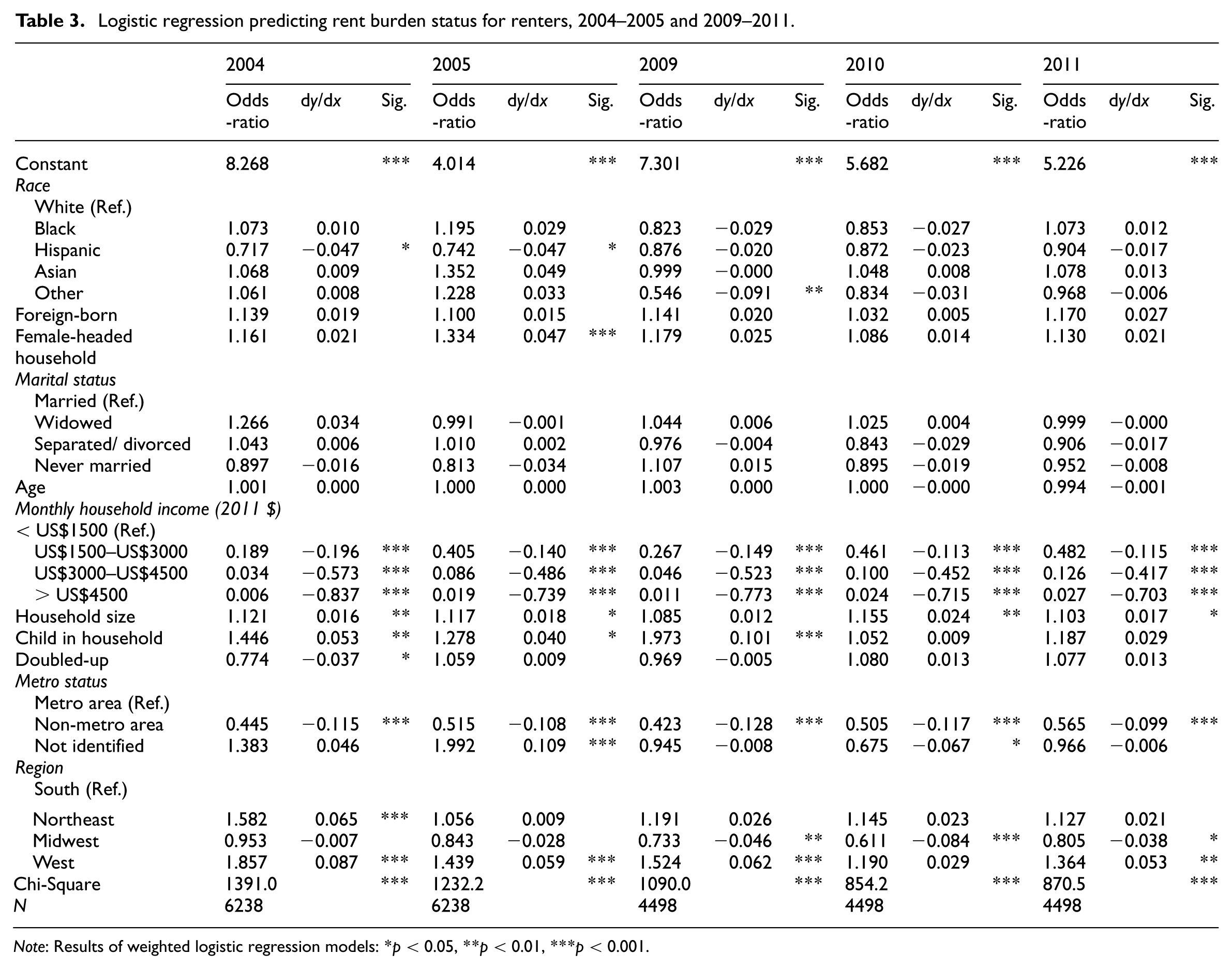

The descriptive statistics suggest that certain demographic groups are at higher risk for being rent burdened. In Table 3, we use logistic regression models to identify those traits and characteristics that predict rent burden after controlling for a variety of covariates. A number of results from the model summarised in Table 3 deserve mention because they do not match the results from the descriptive statistics presented in Table 1. First, the results in Table 3 indicate limited explanatory power of race and nativity status in predicting rent burden in both the pre- and post-recessionary periods. These results suggest that the racial and nativity disparities observed in Table 1 are likely a product of other factors, such as income disparities, rather than a function of race or nativity, per se. One exception is the negative relationship with experiencing rent burden for Hispanic households relative to white households in 2004 and 2005. This relationship is no longer statistically significant in the years after the recession. This result may be explained by how the household incomes of Hispanics map onto the income categories we control for in the models. For example, in 2004 the average monthly household income for Hispanics categorised in the lowest monthly household income category (less than US$1500 per month) was US$866 compared with about US$800 for white and black households. Similar income differences existed in 2005, but not for the post-recession years we include in our analysis. Because of the coarse way that we control for monthly household income in our models, we are not able to account for the fact that in the pre-recession years Hispanic households included in the lowest household income category were wealthier than white households in the same income category and therefore were somewhat less likely to experience rent burden. Second, while female-headed households are disproportionately rent burdened, regression models suggest that gender is not a consistent predictor of rent burden. Odds ratios show that female-headed households are at a higher risk of being rent burdened, but the coefficients are not statistically significant in a majority of the years. Therefore, like the finding related to race and nativity, it is likely that other attributes associated with female-headed households, such as the presence of children and lower incomes, might be the driver of the disparity that is evident in the descriptive statistics.

Logistic regression predicting rent burden status for renters, 2004–2005 and 2009–2011.

Note: Results of weighted logistic regression models: *p < 0.05, **p < 0.01, ***p < 0.001.

While household characteristics such as race, nativity, gender and marital status had limited explanatory power in these models, household size and composition were important predictors of rent burden. Household size was a persistent predictor of rent burden with each additional person in a household associated with an increase in the probability of the household experiencing rent burden by as much as 2% in some years. The presence of at least one child in the house was also associated with a statistically significant increase in the probability of a household facing rent burden in most years considered in the study. These household attributes may produce higher rates of rent burden in two primary ways. First, rent costs may increase as households with more people require larger, more expensive housing. Second, the presence of a child may constrain the earning potential of the adults in that household.

Location also has predictive power regarding the likelihood that a renter household will experience rent burden. Across all years included in this analysis, renter households living in metropolitan areas of the USA faced a significantly higher likelihood of experiencing rent burden than those living in non-metropolitan areas. This difference was relatively consistent across years, with non-metropolitan households 10–13% less likely to experience rent burden than metropolitan households. In addition to the metropolitan versus non-metropolitan split, certain regions of the country were associated with higher levels of rent burden. In many years, renter households living in the Northeast and West of the USA were more likely to experience rent burden than renter households living in the South or Midwest.

These regional differences in rent burden are likely due to the different housing and economic dynamics found in metropolitan and non-metropolitan areas and different regions of the country. For example, earnings for households in non-metropolitan areas are lower than the earnings of households in metropolitan areas, but rental housing costs are typically substantially lower in non-metropolitan areas than in metropolitan areas. On a regional basis, data from the US Census Bureau indicate that household incomes were higher in the West and the Northeast in comparison with the Midwest and the South. At the same time, rental vacancy rates were considerably lower in the Northeast and West (around 7% in 2005) compared with the Midwest and the South (around 12% in 2005).

Of all the predictors included in the logistic models, household income was most important in predicting rent burden. Not surprisingly, renter households with higher monthly incomes were less likely to experience rent burden than were those renter households with lower monthly incomes. Across the years included in this analysis households earning between US$3000 and US$4500 per month were 43–57% less likely to experience rent burden than were households with less than US$1500 of income per month.

As noted above, we rely on utility expenditure and rent data from the SIPP in order to calculate gross rent expenses for households. Given potential concerns over the validity of the utility data in SIPP, we conducted analyses of rent burden without utility costs in order to see if there are systematic differences in the results based on the two different specifications of rent burden. The logistic regression models produce substantively similar results, with the only exception being that non-native born households have a statistically significant and positive association with rent burden in the model in which utility costs are excluded. Given that nativity is the only difference in the two models, we feel comfortable that the utility cost data in SIPP did not distort the key findings of this study.

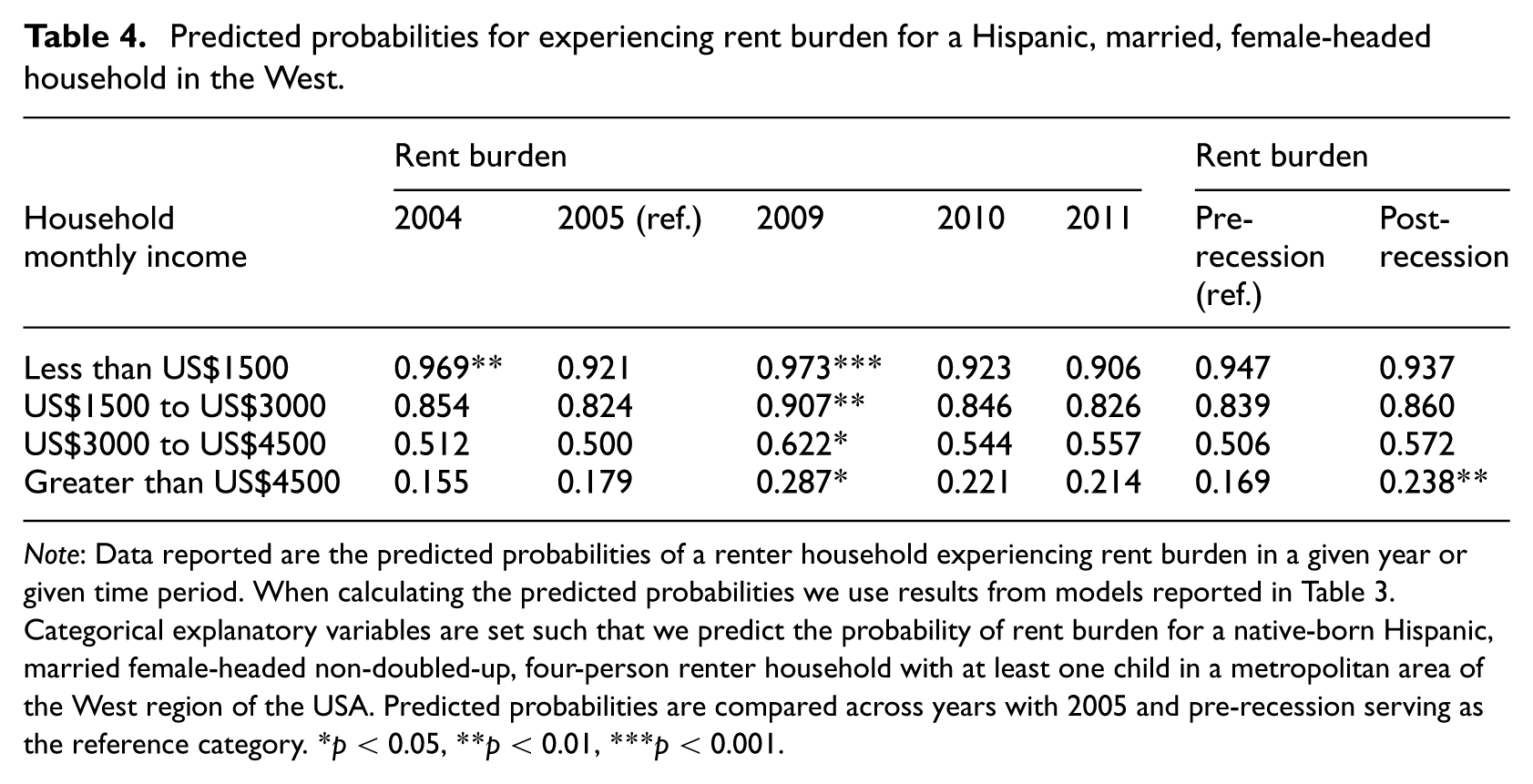

The results of the logistic regression models described above help to explain the relationship between various covariates and rent burden, but do not assess the likelihood of a specific household actually experiencing rent burden. In addition, the non-linear form of the logistic regression model makes it difficult to easily assess the likelihood that a household will experience rent burden. In Table 4, we present a set of predicted probabilities of experiencing rent burden for two hypothetical households at various income levels. We use the results from models presented in Table 3 to calculate the predicted probabilities for rent burden. When calculating the predicted probabilities we specify categorical predictors at pre-determined values, such that we model predicted rent burden probabilities across a range of household incomes for a native-born Hispanic, married, female-headed, non-doubled-up, four-person renter household with at least one child living in a metropolitan area of the West region of the USA.

Predicted probabilities for experiencing rent burden for a Hispanic, married, female-headed household in the West.

Note: Data reported are the predicted probabilities of a renter household experiencing rent burden in a given year or given time period. When calculating the predicted probabilities we use results from models reported in Table 3. Categorical explanatory variables are set such that we predict the probability of rent burden for a native-born Hispanic, married female-headed non-doubled-up, four-person renter household with at least one child in a metropolitan area of the West region of the USA. Predicted probabilities are compared across years with 2005 and pre-recession serving as the reference category. *p < 0.05, **p < 0.01, ***p < 0.001.

The results in Table 4 indicate that household income is an important factor in predicting rent burden. For households that fall into the lowest income category considered in this analysis (less than US$1500 per month) the predicted probability of experiencing rent burden was above 90%. Higher income categories were associated with progressively lower predicted probabilities of rent burden. In all income categories there was a significantly higher predicted probability of experiencing rent burden in 2009 compared with 2005. When compared with 2005, differences in the predicted probabilities of experiencing rent burden in 2010 and 2011 were no longer statistically significant, indicating that the effect of the recession on rent burden may have waned over time. To increase the statistical power of the models, we collapsed the data from 2004–2005 and 2009–2011 into pre and post-recession models, respectively. When comparing the predicted probabilities from the pre-recession period (2004–2005) to the post-recession period (2009–2011), there was a statistically significant increase in the probability of rent burden among the highest income households.

Behavioural responses to rent burden

In order to understand how exiting from rent burden changed after the Great Recession, we examined the rate of exit from rent burdened status both before and after the recession. Exits can only be calculated for periods where two consecutive years of data are available for the same households, so in this analysis we calculate the rate of exit from rent burden for 2005, 2010 and 2011. For example, a 2005 exit occurred if a household was rent burdened in 2004 and no longer rent burdened in 2005. Results suggest that households were less likely to exit rent burden in the post-recession period when compared with the pre-recession period. For example, 26.8% of households that were rent burdened in 2004 exited rent burden in 2005. After the recession, exit rates fell to 24.8% in 2010 and 23.5% in 2011 (the difference in exit rates between 2005 and 2010, and 2005 and 2011 were statistically significant at least at the 95% confidence level). These results indicate that the difficult economic and rental market conditions that prevailed after the recession may have constrained the ability of households to escape a rent burdened state.

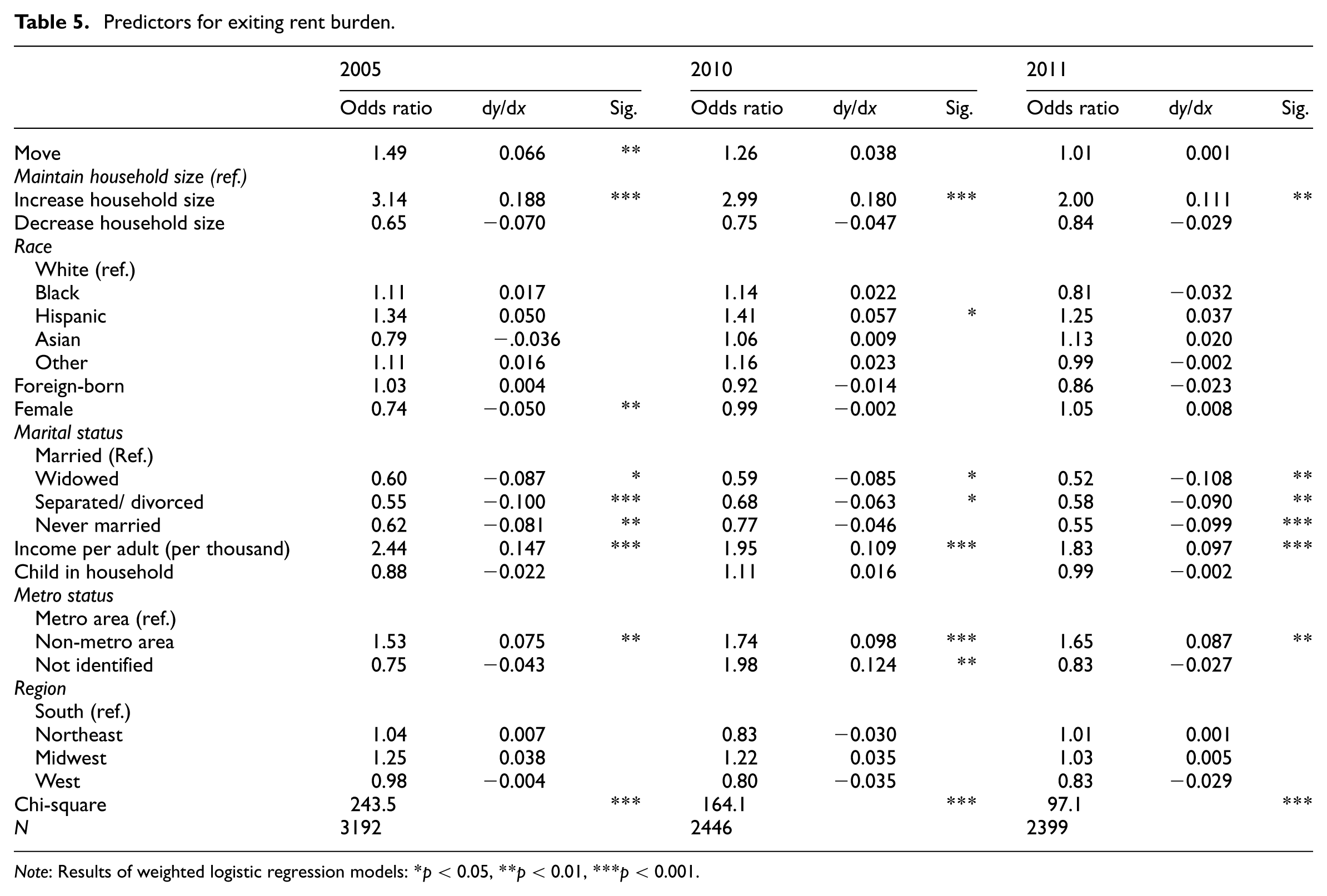

When faced with rent burden, households may respond in a variety of ways to mitigate the financial stress. Two potential household responses include moving, presumably to a cheaper residence, and increasing the number of rent-paying adults living in the household. After constraining the sample to households that were rent burdened in a given year, we estimate a series of logistic regression models to predict whether moving or changes in household composition are associated with exits from rent burden in the following year. Our regression model includes dummy variables for three behavioural responses: moves, increases in the number of adults in the household and decreases in the number of adults in a household. In addition to these dummy variables, we also include a series of covariates that control for demographic characteristics, household attributes and location. In contrast to previous models where we control for household income using dummy variables for household income levels, in these models we control for household income per adult. We make this change because including changes in household size as a variable in the model has implications for aggregate household income and potentially introduces collinearity in a model that also controls for total household income.

As summarised in Table 5, results from these models suggest that higher per adult household income and increases in household size have positive relationships with exiting rent burden. This is true both before and after the recession, but the magnitude of both effects wanes in the years after the recession. Moving has a positive relationship with exiting rent burden in 2005, but has no effect on exiting rent burden in the post-recession years, perhaps reflecting rising rents and stagnant household incomes after the recession. Gender had an effect on exiting rent burden prior to the recession, when female-headed households were about 5% less likely to exit rent burden than male-headed households, but gender did not have a statistically significant relationship with exiting rent burden after the recession. In all years married households had an advantage in exiting rent burden in comparison with the different types of non-married households. This analysis also demonstrates that households in non-metropolitan areas were more likely to exit rent burden than were similarly situated households in metropolitan areas, which is potentially explained by the lower rents typically found in non-metropolitan areas compared with metropolitan areas.

Predictors for exiting rent burden.

Note: Results of weighted logistic regression models: *p < 0.05, **p < 0.01, ***p < 0.001.

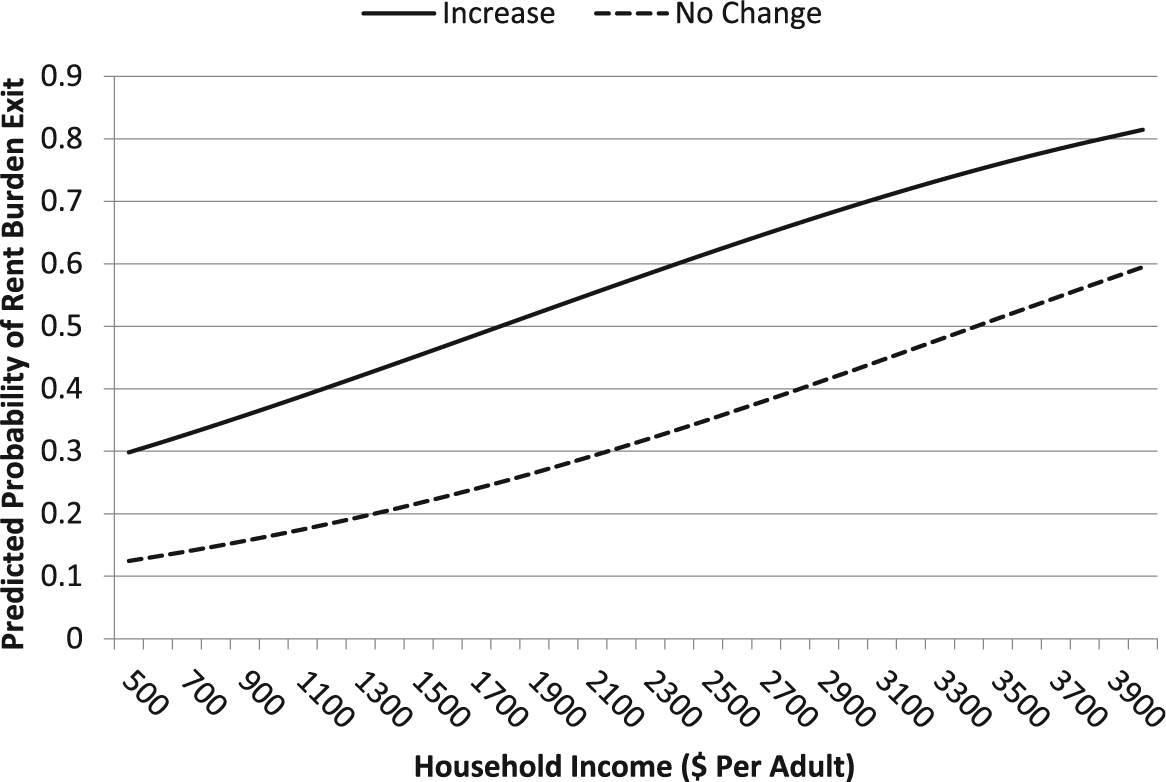

To help interpret the results from the models presented in Table 5 we calculated predicted probabilities for exit from rent burden in 2010 for a household that increased the number of adults compared with one that maintained the same number of adults living in the household. When calculating the predicted probabilities we specify categorical predictors at pre-determined values, such that we model predicted probabilities of exiting rent burden across a range of household incomes for a native-born black, married, male-headed, non-doubled-up renter household with at least one child living in a metropolitan area of the West region of the USA. Figure 1 demonstrates that increasing household size improved the probability that a rent-burdened household would exit that state. Households that changed their household size by adding one or more adults increased their household incomes by approximately 50% and were much more likely to exit rent burden than comparable households that did not increase the number of adults in the household.

Predicted probabilities for exiting rent burden for households with an increase and no change in the number of adults in the household (2010).

The effectiveness of increasing household size as a strategy for exiting rent burden decreased over time. Figure 2 illustrates the predicted probability of exiting rent burden for households that increased the number of adults living in the household for 2005, 2010 and 2011. In Figure 2, we model predicted probabilities of exiting rent burden across a range of incomes for the same hypothetical household used in Figure 1. The predicted probability curves indicate that increasing the household size for a household with US$1500 household income per adult resulted in a predicted probability of exiting rent burden of about 57% in 2005, 45% in 2010 and only 32% in 2011. Thus, the strategy of increasing household size as a means of exiting rent burden was significantly less effective in the post-recession years.

Predicted probabilities for exiting rent burden for households with an increase in the number of adults in the household (2005, 2010 and 2011).

Sensitivity analysis

To assess the robustness of the findings described above, we conducted two series of sensitivity analyses. First, rather than making rent burden a dichotomous variable in which a household is either burdened or not, we created a continuous rent burden variable equal to the ratio of gross household expenses to income. Both the descriptive statistics in Table 1 and the results of the logistic regression in Table 3 were very similar when predicting a continuous rent burden dependent variable. Specifically, similar disparities exist in the descriptive statistics and in the regression model, while the same independent variables tend to be significant when the dependent variable is a continuous measure of rent burden.

The second sensitivity analysis addresses potential concerns about the different composition of the samples in the pre- and post-recession periods. Although the samples are nationally representative, there are differences in the composition of the rental households used in each period. Therefore, in order to isolate the role of the recession on rent burden outcomes, we employ a propensity score matching approach in which sample households are matched based on observable characteristics. Using the recession as the treatment effect, the analyses show a statistically significant average treatment effect on the treated. The interpretation of this result is that the probability of rent burden among the treatment group (post-recession) was significantly higher than the probability of rent burden among the control group (pre-recession). The matching results suggest that the differences found in this study between the pre- and post-recession periods are most likely not a function of changes in the composition of the samples.

Discussion

In this article, we present results from a series of predictive models that help to explain the characteristics associated with risk for rent burden for renter households. Although descriptive statistics suggest significant racial- and nativity-based disparities in experiencing rent burden during these time periods, those disparities disappeared after controlling for income and other household attributes. Instead, logistic regression models suggest that households with lower incomes, larger households, households with children and households in metropolitan areas are highly associated with increased risk of rent burden.

The comparison of periods before and after the Great Recession produces interesting findings. First, rent burden has unambiguously increased post-recession and this finding is consistent with findings from previous studies. Second, exits from rent burden appear to be more challenging after the recession, as tight rental market conditions and stagnating earnings may have frustrated efforts by households to exit a rent burdened state. Finally, after the recession, rent burden has become more pervasive for higher income households. Given the challenging rental housing market conditions in the USA, there is a risk that rent burden will continue to persist at historically high levels, and affect an increasingly affluent set of households.

The findings of this study are relevant for advocates and policymakers concerned about the affordability of housing in the USA. One strategy that policymakers could pursue to reduce rent burden in the USA is to offer more government-subsidised housing, but in our assessment, the appetite for this kind of policy change is waning. A different approach might be to follow the lead of some states that offer renter households, perhaps below a given household income threshold, the ability to deduct some portion of their rent payments from their incomes for tax purposes. Such a policy would mimic the well-known and politically popular policy that allows homeowners to deduct mortgage interest and property tax payments from their incomes when calculating their tax burden. Other scholars have suggested modifications to the Earned Income Tax Credit (EITC) program in the USA that would offer additional money to recipients to defray housing expenses (Stegman et al., 2003). A more market-based solution is to reduce restrictions on residential density in developments in exchange for the inclusion of subsidised housing (Mukhija et al., 2010). Such a policy would increase the supply of housing and reduce the cost to build housing, while producing housing that is specifically affordable to lower income households. While these policy suggestions hold some promise of reducing rent burden, it is important to keep in mind that households with extremely low incomes require deeper housing subsidies than market-based solutions for affordable housing are typically designed to offer.

While the problem of rent burden has crept up the income ladder in the years since the Great Recession, it is important to not lose sight of the fact that rent burden is a problem that is disproportionately experienced by renter households with low and moderate household incomes. Thus, our research findings provide some nuance to the idea that housing tenure is an important component of class distinctions in the USA (Shlay, 2015). While we often acknowledge social, political and economic power differentials between homeowners and renters in a way that reflexively confers higher status to homeowners over renters (Shlay, 2015), it is also true that renters as a group are stratified by the same characteristics. As rents increase and incomes stagnate, larger proportions of household income devoted to housing can put a strain on a greater number of households in the USA, but particularly those renters at the lower end of the income spectrum. For these renter households, housing costs may crowd out expenditures on food, clothing and other basic necessities, much less investments in human capital that play an important role in increased socioeconomic mobility. As rent burden increases, households are more prone to housing insecurity and the negative consequences, including increased unemployment, associated with evictions and other types of forced displacement (Desmond and Gershenson, 2016). Thus it is possible to see how renting housing in the USA subjects households to additional financial stresses related solely to status as a renter without any of the tax benefits that accrue to homeowners.

Solutions to rent burden pursued by households, such as moving or increasing the number of adults in the household, may help to resolve the rent burden problem but also could carry substantial costs that afflict renters disproportionately. For example, moving to a cheaper apartment may resolve rent burden, but disrupt place-based, supportive social networks that are important for psychological and material wellbeing. How long such disruptions last and what longer-term effects they might have on household members is contested (Pettit, 2004). Though the negative effects often attributed to overcrowded residential situations are disputed (Myers et al., 1996), it is reasonable to believe that at some point adding an additional adult to a household to help pay for rent can also increase social tension as more people share a fixed amount of living space (Skobba and Goetz, 2015). Once again, because lower income renter households disproportionately experience rent burden, it is lower income renter households that are more likely to face the potential costs associated with residential moves and increased household sizes. Thus, the research findings from this article support the idea that housing costs for renters are an important, and often overlooked, component of the larger story of rising inequality in American society.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.