Abstract

Concerns about global warming and growing scarcity of fossil fuels require substantial changes in energy consumption patterns and energy systems, as targeted by many countries around the world. One key element to achieve such transformation is to increase energy efficiency of the housing stock. In this context, it is frequently argued that private investments are too low in the light of the potential energy cost savings. However, heterogeneous incentives to invest in energy efficiency, especially for owner-occupants and landlords, may serve as one explanation. This is particularly important for countries with a large rental sector, like Germany. Nevertheless, previous literature largely focuses on the payoffs owner-occupants receive, leaving out the rental market. This paper addresses this gap by comparing the capitalisation of energy efficiency in selling prices and rents, for both types of residences. For this purpose data from the Berlin housing market are analysed using hedonic regressions. The estimations reveal that energy efficiency is well capitalised in apartment prices and rents. The comparison of implicit prices and the net present value of energy cost savings/rents reveals that investors anticipate future energy and house price movements reasonably. However, in the rental segment, the value of future energy cost savings exceeds tenants’ implicit willingness to pay by a factor of 2.5. This can either be interpreted as a result of market power of tenants, uncertainty in the rental relationship or the ‘landlord–tenant dilemma’.

Introduction

The energy efficiency of real estate plays a key role in policies directed towards low carbon economies. In industrialised countries, for example, about 40% of total energy consumption is used for space heating and cooling (OECD, 2003). In most studies on residential energy consumption, energy is understood as input for the production of housing services like a warm home. Energy, however, can be substituted by capital inputs, i.e. energy efficiency investments, which have been identified as cost-effective alternatives to energy inputs. Scholars in the fields of climate policy as well as energy economics identified the so-called ‘energy efficiency gap’– the finding that energy efficiency measures are underutilised compared to their potential energy cost savings (see, e.g., Allcott and Greenstone, 2012; Bardhan et al., 2013; Schleich and Gruber, 2008). The fact that so many households do not exhaust the potentials of retrofitting appears puzzling to many authors (see, e.g., Eichholtz et al., 2010, 2013; Mills and Schleich, 2012; Nair et al., 2010).

One reason might be the so far under-researched threefold character of real estate in the energy efficiency context: it serves as production input for firms, as consumption good for households, and as financial asset for investors (which also holds for energy-intensive appliances in general; See Davis, 2008). In the residential context, research particularly focuses on housing as owner-occupied consumption good, i.e. the choice and valuation of the efficient production technology of energy intense services (Quigley, 1984). However, most home owners, even owner-occupants, understand their property also as financial asset. They might expect, additional to cost savings, returns from investment in terms of capital gains when reselling their property. This is particularly true for the case of rental apartments. Landlords are most likely not interested in energy savings per se – they are interested in the value and economic benefits energy efficiency generates in terms of sale price and rental income increases, as well as vacancy risk reductions. As most studies argue, landlords often cannot pass on the investment costs to tenants due to market imperfections, which is called the ‘landlord-tenant dilemma’ (see, e.g., Schleich and Gruber, 2008). As a result, it is argued that landlords – compared to owner-occupants – produce less energy efficient homes, which is confirmed by empirical studies (see Rehdanz, 2007).

Thus, to comprehensively understand investors’ rationale, particularly that of landlords, research should also analyse the potential effects energy efficiency has on the selling price of a dwelling and the generated rental income streams. However, while changes in price, rental income, or the risk of vacancy must be considered as important determinants of investment decisions, the influence of energy efficiency has only been selectively studied. Available insights are focused on US housing markets and are largely limited to the analysis of owner-occupied residences. The findings suggest that energy savings are efficiently capitalised in house prices. However, while there are several studies which analyse the impact of energy efficiency on office prices and rents, there are still very few papers that would empirically address economic benefits for landlords, i.e., how energy efficiency affects rental income or selling prices (to our knowledge, to date only Hyland et al. 2013, and Fuerst et al., 2015, assess this aspect). For a long time, this could have been explained by a lack of data. However, this has changed and a growing number of researchers are evaluating the economic effects of ‘green’ real estate investments in different contexts (e.g. Brounen et al., 2012; Eichholtz et al., 2010, 2013; Fuerst and McAllister, 2011).

The aim of the present paper is to compare the willingness of owner-occupants, landlords, and tenants to pay for energy efficiency and to gain deeper insights about the underlying investment rationale. In a first step, we analyse how energy requirements for space heating capitalise in rental and owner-occupied apartment prices. In a second step, we assess the impact of energy efficiency on rents. Based on this information and actual energy prices, we evaluate in a final step whether homeowners’ calculations are grounded on reasonable discount rates and expectations. These questions are analysed using micro-data from Berlin’s housing market. Thereby, we benefit from the growing online market for residences and use data obtained from the leading online housing market portals in Germany, immobilienscout24.de, immonet.de and immowelt.de. In hedonic regressions, we then include the energy performance of buildings as an explanatory variable, along with an extensive set of control variables. Energy performance is measured as the annual energy consumption in kilowatt-hours per square meter of residential living space (kWh/[

The remainder of this paper is structured as follows. In the next section, we provide a brief overview of the relevant empirical literature on energy efficiency capitalisation in real estate prices and rents. We proceed by summarising the underlying arguments, which constitute the ‘landlord-tenant’ or ‘investor-user dilemma’. The third section outlines our empirical strategy, the methods used, and describes the data employed in our study. We then discuss the empirical results and their implications.

Related literature

Empirical studies

The number of studies dealing with the effects of energy efficiency investments on the value of real estate is limited. Most of the recent literature focuses on commercial real estate and analyses the effects of Energy Star® and Leadership in Energy & Environmental Design (LEED) certification schemes (e.g. Eichholtz et al., 2010, 2013; Fuerst and McAllister, 2011). These studies found significant positive effects of environmental certification on real estate prices, office rents, and vacancy risk.

The first generation of studies on residential real estate point in the same direction. These studies, conducted in the 1980s, were all based on US real estate transaction data. Potential effects of energy performance on residential property are, in most cases, analysed based on very small samples of detached or semi-detached dwellings, located in one single city or neighbourhood. All the studies rely upon hedonic regressions, some specifying the functional form using Box-Cox methodology.

The first study by Halvorsen and Pollakowski (1981) analyses sales price spreads between homes having oil and gas-fired heating systems installed. The results suggest that abrupt oil price shifts, like those in the 1970s, are associated with an immediate price decrease of houses using this energy source. Johnson and Kaserman (1983) and Dinan and Miranowski (1989) come to the conclusion that a $1 decrease on the energy bill is capitalised in sales price increases that vary between $11.63 and $20.73 per m2. Laquatra (1986) estimates the implicit price for thermal integrity to be $2510 per unit, indicating, with Horowitz and Haeri (1990), that energy savings are efficiently capitalised in housing market transactions. However, these early studies mainly suffer from very small sample sizes and thus from a potential loss of generality.

The first study that uses a substantially larger amount of transactions was conducted by Nevin and Watson (1998). It is based on data from the American Housing Survey, covering 30 metropolitan statistical areas. In multiple regressions, the authors analyse the impact of utility expenditures on house prices and conclude that housing markets efficiently value energy cost savings. However, while the study employs a larger sample, it lacks accuracy. The paper relies on total utility expenditure instead of energy costs. Thus, general maintenance costs and the specific effects of energy efficiency cannot be disentangled.

The second generation, studies published since 2011, tried to resolve the paucity of small samples by combining transaction data with ‘green’ certification ratings: Brounen and Kok (2011), Bloom et al. (2011), Kahn and Kok (2014), Deng et al. (2012), Walls et al. (2013), and Hyland et al. (2013) all find positive impacts, especially from LEED and Energy Star certifications schemes. But these studies also have shortcomings. Since the certificates only require minimum standards of energy efficiency, the exact value of energy savings cannot be identified in this context. Hyland et al. (2013) match their rating schemes with the results of an engineering model, to compare the potential energy costs savings with the implicit prices. They find that sales prices equal 64%–79% of the net present value (NPV) of energy cost savings, while rents cover about 14%–55% of future energy costs. Overall, Fuerst et al., (2015) provide supporting evidence for the efficient capitalisation of energy performance in house prices for the case of Wales. They conclude, that the lower implicit returns on energy efficiency for landlords compared to owner-occupiers leads to a leveling of prices between energy efficiency classes.

To summarise, the existing literature indicates that – at reasonable discount rates – energy efficiency is well capitalised in house prices. However, the evidence is concentrated on US housing markets. Notably, only few studies (Brounen and Kok, 2011; Deng et al., 2012; Högberg, 2013; Hyland et al., 2013) provide insights on European or Asian housing markets. Moreover, most studies available analyse single-family detached or semi-detached housing, which is most likely to be owner-occupied. There is only one study to date, Hyland et al. (2013), that covers house sales in the rental housing segment, an important market in many countries. This appears even more surprising, given the emphasis of the literature on the discussion of the so-called ‘landlord-tenant dilemma’. In this light, further studies which empirically assess the effects of energy efficiency on rental housing prices and rents appear long overdue.

The impact of the rental relationship on house prices

In the literature on energy efficiency investments, the specific problems in the rental relationship are described as the ‘landlord-tenant dilemma.’ It is argued that neither landlords nor tenants have sufficient incentives to invest because both groups face substantial market failures and market imperfections. The key problems identified are asymmetric information, prohibitively high transaction costs, and uncertainty (Allcott and Greenstone, 2012; Davis, 2011; Levinson and Niemann, 2004; Schleich and Gruber, 2008). In this context, the following arguments are frequently presented.

Typically, tenants cannot evaluate the real quality of a dwelling due to limited technical understanding or missing information on the efforts undertaken by the landlord to produce a certain quality.

A second potential source for reduced WTP of tenants is that they apply relatively high discount rates to future energy savings and energy price increases (Hassett and Metcalf, 1993). In addition, the length of the rental relationship is frequently uncertain, not least because tenants can – in case of strong surges in energy prices – move to a more energy efficient dwelling at comparably low transaction costs. This decreases WTP of tenants compared to owner-occupants.

Moreover, it is claimed that transaction costs incurred when concluding the rental contracts, which allow to fully appropriate the returns of energy saving investments from energy efficiency investments to either the landlord or the tenant (depending on who invests in energy efficiency), are prohibitively high (Schleich and Gruber, 2008).

Typically, housing market mechanisms and the resulting rent asking strategies by landlords are disregarded in the literature on energy efficiency investments. However, these should also play an important role for differences in the implicit price of rented out versus owner-occupied dwellings.

The most important insight in this context is the following one: even if landlords are able to credibly transmit the information about energy savings, this does not imply that tenants are willing to pay the rent (

where

Commonly, excess supply hands over market power to tenants, at least to some extent. 2 In the present context, the value of energy efficiency in a rental dwelling (everything else constant) should be lower compared to the value of energy efficiency in an owner–occupied home, because owner–occupants can fully benefit from energy cost savings.

In summary, all arguments presented indicate that landlords’ returns from energy efficiency investments are likely to be lower compared to those of owner-occupants. Consequently, the NPV and hence the implicit price of energy efficiency should be lower than it is for owner-occupied dwellings as well.

Empirical strategy

Based on the empirical findings and arguments presented in the literature, the empirical strategy to identify potential differences between the capitalisation of energy efficiency in owner-occupied and rental dwellings relies on standard hedonic estimation methods. First introduced by Rosen (1974), hedonic regression models are frequently applied instruments to evaluate the implicit prices of housing characteristics, local amenities, and accessibility (for recent applications see, e.g., Ahlfeldt, 2013; Fuerst et al., 2011; Moro et al., 2013).

In equation (2), the dependent variable is the log price of a dwelling i per square meter (

where

In a second step, we use a data set of rental apartments and regress the monthly rental income per square meter (

where

Data and stylised facts

Housing market conditions and energy prices vary substantially across regions. Accordingly, the value of energy efficiency should also show a distinct regional pattern. Since it is difficult to appropriately control for the specific regional impacts, we concentrate on the Berlin housing market, where already beginning in 2005, the market conditions became more favorable for real estate investors.

Data sources and quality

Empirical real estate research is data demanding. In the past, detailed housing market analysis was not possible due to a lack of information on real estate transactions (DiPasquale, 1999; Eichholtz et al., 2013; Gyourko, 2009; Olsen, 1987). In this study, as alternative to conventional transaction information, we use data collected from Internet rental and selling advertisements of apartments in Berlin. The data were downloaded on a monthly basis from June 2011 through December 2014 from the three most popular German real-estate websites: immobilienscout24.de immonet.de, and immowelt.de. The ads placed on the three websites contain extensive information on numerous structural and locational characteristics of the properties for sale/rent.

However, using Internet advertisements in this context suffers from four major shortcomings that are addressed in the empirical analysis. First, Internet data are often plagued by invalid or duplicated observations. Some advertisements are likely to be published on different websites simultaneously. The duplicates can cause serious distortions of the estimation results. Therefore, we applied a matching algorithm specifically designed to identify duplicates in the data.

Second, the websites might be used by realtors or construction companies for marketing purposes. Some objects, especially apartments offered for sale, are not constructed yet and such ads are placed by the construction firms in order to attract new customers. Hence, a substantial share of these dwellings only exists on paper and might never be built. Not accounting for this would lead us to biased results. Therefore, we identified real new apartments by screening the free text description of the apartments for sale in the ads. In a nutshell, this classification is based on the coefficients of a logit estimation where fake advertisements are included as a binary 0/1 dependent variable. Indicators on whether the apartments are built or not are used as regressors (e.g. future or current year as construction year, key words such as ‘new’ and/or ‘under construction’ etc.). The resulting variable ‘non–existent’ is the inverse probability that the apartment is constructed in reality. 3

A third serious objection against using asked prices and rents in Internet ads is that they may deviate from the final, or transaction, prices and rents. Although appraised data are reported as a valid substitute for real transaction information (Hyland et al., 2013; Malpezzi, 2003), there are only few studies that evaluate the degree of a deviation from transaction prices. The two most prominent studies for Germany are that of Faller et al. (2009) and Henger and Voigtländer (2014). Faller et al. (2009) investigate the differences between offer and transaction prices for Northrhine-Westphalia. Their findings indicate that on average the offers are 8% above the real transaction prices. Including controls for housing characteristics did not turn out to be an explanation for the observed differences. Significantly smaller gaps are found for urban locations and during market expansions, with marginal explanatory power for some housing characteristics (Henger and Voigtländer, 2014).

More generally, systematic mis-pricing of housing characteristics has been found to be very costly to the seller (Knight, 2002; Merlo and Ortalo-Magne, 2004), which is in line with theoretical models of seller behaviour (e.g. Knight et al., 1994). It increases time on the market and reduces the final transaction price. Both effects make it more likely that measurement errors (differences between listing and transaction prices) are unrelated to housing characteristics. This is confirmed by empirical evaluations: among others, Knight et al. (1994) and Semeraro and Fregonara (2013) analyse listed prices and the respective transaction data. Both studies find that coefficients changed only slightly when moving from listed to realised prices. Three out of four coefficients for housing characteristics in Knight et al. (1994) were statistically equal across regressions, although all t-values were greater than six. The only exception is the variable ‘living area’ where the change of coefficients was statistically significant, but small.

Finally, there may be systematic differences between advertisements including and excluding information on the energy performance of a dwelling. Until May 2014, sellers and landlords were not obliged to publish energy performance scores (EPS) in their offers. Therefore, it is necessary to compare the characteristics of both groups of ads: those containing EPS and those that do not. In case of systematic differences between these two groups, estimation results exclusively based on ads including EPS would be biased. Indeed, tests reveal significant differences between the groups. Therefore, it is important to use methods that correct for this selection bias.

Despite these potential data imperfections, we opt for using the data from Internet ads and correct for the sample selection bias by estimating a Heckman two–stage model. The main reason is that alternative data, containing information on energy consumption, house prices, and rents at the micro level, 4 simply do not exist. Moreover, we concentrate upon a large city experiencing a housing market expansion in recent years, which implies significant market power of sellers and landlords. According to the literature, discrepancies between asked and real prices/rents should be relatively small in the first place, while there is only little evidence for a potential systematic mis-pricing of housing characteristics. Moreover, we evaluated the differences between the listed and realised transactions prices for a subsample of our data. The comparison of 29,680 matched transactions from Gutachterausschuss and online ads reveals that differences between both numbers are rather small, and, most importantly, the results are highly robust to the particular choice of the dependent variable. 5

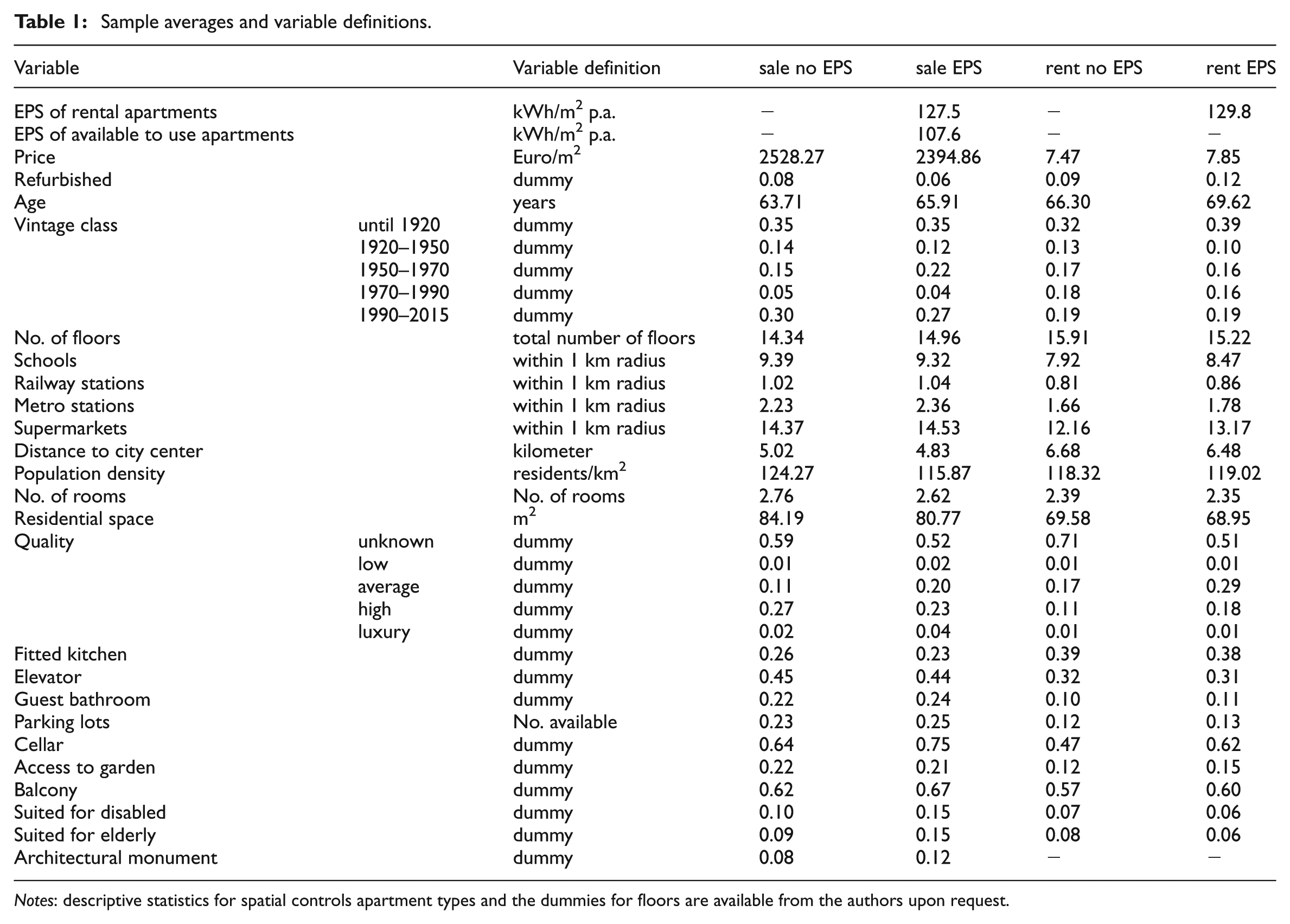

Variable definitions and descriptive statistics

Table 1 presents the descriptive statistics on apartments for rent and for sale. In Berlin, the ‘typical’ dwelling for sale is generally larger and better equipped compared to a rental apartment.

Sample averages and variable definitions.

Notes: descriptive statistics for spatial controls apartment types and the dummies for floors are available from the authors upon request.

Rents and apartment prices

The dependent variables in equations (2) and (3) are the logs of the asked selling price and the asked monthly rent, respectively. Both measures are reported in euros per square meter. In the period under consideration, both prices and rents follow an upward trend – to account for these price movements over time, we include dummies for each month. Again, since we analyse prices in an expanding market, we believe that potential bias between realised prices/rents in transactions and asked prices/rents in advertisements is rather small.

Energy certificates and occupancy status

The first key explanatory variable is the energy performance of buildings – since 2009, it is mandatory for each landlord/seller of a dwelling to provide information on the heating energy requirements of a building if prospective tenants/investors ask for it (European Commission, 2002). The German ‘Energy Performance of Buildings Directive’ (Energieeinsparverordnung, EnEV) allows for two alternative ways of obtaining such a measure. The first one is based on real energy billing information. The so-called ‘consumption based’ energy certificates are normalised to the climatic conditions of the city of Würzburg in the year 2002.

To mitigate a potential user bias, which is the main point of criticism for this measure, performance based certificates are only applicable for apartment buildings and must be calculated as the average of three subsequent heating periods. Furthermore, the EPS refers to the entire building. If the size of the dwelling is small relative to the building’s size, this reduces user bias considerably. The alternative ‘performance based’ measure is based on an engineer’s assessment of the thermal conductivity of a building. The outcome is the theoretical heating energy requirement of a house. Both approaches are intended to be comparable in terms of their outcomes as they provide measures for the annual heating energy requirement (in kilowatt-hours) per square meter of residential space. Arguably, in case of apartment housing, the consumption based measure is by far more frequently applied, since it is easy to calculate and cheaper in the certification process. Typically, EPS ranges from zero to 300 kWh/[

The second key variable of interest is the occupancy status of the apartment for sale. Typically, this variable is included in the ads, because it is an important selection criterion for potential buyers. Since tenancy law in Berlin – if the actual tenant wants to stay in the apartment – forbids a transformation from rental to owner-occupation within a period of seven years after the sale, it is unlikely that investors aim to buy currently rented out dwellings for the purpose of owner-occupation. The German ‘Homeownership Law’ (‘Wohneigentumsgesetz’, WEG), German Civil Code (‘Bürgerliches Gesetzbuch’, BGB), and the Berlin-specific ‘Tenant Eviction Regulation’ (‘Kündigungsschutzklauselveror dnung’) delegate substantial rights to the tenants living in an apartment, which should be sold for purposes of owner-occupation. 6 Alternatively, a potential buyer can try to compensate the tenant for agreeing to cancel the contract. This, however, is costly and should be negatively capitalised in the property price. In our estimation, a dummy variable indicates whether the apartment refers to the rental segment or can be used directly in owner-occupation. 7

Control variables

In the rich literature using hedonic methods in real estate appraisal, various variables have been proven to be important predictors of the property prices. In our study, we control – as far as possible – for the most frequently tested features (see, for a comprehensive summary, e.g., Malpezzi, 2003). The variables included are summarised in Table 1.

Size and type of the dwelling: In almost any study, the size of the dwelling is included as explanatory variable for the (rental) price. In the present paper, size is captured by the number of rooms as well as the total area. Moreover, the studies generally distinguish between the dwelling’s type: In particular, we control for potential effects if the apartment is, for example, a loft, a penthouse, or a souterrain dwelling.

Comfort: The general comfort of an apartment can be characterised by different attributes. Using dummy variables, we control whether an elevator, a cellar, a fitted kitchen, a guest bathroom, or a parking lot is available and if access to a garden or a balcony is included. Moreover, we control if the dwelling is suited for elderly or disabled people. To capture potential differences in the quality of a dwelling, we use the information in the ads indicating whether the apartment is of low, average, high, or luxury quality.

Building attributes: the age of a dwelling is associated with a certain ‘natural’ quality of housing. The housing built in different decades is characterised by specific architectural design, materials, and construction techniques employed as well as aspects of urban planning that affect the quality of life in the apartments. To account for potential differences in the architectural design, we include measures that capture the vintage class of a building, the age of the building, whether it is an architectural monument, and the size of the house approximated by the number of floors.

General housing condition: The general condition is also important for the quality of a dwelling – it should clearly make a difference to potential tenants or buyers, whether an apartment is newly constructed, refurbished, or non-refurbished. Consequently, we include dummies indicating the refurbishment status of a home.

Accessibility: Standard urban economics theory suggests that accessibility is one of the most important predictors for house prices and rents. As common variable to control for this effect, the distance to the city center is used in many hedonic studies. We include the distance in kilometers to the closest of the two main city centres of Berlin: either ‘Gedächtniskirche’ (West Berlin) or ‘Rotes Rathaus’ (East Berlin). The coordinates of advertised apartments are determined using the official list of Berlin’s addresses. 8

Amenities: Moreover, we use the exact coordinates to determine the endowment with local amenities, which play an important role for house prices and rents. We count the number of schools, supermarkets, and metro stations at foot distance (within 1 km radius) as a measure for local infrastructure endowment. To account for neighbourhood characteristics, we add population density. Moreover, we include dummy variables for the 12 districts of Berlin.

Finally, to capture the recent surge of house prices, we include a monthly time trend in the estimation.

Methods

As outlined in the section ‘Data sources and quality’ we face a serious selection bias in our data. While it is obligatory to have an energy performance certificate for each dwelling for sale or for rent since 2009, it was optional to report the energy performance score in online advertisements until May 2014. Obviously, this creates incentives to report only EPS that indicate low energy costs. Thus, we have reason to believe that the estimates obtained from a sample restricted to only those observations including EPS would be biased. One way to correct for such bias is to calibrate a Heckman selection model (Heckman, 1979), as also proposed by Hyland et al. (2013) in an analogous context.

The underlying intuition is that one observes a property price or rent that reflects the energy performance of a building adequately, only if the EPS was reported to the investor or the potential tenant. Otherwise, one observes a price, which does not explicitly reflect energy efficiency. In this context, EPS can be interpreted as an omitted variable that potentially affects both the level of the price and the coefficients of other housing attributes, since increased energy efficiency allows to substitute energy expenditures and other housing services. Missing information on the energy performance imposes uncertainty on potential buyers and tenants, which potentially results in decreased WTP for other housing attributes.

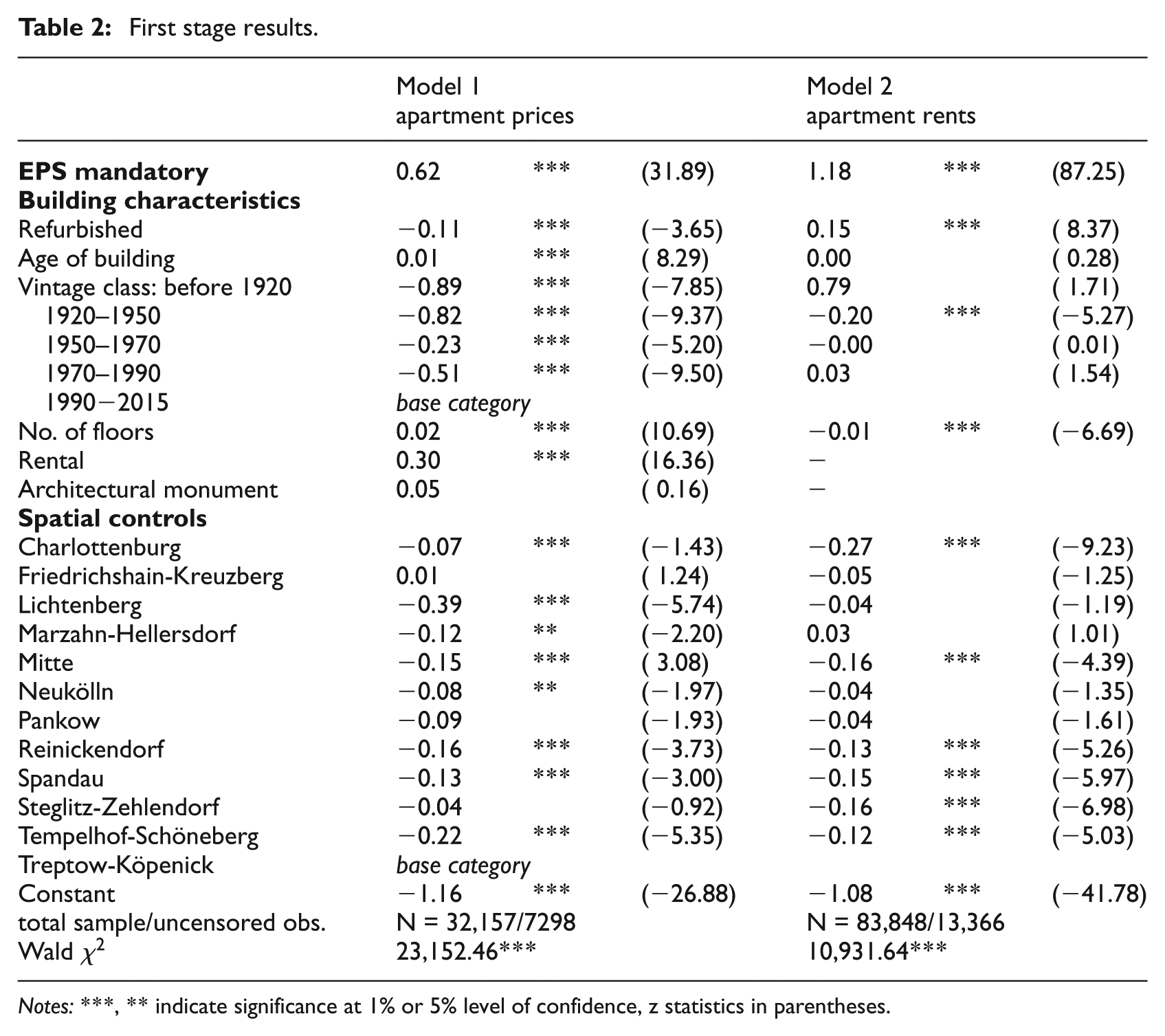

The Heckman procedure accounts for such bias. In a nutshell, the concept consists of two steps. In the first stage, the binary choice of reporting an EPS is estimated in a probit framework. Based on these results, the inverse Mills ratio (

In our case, we estimate the probability of reporting an EPS as a function of housing characteristics, such as the age of the dwelling, the refurbishment status, or the height of the building, among others, which are all potential candidates to affect the energy performance (see Table 2). As identifying restriction, we add a dummy variable ‘mandatory’ to the first stage equation. The variable indicates whether the advertisement was published before May 2014, or under the regime that obliges the reporting of EPS in online ads since May 2014. Our data reveal that the obligation to report EPS increased the share of ads containing such information in the selling sample from roughly 27% to 47.5%. 9 Moreover, the distribution is indeed biased towards better EPS before May 2014.

First stage results.

Notes: ***, ** indicate significance at 1% or 5% level of confidence, z statistics in parentheses.

We estimate the impact of energy efficiency on apartment prices and rents using equations (2) and (3), extended by the inverse Mills ratio obtained from the selection equation and the Internet ads data. The estimation results are reported in Table 3. Overall, both models have substantial explanatory power, indicated by the Wald

Estimates for apartment prices and rents (semi-log specification).

Notes: ***, ** indicate significance at 1% or 5% level of confidence, z statistics in parentheses. Full results are available upon request.

The decision to advertise information on energy efficiency

The results of the first stage show the decision to report EPS in advertisements of apartments for sale and for rent, see Table 2. We regressed this decision on a set of building characteristics and a dummy variable that indicates whether the dwelling is advertised in a period when EPS is mandatory to be reported in ads and controls for the spatial dimension. Our results show that the most important predictor for EPS included in the advertisement is the change in the regulation. For both groups of ads, the likelihood to include EPS has substantially increased with the obligation to report this measure. Moreover, there are significant spatial differences within Berlin. General housing characteristics also affect the likelihood to include information on the energy performance of buildings.

The estimates for both groups differ to some extent when comparing the results for general housing characteristics. The impact of vintage is highly significant for each class in the sales model. By contrast, only buildings constructed between 1920 and 1950 have a lower likelihood to report EPS, while buildings constructed before 1920 have a higher likelihood to report EPS in the rental model (marginally significant).

Interestingly, there is a negative effect of refurbishment in the sales model, while recent refurbishment increases the likelihood to report EPS in Model 2. This might be explained by the fact that landlords have to announce refurbishments and the expected impact on the energy performance to tenants prior to the construction activity. A calculation of the effects is not mandatory for owner-occupants. Landlords therefore clearly have a higher incentive to update their energy performance certificate, which might explain the observed differences. This interpretation is also strengthened by the fact that the rental status of a dwelling increases the likelihood of reporting EPS in the sales model. Finally, in Model 1, we find a very small effect of the age of the building. Further, we controlled for the status of an architectural monument in the sales model. However, this turned out to have no influence on the likelihood to report EPS.

Capitalisation of energy efficiency in prices and rents

Table 3 presents our estimation results for the effects of energy efficiency and occupancy status on house prices. The coefficient of the inverse Mills ratio is highly significant, indicating the non-random selection, as expected. Moreover, the negative sign indicates that simple OLS estimates that do not consider the issue of sample selection are biased towards higher coefficients for EPS.

The key variables in equation (2) are EPS, RP, and EPS

The second variable of interest is the energy performance of the building and its impact on apartment prices. As expected, EPS has a negative sign, which implies that higher energy requirements of dwellings lead to higher price discounts. On average, for each additional kWh/[

By contrast, the coefficient of the interaction term

The question is whether this is a rational response of investors to a low WTP for energy efficiency of tenants or if the rental income from energy efficiency would imply higher apartment prices. Therefore, we estimated the capitalisation of energy performance in rents by regressing the natural log of monthly net rents in euros per m2 on EPS. The results reported in Table 3 indicate that the coefficient for EPS is negative and statistically significant at the 1% level of confidence. However, its magnitude is small. A decrease of annual energy costs by one euro leads to an increase of annual rental income by roughly 0.23 eurocents per m2 (at sample mean).

Overall, the coefficients for the control variables are in line with expectations and the results reported in previous studies. For example, the rental income for a ‘refurbished’ apartment is significantly higher compared to the base, a non-renovated home. Increasing distance to one of Berlin’s city centres incurs price and rental discounts, while closeness to most other local amenities increases tenants’ and investors’ WTP. In rented out apartments, attributes like a built-in kitchen, a second bathroom, a balcony, a parking lot, all increase the rental income. Also the controls for the general quality meet the expectations: low quality decreases the rental income and prices, while the WTP for high quality or luxury dwellings is significantly higher, compared to the base group, a dwelling of average quality.

Are house prices a good reflection of energy cost savings and rental income?

Whether the estimated prices for energy efficiency reflect energy cost savings and rental income reasonably can be assessed in different ways. A first indication whether energy efficiency investments differ from general real estate projects is to calculate commonly used indicators in real estate appraisal, like the price-to-rent ratio (price divided by the gross annual rental revenue). The measure indicates how much risk investors are willing to take in terms of the length of the payback period. For rental apartments, the price-to-rent ratio for energy efficiency equals roughly 27.1. This is very close to the overall price-to-rent ratio of rental dwellings in our sample (27.7). Energy efficiency is obviously rated as being only slightly riskier than real estate investments in general.

In absence of rental income for owner-occupied dwellings, one can compare the cost savings-to-price-ratio (15.5, see the section ‘Capitalisation of energy efficiency in prices and rents’) with the average length of ownership of a dwelling. This gives an indication whether owner-occupants try to match energy savings with their personal benefits or if they expect an additional premium when reselling their home. According to a recently published study by the German Federal Institute for Research on Building, Urban Affairs and Spatial Development (BBSR), the median owner of a single dwelling holds the apartment for 15 years (see Cischinsky et al., 2015: 68). Thus, WTP matches the average length of ownership closely.

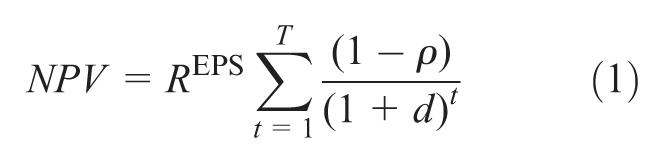

Another approach, which reflects the nature of an investment more adequately, is to compare the NPV of energy cost savings/rental income over the entire technical life-time with the price investors are willing to pay. Based on our estimation results, we first calculate the NPV of the rental income from energy efficiency under two scenarios: In the first case, we assume that the implicit WTP of tenants (

where t is the time index;

Given that scarcity of fossil fuels will increase in the future, it appears reasonable to assume that energy costs and consequently rental income from energy efficiency investments should also rise over time (Scenario 2). Assuming tenants’ WTP to be tied to energy price movements, and taking the past price movements

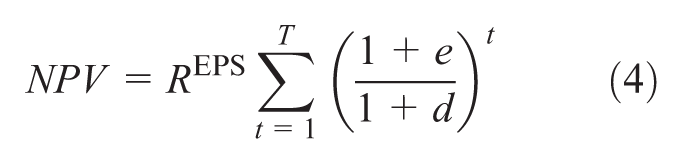

A different picture can be drawn for the value of potential energy cost savings in owner-occupied dwellings. The NPV can be calculated analogously to equation (4), while income is generated by energy cost savings (C) instead of rental income (

Assuming in a first scenario a price of eight eurocents per kWh heating energy, the NPV – all else identical to the rental housing case – of future energy cost savings at constant fuel prices (see equation (5)) equals 22.11 euros over the entire technical lifecycle of 55 years, which exceeds owner-occupants’ WTP by 42%. The spread even increases when assuming an annual run-up of energy costs (e) by 3.5%: the NPV (46.57 euros) exceeds investors’ WTP roughly by factor three. Under the assumption of constant energy prices, owner–occupants expect a remaining technical lifetime of 20 years; Under the assumption of increasing energy cost savings, the remaining lifetime is 15 years, which again meets the average length of ownership quite closely.

The results indicate that owner-occupants and landlords indeed follow two different investment rationales. While owner-occupants seem to orient their WTP primarily on their own direct benefits from reduced energy costs (future sales seem to play a minor role), landlords calculate their energy efficiency investments in strong analogy to general real estate investment projects. Overall, the calculated measures seem to fall in a plausible range and generally confirm and extend the results of the recently published study of Hyland et al. (2013) on the Irish housing market.

Conclusions

In this study, we investigated investors’ WTP for energy efficiency in the Berlin apartment housing market. In line with previous studies, we found that energy efficiency is capitalised in house prices. Moreover, investors seem to account for potential future energy and house price movements. While this is an established finding in the literature around energy efficiency of owner-occupied dwellings, up to date only few insights existed on the capitalisation of energy efficiency in rental apartment prices and the underlying rationale of investors. In this context, the present study adds three key insights to the debate.

The implicit price of energy efficiency in a tenant-occupied dwelling is significantly below the level of available to use (most likely owner–occupied) dwellings – roughly by a factor of 2.5.

This can be interpreted as a rational response of landlords: the rental relationship substantially reduces the revenues (rents vs. cost savings) from energy efficiency investments. A one euro reduction in energy costs corresponds to an increase of only 23 eurocents in rental income. However, whether this is a result of market imperfections, as argued by the authors emphasising the existence of the ‘landlord–tenant dilemma’ or a result of an unequal distribution of market power between landlords and tenants, must be left for future research.

Both groups of investors follow different investment rationales. Landlords apparently optimise their investment in strong analogy to general real estate investment projects. This also includes the implicit assumption that potential investors in the future also have a positive WTP for income generated from energy cost savings. By contrast, this idea is obviously less important for owner-occupants who seem to orientate their WTP on individual energy cost savings/consumer needs, while taking less into account the value of these savings for future owners. The differences might also partially be explained by shorter refurbishment cycles of owner-occupied dwellings. However, these effects should also be subject to future research.

Overall, our results indicate rational behaviour by both groups of real estate investors: Energy price movements seem to be anticipated, current and future revenues are well capitalised in rental apartment prices. However, owner-occupants seem to be too pessimistic about potential revenues from reselling their home. For policy makers, our findings imply a differentiated treatment of rental and owner-occupied housing in future policies towards the ‘Nearly Zero-Energy Buildings’ (NZEB) standard, as, for example, targeted in the European Union by the year 2021. While landlords’ WTP seems to be a rational response to current and future revenues, information for owner-occupants about the potential capital gains when reselling their home might increase individuals’ WTP today and thus willingness to install energy efficiency measures. A promising approach to overcome the potential misalignment of investment horizons of energy efficiency projects and individual investment objectives is to implement instruments of on-bill financing, like, for example, recently introduced in the UK or frequently offered to commercial or public investors by contracting-providers. For landlords, information seems to be a minor problem: overcoming insecurity of tenants about the real energy cost savings – e.g. by credible energy performance certification – and thereby increasing the revenues for landlords can be a stimulus for green investments. As Allcott and Greenstone (2012) point out, direct subsidisation should only be implemented in absence of information inefficiencies.

Future research in this field should also consider the comparison of the effects of EPS on house prices and rents under heterogeneous market conditions. While the findings in our study hold for the growing Berlin market, there are still no studies concerning the implicit price for energy efficiency in markets that are facing population decline and a less favorable market environment. It can be expected that rental revenues and apartment prices would vary substantially, as indicated by the study of Hyland et al. (2013).

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.