Abstract

We investigate the long-run convergence of house prices across the London boroughs based on a pairwise unit root probabilistic testing procedure. In sharp contrast to the earlier literature, we employ a dataset that distinguishes between four different types of property in each borough. Using a quarterly dataset that spans from 1995 to 2014, we find evidence in favour of long-run convergence thereby suggesting that the great majority of London borough house prices are driven by a single common stochastic trend. In a further contribution, we offer new insights through analysing the determinants of long-run convergence, by considering the role of geographic proximity, type of accommodation and amenities (quality of life).

Introduction

Housing is a durable consumption good that is immobile and is frequently used as collateral for loans. When commenting on the state of the national economy and setting UK interest rates, the Bank of England pays close attention to the state of the domestic housing market. However, there is considerable value in understanding how relative regional house prices behave over time. 1 Not only do they have the potential to influence relative regional economic activity, but also the affordability of housing, relocation costs and labour mobility between regions. Following the early work by Meen (1999), it has been argued that shocks to regional house prices ‘ripple out’ across the economy. While the idea of a ripple effect may rely on factors such as spatial patterns in the determinants of house prices, migration, equity transfer and spatial arbitrage, it also requires some notion of a degree of long-run convergence, or the existence of a long-run equilibrium relationship, between regional house prices. However, the literature to date can only offer mixed evidence that long-run equilibrium or cointegrating relationships between all regional house prices actually exist; see, for example, Holmes and Grimes (2008) and Abbott and De Vita (2012), and references therein.

While there is a relatively extensive literature that explores inter-regional house price convergence, there have been far fewer studies that explore intra-regional convergence. With this context in mind, we focus on house price convergence involving the 32 administrative divisions of London, which are defined as boroughs. 2 An analysis of house price convergence within London is of considerable interest. In terms of other European cities, London is of great significance vis-à-vis size, economic importance and as an inward source of migration to both EU and non-EU citizens. Within the UK, the importance of London in terms of both population and national economic activity is also well known. London and the South East of England are considered as the source of house prices shocks that ripple out across the rest of the economy; see, for instance, Holly et al. (2011) for an analysis using impulse response functions that allow for spatial dependence.

Among a small number of studies that conduct intra-regional house price analysis, Hamnett (2009) shows that there has been a limited catching up process with some of the highest rates of price inflation in the lowest priced boroughs, and vice versa. The author here argues that spatially displaced demand from the expensive boroughs may help to explain price rises in the cheaper boroughs. Abbott and De Vita (2012) investigate the long-run convergence of district-level house prices in Greater London using a pairwise approach. They find no overall multidistrict long-run convergence across London boroughs. Indeed, Abbott and De Vita identify evidence of district-level segmentation of house prices in Greater London. 3

Our investigation is intended to deepen our understanding of house price co-movement across the boroughs of London. The stationarity of house price differentials is used as an indicator of long-run intra-city house price convergence, based on a tendency for house prices to not necessarily be equal, but instead move together over time. 4 In other words, do shocks to relative house prices have a permanent effect, or are the effects more short-lived such that house price differentials are restored? In this respect, authors such as DiPasquale and Wheaton (1996) argue that although one might expect house prices across all locations to rise and fall with a market’s fortune, the relative price of more desirable locations compared to less desirable ones perhaps changes very little in the long-run. Indeed, Glaeser and Gottlieb (2009) highlight that house prices represent the interaction of supply conditions and the desire to live and work in certain locales. Factors such as labour and capital mobility may be important, but the influence on housing markets of the movement of people and firms can be complex. Models of spatial equilibrium argue that house prices can vary according to differences in planning rules and amenities (congestion, crime levels, public transportation, schools, weather, etc.). Regional house price interactions may occur from the gradual dissemination of information across space following any shock. In an efficient market, we might expect all regions to react at the same time to a common shock. However, there are many reasons why lags may arise in the case of housing. Consequently, our empirical analysis specifically addresses whether or not the expected general stability of relative prices (or property price premiums) is a generalised phenomenon throughout the boroughs of London.

In the spirit of the earlier studies by Holmes et al. (2011) on inter-state house price convergence in the US, Abbott and De Vita (2012) on intra-borough house price convergence in London and Holmes et al. (2017) on intra-city price convergence in Paris, our empirical analysis is based on Pesaran (2007) who employs a probabilistic unit root testing procedure. Our study also contributes towards an ongoing debate addressed by earlier studies, such as Pollakowski and Ray (1997), as to whether house price relationships between contiguous regions are any stronger than between non-contiguous regions. The verdict on this remains open and we enrich the debate by considering the role of geographic separation between the boroughs as a factor that helps explain the existence of long-run equilibrium relationships involving bivariate house price differentials.

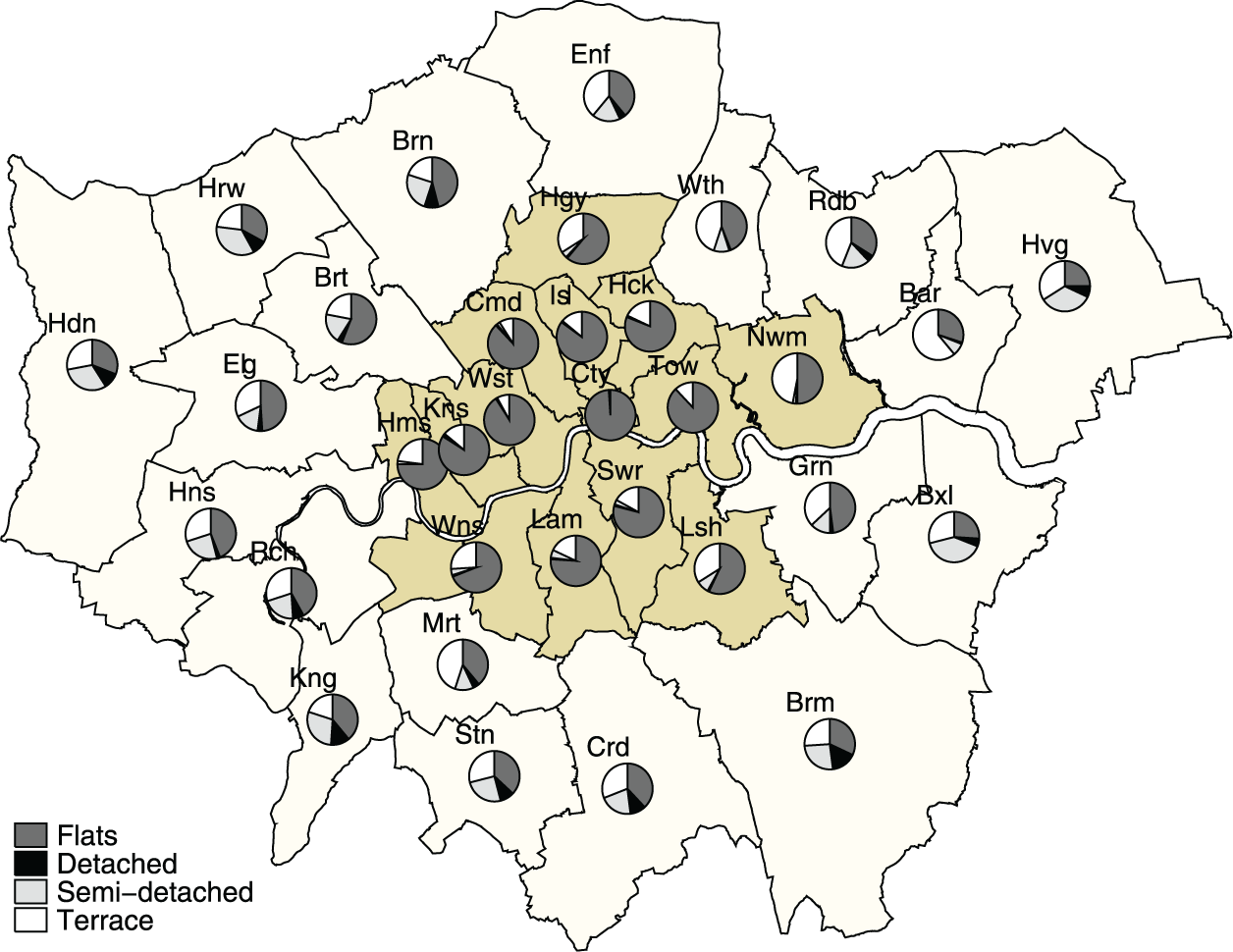

Building upon the earlier work of Abbott and De Vita (2012), we use a highly detailed database in that we distinguish between the prices of different types of dwellings, namely detached houses, flats, semi-detached houses and terrace houses. This is in marked contrast to the typical employment of a single aggregate house price index for each borough. Such a distinction is clearly important when thinking in terms of a property ladder because it allows us to capture the fact that when agents are deciding to purchase real estate of a certain price range, they not only take into account the type of property but also they consider the location of their prospective purchase. In other words, the heterogeneity of the housing market is captured by examining all available buying options. 5

Whether or not house prices drift apart within London has implications for relative affordability, labour mobility, labour mismatch, commuter times and potential localised house price bubbles. Essentially, these are issues relating to economics, financial stability and well-being. The potential policy implications that arise from this are in terms of measures such as transport policy to address commuting issues, house building to address affordability, incentives for employment to be offered in cheaper areas and financial measures to address potential bubbles. Employing a disaggregated dataset enables us to reflect on the extent to which long-run price convergence is more or less likely across these property types. Given that housing affordability has been a key issue of concern, borough price convergence or divergence is of potential interest to policymakers with an eye on long-term affordability.

To summarise, our paper possesses two salient features with respect to the existing literature. First, in terms of employing a highly disaggregated dataset. The second feature of our paper is that in an extension to testing for long-run convergence, we also examine the drivers that determine the likelihood of finding long-run convergence. We not only take into account the role played by the type of accommodation under consideration (heterogeneity), but also a range of factors related to amenities or quality of life such as education standards, crime rates, population densities and income levels.

The paper proceeds as follows. We first outline our econometric modelling approach. Next we describe our data. We then examine long-run house price convergence, before investigating the determinants of house price convergence. We finish with ‘Concluding remarks’.

Econometric methodology: A brief review

Our econometric modelling approach draws upon the work of Pesaran (2007), who develops a pairwise approach to analyse stochastic convergence across a large number of cross section units. We adapt and extend this pairwise approach to the analysis of house prices in the boroughs of London. Stochastic convergence involves applying unit root/stationarity tests to investigate the order of integration of prices relative to a reference (or an average) price level, and as a result the outcome of the tests depends on the choice of that reference price. This is regardless of whether unit root/stationarity tests are applied in a time series or panel context. In sharp contrast to this, the pairwise approach that we adopt in this paper requires testing the order of integration for all possible pairs of prices and, in doing so, does not involve what can be a problematic choice of a single reference unit with respect to which all house price differentials are computed.

As indicated before, the aspect that characterises our empirical analysis is the availability of price information for four different types of properties. A household might aspire towards moving from a semi- to a detached house. However, such a move within a borough may be infeasible on the grounds of cost. Therefore, the household might consider moving to a different borough that has a more accessible price for detached housing. Allowing for other factors that might include distance, amenities, and so on, a process of arbitrage will contribute towards different house prices across different boroughs converging. Of course, it is certainly possible to simplify the analysis by aggregating prices within each borough and proceeding with the application of the pairwise approach, as undertaken by Abbott and De Vita (2012) also for the boroughs of London. While such an aggregate approach can provide valuable insights, one can further exploit the underlying heterogeneity across property types (see Nemov et al., 2016), and so allow for consideration of all purchase possibilities that are available to individuals.

In line with Pesaran (2007), we let

The pairwise approach then proceeds by investigating the order of integration of all

To implement the pairwise approach we consider the application of the augmented Dickey and Fuller (1979) and the Leybourne (1995) unit root tests, denoted ADF and ADFmax respectively, to each time series

Previous pairwise studies of house price convergence by Holmes et al. (2011) and Abbott and De Vita (2012), as well as applications of the pairwise approach in other contexts such as Pesaran (2007), Nourry (2009) and Le Pen (2011), focus on computing the fraction of rejections

We begin by considering the factors that are expected to affect the probability of long-run convergence between pairs of property prices into three groups, namely those that refer to geographic separation between boroughs and location; those that are related to amenities and quality of life; and those that are concerned with the type of housing. The first group of factors include two measures of the geographic separation between boroughs which are based on distance and travel time, as well as indicator variables related to whether or not pairs of boroughs are part of inner or outer Greater London. 7 In this case, we are interested in examining whether a shorter distance (less travel time) is associated with an increase in the likelihood of cointegration. Indeed, it seems reasonable to assume that shorter distances (travel times) between districts may facilitate arbitrage mechanisms that bring house prices into line. In line with previous work by Pollakowski and Ray (1997) and others, we also contribute to the existing literature as to whether house price relationships between contiguous regions are any stronger than between non-contiguous regions.

As to the second group, we include variables that reflect amenities and quality of life differences across boroughs. In doing so, we test the hypothesis that the more similar are any two boroughs with respect to amenities and quality of life, then the more likely is the probability of finding cointegration between their house prices. The inclusion of education standards follows earlier views expressed on the linkages between house prices and education standards. For example, Gibbons and Machin (2006) point out that school quality is capitalised in UK house prices if access to schools is rationed by residential location. More specifically, they find that test-score-based school performance significantly increases property prices, but only the best one in 10 schools generates higher than average prices close by, and that prices are higher close to popular, over-capacity schools. Additional insight is offered by Cheshire and Sheppard (2004), who provide evidence on the complex and subtle ways in which housing markets capitalise the value of local public goods such as school quality, and suggest that this is highly nonlinear. In addition to this, Fack and Grenet (2010) provide evidence supporting the view that housing prices in Paris increase as the performance of public and private schools improves.

Another variable of potential importance is crime, which enters the analysis with the intention of capturing security conditions in the boroughs. Furthermore, we also include population density motivated by the idea that it can serve as a measure of demand pressure and also as an indirect measure of supply shortage. 8 When the population density is high, it may be an indication that the land endowment is very limited and thus the possibilities to augment the supply of housing are constrained.

The amenity variables included in the second group of factors are considered as differentials in absolute terms. This is because we are interested in whether increased differences between the boroughs lead to a lower probability that their respective house prices are cointegrated. As a result of this, in all cases the sign on the estimated coefficient is expected to be negative if the degree similarity of amenities between boroughs is a positive driving force behind house price convergence.

However, in assessing the impact on the likelihood of cointegration, one might also in fact regard the signs on the income and amenity coefficients as being indeterminate. Positive income differentials across city pairs, which are related to productivity and wage differentials, should attract flows of workers thus pushing up housing demand and in turn house prices. When we consider amenities, an increase in crime (education quality) in borough

Lastly, regarding the factors related to the type of housing, these are captured through the use of indicator variables for the different types of properties. These variables enter as control variables, and there is no clear expectation as to the signs on the estimated coefficients. The motivation for including these variables is because the stationarity of pairwise differentials in house prices may be more or less likely between the same as opposed to different house types. Housing transactions involving movements up or down the property ladder might involve relocation from one borough to another on the basis of the same type of property. Of course, it could be that relocating to a different borough involves purchasing a different type of property.

Data

We use HM Land Registry data by borough and by property type for each house sale in London from 1995 to 2014.

9

Overall, the database contains more than 2.5 million observations on prices based on housing transactions, which are used to construct quarterly time-series on the median price (in pounds sterling) paid for detached houses, flats, semi-detached houses and terrace houses in the 32 boroughs that comprise London (although real estate agents may be tempted to push the advantage of an end terrace, these properties are not usually viewed as fully equivalent to a semi-detached house). The sample period runs from 1995q1 to 2014q4, for a total of

The price series are in logarithms, and so the price differentials used in the econometric exercise are in percentage terms; see the figures in Appendix I, ‘Time-series of quarterly property prices’, which also include the median property price in London as a measure of the overall development of property prices over time. Visual inspection of the time series plots in these figures suggest that within each property type the price series are non-stationary and tend to move together over time, so that there could be support for the hypothesis of price cointegration not only across boroughs, but also across property types. Another feature that is apparent from the graphs is the higher variability exhibited by prices of detached and semi-detached houses (particularly in the upper segment of price scale), compared with the prices for terrace houses. As to flats, the higher variability of prices is more frequently observed in the lower and intermediate segments of the price scale. 12

Let us now turn to the data concerning the potential drivers of convergence. For geographic separation it was first necessary to estimate the geographic coordinates (that is, latitude and longitude) of the population-weighted centroids of the London boroughs. Once the coordinates are available, we employ the Stata programme osrmtime developed by Huber and Rust (2016), which uses the Open Source Routing Machine software based on Open Street Maps, to determine the shortest route by car between any two pairs of geographic coordinates, and calculate the corresponding optimal distance (in metres) and optimal travel time (in seconds). The resulting measures of optimal distance and optimal travel time between boroughs

Regarding location, we account for the possibility of boroughs being part of inner and outer Greater London, by means of the dummy variables

Distribution of property type by borough.

The quality of education is measured through the percentages of pupils attending good or outstanding primary and secondary schools in borough

Crime corresponds to the average rate of recorded offences per thousand of population over the financial years 1999/2000 to 2014/2015 (the source of the data is the Metropolitan Police Service, through the London Datastore). Here, relative crime conditions are measured by

For demographic influences we consider

Average household size by borough.

Economic conditions are measured by

Finally, we consider the dummy variables

It is important to appreciate that there are other borough-level factors that could be relevant in terms of influencing flexibility in a market which would affect the relative price differential and so likelihood of long-run convergence. Such factors include regulatory stringency over land use, infrastructure, car dependency, the presence or absence of natural amenities, net population flows across boroughs, racial diversity and income diversity; for a historical perspective see Meen et al. (2016). These factors cannot all be operationalised. However, we do include a measure of borough housing supply (likely to be inversely related to regulatory stringency over land use), a measure based on borough underground station access (inversely related to car dependency), and relative population density (related to population diversity). Of these three measures, borough housing supply was not found to be statistically significant, and was therefore omitted from the subsequent probit analysis. In relative terms, natural amenities are less likely to have changed dramatically over the study period.

Long-run house price convergence

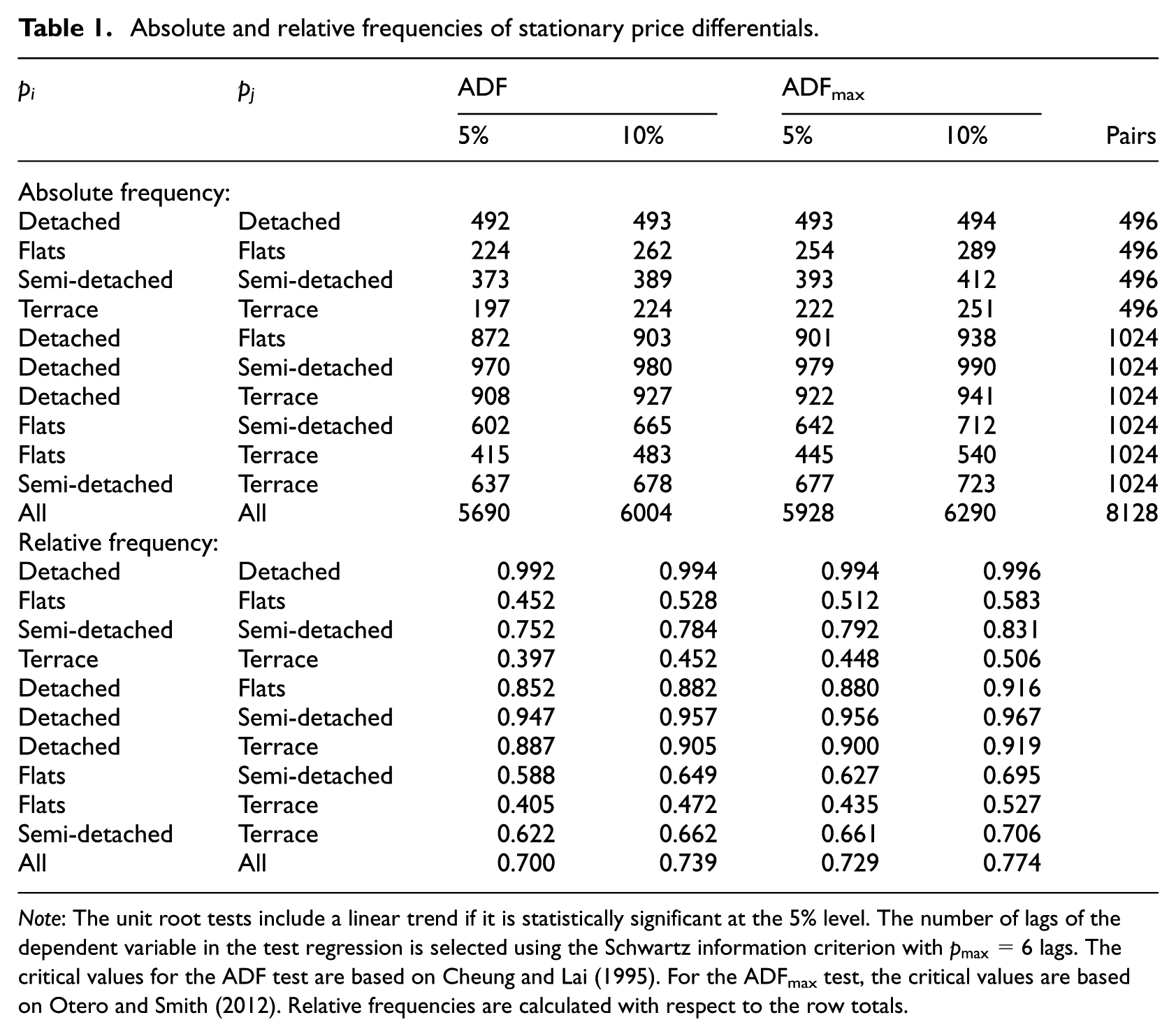

Because we are interested in price differentials, rather than price levels, the use of data in nominal or real terms, the latter obtained after deflating using a national (or even city level) deflator, makes no difference to the results. The top and bottom panels of Table 1 summarise the absolute and relative frequencies of stationary relative prices. The first four rows in each panel present the (absolute and relative) frequencies based on all the differentials that can be constructed using the prices of only detached houses, only flats, only semi-detached houses and only terrace houses (that is, 496 price pairs in each case). In turn, the next six rows in each panel present the corresponding frequencies based on all the relative prices that can be computed using couples of property types, namely detached houses and flats, detached and semi-detached houses, and so on (that is, 1024 price pairs in each case). Overall, the total number of price differentials that can be calculated with the 128 price series under consideration is 8128, as presented in the last row of each panel.

Absolute and relative frequencies of stationary price differentials.

Note: The unit root tests include a linear trend if it is statistically significant at the 5% level. The number of lags of the dependent variable in the test regression is selected using the Schwartz information criterion with

To produce Table 1, the ADF and ADFmax unit root tests were performed at the 5 and 10% significance levels, the optimal lag length was chosen using the Schwarz information criterion (SIC), allowing for a maximum of six lags, and a borough-specific trend term was included in the test regression if it was statistically significant at the 5% significance level. From an economic perspective, the inclusion of the time trend (if significant) is intended to serve the purpose of picking up effects associated to relative changes in amenities between boroughs.

The results presented in Table 1 illustrate that at the 5% significance level, the ADF test yields a rejection frequency of 99.2% for detached houses only, indicative that the overwhelming majority of price differentials are stationary. For semi-detached houses the associated rejection frequency is also considerably high, that is 75.2%, while for flats and terrace houses the corresponding percentages are 45.2 and 39.7%, respectively. Although at first sight these results may not appear surprising, in the sense that they involve homogeneous property types, higher relative frequencies of stationary price differentials are also observed when examining couples of different property types. For instance, if one looks at the ADF test at the 5% level, the results for detached and semi-detached houses, detached and terrace houses, and detached houses and flats reach relative frequencies of rejection of 94.7, 88.7 and 85.2%, respectively. The smallest relative frequency of stationary price differentials is observed for terrace houses only, with 39.7%, although this is certainly not a negligible percentage. Overall, 5690 out of the 8128 price differentials (that is, 70%) are found to be stationary when using a significance level of 5%. In all cases higher relative rates of rejection are obtained when the more powerful ADFmax unit root test is used for inference. The lowest proportion remains the one observed for terraced houses and the highest for detached houses. 17

The results described above highlight that, at least in the case of London, the finding of long-run co-movement of property prices tends to be more prevalent when allowance is made for the type of dwelling. Indeed, results not reported here indicate that when one constructs quarterly time series on the median price (in pounds sterling) paid for all four property types in the 32 boroughs that compose London, then 37.1% (i.e. 184 out of the 496 price differentials) are stationary based on the ADF test at the 5% level. This relative frequency compares very favourably with the 36% value reported by Abbott and De Vita (2012) for the London boroughs, also using the ADF test at the 5% level, and where the optimal number of lags is determined using SIC. 18

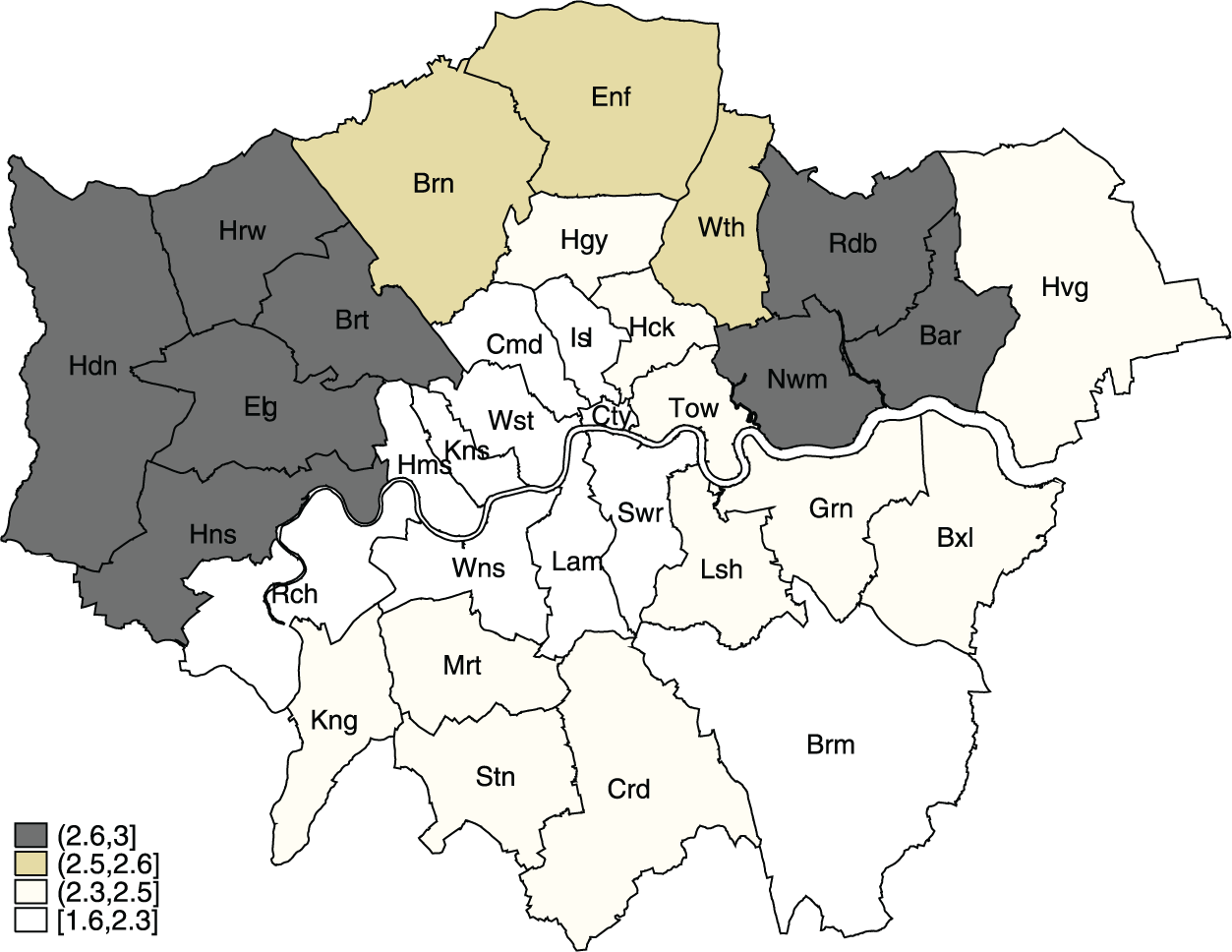

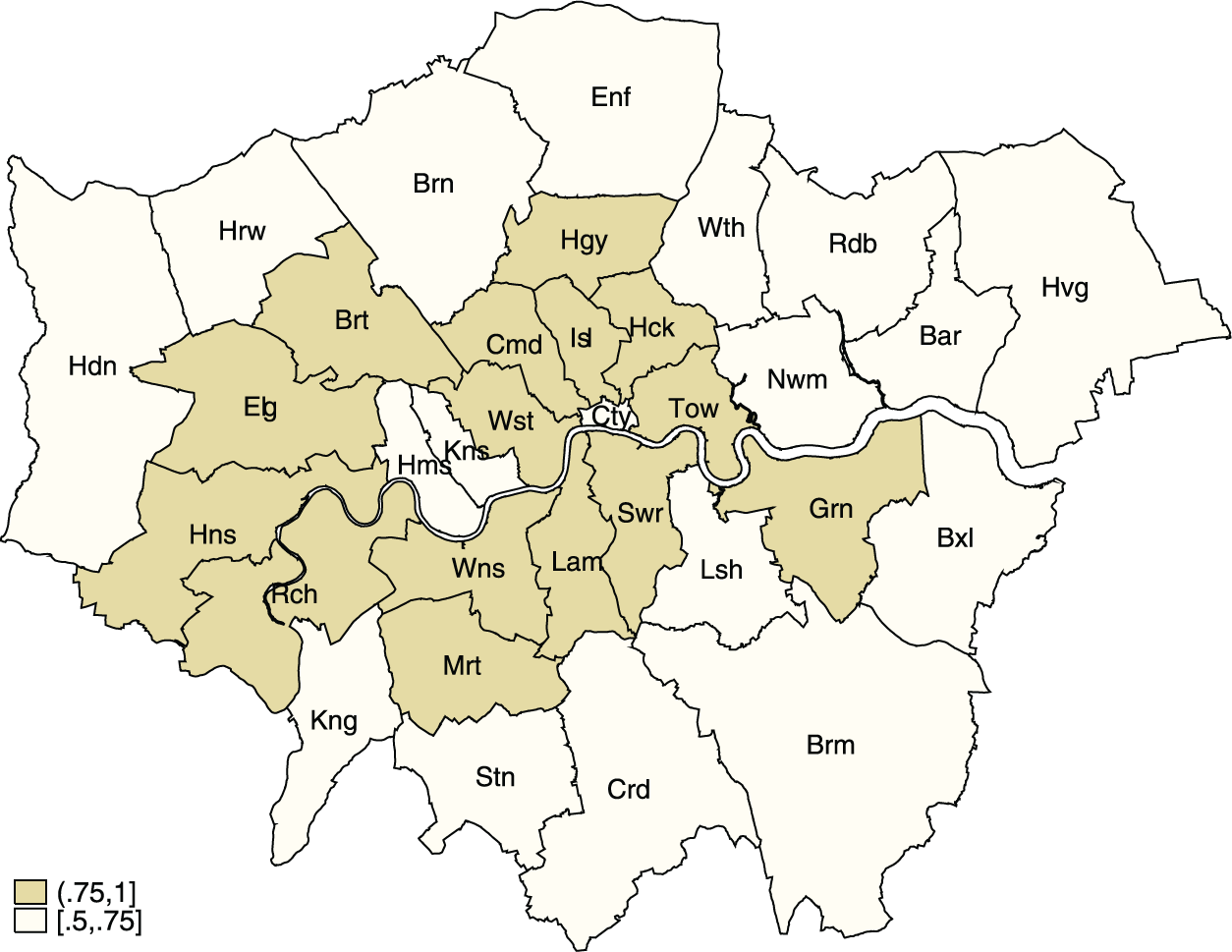

Figure 3 displays the geographic pattern of spatial integration in the boroughs of London, where the darker areas indicate those boroughs with rejection rates greater than 75%, based on the ADFmax unit root test at the 5% significance level, and therefore more long-run convergence with other London boroughs. In turn, the lighter areas show those boroughs with rejection rates between 50 and 75%. Overall, this figure reveals that the highest degree of long-run house price co-movement tends to occur in the boroughs located in the central part of the city. This figure provides the motivation to ask ourselves if it is possible to formulate and estimate a model with the purpose of identifying the variables or drivers that are expected to have an effect on the likelihood of finding cointegration between pairs of property prices.

Proportion of stationary house price differentials.

Lastly, in an attempt to provide a more complete view of the property market in London, we examine whether or not similar developments can be observed in the case of private sector rents. To address this issue, we collected annual data on this variable (measured in pounds per week) for the London boroughs over the period 1997 to 2015, which corresponds to

Determinants of house price convergence

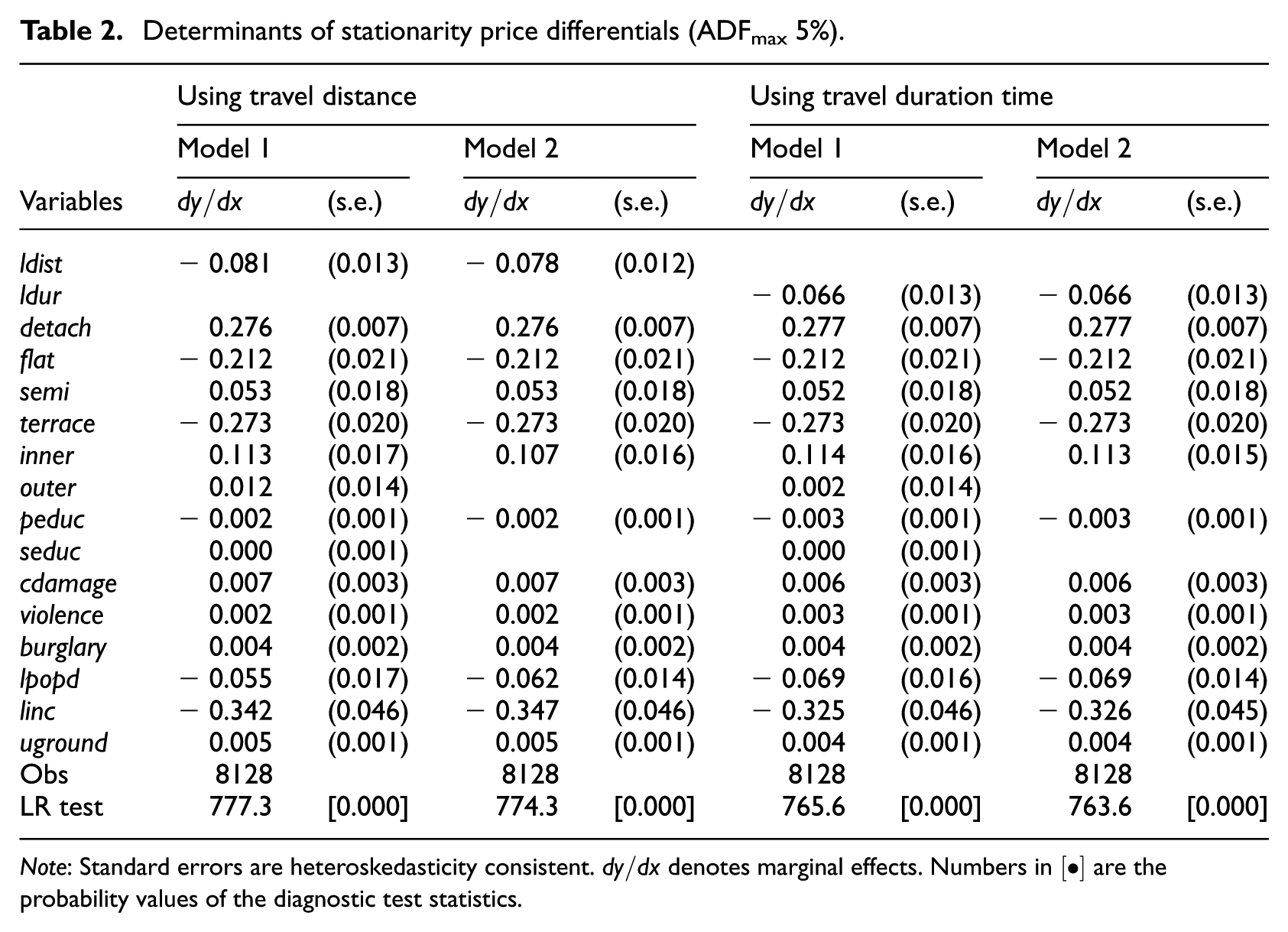

In this section we estimate a binary (probit) model to find the variables that are expected to have an effect on the likelihood of

Table 2 reports the marginal effects when the binary outcome

Determinants of stationarity price differentials (ADFmax 5%).

Note: Standard errors are heteroskedasticity consistent.

Concluding remarks

In this paper we have uncovered evidence supporting the view that long-run property price convergence is present across the London boroughs insofar as price differentials are stationary and prices therefore move in tandem. This co-movement of property prices within regions has important implications for relative affordability and labour mobility. In reaching this finding, we have conducted a probabilistic test of convergence based on the unit root testing of all pairwise house price combinations. In contrast to the existing literature, however, our findings are based on the employment of a richer dataset that explicitly distinguishes between four types of dwelling. By not relying on a single house price measure for each borough, this has enabled us to capture the heterogeneity of the London property market.

While we acknowledge the need to interpret our findings with caution due to potential bias introduced by omitted variables, there is evidence that the probability of finding long-run convergence between any two boroughs is inversely related to the geographic separation (measured through the optimal travel distance and optimal travel time) between them, as well as differences in amenities and quality of life such as considerations based on education, population densities and income levels; public transport connectedness, on the other hand, is found to be directly related. Disparate rather than similar crime rates between boroughs, a negative attribute, are more likely to drive house price convergence. With regard to the unresolved issue concerning the role of geographic separation in house price relationships, our findings are consistent with the view that property price relationships are likely to be stronger between contiguous than non-contiguous boroughs. Finally, we find that the highest proportion of unit root rejections emerges when we consider pairs of semi- and detached as opposed to pairs of flats or terraced houses.

We can reflect on policy implications that might arise from our findings. In our sample, the cheaper properties within each borough are terraced housing and flats and are therefore most relevant to the affordability issue for lower income households. Across boroughs, we find that convergence is less likely for these housing types. This implies relative divergence and therefore potential for relative affordability to worsen. Looking at the earlier presentation of the data, this policy issue is particularly relevant to the inner-London boroughs that are characterised by a high proportion of terraced houses and flats. Policy measures aimed at addressing the relative affordability of cheaper housing should therefore be strongly borough-focused. Further to this, it is desirable to bring crime rates down. If it is also desirable to ensure that borough house prices do not drift apart, then crime rate reductions in high-crime/low house price areas are likely to make cointegration between borough house prices less likely with the prospect of borough house prices drifting further apart. This potential conflict in objectives may lead policymakers to carefully assess priorities.

Footnotes

Appendix 1

Acknowledgements

We gratefully acknowledge the helpful comments and suggestions made by seminar participants at the Universidad del Rosario (Bogota), conference participants at the 2016 meeting of the New Zealand Association of Economists, and three anonymous referees. The usual disclaimer applies.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.