Abstract

In the wake of the housing market crash in the United States in the late 2000s, images of abandoned homes on the periphery of American cities dominated international media. Mexico continues to face a housing crisis that began at the same time, and the media similarly focus on the high rate of housing vacancy in the urban periphery. The vacancy rate is extreme in many newly built subdivisions in Mexico, yet it is also high in most central cities. In this article, I describe the role of government mortgage lending in housing vacancy rates, across and within cities in Mexico. I do this using data from the 2010 Census of Population and Housing for the 100 largest cities in the country. Cities with more housing built under the federal housing finance system have higher vacancy rates overall, and the relationship is strong in central areas of cities as well as the urban periphery. These findings imply that policymakers should not only be concerned with vacancy in newly built suburban developments, but they should also consider how the expansion of credit for new suburban housing has played a role in the hollowing out of central cities. The article has direct implications for Mexico and raises questions about the frame for debate about housing policy internationally. The structure of housing finance systems is often under-scrutinised. Scholars working in emerging markets should work to identify incentives in finance systems and how they shape urbanisation.

Introduction

When the United States housing market crashed in the late 2000s, images of foreclosed tract homes standing empty became the dominant symbol of the financial catastrophe. These photos seemed to capture the excess of a private market run amok, and often accompanied poignant stories of embattled homeowners trying to keep communities intact in the face of neighbourhood disintegration. Other news stories captured the ghostliness of brand new housing developments stopped mid-construction, before a single resident had moved in. Given the international reach of such coverage, it was not surprising that when attention began to focus on empty houses dotting the landscape of Mexico’s ex-urban areas in 2012, news coverage followed this well-established narrative (Economist, 2013). Newspaper articles in the United States in particular have focused on the newly built houses on the periphery of Mexican cities that sit empty, and journalists home in on the plight of people living in neighbourhoods of mostly vacant houses (Eulich, 2013; Guthrie, 2013; Levin and Bain, 2013).

The housing crisis in the United States provides a misleading framework for the problems confronting the Mexican housing system. Speculative home construction outside of city boundaries and high rates of housing vacancy partially obscure the fact that housing problems in Mexico and the United States occurred within very different housing policy environments. The juxtaposition of the two countries’ vacancy crises is analytically useful, however, precisely because of those differences. A lack of government oversight and regulation of a private sector finance system played an important role in the United States housing crisis (Immergluck, 2011). In Mexico, a government agency issues the vast majority of mortgages. The set of incentives for both homebuilders and homebuyers established by the federal system in Mexico, I argue, plays a major role in the vacancy crisis there (Monkkonen, 2011a).

This article analyses housing vacancy rates across urban areas 1 in Mexico and examines whether cities with more INFOANVIT (National Workers’ Housing Fund) loans have more vacancy. Using census data from the year 2010 for the 100 largest cities in Mexico, I also calculate and assess the distribution of vacancy rates within and across cities. I describe what kinds of cities have high vacancy rates overall, and examine vacancy rates in the centres and peripheries of cities separately. The article provides a series of stylised facts about where vacancy is more prevalent in Mexico, especially as it relates to housing finance.

The study confirms some of the expected relationships between high vacancy rates and characteristics of cities such as violence and migration, but highlights the importance of housing finance in Mexico’s high housing vacancy rates. Cities with more mortgage lending have significantly higher vacancy rates. Additionally, the study suggests an underestimated and consequential feature of the housing finance system in Mexico, that the overproduction of new housing is also associated with high vacancy rates in central cities. The vast majority of loans are for new housing in the urban periphery but cities with more government mortgage lending are strongly associated with higher vacancy rates in central cities as well. These findings suggest that a large share of the empty houses in Mexico are not vacant because of foreclosure or abandonment due to an inability to pay a mortgage, but due to the incentive to buy new peripheral housing rather than inhabit older housing in central cities.

In the article’s conclusion, I argue that the present finance system has significant perverse incentives for developers and members. The Mexican government should reform its housing fund to make lending for housing respond to people’s demand, reduce the overall rate of building and prevent the construction of housing that ends up abandoned by owners and illegally occupied by others.

Literature review

Housing vacancy as a policy problem

Every housing market, even those that are very active, has a share of housing sitting vacant at any given point in time. Like structural unemployment, structural vacancy exists for two main reasons. The first is the construction process. Newly built housing is not occupied immediately, and owners often do not live in housing units that are being remodelled or upgraded. The second is the unavoidable friction during the process of buying, selling and renting. Sellers of houses often move out during the sale process or before new owners move in, and rental properties sit vacant after a tenant moves out and while the owner searches for a new one.

Vacancy in excess of the structural vacancy rate is hard to measure, but can negatively impact cities through higher crime rates, decreased property values and longer travel distances (Rosen and Smith, 1983).

Recent decades have revealed the negative environmental impacts associated with urban sprawl, a phenomenon that vacant houses in central cities exacerbate. Scholars argue that the negative environmental impacts of excess housing vacancy overwhelm any mitigating efforts of sustainable building regulations on new housing (Sun et al., 2011). Moreover, high vacancy rates in expanding urban areas lead to inefficient use of infrastructure (Durst and Ward, 2015). Cities in Mexico with more housing built under the new housing finance system have higher rates of peri-urban housing production and higher rates of population loss from their central city areas (Monkkonen and Comandon, 2016). This creates the need for unnecessary horizontal expansion of infrastructure and inefficient use of existing networks.

Rosen and Smith (1983) describe a model of the housing market in which the cost of holding inventory, searching, demand for space in given locations and the costs of changing contracts determine the vacancy rate. National housing vacancy rates were roughly 10 per cent in 2010 (Torres, 2012). By comparison, rental housing unit vacancy in the United States has generally hovered at between five and 10 per cent since 1960, and has been around 2 per cent for owner-occupied housing (US Census Bureau, 2013). Struyk (1988) argues that developing countries, which have higher transaction costs, less contract enforcement, weaker credit markets, fewer investment and savings opportunities and lower holding costs due to low property taxes, tend to have higher vacancy rates than high-income countries. Studies of the market for rental housing in Mexico confirm many of these features (Gilbert and Varley, 1990).

Efforts to reduce housing vacancy rates potentially benefit all cities by increasing access to housing, improving the safety of cities, making land use more efficient, reducing per capita infrastructure costs and increasing economic productivity. In order to reduce the vacancy rate, policymakers need to understand it better.

Housing vacancy in Mexico

Over 14 per cent of Mexico’s housing was vacant in 2010, but in many neighbourhoods vacancy rates were well over 50 per cent. This is of particular concern because many of these houses have been built recently, and purchased through a government-run mortgage financing system. All formal, salaried employees in Mexico, roughly 40 per cent of the workforce, are automatically members of the National Workers’ Housing Fund (INFONAVIT for its initials in Spanish). Members are required to contribute 5 per cent of their salary to the fund. The design is similar to Singapore’s Central Provident Fund (CPF) in that it serves as a pension fund as well as a mortgage bank (Chiquier and Lea, 2009). The main differences between the CPF and INFONAVIT are that the CPF’s investing and lending operations are separate and that members trust that they will receive a pension. In Mexico, on the other hand, there is no split in operations. Moreover, INFONAVIT issues housing loans to members at below market interest rates, so members have an incentive to take a loan because pension payouts are small (Monkkonen, 2011a).

The reality of Mexico’s housing finance system is such that there are mechanisms on both the demand side and supply side that might contribute to high vacancy rates. Members of INFONAVIT have a strong incentive to take out a loan based on their contributions. Many see buying a home as the only way to benefit from mandatory contributions into the fund. Even if people do not intend to move, many purchase a house with their loan with the idea of renting it or retaining it as a weekend home (INFONAVIT, 2012). Importantly, while loans from INFONAVIT are not technically restricted to new houses, the lending criteria on price, quality and legal status of the unit effectively limit them to new houses, purposely built by developers for INFONAVIT clients (Libertun de Duren, 2018).

On the supply side, developers of housing in Mexico have taken advantage of the expansion of INFONAVIT to build subdivisions far from city centres, without services or retail units until years after they are completed (Alegría Olazábal, 2008; Monkkonen, 2011a). Households seeking to buy a house with their INFONAVIT have mostly been restricted to these newly built subdivisions (OECD, 2015). In the early 1990s, after INFONAVIT’s major reforms, developers could even obtain a share of future buyers’ mortgages as construction financing (Puebla, 2002). Buyers’ options were limited to a handful of new developments in a city, guaranteeing clients for developers.

Absentee owners and real estate investment are also causes of vacant housing in Latin America. Holding costs are low. Property tax rates in Mexico are low by international standards and frequently not collected (Unda Gutiérrez and Moreno Jaimes, 2015). On the other hand, the formal rental market is small and many people let property sit vacant rather than rent to strangers (Blanco et al., 2014). Because of this relatively limited rental market, housing belonging to families working outside the country might sit vacant, and, in rural or other low-demand areas, owners use many units as storage or simply withdraw them from the housing market because of limited demand and insecure property rights (Struyk, 1988).

In the most recent National Housing Program, 2014–2018, 2 the federal government advanced several strategies to diversify the housing options available, with housing finance, loans, for example for housing improvement, and self-built housing. One of the Program’s specific areas (Strategy 3.4) is to advance the development of a market for used housing. The Program cites statistics from the National Housing Commission (CONAVI) that roughly 80 per cent of loans were to be for the purchase of newly built housing between 2008 and 2012. The Program was somewhat vague as to how it would achieve this goal. More recent statistics show that two-thirds of loans still go to buyers of newly built houses, mostly located in suburban housing developments (OECD, 2015).

Early case studies of this new suburban vacancy phenomenon in the periphery of Mexico City pointed to the pace and scale of new housing development as a chief cause of the local government’s inability to meet the service needs of new houses (Maya and Cervantes, 1999). Scholars point out that the lack of basic infrastructure, security and schooling services in the city generates an urban environment with a low quality of life. Other studies also emphasise the sheer size of the new developments, and their peripheral location distant from shopping and social activities, as key elements that harm residents’ lives (González Hernández, 2013; Paquette, 2015). Other scholars have recognised this as over-production of housing and a system that decides loans for housing in a non-market manner (Maycotte Pansza and Sánchez Flores, 2010).

Sánchez and Salazar (2011) propose four explanations for high vacancy rates specific to the Mexican context: the economic recession that began in 2008, migration to the United States, violence associated with the ‘war on drugs’, and the housing finance policy of INFONAVIT. The present study examines these hypotheses empirically.

Identifying where housing vacancy is concentrated is an essential component of understanding the roots of the problem in Mexico. An assumption that seems to underlie much of the popular coverage of housing policy in Mexico, and the policy proposals by the Secretariat of Agricultural, Territorial, and Urban Development (SEDATU), is that Mexican cities are sprawling. While cities are expanding rapidly, new peri-urban housing developments in Mexico have a much higher density than the average urban neighbourhood in Mexico (Monkkonen, 2011b). This is especially important as it affects commutes. Formal jobs are concentrated in city centres, leading to larger travel distances and informal work by residents of the periphery (Suárez et al., 2016).

Additionally, housing vacancy is not only a problem in the urban periphery. A report on the territorial development of Puebla-Tlaxcala, for example, found vacancy rates in the city centre of over 40 per cent (OECD, 2013: 134). The growing challenge of central city housing vacancy, which has been studied previously by Ward (1993, 2001), signals a lack of attention to the problems generated by both the irregular urbanisation of previous decades and the redevelopment and upgrading of these neighbourhoods, which are now relatively centrally located. The deteriorated urban environment contributes to the vacancy problem as it lowers the demand for real estate in neighbourhoods in relatively central parts of the city (Monkkonen, 2008).

Data and methods

Mexico’s housing vacancy problem is an urban problem; therefore this analysis focuses on the 100 largest cities in the country. Roughly 21 million of the 35 million housing units in Mexico in 2010 were located in these 100 cities, and they have an average vacancy rate of 14 per cent, the same as the country as a whole. I use data from the 2010 Census of Population and Housing, which is noteworthy as it is the first census to report on vacancy. Great care went into the verification of completed housing units that are vacant in this census, as detailed in the census’ methodology. 3

The overall approach is to first assess and evaluate spatial patterns of high vacancy within cities. Data are not available at the level of the house, thus I cannot distinguish recently built vacant housing from older vacant housing. I assume, however, that peri-urban housing is much more likely to be new than housing in the city centre. Second, after locating vacancy within cities, I examine various arguments about what kinds of cities have higher vacancy rates in general, across urban peripheries and across city centres.

Locating vacancy within cities

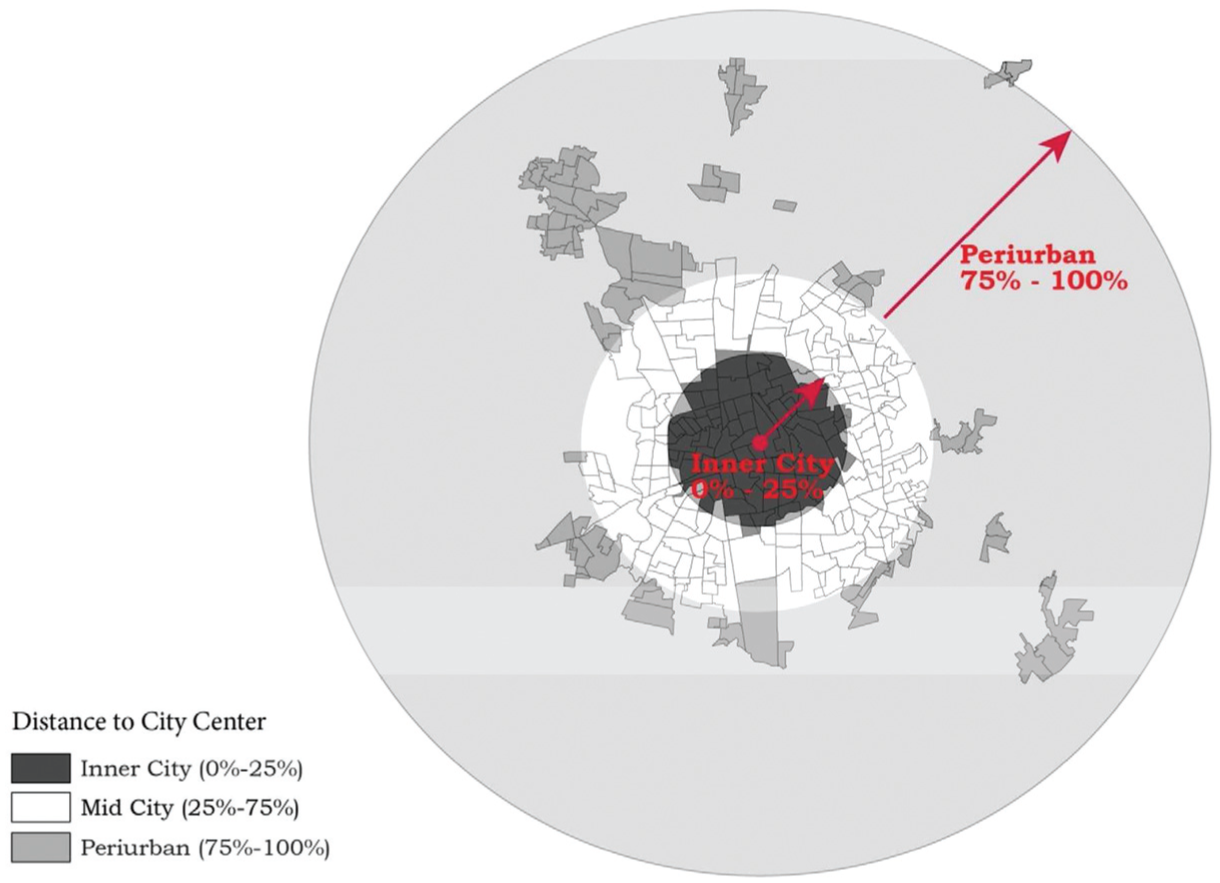

I calculate vacancy rates for the central area of the city and the urban periphery. I define these two areas based on the distance of census tracts 4 from the city centre. 5 I classify the 25 per cent of census tracts closest to the centre of the city as central city, and the 25 per cent furthest from the centre as peri-urban. Centrally located tracts are higher density. They have more housing units but cover less surface area. Figure 1 shows an example of this classification for the city of Aguascalientes, with census tracts categorised into central city and peri-urban.

Census tracts classified by distance to city centre, Aguascalientes.

Figures 2–4 show samples of three cities’ internal patterns of housing vacancy to illustrate the three broad trends across the 100 largest cities. Ciudad Juárez, pictured in Figure 2, is illustrative of a majority of cities, which have two clear clusters of high vacancy rates – one near the city centre and one in the urban periphery.

Share of vacant housing by census tract, Ciudad Juárez, Chihuahua.

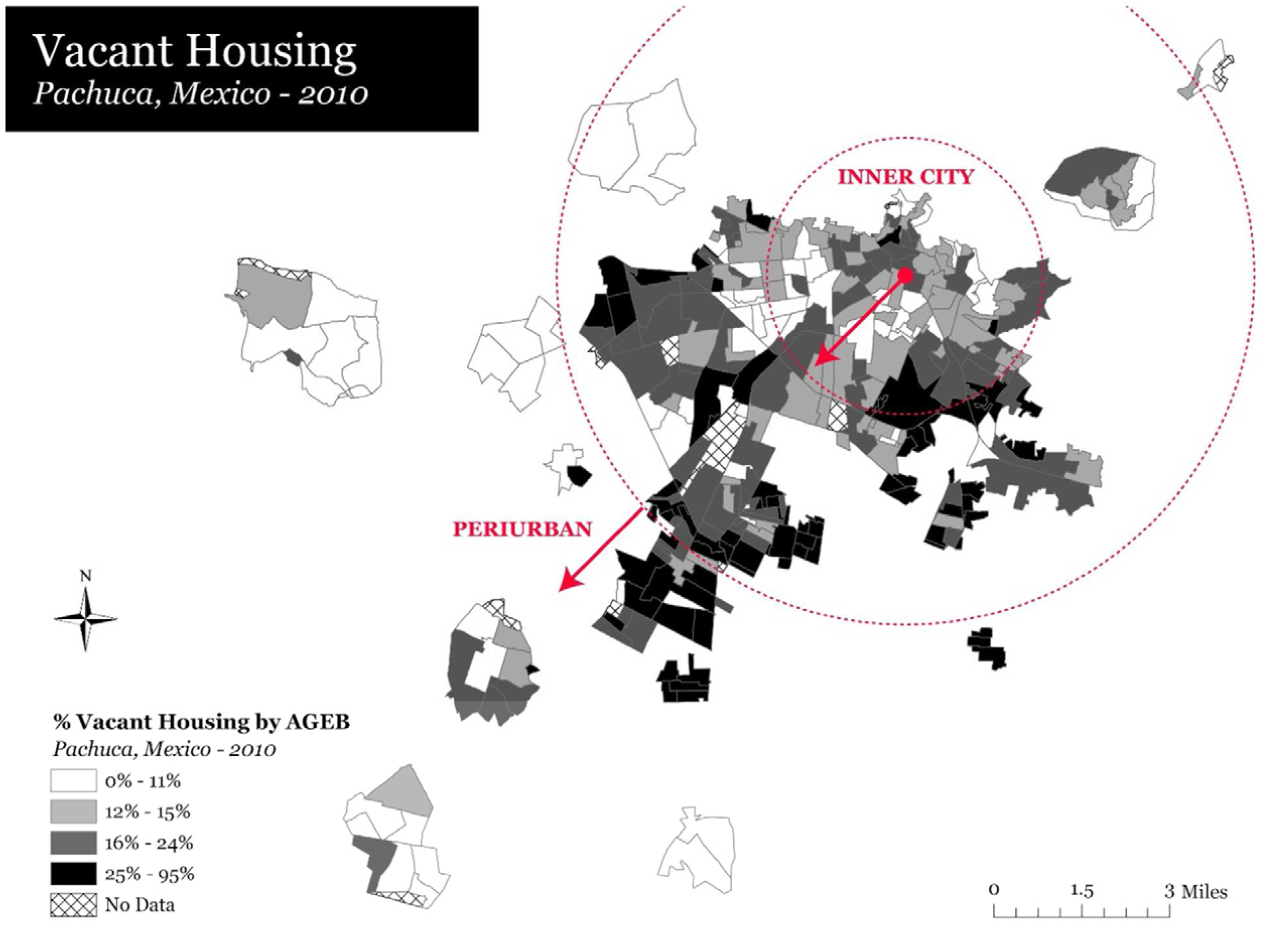

Share of vacant housing by census tract, Pachuca, Hidalgo.

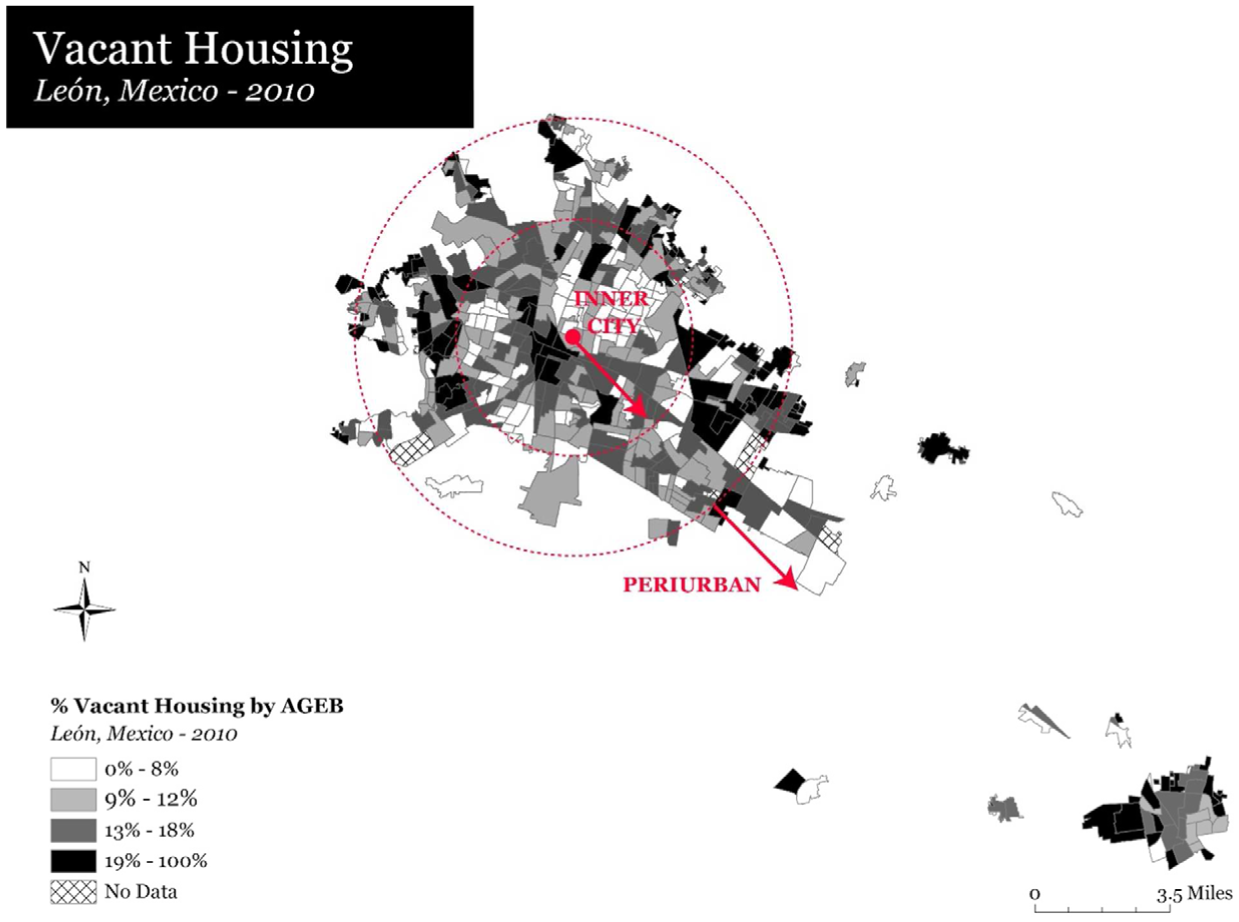

Share of vacant housing by census tract, León, Guanajuato.

The city of Pachuca in Figure 3 has less vacancy in the central city. Most of the high-vacancy tracts are located in the periphery. Finally, Figure 4 is the city of León, which has the least common spatial distribution of vacancy: an even spread of high-vacancy tracts across the city.

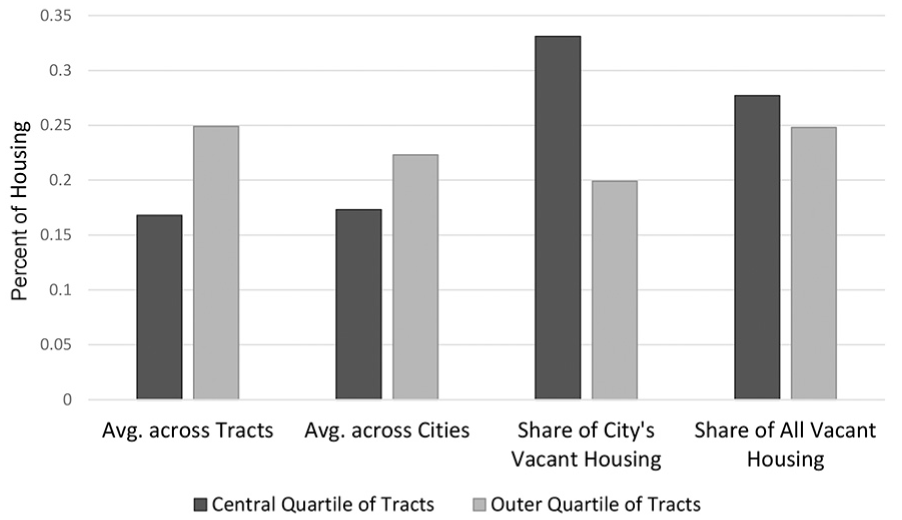

Figure 5 summarises these trends. It shows the average share of vacant housing in the central city and peri-urban parts of cities in two different ways. The first two columns are averages across cities of the vacancy rate for census tracts in the central city and urban periphery. The second two columns are averages across cities of the proportion of that city’s vacant housing that is located in the central city and urban periphery. This distinction is important because although on average the vacancy rate is higher in the peri-urban parts of the city, central city areas have on average a much larger share of these cities’ vacant housing. The caveat here, of course, is that there are more housing units in the central city than in the urban periphery by this definition and these numbers are sensitive to where central city and peri-urban boundaries are drawn. 6 Central city tracts are higher density, so comparing the inner quartile of tracts to the outer quartile of tracts will compare an area with more housing with an area with less housing overall.

Vacancy rates and share of vacant housing, central and outer areas in the 100 largest Mexican cities.

Nonetheless, the data reported in Figure 5 reframe the idea that the housing vacancy phenomenon is exclusively a problem in the urban periphery. In a majority of large cities in Mexico, vacancy rates are higher in the peri-urban parts of the city than they are in the city overall. Yet there are more vacant houses in the central quartile of tracts than in the peri-urban quartile of tracts. About one third of vacant housing in the 100 largest cities is located in the centre of cities, whereas only one fifth is in the urban periphery. Again, this is due to the fact that more housing units are located in city centres, but is important given the greater importance of centrally located land for cities.

Another aspect of vacancy within cities is its relative spatial distribution or spread across neighbourhoods. I examine this with a measure of clustering. Scholars have shown that many kinds of neighbourhood effects are non-linear (Galster, 2012). The negative social impacts of deficient physical infrastructure or public services, or of high poverty rates, often do not have linear impacts on quality of life and social outcomes. Rather, they increase rapidly only after there is more than some threshold amount. Figure 6 shows the distribution of vacancy rates for tracts divided by quartiles of distance to the city centre to illustrate the prevalence of high-vacancy tracts.

Distribution of tract vacancy rates, quartiles of tracts by distance to city centre.

In this sense, the media and scholarly focus on peri-urban vacancy may be warranted, given the large numbers of high vacancy rates in particular neighbourhoods. For example, roughly 30 per cent of vacant units are located in tracts with vacancy rates above 25 per cent, and many more of these high-vacancy tracts are located in the peri-urban areas of cities (40 per cent) than in the inner city (17 per cent). Further, nearly 10 per cent of peri-urban tracts have more than half their housing vacant compared with only 2 per cent of centrally located tracts.

What kinds of cities have more housing vacancy?

In order to test hypotheses about what kinds of cities have higher vacancy rates, I first run Ordinary Least Squares regressions of overall vacancy rates on a set of independent variables, and then use inner city and peri-urban vacancy rates as dependent variables in separate models.

Data limitations prevent me from establishing anything more than descriptive relationships, especially the fact that only one year of vacancy data is available. The one advantage of the centrally controlled structure of INFONAVIT lending is that the prevalence of loans available and exercised in a particular city is plausibly exogenous to demand for housing. Within the INFONAVIT system, state offices receive credits according to a formula based on the number of members in that state, and their accrued points based on years worked, income and family size. This does not necessarily correlate with their demand for housing. Moreover, INFONAVIT applies loan criteria equally across the country, without regard for local market conditions.

I choose control variables based on international literature, which suggests several possibilities such as overbuilding, a drop in demand, a greater level of demand for real estate as an asset than as a physical commodity, or high transactions costs in property sales. I control for the size of the city (number of housing units), its population growth rate, population density and housing market characteristics such as the share of houses that are self-built and the average household size. 7 I also considered an index of marginality and an index measuring urban sprawl, but ultimately rejected them because they are composite measures.

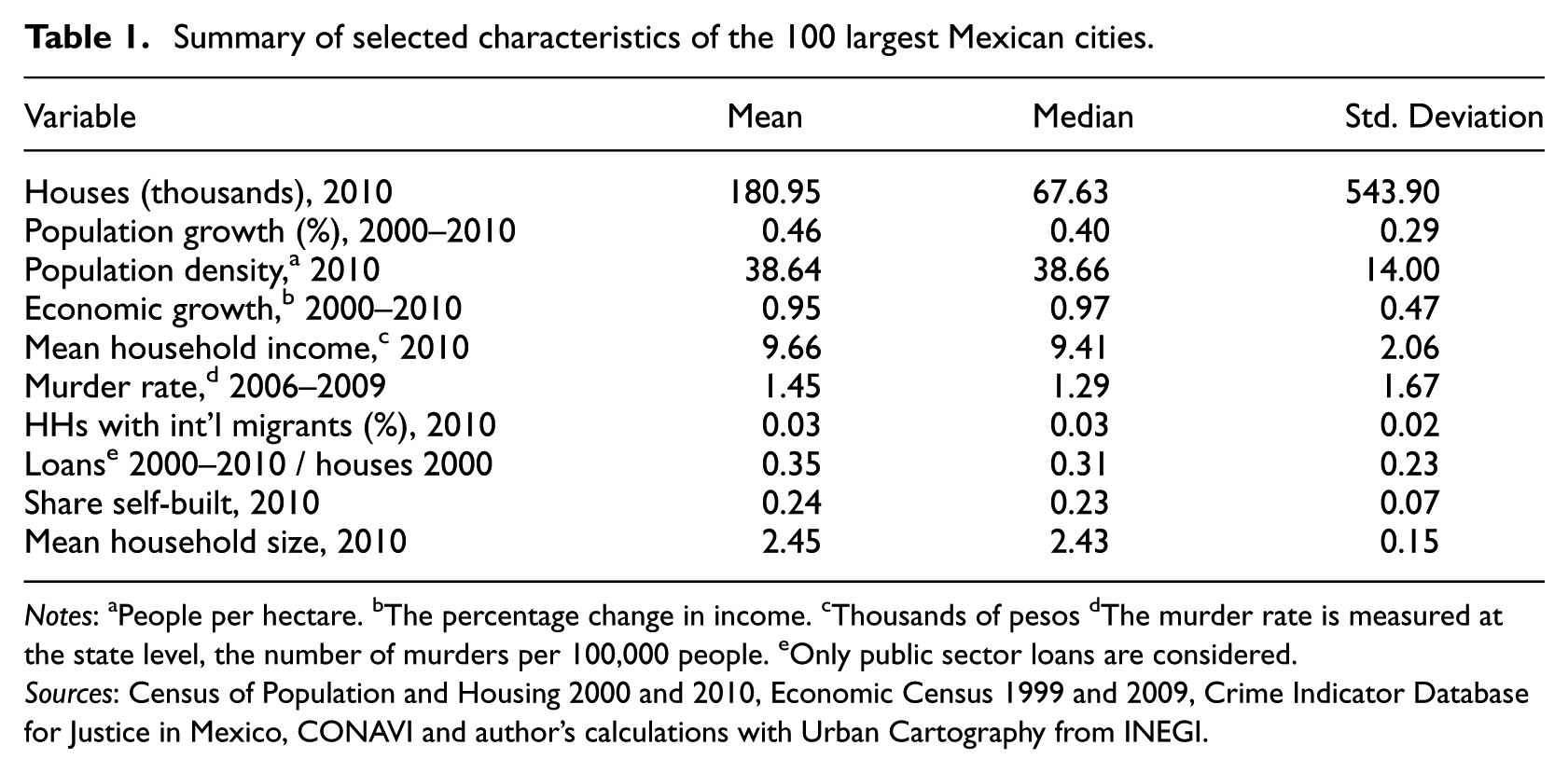

Sánchez and Salazar (2011) propose four factors specific to Mexico: economic recession, migration to the United States, violence and housing finance. I measure the first three using data on the changes in the local economy (value added at the city level) from the Economic Census of Mexico (1999 and 2009), data on international migration 8 from the 2010 Census of Population and Housing and data on drug-related homicides from the Crime Indicator Database for the Justice in Mexico Project at the Trans-Border Institute, University of San Diego (Molzahn et al., 2012). The measure of the prevalence of housing finance in a city relies on data from CONAVI 9 on the housing loans issued in a city between 2000 and 2010. For this last variable, I normalise the number of loans issued by the number of houses in the city in the year 2000 to measure the prevalence of housing finance in a given place. Table 1 reports summary characteristics of all variables.

Summary of selected characteristics of the 100 largest Mexican cities.

Notes: aPeople per hectare. bThe percentage change in income. cThousands of pesos dThe murder rate is measured at the state level, the number of murders per 100,000 people. eOnly public sector loans are considered.

Sources: Census of Population and Housing 2000 and 2010, Economic Census 1999 and 2009, Crime Indicator Database for Justice in Mexico, CONAVI and author’s calculations with Urban Cartography from INEGI.

Analysis

I base my analysis on three OLS regression models: one for the measure of vacancy overall, one for vacancy in the peri-urban part of the city and one for vacancy in the central city. As discussed previously, these are descriptive models that test whether even with controls, the strong bivariate correlations between the prevalence of housing finance and high vacancy rates persist.

Table 2 reports the results of these regressions. I present coefficients and standardised coefficients. The latter uses the same model but standardises variables to have a variance of one, in order to compare the importance of variables measured in different units.

Regression results: City level vacancy rates on city characteristics.

Notes: White robust standard errors reported in brackets. *, ** and *** indicate statistical significance at the 0.01, 0.05 and 0.01 levels respectively. aThe percentage change in value added. bMurder rate is measured at the state level, the number of murders per 100,000 people. cThe percentage of households where a member is living abroad. dThe number of loans issued by public sector agencies from 2000 to 2010 is divided by the number of housing units in the year 2000.

The regression models fail to reject three of the four factors that Sánchez and Salazar (2011) propose as reasons for high levels of housing vacancy. The rate of international migration out of a city, measured by a proxy variable from the population census, is consistently significant across the three regressions, and has the strongest relationship with high vacancy rates in the urban periphery. There is more migration from poorer, smaller cities. Once we control for these factors, however, migration levels stand out as more closely associated with vacancy. This is likely to be due to families’ abandoning houses when they leave, as well as houses built or kept empty for the eventual return of those working abroad.

The prevalence of murders associated with the drug war in Mexico – a measure of narco-violence – is also positively associated with overall vacancy rates. Cartels use vacant houses in peripheral neighbourhoods, for example, as kidnapping houses or safe houses. Fuentes and Hernández (2014) found a strong correlation between housing overproduction, vacancy rates and crime incidence across Juárez’s neighbourhoods. Although vacancy would likely attract crime within a city’s neighbourhoods, it is unlikely that organised crime would move to a new city because of high vacancy rates.

High vacancy rates are most strongly correlated with the prevalence of housing finance from public agencies, 10 especially overall and in central cities as indicated by the standardised coefficients of 0.49 and 0.47. Although this is an expected relationship, it is stronger than anticipated. Although the housing finance variable is not statistically significantly associated with high peri-urban vacancy rates, it is nearly so, and the coefficient is not statistically different from the central city models according to a standard test. Nonetheless, the strong association with central city vacancy is not the typical media presentation of Mexico’s housing vacancy crisis as one of empty new houses. Moreover, along with recent research showing a strong association between lending and population loss in central cities (Monkkonen and Comandon, 2016), the results are reminiscent of the suburbanisation process in the United States in the second half of the 20th century, which also stemmed in part from government mortgage lending policies such as redlining (Jackson, 1985).

The fourth hypothesis proposed by Sánchez and Salazar (2011) – the economic recession – is not significantly associated with variation in vacancy rates at the city level. However, this does not mean that it rejects this hypothesis at a larger scale. The models presented here test the relationship between various factors and the variation in vacancy rates across cities. Since the recession hit the entire country, it might not explain any variation in vacancy across cities but could still be a contributing factor to vacancy nationally. Additionally, several correlates such as migration and violence closely correlate with economic conditions.

Conclusions

This article analyses vacancy rates across large urban areas in Mexico, and reveals that housing vacancy in Mexico is a multifaceted phenomenon. A large number of houses sit vacant in central parts of cities, though the media and scholars have focused on empty and abandoned new houses in peri-urban areas. In analysing the correlates to high vacancy rates across cities, I find that violence and international migration are statistically significant, but that investment in new housing has a stronger relationship. Cities with higher levels of mortgage lending have higher levels of vacancy. This is true for overall levels of vacancy, and the relationship is strong for vacancy rates in city centres as well as urban peripheries. This corroborates other studies that show how a strong bias in lending for new housing in the urban periphery has contributed to population loss in city centres (Monkkonen and Comandon, 2016).

The fact that the United States and Mexico had similar rates of housing vacancy in 2010 (Cresce, 2012) is somewhat surprising considering the very different economic and policy contexts and the relative importance of government in the mortgage industry of each country. In the United States, regulatory agencies allowed private companies to provide housing loans in unsustainable ways to individuals who were not able to afford them in the long-run (Immergluck, 2009). Foreclosures and the bursting of the housing bubble led to high rates of housing vacancy. In contrast, high rates of vacancy in Mexico connect to the government’s strong presence in the housing finance system, not its absence.

The juxtaposition of the housing vacancy crisis in Mexico with that in the United States suggests policymakers reconsider two aspects of the standard frame for debating the role of government in housing policy and housing finance. First, beyond the traditional demand- vs supply-side housing subsidies debate, we must focus on the structure of the housing finance system as housing policy. Housing finance is the most consequential housing and urban policy in many countries. In the case of Mexico, a federal agency runs the majority of the financing system but does not reflect the housing policy goals of the federal government as a whole, which focus on compact cities according to the National Housing Program 2014–2018. As part of this effort, the National Housing Commission created an urban containment perimeter policy in 2013 to direct its housing subsidies specifically to central parts of urban areas. However, as Monkkonen and Giottonini Badilla (2017) demonstrate, INFONAVIT has continued to issue a majority of its loans to the peripheries of cities, outside of the urban containment perimeters.

Additionally, the debate over ‘how large’ a presence the federal government should have or ‘how much’ regulation there should be (Chiquier and Lea, 2009) can be misleading. A more important set of indicators is the set of incentives for different actors in the system. In Mexico, salaried workers must contribute to the INFONAVIT housing fund, and thus have a very strong incentive to use their access to credit. Developers building housing for purchase with INFONAVIT were responding to cost incentives rather than consumer demand (Monkkonen, 2011a). In the United States, mortgage originators had strong incentives to provide loans that were unaffordable to borrowers. In both cases, it was not that more or less regulation was needed; rather, regulations needed to orient incentives in a different direction.

Housing finance is an important tool for smoothing household consumption patterns over time; however, rapidly expanding access to finance is difficult to do in a sustainable manner. Countries with a supply of credit for housing that matches the effective demand and capacity of the lending institutions do not appear to benefit from even more liquidity. In fact, in both the United States and Mexico, the abundance of capital for housing loans was a core driver of the housing crises. The former was highly leveraged and the latter was not, yet the supply of funds led to similar outcomes in both places.

The results of this study suggest that INFONAVIT would benefit from reform in two ways. First, INFONAVIT should separate its lending activities from its investing activities as with Singapore’s CPF. Rather than subsidising members’ housing loans with lower returns on all members’ pensions, INFONAVIT would better serve its members by earning market returns on individuals’ pensions and leaving housing subsidies to CONAVI, a federal agency with the specific mandate of subsidising housing for lower-income households. The internal cross subsidy is also likely to be regressive, as higher-income members of INFONAVIT take out larger loans.

Second, INFONAVIT should give its members a greater degree of control over their contributions into the fund. One way to do this is to reduce the strong incentives to use contributions for a mortgage, by improving returns on pensions. Additionally, INFONAVIT should continue to expand flexibility in what members can purchase with their loan, including loans for plots of land and home improvement. The federal government already heavily emphasises this latter point in policy documents, but the numbers on usage of loans show that the emphasis has not led to major changes. The 2016 Social Security Law sought to give more flexibility to INFONAVIT members, to allow them to designate some of their mandatory 5 per cent to a pension account specifically, but the fund has still not fully implemented this modality. Finally, INFONAVIT should give its members the option to contribute less of their salary to the fund. The combination of high vacancy rates in newly built housing and the continued high volume of housing production indicates that the fund does not lack capital.

Footnotes

Acknowledgements

Thank you first and foremost to Nicole Walters for excellent research assistance. Marissa Ellis Plouin and the OECD Mexico urban and housing team provided valuable guidance and feedback in an early version of the analysis. Also thank you to Eve Bachrach for astute editing and comments, and to anonymous reviewers and editors at Urban Studies for further suggestions.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was partially supported by a grant from the Academic Senate of the University of California, Los Angeles.