Abstract

This study analyses the changes in intra-city housing values in response to improved inter-city connection brought by high-speed rail (HSR), using the opening of the Hangzhou–Fuzhou–Shenzhen Passenger Dedicated Line (HFSL) in Shenzhen, China, as an example. The opening of the HFSL and its integration into the local metro network at Shenzhen North Station provide exogenous intra-city variations in access to the surrounding economic mass. With a difference-in-differences approach, we find that the HFSL showed a negative local effect as housing values declined by 11.5%–13.3% in the proximity of Shenzhen North Station relative to areas further from the station after the opening, possibly due to the negative externalities of the HFSL. The HFSL effect can spread along the metro network and lead to, on average, a 7% appreciation of housing values around metro stations (network effect). The direction and strength of the network effect vary by metro travel time between Shenzhen North Station and metro stations. Housing values decreased by 7.7% around metro stations within 5–15 minutes of metro travel time but increased by 63.6%, 16.6% and 29.2% around metro stations within 15–25, 25–35 and 35–45 minutes of metro travel time to Shenzhen North Station, respectively. The HFSL effect on housing values diminishes when the rail travel time is above 45 minutes. We interpret these findings as evidence of the redistribution effect in the city related to HSR connection.

Introduction

In economic geography and urban economics, households and firms benefit from good access to markets due to the economies of agglomeration (Marshall, 1920), which has motivated massive investment into transport infrastructures in cities and regions worldwide to improve accessibility and facilitate development. One emerging example of such investment is the high-speed rail (HSR). With an operating speed of 250 km per hour (km/h) or above and a large capacity for passenger travel, HSR can produce a progressive contraction of space and greatly improve inter-city connectivity. However, high construction costs remain a major barrier for HSR. It costs, on average, US$17–21 million per km to build the HSR network in China, which is about two-thirds of the cost in other countries (Lawrence et al., 2019). The total investment in the HSR network is estimated to be over 1.8 trillion RMB Yuan (approximately US$300 billion) during the 12th five-year plan (2011–2015) of China (Diao, 2018). Understanding the economic impacts of HSR is crucial for the cost–benefit analysis of HSR projects before considerable amounts of public money are committed to its development.

Literature that investigates the relationship between HSR investment and economic development is increasing. At the inter-city scale, researchers examine the impact of HSR on GDP growth (Ahlfeldt and Feddersen, 2018; Qin, 2017), economic activities (Zheng et al., 2019), fixed asset investment (Diao, 2018), regional disparity (Sasaki et al., 1997), employment and specialisation patterns (Lin, 2017) and city-level real estate prices (Zheng and Kahn, 2013). At the intra-city level, a few researchers have investigated the impact of HSR on the spatial distribution of housing prices within a city (e.g. Andersson et al., 2010; Chen and Haynes, 2015; Diao, Zhu and Zhu, 2017; Gen et al., 2015), which is the interest of this study. One common feature of existing studies on this topic is the primary focus on the local effect of HSR on the housing market, that is, the price dynamics in areas proximate to HSR stations. For example, Andersson et al. (2010) documented a minor effect of HSR on residential property values in southern Taiwan. Chen and Haynes (2015) found that the Beijing–Shanghai HSR line in China has a positive impact on nearby housing values in medium and small cities, while its impact in large cities is minimal. Gen et al. (2015) found that proximity to HSR stations leads to a price premium only when the distance from stations is beyond a certain threshold value. Diao, Zhu and Zhu (2017) showed that inner-city HSR stations tend to increase property values in the surrounding areas, while suburban HSR stations with poor connections to existing urban centres show an insignificant property value effect.

Accessibility benefits of transport infrastructure, including HSR, are local by nature. Commuters living closer to HSR stations enjoy greater gains from regional integration than those living farther away from stations due to better access to economic mass connected by HSR. The inter-city accessibility benefits brought by HSR can be further translated into a price premium for properties near HSR stations relative to distant properties (Chen and Haynes, 2015; Diao, Zhu and Zhu, 2017). In the meantime, accessibility benefits of HSR could have spillover effects for other locations. In particular, the inter-city HSR network is often connected with the intra-city rail transit network at certain transport hubs, forming a larger rail network. Therefore, conceptually accessibility benefits of a new HSR line could spread along the connected intra-city rail transit network, creating broader impacts on the spatial distribution of housing values within a city than previous studies have explored. Determining the distributional consequences of HSR in urban housing markets is fundamental to validate the merits of public investment in HSR. Neglecting potential gains in housing values along intra-city rail transit lines could bring a downward bias to the estimation of the value added by new HSR lines and misguide decision making in transport planning and urban planning. To our knowledge, no existing empirical studies have investigated the network effect of HSR within a city.

This study aims to contribute to the literature by providing evidence of the impact of HSR, which is an increasingly important but empirically understudied inter-city transport mode, on the intra-city distribution of housing values, using the opening of the Hangzhou–Fuzhou–Shenzhen Passenger Dedicated Line (HFSL) in Shenzhen, China, as a quasi-experiment. The 1495-km-long HFSL links several key coastal cities in South-east China, including Hangzhou, Fuzhou and Shenzhen. It has two stations located in Shenzhen (Shenzhen North Station and Pingshan Station) and is connected to the local metro network at Shenzhen North Station. Our analysis consists of two parts. Part 1 assesses the local effect of HSR, that is, the impact of the HFSL on property values in areas around HSR stations. Part 2 evaluates the network effect of HSR, that is, price appreciation (discount) along the metro network due to the introduction of the new HSR line. The two parts collectively draw a more complete picture of the impact of HSR on the intra-city distribution of housing values. We adopt a difference-in-differences (DID) approach in our analysis and assess the treatment effect of the HFSL by comparing the housing price changes in areas close to HSR (or metro) stations and areas further away from the stations before and after the operation of the HFSL. Our findings provide empirical evidence on the redistribution effect of HSR in the intra-city housing markets.

Our work contributes to the growing literature on transport infrastructure and housing values by examining the different channels through which inter-city transport infrastructure can impact the intra-city housing market. Existing studies on the property value effect of transport infrastructure mainly focused on intra-city rail transit systems that improve accessibility and connectivity within a metropolitan area, such as subways or metros (Diao, Zhu and Zhu, 2017; Diao, Fan and Sing, 2017; McMillen and McDonald, 2004; Murakami and Chang, 2018), light rail (Billings, 2011) and commuter rail (Dube et al., 2013). Most empirical studies documented that proximity to intra-city transit stations has a significant positive effect on property values due to accessibility benefits (Baum-Snow and Kahn, 2000; Diao, Zhu and Zhu, 2017; McMillen and McDonald, 2004), while a few studies found a negative effect (Bowes and Ihlanfeldt, 2001; Diao, Zhu and Zhu, 2016; Pan, 2013), possibly due to negative externalities in the station areas, such as noise (Diao, Zhu and Zhu, 2016) and crime rates (Bowes and Ihlanfeldt, 2001). If accessibility to other cities’ markets contributes to the economic performances of households and firms, then the benefit from regional integration could be capitalised into property values. However, research that examines the property value effect of inter-city transport modes on an intra-city scale is rare. A few existing studies, such as Chen and Haynes (2015) and Diao, Zhu and Zhu (2017), had a narrow spatial scope, mainly focusing on the housing price dynamics close to inter-city transport nodes. Relative to the literature, this study examines the redistribution effect of a novel inter-city transport mode, HSR, on housing prices within a city through the network effect.

Our findings are also relevant to the literature on network effects. The economic theory of network effects originated in the 1970s and was advanced significantly between 1985 and 1995 (Katz and Shapiro, 1985; Liebowitz and Margolis, 1994). In their seminal study, Katz and Shapiro (1985) characterised network products as ‘products for which the utility that a user derives from consumption of the good increases with the number of other agents consuming the good’. Theories on the network effect suggest that the value of a network increases with size (Katz and Shapiro, 1985; Liebowitz and Margolis, 1994). However, empirical studies on the network effect in the transport field are rare. One exception is the work by Fesselmeyer and Liu (2018), which showed that the addition of a new line to the rail transit network in Singapore led to a 1.6% to 2.1% increase in the price of public housing within 0.5 km of existing rail transit stations relative to housing further from the stations. In this study, we provide new empirical evidence of the network effects by showing that the connection of inter-city HSR lines to the intra-city metro network could increase the value of an existing metro network, which can be further translated into housing price appreciation around metro stations.

Finally, this study provides a rigorous evaluation of the economic effect of HSR. Existing studies have assessed the HSR effect from different perspectives and provided mixed evidence (Zhu et al., 2016; Fang et al., 2021). Sasaki et al. (1997) documented that the Shinkansen in Japan promoted local development without widening regional inequality. In France, Banister and Berechman (2000) indicated that the introduction of Train à Grande Vitesse (TGV) services between Paris and Lyon led to significant transport benefits, but its economic impacts vary across cities. Ahlfeldt and Feddersen (2018) presented evidence that the HSR line connecting Cologne and Frankfurt in Germany substantially increased the GDP of the regions due to increased accessibility. At the regional scale, Zheng and Kahn (2013) found that HSR in China is associated with rising real estate prices in secondary cities connected by HSR. This study looks at the economic effect of HSR from a different perspective – the intra-city distribution of housing prices – using detailed housing transaction data and different identification strategies. City-level studies on the development effect of HSR encounter selection bias, because transport authorities may purposely locate HSR stations in cities with certain growth trends to facilitate economic development. Our study, focusing on the intra-city distribution of housing values, could avoid the non-random placement of HSR stations, because the authorities are unlikely to consider price dynamics around the metro stations in determining the location of HSR stations.

The rest of this article proceeds as follows. The second section introduces HSR development in Shenzhen to establish the research background. The third section introduces the empirical strategy and data. The fourth section presents empirical results and discusses research findings. The final section concludes the article.

HSR development in Shenzhen

Shenzhen, located in the Pearl River Delta and bordering Hong Kong, is one of the most dynamic and thriving cities in the world. In the past three decades, Shenzhen has experienced China’s most rapid urbanisation and economic growth. In 2018, the city’s GDP was 2.42 trillion RMB (approximately US$372 billion) and ranked third in China, while its per capita GDP ranked first, at 190,000 RMB (approximately US$29,230). Given the extraordinary economic growth, Shenzhen continuously attracts migrants and investments. The city’s population increased from approximately 300,000 in 1980 to over 13 million in 2018, nearly 40 times growth. 1

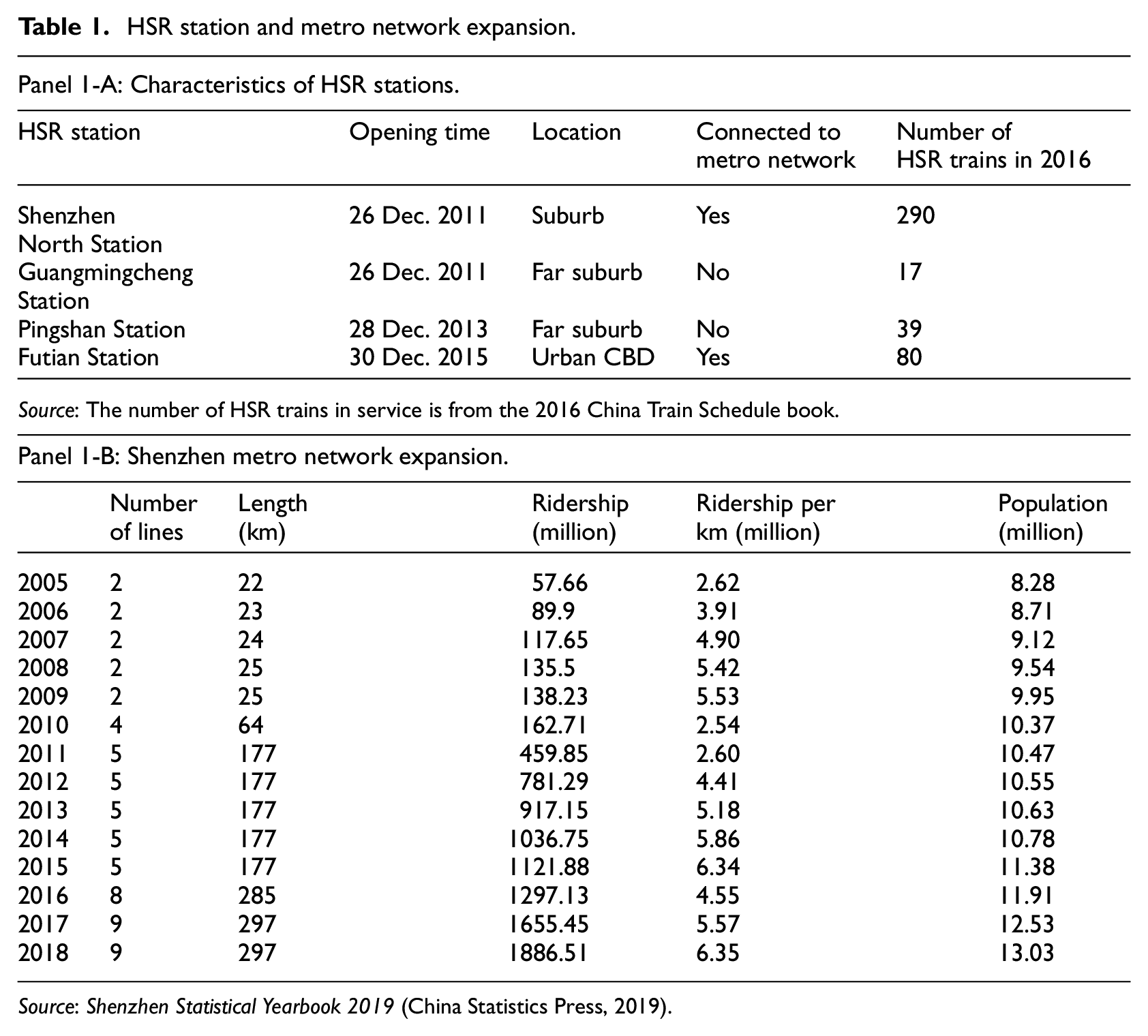

As a regional economic hub, Shenzhen has the second largest inter-city and intra-city railway networks in South China, after the provincial capital of Guangzhou. Currently, two HSR lines and four HSR stations provide inter-city HSR services in Shenzhen. The first is the Guangzhou–Shenzhen–Hong Kong Express Rail Link (XRL). The XRL is 142 km long with seven train stations, among which three are in Shenzhen (Guangmingcheng Station, Shenzhen North Station and Futian Station). The XRL was opened in three phases. The first segment from Guangzhou South Station in Guangzhou to Shenzhen North Station in Shenzhen opened in late December 2011. The service was extended to Futian Station in the CBD of Shenzhen in December 2015. Lastly, Futian Station was connected to West Kowloon Station in Hong Kong in September 2018. The current train speed is about 300 km/h.

The HFSL is the second HSR line in Shenzhen, which connects Shenzhen to Hangzhou, the capital of Zhejiang province. The HFSL operates along the south-east coast of China, with a total length of 1495 km and a train speed of between 250 and 350 km/h, connecting 17 cities with 64 HSR stations. Shenzhen North Station is the terminal station of the HFSL on the Shenzhen end. The next station is Pingshan Station, located in the eastern suburban district of Shenzhen. The HFSL was opened in December 2013. The XRL and HFSL have tremendously enhanced inter-city population mobility. At the intersection of two HSR lines, Shenzhen is attractive to tourists and immigrants, which has beneficial implications for its housing markets.

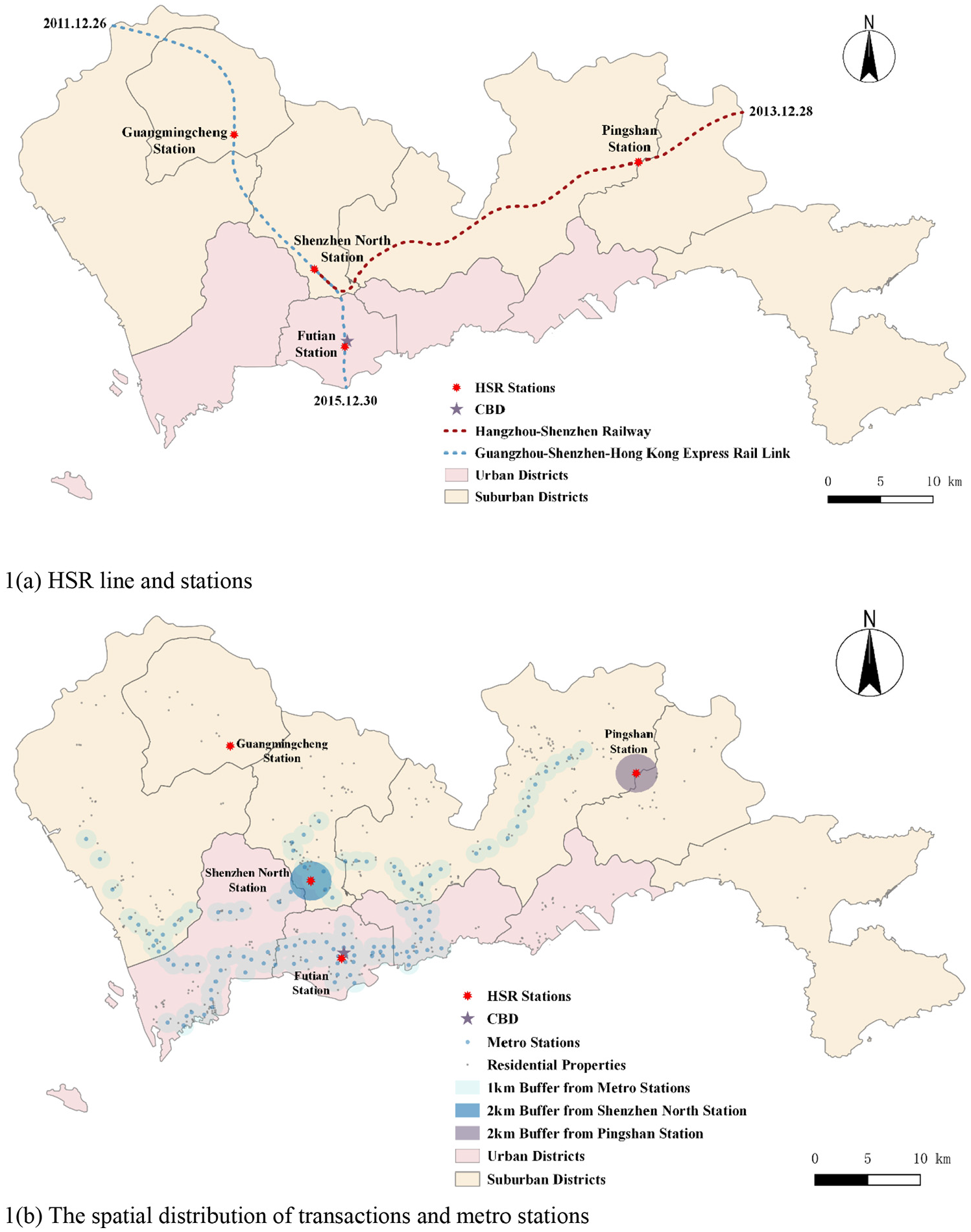

Figure 1 shows the two HSR lines and the location of the four HSR stations in Shenzhen. Panel 1-A in Table 1 summarises the characteristics of individual stations, including opening time, location, connectivity to the metro network and number of HSR train services in 2016. Of the four stations, Shenzhen North Station is in the near suburban area of Shenzhen. As a hub connecting two HSR lines, it has the highest frequency of HSR train services and a superior connectivity to the local metro network. In contrast, Guangmingcheng Station and Pingshan Station are located in the far suburban area without connectivity to the local metro system. The number of HSR train services at these two stations is relatively small. Lastly, Futian Station is in the CBD of Shenzhen with good connectivity to the local metro network. It is a medium-sized station in terms of the number of HSR train services.

HSR station and metro network expansion.

Source: Shenzhen Statistical Yearbook 2019 (China Statistics Press, 2019).

HSR stations, metro stations and housing transactions in Shenzhen: (a) HSR line and stations, and (b) the spatial distribution of transactions and metro stations.

To accommodate increasing demand for intra-city travel, Shenzhen has been actively developing its urban public transportation systems, especially the metro network. The first two metro lines were opened in December 2004 with a total track length of 22 km. In 2018, nine metro lines were in service with a total track length of 297 km. Panel 1-B of Table 1 summarises the city’s metro network expansion from 2005 to 2018. One interesting observation is that the metro network remained unchanged from 2011 to 2015; however, the per km ridership increased substantially from 2.6 million in 2011 to 6.34 million in 2015, a 143.8% increase, though the urban population only experienced an increase of 8.7% and the fares of the Shenzhen metro remained unchanged during the same period. This may suggest that the opening of the two inter-city HSR lines in December 2011 (XRL) and December 2013 (HFSL) contributed to the growth of the intra-city metro ridership. Conceptually, the integration of the inter-city and intra-city rail transit networks could form a larger network for passenger flow and enhance the accessibility around both HSR and metro stations, which can impact price changes in the housing markets. This observation motivates us to study how HSR could affect the housing markets through the intra-city metro network in addition to its local impact on the housing values in areas close to HSR stations.

Conceptually, HSR could affect housing markets through two channels. First, HSR affects housing values in areas close to HSR stations, due to improved inter-city connectivity and/or negative externalities related to inter-city passenger flow such as crowdedness, noise and crime. This is the local effect. Second, HSR indirectly affects property values in other parts of the city through the metro system. This is the network effect. The second channel depends on good integration between HSR and the metro system. One challenge to identify the local and network effects of HSR on the intra-city housing markets is ruling out the impact of metro network expansion on housing values. The metro network in Shenzhen has experienced rapid expansion in the past decades. Existing literature has shown that the improved intra-city accessibility brought by the metro network can be capitalised into property values in Shenzhen, especially for properties within a 1-km catchment area of metro stations (Chang and Murakami, 2019). To separate the HSR effect on housing prices from the metro expansion effect, we need to determine a time period during which the metro network remained stable while the HSR network experienced a big shock.

Panel 1-B in Table 1 shows that the metro network in Shenzhen remained unchanged from 2011 to 2015. During this period, the XRL opened in December 2011, and its extension from Shenzhen North Station to Futian Station opened on 30 December 2015 (Table 1, Panel 1-A). Accordingly, we choose 2012–2015 as the study period, because there is no change in either the metro network or the XRL during this four-year time window. The second HSR line, the HFSL, opened on 28 December 2013, which is approximately the middle point of the study period. The HFSL provides an ideal setting to examine how a new HSR line affects urban housing markets through both the local effect in the proximity of HSR stations and the network effect along the metro corridor.

Our research largely consists of two components. First, we assess the local effect of the HFSL by separately examining the price changes around two HSR stations: Pingshan Station and Shenzhen North Station. Both stations are located along the HFSL, while their effects on local housing markets could be different given individual characteristics. Pingshan Station is a small station located in the far suburban district of Shenzhen without connections to the local metro network. Therefore, we expect the impact on local housing values near Pingshan Station to be relatively small. In contrast, Shenzhen North Station serves as an inter-city transportation hub given its large number of high-speed train services. Although it was opened in late 2011 with the XRL, the introduction of the new HFSL to the station could enhance passenger flow substantially. We expect that the opening of the HFSL will have a significant effect on properties close to Shenzhen North Station. Second, we investigate the network effect of the HFSL by examining the price dynamics around metro stations. The HSR network is connected to the metro network at Shenzhen North Station. The new HFSL is likely to enhance the metro ridership and improve the inter-city accessibility of households along the metro corridor, which could be capitalised into housing values. The detailed empirical strategy and major data sources are introduced in the next section.

Empirical strategy and data sources

Empirical strategies

This study uses the opening of the HFSL in Shenzhen as a pseudo experiment and adopts a DID approach to assess the local and network effects of the HFSL shock on housing values. The DID method has been widely used to interpret the causal impact of various shocks on Chinese housing markets (Chang and Li, 2018, 2020; Chang et al., 2020). To estimate the local effect of HSR on housing values in the proximity of HSR stations, we assign properties within 2 km of an HSR station (Pingshan Station or Shenzhen North Station) into a treatment group, and properties 2–4 km from the HSR stations into a control group. Given the spatial proximity of the treatment and control groups, most confounding factors and omitted variables can be cancelled out, and the result can be interpreted in a causal manner. The model specification is shown in equation (1):

where

Next, we estimate the network effect of the new HSR line on housing values around metro stations. Due to the integration of the HSR and metro networks at Shenzhen North Station, both the accessibility gain and the environmental externalities (noise, crowdedness and crime rate) induced by the HFSL could spread along the metro network, leading to price changes in the housing markets. We employ a DID strategy as shown in equation (2):

where

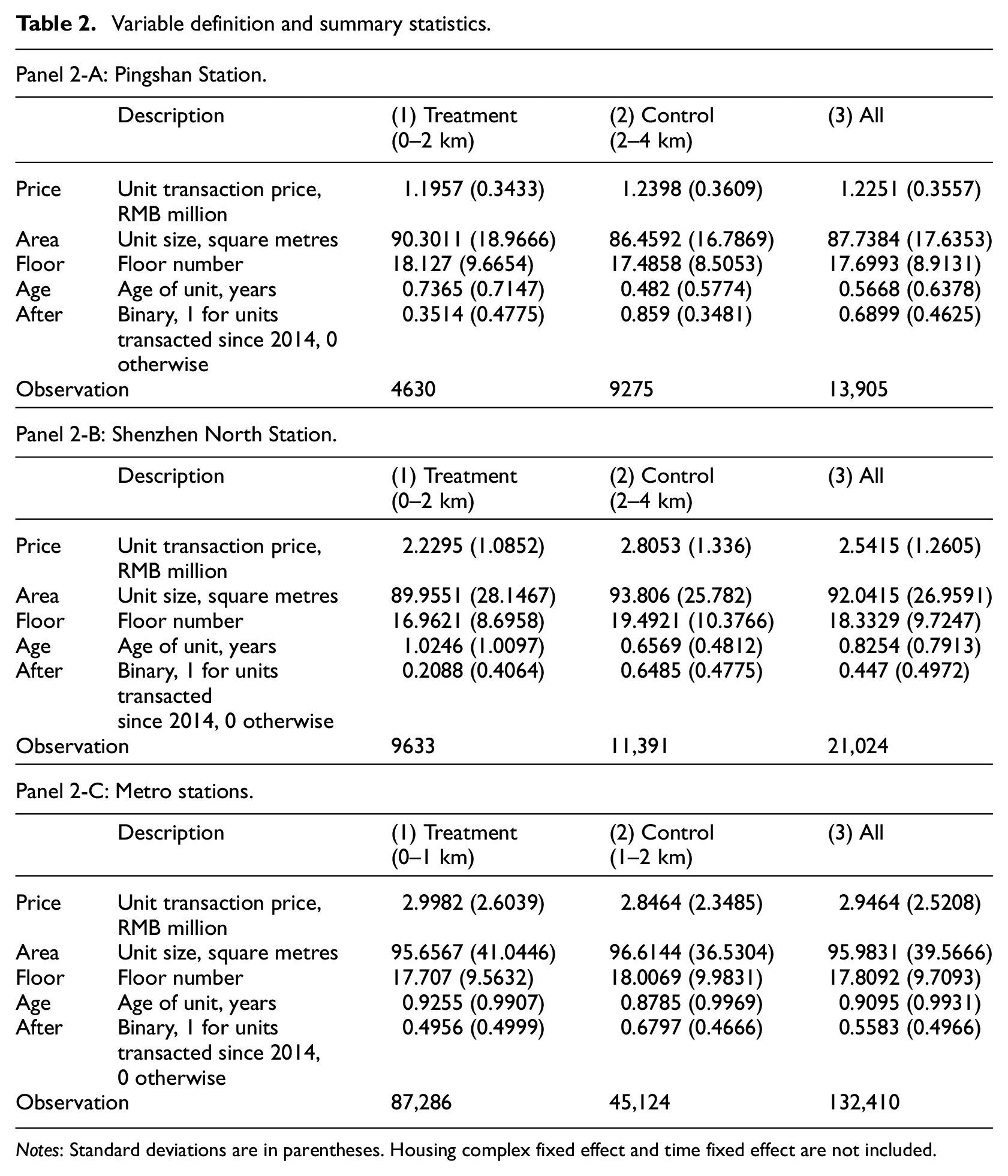

Data source and summary statistics

Housing transaction data in Shenzhen are obtained from www.soufun.com, the largest housing data vendor in China. The dataset includes approximately 224,000 unit transactions in 375 housing complexes from 2012 to 2015. 2 Each transaction record has detailed information on the street address, the name of the housing complex, the transaction price, the date of transaction, the size and age of the unit and the floor number. To control for inflation, we adjust the nominal housing price using the 2019 Shenzhen consumer price index. 3 We geocode the housing complex, HSR stations and metro stations using Geographic Information Systems tools. The spatial distributions of transactions and stations are shown in Figure 1(b). We find that approximately 40% of housing transactions are within a 1-km catchment area of metro stations.

In cleaning the data, we drop transactions if the unit price is lower than 1% or higher than 99% of transactions in the sample. We also drop observations with missing variables such as unit price, unit size, age of unit and floor number. Table 2 presents summary statistics in three panels of key variables in the analysis. Panel 2-A is for housing units transacted near Pingshan Station. It shows that unit price in the treatment group is similar to that in the control group. Panel 2-B summarises housing characteristics near Shenzhen North Station. We find the unit price in the treatment group is lower than that in the control group. Panel 2-C shows the housing characteristics of units close to metro stations. It shows that the unit price closer to metro stations is slightly higher than those far away from metro stations. Table 2 provides preliminary evidence on how HSR affects housing values through different channels, though robust econometrical examination is required to rule out confounding factors, which is shown in the next section.

Variable definition and summary statistics.

Notes: Standard deviations are in parentheses. Housing complex fixed effect and time fixed effect are not included.

Empirical results

The local effect of the HFSL on housing values

We apply equation (1) to examine the local effect of new HSR stations on housing values. Panel 3-A of Table 3 summarises the results of the baseline models for the two HSR stations. The first four columns present the results for Pingshan Station using transactions within different time windows around the opening of the new HFSL. Among the four models, we retain the same two-year pre-treatment period and increasingly extend the post-treatment period in six-month intervals, from six months to 24 months after the opening of the HFSL. The coefficients of the interaction term HSR × After in all regressions are negative, but none are significant. We further change the treatment and control groups to properties within 0–3 km and 3–5 km of Pingshan Station, respectively. The results remain the same. In sum, the HFSL has no significant effect on housing values near Pingshan Station, which is not surprising for a rural station with few HSR train services.

Regression results for the local effect of the HFSL.Panel 3-A: Binary treatment.

Notes: Standard errors are in parentheses and clustered at the housing complex level. *, ** and *** indicate statistical significance at the 10%, 5% and 1% level, respectively.

Similarly, columns (5)–(8) in Panel 3-A of Table 3 repeat the same analysis for properties close to Shenzhen North Station. We find a significant negative effect on housing values. Within two years of the opening of the HFSL, the housing price in the treatment zone declined by approximately 11.5%–13.3% relative to the control zone. As an inter-city transportation hub, the new HSR line attracts many passengers to Shenzhen North Station. Our results suggest that the HSR-induced negative externalities, such as noise and pollution, could outweigh the accessibility benefit and drive down housing prices in areas near the HSR station. As a robustness check, we change the definitions of the treatment and control groups to 0–3 km versus 3–5 km and 0–4 km versus 4–6 km, respectively, and rerun the models. The results remain negative but are not significant. 4 In sum, the new HSR line decreases property values but only within 2 km of Shenzhen North Station.

Parallel trends test and heterogeneity of the local effect

A valid DID regression requires the parallel trends assumption to hold. We verify this assumption by interacting the treatment group dummy and a set of time dummies, each representing a six-month period, in the pre-treatment period and omitting the six-month period right before the treatment. The results are reported in Panel 3-B of Table 3. All interaction terms have an insignificant coefficient, suggesting that the parallel trend assumption is valid in our regression for the local effect.

The baseline models are based on binary variable After, indicating whether the treatment group receives the treatment. The impact of HSR could vary by the frequency of HSR train services at the station. We conduct a continuous treatment version of the DID regression as a robustness check, using the number of HSR train services at each HSR station as the exogenous treatment. We interact the treatment zone (0–2 km from an HSR station) dummy with the natural logarithm of the number of HSR train services. As Pingshan Station has no HSR train service in the pre-treatment period, we use log (Number of HSR Trains + 1) to preserve observations. The results are reported in Panel 3-C of Table 3. The overall patterns are largely consistent with the baseline models reported in Panel 3-A of Table 3, which further supports the heterogeneous local effect of the HFSL on housing values.

The network effect of the HFSL on housing values

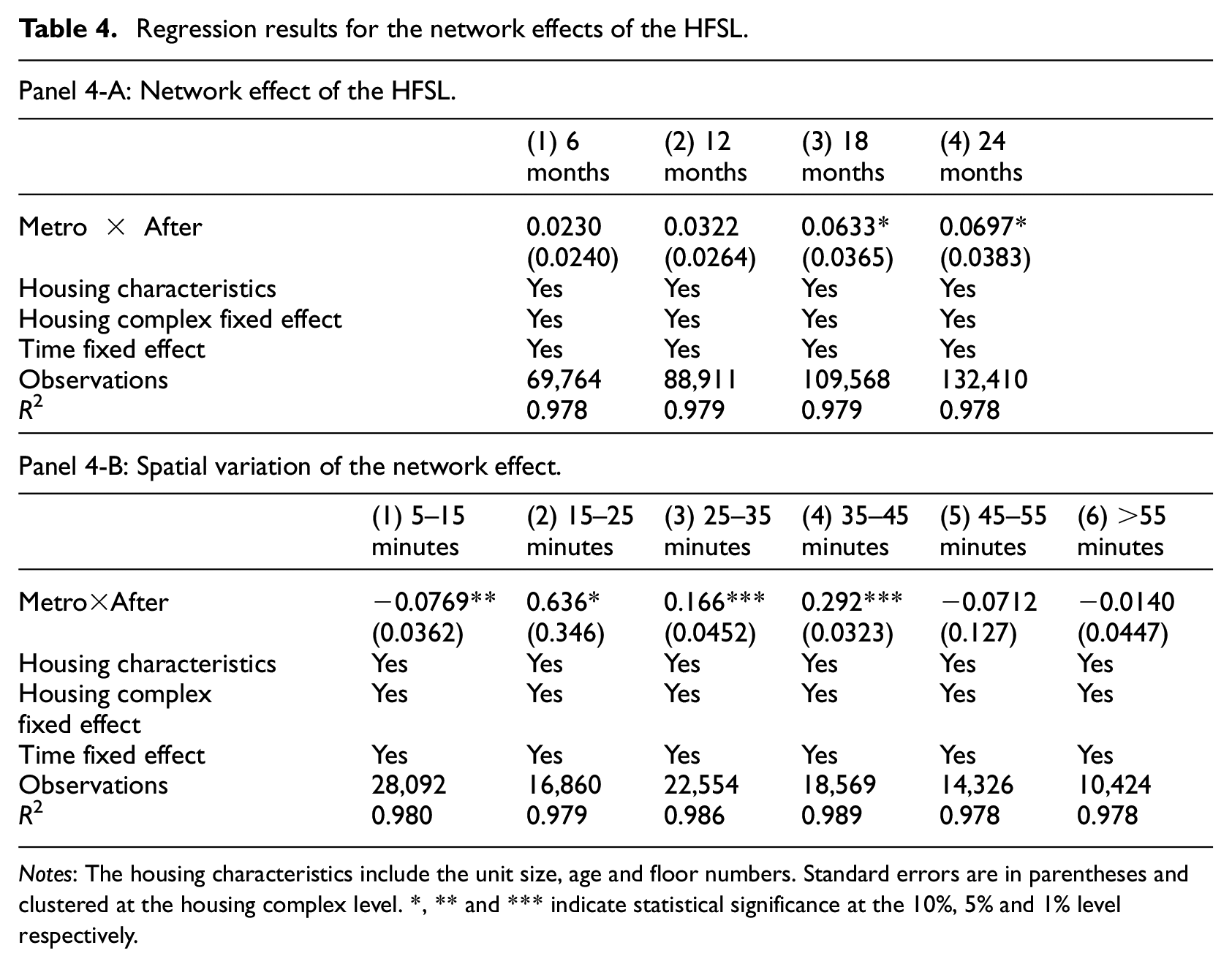

The previous section provides empirical evidence that the new HSR line generates a net negative impact on housing values near Shenzhen North Station. As Shenzhen North Station is an integrated transportation hub that connects the HSR and metro networks, many inter-city passengers from the new HSR line make transfers to the metro system at the station to reach final destinations. Both the inter-city accessibility benefit and the negative environmental externalities created by the new HSR line are likely to spread along the metro network, thus affecting housing values near metro stations. We apply equation (2) to examine the network effect of the HFSL, and report the results in Table 4. The treatment group is defined as housing transactions within the 1-km catchment area of metro stations, and the control group consists of housing transactions within 1–2 km of metro stations. All regressions control for housing attributes, housing complex fixed effects and year and month fixed effects. From column (1) to column (4) in Panel 4-A of Table 4, we incrementally extend the post-treatment time window by six months from six months to 24 months, while retaining the same two-year pre-treatment period. The network effect of the HFSL as captured by the coefficient of Metro × After is relatively small and statistically insignificant in the two models with a six- or 12-month post-opening period. However, if we extend the post-opening period beyond one year, the coefficient of the interaction term indicates an approximately 7% price appreciation, and this effect is marginally significant at the 0.1 level. The finding suggests that, on average, households value the benefits from improved inter-city accessibility. As a robustness check, we change the cut-off for metro stations from 1000 m to 800 m and 1200 m for the treatment zone and rerun the same model. The main findings in the baseline models using the 1000 m cut-off still hold. 5 The network effect of the HFSL with a two-year post-treatment period is approximately 7.0% and 10.0% when the cut-off between the treatment and control zones is 800 m and 1200 m, respectively.

Regression results for the network effects of the HFSL.

Notes: The housing characteristics include the unit size, age and floor numbers. Standard errors are in parentheses and clustered at the housing complex level. *, ** and *** indicate statistical significance at the 10%, 5% and 1% level respectively.

Event study and temporal variation of the network effect

To verify the parallel trends assumption and explore the temporal changes of the network effect, we conduct an event study, and the formula is shown in equation (3). We divide the entire study period into six-month periods, and define the first six-month period after the new HSR line opening as time point T. We interact dummies indicating individual six-month time periods with the treatment dummy (1-km catchment area of metro stations). We use T-1, the six-month period immediately before the opening of the new HSR line, as the reference point. All other variables in equation (3) remain the same as in previous equations.

We plot the coefficients on the interaction terms

Event study for network effect.

Spatial variation of the network effect

In previous sections, we showed that the new HSR line, on average, negatively impacts housing values near Shenzhen North Station (local effect), but it positively affects properties close to metro stations (network effect). How does the positive network effect of HSR distribute along the metro network? We explore the redistribution effect of HSR based on the real metro travel time from Shenzhen North Station to individual metro stations. As Shenzhen North Station generates a negative local impact on nearby housing values, we remove from our sample housing transactions close to metro stations that are within a five-minute metro travel time of Shenzhen North Station. After screening the data, we run the DID regression using a data sample for each 10-minute metro travel time interval from Shenzhen North Station along the metro network. The results are reported in Panel 4-B of Table 4.

Column (1) of Panel 4-B in Table 4 presents the regression results using housing transactions within 5–15-minute travel times of metro stations along the metro network from Shenzhen North Station. It shows that after the opening of the new HSR line, housing prices within the 1-km catchment area of metro stations declined by 7.7% on average, relative to the control group. The result is statistically significant at the 5% level. It indicates that the negative externalities of HSR spread through the metro network and drive down housing values. Column (2) shows the results for the metro stations within a 15–25-minute travel time of Shenzhen North Station. The coefficient of the interaction term is highly positive. Housing values increase by approximately 63.6% for properties close to metro stations relative to those further away from stations, although this effect is marginally significant at the 10% level. We further extend the travel time between metro stations and Shenzhen North Station, and the coefficients of the interaction term are 16.6% and 29.2% in models for metro stations within 25–35 minutes and 35–45 minutes of travel time from Shenzhen North Station, respectively. Both coefficients are highly significant at the 1% level, as shown in columns (3) and (4) of Panel 4-B in Table 4, respectively. Lastly, if the travel time between a metro station and Shenzhen North Station is greater than 45 minutes (columns (5) and (6)), the network effect becomes insignificant.

Panel 4-B in Table 4 indicates a redistribution effect of the new HSR line; positive and negative externalities of HSR can spread along the metro network. The direction and magnitude of the network effect show great variations, depending on the distance from the metro station to Shenzhen North Station. If the metro station is within 15 minutes’ travel time of Shenzhen North Station, the negative externalities of HSR can offset the benefit of improved inter-city accessibility. If the metro station is relatively close to an HSR station, but not too close, the accessibility benefit of HSR outweighs its negative externalities. The benefits from the improved inter-city accessibility can be capitalised into housing values through the network effect. The capitalisation rate decays as travel time between the metro station and the HSR station increases. Lastly, if the metro station is too far away from the HSR station, the benefit from the inter-city accessibility disappears, and the network effect is 0.

Conclusion

To what extent will housing values benefit from the inter-city accessibility benefits brought by HSR, and how are the price changes distributed throughout a city? Answers to these questions have significant implications for understanding the role of HSR in facilitating regional integration and nurturing economic growth. In this study, we use the opening of the HFSL in Shenzhen, China, as a pseudo experiment to estimate the redistribution effect of inter-city transport infrastructure on housing values within a city. The new HFSL links Hangzhou and Shenzhen, which are two important economic and high-tech hubs in China, and is connected to the metro network of Shenzhen at an integrated transport hub, Shenzhen North Station. Our results provide evidence that supports the existence of both the positive accessibility effect and the negative externalities of HSR, which can be capitalised into housing values. We examine two potential channels through which HSR can affect the spatial distribution of housing values in a city: the local effect of HSR on the value of properties in the proximity of HSR stations, and the network effect of HSR on the housing values around metro stations.

We find that, on the one hand, the inter-city commuting flow brought by the HFSL could generate negative externalities for properties located close to HSR stations. The opening of the HFSL can reduce housing values in areas within 2 km of Shenzhen North Station by 11.5%–13.3%, relative to housing values within 2–4 km of the station. On the other hand, the inter-city accessibility benefit of HSR can spread along the intra-city metro network. On average, housing values within 1 km of metro stations experienced a 7% increase after the opening of the HFSL, relative to housing values within 1–2 km of metro stations. We find that the network effect of the HFSL varies by the metro travel time between a metro station and Shenzhen North Station, which is the node that connects the HSR and metro networks. The distribution of the HFSL effect along the metro lines appears to roughly follow a bell curve. More specifically, the opening of the HFSL can reduce housing values by 7.7% around metro stations within 5–15 minutes’ travel time of Shenzhen North Station, and can boost housing values around metro stations further away from Shenzhen North Station. The housing appreciation effect of HSR is estimated to be 63.6%, 16.6% and 29.2% for travel time bands of 15–25, 25–35 and 35–45 minutes to Shenzhen North Station, respectively. The network effect of HSR diminishes when the rail travel time is more than 45 minutes. Our major findings survive a set of robustness checks, including a parallel trends test, a continuous treatment version of DID analysis and alternative delineations of the treatment and control zones.

The research findings have significant policy implications for HSR. Unlike previous studies that mainly focus on the price dynamics around HSR stations, that is, the local effect, we show that HSR could lead to price appreciation among properties around metro stations through the network effect. Omitting the network effect could lead to an underestimation of the economic benefit of HSR, thus bringing bias to the cost–benefit analysis of HSR. Our findings also suggest that a good integration of inter-city and intra-city transport infrastructure could amplify the accessibility benefit of inter-city transport infrastructure investment. This study could potentially contribute to planning for inter-city transport infrastructure and regional integration, as well as for stimulated economic development along intra-city transport corridors.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The work described in this paper was substantially supported by a research grant under the 2020–2021 China Program International Fellowship programme from the Lincoln Institute of Land Policy (C24R003-CZC030520) (Zheng Chang) and the Fundamental Research Funds for the Central Universities, China (Mi Diao).